Auditing Project: Financial Statement Analysis of Zicom Group Limited

VerifiedAdded on 2020/12/09

|16

|3858

|54

Report

AI Summary

This auditing project report provides a comprehensive analysis of Zicom Group Limited's financial statements. It begins with an introduction to audit programs and procedures, including risk assessment and materiality. The report then delves into business risks, including inherent, control, and detection risks, as well as the audit risk model. Analytical procedures are performed using financial ratios, including profitability, liquidity, and gearing ratios, to assess the company's financial performance over a three-year period. The concept of materiality and its impact on audit sampling are discussed, followed by a listing of material account balances and relevant financial report assertions. The project explores financial statements, business risks, financial ratios, and audit procedures. The report also includes recommendations for improving financial performance. This report is a great resource for students looking to understand auditing and financial statement analysis. Desklib provides past papers and solved assignments.

AUDITING PROJECT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................1

TASK 3............................................................................................................................................2

TASK 4............................................................................................................................................6

TASK 5............................................................................................................................................7

TASK 6............................................................................................................................................7

TASK 7 ..........................................................................................................................................9

TASK 8..........................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERECNES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................1

TASK 3............................................................................................................................................2

TASK 4............................................................................................................................................6

TASK 5............................................................................................................................................7

TASK 6............................................................................................................................................7

TASK 7 ..........................................................................................................................................9

TASK 8..........................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERECNES..............................................................................................................................14

INTRODUCTION

An audit program means a plan of audit that is documented and according to which

procedures of the auditor depends. Before starting audit procedure an auditor will make a audit

program on the basis of previous year(s) working papers, size of entity, materiality of risk

associated with the relevant industry and accordingly decide the audit duration, number of audit

staff and audit procedures that have to be followed while doing audit. Audit procedures are

depends upon the inherent risk, detection risk and control risk and accordingly materiality and

sampling are done. Analysis of financial statements is done with the help of profit and loss

account, balance sheet and ratio analysis and conclusion is framed about the financial position of

the company. Generally audit procedures are based upon materiality of transactions and

sampling is done according to audit risks.

TASK 1

In this project, Zicom Group Limited which is dealing in leading specialist equipment

manufacturing and niche engineering service proving with core expertise. In this project, we

discuss about various risk, material account balances and sampling procedures applied by the

auditor while performing its audit procedures.

TASK 2

Business risk refers to the possibility that an organisation will have lower profits than

anticipated profits or experience a loss rather than taking a profits. There are various factors

which are associated with it such as : volume of sale, per unit price, competition, input cost and

legal compliances. Zicom Group Ltd is a leading manufacturer of marine deck machinery, fluid

regulating and material stations, precision engineered & automation equipment etc. It belongs to

the manufacturing industry(Bodnar and Hopwood., 2012). There are various types of business

risks which are described as below :

Risk of material misstatement : Material misstatement risk can be arise due to the

errors in financial statements of a company. It can be occurs due to difference between the

reported figures and what is anticipated to be reported in order for the financial statements to be

fairly presented.

1

An audit program means a plan of audit that is documented and according to which

procedures of the auditor depends. Before starting audit procedure an auditor will make a audit

program on the basis of previous year(s) working papers, size of entity, materiality of risk

associated with the relevant industry and accordingly decide the audit duration, number of audit

staff and audit procedures that have to be followed while doing audit. Audit procedures are

depends upon the inherent risk, detection risk and control risk and accordingly materiality and

sampling are done. Analysis of financial statements is done with the help of profit and loss

account, balance sheet and ratio analysis and conclusion is framed about the financial position of

the company. Generally audit procedures are based upon materiality of transactions and

sampling is done according to audit risks.

TASK 1

In this project, Zicom Group Limited which is dealing in leading specialist equipment

manufacturing and niche engineering service proving with core expertise. In this project, we

discuss about various risk, material account balances and sampling procedures applied by the

auditor while performing its audit procedures.

TASK 2

Business risk refers to the possibility that an organisation will have lower profits than

anticipated profits or experience a loss rather than taking a profits. There are various factors

which are associated with it such as : volume of sale, per unit price, competition, input cost and

legal compliances. Zicom Group Ltd is a leading manufacturer of marine deck machinery, fluid

regulating and material stations, precision engineered & automation equipment etc. It belongs to

the manufacturing industry(Bodnar and Hopwood., 2012). There are various types of business

risks which are described as below :

Risk of material misstatement : Material misstatement risk can be arise due to the

errors in financial statements of a company. It can be occurs due to difference between the

reported figures and what is anticipated to be reported in order for the financial statements to be

fairly presented.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit risk : Audit risk arises when auditor of an organisation express inappropriate audit

option on financial statements that contain material misstatement. Auditor of Zicom Group Ltd

properly follow audit procedure so this risk does not much high in the organisation.

Formula of Audit risk model : AR = ƒ[IR * CR * DR]

Inherent risk : In financial auditing inherent risk arises, especially while dealing with

complex transactions. This risk can be posed by an omission in a financial statement due to a risk

factor other than failure of control. In Zicom Group Ltd this risk is low because auditors of

organisation prepare its financial statements effectively which minimize the chances of errors in

financial transactions.

Control risk : Control risk refers to that risk of inefficiency of organisation controls to

analyse material misstatements in financial statements of company. Management and auditors of

Zicom Group Ltd able to identify and control risk in material misstatements so this risk is low in

organisation.

Detection risk : Detection risk is that risk which is arises when auditors fails to detect a

material misstatements in the financial statements. Auditors of Zicom Group Ltd always try to

follow audit procedures so that material misstatements can be deducted in financial statements.

So this risk does not much affect the assessment.

TASK 3

Analytical procedures using ratios:

Analytical procedures are one of many financial audit processes which help an auditor

understand the client's business and changes in the business, and to identify potential risk areas to

plan other audit procedures.

