Audit Risk and Procedures for Always Precise Instruments Pty Limited

VerifiedAdded on 2023/01/11

|16

|3840

|46

AI Summary

This memo discusses the identification of potential audit risks for Always Precise Instruments Pty Limited and suggests audit procedures to reduce those risks. The risks include stock out or overstock, incorrect recording of raw material receipts, and lack of emergency inventory options. The suggested procedures involve regular stock inspection, manual receipt counting, and installation of emergency inventory options.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

AUDITING

2019

2019

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Audit

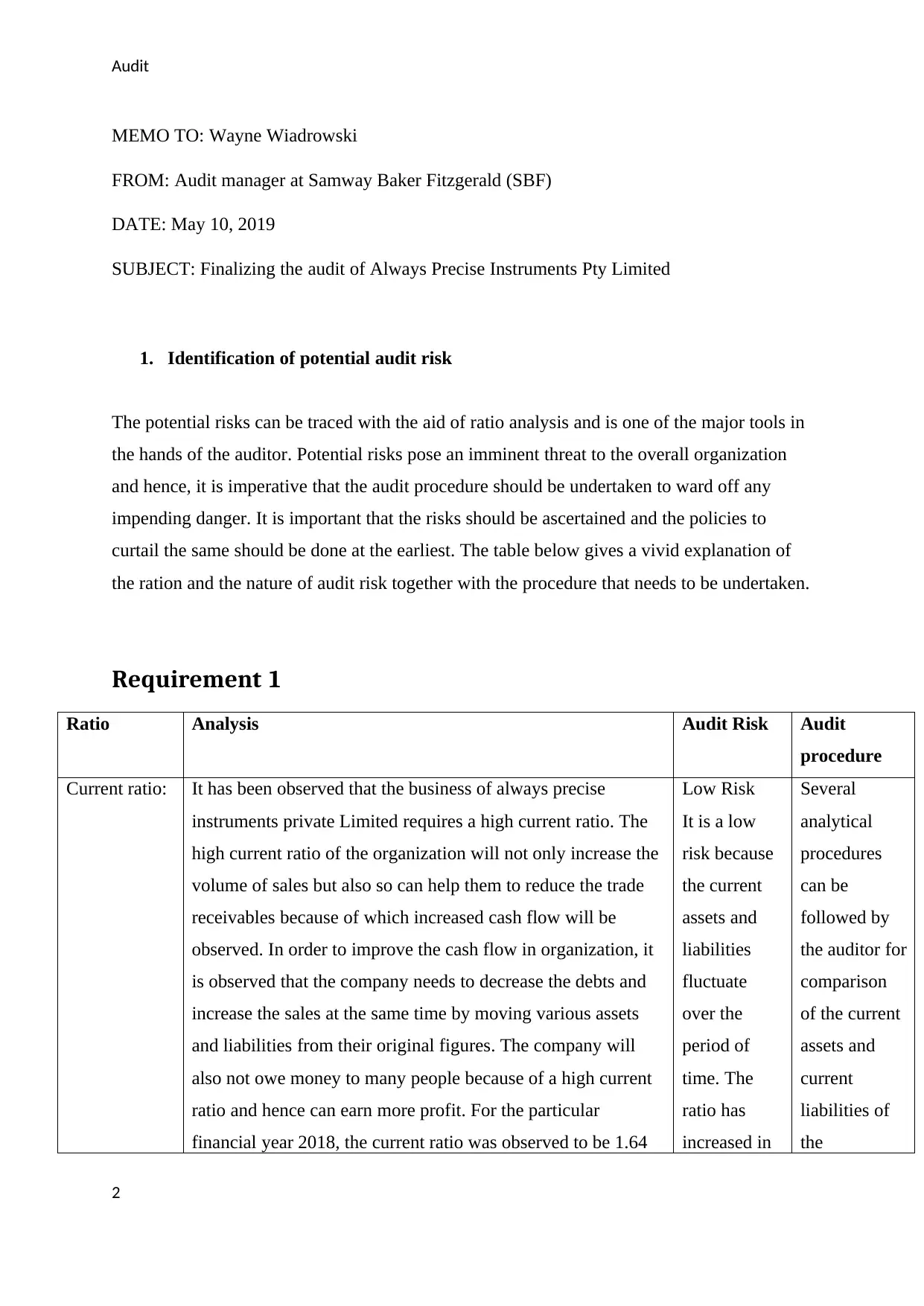

MEMO TO: Wayne Wiadrowski

FROM: Audit manager at Samway Baker Fitzgerald (SBF)

DATE: May 10, 2019

SUBJECT: Finalizing the audit of Always Precise Instruments Pty Limited

1. Identification of potential audit risk

The potential risks can be traced with the aid of ratio analysis and is one of the major tools in

the hands of the auditor. Potential risks pose an imminent threat to the overall organization

and hence, it is imperative that the audit procedure should be undertaken to ward off any

impending danger. It is important that the risks should be ascertained and the policies to

curtail the same should be done at the earliest. The table below gives a vivid explanation of

the ration and the nature of audit risk together with the procedure that needs to be undertaken.

Requirement 1

Ratio Analysis Audit Risk Audit

procedure

Current ratio: It has been observed that the business of always precise

instruments private Limited requires a high current ratio. The

high current ratio of the organization will not only increase the

volume of sales but also so can help them to reduce the trade

receivables because of which increased cash flow will be

observed. In order to improve the cash flow in organization, it

is observed that the company needs to decrease the debts and

increase the sales at the same time by moving various assets

and liabilities from their original figures. The company will

also not owe money to many people because of a high current

ratio and hence can earn more profit. For the particular

financial year 2018, the current ratio was observed to be 1.64

Low Risk

It is a low

risk because

the current

assets and

liabilities

fluctuate

over the

period of

time. The

ratio has

increased in

Several

analytical

procedures

can be

followed by

the auditor for

comparison

of the current

assets and

current

liabilities of

the

2

MEMO TO: Wayne Wiadrowski

FROM: Audit manager at Samway Baker Fitzgerald (SBF)

DATE: May 10, 2019

SUBJECT: Finalizing the audit of Always Precise Instruments Pty Limited

1. Identification of potential audit risk

The potential risks can be traced with the aid of ratio analysis and is one of the major tools in

the hands of the auditor. Potential risks pose an imminent threat to the overall organization

and hence, it is imperative that the audit procedure should be undertaken to ward off any

impending danger. It is important that the risks should be ascertained and the policies to

curtail the same should be done at the earliest. The table below gives a vivid explanation of

the ration and the nature of audit risk together with the procedure that needs to be undertaken.

