Detailed Analysis of Management Accounting System for Zylla Company

VerifiedAdded on 2020/06/04

|15

|5016

|36

Report

AI Summary

This report, prepared for the General Manager of Zylla Company by the Management Accounting Officer, provides a comprehensive overview of the company's management accounting system. It begins with an introduction to management accounting and its importance in achieving business objectives, emphasizing techniques like ratio analysis, budgeting, and forecasting. The report then delves into Task 1, detailing the differences between financial and management accounting, and explores various techniques including cost accounting, inventory management, and financial analysis. Task 2 focuses on methods to enhance company lucrativeness through a robust reporting system, covering performance, operational, job costing, inventory management, and accounts receivable reports. The report further highlights the advantages of implementing a management accounting system, such as improved planning, cost reduction, and enhanced customer service. Finally, Task 3 and 4 examine costing methods, including absorption and marginal costing, and their implications for decision-making. The report concludes by summarizing the key findings and providing references.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

FROM: MANAGEMENT ACCOUNTING OFFICER..................................................................1

TO,...................................................................................................................................................1

GENERAL MANAGER..................................................................................................................1

ZYLLA COMPANY.......................................................................................................................1

SUB: MANAGEMENT ACCOUNTING SYSTEM .....................................................................1

INTORODUCTION........................................................................................................................1

TASK 1............................................................................................................................................1

P1............................................................................................................................................1

P2............................................................................................................................................4

M1...........................................................................................................................................5

TASK 2............................................................................................................................................6

P3............................................................................................................................................6

M2:.........................................................................................................................................8

D2:..........................................................................................................................................8

TASK 3............................................................................................................................................8

P4............................................................................................................................................8

M3.........................................................................................................................................10

D3.........................................................................................................................................10

TASK 4..........................................................................................................................................10

P5..........................................................................................................................................10

M4.........................................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

FROM: MANAGEMENT ACCOUNTING OFFICER..................................................................1

TO,...................................................................................................................................................1

GENERAL MANAGER..................................................................................................................1

ZYLLA COMPANY.......................................................................................................................1

SUB: MANAGEMENT ACCOUNTING SYSTEM .....................................................................1

INTORODUCTION........................................................................................................................1

TASK 1............................................................................................................................................1

P1............................................................................................................................................1

P2............................................................................................................................................4

M1...........................................................................................................................................5

TASK 2............................................................................................................................................6

P3............................................................................................................................................6

M2:.........................................................................................................................................8

D2:..........................................................................................................................................8

TASK 3............................................................................................................................................8

P4............................................................................................................................................8

M3.........................................................................................................................................10

D3.........................................................................................................................................10

TASK 4..........................................................................................................................................10

P5..........................................................................................................................................10

M4.........................................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

FROM: MANAGEMENT ACCOUNTING OFFICER

TO,

GENERAL MANAGER

ZYLLA COMPANY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTORODUCTION

Management accounting is the best tool which is used by each firm for making business

objectives achievable and obtainable. Management Accountant of Zylla Company uses various

techniques and concepts of management accounting, to make the accounting data more useful for

managerial decision-making. The technique of management accounting includes ratio analysis,

fund flow and cash flow statement, budgeting and forecasting etc. The main intent of

management accounting is to show the accounting information in such a manner as to help the

management of Zylla Company in planning and controlling the operations of a company’s

business in which Zylla Company is dealing with their customers (Renz, 2016). Under this

description various management accounting methods are used to make the accounting policies

for the company much stronger than their competitors who are available in the market. While

applying the management accounting methods & techniques in the company, the accountant of

Zylla Company need to know various advantages and disadvantages of Management

Accounting so that the firm can get the sustainability.

TASK 1

P1

Management Accounting is the presentation of accounting information in such a manner

as to help management of a company in the making of policy and day-to-day procedures of a

company. It covers all those services which the accountant of the company can assist top

management and other departments in the formulation of policy, the control of its execution and

1

TO,

GENERAL MANAGER

ZYLLA COMPANY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTORODUCTION

Management accounting is the best tool which is used by each firm for making business

objectives achievable and obtainable. Management Accountant of Zylla Company uses various

techniques and concepts of management accounting, to make the accounting data more useful for

managerial decision-making. The technique of management accounting includes ratio analysis,

fund flow and cash flow statement, budgeting and forecasting etc. The main intent of

management accounting is to show the accounting information in such a manner as to help the

management of Zylla Company in planning and controlling the operations of a company’s

business in which Zylla Company is dealing with their customers (Renz, 2016). Under this

description various management accounting methods are used to make the accounting policies

for the company much stronger than their competitors who are available in the market. While

applying the management accounting methods & techniques in the company, the accountant of

Zylla Company need to know various advantages and disadvantages of Management

Accounting so that the firm can get the sustainability.

