BSBFIM501 Manage Budgets and Financial Plans: YouFood Limited

VerifiedAdded on 2023/06/04

|13

|2458

|334

Report

AI Summary

This report presents a master budget for YouFood Limited, including targeted sales based on market assessment. It details projected costs, proposes a profit structure, and addresses organizational financial procedures, such as cash sales and regulatory compliance. The report summarizes activities, including payment policies and transportation costs, and outlines a plan for budget modifications and a contingency plan for unforeseen circumstances. It also covers basic accounting principles, ATO requirements, financial record keeping, auditing techniques, and budgeting processes. Furthermore, it identifies performance activities, observations on accounting techniques, and solutions for issues like product wastage and fuel costs, culminating in a modified budget for 2018.

Running head: BUDGET

Budget

Name of the Student:

Name of the University:

Authors Note:

Budget

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

BUDGET

Table of Contents

Section 1:....................................................................................................................................2

Section B:...................................................................................................................................5

Section C:...................................................................................................................................7

Reference..................................................................................................................................11

BUDGET

Table of Contents

Section 1:....................................................................................................................................2

Section B:...................................................................................................................................5

Section C:...................................................................................................................................7

Reference..................................................................................................................................11

2

BUDGET

Section 1:

Introduction:

In the content of the report, a master budget for the YouFood Limited is drafted. In the

contents of the master budgets, the targeted sales of the company are also drafted based on

the assessment of the market.

Audience:

The budget is prepared for the CEO, production manager, Sales manager, and sales teams.

Master Budgets:

The presented master budget will elaborate the various projected cost of the organization and

the will identify a proposed profit structure. The master budget will hold the sales and other

expenses of the business for the current financial year (Maskell et al. 2016). In addition to

that, if the audience has any queries then ask for clarifications. From the following

questionnaires

The contents are not relevant

There is an inadequacy in the statement

The sources and assumptions of the amounts

Others.

Budget:

The budget for You Foods

For the Year 2018

Particulars Amounts

BUDGET

Section 1:

Introduction:

In the content of the report, a master budget for the YouFood Limited is drafted. In the

contents of the master budgets, the targeted sales of the company are also drafted based on

the assessment of the market.

Audience:

The budget is prepared for the CEO, production manager, Sales manager, and sales teams.

Master Budgets:

The presented master budget will elaborate the various projected cost of the organization and

the will identify a proposed profit structure. The master budget will hold the sales and other

expenses of the business for the current financial year (Maskell et al. 2016). In addition to

that, if the audience has any queries then ask for clarifications. From the following

questionnaires

The contents are not relevant

There is an inadequacy in the statement

The sources and assumptions of the amounts

Others.

Budget:

