Management Accounting Report: Zylla Company and Financial Analysis

VerifiedAdded on 2020/07/23

|16

|4730

|55

Report

AI Summary

This report delves into management accounting practices, focusing on a case study of the manufacturing company, Zylla. It begins by defining management accounting and exploring essential systems like job costing, cost accounting, inventory management, and price optimization, highlighting their advantages and disadvantages. The report then outlines various managerial accounting reporting methods, including budget reports, receivable reports, and job cost reports. A significant portion is dedicated to calculating costs using marginal and absorption costing techniques, providing a financial analysis of Zylla's operations. Furthermore, the report examines the benefits and drawbacks of different planning tools used for budgetary control. Finally, it addresses how organizations adapt management accounting systems to respond to financial issues, offering a comprehensive overview of the field and practical applications for business decision-making. The report is designed to provide a deeper understanding of the subject and help with the assignment.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

P1 Explaining management accounting along with the essential requirements of different

types of system.......................................................................................................................3

P2 Presenting different methods that can be used for management accounting reporting....6

P3 Calculating cost using marginal and absorption costing technique..................................7

P4 Explaining benefits and drawbacks of different types of planning tools that can be used

for budgetary control purpose................................................................................................9

P5 Comparing how organization adapt management accounting system for responding

monetary issues....................................................................................................................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................15

INTRODUCTION......................................................................................................................3

P1 Explaining management accounting along with the essential requirements of different

types of system.......................................................................................................................3

P2 Presenting different methods that can be used for management accounting reporting....6

P3 Calculating cost using marginal and absorption costing technique..................................7

P4 Explaining benefits and drawbacks of different types of planning tools that can be used

for budgetary control purpose................................................................................................9

P5 Comparing how organization adapt management accounting system for responding

monetary issues....................................................................................................................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................15

INTRODUCTION

Management accounting field of finance is highly concerned with the preparation of

reports regarding internal operations. Now, with the motive to track performance and taking

appropriate decisions business units lay high level of emphasis on using management

accounting tools. Hence, MA is the process of recording, analyzing and evaluating

performance which in turn helps in devising suitable plan for the organizational growth as

well as development. This report is based on Zylla, a manufacturing company, which is

planning to introduce some changes in the operations with the motive to attain success.

Hence, for managing changes in the best possible way Zylla wants to undertake managerial

accounting techniques. In this, report will provide deeper insight about the managerial

accounting systems and reporting aspects that can be undertaken by Zylla. Further, report wil

also shed light on the MA tools that can be used for planning purpose. Report also reflects the

manner in which marginal and absorption costing system helps in making assessment of cost

and profit margin. Besides this, report also entails how financial issues can be addressed

using MA techniques.

P1 Explaining management accounting along with the essential requirements of different

types of system

Management accounting is the process which lays emphasis on analyzing business

costs and operations. Such system is used by the manager for preparing financial report and

records which in turn aid in business decision making. The main motive of manager behind

undertaking management accounting tool is to develop competent strategic and policy

framework that pursuit organizational goals (Soltani, Nayebzadeh and Moeinaddin, 2014).

Zylla’s manager can make appropriate day to day and short term decisions by using

management accounting. Moreover, it assists in tracking performance, forecasting and

planning pertaining to the business operations.

Zylla need to make focus on undertaking below mentioned management accounting

systems such as:

Job costing: By using job costing method, manager of the firm can assess cost and

thereby becomes able to set suitable price of products and services. Under job costing

method, emphasis is placed on summing up of cost pertaining to material, labour and

overhead (Job costing, 2018). By using such tool, manager of Zylla can trace specific cost to

Management accounting field of finance is highly concerned with the preparation of

reports regarding internal operations. Now, with the motive to track performance and taking

appropriate decisions business units lay high level of emphasis on using management

accounting tools. Hence, MA is the process of recording, analyzing and evaluating

performance which in turn helps in devising suitable plan for the organizational growth as

well as development. This report is based on Zylla, a manufacturing company, which is

planning to introduce some changes in the operations with the motive to attain success.

Hence, for managing changes in the best possible way Zylla wants to undertake managerial

accounting techniques. In this, report will provide deeper insight about the managerial

accounting systems and reporting aspects that can be undertaken by Zylla. Further, report wil

also shed light on the MA tools that can be used for planning purpose. Report also reflects the

manner in which marginal and absorption costing system helps in making assessment of cost

and profit margin. Besides this, report also entails how financial issues can be addressed

using MA techniques.

P1 Explaining management accounting along with the essential requirements of different

types of system

Management accounting is the process which lays emphasis on analyzing business

costs and operations. Such system is used by the manager for preparing financial report and

records which in turn aid in business decision making. The main motive of manager behind

undertaking management accounting tool is to develop competent strategic and policy

framework that pursuit organizational goals (Soltani, Nayebzadeh and Moeinaddin, 2014).

Zylla’s manager can make appropriate day to day and short term decisions by using

management accounting. Moreover, it assists in tracking performance, forecasting and

planning pertaining to the business operations.

