UTS Business School Finance 25721: Investment Management Assignment

VerifiedAdded on 2022/10/19

|5

|1059

|207

Homework Assignment

AI Summary

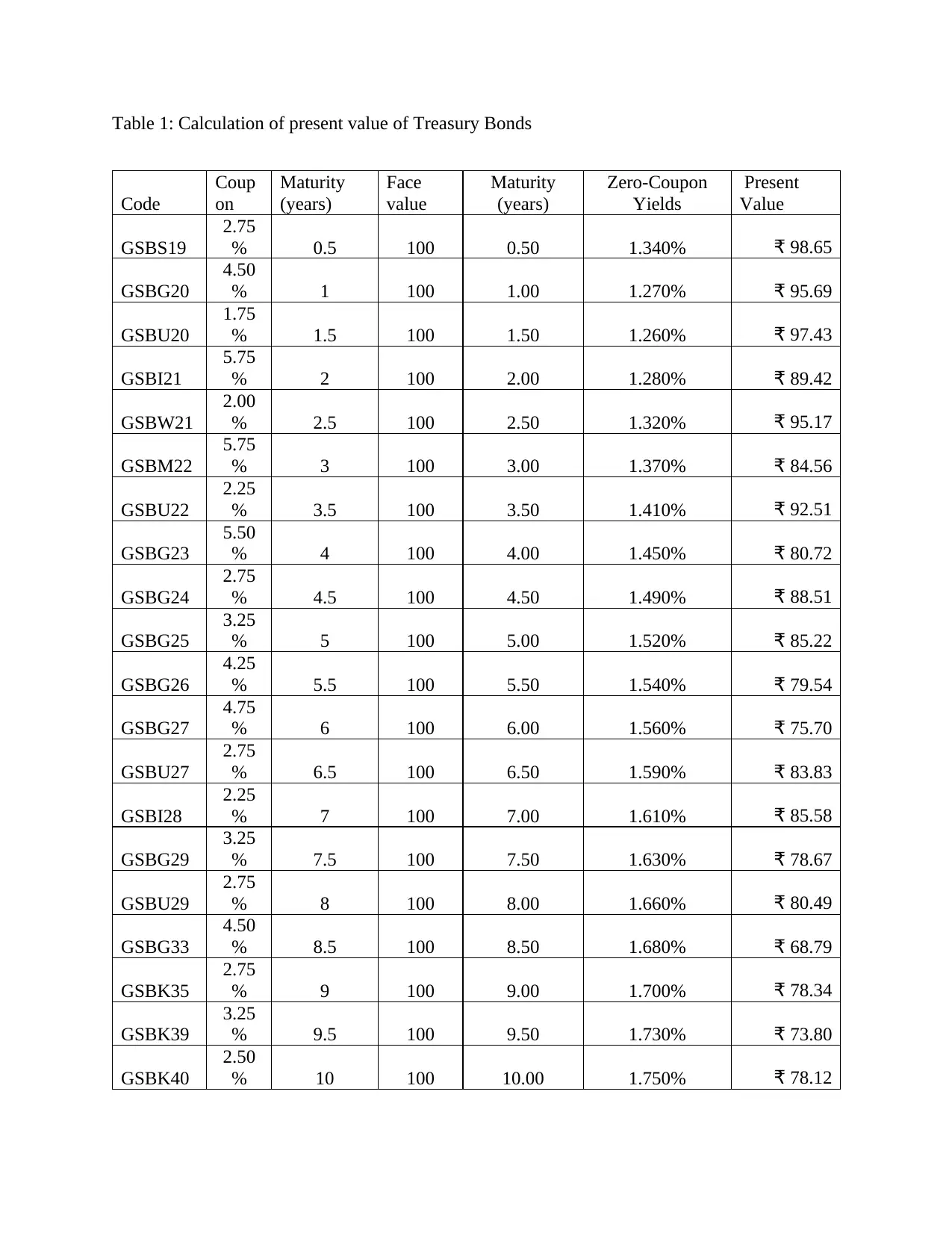

This assignment solution delves into the intricacies of zero coupon bonds, explaining their characteristics, valuation methods, and yield calculations. It begins by defining zero coupon bonds as debt securities that do not pay periodic interest, instead offering returns through the difference between the purchase price and the face value at maturity. The solution provides a numerical example to illustrate the calculation of a bond's present value, considering factors like maturity, yield, and face value. The assignment further explores the relationship between bond prices and yields, highlighting the inverse relationship. A table presents the present value calculations for various Treasury bonds with different coupon rates and maturities. The document also references relevant academic literature to support the analysis. This assignment is designed to help students understand the concepts of zero coupon bonds in investment management.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.