Income Statements of Zicom Group Ltd for the year ended 30.06.2017 and 30.06.2018

(AU $ in million)

2015-16 2016-17 2017-18

Revenue 111 85 76

Cost of revenue 68 43 40

Gross Profit 43 42 36

2

option on financial statements that contain material misstatement. Auditor of Zicom Group Ltd

properly follow audit procedure so this risk does not much high in the organisation.

Formula of Audit risk model : AR = ƒ[IR * CR * DR]

Inherent risk : In financial auditing inherent risk arises, especially while dealing with

complex transactions. This risk can be posed by an omission in a financial statement due to a risk

factor other than failure of control. In Zicom Group Ltd this risk is low because auditors of

organisation prepare its financial statements effectively which minimize the chances of errors in

financial transactions.

Control risk : Control risk refers to that risk of inefficiency of organisation controls to

analyse material misstatements in financial statements of company. Management and auditors of

Zicom Group Ltd able to identify and control risk in material misstatements so this risk is low in

organisation.

Detection risk : Detection risk is that risk which is arises when auditors fails to detect a

material misstatements in the financial statements. Auditors of Zicom Group Ltd always try to

follow audit procedures so that material misstatements can be deducted in financial statements.

So this risk does not much affect the assessment.

TASK 3

Analytical procedures using ratios:

Analytical procedures are one of many financial audit processes which help an auditor

understand the client's business and changes in the business, and to identify potential risk areas to

plan other audit procedures.

Income Statements of Zicom Group Ltd for the year ended 30.06.2017 and 30.06.2018

(AU $ in million)

2015-16 2016-17 2017-18

Revenue 111 85 76

Cost of revenue 68 43 40

Gross Profit 43 42 36

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

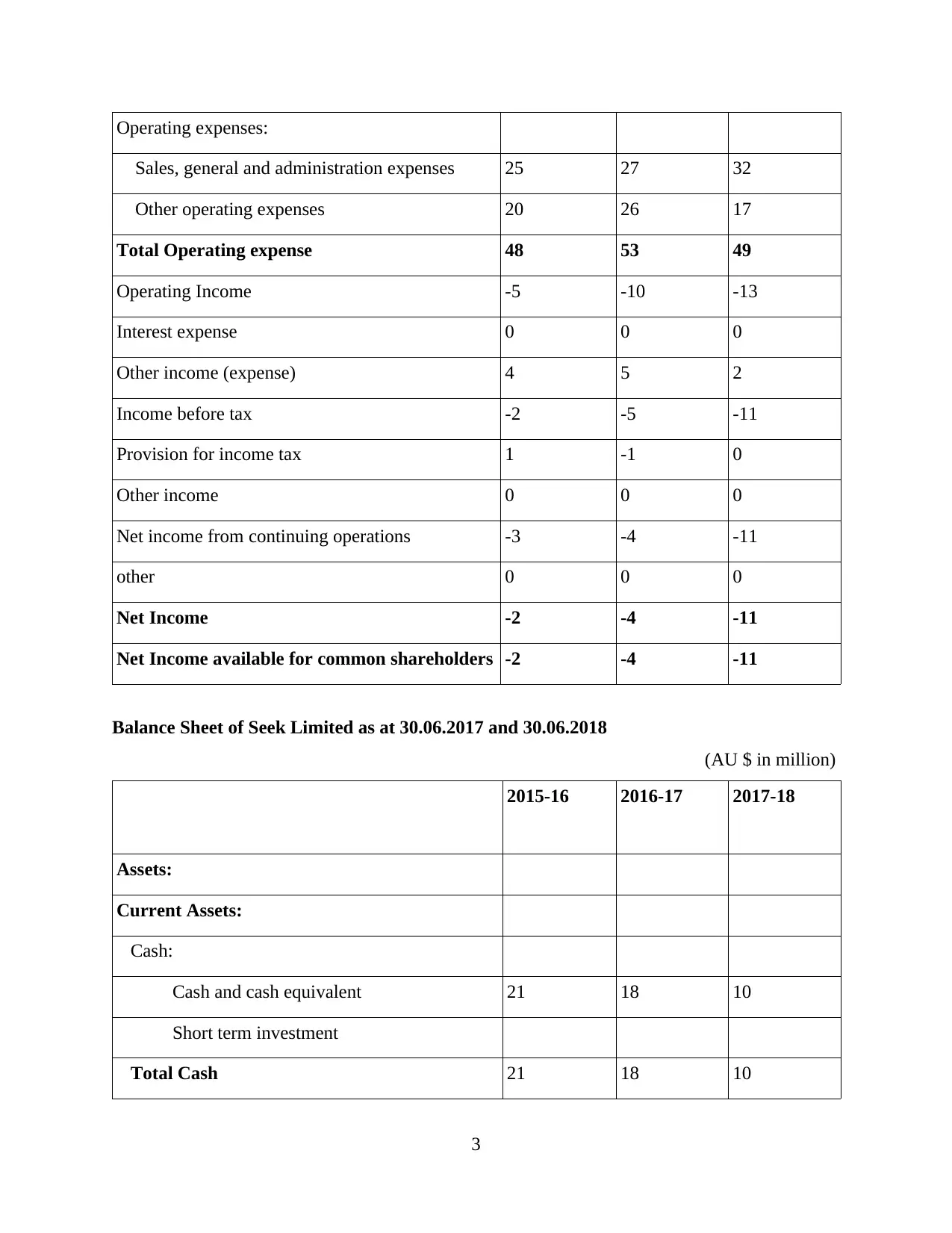

Operating expenses:

Sales, general and administration expenses 25 27 32

Other operating expenses 20 26 17

Total Operating expense 48 53 49

Operating Income -5 -10 -13

Interest expense 0 0 0

Other income (expense) 4 5 2

Income before tax -2 -5 -11

Provision for income tax 1 -1 0

Other income 0 0 0

Net income from continuing operations -3 -4 -11

other 0 0 0

Net Income -2 -4 -11

Net Income available for common shareholders -2 -4 -11

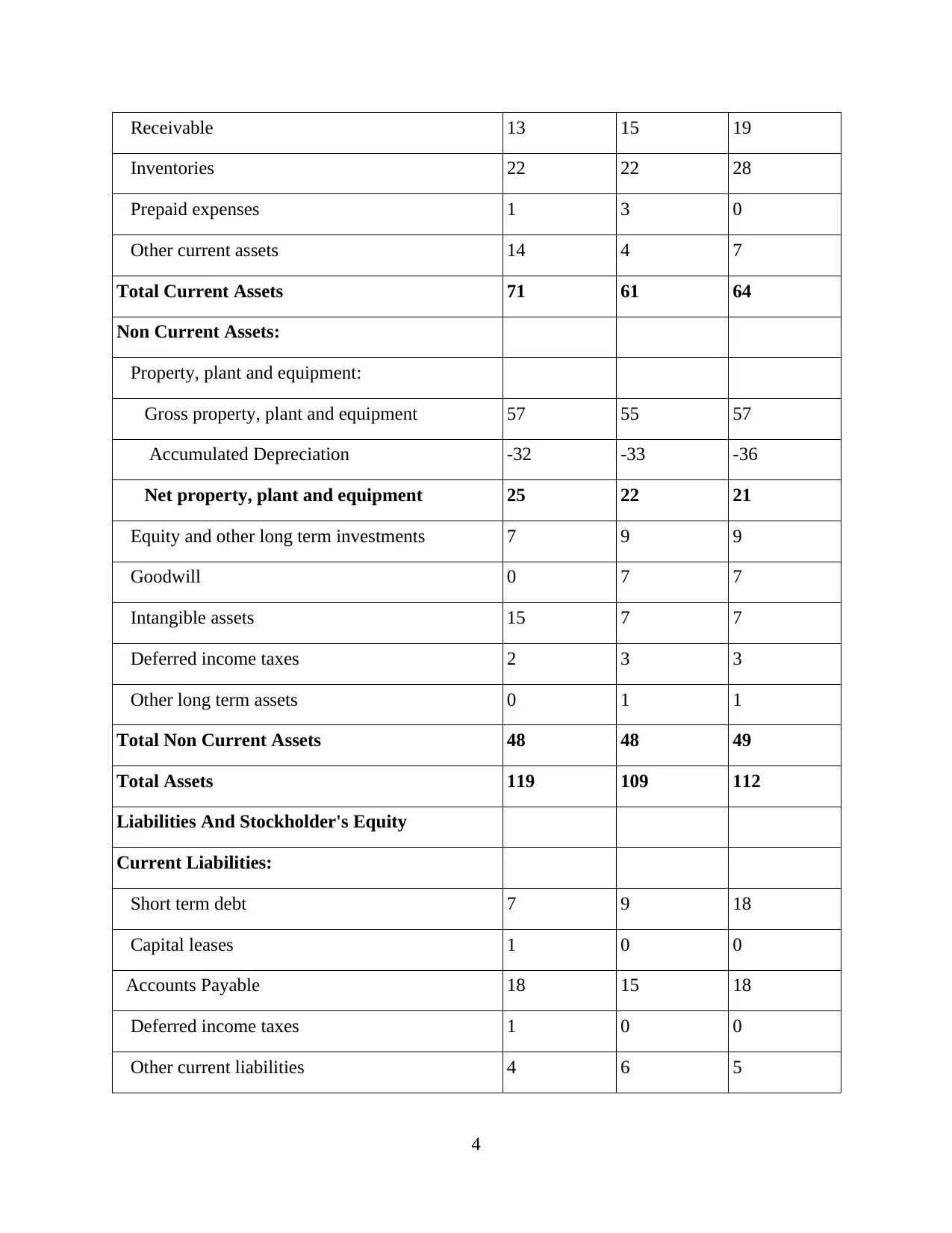

Balance Sheet of Seek Limited as at 30.06.2017 and 30.06.2018

(AU $ in million)

2015-16 2016-17 2017-18

Assets:

Current Assets:

Cash:

Cash and cash equivalent 21 18 10

Short term investment

Total Cash 21 18 10

3

Sales, general and administration expenses 25 27 32

Other operating expenses 20 26 17

Total Operating expense 48 53 49

Operating Income -5 -10 -13

Interest expense 0 0 0

Other income (expense) 4 5 2

Income before tax -2 -5 -11

Provision for income tax 1 -1 0

Other income 0 0 0

Net income from continuing operations -3 -4 -11

other 0 0 0

Net Income -2 -4 -11

Net Income available for common shareholders -2 -4 -11

Balance Sheet of Seek Limited as at 30.06.2017 and 30.06.2018

(AU $ in million)

2015-16 2016-17 2017-18

Assets:

Current Assets:

Cash:

Cash and cash equivalent 21 18 10

Short term investment

Total Cash 21 18 10

3

Receivable 13 15 19

Inventories 22 22 28

Prepaid expenses 1 3 0

Other current assets 14 4 7

Total Current Assets 71 61 64

Non Current Assets:

Property, plant and equipment:

Gross property, plant and equipment 57 55 57

Accumulated Depreciation -32 -33 -36

Net property, plant and equipment 25 22 21

Equity and other long term investments 7 9 9

Goodwill 0 7 7

Intangible assets 15 7 7

Deferred income taxes 2 3 3

Other long term assets 0 1 1

Total Non Current Assets 48 48 49

Total Assets 119 109 112

Liabilities And Stockholder's Equity

Current Liabilities:

Short term debt 7 9 18

Capital leases 1 0 0

Accounts Payable 18 15 18

Deferred income taxes 1 0 0

Other current liabilities 4 6 5

4

Inventories 22 22 28

Prepaid expenses 1 3 0

Other current assets 14 4 7

Total Current Assets 71 61 64

Non Current Assets:

Property, plant and equipment:

Gross property, plant and equipment 57 55 57

Accumulated Depreciation -32 -33 -36

Net property, plant and equipment 25 22 21

Equity and other long term investments 7 9 9

Goodwill 0 7 7

Intangible assets 15 7 7

Deferred income taxes 2 3 3

Other long term assets 0 1 1

Total Non Current Assets 48 48 49

Total Assets 119 109 112

Liabilities And Stockholder's Equity

Current Liabilities:

Short term debt 7 9 18

Capital leases 1 0 0

Accounts Payable 18 15 18

Deferred income taxes 1 0 0

Other current liabilities 4 6 5

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Current Liabilities 30 31 41

Non Current Liabilities:

Long term debt 2 1 1

Deferred tax liabilities 2 1 1

Total Non Current Liabilities 5 2 2

Total Liabilities 35 33 43

Stockholder's Equity:

Common stock 38 36 38

Other equity 0 0 -2

Retained earning 49 41 32

Accumulated other comprehensive income -3 -2 0

Total Stockholder's Equity 85 76 69

Total Liabilities And Stockholder's Equity 119 109 112

For doing analytical procedures of above financial statements of Zicom Group Ltd, it is

necessary to calculate and analyse various ratios like profitability ratios, investment ratios and

liquidity ratios, which are as follows:

Profitability Ratio:

Particulars 2015-16 2016-17 2017-18

Gross Profit ratio (%) 38.84 49.55 47.54

Operating profit ratio

(%)

-4.49 -12.14 -17.57

Net Profit ratio (%) -1.53 -6.37 -14.92

Note: Gross profit ratio = Gross profit/sales*100

Net profit ratio = Net profit/sales*100

5

Non Current Liabilities:

Long term debt 2 1 1

Deferred tax liabilities 2 1 1

Total Non Current Liabilities 5 2 2

Total Liabilities 35 33 43

Stockholder's Equity:

Common stock 38 36 38

Other equity 0 0 -2

Retained earning 49 41 32

Accumulated other comprehensive income -3 -2 0

Total Stockholder's Equity 85 76 69

Total Liabilities And Stockholder's Equity 119 109 112

For doing analytical procedures of above financial statements of Zicom Group Ltd, it is

necessary to calculate and analyse various ratios like profitability ratios, investment ratios and

liquidity ratios, which are as follows:

Profitability Ratio:

Particulars 2015-16 2016-17 2017-18

Gross Profit ratio (%) 38.84 49.55 47.54

Operating profit ratio

(%)

-4.49 -12.14 -17.57

Net Profit ratio (%) -1.53 -6.37 -14.92

Note: Gross profit ratio = Gross profit/sales*100

Net profit ratio = Net profit/sales*100

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

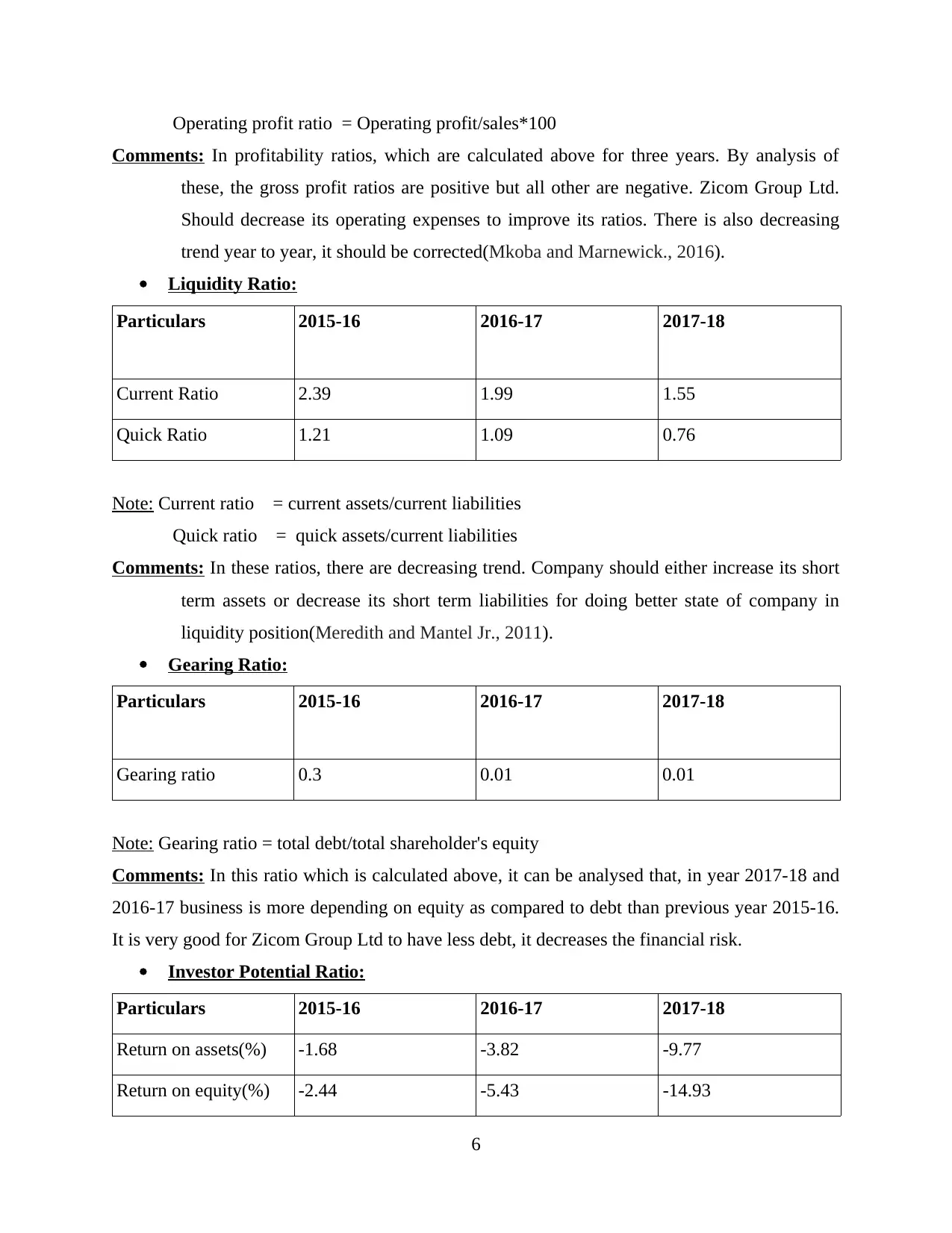

Operating profit ratio = Operating profit/sales*100

Comments: In profitability ratios, which are calculated above for three years. By analysis of

these, the gross profit ratios are positive but all other are negative. Zicom Group Ltd.

