ABC's Financial Performance and Budgeting Process

VerifiedAdded on 2023/01/10

|9

|1989

|69

AI Summary

This document discusses ABC's financial performance using management accounting techniques such as margin analysis and product costing. It also explores the budgeting process, including forecasting, planning, and communication. The advantages and disadvantages of operating a budgetary control system are examined. The document provides insights into budgetary planning and control, including the different categories of budgets. The case of ABC Ltd and its budgeting process is analyzed.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1

Assignment Brief Number 2

Assignment Brief Number 2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

Contents

Part A: ABC’s Financial Performance through using various management accounting techniques

.........................................................................................................................................................3

Part B: Budgeting Process...............................................................................................................3

Major Functions of the Budgeting Process..................................................................................3

Advantages and disadvantages in operating a budgetary control system....................................4

Part C: Budgetary Planning.............................................................................................................4

Different categories of budgets on the given information as under:............................................4

Part D: Budgetary Control...............................................................................................................7

Contents

Part A: ABC’s Financial Performance through using various management accounting techniques

.........................................................................................................................................................3

Part B: Budgeting Process...............................................................................................................3

Major Functions of the Budgeting Process..................................................................................3

Advantages and disadvantages in operating a budgetary control system....................................4

Part C: Budgetary Planning.............................................................................................................4

Different categories of budgets on the given information as under:............................................4

Part D: Budgetary Control...............................................................................................................7

