International Financial Markets and Institutions: Yield & P/E Analysis

VerifiedAdded on 2022/08/27

|15

|2749

|16

Report

AI Summary

This report provides a comprehensive analysis of international financial markets, focusing on yield curves and price-earnings (P/E) ratios. The first section defines yield curves, explains their different types (normal, inverted, and flat), and discusses the theories behind them, including market segmentation and liquidity preference theories. The analysis extends to examining the yield curves for 10-year government bonds in the UK, US, and China, drawing conclusions about market expectations and economic conditions. The second section delves into the P/E ratio, explaining its use in stock valuation and its theoretical underpinnings. It then presents a comparative analysis of P/E ratios for major Australian banks (Westpac, National Australia Bank, Commonwealth Bank, and ANZ) over a five-year period, including graphical representations and comparisons with industry averages. The report concludes with a discussion on the implications of these ratios for investors and the overall health of the banking sector.

Running head: INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Name of the Student

Name of the University

Author Note

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Table of Contents

Answer to Question 1:................................................................................................................2

Yield curve.............................................................................................................................2

Explanation of the Yield Curve..............................................................................................2

Theories of Yield Curve.........................................................................................................4

Yield Curve for the 10-Year Government Bonds..................................................................5

Answer to Question 2:................................................................................................................7

Price Earnings Ratio...............................................................................................................7

Theory of Price Earnings Ratio..............................................................................................7

Data Collection of Organizations...........................................................................................8

Industry price earnings ratio and Index price earnings ratio..................................................9

Comparison of each share for each time period...................................................................11

References................................................................................................................................13

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Table of Contents

Answer to Question 1:................................................................................................................2

Yield curve.............................................................................................................................2

Explanation of the Yield Curve..............................................................................................2

Theories of Yield Curve.........................................................................................................4

Yield Curve for the 10-Year Government Bonds..................................................................5

Answer to Question 2:................................................................................................................7

Price Earnings Ratio...............................................................................................................7

Theory of Price Earnings Ratio..............................................................................................7

Data Collection of Organizations...........................................................................................8

Industry price earnings ratio and Index price earnings ratio..................................................9

Comparison of each share for each time period...................................................................11

References................................................................................................................................13

2

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Answer to Question 1:

Yield curve

Yield curve can be defined as a curve that will display the rate of interest which is

being associated with the different lengths of contract which is for a specific debt instrument.

It will help in summarizing the usual relationship in-between the time of maturity of the debt

which is considered as the term and the yield which is the interest rate that is being associated

with the term.

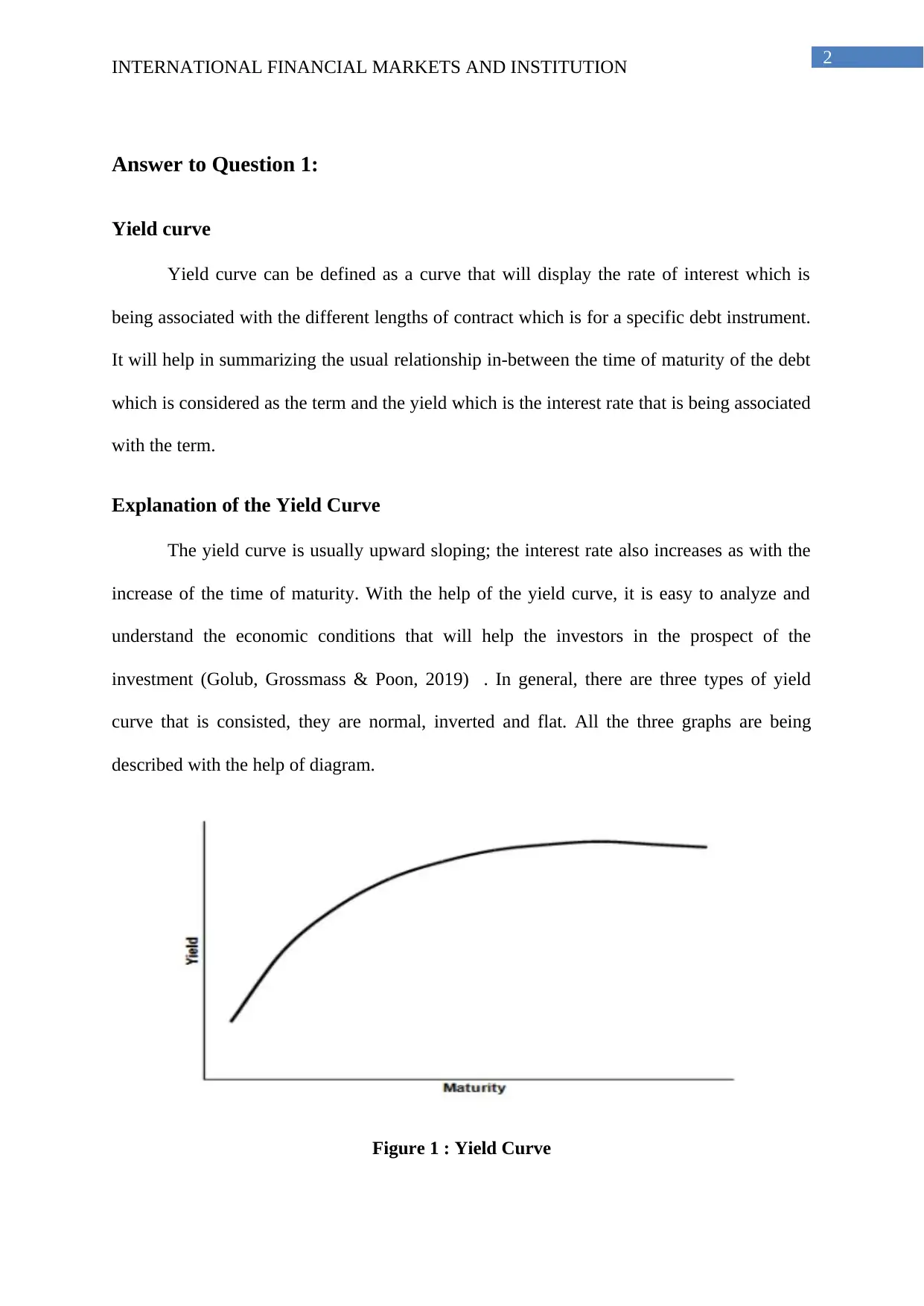

Explanation of the Yield Curve

The yield curve is usually upward sloping; the interest rate also increases as with the

increase of the time of maturity. With the help of the yield curve, it is easy to analyze and

understand the economic conditions that will help the investors in the prospect of the

investment (Golub, Grossmass & Poon, 2019) . In general, there are three types of yield

curve that is consisted, they are normal, inverted and flat. All the three graphs are being

described with the help of diagram.