Requirement 1

Ratio Analysis Audit Risk Audit

procedure

Current ratio: It has been observed that the business of always precise

instruments private Limited requires a high current ratio. The

high current ratio of the organization will not only increase the

volume of sales but also so can help them to reduce the trade

receivables because of which increased cash flow will be

observed. In order to improve the cash flow in organization, it

is observed that the company needs to decrease the debts and

increase the sales at the same time by moving various assets

and liabilities from their original figures. The company will

also not owe money to many people because of a high current

ratio and hence can earn more profit. For the particular

financial year 2018, the current ratio was observed to be 1.64

Low Risk

It is a low

risk because

the current

assets and

liabilities

fluctuate

over the

period of

time. The

ratio has

increased in

Several

analytical

procedures

can be

followed by

the auditor for

comparison

of the current

assets and

current

liabilities of

the

2

Audit

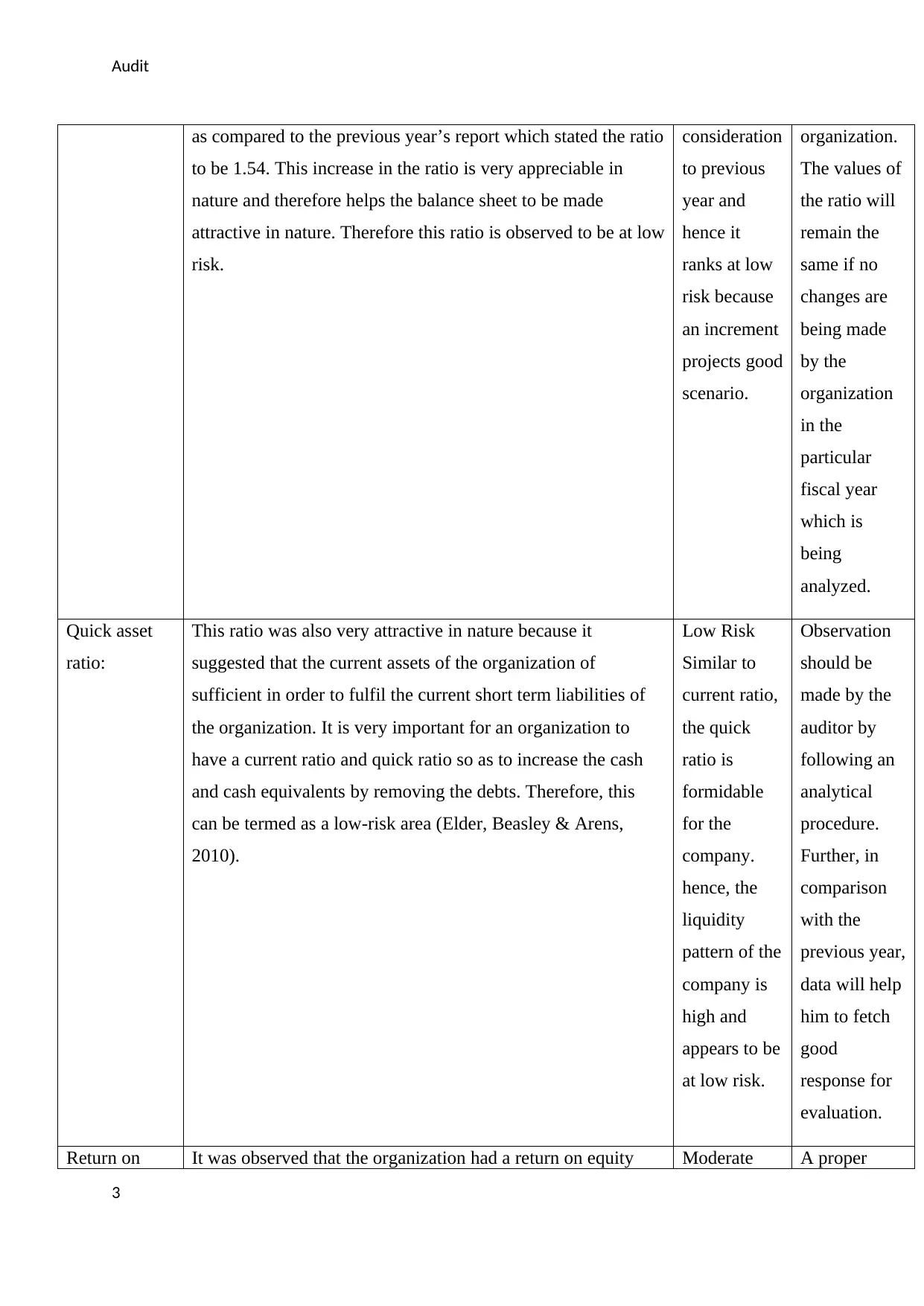

as compared to the previous year’s report which stated the ratio

to be 1.54. This increase in the ratio is very appreciable in

nature and therefore helps the balance sheet to be made

attractive in nature. Therefore this ratio is observed to be at low

risk.

consideration

to previous

year and

hence it

ranks at low

risk because

an increment

projects good

scenario.

organization.

The values of

the ratio will

remain the

same if no

changes are

being made

by the

organization

in the

particular

fiscal year

which is

being

analyzed.

Quick asset

ratio:

This ratio was also very attractive in nature because it

suggested that the current assets of the organization of

sufficient in order to fulfil the current short term liabilities of

the organization. It is very important for an organization to

have a current ratio and quick ratio so as to increase the cash

and cash equivalents by removing the debts. Therefore, this

can be termed as a low-risk area (Elder, Beasley & Arens,

2010).

Low Risk

Similar to

current ratio,

the quick

ratio is

formidable

for the

company.

hence, the

liquidity

pattern of the

company is

high and

appears to be

at low risk.

Observation

should be

made by the

auditor by

following an

analytical

procedure.

Further, in

comparison

with the

previous year,

data will help

him to fetch

good

response for

evaluation.

Return on It was observed that the organization had a return on equity Moderate A proper

3

as compared to the previous year’s report which stated the ratio

to be 1.54. This increase in the ratio is very appreciable in

nature and therefore helps the balance sheet to be made

attractive in nature. Therefore this ratio is observed to be at low

risk.

consideration

to previous

year and

hence it

ranks at low

risk because

an increment

projects good

scenario.

organization.

The values of

the ratio will

remain the

same if no

changes are

being made

by the

organization

in the

particular

fiscal year

which is

being

analyzed.

Quick asset

ratio:

This ratio was also very attractive in nature because it

suggested that the current assets of the organization of

sufficient in order to fulfil the current short term liabilities of

the organization. It is very important for an organization to

have a current ratio and quick ratio so as to increase the cash

and cash equivalents by removing the debts. Therefore, this

can be termed as a low-risk area (Elder, Beasley & Arens,

2010).

Low Risk

Similar to

current ratio,

the quick

ratio is

formidable

for the

company.

hence, the

liquidity

pattern of the

company is

high and

appears to be

at low risk.

Observation

should be

made by the

auditor by

following an

analytical

procedure.

Further, in

comparison

with the

previous year,

data will help

him to fetch

good

response for

evaluation.