3

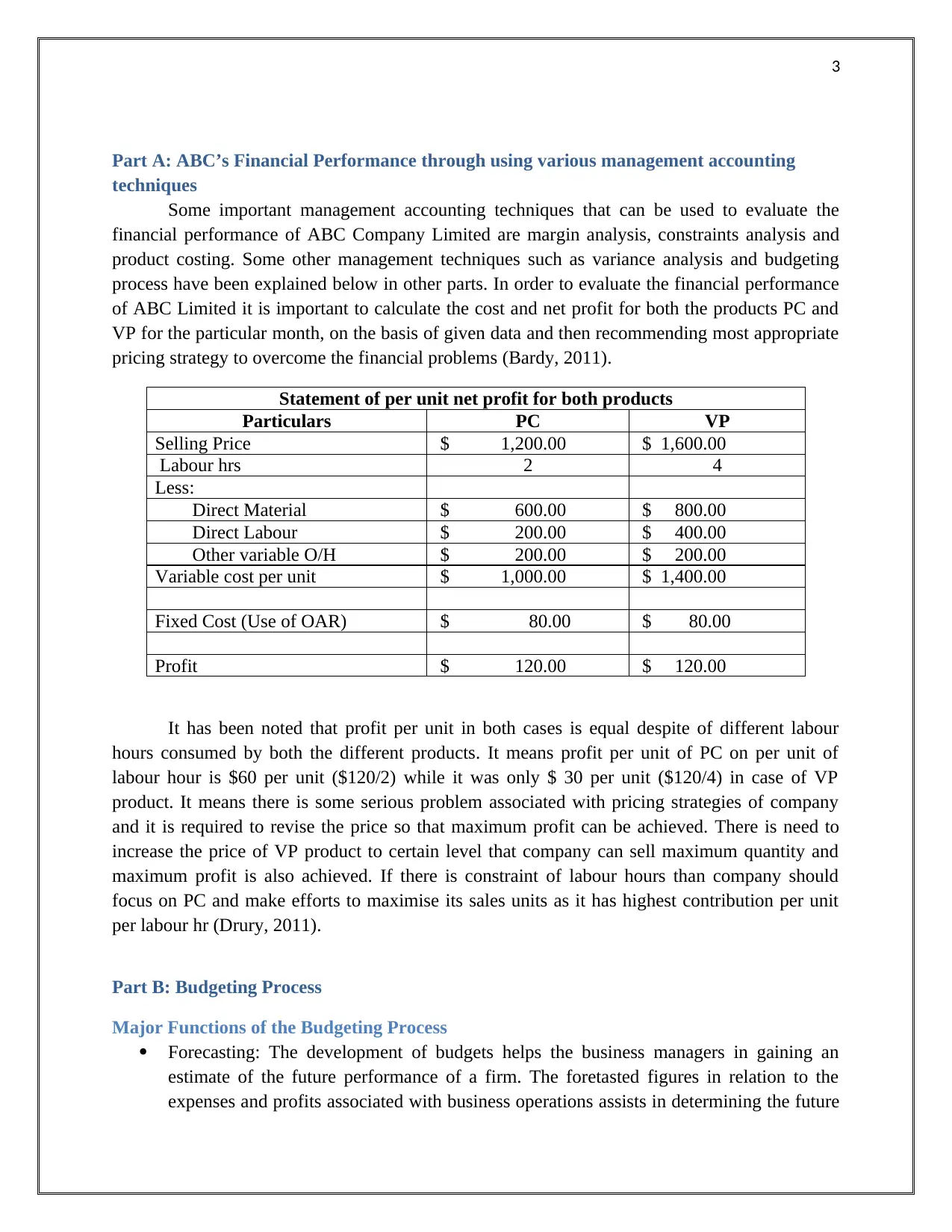

Part A: ABC’s Financial Performance through using various management accounting

techniques

Some important management accounting techniques that can be used to evaluate the

financial performance of ABC Company Limited are margin analysis, constraints analysis and

product costing. Some other management techniques such as variance analysis and budgeting

process have been explained below in other parts. In order to evaluate the financial performance

of ABC Limited it is important to calculate the cost and net profit for both the products PC and

VP for the particular month, on the basis of given data and then recommending most appropriate

pricing strategy to overcome the financial problems (Bardy, 2011).

Statement of per unit net profit for both products

Particulars PC VP

Selling Price $ 1,200.00 $ 1,600.00

Labour hrs 2 4

Less:

Direct Material $ 600.00 $ 800.00

Direct Labour $ 200.00 $ 400.00

Other variable O/H $ 200.00 $ 200.00

Variable cost per unit $ 1,000.00 $ 1,400.00

Fixed Cost (Use of OAR) $ 80.00 $ 80.00

Profit $ 120.00 $ 120.00

It has been noted that profit per unit in both cases is equal despite of different labour

hours consumed by both the different products. It means profit per unit of PC on per unit of

labour hour is $60 per unit ($120/2) while it was only $ 30 per unit ($120/4) in case of VP

product. It means there is some serious problem associated with pricing strategies of company

and it is required to revise the price so that maximum profit can be achieved. There is need to

increase the price of VP product to certain level that company can sell maximum quantity and

maximum profit is also achieved. If there is constraint of labour hours than company should

focus on PC and make efforts to maximise its sales units as it has highest contribution per unit

per labour hr (Drury, 2011).

Part B: Budgeting Process

Major Functions of the Budgeting Process

Forecasting: The development of budgets helps the business managers in gaining an

estimate of the future performance of a firm. The foretasted figures in relation to the

expenses and profits associated with business operations assists in determining the future

Part A: ABC’s Financial Performance through using various management accounting

techniques

Some important management accounting techniques that can be used to evaluate the

financial performance of ABC Company Limited are margin analysis, constraints analysis and

product costing. Some other management techniques such as variance analysis and budgeting

process have been explained below in other parts. In order to evaluate the financial performance

of ABC Limited it is important to calculate the cost and net profit for both the products PC and

VP for the particular month, on the basis of given data and then recommending most appropriate

pricing strategy to overcome the financial problems (Bardy, 2011).

Statement of per unit net profit for both products

Particulars PC VP

Selling Price $ 1,200.00 $ 1,600.00

Labour hrs 2 4

Less:

Direct Material $ 600.00 $ 800.00

Direct Labour $ 200.00 $ 400.00

Other variable O/H $ 200.00 $ 200.00

Variable cost per unit $ 1,000.00 $ 1,400.00

Fixed Cost (Use of OAR) $ 80.00 $ 80.00

Profit $ 120.00 $ 120.00

It has been noted that profit per unit in both cases is equal despite of different labour

hours consumed by both the different products. It means profit per unit of PC on per unit of

labour hour is $60 per unit ($120/2) while it was only $ 30 per unit ($120/4) in case of VP

product. It means there is some serious problem associated with pricing strategies of company

and it is required to revise the price so that maximum profit can be achieved. There is need to

increase the price of VP product to certain level that company can sell maximum quantity and

maximum profit is also achieved. If there is constraint of labour hours than company should

focus on PC and make efforts to maximise its sales units as it has highest contribution per unit

per labour hr (Drury, 2011).