Zylla need to make focus on undertaking below mentioned management accounting

systems such as:

Job costing: By using job costing method, manager of the firm can assess cost and

thereby becomes able to set suitable price of products and services. Under job costing

method, emphasis is placed on summing up of cost pertaining to material, labour and

overhead (Job costing, 2018). By using such tool, manager of Zylla can trace specific cost to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

individual projects. Hence, job costing method helps company in assessing whether cost can

be reduced in later jobs or not. Hence, using job costing method Zylla can set suitable price

and become able to get appropriate profit margin.

Advantages

Helps in determining the profitability of job

Prevents duplication of work and helps in making estimation about similar job

Assists in evaluating quality of work

Facilitates cost control and profit maximization

Disadvantages

Expensive and time consuming in nature

In this, there is the absence of specific methods in relation to differentiating direct and

indirect cost occurring in the process

Job costing method requires close supervision

During inflation, comparison of job cost becomes meaningless

Cost accounting: Aim of such method is to capture company’s cost of production by

assessing input cost undertaken at each step. Along with this, cost accounting system also

lays emphasis on recording information about fixed expenses such as depreciation, rent etc

(Cost costing, 2018). Hence, such MA system provides detailed cost information which

management requires for controlling current operation and making plan about the near future.

Cost accounting system of MA offers following benefits and drawbacks to the business unit:

Advantages

Helps in reducing cost and identifying reasons pertaining to profit or loss

Cost accounting system provides high level of assistance in make or buy decisions

Price fixation and cost control

Disadvantages

It furnishes past information, whereas management is concerning in relation to taking

decision about the future

Cost accounting system does not provide suitable solution when capacity in partially

utilized.

be reduced in later jobs or not. Hence, using job costing method Zylla can set suitable price

and become able to get appropriate profit margin.

Advantages

Helps in determining the profitability of job

Prevents duplication of work and helps in making estimation about similar job

Assists in evaluating quality of work

Facilitates cost control and profit maximization

Disadvantages

Expensive and time consuming in nature

In this, there is the absence of specific methods in relation to differentiating direct and

indirect cost occurring in the process

Job costing method requires close supervision

During inflation, comparison of job cost becomes meaningless

Cost accounting: Aim of such method is to capture company’s cost of production by

assessing input cost undertaken at each step. Along with this, cost accounting system also

lays emphasis on recording information about fixed expenses such as depreciation, rent etc

(Cost costing, 2018). Hence, such MA system provides detailed cost information which

management requires for controlling current operation and making plan about the near future.

Cost accounting system of MA offers following benefits and drawbacks to the business unit:

Advantages

Helps in reducing cost and identifying reasons pertaining to profit or loss

Cost accounting system provides high level of assistance in make or buy decisions

Price fixation and cost control

Disadvantages

It furnishes past information, whereas management is concerning in relation to taking

decision about the future

Cost accounting system does not provide suitable solution when capacity in partially

utilized.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In cost accounting, costs are absorbed on the basis of pre-determined rate which in

turn leads under or over absorption of overhead.

Inventory management: Zylla can manage stock and price more effectually by taking

into account MA system. Inventory management system helps in evaluating whether stock is

efficiently used or not. Ordering and holding are the main costs which in turn highly

associated with the stock management. Hence, Zylla should focus on undertaking economic

order quantity method which in turn helps in determining number of units need to be ordered.

Hence, this in turn helps in reducing cost and avoiding issue pertaining to stock deficiency

within the unit.

Advantages

Reduction in cost in terms of holding and ordering

Ensures smooth functioning of operations by avoiding problems in relation to stock

deficiency. Hence, effectual inventory management helps in making optimal use of

resources such as labour, money etc.

Better planning

Disadvantages

Time-intensive activity

Installation of inventory management software imposes high cost in front of business

unit.

Price optimization: This management accounting software is usually used by the

companies for price determination. In other words, such software gives indication to the

company about prices which best meets its objectives in relation to profit maximization

(Fullerton, Kennedy and Widener, 2014). Further, using such system manager of Zylla can

assess the manner in which customer will respond to different prices for the products or

services. Hence, price optimization system helps company in making appropriate decisions

that makes contribution in the attainment of organizational goals and objectives.

Advantages

Aid in competent and quick decision

Helps in taking suitable pricing decisions

Assists in generating suitable profit margin

turn leads under or over absorption of overhead.

Inventory management: Zylla can manage stock and price more effectually by taking

into account MA system. Inventory management system helps in evaluating whether stock is

efficiently used or not. Ordering and holding are the main costs which in turn highly

associated with the stock management. Hence, Zylla should focus on undertaking economic

order quantity method which in turn helps in determining number of units need to be ordered.

Hence, this in turn helps in reducing cost and avoiding issue pertaining to stock deficiency

within the unit.

Advantages

Reduction in cost in terms of holding and ordering

Ensures smooth functioning of operations by avoiding problems in relation to stock

deficiency. Hence, effectual inventory management helps in making optimal use of

resources such as labour, money etc.

