Zylla Limited: Financial Report on Ferry Acquisition and Expansion

VerifiedAdded on 2020/11/12

|8

|1621

|174

Report

AI Summary

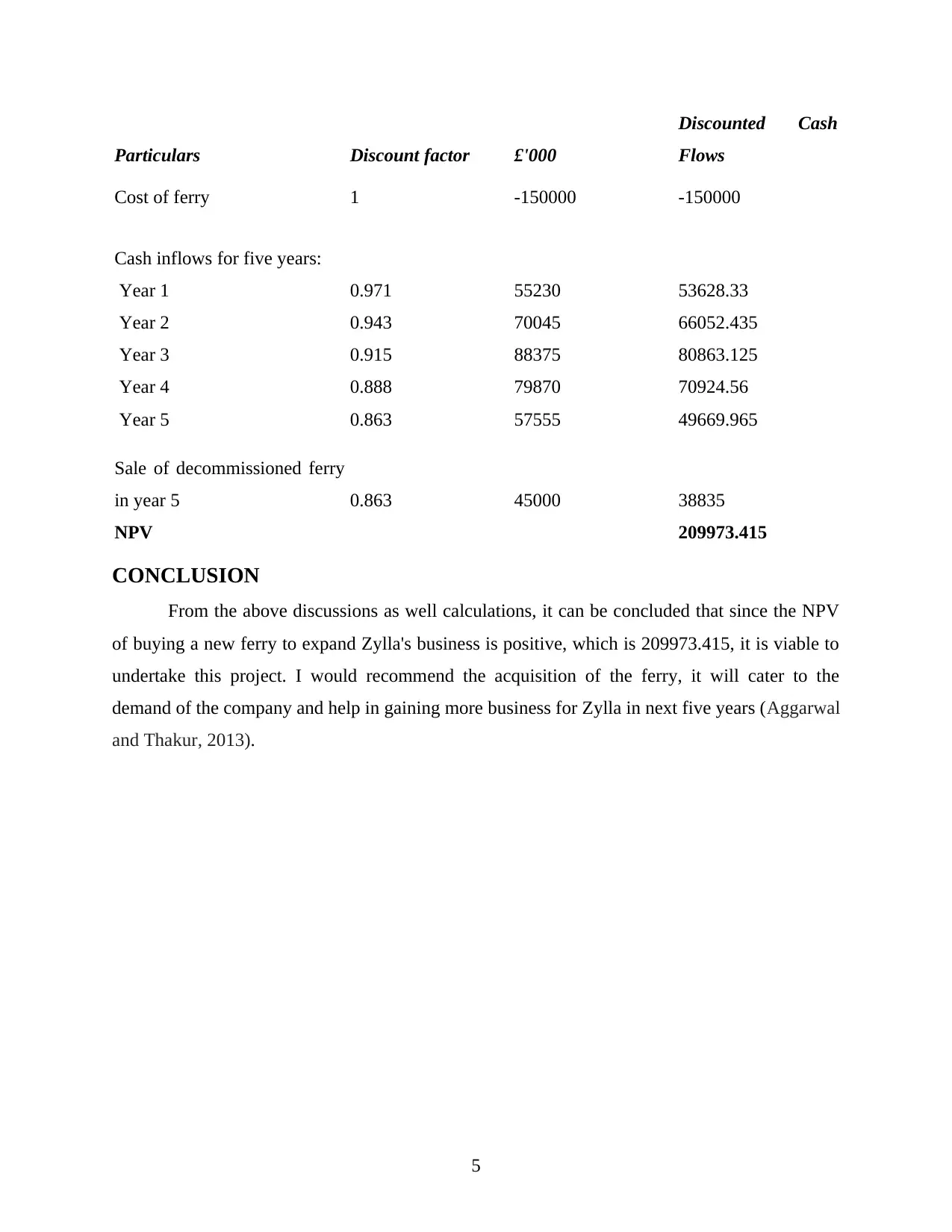

This financial report examines Zylla Limited's potential expansion through the acquisition of a new ferry, evaluating various sources of finance and investment appraisal techniques. The report explores both short-term and long-term financing options, including overdrafts, loans from family and friends, trade credit, debt factoring, bank loans, retained profits, equity financing, and debt financing. It analyzes the advantages and disadvantages of each source. Furthermore, the report applies the Net Present Value (NPV) investment appraisal technique to assess the financial viability of the ferry acquisition, ultimately concluding that the project is viable based on a positive NPV of 209973.415. The report recommends proceeding with the ferry acquisition, which is expected to meet growing demand and benefit Zylla Limited over the next five years. References to relevant literature are also included.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.