Figure 1 : Yield Curve

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Answer to Question 1:

Yield curve

Yield curve can be defined as a curve that will display the rate of interest which is

being associated with the different lengths of contract which is for a specific debt instrument.

It will help in summarizing the usual relationship in-between the time of maturity of the debt

which is considered as the term and the yield which is the interest rate that is being associated

with the term.

Explanation of the Yield Curve

The yield curve is usually upward sloping; the interest rate also increases as with the

increase of the time of maturity. With the help of the yield curve, it is easy to analyze and

understand the economic conditions that will help the investors in the prospect of the

investment (Golub, Grossmass & Poon, 2019) . In general, there are three types of yield

curve that is consisted, they are normal, inverted and flat. All the three graphs are being

described with the help of diagram.

Figure 1 : Yield Curve

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

The graph that is being presented here is stated as the positive yield curve which

shows that the long term yield is much higher than the short term yield. According to the

economists Martin & Ross (2019), if an economy has a normal yield then it will be much

more for the country (Martin & Ross, 2019). It does indicate in the country is that the rate of

unemployment is much lower, the economy is in a growing stage currently. Thus, the desired

results which has been seen in the outcome will show that there will be an increase in the

return of bond as the time goes on (Choudhry, 2019). In the normal yield curve, the investors

will assume at the time of investing on bond is that the economy is in a healthier stage as it

will provide a support to the inflation rate which may cause an increase in the rate of interest.

If the rate of interest increases, then it will provide a better return on the bonds.

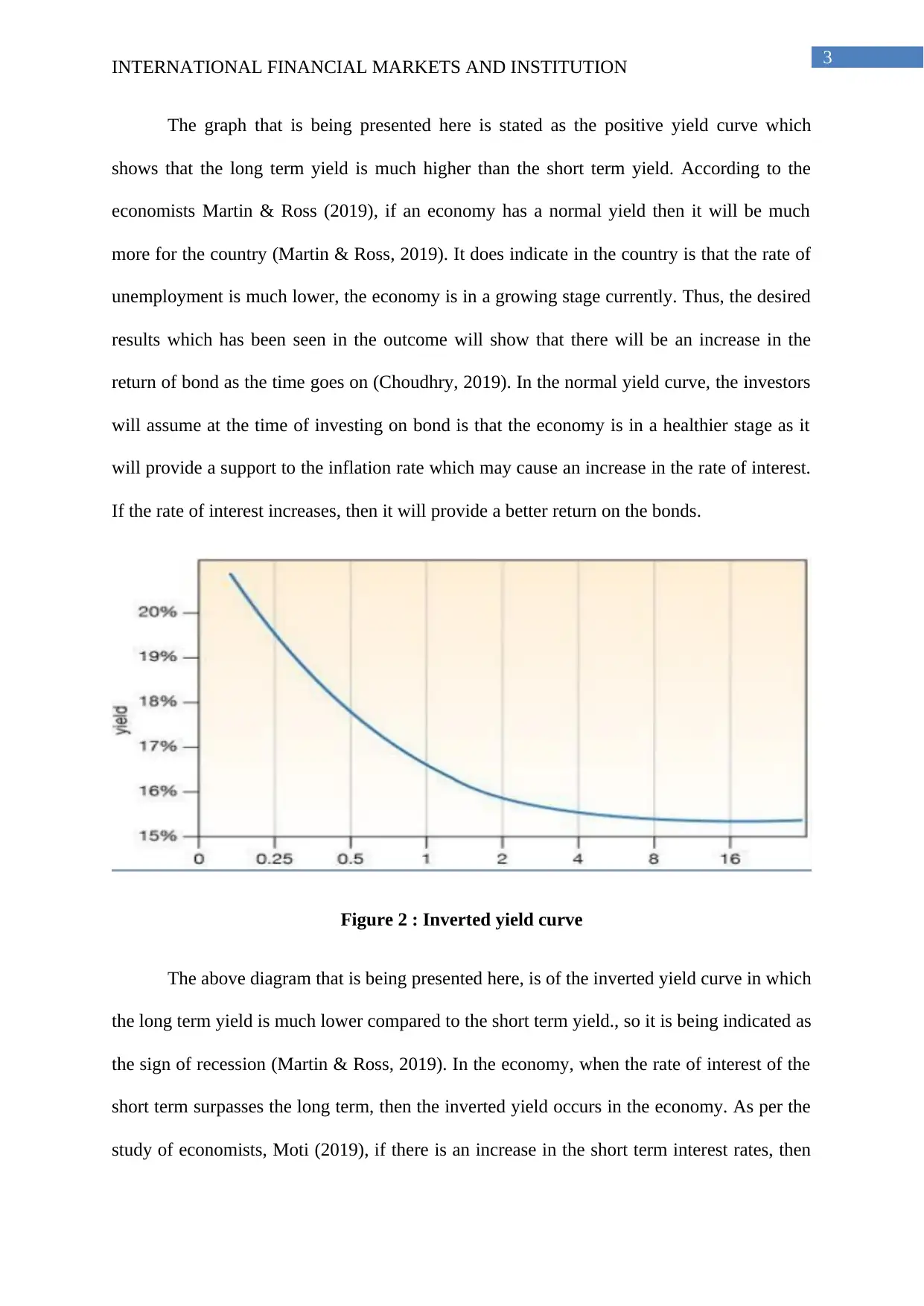

Figure 2 : Inverted yield curve

The above diagram that is being presented here, is of the inverted yield curve in which

the long term yield is much lower compared to the short term yield., so it is being indicated as

the sign of recession (Martin & Ross, 2019). In the economy, when the rate of interest of the

short term surpasses the long term, then the inverted yield occurs in the economy. As per the

study of economists, Moti (2019), if there is an increase in the short term interest rates, then

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

The graph that is being presented here is stated as the positive yield curve which

shows that the long term yield is much higher than the short term yield. According to the

economists Martin & Ross (2019), if an economy has a normal yield then it will be much

more for the country (Martin & Ross, 2019). It does indicate in the country is that the rate of

unemployment is much lower, the economy is in a growing stage currently. Thus, the desired

results which has been seen in the outcome will show that there will be an increase in the

return of bond as the time goes on (Choudhry, 2019). In the normal yield curve, the investors

will assume at the time of investing on bond is that the economy is in a healthier stage as it

will provide a support to the inflation rate which may cause an increase in the rate of interest.

If the rate of interest increases, then it will provide a better return on the bonds.