The budget for You Foods

For the Year 2018

Particulars Amounts

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

BUDGET

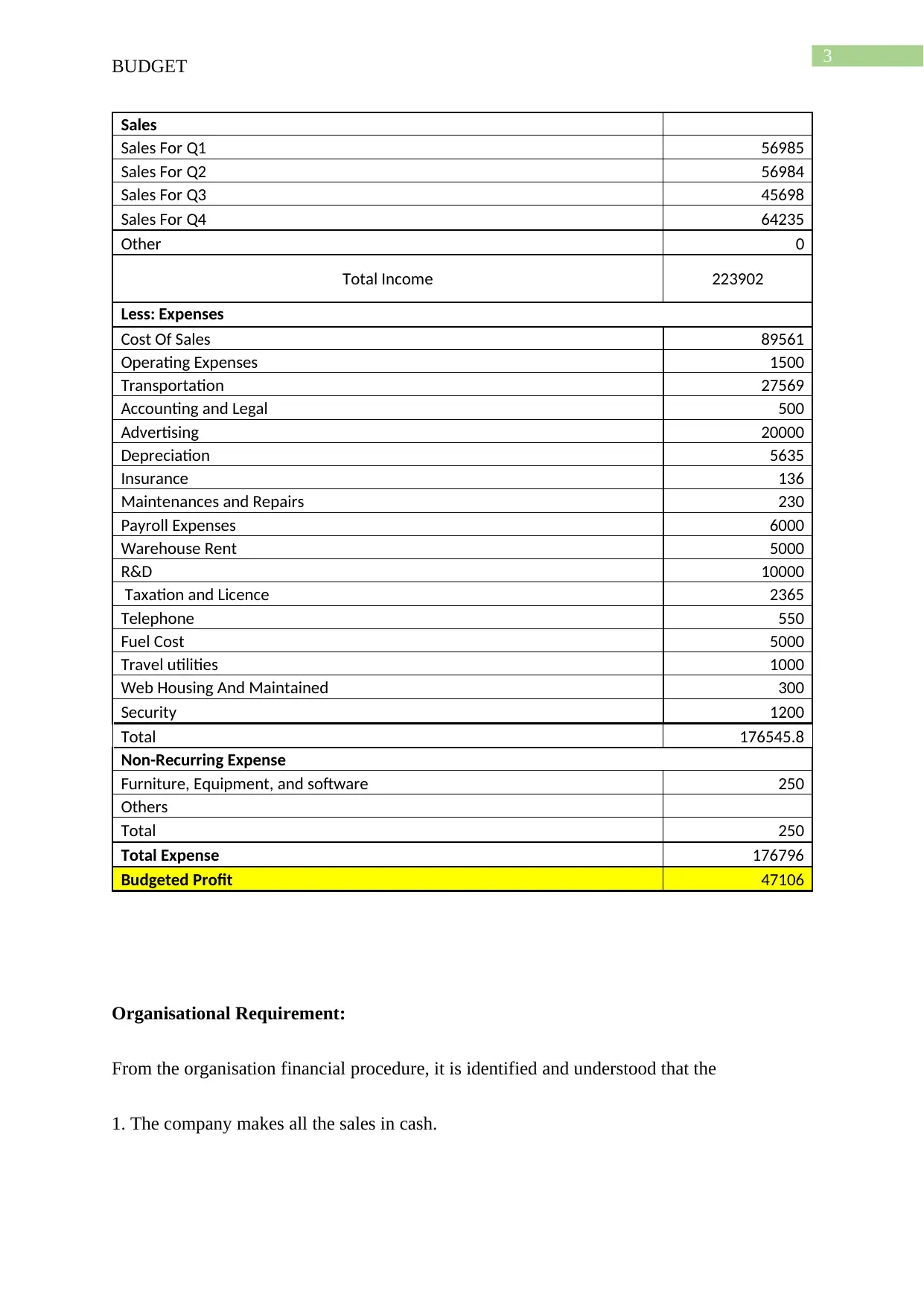

Sales

Sales For Q1 56985

Sales For Q2 56984

Sales For Q3 45698

Sales For Q4 64235

Other 0

Total Income 223902

Less: Expenses

Cost Of Sales 89561

Operating Expenses 1500

Transportation 27569

Accounting and Legal 500

Advertising 20000

Depreciation 5635

Insurance 136

Maintenances and Repairs 230

Payroll Expenses 6000

Warehouse Rent 5000

R&D 10000

Taxation and Licence 2365

Telephone 550

Fuel Cost 5000

Travel utilities 1000

Web Housing And Maintained 300

Security 1200

Total 176545.8

Non-Recurring Expense

Furniture, Equipment, and software 250

Others

Total 250

Total Expense 176796

Budgeted Profit 47106

Organisational Requirement:

From the organisation financial procedure, it is identified and understood that the

1. The company makes all the sales in cash.

BUDGET

Sales

Sales For Q1 56985

Sales For Q2 56984

Sales For Q3 45698

Sales For Q4 64235

Other 0

Total Income 223902

Less: Expenses

Cost Of Sales 89561

Operating Expenses 1500

Transportation 27569

Accounting and Legal 500

Advertising 20000

Depreciation 5635

Insurance 136

Maintenances and Repairs 230

Payroll Expenses 6000

Warehouse Rent 5000

R&D 10000

Taxation and Licence 2365

Telephone 550

Fuel Cost 5000

Travel utilities 1000

Web Housing And Maintained 300

Security 1200

Total 176545.8

Non-Recurring Expense

Furniture, Equipment, and software 250

Others

Total 250

Total Expense 176796

Budgeted Profit 47106

Organisational Requirement:

From the organisation financial procedure, it is identified and understood that the

1. The company makes all the sales in cash.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

BUDGET

2. In addition to that as the company is engaged in the food industry, it requires fulfilling

some safety and other regulations that make the cost of the company a bit higher.

3. Another financial indicator for the company is the cost of delivery as this is a B2C business

model business (Barr and McClellan 2018).