Part B: Budgeting Process

Major Functions of the Budgeting Process

Forecasting: The development of budgets helps the business managers in gaining an

estimate of the future performance of a firm. The foretasted figures in relation to the

expenses and profits associated with business operations assists in determining the future

4

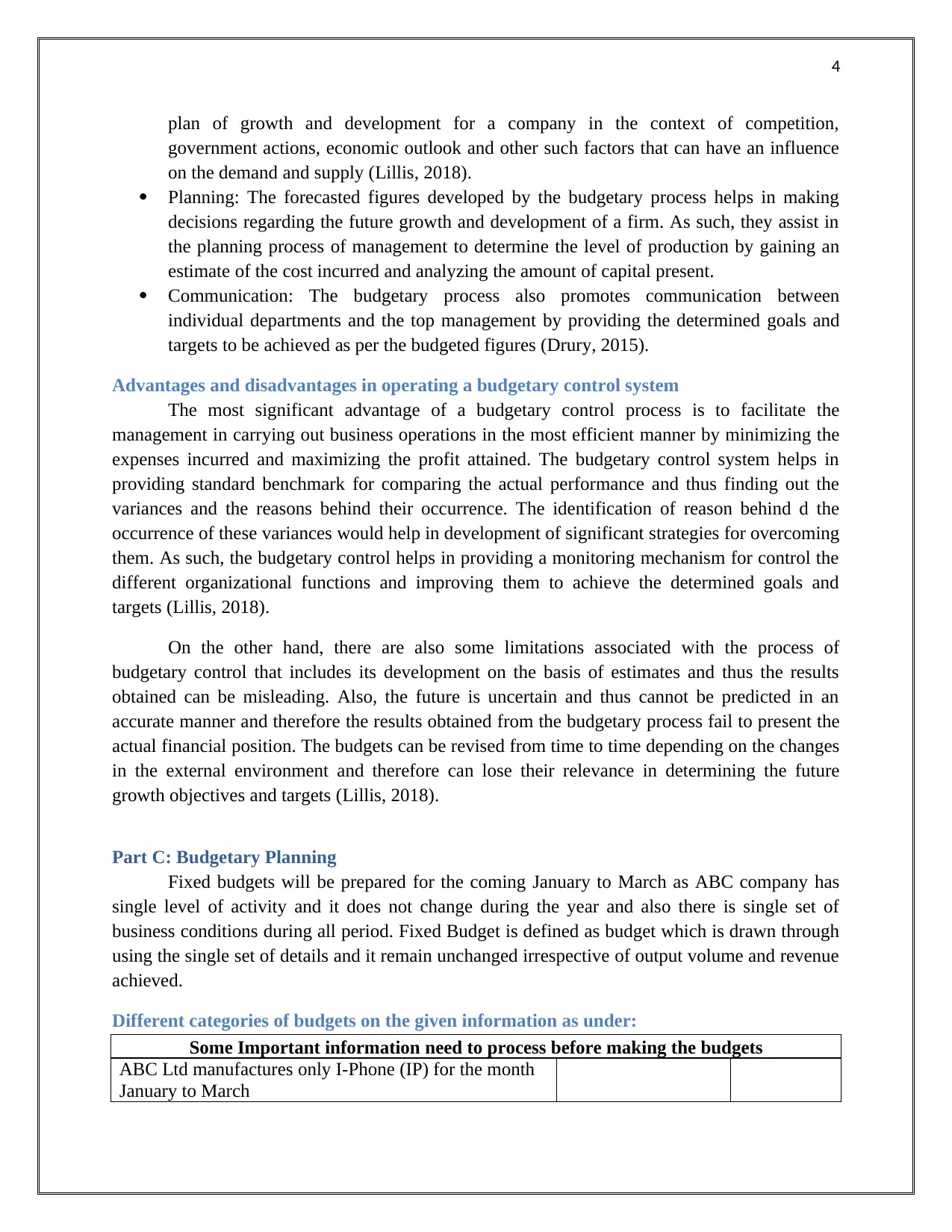

plan of growth and development for a company in the context of competition,

government actions, economic outlook and other such factors that can have an influence

on the demand and supply (Lillis, 2018).

Planning: The forecasted figures developed by the budgetary process helps in making

decisions regarding the future growth and development of a firm. As such, they assist in

the planning process of management to determine the level of production by gaining an

estimate of the cost incurred and analyzing the amount of capital present.

Communication: The budgetary process also promotes communication between

individual departments and the top management by providing the determined goals and

targets to be achieved as per the budgeted figures (Drury, 2015).

Advantages and disadvantages in operating a budgetary control system

The most significant advantage of a budgetary control process is to facilitate the

management in carrying out business operations in the most efficient manner by minimizing the

expenses incurred and maximizing the profit attained. The budgetary control system helps in

providing standard benchmark for comparing the actual performance and thus finding out the

variances and the reasons behind their occurrence. The identification of reason behind d the

occurrence of these variances would help in development of significant strategies for overcoming

them. As such, the budgetary control helps in providing a monitoring mechanism for control the

different organizational functions and improving them to achieve the determined goals and

targets (Lillis, 2018).

