Management Accounting and Control

VerifiedAdded on 2020/12/29

|12

|3662

|485

Report

AI Summary

This report analyzes the management accounting and control system of Tottenham Ltd., a toy manufacturing company. It examines relevant costs and income, qualitative factors influencing decision-making, and the application of standard costing and variance analysis. The report provides insights into key business decisions, including discontinuation, special selling prices, product mix, and make-or-buy decisions. Desklib provides past papers and solved assignments for students.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management accounting

and control

and control

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

A. Evaluation of relevant costs and income................................................................................1

B. Qualitative factors need into decision making.......................................................................3

PART B............................................................................................................................................4

Standard costing and variance analysis.......................................................................................4

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

A. Evaluation of relevant costs and income................................................................................1

B. Qualitative factors need into decision making.......................................................................3

PART B............................................................................................................................................4

Standard costing and variance analysis.......................................................................................4

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

INTRODUCTION

Management accounting and control is also called management control. It is one of the

oldest and most important feature of business management. Tottenham Ltd. which is a

manufacturing company of toys, use management control system for resolving financial

consequence in the organisation, to determine judgements on resource allocation, to help

management of the organisation while improving internal environment. In this project report

many pricing strategies are used to determine the best price for the product, decision regarding to

shut down and keep open the part of the business are taken, make or buy approach is used to

analyse the profits for the organisation, standard costing and variance analysis methods are

explained to determine or evaluate the variances among the costs (Abdel-Kader, 2011).

PART A

A. Evaluation of relevant costs and income

Tottenham Ltd manufactures toys in three division. It's first two division i.e. alpha and

Romeo make different parts of the toys and third division i.e. Charlie assemble those parts to

make final product. Manager of Charlie division is focusing on buying products from outsiders

and managers of alpha and Romeo wants to sell their product to outsiders. Directors of company

wants Charlie to give preference to alpha and Romeo over outsiders so that come doesn't faces

loss and should not take shutting down decision.