Return on It was observed that the organization had a return on equity Moderate A proper

3

Audit

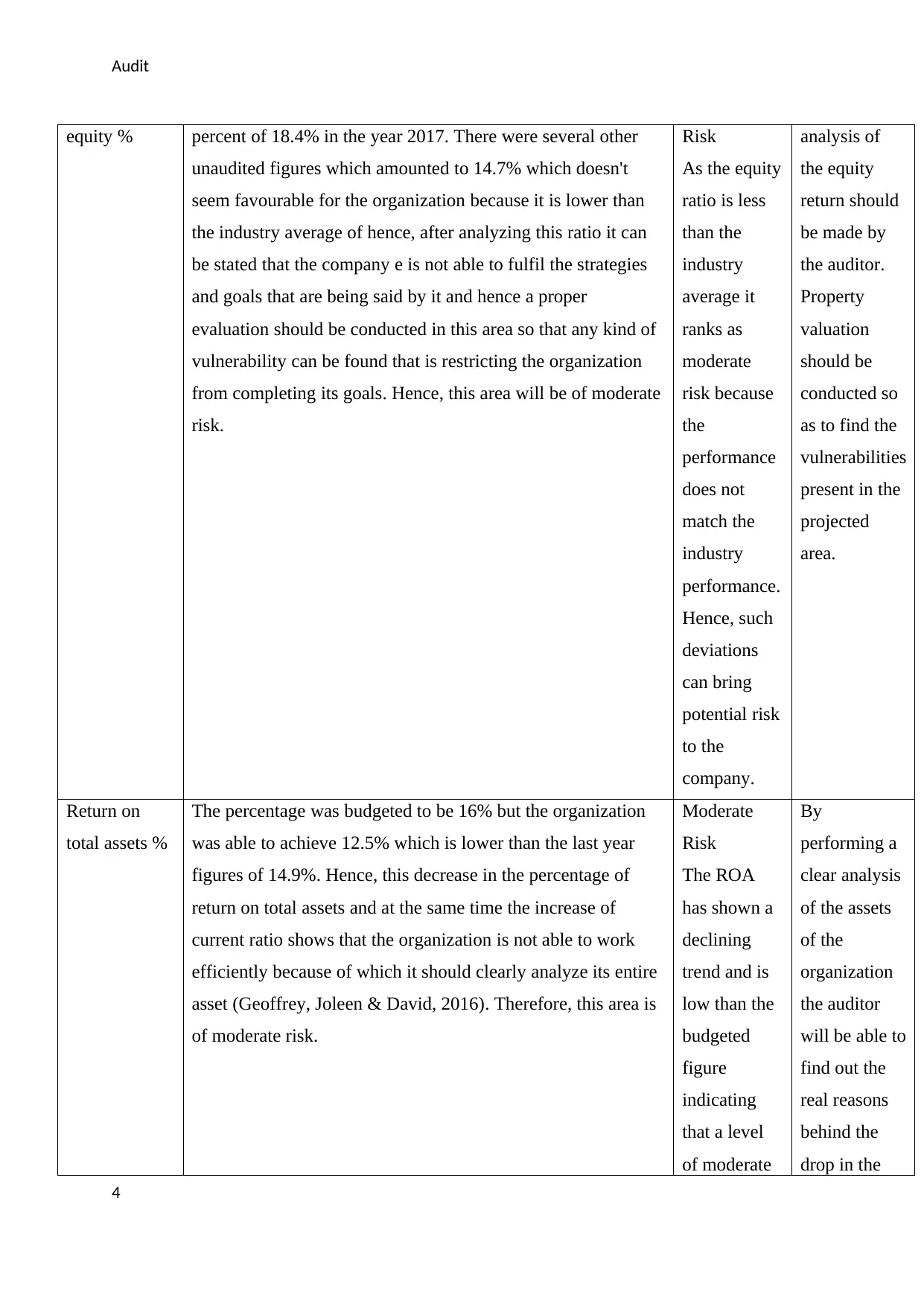

equity % percent of 18.4% in the year 2017. There were several other

unaudited figures which amounted to 14.7% which doesn't

seem favourable for the organization because it is lower than

the industry average of hence, after analyzing this ratio it can

be stated that the company e is not able to fulfil the strategies

and goals that are being said by it and hence a proper

evaluation should be conducted in this area so that any kind of

vulnerability can be found that is restricting the organization

from completing its goals. Hence, this area will be of moderate

risk.

Risk

As the equity

ratio is less

than the

industry

average it

ranks as

moderate

risk because

the

performance

does not

match the

industry

performance.

Hence, such

deviations

can bring

potential risk

to the

company.

analysis of

the equity

return should

be made by

the auditor.

Property

valuation

should be

conducted so

as to find the

vulnerabilities

present in the

projected

area.

Return on

total assets %

The percentage was budgeted to be 16% but the organization

was able to achieve 12.5% which is lower than the last year

figures of 14.9%. Hence, this decrease in the percentage of

return on total assets and at the same time the increase of

current ratio shows that the organization is not able to work

efficiently because of which it should clearly analyze its entire

asset (Geoffrey, Joleen & David, 2016). Therefore, this area is

of moderate risk.

Moderate

Risk

The ROA

has shown a

declining

trend and is

low than the

budgeted

figure

indicating

that a level

of moderate

By

performing a

clear analysis

of the assets

of the

organization

the auditor

will be able to

find out the

real reasons

behind the

drop in the

4

equity % percent of 18.4% in the year 2017. There were several other

unaudited figures which amounted to 14.7% which doesn't

seem favourable for the organization because it is lower than

the industry average of hence, after analyzing this ratio it can

be stated that the company e is not able to fulfil the strategies

and goals that are being said by it and hence a proper

evaluation should be conducted in this area so that any kind of

vulnerability can be found that is restricting the organization

from completing its goals. Hence, this area will be of moderate

risk.

Risk

As the equity

ratio is less

than the

industry

average it

ranks as

moderate

risk because

the

performance

does not

match the

industry

performance.

Hence, such

deviations

can bring

potential risk

to the

company.

analysis of

the equity

return should

be made by

the auditor.

Property

valuation

should be

conducted so

as to find the

vulnerabilities

present in the

projected

area.

Return on

total assets %

The percentage was budgeted to be 16% but the organization

was able to achieve 12.5% which is lower than the last year

figures of 14.9%. Hence, this decrease in the percentage of

return on total assets and at the same time the increase of

current ratio shows that the organization is not able to work

efficiently because of which it should clearly analyze its entire

asset (Geoffrey, Joleen & David, 2016). Therefore, this area is

of moderate risk.