On the other hand, there are also some limitations associated with the process of

budgetary control that includes its development on the basis of estimates and thus the results

obtained can be misleading. Also, the future is uncertain and thus cannot be predicted in an

accurate manner and therefore the results obtained from the budgetary process fail to present the

actual financial position. The budgets can be revised from time to time depending on the changes

in the external environment and therefore can lose their relevance in determining the future

growth objectives and targets (Lillis, 2018).

Part C: Budgetary Planning

Fixed budgets will be prepared for the coming January to March as ABC company has

single level of activity and it does not change during the year and also there is single set of

business conditions during all period. Fixed Budget is defined as budget which is drawn through

using the single set of details and it remain unchanged irrespective of output volume and revenue

achieved.

Different categories of budgets on the given information as under:

Some Important information need to process before making the budgets

ABC Ltd manufactures only I-Phone (IP) for the month

January to March

plan of growth and development for a company in the context of competition,

government actions, economic outlook and other such factors that can have an influence

on the demand and supply (Lillis, 2018).

Planning: The forecasted figures developed by the budgetary process helps in making

decisions regarding the future growth and development of a firm. As such, they assist in

the planning process of management to determine the level of production by gaining an

estimate of the cost incurred and analyzing the amount of capital present.

Communication: The budgetary process also promotes communication between

individual departments and the top management by providing the determined goals and

targets to be achieved as per the budgeted figures (Drury, 2015).

Advantages and disadvantages in operating a budgetary control system

The most significant advantage of a budgetary control process is to facilitate the

management in carrying out business operations in the most efficient manner by minimizing the

expenses incurred and maximizing the profit attained. The budgetary control system helps in

providing standard benchmark for comparing the actual performance and thus finding out the

variances and the reasons behind their occurrence. The identification of reason behind d the

occurrence of these variances would help in development of significant strategies for overcoming

them. As such, the budgetary control helps in providing a monitoring mechanism for control the

different organizational functions and improving them to achieve the determined goals and

targets (Lillis, 2018).

On the other hand, there are also some limitations associated with the process of

budgetary control that includes its development on the basis of estimates and thus the results

obtained can be misleading. Also, the future is uncertain and thus cannot be predicted in an

accurate manner and therefore the results obtained from the budgetary process fail to present the

actual financial position. The budgets can be revised from time to time depending on the changes

in the external environment and therefore can lose their relevance in determining the future

growth objectives and targets (Lillis, 2018).

Part C: Budgetary Planning

Fixed budgets will be prepared for the coming January to March as ABC company has

single level of activity and it does not change during the year and also there is single set of

business conditions during all period. Fixed Budget is defined as budget which is drawn through

using the single set of details and it remain unchanged irrespective of output volume and revenue

achieved.

Different categories of budgets on the given information as under:

Some Important information need to process before making the budgets

ABC Ltd manufactures only I-Phone (IP) for the month

January to March

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

Estimated Contribution $ 600.00 per unit

Month Units Sales

January 3000

February 3000

March 4000

Total Production Cost (Variable Cost + Fixed Cost) $ 200.00

Variable Cost (Direct Material Only) ($70*2) $ 140.00

Each unit of IP requires raw material units of 2 units

Cost of each raw material unit $ 70.00

Actual Sales of previous month December 2500 Units

Raw material units purchased in last December 50000 Units

Raw material consumed in December 5000 Units

Raw material stock remain as on 1st January 45000 Units

Selling Price of each unit of IP

Contribution +

Variable Cost

Selling Price of each unit of IP $600+$140

$

740.00

Sales Budget

Particulars January February March

Unit Sold 3000 3000 4000

Unit Selling price

$

740.00

$

740.00

$

740.00

Total Sales

$

2,220,000.00

$

2,220,000.00

$

2,960,000.00

(Lucey, 2013)