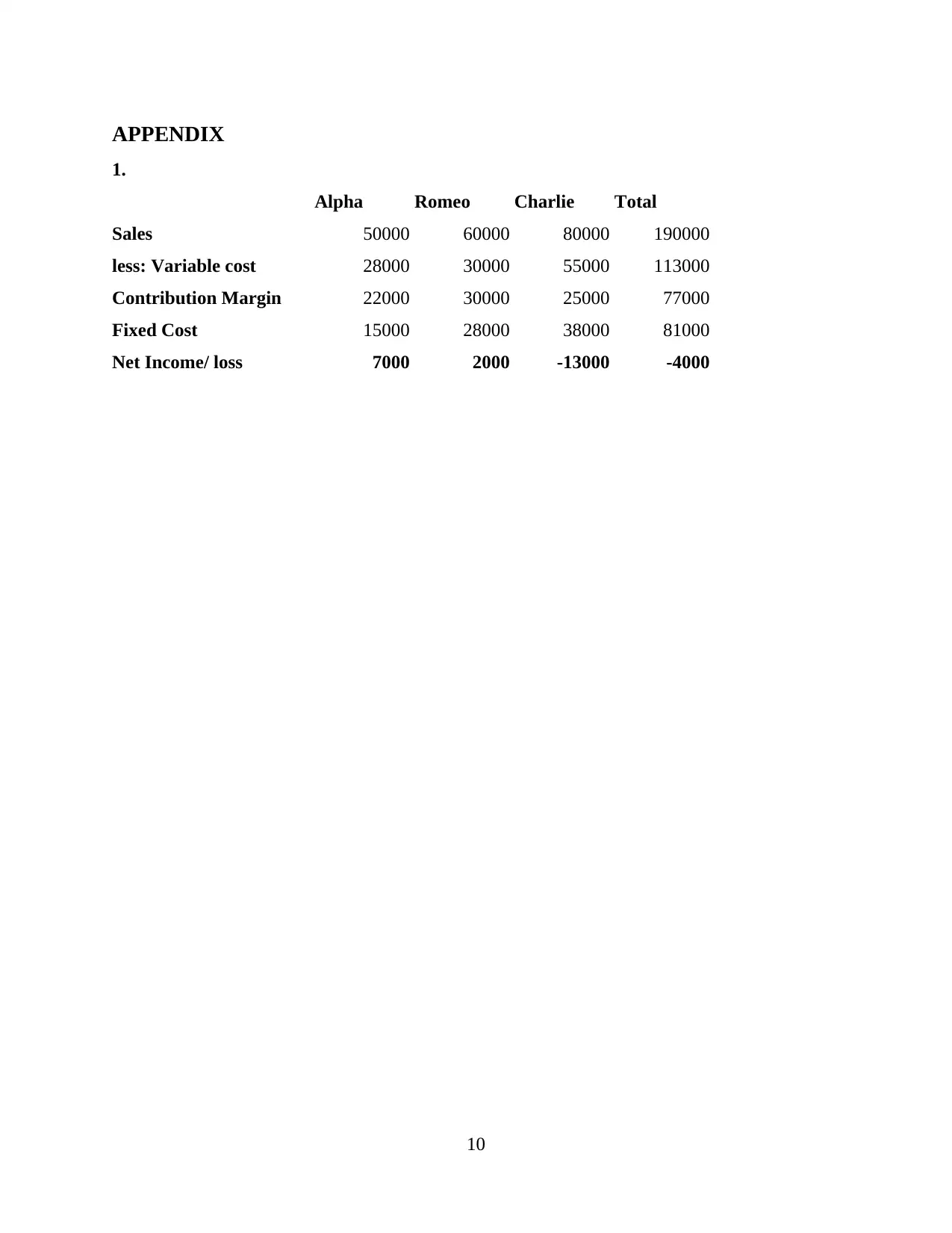

Discontinuation decision: It is one of the most difficult decisions that organisation must

take when to abandon a business division or completely shutting down of business which is

performing poorly. Tottenham Ltd takes discontinuation decision because it faces loss that

means its average margin revenues are less than its average variable costs. It's product is

unprofitable then company need to create a product form income statement and has to separate

variable costs from fixed by preparing a segment contribution margin income statement. As per

appendix 1. the company faces a overall loss of 4000 and it appears that Alpha and Romeo has a

profit of 7000 and 2000 respectively but Charlie has a loss a 13000 which impact on company's

overall profitability. Company calculates all discontinuation costs and incomes for

implementation of discontinuation business. It's shutting down costs includes liquidation costs,

loan repayments, funds to close all debts etc. and company sales their assets for generating

1

Management accounting and control is also called management control. It is one of the

oldest and most important feature of business management. Tottenham Ltd. which is a

manufacturing company of toys, use management control system for resolving financial

consequence in the organisation, to determine judgements on resource allocation, to help

management of the organisation while improving internal environment. In this project report

many pricing strategies are used to determine the best price for the product, decision regarding to

shut down and keep open the part of the business are taken, make or buy approach is used to

analyse the profits for the organisation, standard costing and variance analysis methods are

explained to determine or evaluate the variances among the costs (Abdel-Kader, 2011).

PART A

A. Evaluation of relevant costs and income

Tottenham Ltd manufactures toys in three division. It's first two division i.e. alpha and

Romeo make different parts of the toys and third division i.e. Charlie assemble those parts to

make final product. Manager of Charlie division is focusing on buying products from outsiders

and managers of alpha and Romeo wants to sell their product to outsiders. Directors of company

wants Charlie to give preference to alpha and Romeo over outsiders so that come doesn't faces

loss and should not take shutting down decision.

Discontinuation decision: It is one of the most difficult decisions that organisation must

take when to abandon a business division or completely shutting down of business which is

performing poorly. Tottenham Ltd takes discontinuation decision because it faces loss that

means its average margin revenues are less than its average variable costs. It's product is

unprofitable then company need to create a product form income statement and has to separate

variable costs from fixed by preparing a segment contribution margin income statement. As per

appendix 1. the company faces a overall loss of 4000 and it appears that Alpha and Romeo has a

profit of 7000 and 2000 respectively but Charlie has a loss a 13000 which impact on company's

overall profitability. Company calculates all discontinuation costs and incomes for

implementation of discontinuation business. It's shutting down costs includes liquidation costs,

loan repayments, funds to close all debts etc. and company sales their assets for generating

1

revenues so that they pay all debts. But their revenues are not sufficient to bear all costs that why

Tottenham takes discontinuation decision. (Granlund, M., 2011).