TASK 1

P1

Management Accounting is the presentation of accounting information in such a manner

as to help management of a company in the making of policy and day-to-day procedures of a

company. It covers all those services which the accountant of the company can assist top

management and other departments in the formulation of policy, the control of its execution and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the appreciation of its effectiveness (Quinn, 2014). It emphasizes on future because decisions are

always take for future course of action. When this future turns into present, a critical

investigation is made and variances are ascertained to make corrective action. For this, budgetary

control, standard costing is the methods which highlights the future. The management accounting

is useful to improve the efficiency and also helpful to managers of different departments that

how much resources are available to them and according to these available resources they have

to accomplish their assign tasks.

The main difference between the Financial Accounting & Management Accounting is that

Financial Accounting in the sense that all the company transaction and events are expressed in

terms of money and management accepts them in the form of statements and reports.

Management accounting cannot replace financial accounting. It draws out a major

important part of the information from the financial accounting and changes the same for

managerial uses. Therefore, both the accounting is complementary to each other (Advanced

Management Accounting, 2017).

The scope of management accounting is most wide because financial accounting, cost

accounting and others techniques are used in it. Thus, financial accounting is part of management

accounting.

There are various techniques used in management accounting which are discussed below

Cost Accounting: Cost accounting is used to ascertain the cost of a product or service. In

this accounting, present and past events are used (Parker, 2012). Cost control, cost

analysis for decision-making and price determination are also objectives of cost

accounting. Under cost accounting various techniques is used to estimate the cost of a

particular product. The techniques are standard costing, marginal costing, budgetary

control, etc. Standard Costing is an important technique for cost control, which is one

main objective of management accounting. This involves the technique of determination

of standard costs, their comparison with actual cost and the analysis of the differences i.e.

variances to their causes and points of incidence.

Marginal costing is a managerial technique that considers only variable cost in the

additional introduction of output decisions. Marginal costing is helpful for management of

profitability of different products, departments and divisions of a company.

2

always take for future course of action. When this future turns into present, a critical

investigation is made and variances are ascertained to make corrective action. For this, budgetary

control, standard costing is the methods which highlights the future. The management accounting

is useful to improve the efficiency and also helpful to managers of different departments that

how much resources are available to them and according to these available resources they have

to accomplish their assign tasks.

The main difference between the Financial Accounting & Management Accounting is that

Financial Accounting in the sense that all the company transaction and events are expressed in

terms of money and management accepts them in the form of statements and reports.

Management accounting cannot replace financial accounting. It draws out a major

important part of the information from the financial accounting and changes the same for

managerial uses. Therefore, both the accounting is complementary to each other (Advanced

Management Accounting, 2017).

The scope of management accounting is most wide because financial accounting, cost

accounting and others techniques are used in it. Thus, financial accounting is part of management

accounting.

There are various techniques used in management accounting which are discussed below

Cost Accounting: Cost accounting is used to ascertain the cost of a product or service. In

this accounting, present and past events are used (Parker, 2012). Cost control, cost

analysis for decision-making and price determination are also objectives of cost

accounting. Under cost accounting various techniques is used to estimate the cost of a

particular product. The techniques are standard costing, marginal costing, budgetary

control, etc. Standard Costing is an important technique for cost control, which is one

main objective of management accounting. This involves the technique of determination

of standard costs, their comparison with actual cost and the analysis of the differences i.e.

variances to their causes and points of incidence.

Marginal costing is a managerial technique that considers only variable cost in the

additional introduction of output decisions. Marginal costing is helpful for management of

profitability of different products, departments and divisions of a company.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budgetary control refers to a system of business control that uses budgets to control the

important activities of business. In this continuous comparison are made with actual figure with

budgeted figure.

Inventory Management System: It is an inventory planning which covers the task of

development and administration of policies, systems and procedures which minimize

total costs relating to inventory decisions and related functions such as customer service

requirements, production programming, purchasing and so many things. A well-

developed inventory system precaution to provide the management detailed and up-to-

date information that helps in production planning and control. Inventory control signifies

a planned approach of ascertaining when to indent, what to indent, how much to

inventory so that costs involving purchasing and storing are optimally reduce without

interrupting production and also not affecting sales. To solve these problems of inventory

management various techniques have been evolved by company. These techniques are

EOQ (Economic Order Qty.), Re-Order Level, Fixing Stock Levels, Etc.

Financial Analysis: Financial analysis is an attempt to determine the significance and

meaning of financial statement data so that a forecast for future may be made of the

prospects for earning in a future. The analysis and interpretation of financial statements

helps the manager to present the information to the business executives, investors and

creditors of a company (Papaspyropoulos and et. al., 2012).