Figure 2 : Inverted yield curve

The above diagram that is being presented here, is of the inverted yield curve in which

the long term yield is much lower compared to the short term yield., so it is being indicated as

the sign of recession (Martin & Ross, 2019). In the economy, when the rate of interest of the

short term surpasses the long term, then the inverted yield occurs in the economy. As per the

study of economists, Moti (2019), if there is an increase in the short term interest rates, then

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

the interest rate will be highlighted and it can be seen that the long term securities which has

been out looked as it is poor and in the long term fixed income securities, the yield will tend

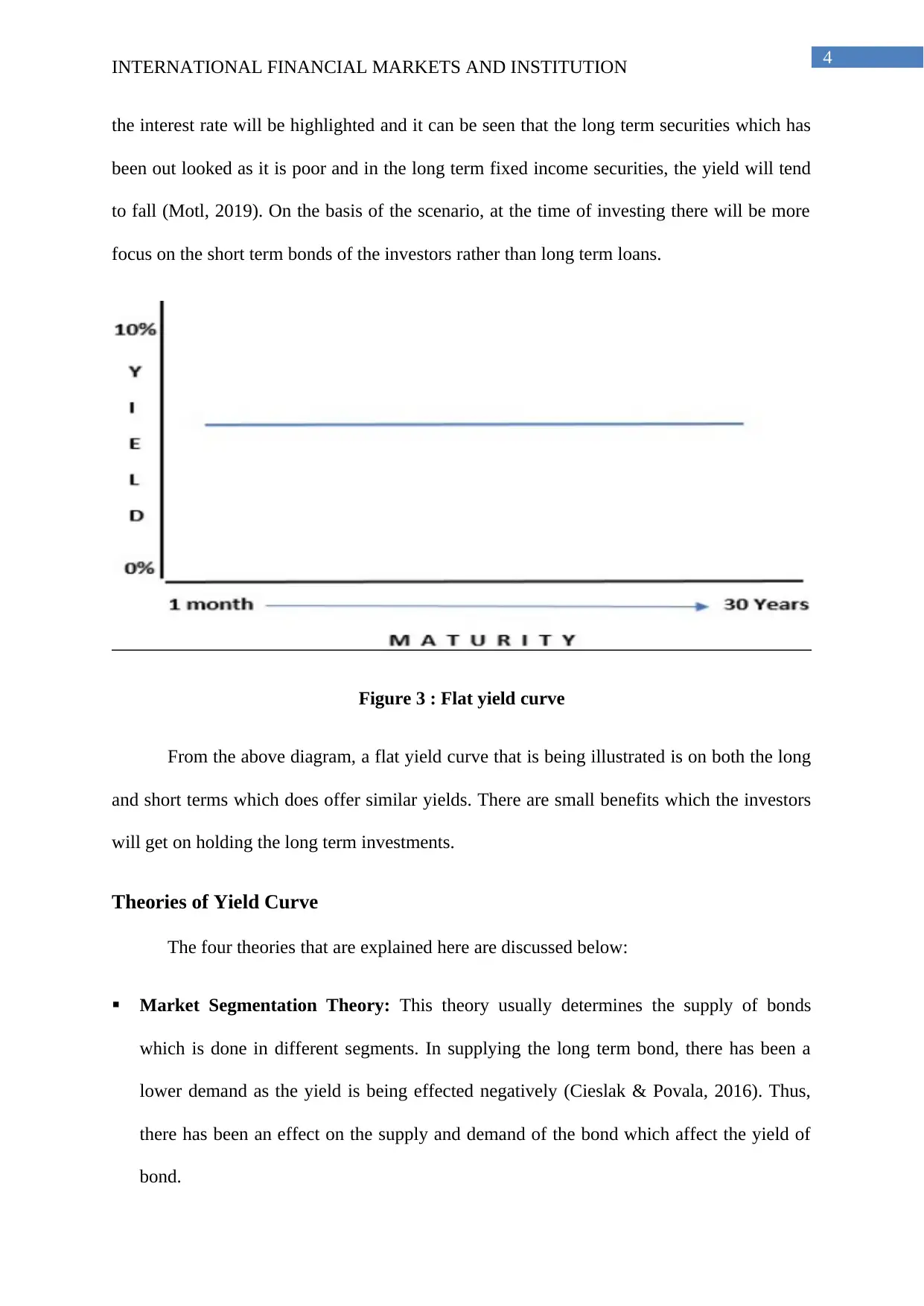

to fall (Motl, 2019). On the basis of the scenario, at the time of investing there will be more

focus on the short term bonds of the investors rather than long term loans.

Figure 3 : Flat yield curve

From the above diagram, a flat yield curve that is being illustrated is on both the long

and short terms which does offer similar yields. There are small benefits which the investors

will get on holding the long term investments.

Theories of Yield Curve

The four theories that are explained here are discussed below:

Market Segmentation Theory: This theory usually determines the supply of bonds

which is done in different segments. In supplying the long term bond, there has been a

lower demand as the yield is being effected negatively (Cieslak & Povala, 2016). Thus,

there has been an effect on the supply and demand of the bond which affect the yield of

bond.

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

the interest rate will be highlighted and it can be seen that the long term securities which has

been out looked as it is poor and in the long term fixed income securities, the yield will tend

to fall (Motl, 2019). On the basis of the scenario, at the time of investing there will be more

focus on the short term bonds of the investors rather than long term loans.

Figure 3 : Flat yield curve

From the above diagram, a flat yield curve that is being illustrated is on both the long

and short terms which does offer similar yields. There are small benefits which the investors

will get on holding the long term investments.

Theories of Yield Curve

The four theories that are explained here are discussed below:

Market Segmentation Theory: This theory usually determines the supply of bonds

which is done in different segments. In supplying the long term bond, there has been a

lower demand as the yield is being effected negatively (Cieslak & Povala, 2016). Thus,

there has been an effect on the supply and demand of the bond which affect the yield of

bond.

5

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Liquidity Preference Theory: In this, the investors do prefer a high liquidity on the

investment that is short term rather than the long term. Thus, it has an inverted curve and

there is preference of short term bonds by an investor.

Yield Curve for the 10-Year Government Bonds

There has been providence of the 10-year Government Bond, of three countries i.e.

United Kingdom, United States and China.