Moderate

Risk

The ROA

has shown a

declining

trend and is

low than the

budgeted

figure

indicating

that a level

of moderate

By

performing a

clear analysis

of the assets

of the

organization

the auditor

will be able to

find out the

real reasons

behind the

drop in the

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Audit

risk exists

and it is

imperative

for the

company to

ensure that

the assets are

put to

effective use

so that the

problem can

be reduced.

ratio of return

on assets.

Gross margin

%

The gross margin of the organization was observed to be 6.5%

which was much lower than the budgeted data because of

which it is very important for the company to call for a detailed

analysis so that any kind of risk present can be identified (Gay

& Simnet, 2015).

High Risk

Low gross

margin is

high risk

because it

reflects the

potential of

the company

in terms of

sales. The

company

failed to

attained a

strong figure

and hence

comes under

panel of high

risk

Because of

the high-risk

present in the

area it is

important for

the order to

compare the

reports from

the last year.

Marketing

expense %

The marketing expense ratio of the company was budgeted to

visit 3.6% but it actually amounted to 4.4% which is not much

affected. They include the cost of advertisement, selling,

Low risk

Marketing

expenses

The auditor

should

analyze the

5

risk exists

and it is

imperative

for the

company to

ensure that

the assets are

put to

effective use

so that the

problem can

be reduced.

ratio of return

on assets.

Gross margin

%

The gross margin of the organization was observed to be 6.5%

which was much lower than the budgeted data because of

which it is very important for the company to call for a detailed

analysis so that any kind of risk present can be identified (Gay

& Simnet, 2015).

High Risk

Low gross

margin is

high risk

because it

reflects the

potential of

the company

in terms of

sales. The

company

failed to

attained a

strong figure

and hence

comes under

panel of high

risk

Because of

the high-risk

present in the

area it is

important for

the order to

compare the

reports from

the last year.

Marketing

expense %

The marketing expense ratio of the company was budgeted to

visit 3.6% but it actually amounted to 4.4% which is not much

affected. They include the cost of advertisement, selling,

Low risk

Marketing

expenses

The auditor

should

analyze the

5

Audit

distribution, etc. fluctuates

over a period

of time and

hence not of

much

concern

because it is

influenced

by various

factors. Since

a small

increment is

seen

therefore, it

is not of high

risk.

shortfalls of

the

organizations

and undertake

marketing

procedures

that can help

to know the

differences

present in the

organization.

Admin

expenses/sales

%

Administrative expenses are the expenses which are incurred

by the organization to fulfil the desktop applications of

executive salaries, director remuneration, etc. The budgeted

figure and actual figure were similar because of which this area

does it consist of many risks (Gay & Simnet, 2015).

Low Risk

Since the

budgeted

figure and

actual figure

were similar

therefore, it

calls for no

action as the

expenses

were

managed

effectively

therefore

have any

risk.

It is important

for the auditor

to analyze the

data so as to

differentiate

between the

actual and

budgeted data

(Roach,

2010).

Times interest The interest earned by the organization was amounting to 3.6 High risk Because this

6

distribution, etc. fluctuates

over a period

of time and

hence not of

much

concern

because it is

influenced

by various

factors. Since

a small

increment is

seen

therefore, it

is not of high

risk.

shortfalls of

the

organizations

and undertake

marketing

procedures

that can help

to know the

differences

present in the

organization.

Admin

expenses/sales

%

Administrative expenses are the expenses which are incurred

by the organization to fulfil the desktop applications of

executive salaries, director remuneration, etc. The budgeted

figure and actual figure were similar because of which this area

does it consist of many risks (Gay & Simnet, 2015).

Low Risk

Since the

budgeted

figure and

actual figure

were similar

therefore, it

calls for no

action as the

expenses

were

managed

effectively

therefore

have any

risk.

It is important

for the auditor

to analyze the

data so as to

differentiate

between the

actual and

budgeted data

(Roach,

2010).

Times interest The interest earned by the organization was amounting to 3.6 High risk Because this

6

Audit

earned Times. Hence, because of the lower ratio, profit can be reduced

and organizational debts can increase because of which this

area is considered to have risk.

Since the

ratio for the

concerned

company is

low, it

appears that

the debt

payment will

be an issue in

making

payments.

is an area of

high risk it is

important for

the auditor to

trace all the

interest that

has been

earned and

weaknesses

present in that

area (Wright

& Charles,

2012).

Days in

inventory

The number of days for which the inventory was kept on hold

by the organization also increased but not with high volatility

because of which decrease is considered to be at low risk.

Low risk

Inventories

tend to have

volatility

depending

from time to

time and

going by the

scenario it

can be said

that such

situation

does not pose

a huge risk.

Proper trend

analysis can

be conducted

by the auditor

for

understanding

the increases

in inventory

(Gay &

Simnet,

2015).

Days in

accounts

receivable

The total number of days for which the account receivables

were kept by the organization was observed to be 53. The total

debt collection of the organization is very ineffective in nature

because of which the budgeted efficiency levels are being

affected. This area constitutes of high risk (Ghandhar &

High risk

The accounts

receivables

kept by the

business is

The auditor

should create

a trend line

and analyze

all the

7

earned Times. Hence, because of the lower ratio, profit can be reduced

and organizational debts can increase because of which this

area is considered to have risk.

Since the

ratio for the

concerned

company is

low, it

appears that

the debt

payment will

be an issue in

making

payments.

is an area of

high risk it is

important for

the auditor to

trace all the

interest that

has been

earned and

weaknesses

present in that

area (Wright

& Charles,

2012).

Days in

inventory

The number of days for which the inventory was kept on hold

by the organization also increased but not with high volatility

because of which decrease is considered to be at low risk.

Low risk

Inventories

tend to have

volatility

depending

from time to

time and

going by the

scenario it

can be said

that such

situation

does not pose

a huge risk.

Proper trend

analysis can

be conducted

by the auditor

for

understanding

the increases

in inventory

(Gay &

Simnet,

2015).

Days in

accounts

receivable

The total number of days for which the account receivables

were kept by the organization was observed to be 53. The total

debt collection of the organization is very ineffective in nature

because of which the budgeted efficiency levels are being

affected. This area constitutes of high risk (Ghandhar &

High risk

The accounts

receivables

kept by the

business is

The auditor

should create

a trend line

and analyze

all the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

Tsahuridu, 2013). high and

hence, this

leads to an

alteration in

the

efficiency of

the budget.

This hurts

the

company’s

performance

and hence,

high risk

follows.

expenses and

bad debts so

as to find

what wrong

practices are

being

conducted by

the

management.

Debt to equity

ratio: 1

The debt to equity ratio of the organization was higher than the

budgeted ratio because of which it can be stated that the

combined decrease in interest rate with an increase in debt of

the organization makes it necessary for the auditor to state this

area as an area of high risk.

High risk

As observed

the debt ratio

of the

company

increased

indicating an

increment in

the level of

debt, such an

action puts

the company

at high risk.