Better planning

Disadvantages

Time-intensive activity

Installation of inventory management software imposes high cost in front of business

unit.

Price optimization: This management accounting software is usually used by the

companies for price determination. In other words, such software gives indication to the

company about prices which best meets its objectives in relation to profit maximization

(Fullerton, Kennedy and Widener, 2014). Further, using such system manager of Zylla can

assess the manner in which customer will respond to different prices for the products or

services. Hence, price optimization system helps company in making appropriate decisions

that makes contribution in the attainment of organizational goals and objectives.

Advantages

Aid in competent and quick decision

Helps in taking suitable pricing decisions

Assists in generating suitable profit margin

Disadvantages

Installation of price-optimization software is expensive in nature

Demands for manager’s training which in turn imposes cost in front of the company

Hence, it can be depicted that in the context of organizational growth and success all the

above depicted management accounting systems are highly required. Using job, inventory,

cost and price optimization system manager of Zylla can make effective and profitable

decisions.

P2 Presenting different methods that can be used for management accounting reporting

Managerial accounting reports are prepared by the managers for meeting the needs or

requirements of internal stakeholders. Unlike financial accounting, managerial reports can be

prepared by the firm as per requirements such as weekly, monthly, quarterly etc. Hence,

preparing and using managerial accounting reports manager of Zylla can take decision

whether they need to make some modifications in the existing strategic and policy

framework. In the context of business unit, managerial accounting report are highly important

for the purpose of decision making. Thus, managerial reports must have characteristics

pertaining to reliability, comparability, clarity, timeliness etc. Hence, there are several types

of managerial accounting reports that can be prepared by Zylla’s manager are:

Budget report: It is also termed as performance report which contains information

about departmental performance. Hence, budget report presents the extent to which revenue

and expenses incurred by each department are in line with the budgeted figures. Along with

this, such report also exhibits causes due to which department fail to meet budgeted financial

figures. Thus, considering such report manager of Zylla can monitor the performance of each

department. Budget report gives indication to the manager about the actions that need to be

undertaken for cost control and profit maximization. Further, input given by budget report

will also provide assistance to the manager in developing competent financial plan or

framework for the upcoming period (Chenhall and Moers, 2015). In addition to this, by

keeping in mind budge report Zylla’s manager can provide personnel with suitable incentive

and thereby would become able to motivate them for performing better.

Receivable report: Accounts receivable ageing report provides information about the

time period which debtors are making payment which owe to them. Credit period which is

given to debtors has high level of impact on working capital management and thereby overall

Installation of price-optimization software is expensive in nature

Demands for manager’s training which in turn imposes cost in front of the company

Hence, it can be depicted that in the context of organizational growth and success all the

above depicted management accounting systems are highly required. Using job, inventory,

cost and price optimization system manager of Zylla can make effective and profitable

decisions.

P2 Presenting different methods that can be used for management accounting reporting

Managerial accounting reports are prepared by the managers for meeting the needs or

requirements of internal stakeholders. Unlike financial accounting, managerial reports can be

prepared by the firm as per requirements such as weekly, monthly, quarterly etc. Hence,

preparing and using managerial accounting reports manager of Zylla can take decision

whether they need to make some modifications in the existing strategic and policy

framework. In the context of business unit, managerial accounting report are highly important

for the purpose of decision making. Thus, managerial reports must have characteristics

pertaining to reliability, comparability, clarity, timeliness etc. Hence, there are several types

of managerial accounting reports that can be prepared by Zylla’s manager are:

Budget report: It is also termed as performance report which contains information

about departmental performance. Hence, budget report presents the extent to which revenue

and expenses incurred by each department are in line with the budgeted figures. Along with

this, such report also exhibits causes due to which department fail to meet budgeted financial

figures. Thus, considering such report manager of Zylla can monitor the performance of each

department. Budget report gives indication to the manager about the actions that need to be

undertaken for cost control and profit maximization. Further, input given by budget report

will also provide assistance to the manager in developing competent financial plan or

framework for the upcoming period (Chenhall and Moers, 2015). In addition to this, by

keeping in mind budge report Zylla’s manager can provide personnel with suitable incentive

and thereby would become able to motivate them for performing better.

Receivable report: Accounts receivable ageing report provides information about the

time period which debtors are making payment which owe to them. Credit period which is

given to debtors has high level of impact on working capital management and thereby overall

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

operations. Moreover, company requires enough funds for meeting day to day monetary

requirements. Hence, by evaluating account receivable report Zylla’s manager can take

suitable decision for effective cash flow management. As such report furnishes information

about the issues associated with the collection process. Thus, by finding debtors who are

unable to pay their balance company can strict credit policies. This in turn helps in getting

funds within the suitable time frame and thereby ensures effectual cash management.

Job cost reports: Zylla’ s manager can assess expenses associated with the specific

project. This report presents job profitability by matching or making evaluation of estimated

revenue. Considering this report, manager of the concerned manufacturing unit can assess

high-earning areas of business (Eldenburg and et.al., 2016). This aspect shows that budget

report assists manager in making efforts in the suitable direction.

