Real Estate Equities: Buy Back and Capital Raising Scenarios

VerifiedAdded on 2023/01/05

|14

|3662

|88

AI Summary

This document discusses the scenarios of buy back and capital raising in real estate equities. It explores the reasons behind buy backs, potential traps and manipulations, and provides real examples of stock buy backs. The document also explains the impact of buy backs on investor confidence and market valuation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1

Name:

Course

Professor’s name

University name

City, State

Date of submission

Name:

Course

Professor’s name

University name

City, State

Date of submission

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

Introduction

Real Estate Equities are among the best traded and marketable securities in the world.

Private real estate equity allows the HNWI and other institutions to invest in debt holdings

and equity in property assets. Institutions like pension funds and endowments are the most

likely to invest in real estate property equity. Using the active management strategy and

model, private equity real estate takes a diversified property ownership approach (Anule, et

al, 2018). Ownership models and strategies can range from raw land developments and

holdings to redevelopment of existing properties or cash flow injections into properties that

are struggling. The assessment of Task 1 and Task 3 of various reals estate equities and

development will be used in analyzing the on market buy back on proceeds.

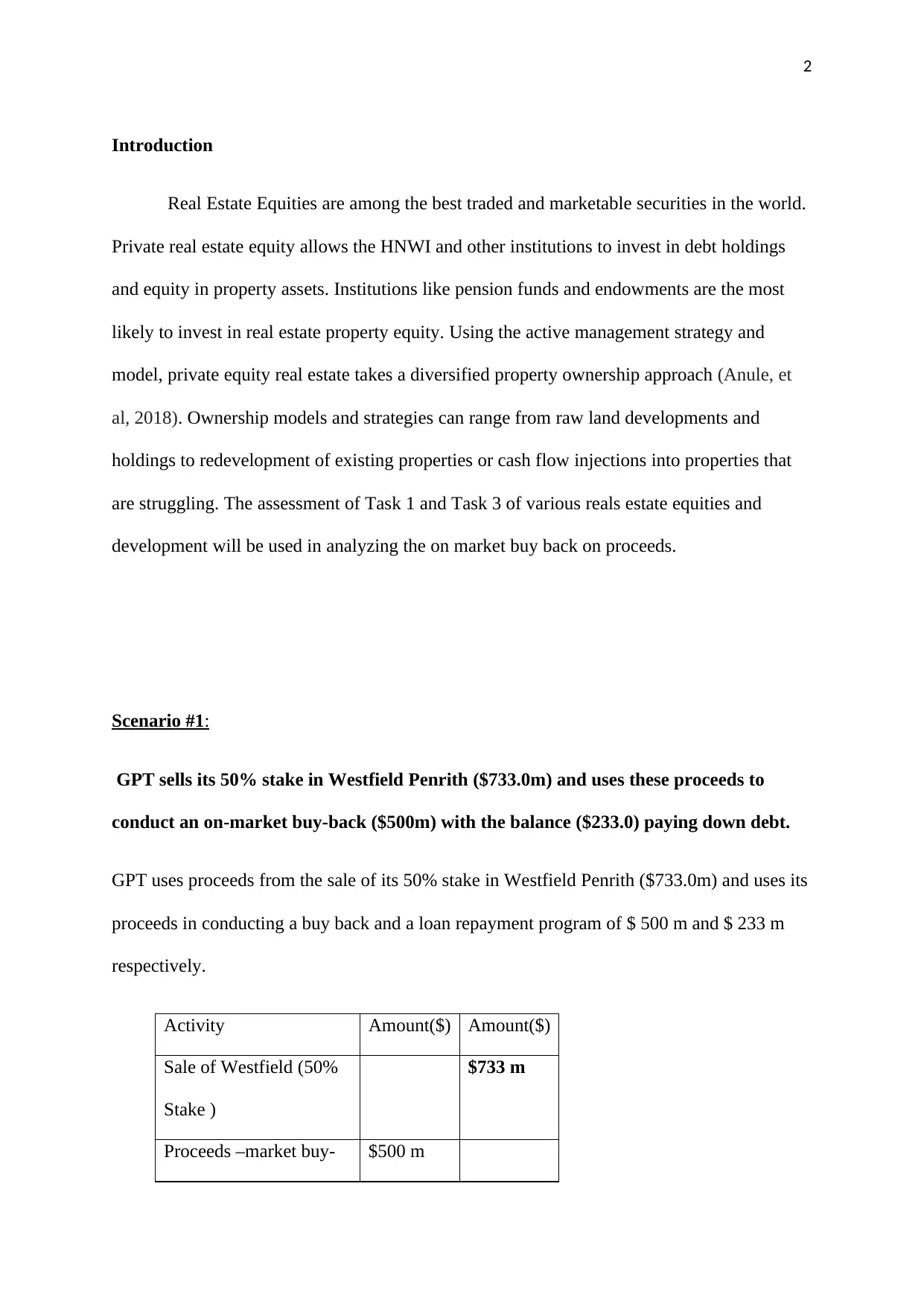

Scenario #1:

GPT sells its 50% stake in Westfield Penrith ($733.0m) and uses these proceeds to

conduct an on-market buy-back ($500m) with the balance ($233.0) paying down debt.