Therefore, it

automatically

comes under

the ambit of

high risk

Proper trend

analysis

should be

conducted so

as to analyze

the bad debts

and maintain

the

management

system of the

organization.

8

Tsahuridu, 2013). high and

hence, this

leads to an

alteration in

the

efficiency of

the budget.

This hurts

the

company’s

performance

and hence,

high risk

follows.

expenses and

bad debts so

as to find

what wrong

practices are

being

conducted by

the

management.

Debt to equity

ratio: 1

The debt to equity ratio of the organization was higher than the

budgeted ratio because of which it can be stated that the

combined decrease in interest rate with an increase in debt of

the organization makes it necessary for the auditor to state this

area as an area of high risk.

High risk

As observed

the debt ratio

of the

company

increased

indicating an

increment in

the level of

debt, such an

action puts

the company

at high risk.

Therefore, it

automatically

comes under

the ambit of

high risk

Proper trend

analysis

should be

conducted so

as to analyze

the bad debts

and maintain

the

management

system of the

organization.

8

Audit

zone

9

zone

9

Audit

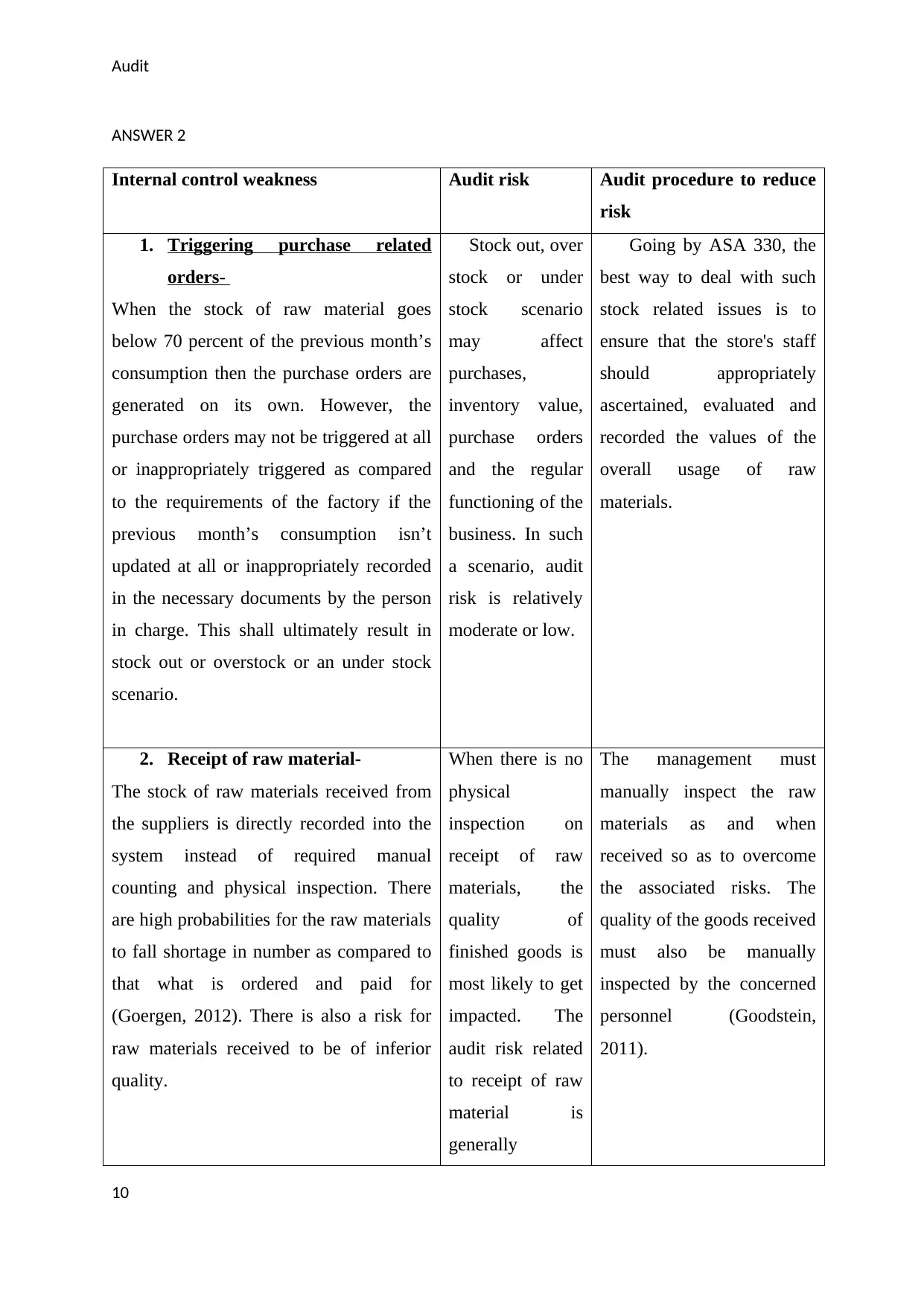

ANSWER 2

Internal control weakness Audit risk Audit procedure to reduce

risk

1. Triggering purchase related

orders-

When the stock of raw material goes

below 70 percent of the previous month’s

consumption then the purchase orders are

generated on its own. However, the

purchase orders may not be triggered at all

or inappropriately triggered as compared

to the requirements of the factory if the

previous month’s consumption isn’t

updated at all or inappropriately recorded

in the necessary documents by the person

in charge. This shall ultimately result in

stock out or overstock or an under stock

scenario.

Stock out, over

stock or under

stock scenario

may affect

purchases,

inventory value,

purchase orders

and the regular

functioning of the

business. In such

a scenario, audit

risk is relatively

moderate or low.

Going by ASA 330, the

best way to deal with such

stock related issues is to

ensure that the store's staff

should appropriately

ascertained, evaluated and

recorded the values of the

overall usage of raw

materials.

2. Receipt of raw material-

The stock of raw materials received from

the suppliers is directly recorded into the

system instead of required manual

counting and physical inspection. There

are high probabilities for the raw materials

to fall shortage in number as compared to

that what is ordered and paid for

(Goergen, 2012). There is also a risk for

raw materials received to be of inferior

quality.

When there is no

physical

inspection on

receipt of raw

materials, the

quality of

finished goods is

most likely to get

impacted. The

audit risk related

to receipt of raw

material is

generally

The management must

manually inspect the raw

materials as and when

received so as to overcome

the associated risks. The

quality of the goods received

must also be manually

inspected by the concerned

personnel (Goodstein,

2011).

10

ANSWER 2

Internal control weakness Audit risk Audit procedure to reduce

risk

1. Triggering purchase related

orders-

When the stock of raw material goes

below 70 percent of the previous month’s

consumption then the purchase orders are

generated on its own. However, the

purchase orders may not be triggered at all

or inappropriately triggered as compared

to the requirements of the factory if the

previous month’s consumption isn’t

updated at all or inappropriately recorded

in the necessary documents by the person

in charge. This shall ultimately result in

stock out or overstock or an under stock

scenario.