P3 Calculating cost using marginal and absorption costing technique

Specifically, there are mainly two types of techniques which can be used by Zylla

such as:

Marginal costing: It highlights increase or decrease takes place in the production cost

when one additional input is manufactured. Marginal costing technique is used under

management accounting in which variable cost is charged on the basis of unit produced or

manufactured (Chiwamit, Modell and Scapens, 2017). On the other side, in marginal costing

technique, fixed cost of the period are written off in against to the aggregate contribution

level.

Absorption costing: This is also known as full costing method under which both fixed

and variable costs are apportioned on the basis of cost centre as well as absorption rates.

Absorption costing method believes that all the costs incurred can be recovered through the

selling price of a product or service. In other words, absorption costing method lays emphasis

on accumulating cost associated with the production process (Marginal and absorption

costing, 2018). Thereafter, with the motive to present suitable view of cost and profit,

production cost is apportioned into individual products.

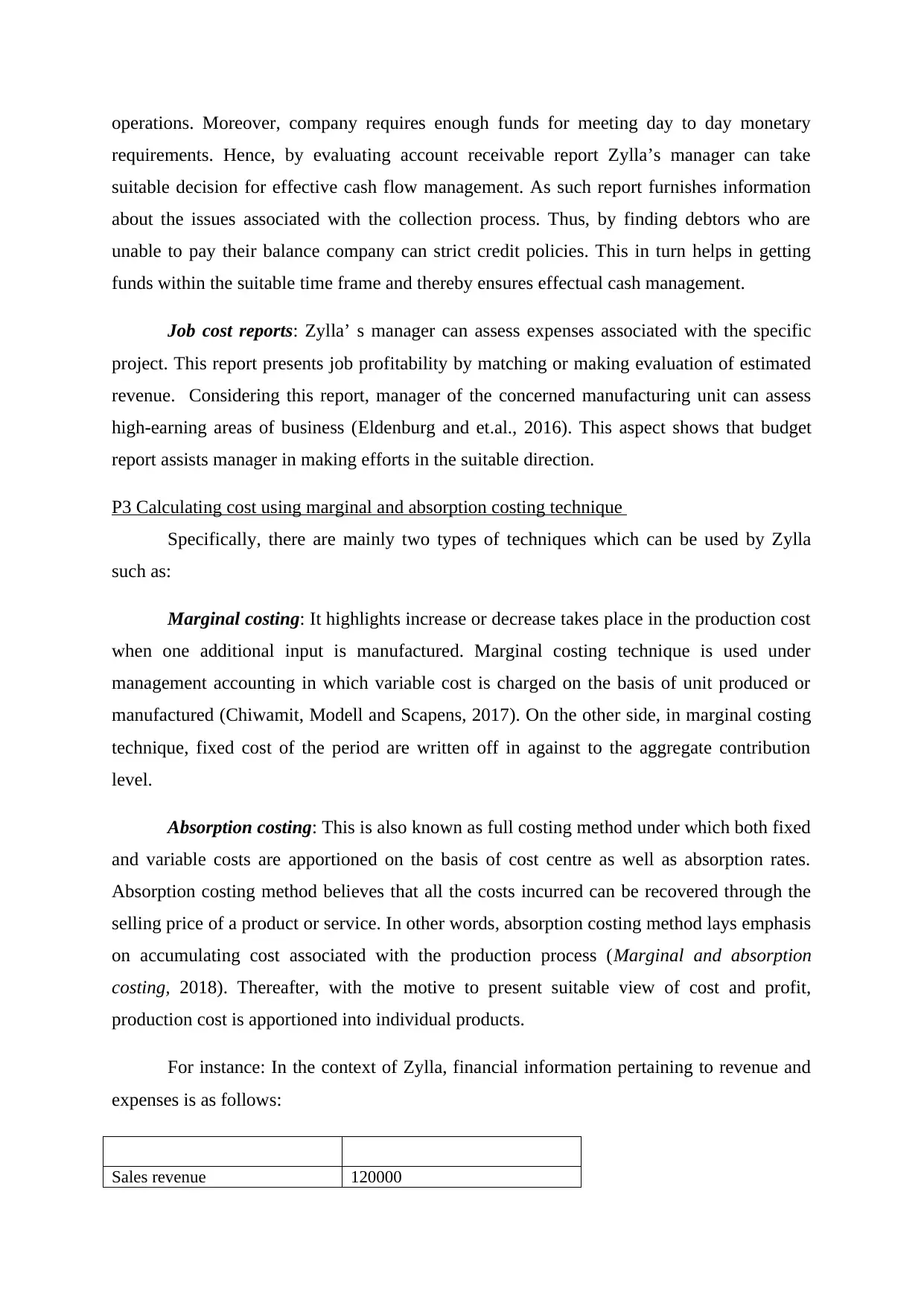

For instance: In the context of Zylla, financial information pertaining to revenue and

expenses is as follows:

Sales revenue 120000

requirements. Hence, by evaluating account receivable report Zylla’s manager can take

suitable decision for effective cash flow management. As such report furnishes information

about the issues associated with the collection process. Thus, by finding debtors who are

unable to pay their balance company can strict credit policies. This in turn helps in getting

funds within the suitable time frame and thereby ensures effectual cash management.