Special selling price decisions: This pricing concept includes two prices that are transfer

prices and selling pricing to other contractors. In peak season when there is more demand and

Tottenham Ltd is not able to meet that demand because its manufacturing cost is high as compare

to outsiders for meeting that demand company takes transfer price decision by purchasing from

outsiders. In remaining season employees remains idle at that time company takes selling prices

decision and sells their product to competitors so that workers use the idle capacity when

demand is low. It also increases performance of all division and achieve profitability in future

(Arjaliès and Mundy, 2013).

Analysis of product mix and limiting factors: Product mix is a complete range of

product that is offered by a organisation. The product lines range from one to many or company

may deal in various products under the same product line. Tottenham Ltd is dealing in three

division i.e. Alpha, Romeo and Charlie. It is a category of that product mix in which company is

manufacturing three types of toys i.e. Toy A, Toy B and Toy C . Breadth, length, Depth and

consistency are the four dimensions of product mix that Tottenham Ltd is using for analysing

product mix where breadth shows number of items in the product line, length refers to number of

items in the product mix, depth means variants of individual product in the product line and

consistency shows the level to which the product lines are closely related to each other in terms

of their production and distribution requirements, price range etc. If company stop manufacturing

of Toy A then production resources is also available for manufacturing Toy B and C. Company's

overall profitability also increases because they produces limited product in all division for

achieving desired target on time with maximum profits (DRURY, 2013).

Make or buy decisions: It is an action of deciding whether company manufacture items

in house i.e. internally or purchasing it from outsiders i.e. external suppliers. Tottenham Ltd

prefer 'make decision' rather than buying from outsider because if Alpha and Romeo sells their

parts to outsider and Charlie is buying from others, it incurs various costs like selling and

distribution, transportation etc. which is minimized to zero if Charlie make final product by

assembling product of Alpha and Romeo. But in peak time company doesn't fulfil demand on

time that why for that particular time period company takes buy decisions. Company's make

decision is less expensive, better controlled of lead time, transportation and storage costs and

2

Tottenham takes discontinuation decision. (Granlund, M., 2011).

Special selling price decisions: This pricing concept includes two prices that are transfer

prices and selling pricing to other contractors. In peak season when there is more demand and

Tottenham Ltd is not able to meet that demand because its manufacturing cost is high as compare

to outsiders for meeting that demand company takes transfer price decision by purchasing from

outsiders. In remaining season employees remains idle at that time company takes selling prices

decision and sells their product to competitors so that workers use the idle capacity when

demand is low. It also increases performance of all division and achieve profitability in future

(Arjaliès and Mundy, 2013).

Analysis of product mix and limiting factors: Product mix is a complete range of

product that is offered by a organisation. The product lines range from one to many or company

may deal in various products under the same product line. Tottenham Ltd is dealing in three

division i.e. Alpha, Romeo and Charlie. It is a category of that product mix in which company is

manufacturing three types of toys i.e. Toy A, Toy B and Toy C . Breadth, length, Depth and

consistency are the four dimensions of product mix that Tottenham Ltd is using for analysing

product mix where breadth shows number of items in the product line, length refers to number of

items in the product mix, depth means variants of individual product in the product line and

consistency shows the level to which the product lines are closely related to each other in terms

of their production and distribution requirements, price range etc. If company stop manufacturing

of Toy A then production resources is also available for manufacturing Toy B and C. Company's

overall profitability also increases because they produces limited product in all division for

achieving desired target on time with maximum profits (DRURY, 2013).

Make or buy decisions: It is an action of deciding whether company manufacture items

in house i.e. internally or purchasing it from outsiders i.e. external suppliers. Tottenham Ltd

prefer 'make decision' rather than buying from outsider because if Alpha and Romeo sells their

parts to outsider and Charlie is buying from others, it incurs various costs like selling and

distribution, transportation etc. which is minimized to zero if Charlie make final product by

assembling product of Alpha and Romeo. But in peak time company doesn't fulfil demand on

time that why for that particular time period company takes buy decisions. Company's make

decision is less expensive, better controlled of lead time, transportation and storage costs and

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

greater assurance of continuous supplier because it's a in-house manufacturing. For example

company's cost of manufacturing product is 10000 and if they purchase from outsiders it cost

12000 that's why company takes manufacturing decision. Company doesn't need to maintain

multiple source policy and worry for small volume requirements in make decision like they

follow in outsourcing.