4. The cost or warehouse and the kitchen of the company are payable at the end of12-month.

5. The accounts of the company are prepared on the applicable accounting standards and the

taxation will be withheld under the provisions of their ITAA 1997.

Summary of the activities.

As there all the sale of the company is made in cash or banking transaction, therefore,

no available debtors are presented in the current moment. In addition to that, the current

payment policies to the creditor or the suppliers of the YouFood are paid for 4 weeks (Drever

et al. 2015).

Secondly, the current atmosphere of the company is not located a particular of, rather

it is delivering the foods that are placed online direct from the kitchen to the customers place

therefore the cost of transportation is very high.

Further, the company does not have its own premises, therefore; the company has

acquired a rented place for warehousing and for essential cooking of the orders. The financial

accounting and the management accounting are prepared in accordance with the requirements

of the company (Rogulenko et al. 2016).

Changes in the plan:

If there are requirements for any change in the budget or the accounting policy then at

first, the problematic areas are to be identified and the modification will be made after finding

all the information if there are many flows in the budget then it should be redrafted. It may

BUDGET

2. In addition to that as the company is engaged in the food industry, it requires fulfilling

some safety and other regulations that make the cost of the company a bit higher.

3. Another financial indicator for the company is the cost of delivery as this is a B2C business

model business (Barr and McClellan 2018).

4. The cost or warehouse and the kitchen of the company are payable at the end of12-month.

5. The accounts of the company are prepared on the applicable accounting standards and the

taxation will be withheld under the provisions of their ITAA 1997.

Summary of the activities.

As there all the sale of the company is made in cash or banking transaction, therefore,

no available debtors are presented in the current moment. In addition to that, the current

payment policies to the creditor or the suppliers of the YouFood are paid for 4 weeks (Drever

et al. 2015).

Secondly, the current atmosphere of the company is not located a particular of, rather

it is delivering the foods that are placed online direct from the kitchen to the customers place

therefore the cost of transportation is very high.

Further, the company does not have its own premises, therefore; the company has

acquired a rented place for warehousing and for essential cooking of the orders. The financial

accounting and the management accounting are prepared in accordance with the requirements

of the company (Rogulenko et al. 2016).

Changes in the plan:

If there are requirements for any change in the budget or the accounting policy then at

first, the problematic areas are to be identified and the modification will be made after finding

all the information if there are many flows in the budget then it should be redrafted. It may

5

BUDGET

take up to 10 days (Crutzen et al. 2017). In this period, a contingency plan also will be

drafted.

Section B:

1. Aspects of basis accounting Principal:

For the preparation and presentation of the various accounting transaction, some

inherent accounting principles are required to be followed. The basic accounting

principles are described hereunder:

Economic entity assumption: this assumption segregates the business owner

from its business. In accounting, the owner and the business are separate

entities. This legalises the existence of the business a separate legal entity as a

distinct person (Miller 2018).

Going Concern Principal: the going concern principal assumes that the

business will exist for a long period that means that the business is not going

to stop the business in the near future.

Accrual basis of accounting: in the accrual basis of accounting the business

transaction is recorded on the accrual basis, there are two types of permissible

accoutring recording techniques cash basis and accrual basis. In cash basis, the

accounting transactions are recorded only when the cash transaction is

received or paid (Alviniussen and Jankensgard 2015). This technic is followed

by small entities. The general principal states that the accounting is to be done

on the accrual method of transaction, where the actual transaction is more

important than the cash possession of the transaction. The accounts are to be

dealt at the transaction date irrespective of the cash received of payments.

2. As per the ATO's requirements, all the transactions or the information are to be

reported to the Australian taxation office are as follows:

BUDGET

take up to 10 days (Crutzen et al. 2017). In this period, a contingency plan also will be

drafted.

Section B:

1. Aspects of basis accounting Principal:

For the preparation and presentation of the various accounting transaction, some

inherent accounting principles are required to be followed. The basic accounting

principles are described hereunder:

Economic entity assumption: this assumption segregates the business owner

from its business. In accounting, the owner and the business are separate

entities. This legalises the existence of the business a separate legal entity as a

distinct person (Miller 2018).

Going Concern Principal: the going concern principal assumes that the

business will exist for a long period that means that the business is not going

to stop the business in the near future.

