XLG Company: Assessing Performance Through Variance Analysis Report

VerifiedAdded on 2023/01/09

|15

|3344

|66

Report

AI Summary

This report provides a detailed analysis of variance within XLG, a cleaning product company, focusing on sales price variance, sales volume contribution variance, material price planning variance, and material price operational variance. It examines the merits and demerits of using variance analysis to assess manager performance. The report also explores the competitive advantages offered by FamaQ and addresses the impact of increased demand for chemicals X and Y, along with the associated risks and solutions related to importing FamaQ. The report includes calculations and interpretations of variances, offering insights into XLG's financial performance and operational efficiency. The report concludes by emphasizing the importance of variance analysis in management accounting and its role in strategic decision-making.

Detailed understanding

variance in assessing

performance and

decision making

variance in assessing

performance and

decision making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. Sales price variance and sales volume contribution variance..................................................1

2. The material price planning variance and material price operational variance.......................3

3. Change in operation and critical analysis of merits and demerits of using variance in

assessing the performance of managers.......................................................................................5

PART B...........................................................................................................................................7

1. FamaQ gives XLG competitive advantage..............................................................................7

2. Demand for chemical X and Y has increased by 45% which is likely to continue according

to market research........................................................................................................................8

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15

working days................................................................................................................................9

CONCLUSION................................................................................................................................9

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. Sales price variance and sales volume contribution variance..................................................1

2. The material price planning variance and material price operational variance.......................3

3. Change in operation and critical analysis of merits and demerits of using variance in

assessing the performance of managers.......................................................................................5

PART B...........................................................................................................................................7

1. FamaQ gives XLG competitive advantage..............................................................................7

2. Demand for chemical X and Y has increased by 45% which is likely to continue according

to market research........................................................................................................................8

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15

working days................................................................................................................................9

CONCLUSION................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the process of analysing internal reports and determining actual

position of business so that it could be assessed that all the plans that were formulated previously

are able to result positively or not. It is very important for all the organisations to make sure that

they are using correct approaches for conducting management accounting on yearly basis

(Agrawal and Cooper, 2017). It is very important to make sure that all the predetermined

objectives are achieved. Present report is based upon XLG which is a cleaning product company

located in eastern Britain. It is producing two different types of cleaning agents which are

chemical X and Y. Present assignment covers various topics such as sales price, volume

contribution variance, material price planning and operational variance and merits and demerits

of using all the variances to asses the performance of performance. Apart from this, the risk

which may take place when the chemical famaQ will be imported and the way in which the risk

could be resolved are also covered in this report.