B. Qualitative factors need into decision making

Qualitative factors are the final output of organisation's performance which are difficult

to measure in accounting terms. Profit margin, sales turnover and management decisions etc. are

the strategic choice for evaluation of company's qualitative factors. Manager consider this factors

as a part of self analysis for decision making (Parker, 2012). Below are the example of

qualitative factors:

Discontinuation decision: Investors is one of the most important qualitative factors

which influence on discontinuation decision. They allocates capital with an belief of financial

returns in future. Depending on the level of investment involved which means if a large

investment of funds is involved then decision is more likely to be quantitative in nature but in

Tottenham Ltd case investment is minor and it impact on qualitative factors which plays a

important role in the decision making like company has to achieve desirable profit so that

investors get favourable returns on their investments and they decided to reinvest in future also.

Special selling price decisions: Product cost, quality of toys and customers are the

qualitative factors which influence this decision. Tottenham Ltd considered cost of product for

taking effective price decisions which includes amount spent on product development, its testing

and packaging. The organisation need to get the idea of customer perception, it will help to set a

proper price that customers are able to bear. Company has to maintain its product's quality,

supply on time and effective selling price so that it can attract both new and existing customers.

If Tottenham Ltd make decision on basis of above factors and focus on effective selling price of

toys which should be less than its competitor's product price which reduced the chances of

customer's switching towards it's competitors (Soin and Collier, 2013).

Analysis of product mix and limiting factors: Qualitative factors like image of

company, its tradition towards society and standard of living are analysed under this decision.

Company should produce such products that helps in building positive market image to improve

its sales. Company should focus on manufacturing toys for both girls and boys rather than

3

company's cost of manufacturing product is 10000 and if they purchase from outsiders it cost

12000 that's why company takes manufacturing decision. Company doesn't need to maintain

multiple source policy and worry for small volume requirements in make decision like they

follow in outsourcing.

B. Qualitative factors need into decision making

Qualitative factors are the final output of organisation's performance which are difficult

to measure in accounting terms. Profit margin, sales turnover and management decisions etc. are

the strategic choice for evaluation of company's qualitative factors. Manager consider this factors

as a part of self analysis for decision making (Parker, 2012). Below are the example of

qualitative factors:

Discontinuation decision: Investors is one of the most important qualitative factors

which influence on discontinuation decision. They allocates capital with an belief of financial

returns in future. Depending on the level of investment involved which means if a large

investment of funds is involved then decision is more likely to be quantitative in nature but in

Tottenham Ltd case investment is minor and it impact on qualitative factors which plays a

important role in the decision making like company has to achieve desirable profit so that

investors get favourable returns on their investments and they decided to reinvest in future also.

Special selling price decisions: Product cost, quality of toys and customers are the

qualitative factors which influence this decision. Tottenham Ltd considered cost of product for

taking effective price decisions which includes amount spent on product development, its testing

and packaging. The organisation need to get the idea of customer perception, it will help to set a

proper price that customers are able to bear. Company has to maintain its product's quality,

supply on time and effective selling price so that it can attract both new and existing customers.

If Tottenham Ltd make decision on basis of above factors and focus on effective selling price of

toys which should be less than its competitor's product price which reduced the chances of

customer's switching towards it's competitors (Soin and Collier, 2013).

Analysis of product mix and limiting factors: Qualitative factors like image of

company, its tradition towards society and standard of living are analysed under this decision.

Company should produce such products that helps in building positive market image to improve

its sales. Company should focus on manufacturing toys for both girls and boys rather than

3

focusing on single gender. It will help to meet traditions towards society. Company should target

upper class as well as lower class of buyers and manufacture such toys that fits in their budget.

With the help of this decision Tottenham Ltd is able to target customers according to their

standard of living (Wickramasinghe and Alawattage, 2012).

Make or buy decisions: Cost of product and its quality helps Tottenham Ltd in taking

make decision because its manufacturing cost is less than market. If company is manufacturing

the products within the organisation it guarantees the quality and reliability of product and it will

also save cost and resources for the company. That's why the company considers the make

decision rather than considering buy decision. Because buying from outside will charge more

cost with no guarantee of quality and reliability (Ward, 2012).