The techniques of financial analysis include the following:

Comparative statements and trend analysis

Ratio analysis

Funds flow analysis

Cash flow analysis

Financial analysis helps the Accountant to analysis the performance of the company in all

aspects because he has techniques and with the help of these he can make future suggestions to

the top management. If the financial position of a company is good, the company makes payment

to debt and pay dividend to the shareholders.

P2

There are various methods or manners which are used by the company to raise the

lucrativeness. This can be done by healthy reporting system of a company in which a manger

3

important activities of business. In this continuous comparison are made with actual figure with

budgeted figure.

Inventory Management System: It is an inventory planning which covers the task of

development and administration of policies, systems and procedures which minimize

total costs relating to inventory decisions and related functions such as customer service

requirements, production programming, purchasing and so many things. A well-

developed inventory system precaution to provide the management detailed and up-to-

date information that helps in production planning and control. Inventory control signifies

a planned approach of ascertaining when to indent, what to indent, how much to

inventory so that costs involving purchasing and storing are optimally reduce without

interrupting production and also not affecting sales. To solve these problems of inventory

management various techniques have been evolved by company. These techniques are

EOQ (Economic Order Qty.), Re-Order Level, Fixing Stock Levels, Etc.

Financial Analysis: Financial analysis is an attempt to determine the significance and

meaning of financial statement data so that a forecast for future may be made of the

prospects for earning in a future. The analysis and interpretation of financial statements

helps the manager to present the information to the business executives, investors and

creditors of a company (Papaspyropoulos and et. al., 2012).

The techniques of financial analysis include the following:

Comparative statements and trend analysis

Ratio analysis

Funds flow analysis

Cash flow analysis

Financial analysis helps the Accountant to analysis the performance of the company in all

aspects because he has techniques and with the help of these he can make future suggestions to

the top management. If the financial position of a company is good, the company makes payment

to debt and pay dividend to the shareholders.

P2

There are various methods or manners which are used by the company to raise the

lucrativeness. This can be done by healthy reporting system of a company in which a manger

3

records each and every transaction related to the company with the fairness and without any

fraud in transactions. All these transactions are made by and getting helped by the financial

statement of a company, which present truthfulness about the company financial position. With

help to these financial reports a company manager makes strategies and business policy for a

company (Otley and Emmanuel, 2013). Past data also useful for the manger while making the

strategy. With the past mistake company in future cannot repeat this mistake. The investment

decisions are based on these reports and financial statement of a company. If a company have a

sufficient money, they invest this money in their projects and paying the debts and also to their

creditors and also helpful to declare the interim dividend to their shareholders.

Good financial strategy helps the company to survive in the highly competitive market

and compete with their competitors. Having good finance company can import the latest

technology machines and equipment’s.

There are many financial reporting systems which are used by a company and a some reporting

system are discussed below:

Performance Reporting System: In this system past and present performance are

evaluated. If the present performance is better than the past, than there is no need to take

corrective measures and this performance is helpful for future, while making the report

for the future (Morales and Lambert, 2013). If there is any deviation occurs between

these performances the corrective action taken by the manager and this mistake cannot

repeat in the future and this mistake occurs when the past is better than the future.

Performance measures helpful to the manger in making the future report for the company.

Operational Reporting: In this reporting system the operations related to a

manufacturing is reported. It is basically for the manufacturing industries because they do

operations on regular basis. In this reporting industry operations are evaluated and

overseen by the manager of the industry. The actual cost with the standard cost is

measured by the manager for the product which is manufactured.

Job Costing Reporting: This is a competent technique used by the manager of a

manufacturing company to analyses the actual cost incurred on a particular job. Like how

much labor cost incurred, how much raw material used in a job and manufacturing

expenses related to the job are disclosed in a reporting to the senior manager of the

company.

4

fraud in transactions. All these transactions are made by and getting helped by the financial

statement of a company, which present truthfulness about the company financial position. With

help to these financial reports a company manager makes strategies and business policy for a

company (Otley and Emmanuel, 2013). Past data also useful for the manger while making the

strategy. With the past mistake company in future cannot repeat this mistake. The investment

decisions are based on these reports and financial statement of a company. If a company have a

sufficient money, they invest this money in their projects and paying the debts and also to their

creditors and also helpful to declare the interim dividend to their shareholders.

Good financial strategy helps the company to survive in the highly competitive market

and compete with their competitors. Having good finance company can import the latest

technology machines and equipment’s.

There are many financial reporting systems which are used by a company and a some reporting

system are discussed below:

Performance Reporting System: In this system past and present performance are

evaluated. If the present performance is better than the past, than there is no need to take

corrective measures and this performance is helpful for future, while making the report

for the future (Morales and Lambert, 2013). If there is any deviation occurs between

these performances the corrective action taken by the manager and this mistake cannot

repeat in the future and this mistake occurs when the past is better than the future.

Performance measures helpful to the manger in making the future report for the company.