Should decrease its operating expenses to improve its ratios. There is also decreasing

trend year to year, it should be corrected(Mkoba and Marnewick., 2016).

Liquidity Ratio:

Particulars 2015-16 2016-17 2017-18

Current Ratio 2.39 1.99 1.55

Quick Ratio 1.21 1.09 0.76

Note: Current ratio = current assets/current liabilities

Quick ratio = quick assets/current liabilities

Comments: In these ratios, there are decreasing trend. Company should either increase its short

term assets or decrease its short term liabilities for doing better state of company in

liquidity position(Meredith and Mantel Jr., 2011).

Gearing Ratio:

Particulars 2015-16 2016-17 2017-18

Gearing ratio 0.3 0.01 0.01

Note: Gearing ratio = total debt/total shareholder's equity

Comments: In this ratio which is calculated above, it can be analysed that, in year 2017-18 and

2016-17 business is more depending on equity as compared to debt than previous year 2015-16.

It is very good for Zicom Group Ltd to have less debt, it decreases the financial risk.

Investor Potential Ratio:

Particulars 2015-16 2016-17 2017-18

Return on assets(%) -1.68 -3.82 -9.77

Return on equity(%) -2.44 -5.43 -14.93

6

Comments: In profitability ratios, which are calculated above for three years. By analysis of

these, the gross profit ratios are positive but all other are negative. Zicom Group Ltd.

Should decrease its operating expenses to improve its ratios. There is also decreasing

trend year to year, it should be corrected(Mkoba and Marnewick., 2016).

Liquidity Ratio:

Particulars 2015-16 2016-17 2017-18

Current Ratio 2.39 1.99 1.55

Quick Ratio 1.21 1.09 0.76

Note: Current ratio = current assets/current liabilities

Quick ratio = quick assets/current liabilities

Comments: In these ratios, there are decreasing trend. Company should either increase its short

term assets or decrease its short term liabilities for doing better state of company in

liquidity position(Meredith and Mantel Jr., 2011).

Gearing Ratio:

Particulars 2015-16 2016-17 2017-18

Gearing ratio 0.3 0.01 0.01

Note: Gearing ratio = total debt/total shareholder's equity

Comments: In this ratio which is calculated above, it can be analysed that, in year 2017-18 and

2016-17 business is more depending on equity as compared to debt than previous year 2015-16.

It is very good for Zicom Group Ltd to have less debt, it decreases the financial risk.

Investor Potential Ratio:

Particulars 2015-16 2016-17 2017-18

Return on assets(%) -1.68 -3.82 -9.77

Return on equity(%) -2.44 -5.43 -14.93

6

Note: Return on assets = Net profit/Total assets

Return on equity = Profit after tax/Net worth

Comments: In these ratio after calculating three year ratios as shown above, it can be easily

analysed that return is less in current year than year 2017-18 in both ratios as compared to

previous years. This mean, Zicom Group Ltd is not using assets & funds effectively and

efficiently which is invested by shareholders in the company. It can demotivate the investors to

not investing in this company due to low rate of return. Company should take corrective major

to enhance the income so that new investors can come and invest fund.

TASK 4

Materiality means those assets and liabilities whose increase or decrease can impact the

decision regarding financial statements for the users of financial statements and accordingly the

audit sample is made. In material, account balance refers to the size of recorded account balance

in the financial statement and it focuses towards physical aspects of things. Materiality refers to

the errors contained in balances and transactions while preparing the financial statements of

organisation. It is helpful for the planning purpose. For example , If auditor of Zicom Group Ltd

has shown wrongly $1000 as fixed assets where it has to be shown as current liability because it

amount of interest payable. So it is important for an auditor to find the errors while preparing the

financial statements as a result planning can be done effectively. If organisation has planned to

expand its business in different market and it is possible when financial statements provides

relevant information such as profits available in current year for company. For expansion, money

is needed and if corporation has sufficient profits as per the information available in financial

statement than it can plan for business expansion(Feng and Hudson., 2011). So it is helpful in

planning as well as decision making as a result management of company can take important

decision regarding expansion of its business (Turner., 2016).