Job cost reports: Zylla’ s manager can assess expenses associated with the specific

project. This report presents job profitability by matching or making evaluation of estimated

revenue. Considering this report, manager of the concerned manufacturing unit can assess

high-earning areas of business (Eldenburg and et.al., 2016). This aspect shows that budget

report assists manager in making efforts in the suitable direction.

P3 Calculating cost using marginal and absorption costing technique

Specifically, there are mainly two types of techniques which can be used by Zylla

such as:

Marginal costing: It highlights increase or decrease takes place in the production cost

when one additional input is manufactured. Marginal costing technique is used under

management accounting in which variable cost is charged on the basis of unit produced or

manufactured (Chiwamit, Modell and Scapens, 2017). On the other side, in marginal costing

technique, fixed cost of the period are written off in against to the aggregate contribution

level.

Absorption costing: This is also known as full costing method under which both fixed

and variable costs are apportioned on the basis of cost centre as well as absorption rates.

Absorption costing method believes that all the costs incurred can be recovered through the

selling price of a product or service. In other words, absorption costing method lays emphasis

on accumulating cost associated with the production process (Marginal and absorption

costing, 2018). Thereafter, with the motive to present suitable view of cost and profit,

production cost is apportioned into individual products.

For instance: In the context of Zylla, financial information pertaining to revenue and

expenses is as follows:

Sales revenue 120000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Raw material cost 25000