PART A

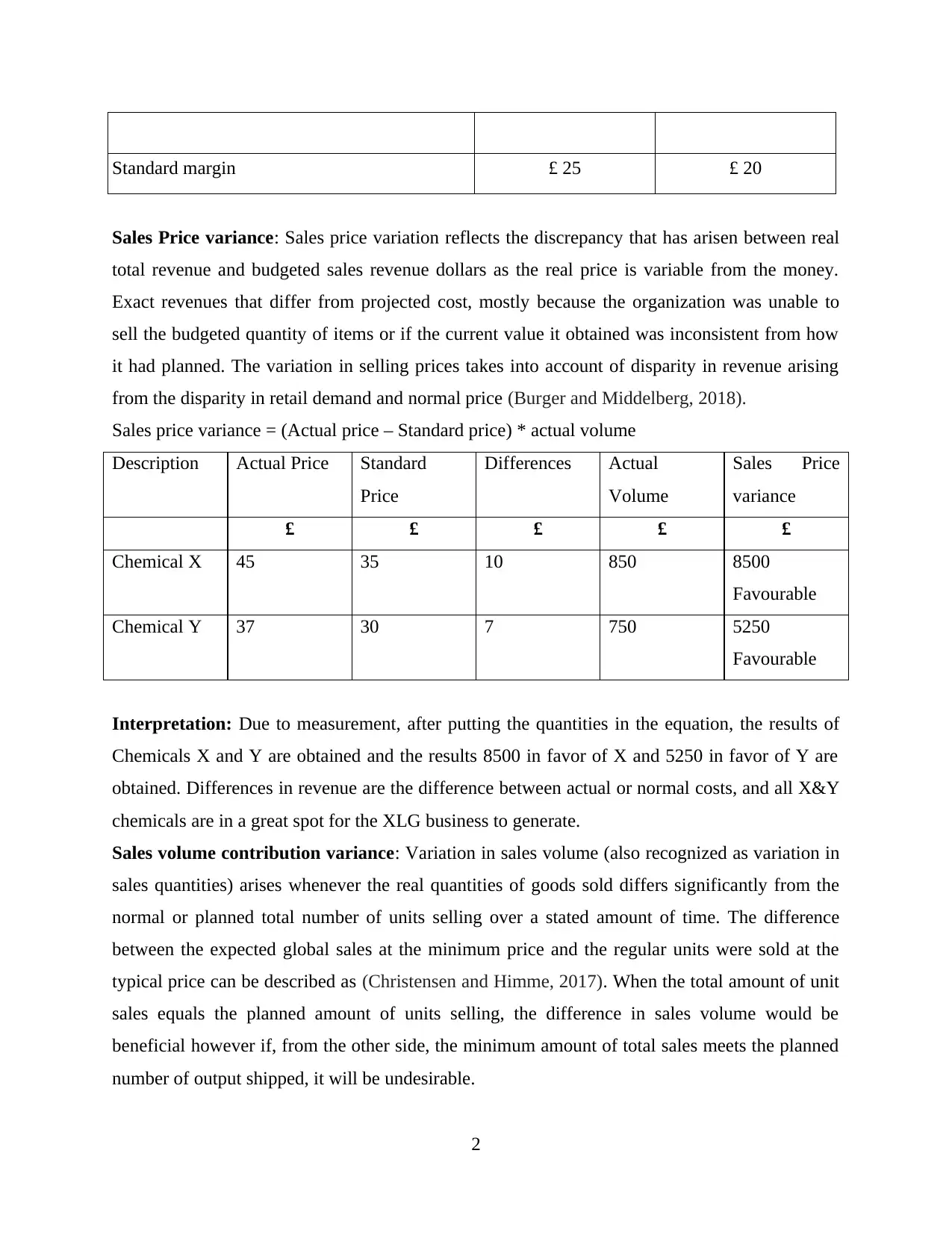

1. Sales price variance and sales volume contribution variance

There are providing information’s in order to calculate sales price variance as well as sales

volume contribution variance. This information is related of chemical X and Chemical Y such

as:

Given Information:

Total units sold: 1600

Material price variance: £ 27000 Favourable

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

Standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

1

Management accounting is the process of analysing internal reports and determining actual

position of business so that it could be assessed that all the plans that were formulated previously

are able to result positively or not. It is very important for all the organisations to make sure that

they are using correct approaches for conducting management accounting on yearly basis

(Agrawal and Cooper, 2017). It is very important to make sure that all the predetermined

objectives are achieved. Present report is based upon XLG which is a cleaning product company

located in eastern Britain. It is producing two different types of cleaning agents which are

chemical X and Y. Present assignment covers various topics such as sales price, volume

contribution variance, material price planning and operational variance and merits and demerits

of using all the variances to asses the performance of performance. Apart from this, the risk

which may take place when the chemical famaQ will be imported and the way in which the risk

could be resolved are also covered in this report.

PART A

1. Sales price variance and sales volume contribution variance

There are providing information’s in order to calculate sales price variance as well as sales

volume contribution variance. This information is related of chemical X and Chemical Y such

as:

Given Information:

Total units sold: 1600

Material price variance: £ 27000 Favourable

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

Standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Standard margin £ 25 £ 20

Sales Price variance: Sales price variation reflects the discrepancy that has arisen between real

total revenue and budgeted sales revenue dollars as the real price is variable from the money.

Exact revenues that differ from projected cost, mostly because the organization was unable to

sell the budgeted quantity of items or if the current value it obtained was inconsistent from how

it had planned. The variation in selling prices takes into account of disparity in revenue arising

from the disparity in retail demand and normal price (Burger and Middelberg, 2018).

Sales price variance = (Actual price – Standard price) * actual volume

Description Actual Price Standard

Price

Differences Actual

Volume

Sales Price

variance

£ £ £ £ £

Chemical X 45 35 10 850 8500

Favourable

Chemical Y 37 30 7 750 5250

Favourable

Interpretation: Due to measurement, after putting the quantities in the equation, the results of

Chemicals X and Y are obtained and the results 8500 in favor of X and 5250 in favor of Y are

obtained. Differences in revenue are the difference between actual or normal costs, and all X&Y

chemicals are in a great spot for the XLG business to generate.

Sales volume contribution variance: Variation in sales volume (also recognized as variation in

sales quantities) arises whenever the real quantities of goods sold differs significantly from the

normal or planned total number of units selling over a stated amount of time. The difference

between the expected global sales at the minimum price and the regular units were sold at the

typical price can be described as (Christensen and Himme, 2017). When the total amount of unit

sales equals the planned amount of units selling, the difference in sales volume would be

beneficial however if, from the other side, the minimum amount of total sales meets the planned

number of output shipped, it will be undesirable.

2

Sales Price variance: Sales price variation reflects the discrepancy that has arisen between real

total revenue and budgeted sales revenue dollars as the real price is variable from the money.

Exact revenues that differ from projected cost, mostly because the organization was unable to

sell the budgeted quantity of items or if the current value it obtained was inconsistent from how

it had planned. The variation in selling prices takes into account of disparity in revenue arising

from the disparity in retail demand and normal price (Burger and Middelberg, 2018).

