Accounting Information Systems Case Study: Y Not Flowers, Inc. (YNF)

VerifiedAdded on 2023/06/07

|6

|747

|467

Case Study

AI Summary

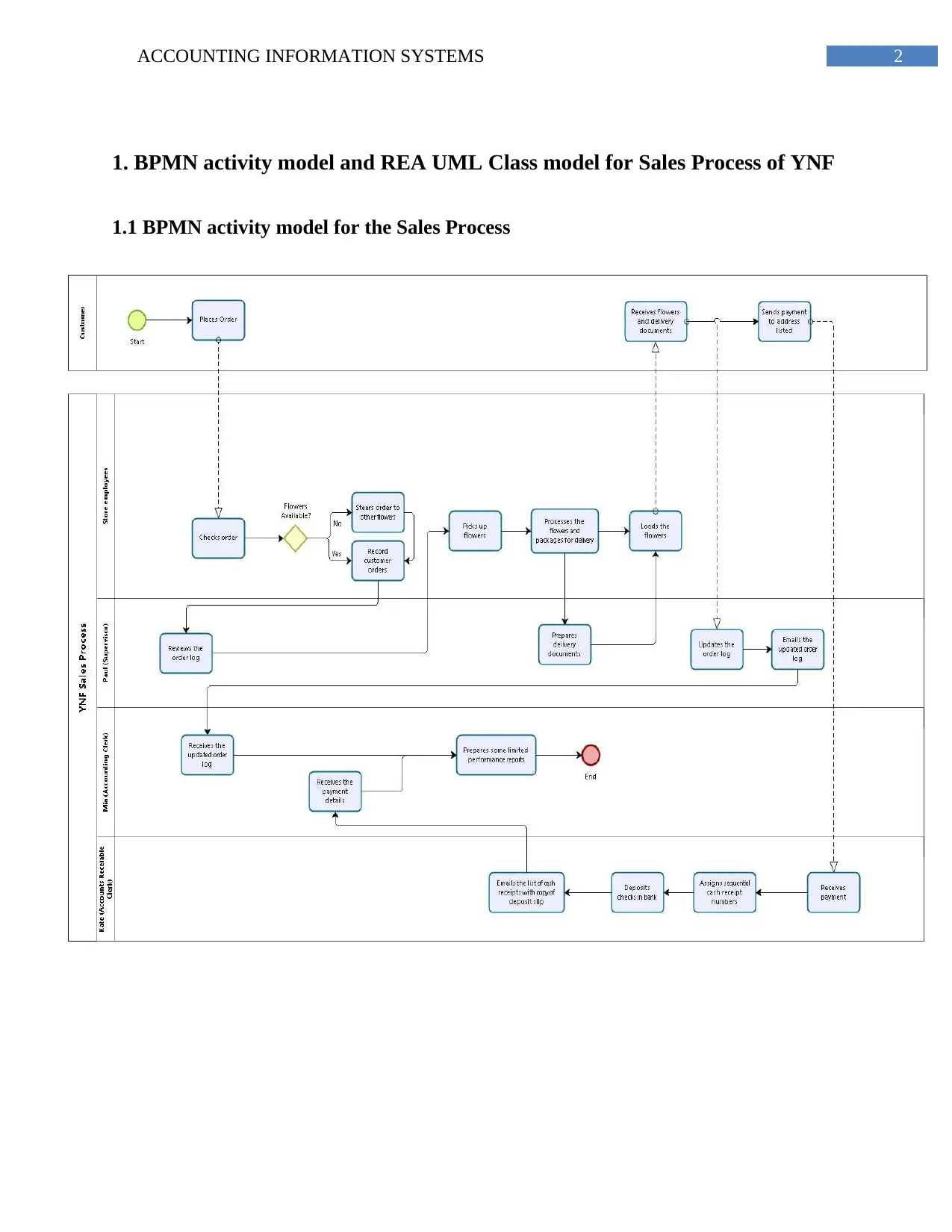

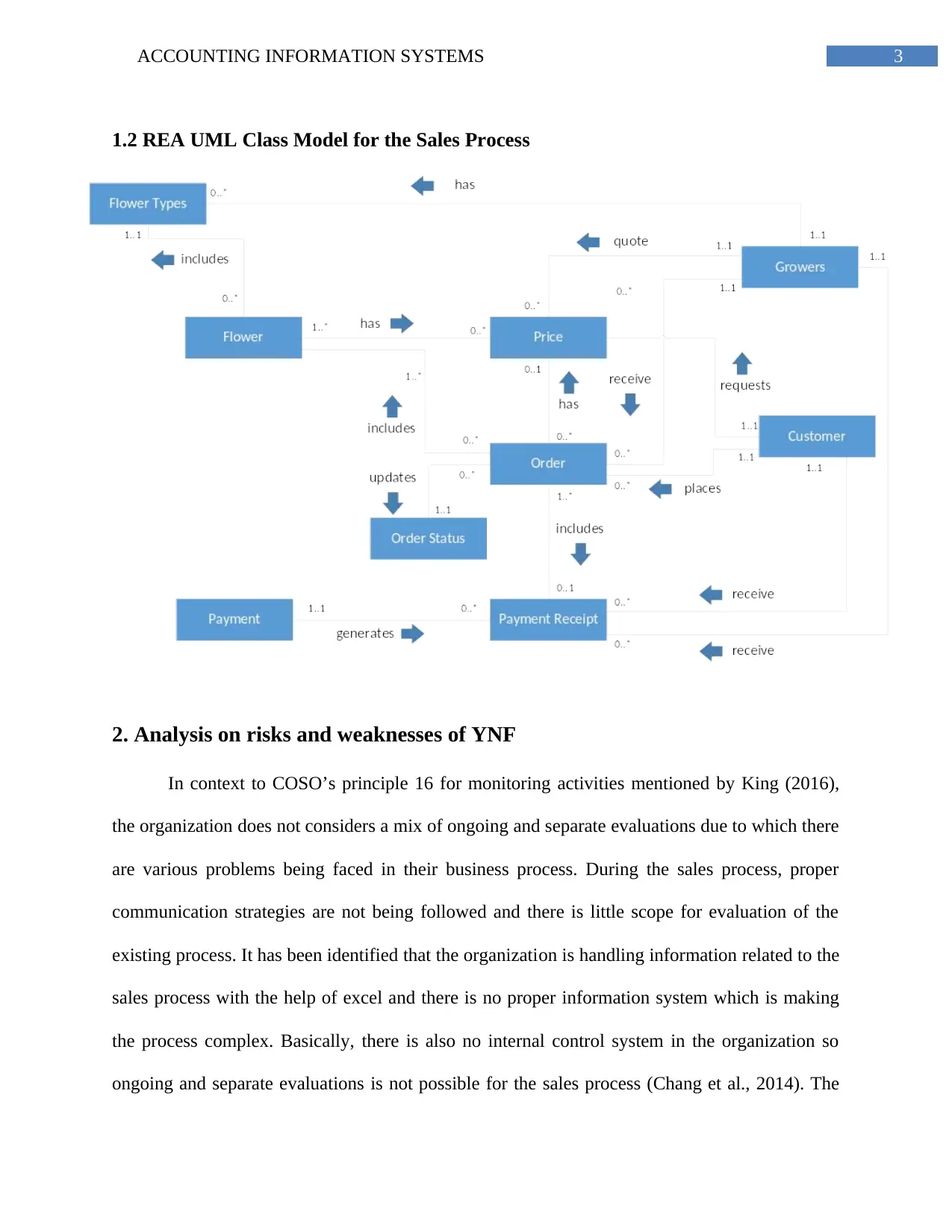

This case study provides an analysis of Y Not Flowers, Inc.'s (YNF) accounting information systems, focusing on the sales process and associated risks. It includes a BPMN activity model and an REA UML class model to illustrate the sales process. The analysis identifies weaknesses within YNF's current systems, particularly the lack of a formal information system and reliance on Excel for data management. The study also highlights the organization's failure to adhere to COSO principles related to monitoring activities and communication of internal control deficiencies. Recommendations are made for implementing regular evaluations and improving communication channels to address these shortcomings and enhance the overall effectiveness of the sales process and internal controls within YNF.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.