GPT uses proceeds from the sale of its 50% stake in Westfield Penrith ($733.0m) and uses its

proceeds in conducting a buy back and a loan repayment program of $ 500 m and $ 233 m

respectively.

Activity Amount($) Amount($)

Sale of Westfield (50%

Stake )

$733 m

Proceeds –market buy- $500 m

Introduction

Real Estate Equities are among the best traded and marketable securities in the world.

Private real estate equity allows the HNWI and other institutions to invest in debt holdings

and equity in property assets. Institutions like pension funds and endowments are the most

likely to invest in real estate property equity. Using the active management strategy and

model, private equity real estate takes a diversified property ownership approach (Anule, et

al, 2018). Ownership models and strategies can range from raw land developments and

holdings to redevelopment of existing properties or cash flow injections into properties that

are struggling. The assessment of Task 1 and Task 3 of various reals estate equities and

development will be used in analyzing the on market buy back on proceeds.

Scenario #1:

GPT sells its 50% stake in Westfield Penrith ($733.0m) and uses these proceeds to

conduct an on-market buy-back ($500m) with the balance ($233.0) paying down debt.

GPT uses proceeds from the sale of its 50% stake in Westfield Penrith ($733.0m) and uses its

proceeds in conducting a buy back and a loan repayment program of $ 500 m and $ 233 m

respectively.

Activity Amount($) Amount($)

Sale of Westfield (50%

Stake )