PART B

Standard costing and variance analysis

“Standard costing and variance analysis are appropriate to any type and size of

organisation” Mostly managers agrees to this statement because these two methods are used to

analyse business position as well as the variances in the cost which shows the performance level

of the organisation. When actual cost is lower then standard cost, it is favourable variance, and

when standard cost is lower then actual cost, it is adverse variance. Favourable variance shows

higher level of performance and adverse variance shows the poor performance of the

organisation. These methods are also helpful in controlling cost and setting right price for the

product of industries like construction, manufacturing etc.. These methods are used by every

kind of the organisation whether it is small, medium or large. It helps small industry to minimize

the cost and maximize the profits. In large scale industries it is used to find out the difference

between standard and actual cost. These are very beneficial for medium scale industries also

because these industries have lower funds and huge objectives. These methods are helpful in

achieving the predetermined goals of such type of industries, by providing it the idea of the cost

that it should set for its product. These two methods are explained below:

Standard costing

It is an accounting technique that organisations use to determine the variation between

actual cost and standard cost of goods. It is probably coordinated with a manufacturer's profit

plan for an accounting year and concerned with the product costs that are direct materials, direct

4

upper class as well as lower class of buyers and manufacture such toys that fits in their budget.

With the help of this decision Tottenham Ltd is able to target customers according to their

standard of living (Wickramasinghe and Alawattage, 2012).

Make or buy decisions: Cost of product and its quality helps Tottenham Ltd in taking

make decision because its manufacturing cost is less than market. If company is manufacturing

the products within the organisation it guarantees the quality and reliability of product and it will

also save cost and resources for the company. That's why the company considers the make

decision rather than considering buy decision. Because buying from outside will charge more

cost with no guarantee of quality and reliability (Ward, 2012).

PART B

Standard costing and variance analysis

“Standard costing and variance analysis are appropriate to any type and size of

organisation” Mostly managers agrees to this statement because these two methods are used to

analyse business position as well as the variances in the cost which shows the performance level

of the organisation. When actual cost is lower then standard cost, it is favourable variance, and

when standard cost is lower then actual cost, it is adverse variance. Favourable variance shows

higher level of performance and adverse variance shows the poor performance of the

organisation. These methods are also helpful in controlling cost and setting right price for the

product of industries like construction, manufacturing etc.. These methods are used by every

kind of the organisation whether it is small, medium or large. It helps small industry to minimize

the cost and maximize the profits. In large scale industries it is used to find out the difference

between standard and actual cost. These are very beneficial for medium scale industries also

because these industries have lower funds and huge objectives. These methods are helpful in

achieving the predetermined goals of such type of industries, by providing it the idea of the cost

that it should set for its product. These two methods are explained below:

Standard costing

It is an accounting technique that organisations use to determine the variation between

actual cost and standard cost of goods. It is probably coordinated with a manufacturer's profit

plan for an accounting year and concerned with the product costs that are direct materials, direct

4

labour and overheads. It is very helpful for the management to take decisions because if variance

arises, management becomes aware about the difference of manufacturing and standard cost. If

actual costs are higher then budgeted cost then variance is adverse, but if budget costs are higher

then actual the variance is favourable (Standard costing, 2017).

Importance of standard costing

Standard costing is very important management tool which helps the management to keep

an idea of variations in the actual and standard cost. It is very helpful for the large organisations

because large organisations plan in advance for each kind of uncertainty and expenses. It is

usually related to the manufacturing cost of the company. It helps management to deal with

variances at the time they occur, it provides the ideas of variances to the management. It is used

while finding the solutions of managerial problems, so it is very important for the management.

It is also important for the effective performance of business, because when the management is

aware of the variance situation then they can try to reduce the possibility of variances and

increase the efficiency.

Benefits of standard costing:

Increase the efficiency: Standard costing is beneficial while the management is thinking

to increase the efficiency of the business. For example responsibility of account handler of a

construction company is to predict the standard cost of direct material, labour and other

overheads and predetermined standard cost is helpful in increasing efficiency of the business

(Hiebl, 2014).

Managerial planning: It is a process of using all available resources in such manner that

maximises the profits. For example managers of financial services industry plan for economic

operations for effective standard cost. If the standard cost is properly determined by the

management then it can help to discover inefficiencies in operations and management can plan to

remove those inefficiencies from business.

Effective utilisation of resources: Standard costing is also helpful in effective utilisation

of resources because it can help to estimate the resources required for the company in future. For

example if the management of manufacturing company have the idea of required resources then

purchased resources will be sufficient for the production and in such way they can effectively

use the resources.