United States

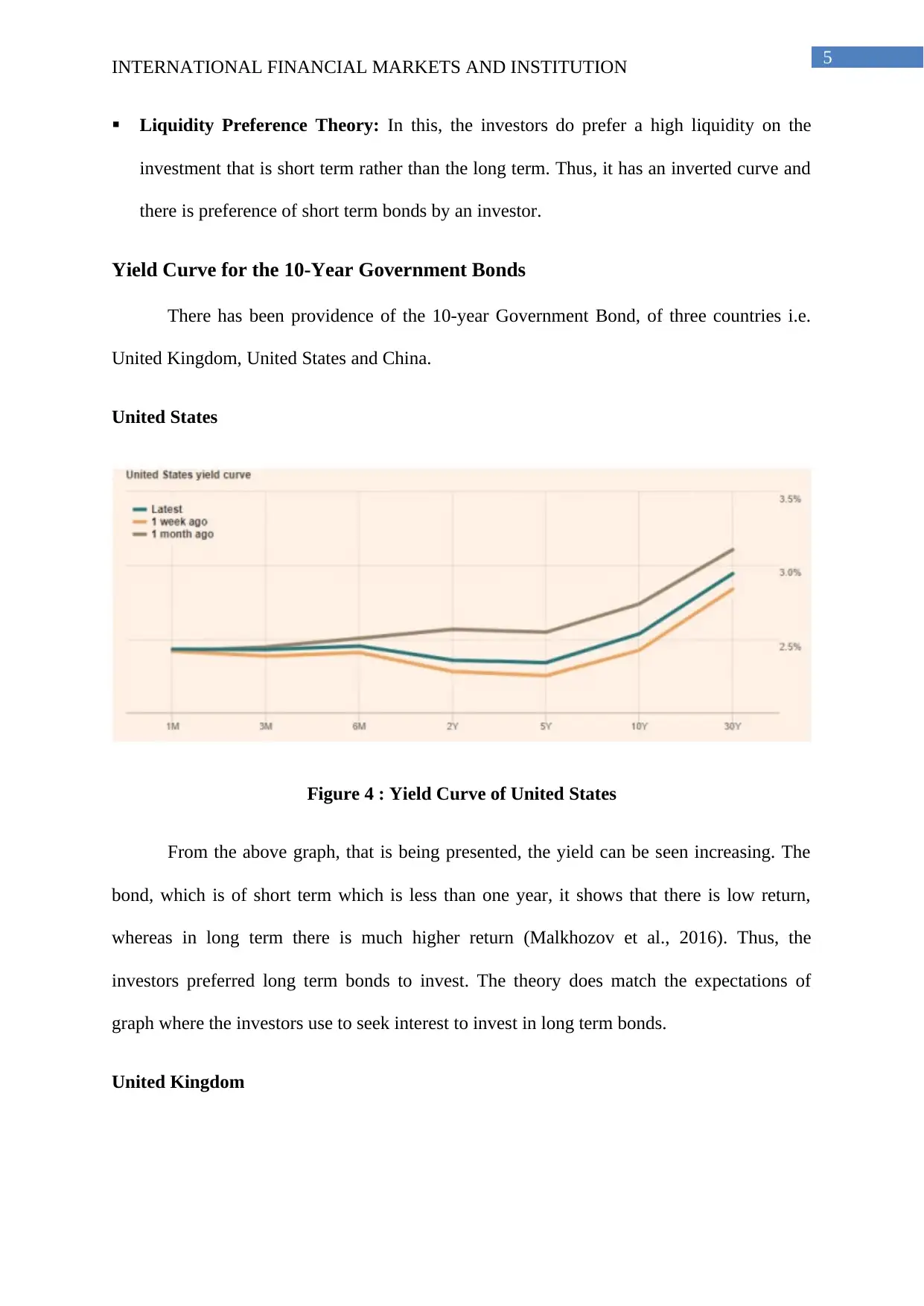

Figure 4 : Yield Curve of United States

From the above graph, that is being presented, the yield can be seen increasing. The

bond, which is of short term which is less than one year, it shows that there is low return,

whereas in long term there is much higher return (Malkhozov et al., 2016). Thus, the

investors preferred long term bonds to invest. The theory does match the expectations of

graph where the investors use to seek interest to invest in long term bonds.

United Kingdom

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Liquidity Preference Theory: In this, the investors do prefer a high liquidity on the

investment that is short term rather than the long term. Thus, it has an inverted curve and

there is preference of short term bonds by an investor.

Yield Curve for the 10-Year Government Bonds

There has been providence of the 10-year Government Bond, of three countries i.e.

United Kingdom, United States and China.

United States

Figure 4 : Yield Curve of United States

From the above graph, that is being presented, the yield can be seen increasing. The

bond, which is of short term which is less than one year, it shows that there is low return,

whereas in long term there is much higher return (Malkhozov et al., 2016). Thus, the

investors preferred long term bonds to invest. The theory does match the expectations of

graph where the investors use to seek interest to invest in long term bonds.