Operational Reporting: In this reporting system the operations related to a

manufacturing is reported. It is basically for the manufacturing industries because they do

operations on regular basis. In this reporting industry operations are evaluated and

overseen by the manager of the industry. The actual cost with the standard cost is

measured by the manager for the product which is manufactured.

Job Costing Reporting: This is a competent technique used by the manager of a

manufacturing company to analyses the actual cost incurred on a particular job. Like how

much labor cost incurred, how much raw material used in a job and manufacturing

expenses related to the job are disclosed in a reporting to the senior manager of the

company.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory/ Stock Management Reporting: In this reporting, manager report that how

much inventories are there in a manufacturing unit and also state that how much closing

stock are available in the store (Lukka and Modell, 2010). In his report he also gives

information to the purchase department that how much stocks are needed in future and

how much are available in the present. Manager also sees that there is an effective

utilization of the stock in a proper way or not and also sees the working of the labor that

the labor misuses the raw material or wastes them. In this reporting manager tells

everything in a state manner to the concern departments.

Account Receivable Report: This is receivable report tells about that how much

company have a debtors and in these debtors how much they are bad-debts. This

reporting helps the manager that how much money will come in future or not. And also

help to record that how much money comes from the bills which are drawn.

M1

Advantages Of Implementing The Management Accounting: Management accounting helps

the firm to gain the sustainability and also used in the firm for getting its pre-set targets.

1. It helps in proper planning for financial resources of a company.

2. The tools & techniques of management accounting are helpful to the management

in controlling the activities of the company (Luft and Shields, 2010).

3. It also increases the profitability to the company, while reducing the cost in

production and also eliminating the wastages.

4. The techniques of budgetary control & standard costing help management in

evaluating the performance of different departments, persons, machines etc. in the

company.

5. Better customer services given with the help of management accounting.

TASK 2

P3

Costing: This is a system which is assigned the cost on the every element of a business in which

a company dealing. Costing is generally used to develop costs for any or all the following:

- Customers

- Distribution Channels

5

much inventories are there in a manufacturing unit and also state that how much closing

stock are available in the store (Lukka and Modell, 2010). In his report he also gives

information to the purchase department that how much stocks are needed in future and

how much are available in the present. Manager also sees that there is an effective

utilization of the stock in a proper way or not and also sees the working of the labor that

the labor misuses the raw material or wastes them. In this reporting manager tells

everything in a state manner to the concern departments.

Account Receivable Report: This is receivable report tells about that how much

company have a debtors and in these debtors how much they are bad-debts. This

reporting helps the manager that how much money will come in future or not. And also

help to record that how much money comes from the bills which are drawn.

M1

Advantages Of Implementing The Management Accounting: Management accounting helps

the firm to gain the sustainability and also used in the firm for getting its pre-set targets.

1. It helps in proper planning for financial resources of a company.

2. The tools & techniques of management accounting are helpful to the management

in controlling the activities of the company (Luft and Shields, 2010).

3. It also increases the profitability to the company, while reducing the cost in

production and also eliminating the wastages.

4. The techniques of budgetary control & standard costing help management in

evaluating the performance of different departments, persons, machines etc. in the

company.

5. Better customer services given with the help of management accounting.

TASK 2

P3

Costing: This is a system which is assigned the cost on the every element of a business in which

a company dealing. Costing is generally used to develop costs for any or all the following:

- Customers

- Distribution Channels

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

- Products

- Geographic regions where the company has a business or wants to establish their

business.

- Product lines offering by the company

- Manufacturing processes

Costing is also including the assignment of fixed costs, which are same, irrespective of the level

of production. This type of costing is called as absorption costing.

The costing helpful to the manger of a company to assign the cost on the

product while using the techniques of the costing.

Absorption Costing: It is a managerial accounting cost method of expensing under which all the

cost associated with manufacturing units are considered. Some of the direct costs are associated

with manufacturing a product include wages for labor , raw materials used in a product and other

overhead costs used in producing the goods. Absorption costing includes anything that is direct

cost in producing a good as the cost base.

Marginal Costing:Marginal cost is the up or down in the total production cost if output is

increased by one more unit. Marginal costs are variable costs including labor and material costs;

add an estimated portion of fixed costs such as administration expenses and selling expenses. It

helps profit planning through break-even point charts and profit which is plotted in the graph.

Comparative profitability can easily be assessed and brought to the notice of the management of

a company for decision- making.