5

arises, management becomes aware about the difference of manufacturing and standard cost. If

actual costs are higher then budgeted cost then variance is adverse, but if budget costs are higher

then actual the variance is favourable (Standard costing, 2017).

Importance of standard costing

Standard costing is very important management tool which helps the management to keep

an idea of variations in the actual and standard cost. It is very helpful for the large organisations

because large organisations plan in advance for each kind of uncertainty and expenses. It is

usually related to the manufacturing cost of the company. It helps management to deal with

variances at the time they occur, it provides the ideas of variances to the management. It is used

while finding the solutions of managerial problems, so it is very important for the management.

It is also important for the effective performance of business, because when the management is

aware of the variance situation then they can try to reduce the possibility of variances and

increase the efficiency.

Benefits of standard costing:

Increase the efficiency: Standard costing is beneficial while the management is thinking

to increase the efficiency of the business. For example responsibility of account handler of a

construction company is to predict the standard cost of direct material, labour and other

overheads and predetermined standard cost is helpful in increasing efficiency of the business

(Hiebl, 2014).

Managerial planning: It is a process of using all available resources in such manner that

maximises the profits. For example managers of financial services industry plan for economic

operations for effective standard cost. If the standard cost is properly determined by the

management then it can help to discover inefficiencies in operations and management can plan to

remove those inefficiencies from business.

Effective utilisation of resources: Standard costing is also helpful in effective utilisation

of resources because it can help to estimate the resources required for the company in future. For

example if the management of manufacturing company have the idea of required resources then

purchased resources will be sufficient for the production and in such way they can effectively

use the resources.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Proper decisions: It provides the information of business position and it is beneficial for

the management to make clear decisions for the best performance of the business.

Cost control: Standard costing is also helpful for small scale industries to compare actual

cost and standard cost. When actual costs are higher then standard cost it is a sign for the

company to reduce the cost or to control the cost (Hülle, Kaspar and Möller, 2011).

Purpose of standard costing

To study time and speed: While using standard costing method managers of company

have to study the time and speed involves in manufacturing process. The main purpose of

standard costing method is to reduce the time and increase the cost in effective manner (Hilton

and Platt, 2013).

To formulate production policy: It helps to formulate production policy for mining and

metal industry. The management is able to make accurate standards if they have proper

production knowledge, which is only possible by good production policy.

To delegate powers: It is helpful in evaluating performance of employees and whose

performance is good, that employee will be promoted by higher authority and get more power to

make decisions.

Management by exceptions: It means to concentrate big projects of the organisation

instead of small projects. For example in real estate industry it is easy with standard costing. In

standard costing managers make standards of cost involved in products. While focusing on the

project, the management only have to check the cost standard then take the decision to invest

time in that project or not.

Variance analysis

It is used by small as well as large level of organisations to maintain control over the

business. It helps the management to understand the reason of fluctuation and to find out ways to

change the same situation. It is the difference of budgeted and actual cost. It is implemented to

study the actual and planned behaviour of the organisation. It is the investigation of fluctuation in

financial execution from the standards characterized in organisational budgets. Price variances

are used to identify, whether the organisation paid more for each unit of input. Quantity

variances used to identify, whether the organisation used more part of the input.

Importance of variance analysis

6

the management to make clear decisions for the best performance of the business.

Cost control: Standard costing is also helpful for small scale industries to compare actual

cost and standard cost. When actual costs are higher then standard cost it is a sign for the

company to reduce the cost or to control the cost (Hülle, Kaspar and Möller, 2011).

Purpose of standard costing

To study time and speed: While using standard costing method managers of company

have to study the time and speed involves in manufacturing process. The main purpose of

standard costing method is to reduce the time and increase the cost in effective manner (Hilton

and Platt, 2013).

To formulate production policy: It helps to formulate production policy for mining and

metal industry. The management is able to make accurate standards if they have proper

production knowledge, which is only possible by good production policy.

To delegate powers: It is helpful in evaluating performance of employees and whose

performance is good, that employee will be promoted by higher authority and get more power to

make decisions.

Management by exceptions: It means to concentrate big projects of the organisation

instead of small projects. For example in real estate industry it is easy with standard costing. In

standard costing managers make standards of cost involved in products. While focusing on the

project, the management only have to check the cost standard then take the decision to invest

time in that project or not.

