Money and Banking: Yield Curve Analysis of Australia and Netherlands

VerifiedAdded on 2020/02/24

|9

|1003

|62

Report

AI Summary

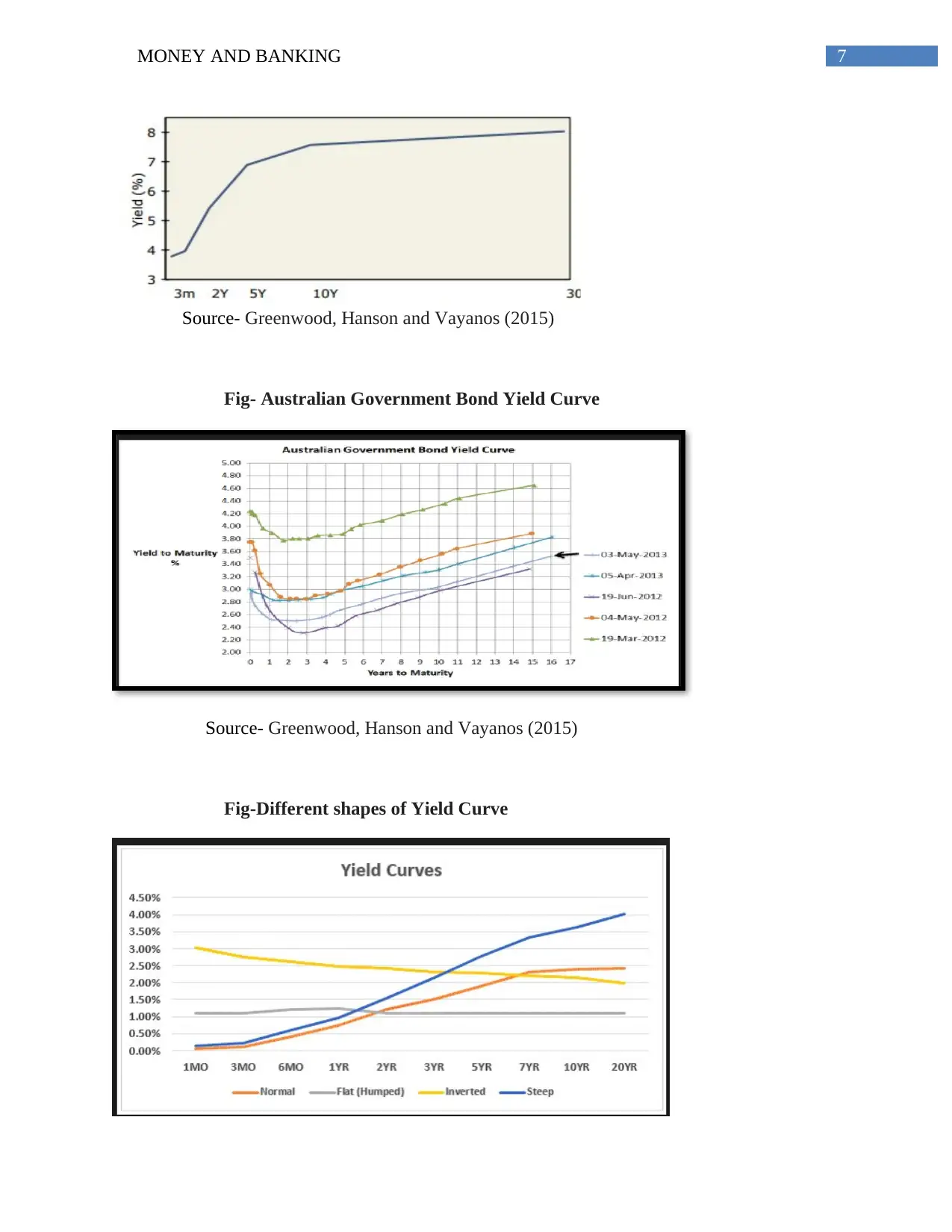

This report provides an in-depth analysis of the yield curves of Australia and the Netherlands. It examines the impact of the yield curve's level, steepness, and curvature on fixed income instruments. The report discusses how these factors influence interest rates and the volatility within the bond market. It also compares the economic implications of yield curve shapes, including upward sloping, flat, and inverted curves, and their relationship to economic activity, inflation, and recession predictions. Furthermore, the report considers the factors that influence the slope of the yield curve, and its relevance in making financial decisions within the economies of Australia and the Netherlands. Various figures illustrating the different shapes of the yield curve are also included to support the analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.