$733 m

Proceeds –market buy- $500 m

3

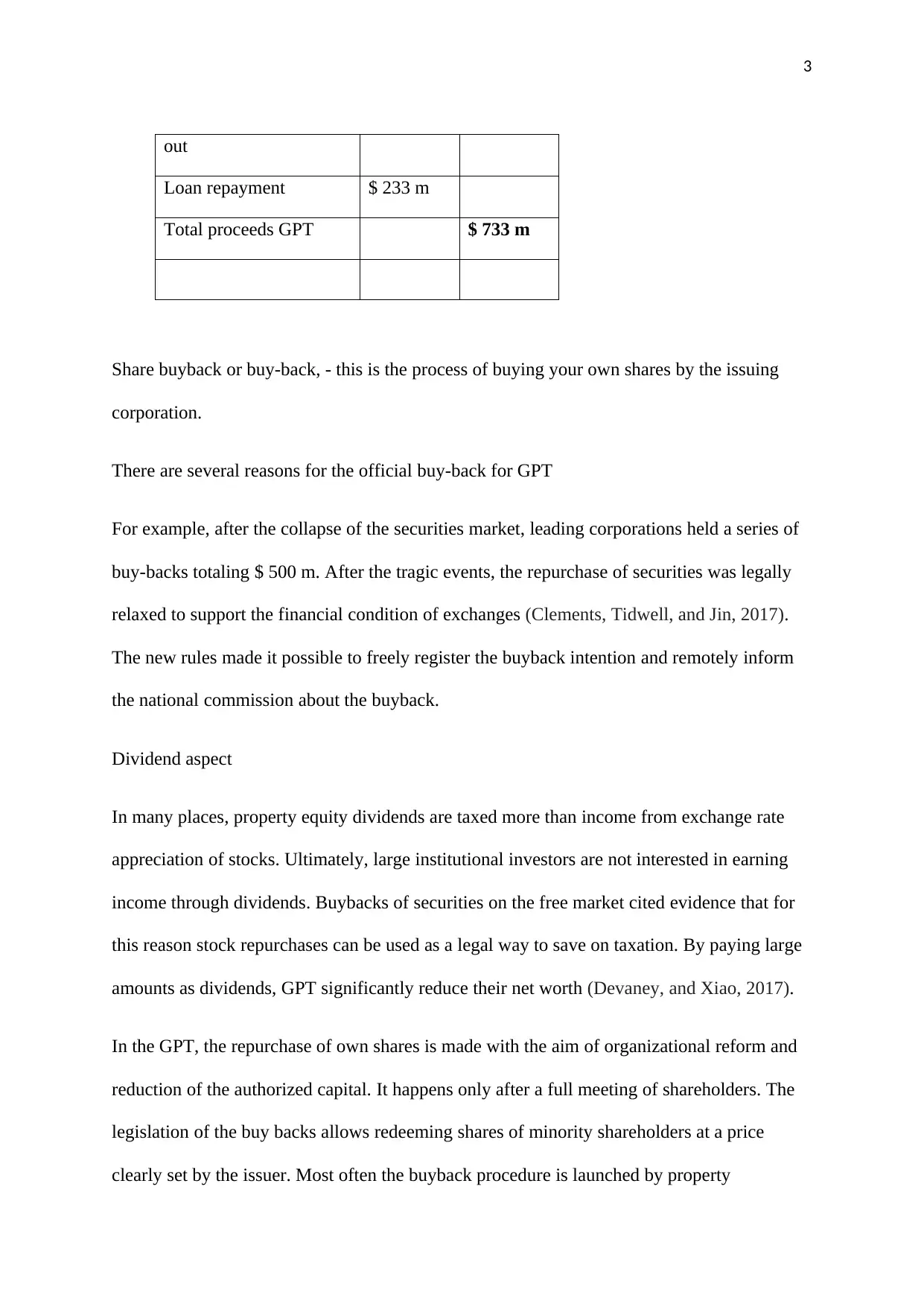

out

Loan repayment $ 233 m

Total proceeds GPT $ 733 m

Share buyback or buy-back, - this is the process of buying your own shares by the issuing

corporation.

There are several reasons for the official buy-back for GPT

For example, after the collapse of the securities market, leading corporations held a series of

buy-backs totaling $ 500 m. After the tragic events, the repurchase of securities was legally

relaxed to support the financial condition of exchanges (Clements, Tidwell, and Jin, 2017).

The new rules made it possible to freely register the buyback intention and remotely inform

the national commission about the buyback.

Dividend aspect

In many places, property equity dividends are taxed more than income from exchange rate

appreciation of stocks. Ultimately, large institutional investors are not interested in earning

income through dividends. Buybacks of securities on the free market cited evidence that for

this reason stock repurchases can be used as a legal way to save on taxation. By paying large

amounts as dividends, GPT significantly reduce their net worth (Devaney, and Xiao, 2017).

In the GPT, the repurchase of own shares is made with the aim of organizational reform and

reduction of the authorized capital. It happens only after a full meeting of shareholders. The

legislation of the buy backs allows redeeming shares of minority shareholders at a price

clearly set by the issuer. Most often the buyback procedure is launched by property

out

Loan repayment $ 233 m

Total proceeds GPT $ 733 m

Share buyback or buy-back, - this is the process of buying your own shares by the issuing

corporation.

There are several reasons for the official buy-back for GPT

For example, after the collapse of the securities market, leading corporations held a series of

buy-backs totaling $ 500 m. After the tragic events, the repurchase of securities was legally

relaxed to support the financial condition of exchanges (Clements, Tidwell, and Jin, 2017).

The new rules made it possible to freely register the buyback intention and remotely inform

the national commission about the buyback.

Dividend aspect

In many places, property equity dividends are taxed more than income from exchange rate

appreciation of stocks. Ultimately, large institutional investors are not interested in earning

income through dividends. Buybacks of securities on the free market cited evidence that for

this reason stock repurchases can be used as a legal way to save on taxation. By paying large

amounts as dividends, GPT significantly reduce their net worth (Devaney, and Xiao, 2017).

In the GPT, the repurchase of own shares is made with the aim of organizational reform and

reduction of the authorized capital. It happens only after a full meeting of shareholders. The

legislation of the buy backs allows redeeming shares of minority shareholders at a price

clearly set by the issuer. Most often the buyback procedure is launched by property

4

companies engaged in the export of oil, gas and precious metals. Excess cash exposes such

companies to excessive inflationary risks.

Real examples of stock buy backs

Stock repurchase is a form of investment that allows issuers with very low risks to invest in

their own business. According to a study conducted the property industry was the most

attractive spectrum of the economy for repurchases in the coming years.

Periodically, the stock market repurchases its own shares by the issuer. Why is this done and

what are the real reasons for these actions of companies on the exchange? Just like that, no

one will buy back their assets. Companies pursue some of their goals, which in turn should

bring them certain benefits. But what about ordinary private investors? What should they do

when the buyback is announced on the exchange? Sell, buy or stay away? Is it possible to

make money on it and what steps should be taken if information about the buyback has

appeared?

By purchasing GPT shares in the secondary market, the property company pursue their

interests first of all and increase investor confidence in it, which in most cases has a positive

effect on the further growth of quotations (Hogan, 2016). Consider the main reasons for the

repurchase in order to understand how the situation on the exchange may develop in the

future.

Quotes fall

companies engaged in the export of oil, gas and precious metals. Excess cash exposes such

companies to excessive inflationary risks.

Real examples of stock buy backs

Stock repurchase is a form of investment that allows issuers with very low risks to invest in

their own business. According to a study conducted the property industry was the most

attractive spectrum of the economy for repurchases in the coming years.

Periodically, the stock market repurchases its own shares by the issuer. Why is this done and

what are the real reasons for these actions of companies on the exchange? Just like that, no

one will buy back their assets. Companies pursue some of their goals, which in turn should

bring them certain benefits. But what about ordinary private investors? What should they do

when the buyback is announced on the exchange? Sell, buy or stay away? Is it possible to

make money on it and what steps should be taken if information about the buyback has

appeared?