Cash collection budget from sales

Particulars January February March

Total Sales $ 2,220,000.00 $ 2,220,000.00 $ 2,960,000.00

Cash Collected

40% in current month $ 888,000.00 $ 888,000.00 $ 1,184,000.00

60% in following month

(2500 units sold in

December) $ 1,110,000.00 $ 1,332,000.00 $ 1,332,000.00

Total Cash Collections $ 1,998,000.00 $ 2,220,000.00 $ 2,516,000.00

Estimated Contribution $ 600.00 per unit

Month Units Sales

January 3000

February 3000

March 4000

Total Production Cost (Variable Cost + Fixed Cost) $ 200.00

Variable Cost (Direct Material Only) ($70*2) $ 140.00

Each unit of IP requires raw material units of 2 units

Cost of each raw material unit $ 70.00

Actual Sales of previous month December 2500 Units

Raw material units purchased in last December 50000 Units

Raw material consumed in December 5000 Units

Raw material stock remain as on 1st January 45000 Units

Selling Price of each unit of IP

Contribution +

Variable Cost

Selling Price of each unit of IP $600+$140

$

740.00

Sales Budget

Particulars January February March

Unit Sold 3000 3000 4000

Unit Selling price

$

740.00

$

740.00

$

740.00

Total Sales

$

2,220,000.00

$

2,220,000.00

$

2,960,000.00

(Lucey, 2013)