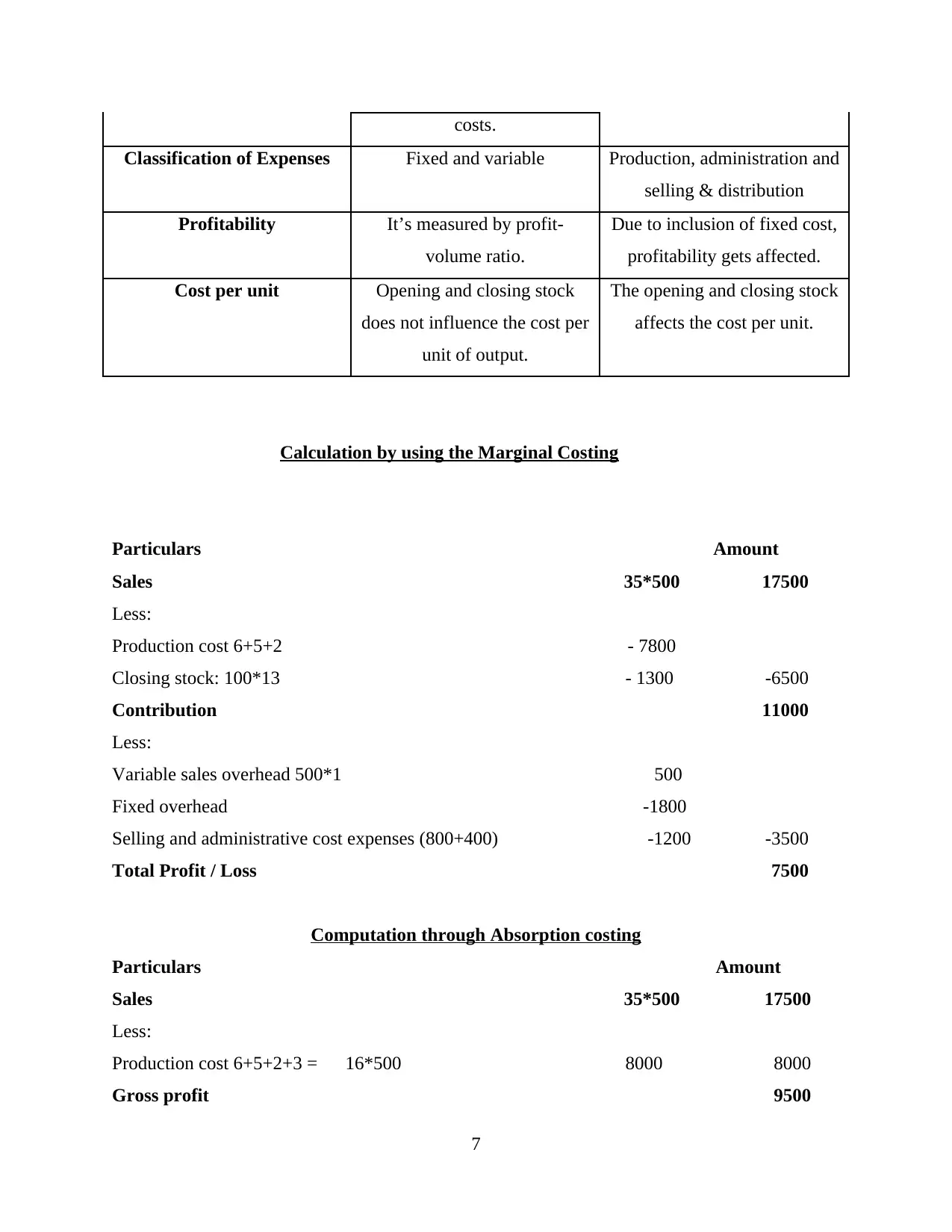

Key difference Between marginal costing and absorption costing:

BASIS FOR

COMPARISON

MARGINAL COSTING ABSORPTION COSTING

Meaning A decision-making tool for

ascertaining the total cost of

production.

Apportionment of the total

costs to the cost centre in order

to determine the total cost of

the production.

Cost Recognition The variable cost is considered

as product cost while fixed

cost is considered as period

Both fixed and variable cost is

considered as product cost.

6

- Geographic regions where the company has a business or wants to establish their

business.

- Product lines offering by the company

- Manufacturing processes

Costing is also including the assignment of fixed costs, which are same, irrespective of the level

of production. This type of costing is called as absorption costing.

The costing helpful to the manger of a company to assign the cost on the

product while using the techniques of the costing.

Absorption Costing: It is a managerial accounting cost method of expensing under which all the

cost associated with manufacturing units are considered. Some of the direct costs are associated

with manufacturing a product include wages for labor , raw materials used in a product and other

overhead costs used in producing the goods. Absorption costing includes anything that is direct

cost in producing a good as the cost base.

Marginal Costing:Marginal cost is the up or down in the total production cost if output is

increased by one more unit. Marginal costs are variable costs including labor and material costs;

add an estimated portion of fixed costs such as administration expenses and selling expenses. It

helps profit planning through break-even point charts and profit which is plotted in the graph.

Comparative profitability can easily be assessed and brought to the notice of the management of

a company for decision- making.