Accrual basis of accounting: in the accrual basis of accounting the business

transaction is recorded on the accrual basis, there are two types of permissible

accoutring recording techniques cash basis and accrual basis. In cash basis, the

accounting transactions are recorded only when the cash transaction is

received or paid (Alviniussen and Jankensgard 2015). This technic is followed

by small entities. The general principal states that the accounting is to be done

on the accrual method of transaction, where the actual transaction is more

important than the cash possession of the transaction. The accounts are to be

dealt at the transaction date irrespective of the cash received of payments.

2. As per the ATO's requirements, all the transactions or the information are to be

reported to the Australian taxation office are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

BUDGET

Cash book

Invoices.

Assets for CGT purpose

Financial statements

Others

3. Financial record keeping:

The financial record keeping means the preparation and presentation of the financial

transactions, the financial transaction is to be documented in the prescribed sequenced

orders rather it can be said the financial documents are the representations of the

transaction of the business, individual and others (Smith et al. 2015). The financial

documents are to be recorded in accordance with the accounting principal and

accounting standards. Further, the type of the business will vary the presentation of

the financial documents. In addition to that, the financial, the recording will be based

on the nature and activities of the business.

Financial Auditing:

The auditing is processes that describe and comment on the viability of the

financial statements whether they are true or not. The true effect will

commence when the accounts are prepared based on appropriate AAS. In

addition to that, the auditing process will be conducted based on auditing

standards. The auditing is required to determine the accuracy of the accounting

and the discloser requirement for the preparation of the financial stamens are

adequate or not (Rubin 2016).

Budgeting technical:

Budgeting is the process that created a pre-plan for the collection and spending

of money. The collection plan and sending plan is regarded as budgets.

BUDGET

Cash book

Invoices.

Assets for CGT purpose

Financial statements

Others

3. Financial record keeping:

The financial record keeping means the preparation and presentation of the financial

transactions, the financial transaction is to be documented in the prescribed sequenced

orders rather it can be said the financial documents are the representations of the

transaction of the business, individual and others (Smith et al. 2015). The financial

documents are to be recorded in accordance with the accounting principal and

accounting standards. Further, the type of the business will vary the presentation of

the financial documents. In addition to that, the financial, the recording will be based

on the nature and activities of the business.

Financial Auditing:

The auditing is processes that describe and comment on the viability of the

financial statements whether they are true or not. The true effect will

commence when the accounts are prepared based on appropriate AAS. In

addition to that, the auditing process will be conducted based on auditing

standards. The auditing is required to determine the accuracy of the accounting

and the discloser requirement for the preparation of the financial stamens are

adequate or not (Rubin 2016).

Budgeting technical:

Budgeting is the process that created a pre-plan for the collection and spending

of money. The collection plan and sending plan is regarded as budgets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

BUDGET

Concisely it can be said budgeting is the process where the management

predetermines the process all collection of the funds from various sources like

making sales of goods or service or getting cash inflows from other sources.

Moreover, the budget empowers more important for its spending. As the

income is not relatively assessable but a proper expenditure, planning can be

developed based on the knowledge (Kireeva 2016). There are many types of

budgets like sales budges, purchase budgets and others. There is another type

of budget that is called "Master Budget” that refers to the collection of the

funds and making the expenditure. This envelopes the proper costing and cash

reformation structure of an entity.

For a successful budgeting, the following points are to be considered:

Understand the organizational needs

Assess the markets

Get the information related to the budget from reliable sources.

Redefine the sources that are contributory and adequate or not.

Define the costs

Section C:

Performance Activity:

Introduction: In the contents of the report, the various observation of the accounting

techniques and the information of the business activities are identified. The reliable assertion

and modification of the budgets are made with the assertions of the regulation. In addition to

that, a contingency plan is developed for the modification and the budget (Réka et al. 2014).

Observation:

BUDGET

Concisely it can be said budgeting is the process where the management

predetermines the process all collection of the funds from various sources like

making sales of goods or service or getting cash inflows from other sources.

Moreover, the budget empowers more important for its spending. As the

income is not relatively assessable but a proper expenditure, planning can be

developed based on the knowledge (Kireeva 2016). There are many types of

budgets like sales budges, purchase budgets and others. There is another type

of budget that is called "Master Budget” that refers to the collection of the

funds and making the expenditure. This envelopes the proper costing and cash

reformation structure of an entity.