Cash collection budget from sales

Particulars January February March

Total Sales $ 2,220,000.00 $ 2,220,000.00 $ 2,960,000.00

Cash Collected

40% in current month $ 888,000.00 $ 888,000.00 $ 1,184,000.00

60% in following month

(2500 units sold in

December) $ 1,110,000.00 $ 1,332,000.00 $ 1,332,000.00

Total Cash Collections $ 1,998,000.00 $ 2,220,000.00 $ 2,516,000.00

6

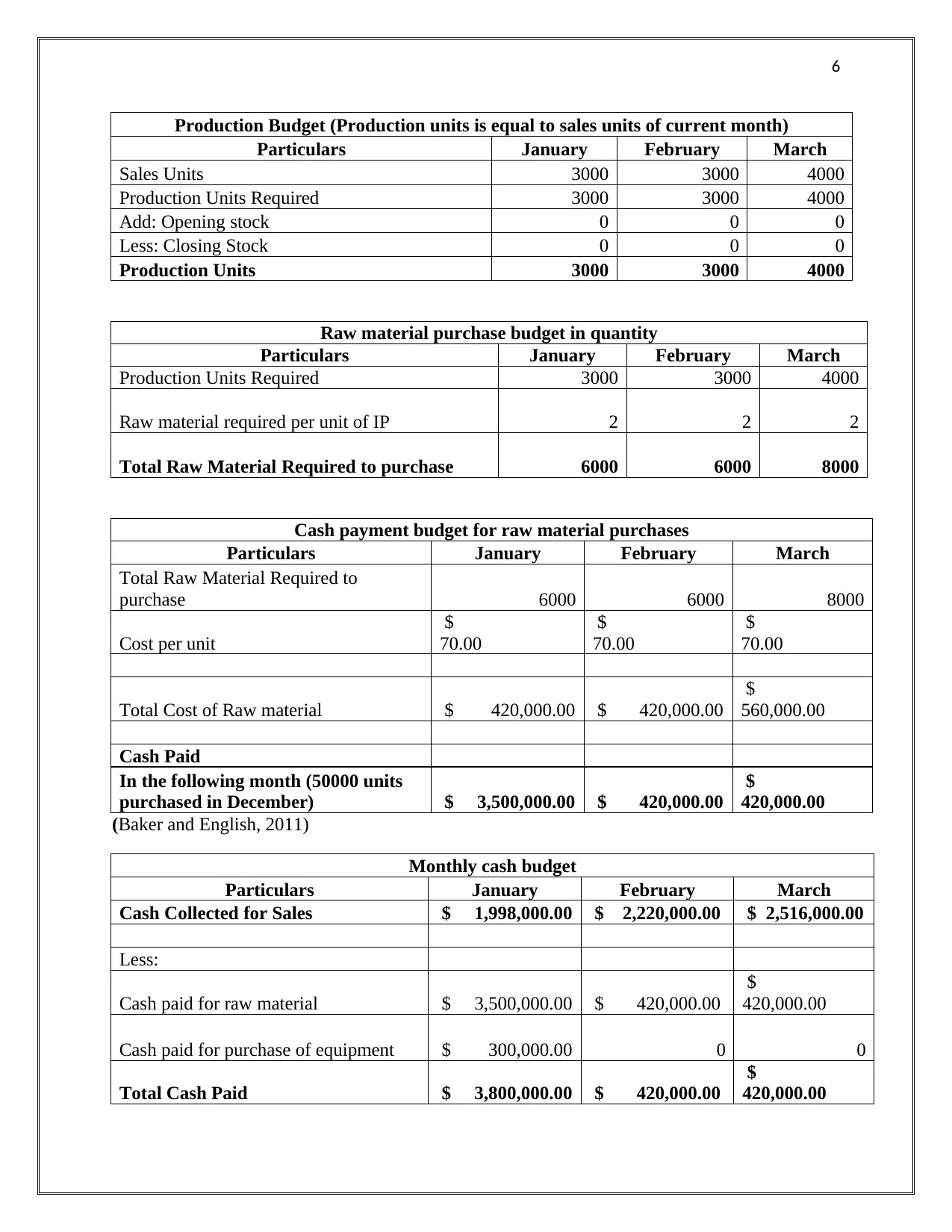

Production Budget (Production units is equal to sales units of current month)

Particulars January February March

Sales Units 3000 3000 4000

Production Units Required 3000 3000 4000

Add: Opening stock 0 0 0

Less: Closing Stock 0 0 0

Production Units 3000 3000 4000

Raw material purchase budget in quantity

Particulars January February March

Production Units Required 3000 3000 4000

Raw material required per unit of IP 2 2 2

Total Raw Material Required to purchase 6000 6000 8000

Cash payment budget for raw material purchases

Particulars January February March

Total Raw Material Required to

purchase 6000 6000 8000

Cost per unit

$

70.00

$

70.00

$

70.00

Total Cost of Raw material $ 420,000.00 $ 420,000.00

$

560,000.00

Cash Paid

In the following month (50000 units

purchased in December) $ 3,500,000.00 $ 420,000.00

$

420,000.00

(Baker and English, 2011)

Monthly cash budget

Particulars January February March

Cash Collected for Sales $ 1,998,000.00 $ 2,220,000.00 $ 2,516,000.00

Less:

Cash paid for raw material $ 3,500,000.00 $ 420,000.00

$

420,000.00

Cash paid for purchase of equipment $ 300,000.00 0 0

Total Cash Paid $ 3,800,000.00 $ 420,000.00

$

420,000.00

Production Budget (Production units is equal to sales units of current month)

Particulars January February March

Sales Units 3000 3000 4000

Production Units Required 3000 3000 4000

Add: Opening stock 0 0 0

Less: Closing Stock 0 0 0

Production Units 3000 3000 4000

Raw material purchase budget in quantity

Particulars January February March

Production Units Required 3000 3000 4000

Raw material required per unit of IP 2 2 2

Total Raw Material Required to purchase 6000 6000 8000

Cash payment budget for raw material purchases

Particulars January February March

Total Raw Material Required to

purchase 6000 6000 8000

Cost per unit

$

70.00

$

70.00

$

70.00

Total Cost of Raw material $ 420,000.00 $ 420,000.00

$

560,000.00

Cash Paid

In the following month (50000 units

purchased in December) $ 3,500,000.00 $ 420,000.00

$

420,000.00

(Baker and English, 2011)

Monthly cash budget

Particulars January February March

Cash Collected for Sales $ 1,998,000.00 $ 2,220,000.00 $ 2,516,000.00

Less:

Cash paid for raw material $ 3,500,000.00 $ 420,000.00

$

420,000.00

Cash paid for purchase of equipment $ 300,000.00 0 0

Total Cash Paid $ 3,800,000.00 $ 420,000.00

$

420,000.00

7

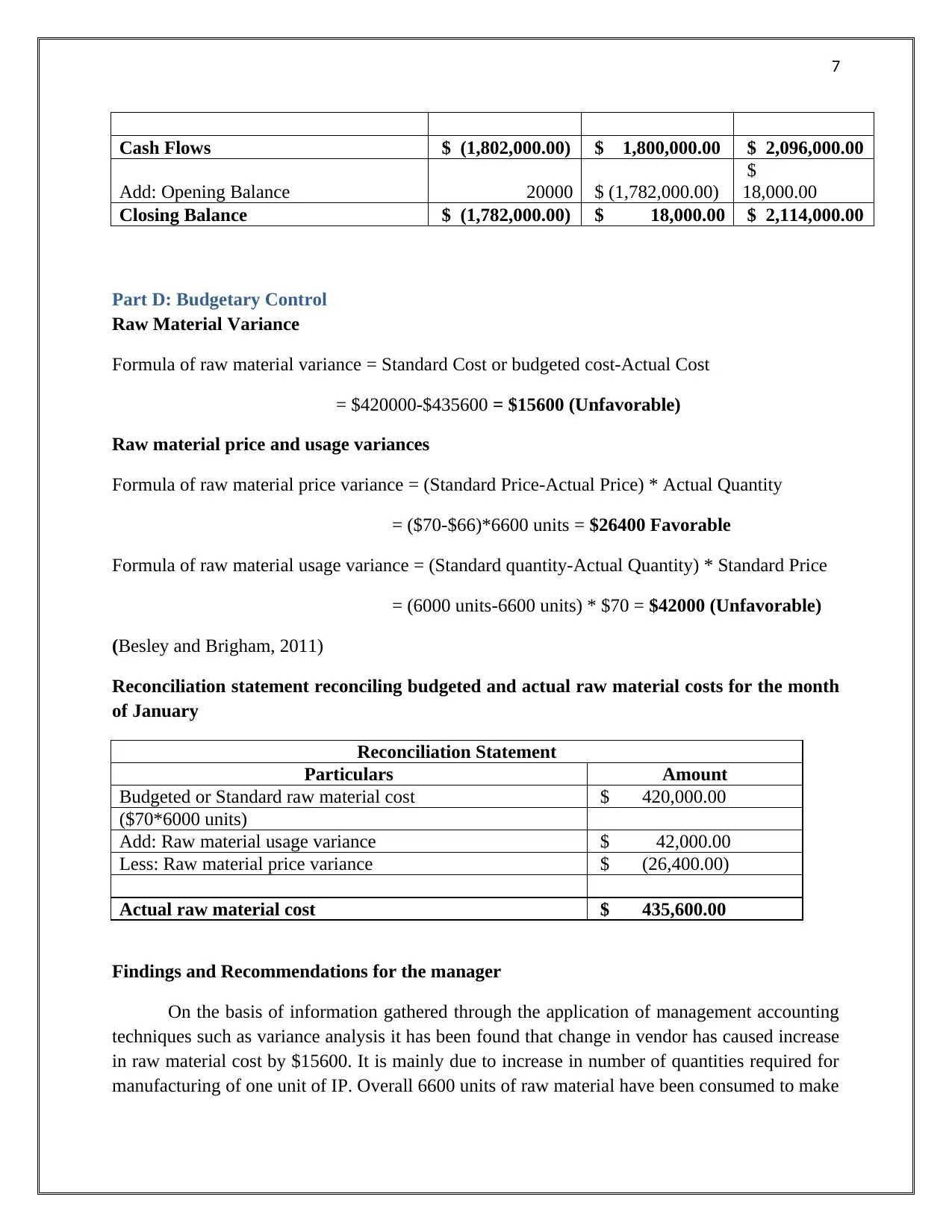

Cash Flows $ (1,802,000.00) $ 1,800,000.00 $ 2,096,000.00

Add: Opening Balance 20000 $ (1,782,000.00)

$

18,000.00

Closing Balance $ (1,782,000.00) $ 18,000.00 $ 2,114,000.00

Part D: Budgetary Control

Raw Material Variance

Formula of raw material variance = Standard Cost or budgeted cost-Actual Cost

= $420000-$435600 = $15600 (Unfavorable)

Raw material price and usage variances

Formula of raw material price variance = (Standard Price-Actual Price) * Actual Quantity

= ($70-$66)*6600 units = $26400 Favorable

Formula of raw material usage variance = (Standard quantity-Actual Quantity) * Standard Price

= (6000 units-6600 units) * $70 = $42000 (Unfavorable)

(Besley and Brigham, 2011)

Reconciliation statement reconciling budgeted and actual raw material costs for the month

of January

Reconciliation Statement

Particulars Amount

Budgeted or Standard raw material cost $ 420,000.00

($70*6000 units)

Add: Raw material usage variance $ 42,000.00

Less: Raw material price variance $ (26,400.00)

Actual raw material cost $ 435,600.00

Findings and Recommendations for the manager

On the basis of information gathered through the application of management accounting

techniques such as variance analysis it has been found that change in vendor has caused increase

in raw material cost by $15600. It is mainly due to increase in number of quantities required for

manufacturing of one unit of IP. Overall 6600 units of raw material have been consumed to make

Cash Flows $ (1,802,000.00) $ 1,800,000.00 $ 2,096,000.00

Add: Opening Balance 20000 $ (1,782,000.00)

$

18,000.00

Closing Balance $ (1,782,000.00) $ 18,000.00 $ 2,114,000.00

Part D: Budgetary Control

Raw Material Variance

Formula of raw material variance = Standard Cost or budgeted cost-Actual Cost

= $420000-$435600 = $15600 (Unfavorable)