Stock out, over

stock or under

stock scenario

may affect

purchases,

inventory value,

purchase orders

and the regular

functioning of the

business. In such

a scenario, audit

risk is relatively

moderate or low.

Going by ASA 330, the

best way to deal with such

stock related issues is to

ensure that the store's staff

should appropriately

ascertained, evaluated and

recorded the values of the

overall usage of raw

materials.

2. Receipt of raw material-

The stock of raw materials received from

the suppliers is directly recorded into the

system instead of required manual

counting and physical inspection. There

are high probabilities for the raw materials

to fall shortage in number as compared to

that what is ordered and paid for

(Goergen, 2012). There is also a risk for

raw materials received to be of inferior

quality.

When there is no

physical

inspection on

receipt of raw

materials, the

quality of

finished goods is

most likely to get

impacted. The

audit risk related

to receipt of raw

material is

generally

The management must

manually inspect the raw

materials as and when

received so as to overcome

the associated risks. The

quality of the goods received

must also be manually

inspected by the concerned

personnel (Goodstein,

2011).

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Audit

moderate or low.

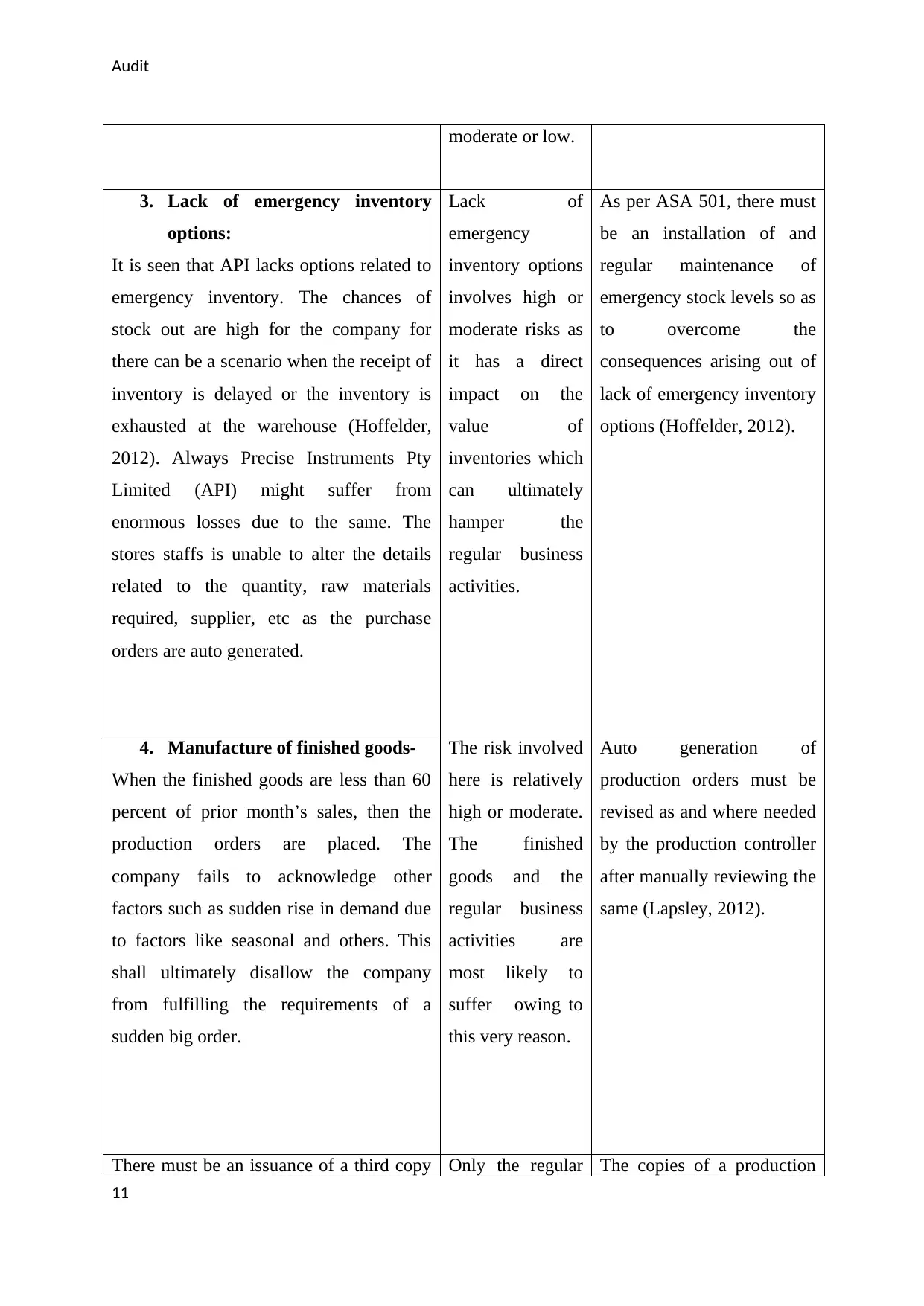

3. Lack of emergency inventory

options:

It is seen that API lacks options related to

emergency inventory. The chances of

stock out are high for the company for

there can be a scenario when the receipt of

inventory is delayed or the inventory is

exhausted at the warehouse (Hoffelder,

2012). Always Precise Instruments Pty

Limited (API) might suffer from

enormous losses due to the same. The

stores staffs is unable to alter the details

related to the quantity, raw materials

required, supplier, etc as the purchase

orders are auto generated.

Lack of

emergency

inventory options

involves high or

moderate risks as

it has a direct

impact on the

value of

inventories which

can ultimately

hamper the

regular business

activities.

As per ASA 501, there must

be an installation of and

regular maintenance of

emergency stock levels so as

to overcome the

consequences arising out of

lack of emergency inventory

options (Hoffelder, 2012).

4. Manufacture of finished goods-

When the finished goods are less than 60

percent of prior month’s sales, then the

production orders are placed. The

company fails to acknowledge other

factors such as sudden rise in demand due

to factors like seasonal and others. This

shall ultimately disallow the company

from fulfilling the requirements of a

sudden big order.

The risk involved

here is relatively

high or moderate.

The finished

goods and the

regular business

activities are

most likely to

suffer owing to

this very reason.

Auto generation of

production orders must be

revised as and where needed

by the production controller

after manually reviewing the

same (Lapsley, 2012).

There must be an issuance of a third copy Only the regular The copies of a production

11

moderate or low.

3. Lack of emergency inventory

options:

It is seen that API lacks options related to

emergency inventory. The chances of

stock out are high for the company for

there can be a scenario when the receipt of

inventory is delayed or the inventory is

exhausted at the warehouse (Hoffelder,

2012). Always Precise Instruments Pty

Limited (API) might suffer from

enormous losses due to the same. The

stores staffs is unable to alter the details

related to the quantity, raw materials

required, supplier, etc as the purchase

orders are auto generated.