Direct labour expenses 15000

Manufacturing overheads

Fixed 8000

Variable 12000

Distribution & administration

expenses

Fixed 5000

Variable 7000

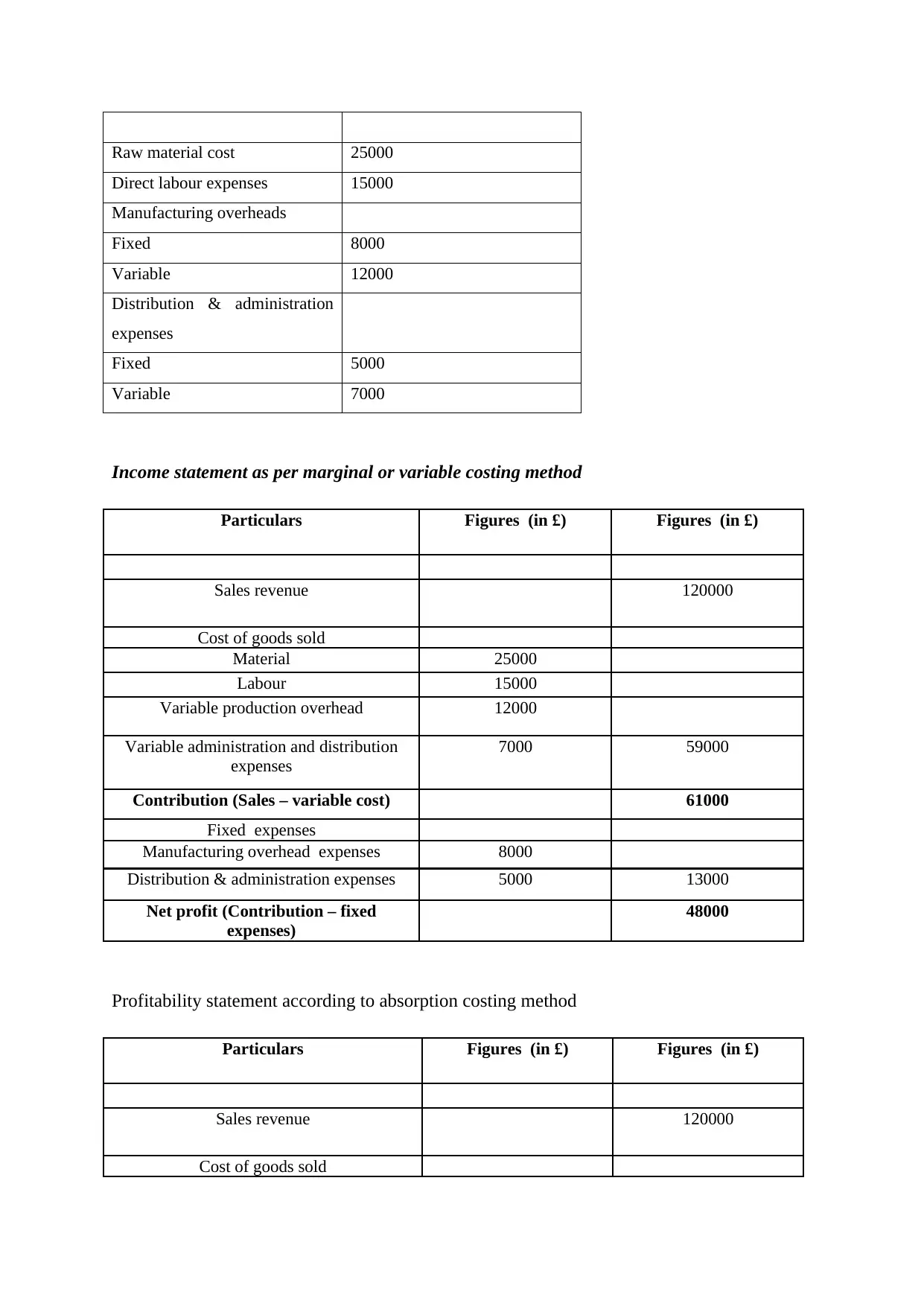

Income statement as per marginal or variable costing method

Particulars Figures (in £) Figures (in £)

Sales revenue 120000

Cost of goods sold

Material 25000

Labour 15000

Variable production overhead 12000

Variable administration and distribution

expenses

7000 59000

Contribution (Sales – variable cost) 61000

Fixed expenses

Manufacturing overhead expenses 8000

Distribution & administration expenses 5000 13000

Net profit (Contribution – fixed

expenses)

48000

Profitability statement according to absorption costing method

Particulars Figures (in £) Figures (in £)

Sales revenue 120000

Cost of goods sold

Direct labour expenses 15000

Manufacturing overheads

Fixed 8000

Variable 12000

Distribution & administration

expenses

Fixed 5000

Variable 7000

Income statement as per marginal or variable costing method

Particulars Figures (in £) Figures (in £)

Sales revenue 120000

Cost of goods sold

Material 25000

Labour 15000

Variable production overhead 12000

Variable administration and distribution

expenses

7000 59000

Contribution (Sales – variable cost) 61000

Fixed expenses

Manufacturing overhead expenses 8000

Distribution & administration expenses 5000 13000

Net profit (Contribution – fixed

expenses)

48000

Profitability statement according to absorption costing method

Particulars Figures (in £) Figures (in £)

Sales revenue 120000

Cost of goods sold

Material 25000

Labour 15000

fixed production overhead 8000

Variable manufacturing expenses 12000 60000

Gross profit 60000

Administration and selling expenses

fixed 5000

Variable expenses 7000 12000

Net profit (GP – indirect expenses) 48000

The above depicted table shows that net margin as per both marginal and absorption

costing method accounts for £48000 respectively. The main difference between marginal and

absorption costing is the consideration of fixed cost. In other words, under marginal costing

method all the fixed costs whether related to production or selling and administration are

deducted from contribution margin. In contrast to this, as per full costing method both fixed

and variable manufacturing expenses such as £20000 are subtracted from revenue. Moreover,

absorption costing method believes that fixed cost can easily be recovered through selling

prices. Further, under absorption costing method variances take place in the opening and

closing stock has significant impact on cost per unit. On the other hand, in marginal costing

method, variances exist in the opening and ending stock does not have influence on cost per

unit of output.

P4 Explaining benefits and drawbacks of different types of planning tools that can be used for

budgetary control purpose

Budget is the main part of business unit that manager prepares with the motive to

spend money in an appropriate manner. There are several modern and traditional tools are

available that can be employed by Zylla’s manager for preparing financial plan or

framework. Currently, Zylla is preparing budget using incremental technique which comes

under the category of traditional tools. On the basis of such technique, firm makes some

additions in the past framework for arriving at new budget. Howeveincremental budgeting

technique is less important in the today’s dynamic environment. Hence, several tools are

available that business entity of Zylla can use for planning and budgetary control purpose.

Activity based budgeting: This modern budgeting technique emphasizes on assessing

and evaluating cost associated with very activity. ABB completely avoid traditional aspects

Labour 15000

fixed production overhead 8000

Variable manufacturing expenses 12000 60000

Gross profit 60000

Administration and selling expenses

fixed 5000

Variable expenses 7000 12000

Net profit (GP – indirect expenses) 48000

The above depicted table shows that net margin as per both marginal and absorption

costing method accounts for £48000 respectively. The main difference between marginal and

absorption costing is the consideration of fixed cost. In other words, under marginal costing

method all the fixed costs whether related to production or selling and administration are

deducted from contribution margin. In contrast to this, as per full costing method both fixed

and variable manufacturing expenses such as £20000 are subtracted from revenue. Moreover,

absorption costing method believes that fixed cost can easily be recovered through selling

prices. Further, under absorption costing method variances take place in the opening and

closing stock has significant impact on cost per unit. On the other hand, in marginal costing

method, variances exist in the opening and ending stock does not have influence on cost per

unit of output.

P4 Explaining benefits and drawbacks of different types of planning tools that can be used for

budgetary control purpose

Budget is the main part of business unit that manager prepares with the motive to

spend money in an appropriate manner. There are several modern and traditional tools are

available that can be employed by Zylla’s manager for preparing financial plan or

framework. Currently, Zylla is preparing budget using incremental technique which comes

under the category of traditional tools. On the basis of such technique, firm makes some

additions in the past framework for arriving at new budget. Howeveincremental budgeting

technique is less important in the today’s dynamic environment. Hence, several tools are

available that business entity of Zylla can use for planning and budgetary control purpose.