Sales price variance = (Actual price – Standard price) * actual volume

Description Actual Price Standard

Price

Differences Actual

Volume

Sales Price

variance

£ £ £ £ £

Chemical X 45 35 10 850 8500

Favourable

Chemical Y 37 30 7 750 5250

Favourable

Interpretation: Due to measurement, after putting the quantities in the equation, the results of

Chemicals X and Y are obtained and the results 8500 in favor of X and 5250 in favor of Y are

obtained. Differences in revenue are the difference between actual or normal costs, and all X&Y

chemicals are in a great spot for the XLG business to generate.

Sales volume contribution variance: Variation in sales volume (also recognized as variation in

sales quantities) arises whenever the real quantities of goods sold differs significantly from the

normal or planned total number of units selling over a stated amount of time. The difference

between the expected global sales at the minimum price and the regular units were sold at the

typical price can be described as (Christensen and Himme, 2017). When the total amount of unit

sales equals the planned amount of units selling, the difference in sales volume would be

beneficial however if, from the other side, the minimum amount of total sales meets the planned

number of output shipped, it will be undesirable.

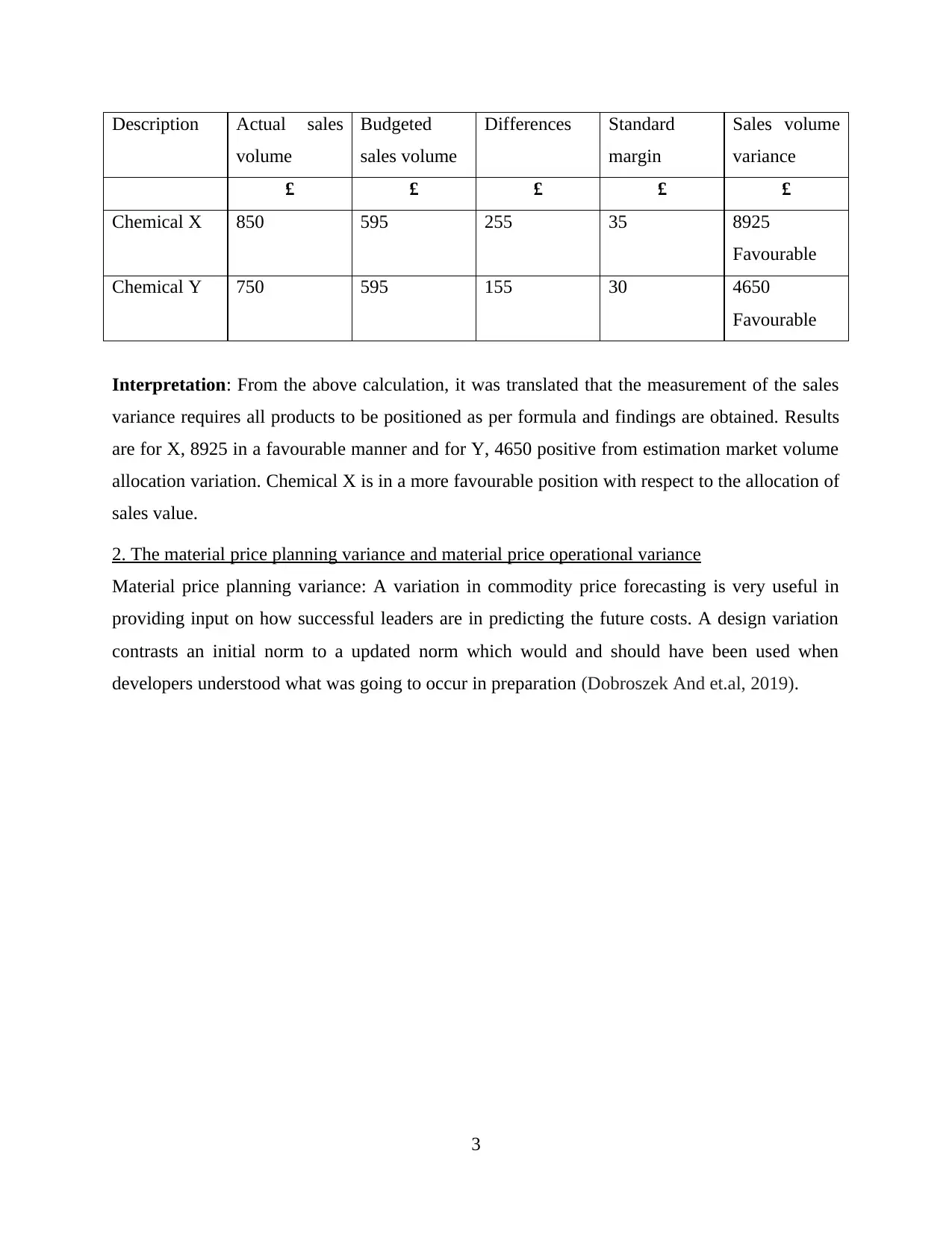

2

Description Actual sales

volume

Budgeted

sales volume

Differences Standard

margin

Sales volume

variance

£ £ £ £ £

Chemical X 850 595 255 35 8925

Favourable

Chemical Y 750 595 155 30 4650

Favourable

Interpretation: From the above calculation, it was translated that the measurement of the sales

variance requires all products to be positioned as per formula and findings are obtained. Results

are for X, 8925 in a favourable manner and for Y, 4650 positive from estimation market volume

allocation variation. Chemical X is in a more favourable position with respect to the allocation of

sales value.