Raw material price and usage variances

Formula of raw material price variance = (Standard Price-Actual Price) * Actual Quantity

= ($70-$66)*6600 units = $26400 Favorable

Formula of raw material usage variance = (Standard quantity-Actual Quantity) * Standard Price

= (6000 units-6600 units) * $70 = $42000 (Unfavorable)

(Besley and Brigham, 2011)

Reconciliation statement reconciling budgeted and actual raw material costs for the month

of January

Reconciliation Statement

Particulars Amount

Budgeted or Standard raw material cost $ 420,000.00

($70*6000 units)

Add: Raw material usage variance $ 42,000.00

Less: Raw material price variance $ (26,400.00)

Actual raw material cost $ 435,600.00

Findings and Recommendations for the manager

On the basis of information gathered through the application of management accounting

techniques such as variance analysis it has been found that change in vendor has caused increase

in raw material cost by $15600. It is mainly due to increase in number of quantities required for

manufacturing of one unit of IP. Overall 6600 units of raw material have been consumed to make

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

3000 units of IP instead of 6000 units of raw material. It means 600 units of raw material have

become obsolete or it is has come with required quality. It is responsibility of procurement

department to look after the procurement process and check the quality of raw material before

selecting the vendor. Procurement department is responsible for purchase of raw material, so

they will be held responsible for this financial problem (Lucey, 2013).

The corrective action that can be taken in this situation is to ask the vendor to provide

proper quality tested raw material so that quantity required for raw material cannot increase from

the budgeted number. Another corrective action that can be taken is to change the vendor and

select vendor provided in the list at the predetermined price of raw material. As the raw material

price variance is favorable due to lower actual raw material cost than the budgeted cost, it is

suggested that to ask vendor to make sure all the raw materials should pass the quality test and if

it cannot than such raw material should be returned back (Lucey, 2013).

3000 units of IP instead of 6000 units of raw material. It means 600 units of raw material have

become obsolete or it is has come with required quality. It is responsibility of procurement

department to look after the procurement process and check the quality of raw material before

selecting the vendor. Procurement department is responsible for purchase of raw material, so

they will be held responsible for this financial problem (Lucey, 2013).

The corrective action that can be taken in this situation is to ask the vendor to provide

proper quality tested raw material so that quantity required for raw material cannot increase from

the budgeted number. Another corrective action that can be taken is to change the vendor and

select vendor provided in the list at the predetermined price of raw material. As the raw material

price variance is favorable due to lower actual raw material cost than the budgeted cost, it is

suggested that to ask vendor to make sure all the raw materials should pass the quality test and if

it cannot than such raw material should be returned back (Lucey, 2013).

9

References

Baker, H. K., and English, P. 2011. Capital Budgeting Valuation: Financial Analysis for Today's

Investment Projects. USA: John Wiley & Sons

Bardy, R., 2011. Management control in a business network: new challenges for accounting.

Qualitative Research in Accounting & Management 3(2), pp.161 – 181.

Besley, S. and Brigham, E. F. 2011. Essentials of Managerial Finance. NewYork: Cengage

Learning.

Drury, C. 2011. Management and Cost Accounting, 6th ed.UK: Thomson.

Drury, C. 2015. Management Accounting for Business Decisions. Germany: Cengage Learning

EMEA.

Lillis, A., 2018. Qualitative management accounting research: rationale, pitfalls and potential: A

comment on Vaivio. Qualitative Research in Accounting & Management 5(3). pp.239 – 246.

Lucey, T. 2013. Management Accounting. Germany: Cengage Learning EMEA.

References

Baker, H. K., and English, P. 2011. Capital Budgeting Valuation: Financial Analysis for Today's

Investment Projects. USA: John Wiley & Sons

Bardy, R., 2011. Management control in a business network: new challenges for accounting.

Qualitative Research in Accounting & Management 3(2), pp.161 – 181.

Besley, S. and Brigham, E. F. 2011. Essentials of Managerial Finance. NewYork: Cengage

Learning.

Drury, C. 2011. Management and Cost Accounting, 6th ed.UK: Thomson.

Drury, C. 2015. Management Accounting for Business Decisions. Germany: Cengage Learning

EMEA.

Lillis, A., 2018. Qualitative management accounting research: rationale, pitfalls and potential: A

comment on Vaivio. Qualitative Research in Accounting & Management 5(3). pp.239 – 246.

Lucey, T. 2013. Management Accounting. Germany: Cengage Learning EMEA.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.