By purchasing GPT shares in the secondary market, the property company pursue their

interests first of all and increase investor confidence in it, which in most cases has a positive

effect on the further growth of quotations (Hogan, 2016). Consider the main reasons for the

repurchase in order to understand how the situation on the exchange may develop in the

future.

Quotes fall

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

Due to a significant decline in stock prices and a further decline, investor confidence in these

securities (as well as in the company itself) also begins to decline. To stop a further decline

and increase the level of investor loyalty, the company makes a repurchase of shares in the

market.

GPT property stock repurchase actions show the confidence of the company's management in

the prospects for its development in the future. This has a positive effect on current quotes,

forcing them to grow a little. But usually this has a rather short-term effect. Everything will

depend on the volume of repurchased assets. With a fairly large demand, one can observe a

rather significant growth, which can develop into a long-term bullish trend.

Market undervaluation

If the opportunity arises to purchase shares in the secondary market at a good discount from

their fair price and finances allow, then why not take advantage of this. Such deviations

periodically occur on the market as a result of many factors, the main of which is investor

sentiment. The company can be quite stable in the market, show good pace of development

and profit. But with the appearance of only one negative factor, sometimes even not directly

affecting the company’s activities, investors begin to sell off their assets, which leads to

lower prices. But nothing happened to the business itself. He continues to work and develop.

Only here the capitalization of the company (and the shares themselves) can decrease during

this time by 20 - 30 - 40%. Such a discount is very attractive when purchasing own shares at

reduced prices today, the company is confident in their further growth. And after a while,

when quotes are restored, they can be sold back, decently earning on the difference.

Due to a significant decline in stock prices and a further decline, investor confidence in these

securities (as well as in the company itself) also begins to decline. To stop a further decline

and increase the level of investor loyalty, the company makes a repurchase of shares in the

market.

GPT property stock repurchase actions show the confidence of the company's management in

the prospects for its development in the future. This has a positive effect on current quotes,

forcing them to grow a little. But usually this has a rather short-term effect. Everything will

depend on the volume of repurchased assets. With a fairly large demand, one can observe a

rather significant growth, which can develop into a long-term bullish trend.

Market undervaluation

If the opportunity arises to purchase shares in the secondary market at a good discount from

their fair price and finances allow, then why not take advantage of this. Such deviations

periodically occur on the market as a result of many factors, the main of which is investor

sentiment. The company can be quite stable in the market, show good pace of development

and profit. But with the appearance of only one negative factor, sometimes even not directly

affecting the company’s activities, investors begin to sell off their assets, which leads to

lower prices. But nothing happened to the business itself. He continues to work and develop.

Only here the capitalization of the company (and the shares themselves) can decrease during

this time by 20 - 30 - 40%. Such a discount is very attractive when purchasing own shares at

reduced prices today, the company is confident in their further growth. And after a while,

when quotes are restored, they can be sold back, decently earning on the difference.

6

Potential traps and manipulations

Share buybacks can be used to manipulate a company's financial performance. The

withdrawal of a certain part of the assets from free circulation leads to a change in an

important coefficient - EPS earnings per share.

EPS = total company profit / number of shares outstanding

As a result, stocks are becoming underestimated by this fundamental indicator. And many

investors, seeing such an attractive option, start buying up supposedly cheap assets that are

sold at a good discount (Hogan, 2016).

If the planned percentage of repurchased shares is small that is $500 m, then this will

hardly affect the quotes. In extreme cases, it will have a short-term effect of price changes.

With sufficiently large volumes of buyback, one can observe a rather strong skew of demand

over supply, which naturally will push quotes up. When the conditions of the purchase

become attractive enough, a massive buying by investors begins in order to profit from this

procedure. As a result, supply far exceeds demand. And in order to satisfy all sellers, the

company determines the total number and amount of their applications and distributes it to

everyone in a certain proportion. For example, if the total planned redemption volume is 500

million, and applications have been filed in the amount of 5 billion, then each owner has a

buyback (Hoesli, Milcheva, and Moss, 2016).

Buy Back - repurchase of shares by their issuer. The purpose of buy back is to reduce

the number of valuable companies traded in the market. Thus, companies limit the supply of

Potential traps and manipulations

Share buybacks can be used to manipulate a company's financial performance. The

withdrawal of a certain part of the assets from free circulation leads to a change in an

important coefficient - EPS earnings per share.

EPS = total company profit / number of shares outstanding

As a result, stocks are becoming underestimated by this fundamental indicator. And many

investors, seeing such an attractive option, start buying up supposedly cheap assets that are

sold at a good discount (Hogan, 2016).

If the planned percentage of repurchased shares is small that is $500 m, then this will

hardly affect the quotes. In extreme cases, it will have a short-term effect of price changes.

With sufficiently large volumes of buyback, one can observe a rather strong skew of demand

over supply, which naturally will push quotes up. When the conditions of the purchase

become attractive enough, a massive buying by investors begins in order to profit from this

procedure. As a result, supply far exceeds demand. And in order to satisfy all sellers, the

company determines the total number and amount of their applications and distributes it to

everyone in a certain proportion. For example, if the total planned redemption volume is 500

million, and applications have been filed in the amount of 5 billion, then each owner has a

buyback (Hoesli, Milcheva, and Moss, 2016).