For a successful budgeting, the following points are to be considered:

Understand the organizational needs

Assess the markets

Get the information related to the budget from reliable sources.

Redefine the sources that are contributory and adequate or not.

Define the costs

Section C:

Performance Activity:

Introduction: In the contents of the report, the various observation of the accounting

techniques and the information of the business activities are identified. The reliable assertion

and modification of the budgets are made with the assertions of the regulation. In addition to

that, a contingency plan is developed for the modification and the budget (Réka et al. 2014).

Observation:

8

BUDGET

In the practical observation, it is ascertained that a large portion of the perishable

products are wasted daily and the company has nor regulated any provisions for that. Further,

in the proposed budget the fuel costs are not adequate it is approximately 15% higher because

of the increased price (Suomalainen et al. 2015). Another observation located in the study of

the accounts is that the sales for the last quarter will be affected due to the current market

slow down. Instead of the above, the company has to arrange for the preparation o and

presentation of the record as per the instruction of the ATO. Further, it is observed that there

are some flaws in the accounting of the inventory and stocktaking. The cost of administrative

and security are lower.

Solution:

For the above-identified problems that company has to make suitable arrangement for

the redrafting, the budges as they are some significant and important required changes are to

be dealt. Further for the reporting propose to the Australia Taxation Office (Kireeva 2016). A

contingency plan is drafted for the changes in ten marketing behaviour and the increase i9n

the cost as this will affect the profitability of the YOU FOOD. The contingency plan will

consist the technic to increase the sales in the slowdown in the Q 2 and Q 3.

Implementation:

The above-stated plans are implemented in the commencement of the quarter 2. For

the slowdown in the quarter 2 and quarter 3, the company initiated provisional discounts

options and promoted the business offerings. In addition to that, a major portion of the of the

advertisement cost is allocated for this slow down period to boost the sales.

Monitoring:

BUDGET

In the practical observation, it is ascertained that a large portion of the perishable

products are wasted daily and the company has nor regulated any provisions for that. Further,

in the proposed budget the fuel costs are not adequate it is approximately 15% higher because

of the increased price (Suomalainen et al. 2015). Another observation located in the study of

the accounts is that the sales for the last quarter will be affected due to the current market

slow down. Instead of the above, the company has to arrange for the preparation o and

presentation of the record as per the instruction of the ATO. Further, it is observed that there

are some flaws in the accounting of the inventory and stocktaking. The cost of administrative

and security are lower.

Solution:

For the above-identified problems that company has to make suitable arrangement for

the redrafting, the budges as they are some significant and important required changes are to

be dealt. Further for the reporting propose to the Australia Taxation Office (Kireeva 2016). A

contingency plan is drafted for the changes in ten marketing behaviour and the increase i9n

the cost as this will affect the profitability of the YOU FOOD. The contingency plan will

consist the technic to increase the sales in the slowdown in the Q 2 and Q 3.

Implementation:

The above-stated plans are implemented in the commencement of the quarter 2. For

the slowdown in the quarter 2 and quarter 3, the company initiated provisional discounts

options and promoted the business offerings. In addition to that, a major portion of the of the

advertisement cost is allocated for this slow down period to boost the sales.

Monitoring:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

BUDGET

Next step after the implication is monitoring and controlling the business activities

that are implemented so that the contingency plan works well. The monitoring is required for

controlling the changes in the performance.