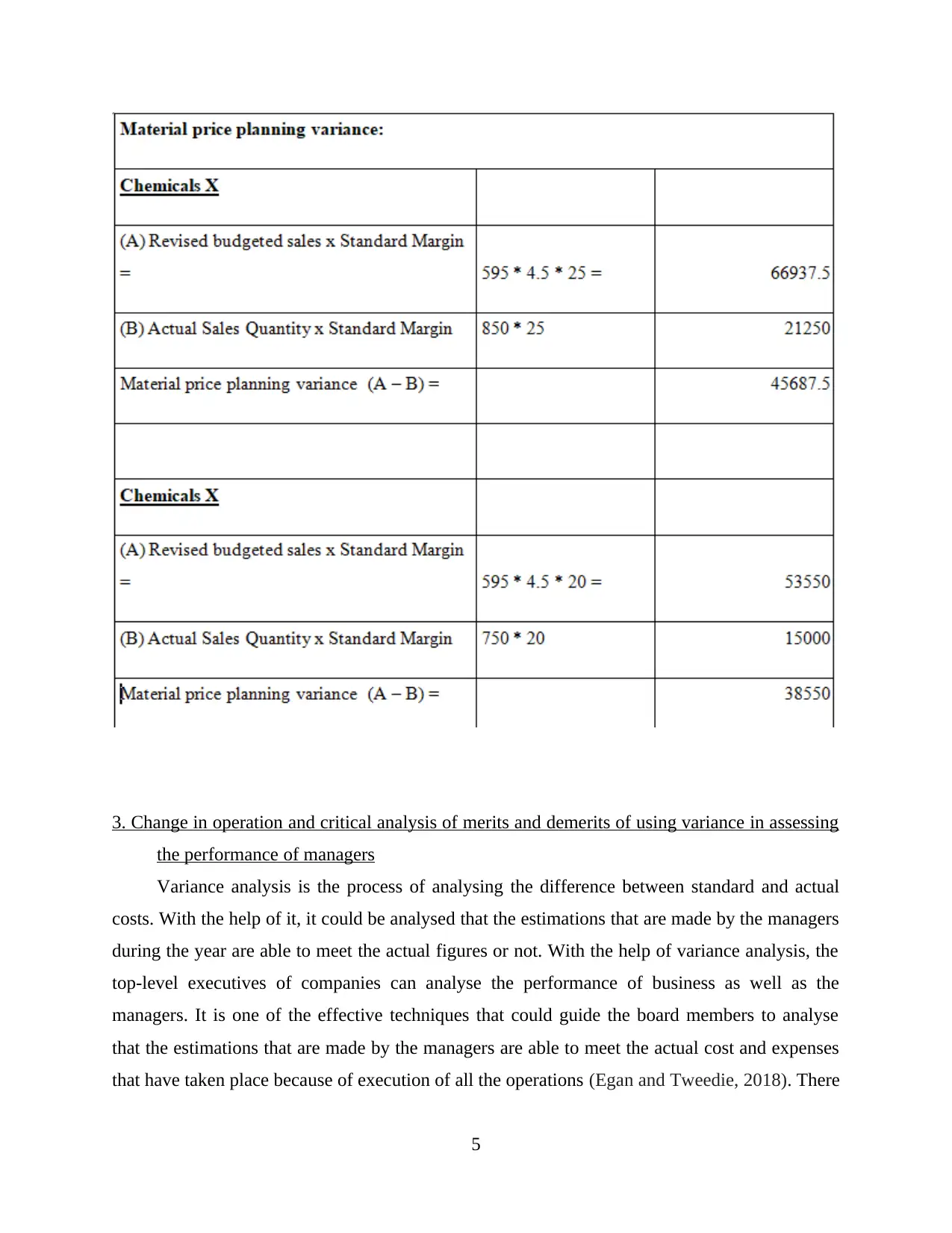

2. The material price planning variance and material price operational variance

Material price planning variance: A variation in commodity price forecasting is very useful in

providing input on how successful leaders are in predicting the future costs. A design variation

contrasts an initial norm to a updated norm which would and should have been used when

developers understood what was going to occur in preparation (Dobroszek And et.al, 2019).

3

volume

Budgeted

sales volume

Differences Standard

margin

Sales volume

variance

£ £ £ £ £

Chemical X 850 595 255 35 8925

Favourable

Chemical Y 750 595 155 30 4650

Favourable

Interpretation: From the above calculation, it was translated that the measurement of the sales

variance requires all products to be positioned as per formula and findings are obtained. Results

are for X, 8925 in a favourable manner and for Y, 4650 positive from estimation market volume

allocation variation. Chemical X is in a more favourable position with respect to the allocation of

sales value.