Buy Back - repurchase of shares by their issuer. The purpose of buy back is to reduce

the number of valuable companies traded in the market. Thus, companies limit the supply of

7

shares, increasing the demand for the remaining. Also, buy back is used to eliminate

unwanted shareholders from the game. Among other things, the buy-back procedure allows

companies to invest in themselves. By reducing the number of shares circulating in the

market, the issuer and existing investors increase their share in the business. Holding a buy

back suggests that the company’s management is optimistic and believes that the current

stock price is underestimated. Also, buy back can be the result of purely operational

processes. For example, a company needs to break free of cash or raise net income per share.

Buy back can be carried out according to 2 scenarios: 1. The company redeems its own

shares in the open market. 2. The company repurchases shares using options. Shareholders

are made an offer to redeem shares during a certain period with a premium. Premium - a

premium to the current price at which securities are traded on the stock exchange.

The terms of the option specify the buyback price and the time during which the

purchase will be made. The investor can either accept or reject the offer. If the market price is

higher than the one indicated in the option, investors do not sell their securities, as this is

unprofitable. The biggest risk is a sharp change in quotes decided to hold buy back using

options. Example, The stated price per share was $ 25-27 dollars, while the market price

fluctuated around $ 47 dollars apiece. That is, Dell had to pay 2 times more for its own

securities than they cost on the market. The fact is that at the time of the sale of options, the

indicated price seemed adequate due to the depression in the high-tech products market.

The situation was further aggravated by the fact that the repurchase of shares at an

inflated price coincided with a negative cash flow. Management is guided by the current

market situation and the financial condition of the company. According to experts, the

buyback reason is rather psychological. The buyback should convince investors of the

prospect of securities. Buy Back Program The term “Buy Back Program” has no relation to

shares, increasing the demand for the remaining. Also, buy back is used to eliminate

unwanted shareholders from the game. Among other things, the buy-back procedure allows

companies to invest in themselves. By reducing the number of shares circulating in the

market, the issuer and existing investors increase their share in the business. Holding a buy

back suggests that the company’s management is optimistic and believes that the current

stock price is underestimated. Also, buy back can be the result of purely operational

processes. For example, a company needs to break free of cash or raise net income per share.

Buy back can be carried out according to 2 scenarios: 1. The company redeems its own

shares in the open market. 2. The company repurchases shares using options. Shareholders

are made an offer to redeem shares during a certain period with a premium. Premium - a

premium to the current price at which securities are traded on the stock exchange.

The terms of the option specify the buyback price and the time during which the

purchase will be made. The investor can either accept or reject the offer. If the market price is

higher than the one indicated in the option, investors do not sell their securities, as this is

unprofitable. The biggest risk is a sharp change in quotes decided to hold buy back using

options. Example, The stated price per share was $ 25-27 dollars, while the market price

fluctuated around $ 47 dollars apiece. That is, Dell had to pay 2 times more for its own

securities than they cost on the market. The fact is that at the time of the sale of options, the

indicated price seemed adequate due to the depression in the high-tech products market.

The situation was further aggravated by the fact that the repurchase of shares at an

inflated price coincided with a negative cash flow. Management is guided by the current

market situation and the financial condition of the company. According to experts, the

buyback reason is rather psychological. The buyback should convince investors of the

prospect of securities. Buy Back Program The term “Buy Back Program” has no relation to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

the stock market. However, it is often used by American retailers to attract customers. The

general meaning of such shares is the exchange of old products for new with surcharge

(Lang, and Scholz, 2015).

Scenario 3

Scenario#3: GWSCF acquire a $725m retail portfolio on an initial yield of 5.95%

funded 100% from equity. GPT does participate in the GWSCF capital raising to

maintain its 28.7% ownership stake in GWSCF.

GWSCF acquired a $ 725 m portfolio that was funded by 100% equity on a yield of 5.95%.

Capital raising by GWSCF maintains a 28.7% ownership stake in the GPT. The capital raised

is 28.7%.

Capital is a combination of equity and borrowed capital. Equity - the amount of authorized,

reserve and additional capital, as well as retained earnings and earmarked financing. Under

the dominance of the financial concept of capital, a change in the value of net assets indicates

a change in the organization's own capital, i.e. about the growth or decrease in its

capitalization for the period (Lang, and Schaefers, 2015).

respectively.

Activity Amount($) Amount($)

GWSCF- Acquired $725 m

Equity Funding 100%

Yield 5.95%

Total proceeds GPT 28.7%

the stock market. However, it is often used by American retailers to attract customers. The

general meaning of such shares is the exchange of old products for new with surcharge

(Lang, and Scholz, 2015).

Scenario 3

Scenario#3: GWSCF acquire a $725m retail portfolio on an initial yield of 5.95%

funded 100% from equity. GPT does participate in the GWSCF capital raising to

maintain its 28.7% ownership stake in GWSCF.

