Cost Report for XYZ Ltd: Variance Analysis, KPIs, and Suggestions

VerifiedAdded on 2023/04/21

|12

|867

|467

Report

AI Summary

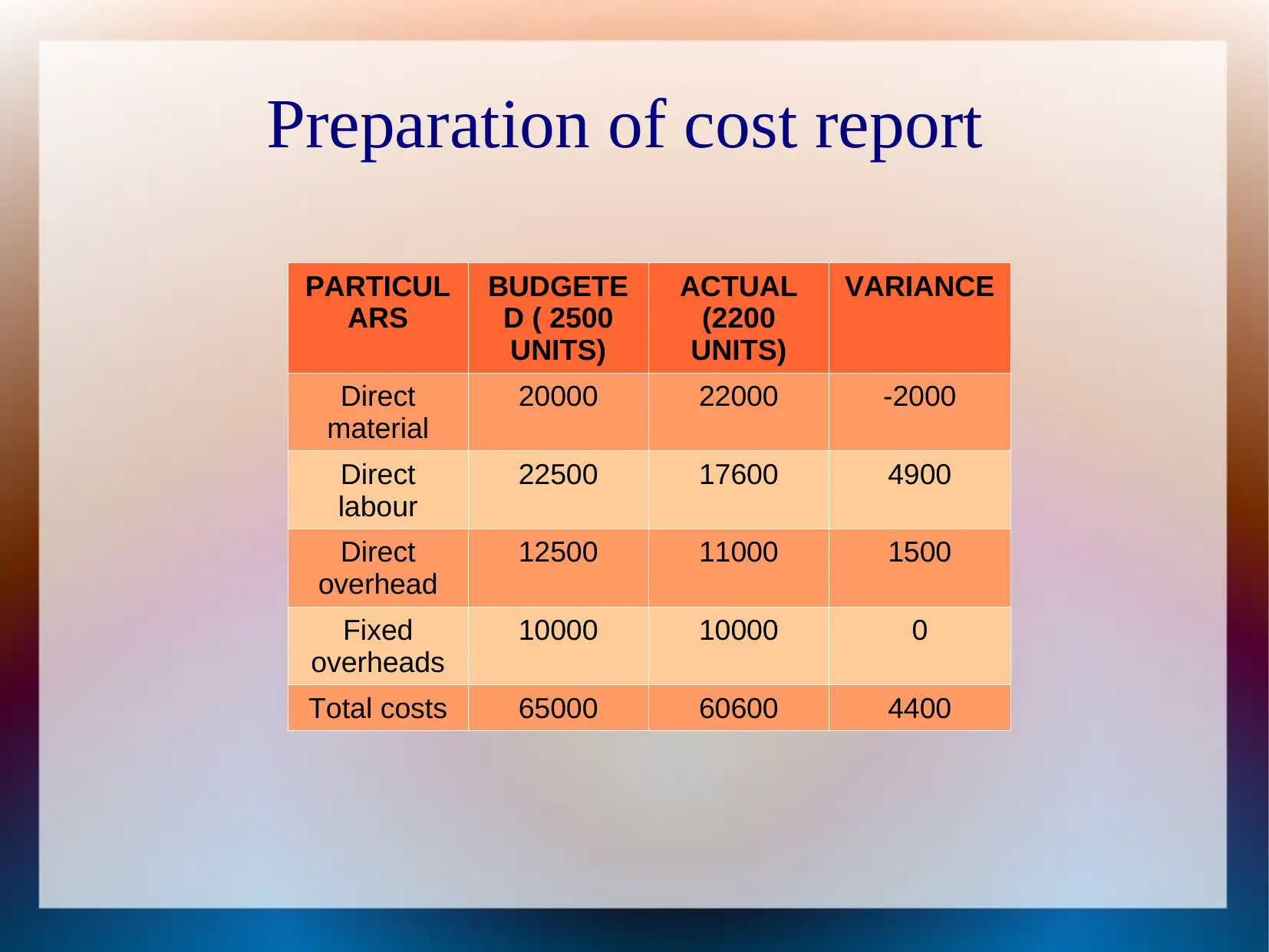

This report provides a detailed cost analysis for XYZ Ltd, comparing budgeted and actual costs to identify variances in direct materials, direct labor, and overhead. It interprets these variances, highlighting the impact of material price increases and labor rate differences. The report also outlines key performance indicators (KPIs) such as sales revenues, costs, profitability, product quality, and waiting time, suggesting that XYZ Ltd should regularly monitor these indicators for potential improvements. Furthermore, it offers practical suggestions for cost reduction, including lowering material buying prices, bargaining with labor, increasing production volume, and controlling unnecessary expenditures. The report concludes with recommendations for enhancing value and quality through better materials, advanced technology, and strategic initiatives like innovation and diversification. The report ends by providing a list of references.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.