2. The material price planning variance and material price operational variance

Material price planning variance: A variation in commodity price forecasting is very useful in

providing input on how successful leaders are in predicting the future costs. A design variation

contrasts an initial norm to a updated norm which would and should have been used when

developers understood what was going to occur in preparation (Dobroszek And et.al, 2019).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

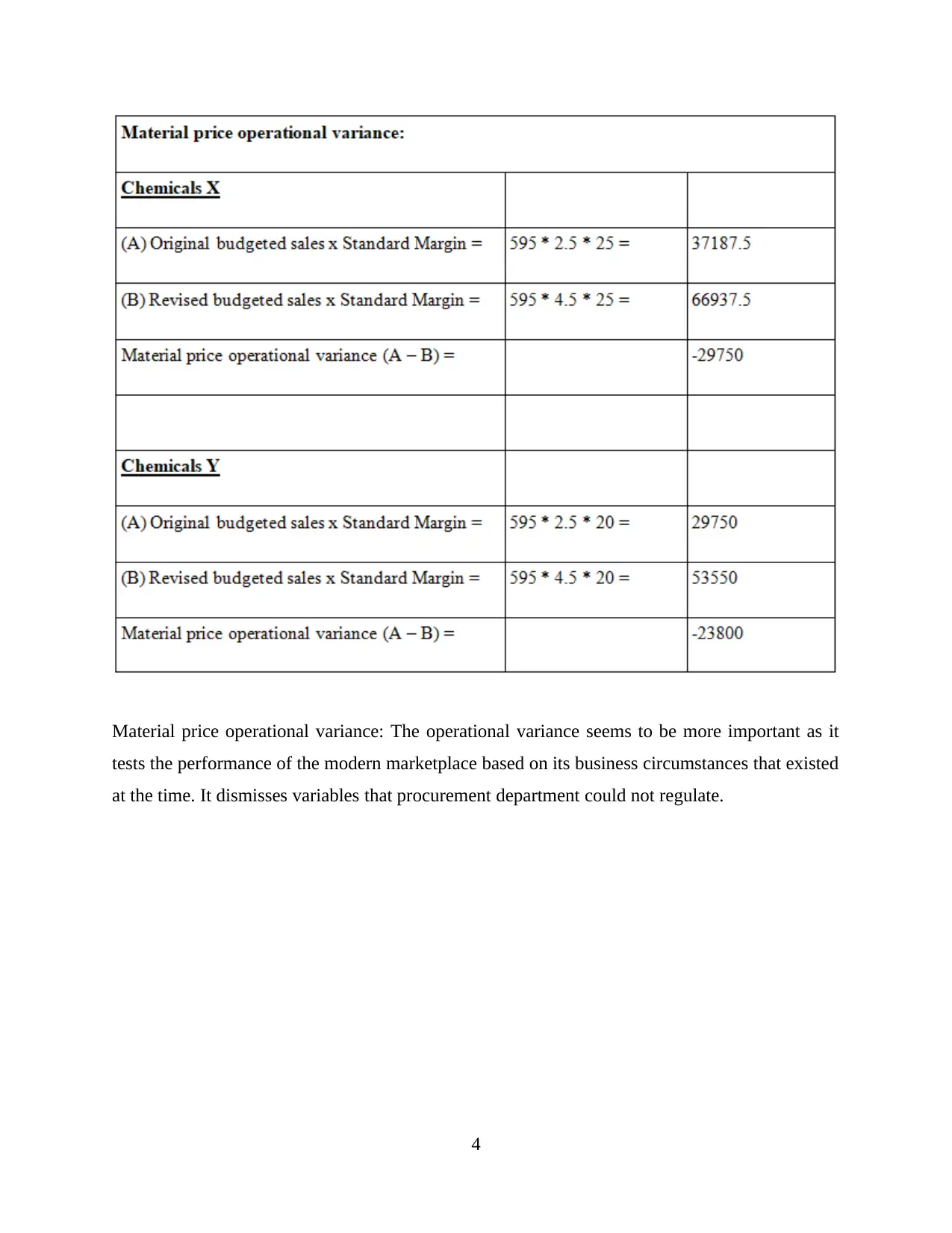

Material price operational variance: The operational variance seems to be more important as it

tests the performance of the modern marketplace based on its business circumstances that existed

at the time. It dismisses variables that procurement department could not regulate.