GWSCF acquired a $ 725 m portfolio that was funded by 100% equity on a yield of 5.95%.

Capital raising by GWSCF maintains a 28.7% ownership stake in the GPT. The capital raised

is 28.7%.

Capital is a combination of equity and borrowed capital. Equity - the amount of authorized,

reserve and additional capital, as well as retained earnings and earmarked financing. Under

the dominance of the financial concept of capital, a change in the value of net assets indicates

a change in the organization's own capital, i.e. about the growth or decrease in its

capitalization for the period (Lang, and Schaefers, 2015).

respectively.

Activity Amount($) Amount($)

GWSCF- Acquired $725 m

Equity Funding 100%

Yield 5.95%

Total proceeds GPT 28.7%

9

Capital

Borrowed capital is loans, loans and payables, i.e. obligations of the organization to

individuals and legal entities.

Funds supporting the activities of the enterprise are usually divided into own and borrowed.

Borrowed capital is capital that is attracted by the company from the outside in the form of

loans, financial assistance, amounts received on bail, and other external sources for a specific

period, on certain conditions, under any guarantees.

Return on equity

Return on Ordinary Share Capital (ROCE) is calculated as the ratio of net profit minus

dividends on preferred shares to ordinary share capital. The formula for calculating the

indicator is as follows:

ROCE = (net income - dividends on preferred shares) / average annual amount of ordinary

share capital

The average annual value of assets is calculated on the basis of the balance sheet of the

enterprise as the half of the sum of assets at the beginning and at the end of the year or as the

arithmetic average of the balance at the end of the quarters included in the reporting year

(Moss, 2018).

If the company does not have preferred shares and is not bound by the obligation to pay

dividends, then the value of this indicator is equivalent to ROE.

Capital

Borrowed capital is loans, loans and payables, i.e. obligations of the organization to

individuals and legal entities.

Funds supporting the activities of the enterprise are usually divided into own and borrowed.

Borrowed capital is capital that is attracted by the company from the outside in the form of

loans, financial assistance, amounts received on bail, and other external sources for a specific

period, on certain conditions, under any guarantees.

Return on equity

Return on Ordinary Share Capital (ROCE) is calculated as the ratio of net profit minus

dividends on preferred shares to ordinary share capital. The formula for calculating the

indicator is as follows:

ROCE = (net income - dividends on preferred shares) / average annual amount of ordinary

share capital

The average annual value of assets is calculated on the basis of the balance sheet of the

enterprise as the half of the sum of assets at the beginning and at the end of the year or as the

arithmetic average of the balance at the end of the quarters included in the reporting year

(Moss, 2018).

If the company does not have preferred shares and is not bound by the obligation to pay

dividends, then the value of this indicator is equivalent to ROE.

10

ROIC = NOPLAT / invested capital * 100%

where, NOPLAT is net operating income net of adjusted taxes.

Invested capital - capital invested in the main activities of the company. As invested

capital, only capital invested in the main activity of the company should be considered, just

as the profit in question is the profit from the main activity. In general terms, invested capital

can be calculated as the sum of current assets in core activities, net fixed assets and net other

assets (net of interest-free liabilities). Another calculation option - the amount of equity and

long-term liabilities is considered as invested funds. Details of determining the amount of

invested capital will depend on the characteristics of accounting and business structure.

The main condition that must be achieved in this case is that the analysis should take

into account that and only that capital that was used to make a profit, included in the

calculation. In practice, they often resort to a simplified approach, in which the main activity

of the company is not distinguished, and the analysis is conducted for all investments and all

income. The error of this assumption will depend on the size of the non-operating profit of

the company in the period under review and how large are the investments in non-core

From the ratio it is clear that the correct use of borrowed funds allows to increase the income

of shareholders due to the effect of financial leverage. This effect is achieved due to the fact

that the profit received from the activities of the company is significantly higher than the loan

rate. By the amount of financial leverage, you can determine how the borrowed funds are

used - for the development of production or for patching holes in the budget.

ROA = ((net profit + interest payments) * (1 - tax rate)) / assets of the enterprise * 100%

Net profit (Net Profit) is the difference between the revenue received and all expenses of the

company for the corresponding period. Includes tax expense.

ROIC = NOPLAT / invested capital * 100%

where, NOPLAT is net operating income net of adjusted taxes.

Invested capital - capital invested in the main activities of the company. As invested

capital, only capital invested in the main activity of the company should be considered, just

as the profit in question is the profit from the main activity. In general terms, invested capital

can be calculated as the sum of current assets in core activities, net fixed assets and net other

assets (net of interest-free liabilities). Another calculation option - the amount of equity and

long-term liabilities is considered as invested funds. Details of determining the amount of

invested capital will depend on the characteristics of accounting and business structure.