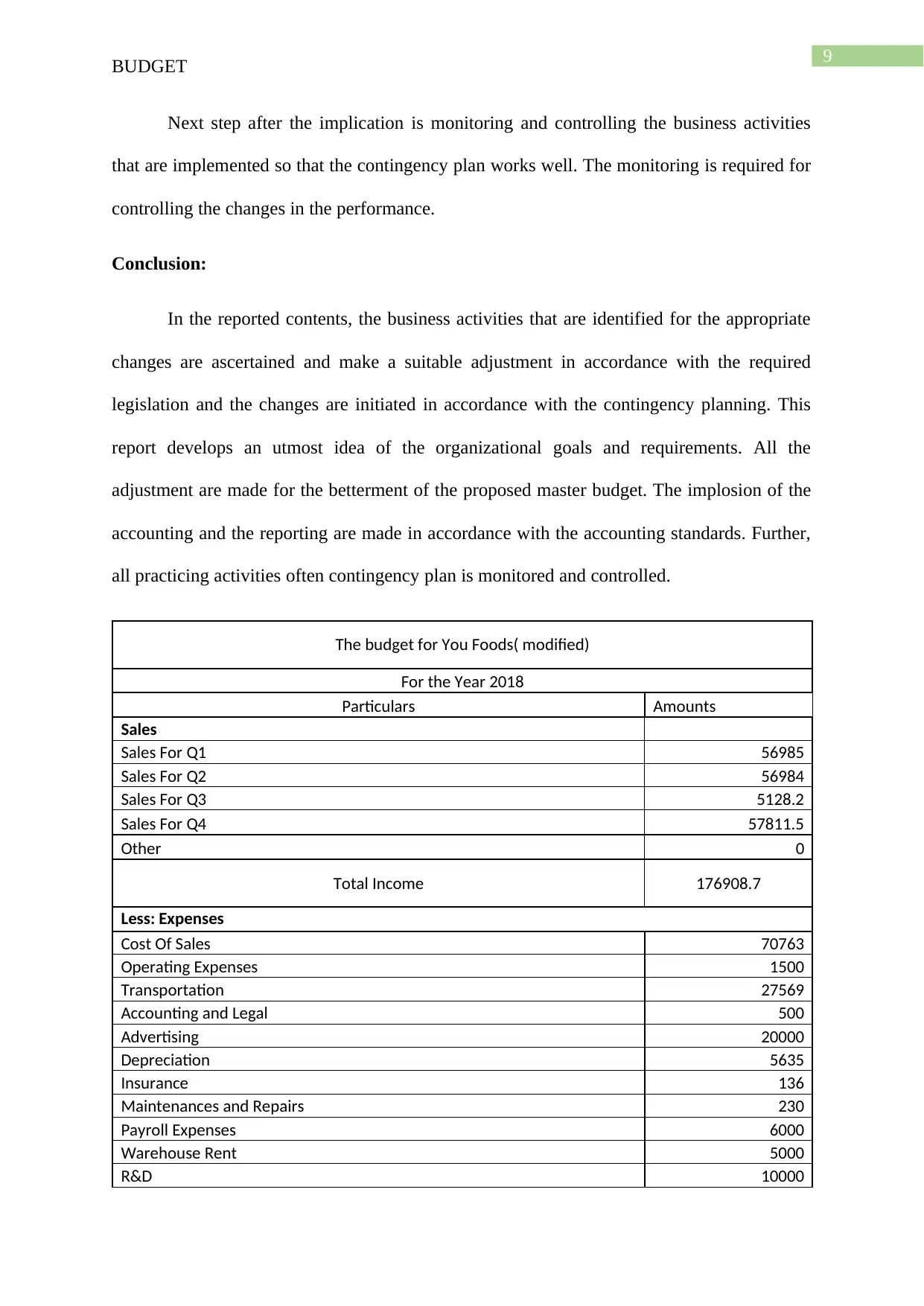

Conclusion:

In the reported contents, the business activities that are identified for the appropriate

changes are ascertained and make a suitable adjustment in accordance with the required

legislation and the changes are initiated in accordance with the contingency planning. This

report develops an utmost idea of the organizational goals and requirements. All the

adjustment are made for the betterment of the proposed master budget. The implosion of the

accounting and the reporting are made in accordance with the accounting standards. Further,

all practicing activities often contingency plan is monitored and controlled.

The budget for You Foods( modified)

For the Year 2018

Particulars Amounts

Sales

Sales For Q1 56985

Sales For Q2 56984

Sales For Q3 5128.2

Sales For Q4 57811.5

Other 0

Total Income 176908.7

Less: Expenses

Cost Of Sales 70763

Operating Expenses 1500

Transportation 27569

Accounting and Legal 500

Advertising 20000

Depreciation 5635

Insurance 136

Maintenances and Repairs 230

Payroll Expenses 6000

Warehouse Rent 5000

R&D 10000

BUDGET

Next step after the implication is monitoring and controlling the business activities

that are implemented so that the contingency plan works well. The monitoring is required for

controlling the changes in the performance.

Conclusion:

In the reported contents, the business activities that are identified for the appropriate

changes are ascertained and make a suitable adjustment in accordance with the required

legislation and the changes are initiated in accordance with the contingency planning. This

report develops an utmost idea of the organizational goals and requirements. All the

adjustment are made for the betterment of the proposed master budget. The implosion of the

accounting and the reporting are made in accordance with the accounting standards. Further,

all practicing activities often contingency plan is monitored and controlled.