4

tests the performance of the modern marketplace based on its business circumstances that existed

at the time. It dismisses variables that procurement department could not regulate.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Change in operation and critical analysis of merits and demerits of using variance in assessing

the performance of managers

Variance analysis is the process of analysing the difference between standard and actual

costs. With the help of it, it could be analysed that the estimations that are made by the managers

during the year are able to meet the actual figures or not. With the help of variance analysis, the

top-level executives of companies can analyse the performance of business as well as the

managers. It is one of the effective techniques that could guide the board members to analyse

that the estimations that are made by the managers are able to meet the actual cost and expenses

that have taken place because of execution of all the operations (Egan and Tweedie, 2018). There

5

the performance of managers

Variance analysis is the process of analysing the difference between standard and actual

costs. With the help of it, it could be analysed that the estimations that are made by the managers

during the year are able to meet the actual figures or not. With the help of variance analysis, the

top-level executives of companies can analyse the performance of business as well as the

managers. It is one of the effective techniques that could guide the board members to analyse

that the estimations that are made by the managers are able to meet the actual cost and expenses

that have taken place because of execution of all the operations (Egan and Tweedie, 2018). There

5

are various types of advantages and disadvantages of using variance analysis for the purpose of

determining the performance of managers. It is very important for the senior authorities of all the

companies to make sure that they are aware of all of them as it may leave impact upon the

organisational strategies that will be formulated for effective execution of future activities. One

of the main benefits of variance analysis for business is that it can facilitate the analysis of actual

position of business. Apart from this it can also help the top management to analyse the

performance of all the managers working within the organisation as higher difference between

actual and standard cost will provide the information of weak estimation skills. It will

demonstrate ineffective performance of the managers. Additionally, when the different will be

low between budgeted and actual expenses will state the managers are performing all their duties

properly.

Advantage

• Another advantage of the variance will be its expenditure-limit value. In the presence of

unfavourable variation managers take action to track equally. Where there are insufficient

explanations for doing so and appropriate precautionary actions are implemented, proof of an

unfavourable variance is evaluated first (Grossi and et.al, 2019).

• The potential adjustment of the sums money earmarked is ambiguity or variability. Even if

there's no reasonable reason for ambiguity in response to an inaccurate budget calculation, the

viewpoints for potential should be revised or revamped.

• Analysis of variance is a useful necessity of surveillance since it emphasizes elements in which

actual interaction fluctuates from predicted operational processes. A further advantage is that

trying to find key elements for which facilities are not used efficiently and factors in which

improvements are needed can be valuable. The analysis of variation therefore promotes

organizational versatility. Examination of variances can also be used to areas increase that costs

exceeded and to determine if the specified structured costs are acceptable (Velte, 2019).

• This strategy has the crucial advantage everything that serves as a control tool. It will become

achievable since this management of the company could become interested to understand what

practices are not going to perform well by wanting to find a difference between real and

generally assumed financial documents. For example, if forecasted revenues of a specific good

are 500 devices even when actual sales are 250 units, then fluctuation will be 250 units (500

6

determining the performance of managers. It is very important for the senior authorities of all the

companies to make sure that they are aware of all of them as it may leave impact upon the

organisational strategies that will be formulated for effective execution of future activities. One

of the main benefits of variance analysis for business is that it can facilitate the analysis of actual

position of business. Apart from this it can also help the top management to analyse the

performance of all the managers working within the organisation as higher difference between

actual and standard cost will provide the information of weak estimation skills. It will

demonstrate ineffective performance of the managers. Additionally, when the different will be

low between budgeted and actual expenses will state the managers are performing all their duties

properly.

Advantage

• Another advantage of the variance will be its expenditure-limit value. In the presence of

unfavourable variation managers take action to track equally. Where there are insufficient

explanations for doing so and appropriate precautionary actions are implemented, proof of an

unfavourable variance is evaluated first (Grossi and et.al, 2019).

• The potential adjustment of the sums money earmarked is ambiguity or variability. Even if

there's no reasonable reason for ambiguity in response to an inaccurate budget calculation, the

viewpoints for potential should be revised or revamped.

• Analysis of variance is a useful necessity of surveillance since it emphasizes elements in which

actual interaction fluctuates from predicted operational processes. A further advantage is that

trying to find key elements for which facilities are not used efficiently and factors in which

improvements are needed can be valuable. The analysis of variation therefore promotes

organizational versatility. Examination of variances can also be used to areas increase that costs

exceeded and to determine if the specified structured costs are acceptable (Velte, 2019).

• This strategy has the crucial advantage everything that serves as a control tool. It will become

achievable since this management of the company could become interested to understand what

practices are not going to perform well by wanting to find a difference between real and

generally assumed financial documents. For example, if forecasted revenues of a specific good

are 500 devices even when actual sales are 250 units, then fluctuation will be 250 units (500

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

units-250 units). Using this variation, enterprise managers should make successful policies and

ideas to improve sales (Iredele, Ogunleye and Okpala, 2017).

• Another major benefit of this procedure is that corporations can use it to gain competitive

advantage over traditional corporations. It is so since this allows corporate organisations to

become even more constructive in the pursuit of implementing strategic goals and policies. It

also helps executives to be familiar with existing threats and approaches to recover from those

threats. Corporations that pertain this strategy to improve their business are becoming more

profitable but more efficient.

Disadvantage

• Significant delay has been one of the biggest problems relating to variance analysis. This and

that at the end of every season employees just want a review of the variance analysis. For this

motive, accounting personnel are expected to plan this document to every and so every exercise.