Key difference Between marginal costing and absorption costing:

BASIS FOR

COMPARISON

MARGINAL COSTING ABSORPTION COSTING

Meaning A decision-making tool for

ascertaining the total cost of

production.

Apportionment of the total

costs to the cost centre in order

to determine the total cost of

the production.

Cost Recognition The variable cost is considered

as product cost while fixed

cost is considered as period

Both fixed and variable cost is

considered as product cost.

6

costs.

Classification of Expenses Fixed and variable Production, administration and

selling & distribution

Profitability It’s measured by profit-

volume ratio.

Due to inclusion of fixed cost,

profitability gets affected.

Cost per unit Opening and closing stock

does not influence the cost per

unit of output.

The opening and closing stock

affects the cost per unit.

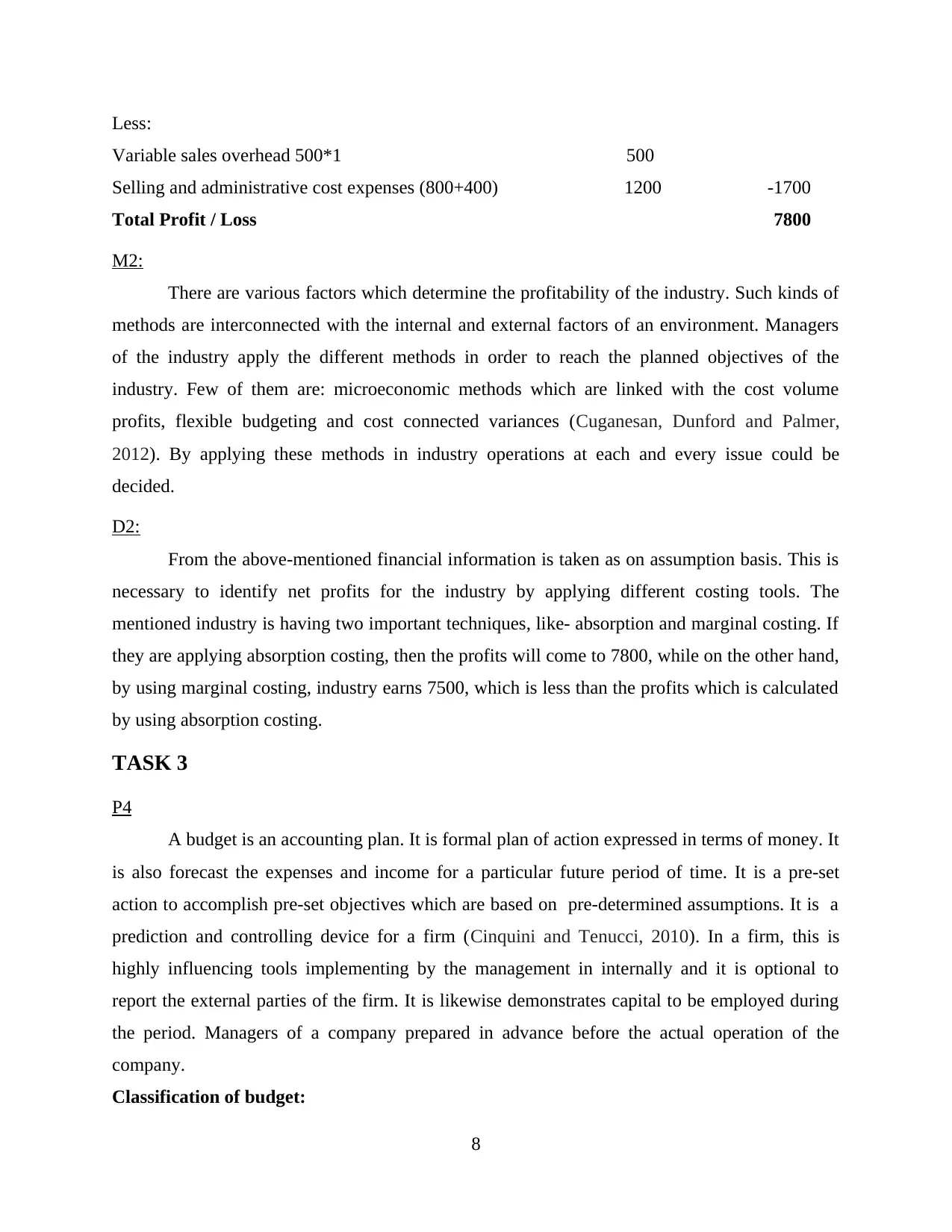

Calculation by using the Marginal Costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Computation through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500 8000 8000

Gross profit 9500

7

Classification of Expenses Fixed and variable Production, administration and

selling & distribution

Profitability It’s measured by profit-

volume ratio.