United Kingdom

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

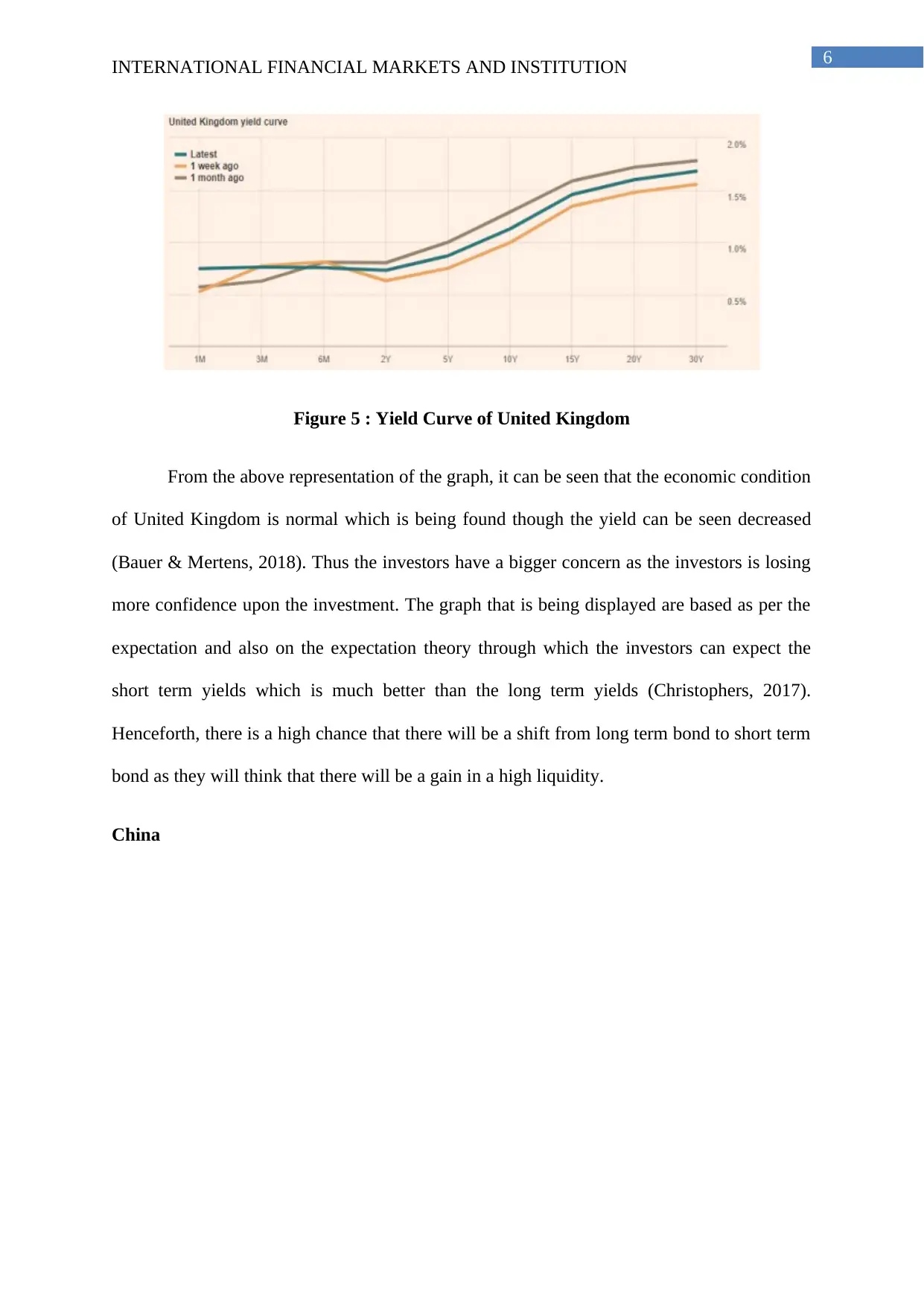

Figure 5 : Yield Curve of United Kingdom

From the above representation of the graph, it can be seen that the economic condition

of United Kingdom is normal which is being found though the yield can be seen decreased

(Bauer & Mertens, 2018). Thus the investors have a bigger concern as the investors is losing

more confidence upon the investment. The graph that is being displayed are based as per the

expectation and also on the expectation theory through which the investors can expect the

short term yields which is much better than the long term yields (Christophers, 2017).

Henceforth, there is a high chance that there will be a shift from long term bond to short term

bond as they will think that there will be a gain in a high liquidity.

China

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Figure 5 : Yield Curve of United Kingdom

From the above representation of the graph, it can be seen that the economic condition

of United Kingdom is normal which is being found though the yield can be seen decreased

(Bauer & Mertens, 2018). Thus the investors have a bigger concern as the investors is losing

more confidence upon the investment. The graph that is being displayed are based as per the

expectation and also on the expectation theory through which the investors can expect the

short term yields which is much better than the long term yields (Christophers, 2017).

Henceforth, there is a high chance that there will be a shift from long term bond to short term

bond as they will think that there will be a gain in a high liquidity.

China

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

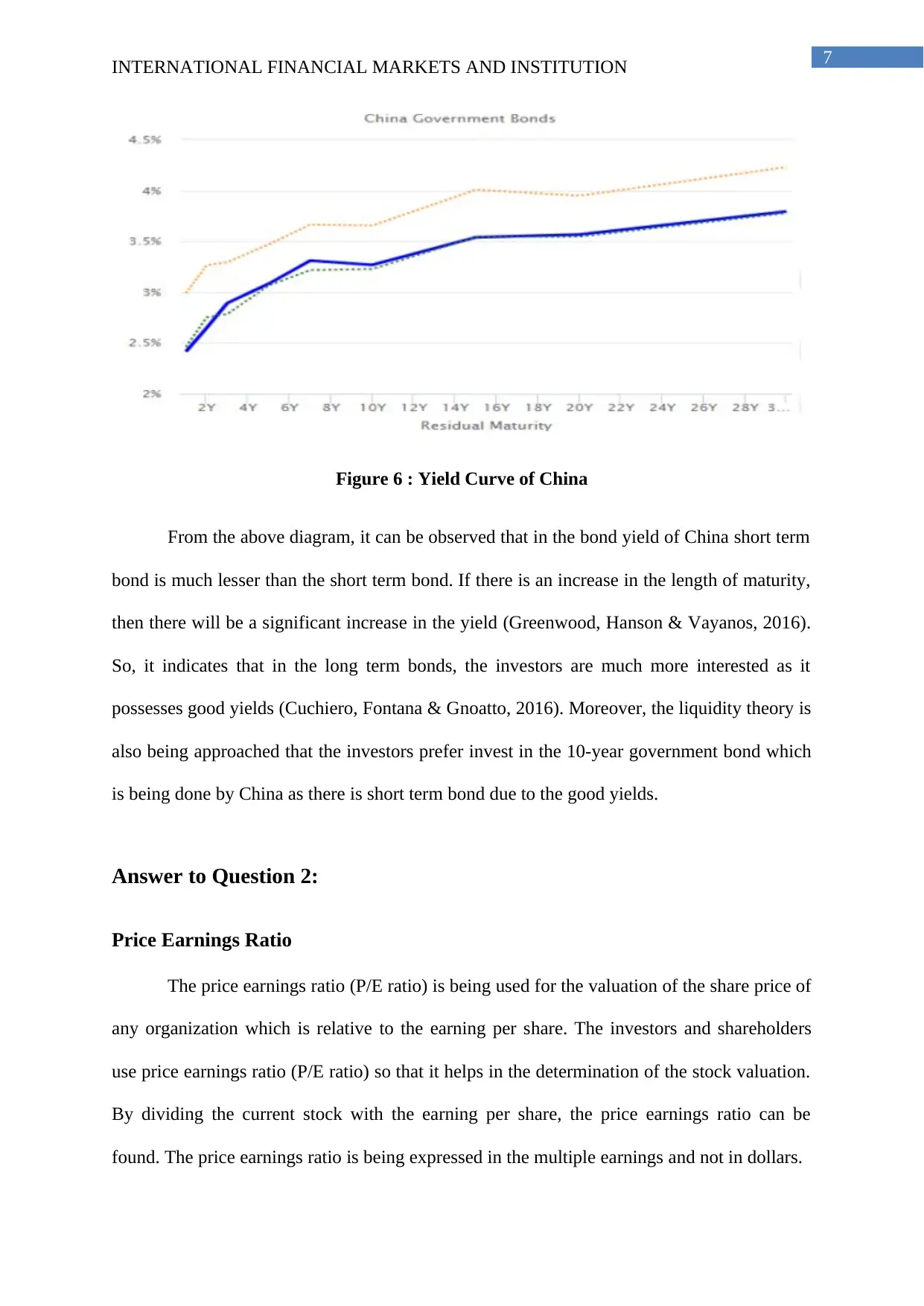

Figure 6 : Yield Curve of China

From the above diagram, it can be observed that in the bond yield of China short term

bond is much lesser than the short term bond. If there is an increase in the length of maturity,

then there will be a significant increase in the yield (Greenwood, Hanson & Vayanos, 2016).