Lack of

emergency

inventory options

involves high or

moderate risks as

it has a direct

impact on the

value of

inventories which

can ultimately

hamper the

regular business

activities.

As per ASA 501, there must

be an installation of and

regular maintenance of

emergency stock levels so as

to overcome the

consequences arising out of

lack of emergency inventory

options (Hoffelder, 2012).

4. Manufacture of finished goods-

When the finished goods are less than 60

percent of prior month’s sales, then the

production orders are placed. The

company fails to acknowledge other

factors such as sudden rise in demand due

to factors like seasonal and others. This

shall ultimately disallow the company

from fulfilling the requirements of a

sudden big order.

The risk involved

here is relatively

high or moderate.

The finished

goods and the

regular business

activities are

most likely to

suffer owing to

this very reason.

Auto generation of

production orders must be

revised as and where needed

by the production controller

after manually reviewing the

same (Lapsley, 2012).

There must be an issuance of a third copy Only the regular The copies of a production

11

Audit

of a production order also that needs to be

shared with the one who is an in charge of

the finished goods department. This will

make the stores staff aware of the delivery

of upcoming stock and therefore, he will

manage his stock accordingly.

functioning of the

business

activities is

impacted as the

risk involved here

is very low.

order must not only be

shared with the production

controller and raw materials

store but with stores staff as

well. It will not only create

room for transparency but

will also smoothen the

overall functioning of the

organization (Merchant,

2012).

5. Selection of supplier of raw

material and finished goods-

There is an auto selection of the suppliers

in the system used by the company. The

auto selection is highly based on the latest

price as per the last invoice and their

delivery times. This shall ultimately result

in various significant issues. The first

issue is that API fails to acknowledge

current market conditions and

developments as it takes previous prices

into its consideration while making orders

related to purchases of raw materials.

There are high probabilities for the prices

to fluctuate depending on various market

developments. Owing to this the company

might lose out on a better deal. The second

issue is that the company constructs time

analysis on the basis of the time gap

between the date of purchase order and the

date at which the goods are received

(Matthew, 2015). There are probabilities

Here the risks

arising are

moderate and it is

the decision

making with

respect to

purchase of raw

materials and the

finished goods

that seems to be

affected.

The management can ask for

quotations from various

suppliers and then evaluate

and draw comparisons

between them (ASA 520).

The management must draw

decisions on the basis of

results drawn from such

comparisons (Livne, 2015).

12

of a production order also that needs to be

shared with the one who is an in charge of

the finished goods department. This will

make the stores staff aware of the delivery

of upcoming stock and therefore, he will

manage his stock accordingly.

functioning of the

business

activities is

impacted as the

risk involved here

is very low.

order must not only be

shared with the production

controller and raw materials

store but with stores staff as

well. It will not only create

room for transparency but

will also smoothen the

overall functioning of the

organization (Merchant,

2012).

5. Selection of supplier of raw

material and finished goods-

There is an auto selection of the suppliers

in the system used by the company. The

auto selection is highly based on the latest

price as per the last invoice and their

delivery times. This shall ultimately result

in various significant issues. The first

issue is that API fails to acknowledge

current market conditions and

developments as it takes previous prices

into its consideration while making orders

related to purchases of raw materials.

There are high probabilities for the prices

to fluctuate depending on various market

developments. Owing to this the company

might lose out on a better deal. The second

issue is that the company constructs time

analysis on the basis of the time gap

between the date of purchase order and the

date at which the goods are received

(Matthew, 2015). There are probabilities

Here the risks

arising are

moderate and it is

the decision

making with

respect to

purchase of raw

materials and the

finished goods

that seems to be

affected.

The management can ask for

quotations from various

suppliers and then evaluate

and draw comparisons

between them (ASA 520).

The management must draw

decisions on the basis of

results drawn from such

comparisons (Livne, 2015).

12

Audit

for the inflation or deflation in dates due

to errors made by the personnel. This shall

disallow the company from procuring a

better deal.

6. Recording of transactions

At API the orders are only placed with

suppliers whose names are already

recorded on the master file. The alteration

in master file with respect to raw materials

and finished goods inventory is solely

made by the production controller. This

indicates that API shall not consider such

suppliers who are able to supply raw

materials at a cheaper rate or a better

quality or a better time gap as their names

are not recorded in the master file of the

company. There are probabilities for the

production controller to take undue

advantages of such a scenario and

therefore, indulge in trading malpractices

which will ultimately allow the company

to suffer (Mock et. al, 2013).

There are high

risks for collusion

and trading

malpractices to

take place. The

risk involved here

is comparatively

moderate.

The process of placing

orders must be reviewed

from time to time in order to

detect a proper alternative

with respect to purchases of

raw materials (Niemi &

Sundgren, 2012).

7. Rectification of the shortfalls

The placing of orders is done as per the

master file and if any of the records is

unavailable or not recorded then it will

lead to major issues. This will lead to

Chances are there

that the company

will face an

uphill task

because the

To ensure that the entry is

not missed, it is essential

that the company must

evaluate the entries from

time to time (ASA 520).

13

for the inflation or deflation in dates due

to errors made by the personnel. This shall

disallow the company from procuring a

better deal.

6. Recording of transactions

At API the orders are only placed with

suppliers whose names are already

recorded on the master file. The alteration

in master file with respect to raw materials

and finished goods inventory is solely

made by the production controller. This

indicates that API shall not consider such

suppliers who are able to supply raw

materials at a cheaper rate or a better

quality or a better time gap as their names

are not recorded in the master file of the

company. There are probabilities for the

production controller to take undue

advantages of such a scenario and

therefore, indulge in trading malpractices

which will ultimately allow the company

to suffer (Mock et. al, 2013).

There are high

risks for collusion

and trading

malpractices to

take place. The

risk involved here

is comparatively

moderate.

The process of placing

orders must be reviewed

from time to time in order to

detect a proper alternative

with respect to purchases of

raw materials (Niemi &

Sundgren, 2012).

7. Rectification of the shortfalls

The placing of orders is done as per the

master file and if any of the records is

unavailable or not recorded then it will

lead to major issues. This will lead to

Chances are there

that the company

will face an

uphill task

because the

To ensure that the entry is

not missed, it is essential

that the company must

evaluate the entries from

time to time (ASA 520).

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

delay in service and will even impact the

inventory of the company.

production

controller takes

the entire

decision and

there might be a

possibility of the

entry being

ignored.

This will help in locating the

difference and brings the

deficiency to the forefront.

8. Fluctuations in prices

There are chances that the prices will

fluctuate and due to this the company will

fail to grab the best deal.

Here the risk is

moderate as with

the aid of proper

decision making

and analysis the

company can

procure the deal.