As a result, it takes too much time in the whole differential research project. Since managers

often delay making appropriate decisions for this next year but they require to disclose the

financial statements that financial department would provide late. Besides that, analysis of

variance is a beneficial option that is not reasonably priced to all kinds of enterprises. Limited

businesses in general cannot incorporate this strategy in their Monetary Viewpoint performance

review process (NICOLETA, 2019).

Establish standards of reason for deviation in financial statement are not widely available. Each

of which accountants and auditors can go through various data sources, including such labor

rates, inventory billing and much more. Each of these resistance values evaluation of variances in

complicated problems less efficient.

• This approach is not useful for multi-financial reasons other than certain disadvantages. To

have an examination, it explores only economic concerns. And also the study of variances, there

is no detailed survey of any particular element. It only provides financial information relating to

pleasant and unpleasant variances. Manager will find out wide range of information for a proper

description.

7

ideas to improve sales (Iredele, Ogunleye and Okpala, 2017).

• Another major benefit of this procedure is that corporations can use it to gain competitive

advantage over traditional corporations. It is so since this allows corporate organisations to

become even more constructive in the pursuit of implementing strategic goals and policies. It

also helps executives to be familiar with existing threats and approaches to recover from those

threats. Corporations that pertain this strategy to improve their business are becoming more

profitable but more efficient.

Disadvantage

• Significant delay has been one of the biggest problems relating to variance analysis. This and

that at the end of every season employees just want a review of the variance analysis. For this

motive, accounting personnel are expected to plan this document to every and so every exercise.

As a result, it takes too much time in the whole differential research project. Since managers

often delay making appropriate decisions for this next year but they require to disclose the

financial statements that financial department would provide late. Besides that, analysis of

variance is a beneficial option that is not reasonably priced to all kinds of enterprises. Limited

businesses in general cannot incorporate this strategy in their Monetary Viewpoint performance

review process (NICOLETA, 2019).

Establish standards of reason for deviation in financial statement are not widely available. Each

of which accountants and auditors can go through various data sources, including such labor

rates, inventory billing and much more. Each of these resistance values evaluation of variances in

complicated problems less efficient.

• This approach is not useful for multi-financial reasons other than certain disadvantages. To

have an examination, it explores only economic concerns. And also the study of variances, there

is no detailed survey of any particular element. It only provides financial information relating to

pleasant and unpleasant variances. Manager will find out wide range of information for a proper

description.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

1. FamaQ gives XLG competitive advantage

The research section includes the critical assessment of the possible alternatives for XLG

adopted in this research. Company XLG is the manufacturer of marketed Chemical X and Y

cleaning agents and operates in a competitive environment. The core competency for the product

is patent protected against competition by all this. Hardly any corporation competition can copy

Fama Q. XLG also gets comparative advantages with this good or service. As stated in the case

company XLG imported goods Fama Q form Brazil and yet owing to lock-down, Coronavirus

break-out and enforced travel project prohibitions it has now become important when carrying

goods from one place (Octavia, 2019). This is true that Fama Q provides the XLG firm a

competitive advantage as it is the supplier's strongest cleaning agent and XLG takes protection to

protect its UK dominant market position from the rivals. With the Chemical X, the selling price

difference is £8500 and it's in a good position and for Chemical Y it is £5250 this seems to be in

preference.

2. Demand for chemical X and Y has increased by 45% which is likely to continue according to

market research

Prices for Chemical X and Y is increasing by 45 percent, so companies must also

commence their output according to marketing strategies because they need to stop buying

Brazilian consumer goods. The company but also any government minister who has to endure is

affected by the suspension operation in the country and around the world. Existing average cost

of the preservative is £2.50 per module, and besides owing to this global epidemic condition it

will improve the unit cost of £ 4.50 per group and then as a matter of fact XLG supplier will

have to pay £ 3.70 per unit to Fama Q. It will minimize the profitability of a company but that is

not worthwhile regarding the air mobility of capital intensive substrate. Business now wishes to

create fama Q in UK, rather than importing fama Q. It is also mentioned in the case study of

XLG that it is likely that demand for chemicals y and X may improve by about 45 percent thus

according changing market analysis (Rosenthal, 2019). This is therefore important for analyzing

potential alternatives for corporations and their implications on market over the coming time

frame on the premise of all the above knowledge. Appropriate assessment possibilities in the

present situation are quite essential to assessing the quality and credit worthiness of business

8

1. FamaQ gives XLG competitive advantage

The research section includes the critical assessment of the possible alternatives for XLG

adopted in this research. Company XLG is the manufacturer of marketed Chemical X and Y

cleaning agents and operates in a competitive environment. The core competency for the product

is patent protected against competition by all this. Hardly any corporation competition can copy

Fama Q. XLG also gets comparative advantages with this good or service. As stated in the case

company XLG imported goods Fama Q form Brazil and yet owing to lock-down, Coronavirus

break-out and enforced travel project prohibitions it has now become important when carrying

goods from one place (Octavia, 2019). This is true that Fama Q provides the XLG firm a

competitive advantage as it is the supplier's strongest cleaning agent and XLG takes protection to

protect its UK dominant market position from the rivals. With the Chemical X, the selling price

difference is £8500 and it's in a good position and for Chemical Y it is £5250 this seems to be in

preference.