So, it indicates that in the long term bonds, the investors are much more interested as it

possesses good yields (Cuchiero, Fontana & Gnoatto, 2016). Moreover, the liquidity theory is

also being approached that the investors prefer invest in the 10-year government bond which

is being done by China as there is short term bond due to the good yields.

Answer to Question 2:

Price Earnings Ratio

The price earnings ratio (P/E ratio) is being used for the valuation of the share price of

any organization which is relative to the earning per share. The investors and shareholders

use price earnings ratio (P/E ratio) so that it helps in the determination of the stock valuation.

By dividing the current stock with the earning per share, the price earnings ratio can be

found. The price earnings ratio is being expressed in the multiple earnings and not in dollars.

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Figure 6 : Yield Curve of China

From the above diagram, it can be observed that in the bond yield of China short term

bond is much lesser than the short term bond. If there is an increase in the length of maturity,

then there will be a significant increase in the yield (Greenwood, Hanson & Vayanos, 2016).

So, it indicates that in the long term bonds, the investors are much more interested as it

possesses good yields (Cuchiero, Fontana & Gnoatto, 2016). Moreover, the liquidity theory is

also being approached that the investors prefer invest in the 10-year government bond which

is being done by China as there is short term bond due to the good yields.

Answer to Question 2:

Price Earnings Ratio

The price earnings ratio (P/E ratio) is being used for the valuation of the share price of

any organization which is relative to the earning per share. The investors and shareholders

use price earnings ratio (P/E ratio) so that it helps in the determination of the stock valuation.

By dividing the current stock with the earning per share, the price earnings ratio can be

found. The price earnings ratio is being expressed in the multiple earnings and not in dollars.

8

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Theory of Price Earnings Ratio

On study of certain economists, it can be seen that the investors do have the concern

of checking the other share of organization. Thus, the ratio through which the investors does

the comparison and check it is with the price earnings ratio so that it can give a clear idea

about the financial status of the organization (Kumar & Venoor, 2018). Though at the time of

interpretation, sometimes it is difficult to find out the results by analyst. The information that

has been provided is being important as well as informative so further it is very much

difficult at the time of analyzing.

The study shows that, at the time of looking into the price earnings ratio, the

information that is being analyzed are either compared to the historical data of the

organization or with the competitor’s organization which is usually on the same industry. At

the time of buying the shares of the organization, the investors do want to invest at the

organization in which they are will get a better return. With the help of price earnings ratio, it

can be easily determined the value of the stock as it shows the fair price that is being paid

(Öztürk & Karabulut, 2018). The organizations that have a high price earnings ratio it is

known as the growth stocks that will state that it will give a better result in the future and the

expectation sis much higher compared to the other organizations. There has been a

disadvantage in the growing stock as it can be risk at the time of investment due to the much

more vitality (Siladjaja & Anwar, 2019). If the organizations do have the high price earnings

ratio, then it is being indicated that the stock is being overvalued. On the other side, it can be

seen that the organizations those have a lower price earnings ratio, will be considered as an

undervalued stock.

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Theory of Price Earnings Ratio

On study of certain economists, it can be seen that the investors do have the concern

of checking the other share of organization. Thus, the ratio through which the investors does

the comparison and check it is with the price earnings ratio so that it can give a clear idea

about the financial status of the organization (Kumar & Venoor, 2018). Though at the time of

interpretation, sometimes it is difficult to find out the results by analyst. The information that

has been provided is being important as well as informative so further it is very much

difficult at the time of analyzing.

The study shows that, at the time of looking into the price earnings ratio, the

information that is being analyzed are either compared to the historical data of the

organization or with the competitor’s organization which is usually on the same industry. At

the time of buying the shares of the organization, the investors do want to invest at the

organization in which they are will get a better return. With the help of price earnings ratio, it

can be easily determined the value of the stock as it shows the fair price that is being paid

(Öztürk & Karabulut, 2018). The organizations that have a high price earnings ratio it is

known as the growth stocks that will state that it will give a better result in the future and the

expectation sis much higher compared to the other organizations. There has been a

disadvantage in the growing stock as it can be risk at the time of investment due to the much

more vitality (Siladjaja & Anwar, 2019). If the organizations do have the high price earnings

ratio, then it is being indicated that the stock is being overvalued. On the other side, it can be

seen that the organizations those have a lower price earnings ratio, will be considered as an