The budget for You Foods( modified)

For the Year 2018

Particulars Amounts

Sales

Sales For Q1 56985

Sales For Q2 56984

Sales For Q3 5128.2

Sales For Q4 57811.5

Other 0

Total Income 176908.7

Less: Expenses

Cost Of Sales 70763

Operating Expenses 1500

Transportation 27569

Accounting and Legal 500

Advertising 20000

Depreciation 5635

Insurance 136

Maintenances and Repairs 230

Payroll Expenses 6000

Warehouse Rent 5000

R&D 10000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

BUDGET

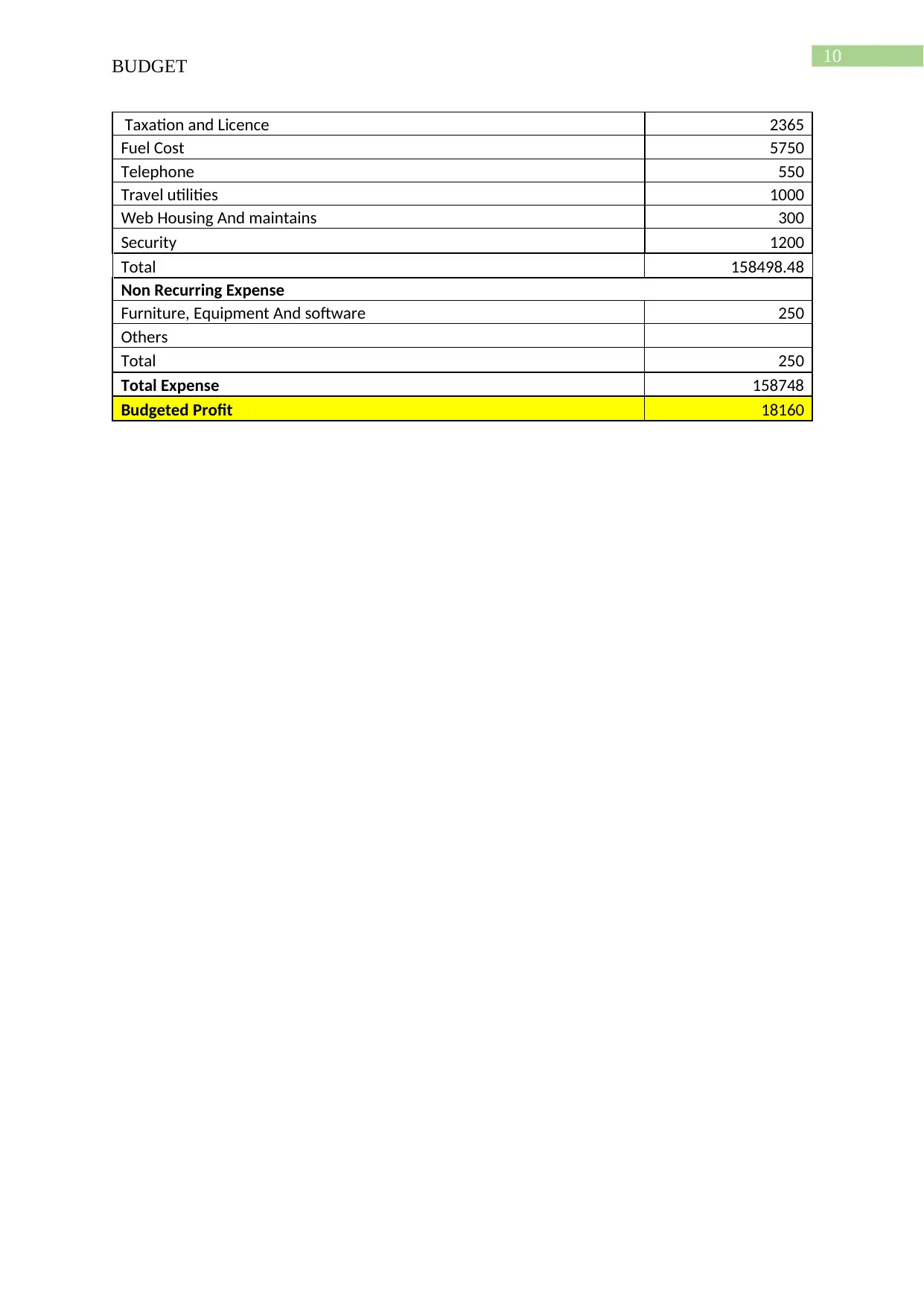

Taxation and Licence 2365

Fuel Cost 5750

Telephone 550

Travel utilities 1000

Web Housing And maintains 300

Security 1200

Total 158498.48

Non Recurring Expense

Furniture, Equipment And software 250

Others

Total 250

Total Expense 158748

Budgeted Profit 18160

BUDGET

Taxation and Licence 2365

Fuel Cost 5750

Telephone 550

Travel utilities 1000

Web Housing And maintains 300

Security 1200

Total 158498.48

Non Recurring Expense

Furniture, Equipment And software 250

Others

Total 250

Total Expense 158748

Budgeted Profit 18160

11

BUDGET

Reference

Alviniussen, A. and Jankensgard, H., 2015. Enterprise risk budgeting: bringing risk

management into the financial planning process.

Barr, M.J. and McClellan, G.S., 2018. Budgets and financial management in higher

education. John Wiley & Sons.

Crutzen, N., Zvezdov, D. and Schaltegger, S., 2017. Sustainability and management control.

Exploring and theorizing control patterns in large European firms. Journal of cleaner

production, 143, pp.1291-1301.

Drever, A.I., Odders‐White, E., Kalish, C.W., Else‐Quest, N.M., Hoagland, E.M. and Nelms,

E.N., 2015. Foundations of financial well‐being: Insights into the role of executive function,

financial socialization, and experience‐based learning in childhood and youth. Journal of

Consumer Affairs, 49(1), pp.13-38.

Kireeva, E.V., 2016. Effective management of personal finance. Современные тенденции

развития науки и технологий, (5-7), pp.5-7.

Maskell, B.H., Baggaley, B. and Grasso, L., 2016. Practical lean accounting: a proven