Variance analysis

It is used by small as well as large level of organisations to maintain control over the

business. It helps the management to understand the reason of fluctuation and to find out ways to

change the same situation. It is the difference of budgeted and actual cost. It is implemented to

study the actual and planned behaviour of the organisation. It is the investigation of fluctuation in

financial execution from the standards characterized in organisational budgets. Price variances

are used to identify, whether the organisation paid more for each unit of input. Quantity

variances used to identify, whether the organisation used more part of the input.

Importance of variance analysis

6

It helps managers to make more accurate and effective budget for future. Mainly it is

used to find out the reason of variation in cost. When the managers identify the cause of the

adverse variance then they try to find way to reduce cost so that favourable variance can arise

which is beneficial for the organisation. Once the cause is identified management take actions to

remove the adverse variation. For example in auto mobile industry it is used to evaluate the

productivity and quality of the project. The organisation plans for budget to reduce cost and

increase profits of the business in the future (Maas, Schaltegger and Crutzen, 2016).

Benefits of variance analysis

Managing risk: In medium scale industries variance analysis helps the finance

department to gather internal information which is required to understand the reasons for

manageable and difficult variances. When finance department is aware of such variances, it

focuses on implementation of such policies, that can minimize risks arising from such variances.

Performance evaluation: Variance analysis is used by insurance sector to evaluate

performance of individual employee and controlling department. Favourable variances show the

good performance level and adverse variance indicates poor performance level of the

department.

Accountability: Variance analysis is a system of accountability within the organisation.

Each employee of the company is accountable for the poor performance and adverse variance

result of the organisation.

Controlling extra expenses: Main benefit of variance analysis is that it controls the extra

expenses. For example Management of healthcare industry takes favourable controlling action in

case of adverse variance outcome.

Creating shareholder value: every organisation is focused to maintain the proper

records of the information, this increases the chance of favourable variances and it strengthen the

financial position which attracts the shareholders to invest in the business.

Purpose of variance analysis

Cost control: One of the main purpose of variance analysis is to interpret the cost

components of a product or service and take appropriate actions to control the cost.

To help in improvement planning: Variance analysis is used by large scale industries to

make modification or changes in the weaken areas which are identified while the analysis. If

7

used to find out the reason of variation in cost. When the managers identify the cause of the

adverse variance then they try to find way to reduce cost so that favourable variance can arise

which is beneficial for the organisation. Once the cause is identified management take actions to

remove the adverse variation. For example in auto mobile industry it is used to evaluate the

productivity and quality of the project. The organisation plans for budget to reduce cost and

increase profits of the business in the future (Maas, Schaltegger and Crutzen, 2016).

Benefits of variance analysis

Managing risk: In medium scale industries variance analysis helps the finance

department to gather internal information which is required to understand the reasons for

manageable and difficult variances. When finance department is aware of such variances, it

focuses on implementation of such policies, that can minimize risks arising from such variances.

Performance evaluation: Variance analysis is used by insurance sector to evaluate

performance of individual employee and controlling department. Favourable variances show the

good performance level and adverse variance indicates poor performance level of the

department.

Accountability: Variance analysis is a system of accountability within the organisation.

Each employee of the company is accountable for the poor performance and adverse variance

result of the organisation.

Controlling extra expenses: Main benefit of variance analysis is that it controls the extra

expenses. For example Management of healthcare industry takes favourable controlling action in

case of adverse variance outcome.

Creating shareholder value: every organisation is focused to maintain the proper

records of the information, this increases the chance of favourable variances and it strengthen the

financial position which attracts the shareholders to invest in the business.

Purpose of variance analysis

Cost control: One of the main purpose of variance analysis is to interpret the cost

components of a product or service and take appropriate actions to control the cost.

To help in improvement planning: Variance analysis is used by large scale industries to

make modification or changes in the weaken areas which are identified while the analysis. If

7

there is requirement of any adjustment or improvement that would ultimately lead to improved

performance.

Motivating managers: Variance analyses is also a way to motivate the managers or

employees because it evaluates the performance of the employees. It is helpful for the executives

of organisations to provide reward to the employees for their good performance and motivate

them.

Analysis of performance: Variance analysis help the management to analyse the

performance of business by different variance methods. Favourable variances are the result of

good business performance (Otley and Emmanuel, 2013).