undervalued stock.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

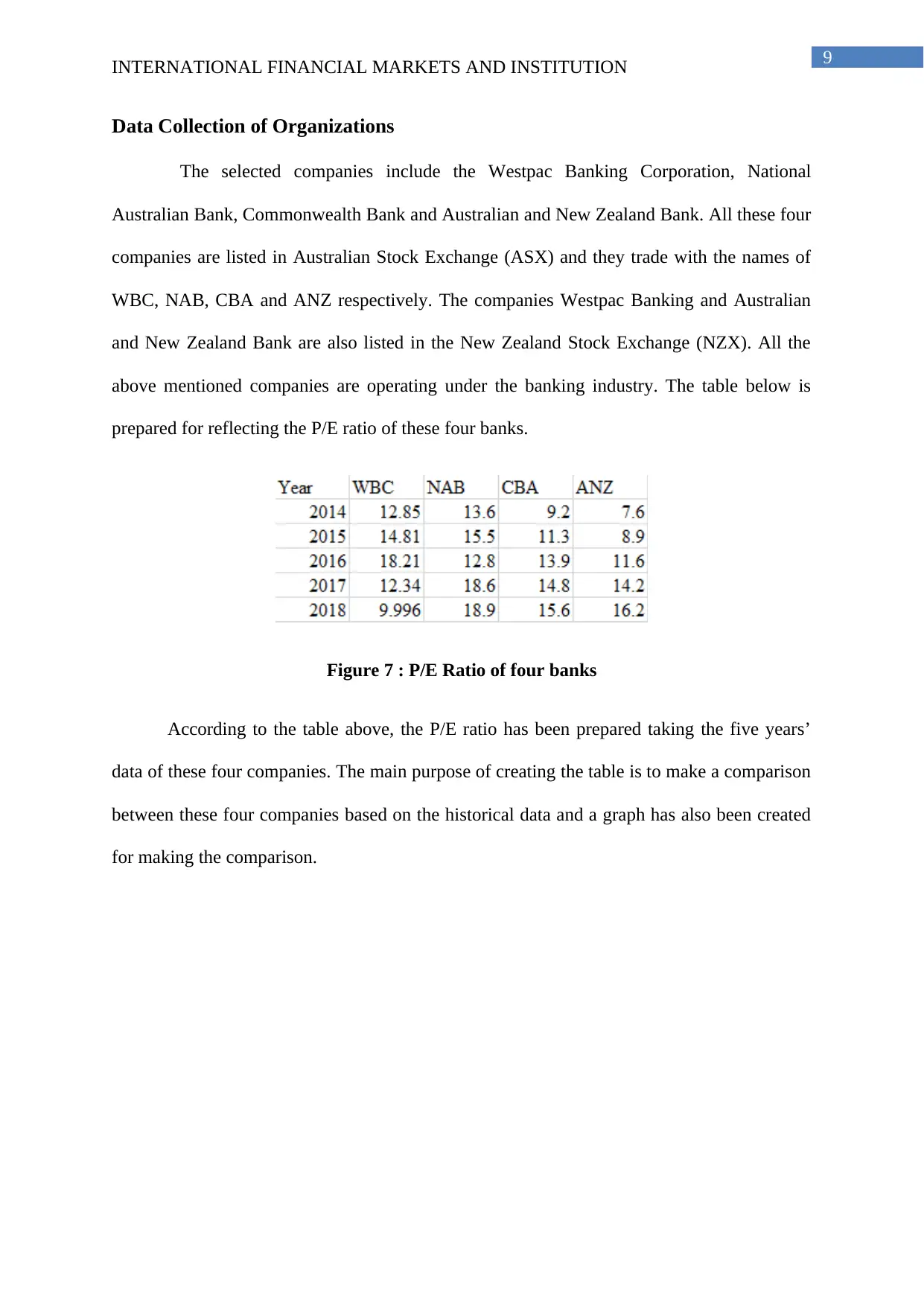

Data Collection of Organizations

The selected companies include the Westpac Banking Corporation, National

Australian Bank, Commonwealth Bank and Australian and New Zealand Bank. All these four

companies are listed in Australian Stock Exchange (ASX) and they trade with the names of

WBC, NAB, CBA and ANZ respectively. The companies Westpac Banking and Australian

and New Zealand Bank are also listed in the New Zealand Stock Exchange (NZX). All the

above mentioned companies are operating under the banking industry. The table below is

prepared for reflecting the P/E ratio of these four banks.

Figure 7 : P/E Ratio of four banks

According to the table above, the P/E ratio has been prepared taking the five years’

data of these four companies. The main purpose of creating the table is to make a comparison

between these four companies based on the historical data and a graph has also been created

for making the comparison.

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Data Collection of Organizations

The selected companies include the Westpac Banking Corporation, National

Australian Bank, Commonwealth Bank and Australian and New Zealand Bank. All these four

companies are listed in Australian Stock Exchange (ASX) and they trade with the names of

WBC, NAB, CBA and ANZ respectively. The companies Westpac Banking and Australian

and New Zealand Bank are also listed in the New Zealand Stock Exchange (NZX). All the

above mentioned companies are operating under the banking industry. The table below is

prepared for reflecting the P/E ratio of these four banks.

Figure 7 : P/E Ratio of four banks

According to the table above, the P/E ratio has been prepared taking the five years’

data of these four companies. The main purpose of creating the table is to make a comparison

between these four companies based on the historical data and a graph has also been created

for making the comparison.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

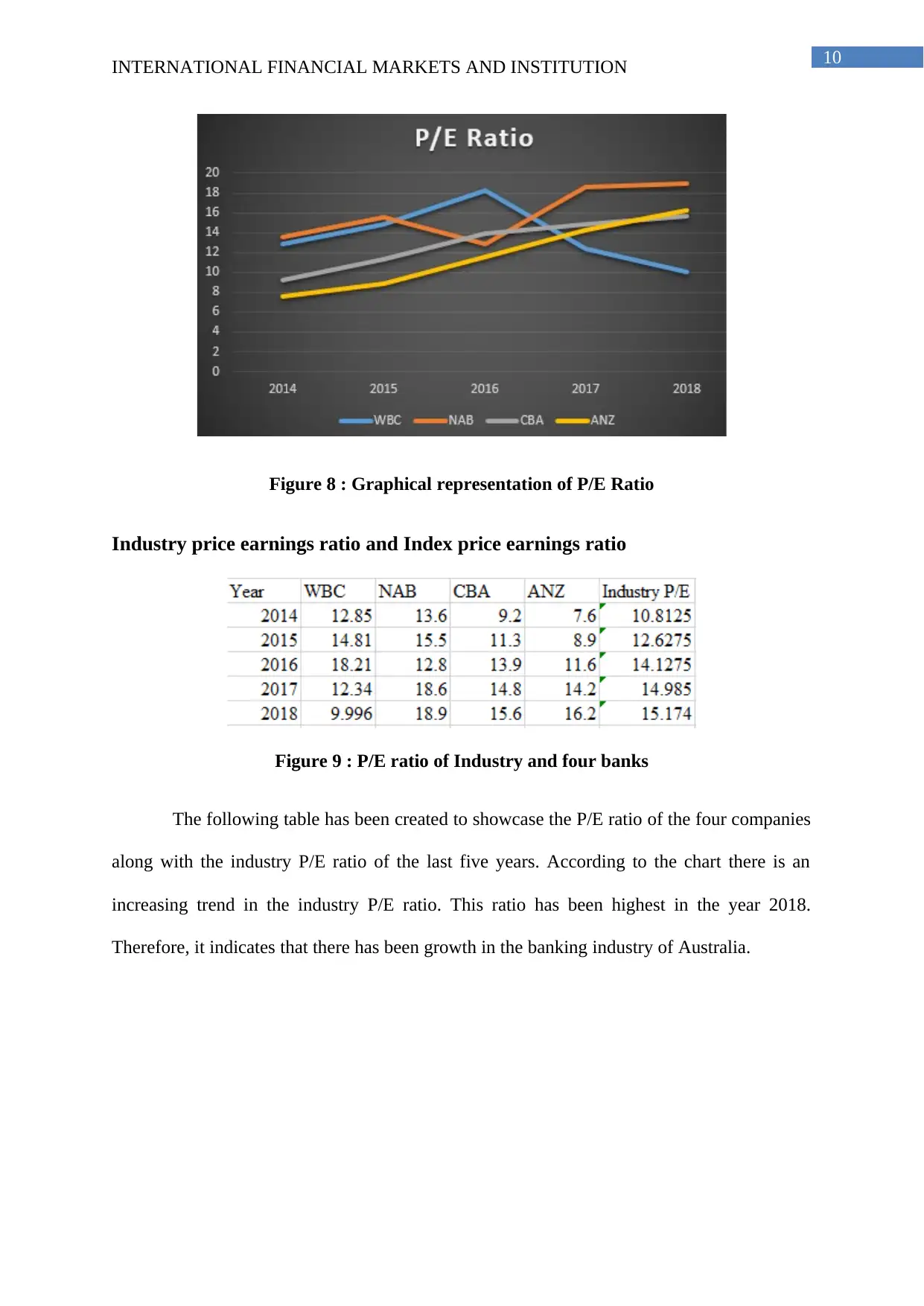

Figure 8 : Graphical representation of P/E Ratio

Industry price earnings ratio and Index price earnings ratio

Figure 9 : P/E ratio of Industry and four banks

The following table has been created to showcase the P/E ratio of the four companies

along with the industry P/E ratio of the last five years. According to the chart there is an

increasing trend in the industry P/E ratio. This ratio has been highest in the year 2018.