The main condition that must be achieved in this case is that the analysis should take

into account that and only that capital that was used to make a profit, included in the

calculation. In practice, they often resort to a simplified approach, in which the main activity

of the company is not distinguished, and the analysis is conducted for all investments and all

income. The error of this assumption will depend on the size of the non-operating profit of

the company in the period under review and how large are the investments in non-core

From the ratio it is clear that the correct use of borrowed funds allows to increase the income

of shareholders due to the effect of financial leverage. This effect is achieved due to the fact

that the profit received from the activities of the company is significantly higher than the loan

rate. By the amount of financial leverage, you can determine how the borrowed funds are

used - for the development of production or for patching holes in the budget.

ROA = ((net profit + interest payments) * (1 - tax rate)) / assets of the enterprise * 100%

Net profit (Net Profit) is the difference between the revenue received and all expenses of the

company for the corresponding period. Includes tax expense.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

Assets of an enterprise (Assets) - a combination of property and funds belonging to an

enterprise, firm, company (buildings, structures, machinery and equipment, inventories, bank

deposits, securities, patents, copyrights, property having a monetary value). For calculations,

the average annual value of the company’s assets is used (the amount of assets at the

beginning and at the end of the year divided in half (Owusu Junior, et al, 2019).

Gross profit margin (GPM) is another name for this ratio - Gross margin ratio.

Operating profit margin (OPM) - shows the share of operating profit in sales. It is calculated

by the formula:

OPM = OP / NS = Operating Profit / Total Revenue

Net profit margin (NPM) - shows the share of net profit in sales. It is calculated by the

formula:

NPM = NI / NS = Net Profit / Total Revenue

Coefficients that assess the profitability of capital invested in the company. The

calculation is made for the annual period using the average value of the corresponding items

of assets and liabilities. To calculate for a period of less than one year, the profit value is

multiplied by the corresponding coefficient (12, 4, 2), and the average value of current assets

for the period is used. To obtain the values in percent, as in previous cases, it is necessary to

multiply the value of the coefficient by 100%.

Return on current assets (RCA) - demonstrates the ability of the company to provide a

sufficient amount of profit in relation to the current working capital of the company. The

higher the value of this coefficient, the more efficiently used working capital.

It is calculated by the formula: NI / CA = Net Profit / Working Capital.

Assets of an enterprise (Assets) - a combination of property and funds belonging to an

enterprise, firm, company (buildings, structures, machinery and equipment, inventories, bank

deposits, securities, patents, copyrights, property having a monetary value). For calculations,

the average annual value of the company’s assets is used (the amount of assets at the

beginning and at the end of the year divided in half (Owusu Junior, et al, 2019).

Gross profit margin (GPM) is another name for this ratio - Gross margin ratio.

Operating profit margin (OPM) - shows the share of operating profit in sales. It is calculated

by the formula:

OPM = OP / NS = Operating Profit / Total Revenue

Net profit margin (NPM) - shows the share of net profit in sales. It is calculated by the

formula:

NPM = NI / NS = Net Profit / Total Revenue

Coefficients that assess the profitability of capital invested in the company. The

calculation is made for the annual period using the average value of the corresponding items

of assets and liabilities. To calculate for a period of less than one year, the profit value is

multiplied by the corresponding coefficient (12, 4, 2), and the average value of current assets

for the period is used. To obtain the values in percent, as in previous cases, it is necessary to

multiply the value of the coefficient by 100%.

Return on current assets (RCA) - demonstrates the ability of the company to provide a

sufficient amount of profit in relation to the current working capital of the company. The

higher the value of this coefficient, the more efficiently used working capital.

It is calculated by the formula: NI / CA = Net Profit / Working Capital.

12

Return on non-current assets (RFA) - demonstrates the ability of the company to provide a

sufficient amount of profit in relation to fixed assets of the company. The higher the value of

this coefficient, the more efficiently the fixed assets are used. It is calculated by the formula:

NI / FA = Net profit / Working capital.

Determines the proportion of funds invested in the activities of the enterprise by its

owners. The higher the value of this coefficient, the more financially stable, stable and

independent of external creditors of the enterprise (Rajagopal, 2015).

The concentration ratio of equity capital is calculated by the following formula:

Ksk = SL \ WB

where SK is the WB equity capital is the balance sheet currency.

Conclusion and Recommendations

Management is guided by the current market situation and the financial condition of

the company. Thus, own working capital represents the share of current assets of the

enterprise, free from short-term obligations. If current assets exceed the amount of short-term

liabilities, the company can not only repay these obligations, but also has reserves in working

capital. As soon as the market price falls below the mark stated in the option, the transaction

will be profitable for investors. If the option expires, the company must redeem the shares at

the stated price.

References

Return on non-current assets (RFA) - demonstrates the ability of the company to provide a

sufficient amount of profit in relation to fixed assets of the company. The higher the value of

this coefficient, the more efficiently the fixed assets are used. It is calculated by the formula:

NI / FA = Net profit / Working capital.

Determines the proportion of funds invested in the activities of the enterprise by its

owners. The higher the value of this coefficient, the more financially stable, stable and

independent of external creditors of the enterprise (Rajagopal, 2015).

