Financial Analysis and Report: Zylla Ltd's Ferry Acquisition Plan

VerifiedAdded on 2023/01/11

|8

|1419

|54

Report

AI Summary

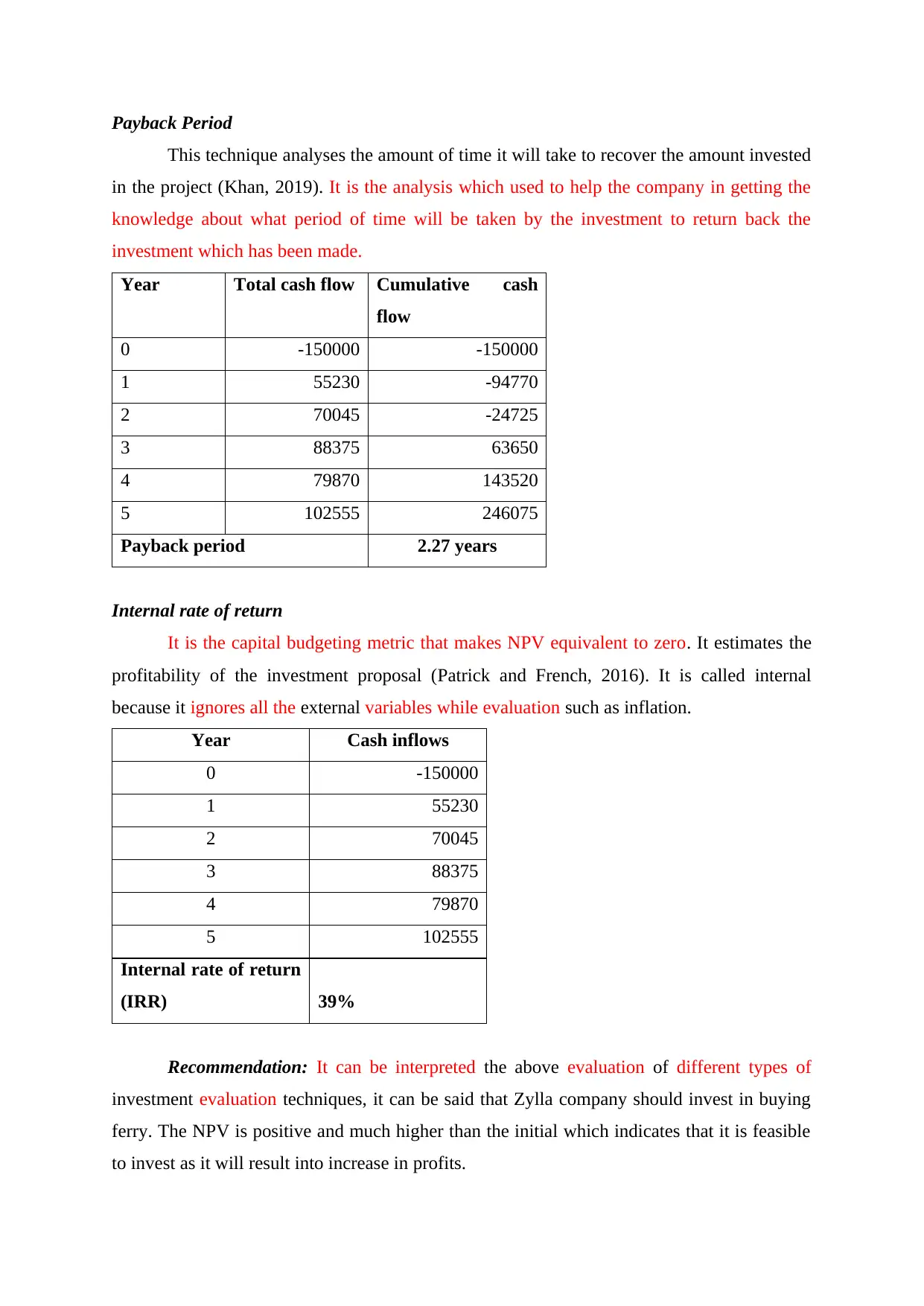

This report, prepared for Zylla Ltd, a company operating ferries, examines the financial implications of acquiring a new ferry to meet increased demand. The report details the sources of finance, both short-term (trade credit, customer advances, factoring services) and long-term (equity/debentures, term loans, retained earnings), available to fund the acquisition and expansion. It also analyzes various capital budgeting techniques, including Accounting Rate of Return (ARR), Net Present Value (NPV), Payback Period, and Internal Rate of Return (IRR), to assess the project's financial viability. Based on these analyses, the report recommends that Zylla Ltd invest in the ferry, concluding that the investment is financially sound and will increase profits. The report also includes a conclusion summarizing the key findings and recommendations, along with a list of cited references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.