Due to inclusion of fixed cost,

profitability gets affected.

Cost per unit Opening and closing stock

does not influence the cost per

unit of output.

The opening and closing stock

affects the cost per unit.

Calculation by using the Marginal Costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Computation through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500 8000 8000

Gross profit 9500

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

M2:

There are various factors which determine the profitability of the industry. Such kinds of

methods are interconnected with the internal and external factors of an environment. Managers

of the industry apply the different methods in order to reach the planned objectives of the

industry. Few of them are: microeconomic methods which are linked with the cost volume

profits, flexible budgeting and cost connected variances (Cuganesan, Dunford and Palmer,

2012). By applying these methods in industry operations at each and every issue could be

decided.

D2:

From the above-mentioned financial information is taken as on assumption basis. This is

necessary to identify net profits for the industry by applying different costing tools. The

mentioned industry is having two important techniques, like- absorption and marginal costing. If

they are applying absorption costing, then the profits will come to 7800, while on the other hand,

by using marginal costing, industry earns 7500, which is less than the profits which is calculated

by using absorption costing.

TASK 3

P4

A budget is an accounting plan. It is formal plan of action expressed in terms of money. It

is also forecast the expenses and income for a particular future period of time. It is a pre-set

action to accomplish pre-set objectives which are based on pre-determined assumptions. It is a

prediction and controlling device for a firm (Cinquini and Tenucci, 2010). In a firm, this is

highly influencing tools implementing by the management in internally and it is optional to

report the external parties of the firm. It is likewise demonstrates capital to be employed during

the period. Managers of a company prepared in advance before the actual operation of the

company.

Classification of budget:

8

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

M2:

There are various factors which determine the profitability of the industry. Such kinds of

methods are interconnected with the internal and external factors of an environment. Managers

of the industry apply the different methods in order to reach the planned objectives of the

industry. Few of them are: microeconomic methods which are linked with the cost volume

profits, flexible budgeting and cost connected variances (Cuganesan, Dunford and Palmer,

2012). By applying these methods in industry operations at each and every issue could be

decided.

D2:

From the above-mentioned financial information is taken as on assumption basis. This is

necessary to identify net profits for the industry by applying different costing tools. The

mentioned industry is having two important techniques, like- absorption and marginal costing. If

they are applying absorption costing, then the profits will come to 7800, while on the other hand,

by using marginal costing, industry earns 7500, which is less than the profits which is calculated

by using absorption costing.

TASK 3

P4

A budget is an accounting plan. It is formal plan of action expressed in terms of money. It

is also forecast the expenses and income for a particular future period of time. It is a pre-set

action to accomplish pre-set objectives which are based on pre-determined assumptions. It is a

prediction and controlling device for a firm (Cinquini and Tenucci, 2010). In a firm, this is

highly influencing tools implementing by the management in internally and it is optional to

report the external parties of the firm. It is likewise demonstrates capital to be employed during

the period. Managers of a company prepared in advance before the actual operation of the

company.

Classification of budget:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Production Budget: This budget is made by estimated production for budget period.

normally, the production budget is totally depends on the sales budget. During

incorporating budget, the production manager will believe the physical availability like

plant, power, raw materials and labor. Production budget of a company for attaining the

sales target.

Purchase Budget: This includes direct and indirect material while preparing this. The

purchasing budget might be expressed in monetary or quantity term. It enables

purchasing division to plan its operations with in a time frame in repeat of purchases so

that long-term forward contracts can be configured (Cadez and Guilding, 2012).

Cash budget: This is the estimated cash inflow and outflow over a specific period of

time. It is crucial and one of the last to be made. This is detailed projection and the

resultants cash balance while preparing the budget. This helps the management for

identify the future liquidity needs of the firm, estimation for business of those

requirement, exercising control over cash. So, cash budget could play a vast role in the

firm.

There are so many forecasting tools that can be help for the firm for budgetary control: some of

them are discussed hereunder:

Forecasting Tool: This tool is used by the management of company to forecast about the

internal and external factors which affects the business activities to make effective strategies and

plans which enhance the ability of company to perform their functions. By using such tools and

techniques, manager of company can easily prepare different reports and budgets which are

working as standards which guides different activities of employees. This enables them to

perform their activities with the help of such standards and achieve their targets effectively. Such

forecasting about future actions helps in preparation of different budgets which helps in

allocation of resources according to that and control the budgets of company efficiently. This can

also be called as planning tool which helps in plan about future actions. This includes the

forecast about cash flow, industry association, production chart etc. This can be defined below:

Cash flow statements: This is the important forecasting tool which is used by the

management of company to planning about cash needs of the different departments of

company in effectively operate their functions (Burritt and Schaltegger, 2010). This helps

in identification of the need of cash in payment of their bills when there is chance

9

normally, the production budget is totally depends on the sales budget. During

incorporating budget, the production manager will believe the physical availability like

plant, power, raw materials and labor. Production budget of a company for attaining the

sales target.