Therefore, it indicates that there has been growth in the banking industry of Australia.

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Figure 8 : Graphical representation of P/E Ratio

Industry price earnings ratio and Index price earnings ratio

Figure 9 : P/E ratio of Industry and four banks

The following table has been created to showcase the P/E ratio of the four companies

along with the industry P/E ratio of the last five years. According to the chart there is an

increasing trend in the industry P/E ratio. This ratio has been highest in the year 2018.

Therefore, it indicates that there has been growth in the banking industry of Australia.

11

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

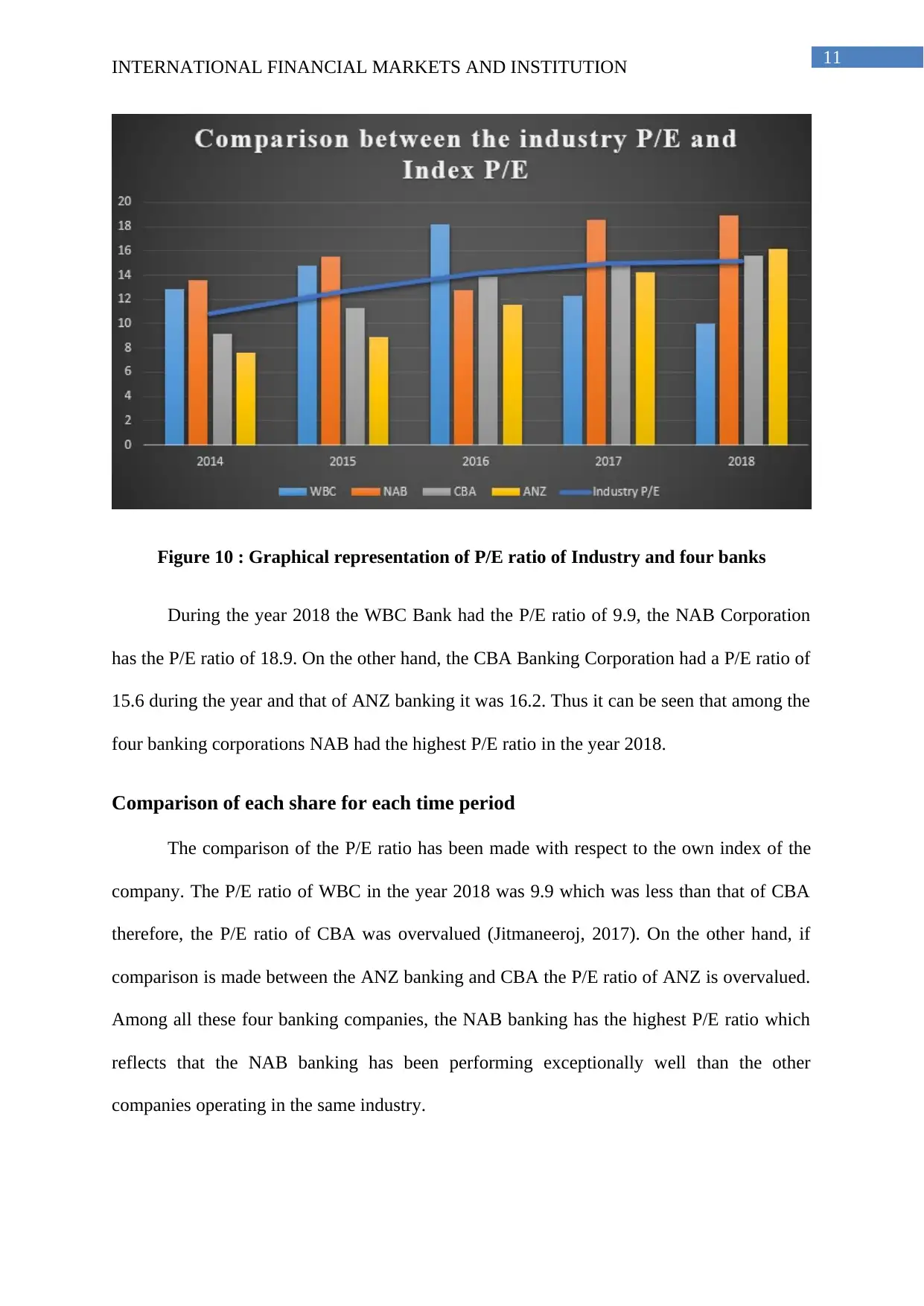

Figure 10 : Graphical representation of P/E ratio of Industry and four banks

During the year 2018 the WBC Bank had the P/E ratio of 9.9, the NAB Corporation

has the P/E ratio of 18.9. On the other hand, the CBA Banking Corporation had a P/E ratio of

15.6 during the year and that of ANZ banking it was 16.2. Thus it can be seen that among the

four banking corporations NAB had the highest P/E ratio in the year 2018.

Comparison of each share for each time period

The comparison of the P/E ratio has been made with respect to the own index of the

company. The P/E ratio of WBC in the year 2018 was 9.9 which was less than that of CBA

therefore, the P/E ratio of CBA was overvalued (Jitmaneeroj, 2017). On the other hand, if

comparison is made between the ANZ banking and CBA the P/E ratio of ANZ is overvalued.

Among all these four banking companies, the NAB banking has the highest P/E ratio which

reflects that the NAB banking has been performing exceptionally well than the other

companies operating in the same industry.

INTERNATIONAL FINANCIAL MARKETS AND INSTITUTION

Figure 10 : Graphical representation of P/E ratio of Industry and four banks

During the year 2018 the WBC Bank had the P/E ratio of 9.9, the NAB Corporation

has the P/E ratio of 18.9. On the other hand, the CBA Banking Corporation had a P/E ratio of

15.6 during the year and that of ANZ banking it was 16.2. Thus it can be seen that among the

four banking corporations NAB had the highest P/E ratio in the year 2018.

Comparison of each share for each time period

The comparison of the P/E ratio has been made with respect to the own index of the

company. The P/E ratio of WBC in the year 2018 was 9.9 which was less than that of CBA

therefore, the P/E ratio of CBA was overvalued (Jitmaneeroj, 2017). On the other hand, if

comparison is made between the ANZ banking and CBA the P/E ratio of ANZ is overvalued.

Among all these four banking companies, the NAB banking has the highest P/E ratio which

reflects that the NAB banking has been performing exceptionally well than the other

companies operating in the same industry.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.