TASK 5

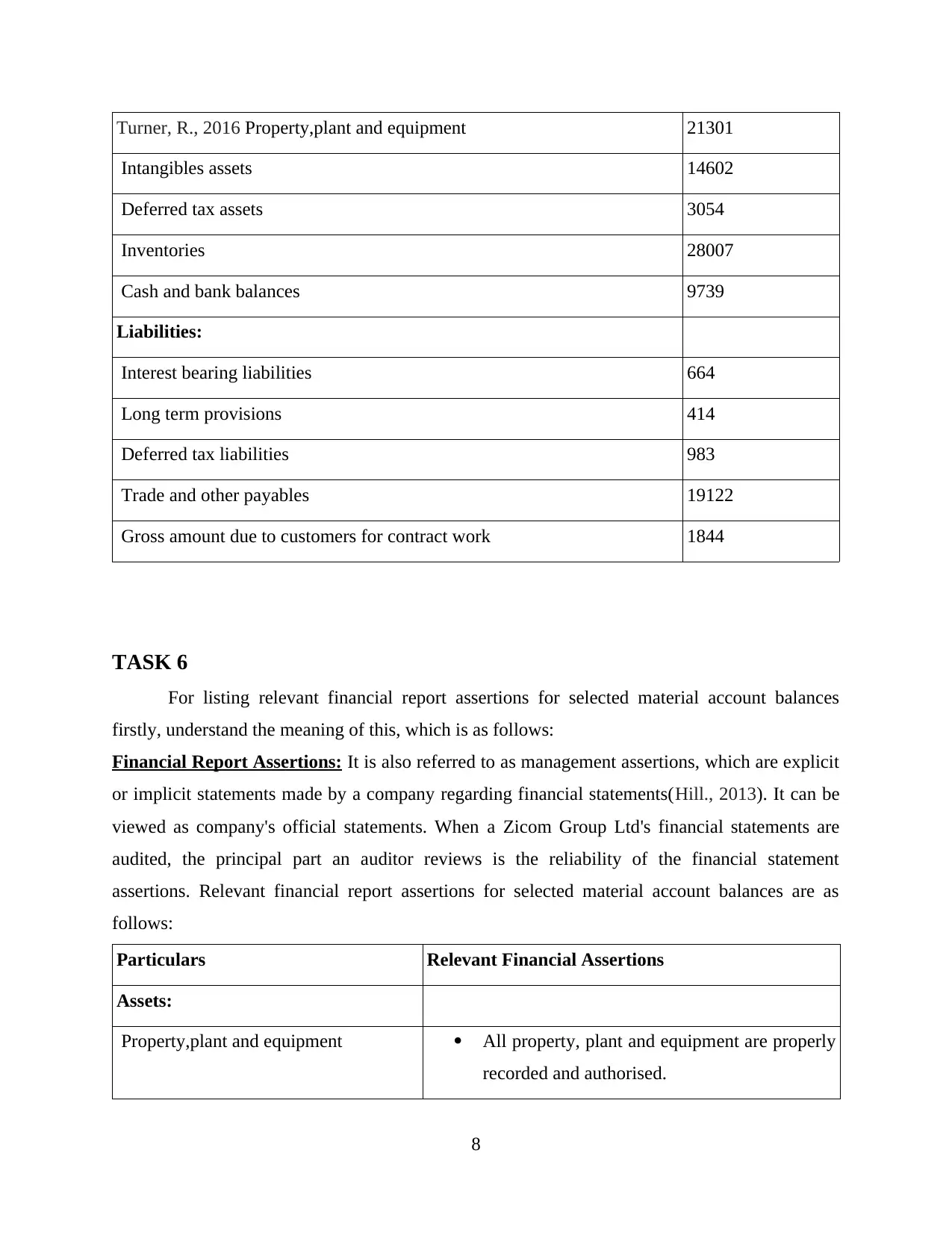

Ten different material account balances are as follows:

Particulars Amount

Assets:

7

Return on equity = Profit after tax/Net worth

Comments: In these ratio after calculating three year ratios as shown above, it can be easily

analysed that return is less in current year than year 2017-18 in both ratios as compared to

previous years. This mean, Zicom Group Ltd is not using assets & funds effectively and

efficiently which is invested by shareholders in the company. It can demotivate the investors to

not investing in this company due to low rate of return. Company should take corrective major

to enhance the income so that new investors can come and invest fund.

TASK 4

Materiality means those assets and liabilities whose increase or decrease can impact the

decision regarding financial statements for the users of financial statements and accordingly the

audit sample is made. In material, account balance refers to the size of recorded account balance

in the financial statement and it focuses towards physical aspects of things. Materiality refers to

the errors contained in balances and transactions while preparing the financial statements of

organisation. It is helpful for the planning purpose. For example , If auditor of Zicom Group Ltd

has shown wrongly $1000 as fixed assets where it has to be shown as current liability because it

amount of interest payable. So it is important for an auditor to find the errors while preparing the

financial statements as a result planning can be done effectively. If organisation has planned to

expand its business in different market and it is possible when financial statements provides

relevant information such as profits available in current year for company. For expansion, money

is needed and if corporation has sufficient profits as per the information available in financial

statement than it can plan for business expansion(Feng and Hudson., 2011). So it is helpful in

planning as well as decision making as a result management of company can take important

decision regarding expansion of its business (Turner., 2016).

TASK 5

Ten different material account balances are as follows:

Particulars Amount

Assets:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Turner, R., 2016 Property,plant and equipment 21301

Intangibles assets 14602

Deferred tax assets 3054

Inventories 28007

Cash and bank balances 9739

Liabilities:

Interest bearing liabilities 664

Long term provisions 414

Deferred tax liabilities 983

Trade and other payables 19122

Gross amount due to customers for contract work 1844

TASK 6

For listing relevant financial report assertions for selected material account balances

firstly, understand the meaning of this, which is as follows:

Financial Report Assertions: It is also referred to as management assertions, which are explicit

or implicit statements made by a company regarding financial statements(Hill., 2013). It can be

viewed as company's official statements. When a Zicom Group Ltd's financial statements are

audited, the principal part an auditor reviews is the reliability of the financial statement

assertions. Relevant financial report assertions for selected material account balances are as

follows:

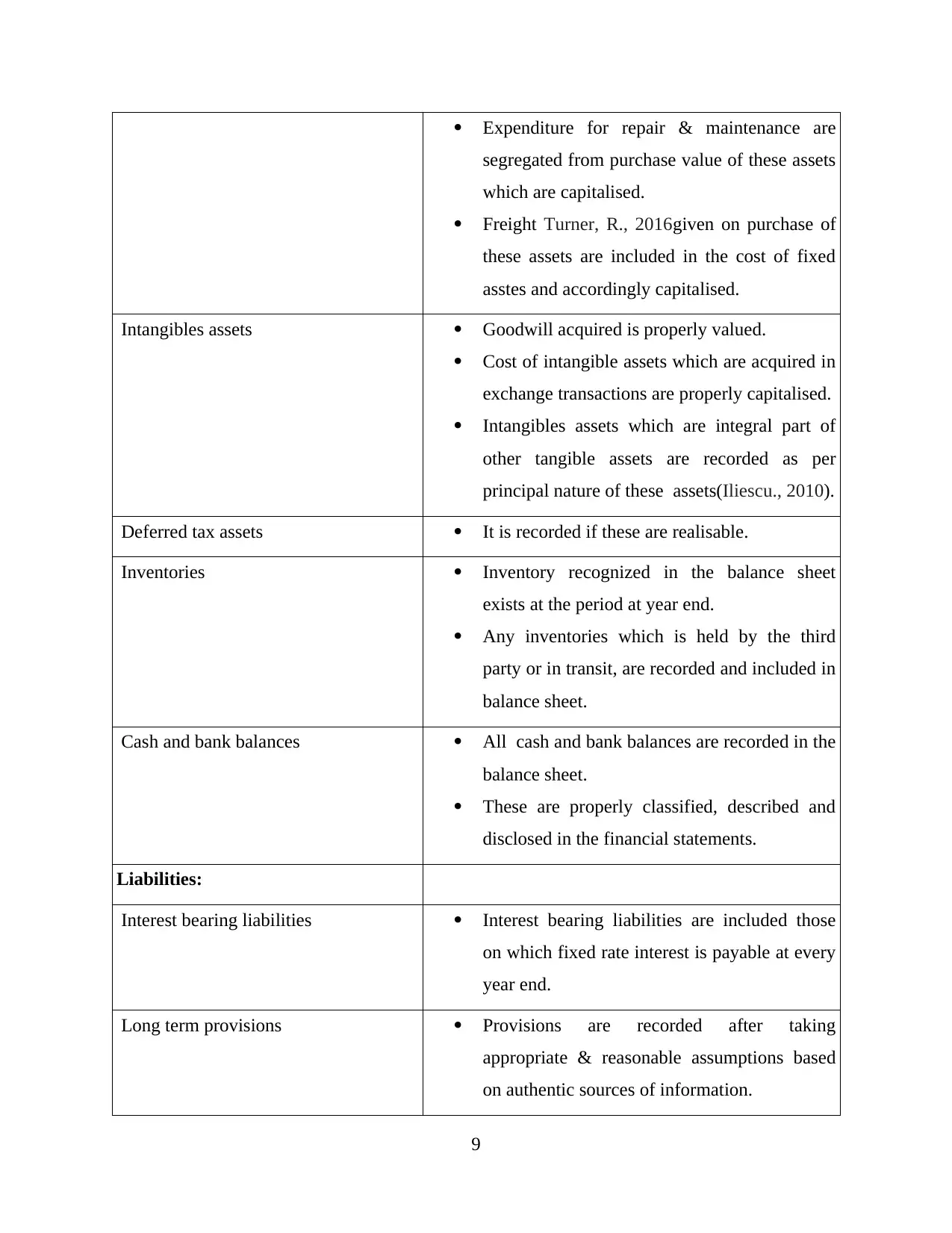

Particulars Relevant Financial Assertions

Assets:

Property,plant and equipment All property, plant and equipment are properly

recorded and authorised.

8

Intangibles assets 14602

Deferred tax assets 3054

Inventories 28007

Cash and bank balances 9739

Liabilities:

Interest bearing liabilities 664

Long term provisions 414

Deferred tax liabilities 983

Trade and other payables 19122

Gross amount due to customers for contract work 1844

TASK 6

For listing relevant financial report assertions for selected material account balances

firstly, understand the meaning of this, which is as follows:

Financial Report Assertions: It is also referred to as management assertions, which are explicit

or implicit statements made by a company regarding financial statements(Hill., 2013). It can be

viewed as company's official statements. When a Zicom Group Ltd's financial statements are

audited, the principal part an auditor reviews is the reliability of the financial statement

assertions. Relevant financial report assertions for selected material account balances are as

follows:

Particulars Relevant Financial Assertions

Assets:

Property,plant and equipment All property, plant and equipment are properly

recorded and authorised.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Expenditure for repair & maintenance are

segregated from purchase value of these assets

which are capitalised.

Freight Turner, R., 2016given on purchase of

these assets are included in the cost of fixed

asstes and accordingly capitalised.

Intangibles assets Goodwill acquired is properly valued.

Cost of intangible assets which are acquired in

exchange transactions are properly capitalised.

Intangibles assets which are integral part of

other tangible assets are recorded as per

principal nature of these assets(Iliescu., 2010).

Deferred tax assets It is recorded if these are realisable.

Inventories Inventory recognized in the balance sheet

exists at the period at year end.

Any inventories which is held by the third

party or in transit, are recorded and included in

balance sheet.

Cash and bank balances All cash and bank balances are recorded in the

balance sheet.

These are properly classified, described and

disclosed in the financial statements.

Liabilities:

Interest bearing liabilities Interest bearing liabilities are included those

on which fixed rate interest is payable at every

year end.

Long term provisions Provisions are recorded after taking

appropriate & reasonable assumptions based

on authentic sources of information.

9

segregated from purchase value of these assets

which are capitalised.

Freight Turner, R., 2016given on purchase of

these assets are included in the cost of fixed

asstes and accordingly capitalised.

Intangibles assets Goodwill acquired is properly valued.

Cost of intangible assets which are acquired in

exchange transactions are properly capitalised.

Intangibles assets which are integral part of

other tangible assets are recorded as per

principal nature of these assets(Iliescu., 2010).

Deferred tax assets It is recorded if these are realisable.

Inventories Inventory recognized in the balance sheet

exists at the period at year end.

Any inventories which is held by the third

party or in transit, are recorded and included in

balance sheet.