CONCLUSION

From the above project report it has been concluded that, Management control system

used by Tottenham Ltd. while implementing strategies like resource allocation, resolving

financial issues etc. It is also explained in this report that company should discontinue the

production of the product and while using make or buy approach company should make the

product. In this report different qualitative methods are used to evaluate the quality of the

production. Standard costing and variance analysis are used to determine the difference of actual

and standard cost while taking production decisions. These two methods are used by various size

of the organisation like small, medium and large and very beneficial for the management of the

organisation.

8

performance.

Motivating managers: Variance analyses is also a way to motivate the managers or

employees because it evaluates the performance of the employees. It is helpful for the executives

of organisations to provide reward to the employees for their good performance and motivate

them.

Analysis of performance: Variance analysis help the management to analyse the

performance of business by different variance methods. Favourable variances are the result of

good business performance (Otley and Emmanuel, 2013).

CONCLUSION

From the above project report it has been concluded that, Management control system

used by Tottenham Ltd. while implementing strategies like resource allocation, resolving

financial issues etc. It is also explained in this report that company should discontinue the

production of the product and while using make or buy approach company should make the

product. In this report different qualitative methods are used to evaluate the quality of the

production. Standard costing and variance analysis are used to determine the difference of actual

and standard cost while taking production decisions. These two methods are used by various size

of the organisation like small, medium and large and very beneficial for the management of the

organisation.

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals:

Abdel-Kader, M. G. ed., 2011. Review of management accounting research. Springer.

Arjaliès, D. L. and Mundy, J., 2013. The use of management control systems to manage CSR

strategy: A levers of control perspective. Management Accounting Research. 24(4).

pp.284-300.

DRURY, C. M., 2013. Management and cost accounting. Springer.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control research.

Journal of Management Control. 24(3). pp.223-240.

Hilton, R. W. and Platt, D. E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Hülle, J., Kaspar, R. and Möller, K., 2011. Multiple Criteria Decision‐Making in Management

Accounting and Control‐State of the Art and Research Perspectives Based on a

Bibliometric Study. Journal of Multi‐Criteria Decision Analysis. 18(5-6). pp.253-265.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

Otley, D. and Emmanuel, K. M. C., 2013. Readings in accounting for management control.

Springer.

Parker, L. D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and

control.

Ward, K., 2012. Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2012. Management accounting change: approaches

and perspectives. Routledge.

Online

Standard costing, 2017.[online] available through:

<www.accountingtools.com/articles/2017/5/14/standard-costing>

9

Books and Journals:

Abdel-Kader, M. G. ed., 2011. Review of management accounting research. Springer.

Arjaliès, D. L. and Mundy, J., 2013. The use of management control systems to manage CSR

strategy: A levers of control perspective. Management Accounting Research. 24(4).

pp.284-300.

DRURY, C. M., 2013. Management and cost accounting. Springer.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control research.

Journal of Management Control. 24(3). pp.223-240.

Hilton, R. W. and Platt, D. E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Hülle, J., Kaspar, R. and Möller, K., 2011. Multiple Criteria Decision‐Making in Management

Accounting and Control‐State of the Art and Research Perspectives Based on a

Bibliometric Study. Journal of Multi‐Criteria Decision Analysis. 18(5-6). pp.253-265.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

Otley, D. and Emmanuel, K. M. C., 2013. Readings in accounting for management control.

Springer.

Parker, L. D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and

control.

Ward, K., 2012. Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2012. Management accounting change: approaches

and perspectives. Routledge.

Online

Standard costing, 2017.[online] available through:

<www.accountingtools.com/articles/2017/5/14/standard-costing>

9

APPENDIX

1.

Alpha Romeo Charlie Total

Sales 50000 60000 80000 190000

less: Variable cost 28000 30000 55000 113000

Contribution Margin 22000 30000 25000 77000

Fixed Cost 15000 28000 38000 81000

Net Income/ loss 7000 2000 -13000 -4000

10

1.

Alpha Romeo Charlie Total

Sales 50000 60000 80000 190000

less: Variable cost 28000 30000 55000 113000

Contribution Margin 22000 30000 25000 77000

Fixed Cost 15000 28000 38000 81000

Net Income/ loss 7000 2000 -13000 -4000

10

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.