Activity based budgeting: This modern budgeting technique emphasizes on assessing

and evaluating cost associated with very activity. ABB completely avoid traditional aspects

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

pertaining to making some changes in the past budget as per inflationary trends. In this, focus

is placed on analyzing relationship between each cost and business activity (Schaltegger and

Burritt, 2017). Under ABB, activities which incur cost are recorded, analyzed and researched.

Hence, in this budgeting technique by taking into account cost drivers funds are allocated to

each activity.

Advantages:

ABB technique facilitates selling price fixation pertaining to multi-products because

in this overheads are allocated on the basis of related suitable cost drivers.

Assists is presenting suitable and reliable view of cost by developing link between

cost and activities.

Gives clear indication regarding the control of overhead cost by highlight redundant

and unproductive activities.

Disadvantages:

Demands for managerial training because without having ability to recognize cost

driver manager would not become able to develop suitable budget.

Highly time consuming activity

It is not suitable where companies require monthly profitability statements

Zero based budgeting: ABB may be served as a reform over traditional tool such as

incremental technique. In the case of zero base budgeting technique, manager starts from

scratch with zero base. Further, as per ZBB, every function of an organization is analyzed for

its need ad cost. In other words, ZBB method entails that company should make focus on

assessing alternative and cost effective ways of performing activities. Hence, in this prior

emphasis is placed on analyzing activities that need to be performed within the period for

getting the desired level of outcome or success (Cooper, Ezzamel and Qu, 2017). Thereafter,

manager focuses on finding optimal ways to perform the same. Hence, in this, every line of

item is clearly justified by the manager which in turn considered as highly prominent.

Advantages:

Efficient: ZBB ensures effective and efficient allocation of financial resources among

departments by avoiding historical numbers.

is placed on analyzing relationship between each cost and business activity (Schaltegger and

Burritt, 2017). Under ABB, activities which incur cost are recorded, analyzed and researched.

Hence, in this budgeting technique by taking into account cost drivers funds are allocated to

each activity.

Advantages:

ABB technique facilitates selling price fixation pertaining to multi-products because

in this overheads are allocated on the basis of related suitable cost drivers.

Assists is presenting suitable and reliable view of cost by developing link between

cost and activities.

Gives clear indication regarding the control of overhead cost by highlight redundant

and unproductive activities.

Disadvantages:

Demands for managerial training because without having ability to recognize cost

driver manager would not become able to develop suitable budget.

Highly time consuming activity

It is not suitable where companies require monthly profitability statements

Zero based budgeting: ABB may be served as a reform over traditional tool such as

incremental technique. In the case of zero base budgeting technique, manager starts from

scratch with zero base. Further, as per ZBB, every function of an organization is analyzed for

its need ad cost. In other words, ZBB method entails that company should make focus on

assessing alternative and cost effective ways of performing activities. Hence, in this prior

emphasis is placed on analyzing activities that need to be performed within the period for

getting the desired level of outcome or success (Cooper, Ezzamel and Qu, 2017). Thereafter,

manager focuses on finding optimal ways to perform the same. Hence, in this, every line of

item is clearly justified by the manager which in turn considered as highly prominent.

Advantages:

Efficient: ZBB ensures effective and efficient allocation of financial resources among

departments by avoiding historical numbers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accurate: It focuses on relooking every item of cash flow which in turn helps in

presenting accurate view of monetary aspects.

Decline in redundant activities: ZBB leads reduction in unproductive activities

because it focuses on finding cost-effective ways of doing activities. Effective co-ordination and communication: In ZBB, employees are involved in the

decision making process which in turn places positive impact on their motivational

aspects. Thus, effective co-ordination and communication can be built by Zylla using

ZBB.

Disadvantages:

Time consuming: Preparation of budgeting according to ZBB is highly time

consuming because in this no prior aspects are considered by the manager.

High manpower requirement: In this, entire budget is start from scratch which in turn

may require involvement of large number of personnel. Hence, most of the

departments have to spend adequate time and resources for the same.

Lack of expertise: Zylla also need to conduct training sessions for the managers in

relation to developing their ability regarding the explanation of every cost of item.

This in turn also imposes cost in front of Zylla and impacts profit margin.

Variance analysis: For the purpose of budgetary control, variance analysis tool is

recognized as highly effectual. It may be presented as a quantitative investigation tool which

helps in ascertaining differences that take place between actual and planned behaviour.

Hence, it helps in identifying deviations which take place between actual and budgeted

income or expenses (Jermias, 2017). Variance analysis tool helps in identifying reasons take

place behind the occurrence of deviations and indicate requirement in relation to taking

appropriate measure for improvement.

Advantages:

It helps in taking remedial measure or action on time and thereby improves overall

performance level.