Cash and bank balances All cash and bank balances are recorded in the

balance sheet.

These are properly classified, described and

disclosed in the financial statements.

Liabilities:

Interest bearing liabilities Interest bearing liabilities are included those

on which fixed rate interest is payable at every

year end.

Long term provisions Provisions are recorded after taking

appropriate & reasonable assumptions based

on authentic sources of information.

9

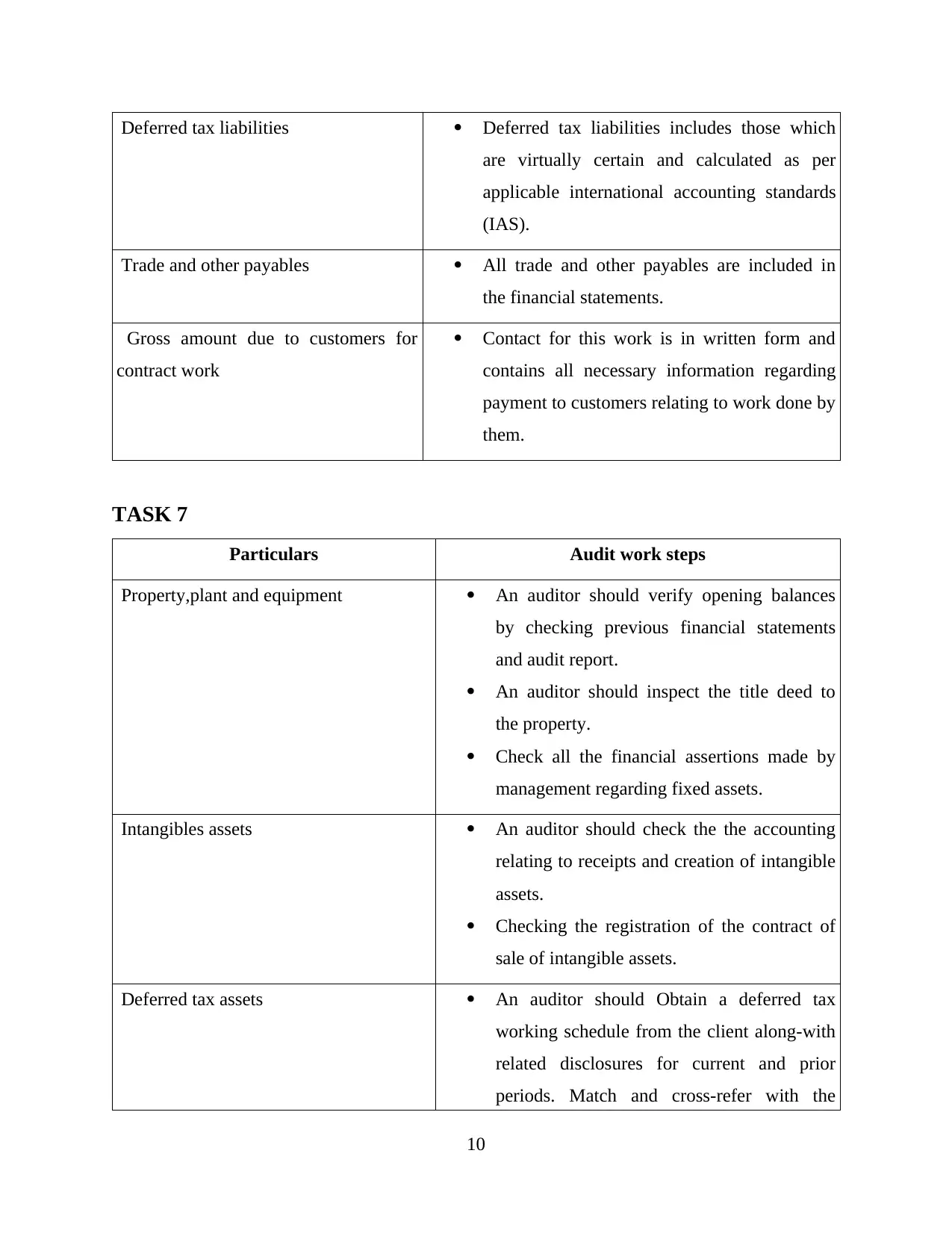

Deferred tax liabilities Deferred tax liabilities includes those which

are virtually certain and calculated as per

applicable international accounting standards

(IAS).

Trade and other payables All trade and other payables are included in

the financial statements.

Gross amount due to customers for

contract work

Contact for this work is in written form and

contains all necessary information regarding

payment to customers relating to work done by

them.

TASK 7

Particulars Audit work steps

Property,plant and equipment An auditor should verify opening balances

by checking previous financial statements

and audit report.

An auditor should inspect the title deed to

the property.

Check all the financial assertions made by

management regarding fixed assets.

Intangibles assets An auditor should check the the accounting

relating to receipts and creation of intangible

assets.

Checking the registration of the contract of

sale of intangible assets.

Deferred tax assets An auditor should Obtain a deferred tax

working schedule from the client along-with

related disclosures for current and prior

periods. Match and cross-refer with the

10

are virtually certain and calculated as per

applicable international accounting standards

(IAS).

Trade and other payables All trade and other payables are included in

the financial statements.

Gross amount due to customers for

contract work

Contact for this work is in written form and

contains all necessary information regarding

payment to customers relating to work done by

them.

TASK 7

Particulars Audit work steps

Property,plant and equipment An auditor should verify opening balances

by checking previous financial statements

and audit report.

An auditor should inspect the title deed to

the property.

Check all the financial assertions made by

management regarding fixed assets.

Intangibles assets An auditor should check the the accounting

relating to receipts and creation of intangible

assets.

Checking the registration of the contract of

sale of intangible assets.

Deferred tax assets An auditor should Obtain a deferred tax

working schedule from the client along-with

related disclosures for current and prior

periods. Match and cross-refer with the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.