Purchase Budget: This includes direct and indirect material while preparing this. The

purchasing budget might be expressed in monetary or quantity term. It enables

purchasing division to plan its operations with in a time frame in repeat of purchases so

that long-term forward contracts can be configured (Cadez and Guilding, 2012).

Cash budget: This is the estimated cash inflow and outflow over a specific period of

time. It is crucial and one of the last to be made. This is detailed projection and the

resultants cash balance while preparing the budget. This helps the management for

identify the future liquidity needs of the firm, estimation for business of those

requirement, exercising control over cash. So, cash budget could play a vast role in the

firm.

There are so many forecasting tools that can be help for the firm for budgetary control: some of

them are discussed hereunder:

Forecasting Tool: This tool is used by the management of company to forecast about the

internal and external factors which affects the business activities to make effective strategies and

plans which enhance the ability of company to perform their functions. By using such tools and

techniques, manager of company can easily prepare different reports and budgets which are

working as standards which guides different activities of employees. This enables them to

perform their activities with the help of such standards and achieve their targets effectively. Such

forecasting about future actions helps in preparation of different budgets which helps in

allocation of resources according to that and control the budgets of company efficiently. This can

also be called as planning tool which helps in plan about future actions. This includes the

forecast about cash flow, industry association, production chart etc. This can be defined below:

Cash flow statements: This is the important forecasting tool which is used by the

management of company to planning about cash needs of the different departments of

company in effectively operate their functions (Burritt and Schaltegger, 2010). This helps

in identification of the need of cash in payment of their bills when there is chance

9

regrading arrival of receivables. This helps in preparation of entire annual budget by

expecting income from the sales activities of business. This contributes in effective

performance of their function and timely make payment to their suppliers and ensure that

can pay the bills on time.

Situational Tool: This includes such tools and techniques which is used by the management of

company to understand about the situations which are present and going to happen in future. This

helps in preparation of different plans which provides strength to deal with such situations

effectively and achieve their desired results. This is the planning tool which is used to make

future actions and provides the solutions regarding problems faced by employees during

performance of their work. It includes many tools which are used for situational analysis like

SWOT analysis, PESTLE analysis etc. This helps in identification of their strength and

weaknesses control use of different resources which increase their cost of production. Such

analysis helps in effective allocation and optimum utilisation of their available resources to

achieve desired result at minimum cost. So, this analysis work as budgetary control tool which

helps the manager to control their cost and expenses by plan their future actions (Boyns and

Edwards, 2013).

M3

From this report, this has been examined that the company needs to follow different

planning methods, so that it can achieve its pre-set objectives and goals. However, this is the

most important method for taking advantage in the uninterrupted development of a company

financial position. With the help of different planning methods, company can measure their

financial strength and weakness by forecasting budget in an efficient and effective way.

D3

With the help of planning methods, a company could decide the financial related troubles

in a competent manner. The above referred planning methods are helpful to solve the financial

troubles, so that the Zylla Company could get uninterrupted development.

TASK 4

P5

In a Zylla Company, this is determined that profitability could increase by applying a

sufficient tools and techniques. There are many tools and techniques which can be used by the

10

expecting income from the sales activities of business. This contributes in effective

performance of their function and timely make payment to their suppliers and ensure that

can pay the bills on time.

Situational Tool: This includes such tools and techniques which is used by the management of

company to understand about the situations which are present and going to happen in future. This

helps in preparation of different plans which provides strength to deal with such situations

effectively and achieve their desired results. This is the planning tool which is used to make

future actions and provides the solutions regarding problems faced by employees during

performance of their work. It includes many tools which are used for situational analysis like

SWOT analysis, PESTLE analysis etc. This helps in identification of their strength and

weaknesses control use of different resources which increase their cost of production. Such

analysis helps in effective allocation and optimum utilisation of their available resources to

achieve desired result at minimum cost. So, this analysis work as budgetary control tool which

helps the manager to control their cost and expenses by plan their future actions (Boyns and

Edwards, 2013).

M3

From this report, this has been examined that the company needs to follow different

planning methods, so that it can achieve its pre-set objectives and goals. However, this is the

most important method for taking advantage in the uninterrupted development of a company

financial position. With the help of different planning methods, company can measure their

financial strength and weakness by forecasting budget in an efficient and effective way.

D3

With the help of planning methods, a company could decide the financial related troubles

in a competent manner. The above referred planning methods are helpful to solve the financial

troubles, so that the Zylla Company could get uninterrupted development.

TASK 4

P5

In a Zylla Company, this is determined that profitability could increase by applying a

sufficient tools and techniques. There are many tools and techniques which can be used by the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.