The concentration ratio of equity capital is calculated by the following formula:

Ksk = SL \ WB

where SK is the WB equity capital is the balance sheet currency.

Conclusion and Recommendations

Management is guided by the current market situation and the financial condition of

the company. Thus, own working capital represents the share of current assets of the

enterprise, free from short-term obligations. If current assets exceed the amount of short-term

liabilities, the company can not only repay these obligations, but also has reserves in working

capital. As soon as the market price falls below the mark stated in the option, the transaction

will be profitable for investors. If the option expires, the company must redeem the shares at

the stated price.

References

13

Anule, S. A., Jagun, Z. T., Omirin, M. M., Bornoma, A. H., & Ahmed, A. A. (2018).

Performance evaluation on aggregate bases of real estate in a mixed asset portfolio in

Lagos. Open Journal of Science and Technology, 1(1), 1-4.

Clements, S., Tidwell, A. and Jin, C., 2017. Futures markets and real estate public equity:

Connectivity of lumber futures and Timber REITs. Journal of Forest Economics, 28, pp.70-

79.

Devaney, S. and Xiao, Q., 2017. Cyclical co-movements of private real estate, public real

estate and equity markets: A cross-continental spectrum. Journal of Multinational Financial

Management, 42, pp.132-151.

Hogan, J.D., 2016. The Impact of Own, Rival and Market Effects on Real Estate Private

Equity Fund Performance.

Hoesli, M.E., Milcheva, S. and Moss, A., 2016. Real Estate Company Reactions to Financial

Market Regulation.

Kiehelä, S. and Falkenbach, H., 2015. Performance of non-core private equity real estate

funds: a European view. The Journal of Portfolio Management, 41(6), pp.62-72.

Lang, S. and Scholz, A., 2015. The diverging role of the systematic risk factors: evidence

from real estate stock markets. Journal of Property Investment & Finance, 33(1), pp.81-106.

Lang, S. and Schaefers, W., 2015. Examining the sentiment-return relationship in European

real estate stock markets. Journal of European Real Estate Research, 8(1), pp.24-45.

Moss, A., 2018. The use of listed real estate in Real Asset Funds. Reading.

Anule, S. A., Jagun, Z. T., Omirin, M. M., Bornoma, A. H., & Ahmed, A. A. (2018).

Performance evaluation on aggregate bases of real estate in a mixed asset portfolio in

Lagos. Open Journal of Science and Technology, 1(1), 1-4.

Clements, S., Tidwell, A. and Jin, C., 2017. Futures markets and real estate public equity:

Connectivity of lumber futures and Timber REITs. Journal of Forest Economics, 28, pp.70-

79.

Devaney, S. and Xiao, Q., 2017. Cyclical co-movements of private real estate, public real

estate and equity markets: A cross-continental spectrum. Journal of Multinational Financial

Management, 42, pp.132-151.

Hogan, J.D., 2016. The Impact of Own, Rival and Market Effects on Real Estate Private

Equity Fund Performance.

Hoesli, M.E., Milcheva, S. and Moss, A., 2016. Real Estate Company Reactions to Financial

Market Regulation.

Kiehelä, S. and Falkenbach, H., 2015. Performance of non-core private equity real estate

funds: a European view. The Journal of Portfolio Management, 41(6), pp.62-72.

Lang, S. and Scholz, A., 2015. The diverging role of the systematic risk factors: evidence

from real estate stock markets. Journal of Property Investment & Finance, 33(1), pp.81-106.

Lang, S. and Schaefers, W., 2015. Examining the sentiment-return relationship in European

real estate stock markets. Journal of European Real Estate Research, 8(1), pp.24-45.

Moss, A., 2018. The use of listed real estate in Real Asset Funds. Reading.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14

Owusu Junior, P., Tweneboah, G., Ijasan, K. and Jeyasreedharan, N., 2019. Modelling return

behaviour of global real estate investment trusts equities: Evidence from generalised lambda

distribution. Journal of European Real Estate Research.

Rajagopal, S., 2015. LONG MEMORY IN STOCK RETURNS: A STUDY OF REAL

ESTATE EQUITIES IN AN EMERGING MARKET. In Allied Academies International

Conference. Academy of Accounting and Financial Studies. Proceedings (Vol. 20, No. 1, p.

31). Jordan Whitney Enterprises, Inc.

Owusu Junior, P., Tweneboah, G., Ijasan, K. and Jeyasreedharan, N., 2019. Modelling return

behaviour of global real estate investment trusts equities: Evidence from generalised lambda

distribution. Journal of European Real Estate Research.

Rajagopal, S., 2015. LONG MEMORY IN STOCK RETURNS: A STUDY OF REAL

ESTATE EQUITIES IN AN EMERGING MARKET. In Allied Academies International

Conference. Academy of Accounting and Financial Studies. Proceedings (Vol. 20, No. 1, p.

31). Jordan Whitney Enterprises, Inc.

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.