2. Demand for chemical X and Y has increased by 45% which is likely to continue according to

market research

Prices for Chemical X and Y is increasing by 45 percent, so companies must also

commence their output according to marketing strategies because they need to stop buying

Brazilian consumer goods. The company but also any government minister who has to endure is

affected by the suspension operation in the country and around the world. Existing average cost

of the preservative is £2.50 per module, and besides owing to this global epidemic condition it

will improve the unit cost of £ 4.50 per group and then as a matter of fact XLG supplier will

have to pay £ 3.70 per unit to Fama Q. It will minimize the profitability of a company but that is

not worthwhile regarding the air mobility of capital intensive substrate. Business now wishes to

create fama Q in UK, rather than importing fama Q. It is also mentioned in the case study of

XLG that it is likely that demand for chemicals y and X may improve by about 45 percent thus

according changing market analysis (Rosenthal, 2019). This is therefore important for analyzing

potential alternatives for corporations and their implications on market over the coming time

frame on the premise of all the above knowledge. Appropriate assessment possibilities in the

present situation are quite essential to assessing the quality and credit worthiness of business

8

planning. In this situation , in order to maximize their amount of profit, individuals must keep

selling raw materials from Brazil and find their replacement or producing themselves in the UK

to manage their costs. So even though original film prices rising owing to increasing shipping

costs, this can minimize demand or minimize the amount of profit for XLG organization as well.

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15

working days

Making a product in the United Kingdom minimizes overall costs as well as reducing

timely delivery, that's quite significant in helping monitor too much persons. Since present an

increase manner, several companies or corporations that can provide services and products at

cheaper cost. Whenever industry gets extremely low costs and makes Fama Q divisions in the

UK then they'll have to repeat the process and keep selling from Brazil before the predicament

becomes acceptable.

XLG management is actively charging £3.70 to Fama Q and if they keep manufacturing in

the UK they will have £ 3 cost of production that takes 15 days shorter time to manufacture.

XLG retailer started to extend its reliance and initiate manufacturing products internationally as

it helps reduce costs by decreasing infrastructure and insurance premiums penalties (Setiawan,

Rahmawati and Widagdo, 2019). Work production from elsewhere in the UK not only takes

almost all hours at work that could aggravate the employee to place the order. In this pandemic

scenario, after considering all the variables and considerations that correspond to the further

operational costs and thereby boost the wholesale price, managers need to understand and make

strategic decisions that they should always implement with regards to the organization in order to

safeguard their performance and competitive value of goods and services. Lookdown satiations

develop considerable complications for the community where sustainability reporting seems to

be very impossible, employees find it hard to keep certain employers security and income

producing corporations. In this way necessary, it is the movement's perfect hope to protect its

performance (Situngkir and Napitupulu, 2019).

CONCLUSION

It has been observed from the current discussion that developing economic climate provides

various conflicts along with problems through support the growth and profitability of the

business. Utilising accounting principles, managers will make appropriate important decisions

9

selling raw materials from Brazil and find their replacement or producing themselves in the UK

to manage their costs. So even though original film prices rising owing to increasing shipping

costs, this can minimize demand or minimize the amount of profit for XLG organization as well.

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15

working days

Making a product in the United Kingdom minimizes overall costs as well as reducing

timely delivery, that's quite significant in helping monitor too much persons. Since present an

increase manner, several companies or corporations that can provide services and products at

cheaper cost. Whenever industry gets extremely low costs and makes Fama Q divisions in the

UK then they'll have to repeat the process and keep selling from Brazil before the predicament

becomes acceptable.

XLG management is actively charging £3.70 to Fama Q and if they keep manufacturing in

the UK they will have £ 3 cost of production that takes 15 days shorter time to manufacture.

XLG retailer started to extend its reliance and initiate manufacturing products internationally as

it helps reduce costs by decreasing infrastructure and insurance premiums penalties (Setiawan,

Rahmawati and Widagdo, 2019). Work production from elsewhere in the UK not only takes

almost all hours at work that could aggravate the employee to place the order. In this pandemic

scenario, after considering all the variables and considerations that correspond to the further

operational costs and thereby boost the wholesale price, managers need to understand and make

strategic decisions that they should always implement with regards to the organization in order to

safeguard their performance and competitive value of goods and services. Lookdown satiations

develop considerable complications for the community where sustainability reporting seems to

be very impossible, employees find it hard to keep certain employers security and income

producing corporations. In this way necessary, it is the movement's perfect hope to protect its

performance (Situngkir and Napitupulu, 2019).

CONCLUSION

It has been observed from the current discussion that developing economic climate provides

various conflicts along with problems through support the growth and profitability of the

business. Utilising accounting principles, managers will make appropriate important decisions

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.