system for measuring and managing the lean enterprise. Productivity Press.

Miller, G., 2018. Performance based budgeting. Routledge.

Réka, C.I., Ştefan, P. and Daniel, C.V., 2014. TRADITIONAL BUDGETING VERSUS

BEYOND BUDGETING: A LITERATURE REVIEW. Annals of the University of Oradea,

Economic Science Series, 23(1).

Rogulenko, T., Ponomareva, S., Bodiaco, A., Mironenko, V. and Zelenov, V., 2016.

Budgeting-Based Organization of Internal Control. International Journal of Environmental

and Science Education, 11(11), pp.4104-4117.

BUDGET

Reference

Alviniussen, A. and Jankensgard, H., 2015. Enterprise risk budgeting: bringing risk

management into the financial planning process.

Barr, M.J. and McClellan, G.S., 2018. Budgets and financial management in higher

education. John Wiley & Sons.

Crutzen, N., Zvezdov, D. and Schaltegger, S., 2017. Sustainability and management control.

Exploring and theorizing control patterns in large European firms. Journal of cleaner

production, 143, pp.1291-1301.

Drever, A.I., Odders‐White, E., Kalish, C.W., Else‐Quest, N.M., Hoagland, E.M. and Nelms,

E.N., 2015. Foundations of financial well‐being: Insights into the role of executive function,

financial socialization, and experience‐based learning in childhood and youth. Journal of

Consumer Affairs, 49(1), pp.13-38.

Kireeva, E.V., 2016. Effective management of personal finance. Современные тенденции

развития науки и технологий, (5-7), pp.5-7.

Maskell, B.H., Baggaley, B. and Grasso, L., 2016. Practical lean accounting: a proven

system for measuring and managing the lean enterprise. Productivity Press.

Miller, G., 2018. Performance based budgeting. Routledge.

Réka, C.I., Ştefan, P. and Daniel, C.V., 2014. TRADITIONAL BUDGETING VERSUS

BEYOND BUDGETING: A LITERATURE REVIEW. Annals of the University of Oradea,

Economic Science Series, 23(1).

Rogulenko, T., Ponomareva, S., Bodiaco, A., Mironenko, V. and Zelenov, V., 2016.

Budgeting-Based Organization of Internal Control. International Journal of Environmental

and Science Education, 11(11), pp.4104-4117.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.