Analysis of Funding Sources and Investment Appraisal for Zylla Ltd.

VerifiedAdded on 2020/10/05

|9

|1602

|109

Report

AI Summary

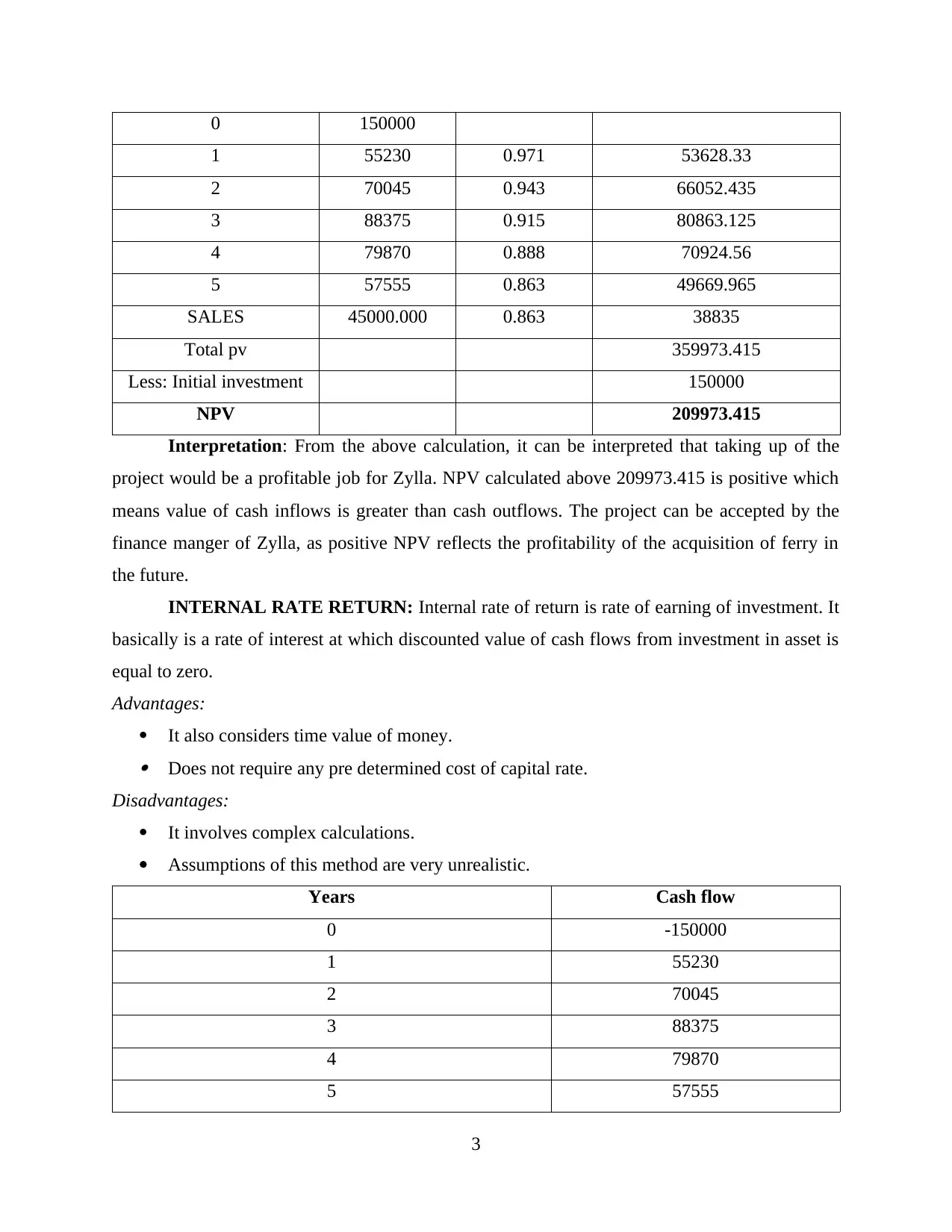

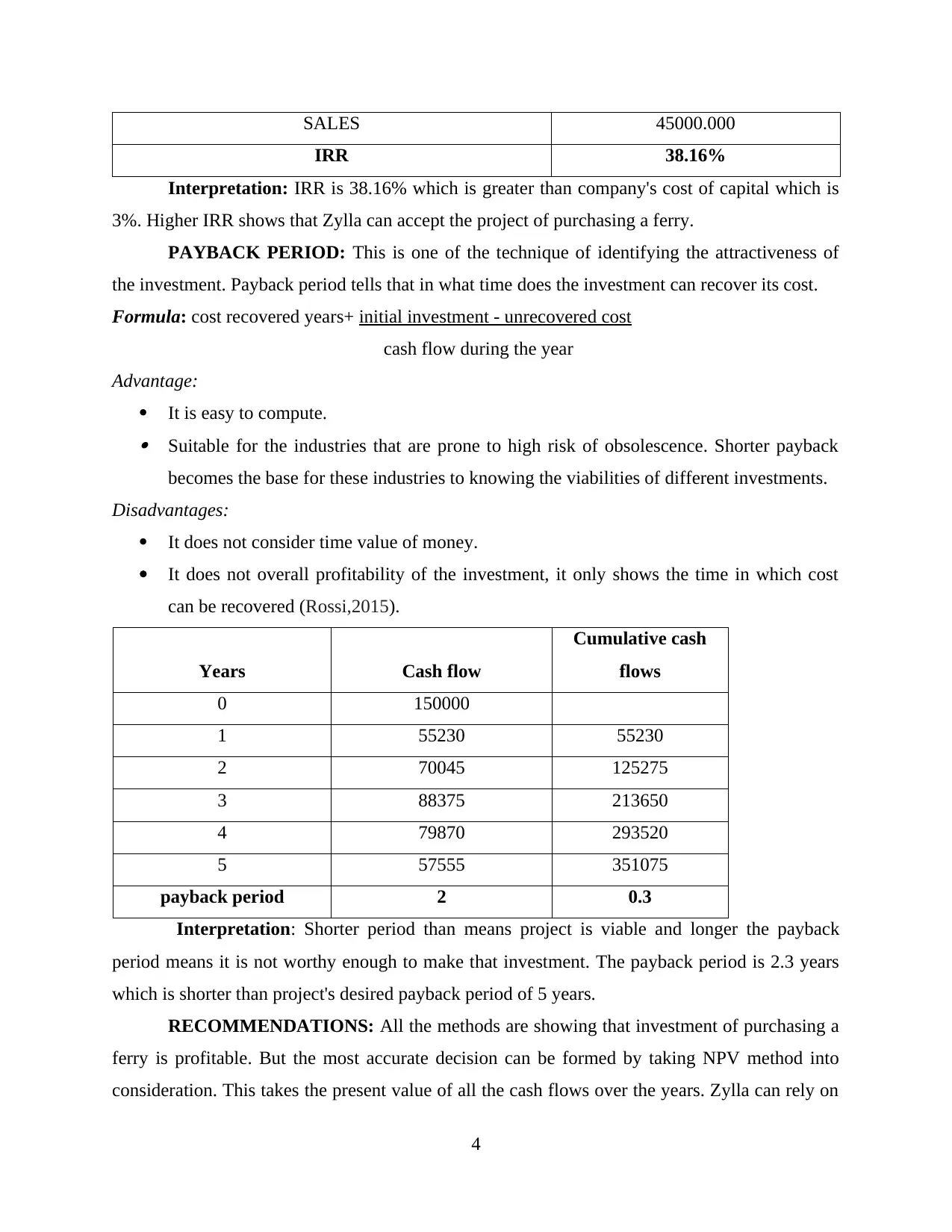

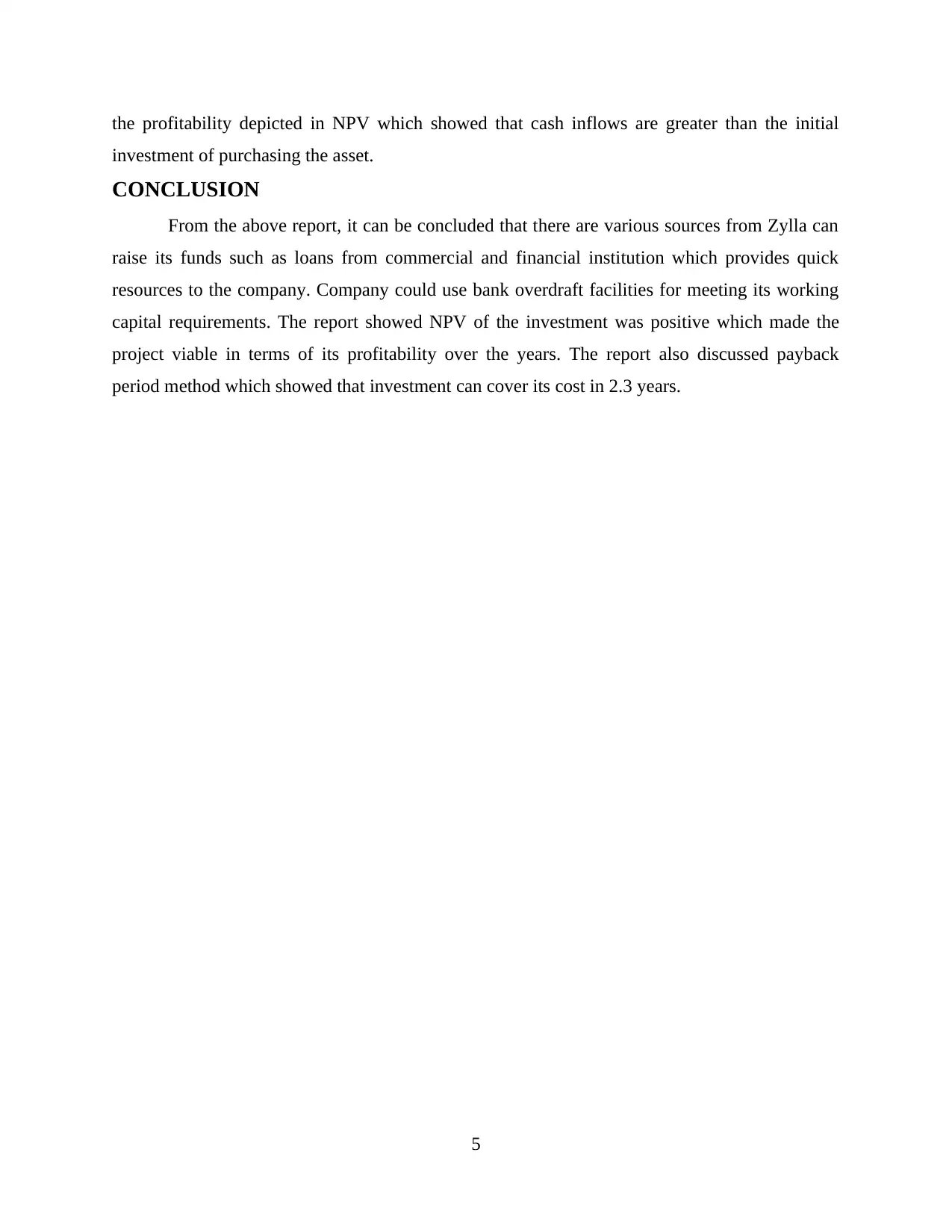

This report analyzes the financial strategies of Zylla Ltd., a company providing services for crossing people, goods, and vehicles. It explores both short-term and long-term funding sources, including equity shares, loans, bank overdrafts, discounted bills, and commercial paper, considering their suitability for acquiring a ferry and meeting working capital requirements. The report evaluates investment appraisal techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), and Payback Period to assess the viability of the ferry acquisition project. The NPV calculation reveals a positive value, indicating the project's profitability. The IRR of 38.16% exceeds the company's cost of capital, further supporting the investment. The payback period of 2.3 years suggests a relatively quick return on investment. The report concludes with recommendations, emphasizing the accuracy of the NPV method and suggesting Zylla Ltd. proceed with the investment based on the positive financial indicators. The report references several financial management books and journals.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.