Assists in developing realistic and achievable plan for the upcoming time period.

Helps in fixing the accountability of individual or department

Such quantitative tool clearly highlights inefficient performances and the level of

same.

presenting accurate view of monetary aspects.

Decline in redundant activities: ZBB leads reduction in unproductive activities

because it focuses on finding cost-effective ways of doing activities. Effective co-ordination and communication: In ZBB, employees are involved in the

decision making process which in turn places positive impact on their motivational

aspects. Thus, effective co-ordination and communication can be built by Zylla using

ZBB.

Disadvantages:

Time consuming: Preparation of budgeting according to ZBB is highly time

consuming because in this no prior aspects are considered by the manager.

High manpower requirement: In this, entire budget is start from scratch which in turn

may require involvement of large number of personnel. Hence, most of the

departments have to spend adequate time and resources for the same.

Lack of expertise: Zylla also need to conduct training sessions for the managers in

relation to developing their ability regarding the explanation of every cost of item.

This in turn also imposes cost in front of Zylla and impacts profit margin.

Variance analysis: For the purpose of budgetary control, variance analysis tool is

recognized as highly effectual. It may be presented as a quantitative investigation tool which

helps in ascertaining differences that take place between actual and planned behaviour.

Hence, it helps in identifying deviations which take place between actual and budgeted

income or expenses (Jermias, 2017). Variance analysis tool helps in identifying reasons take

place behind the occurrence of deviations and indicate requirement in relation to taking

appropriate measure for improvement.

Advantages:

It helps in taking remedial measure or action on time and thereby improves overall

performance level.

Assists in developing realistic and achievable plan for the upcoming time period.

Helps in fixing the accountability of individual or department

Such quantitative tool clearly highlights inefficient performances and the level of

same.

Highly suitable for cost control and profit maximization

Disadvantages:

If budgeted plan is not suitable or realistic in nature then it leads more unfavourable

variances. This in turn leads further inappropriate decision making.

Time consuming exercise

Responsibility centres: In regard to planning and budgetary control, responsibility centres

can be created by Zylla. Hence, by taking inputs from the manager of each responsibility

centre such as sales, expenses etc Zylla can set suitable financial framework for upcoming

time period.

Variance analysis: This managerial accounting tool also assists in doing planning for the

near future prominently. Variance analysis tool helps in identifying reasons due to which

deviations are occurred in the different areas. Hence, referring the outcome of variance

analysis and causes behind the same manager of Zylla can do proper financial forecast and

thereby become able to develop competent budgeting framework.

Capital budgeting: By taking into account capital budgeting tools and techniques

Zylla can do better planning. There are several tools such as payback method, net present

value, average and internal rate of return which helps in assessing the viability of capital

investment project more effectually. Payback method presents the time frame within which

company will recover amount initially invested by it. Further, NPV and IRR method presents

return associated with the investment proposals by considering time value of money concept.

Thus, using investment appraisal tools business unit can select suitable proposal and thereby

would become able to generate high profit.

P5 Comparing how organization adapt management accounting system for responding

monetary issues

In the context of business unit, issues are usually occur pertaining to the monetary

aspects and thereby closely influences overall functioning. Hence, company can attain

success in the strategic business arena only when it responds monetary issues within the

suitable time frame. Thus, there are several MA tools which Zylla can employ for dealing

with the monetary issues such as benchmarking, key performance indicators, financial

governance, balance scorecard etc.

Disadvantages:

If budgeted plan is not suitable or realistic in nature then it leads more unfavourable

variances. This in turn leads further inappropriate decision making.

Time consuming exercise

Responsibility centres: In regard to planning and budgetary control, responsibility centres

can be created by Zylla. Hence, by taking inputs from the manager of each responsibility

centre such as sales, expenses etc Zylla can set suitable financial framework for upcoming

time period.

Variance analysis: This managerial accounting tool also assists in doing planning for the

near future prominently. Variance analysis tool helps in identifying reasons due to which

deviations are occurred in the different areas. Hence, referring the outcome of variance

analysis and causes behind the same manager of Zylla can do proper financial forecast and

thereby become able to develop competent budgeting framework.

Capital budgeting: By taking into account capital budgeting tools and techniques

Zylla can do better planning. There are several tools such as payback method, net present

value, average and internal rate of return which helps in assessing the viability of capital

investment project more effectually. Payback method presents the time frame within which

company will recover amount initially invested by it. Further, NPV and IRR method presents

return associated with the investment proposals by considering time value of money concept.

Thus, using investment appraisal tools business unit can select suitable proposal and thereby

would become able to generate high profit.

P5 Comparing how organization adapt management accounting system for responding

monetary issues

In the context of business unit, issues are usually occur pertaining to the monetary

aspects and thereby closely influences overall functioning. Hence, company can attain

success in the strategic business arena only when it responds monetary issues within the

suitable time frame. Thus, there are several MA tools which Zylla can employ for dealing

with the monetary issues such as benchmarking, key performance indicators, financial

governance, balance scorecard etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.