The company should have a

department that will look

into the affairs of the pricing

policy. This will help in

grabbing the best deal.

14

delay in service and will even impact the

inventory of the company.

production

controller takes

the entire

decision and

there might be a

possibility of the

entry being

ignored.

This will help in locating the

difference and brings the

deficiency to the forefront.

8. Fluctuations in prices

There are chances that the prices will

fluctuate and due to this the company will

fail to grab the best deal.

Here the risk is

moderate as with

the aid of proper

decision making

and analysis the

company can

procure the deal.

The company should have a

department that will look

into the affairs of the pricing

policy. This will help in

grabbing the best deal.

14

Audit

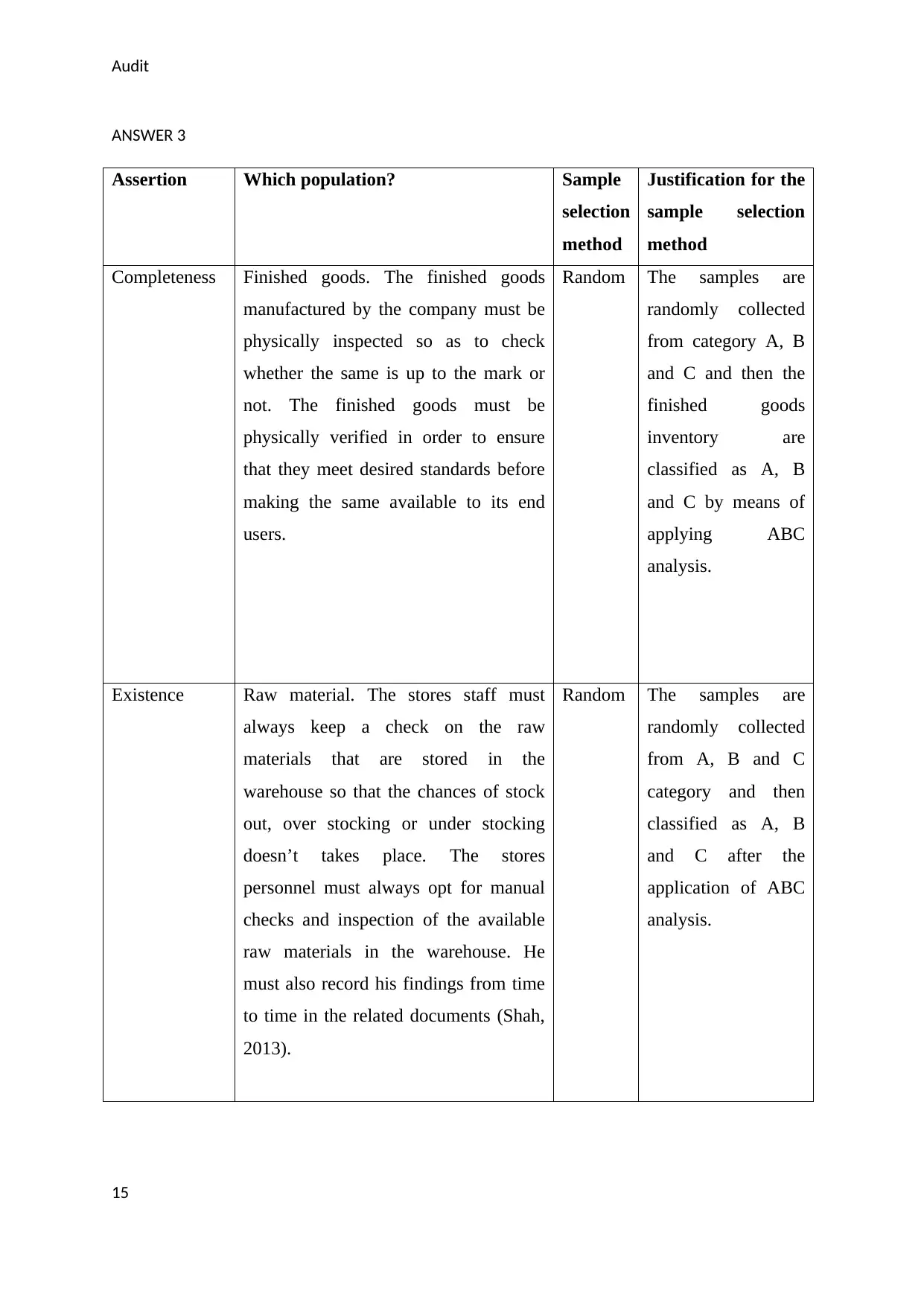

ANSWER 3

Assertion Which population? Sample

selection

method

Justification for the

sample selection

method

Completeness Finished goods. The finished goods

manufactured by the company must be

physically inspected so as to check

whether the same is up to the mark or

not. The finished goods must be

physically verified in order to ensure

that they meet desired standards before

making the same available to its end

users.

Random The samples are

randomly collected

from category A, B

and C and then the

finished goods

inventory are

classified as A, B

and C by means of

applying ABC

analysis.

Existence Raw material. The stores staff must

always keep a check on the raw

materials that are stored in the

warehouse so that the chances of stock

out, over stocking or under stocking

doesn’t takes place. The stores

personnel must always opt for manual

checks and inspection of the available

raw materials in the warehouse. He

must also record his findings from time

to time in the related documents (Shah,

2013).

Random The samples are

randomly collected

from A, B and C

category and then

classified as A, B

and C after the

application of ABC

analysis.

15

ANSWER 3

Assertion Which population? Sample

selection

method

Justification for the

sample selection

method

Completeness Finished goods. The finished goods

manufactured by the company must be

physically inspected so as to check

whether the same is up to the mark or

not. The finished goods must be

physically verified in order to ensure

that they meet desired standards before

making the same available to its end

users.

Random The samples are

randomly collected

from category A, B

and C and then the

finished goods

inventory are

classified as A, B

and C by means of

applying ABC

analysis.

Existence Raw material. The stores staff must

always keep a check on the raw

materials that are stored in the

warehouse so that the chances of stock

out, over stocking or under stocking

doesn’t takes place. The stores

personnel must always opt for manual

checks and inspection of the available

raw materials in the warehouse. He

must also record his findings from time

to time in the related documents (Shah,

2013).

Random The samples are

randomly collected

from A, B and C

category and then

classified as A, B

and C after the

application of ABC

analysis.

15

Audit

References

Elder, J. R., Beasley S. M., & Arens A. A. (2010). Auditing and Assurance Services. Person

Education, New Jersey: USA

Gay, G., & Simnet, R. (2015). Auditing and Assurance Services. McGraw Hill

Geoffrey D. B., Joleen K., K. K.S., and David A. W. (2016). Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors.

Accounting Horizons. 30(1), p.143-156. DOI: https://doi.org/10.2308/acch-51309

Ghandar, A & Tsahuridu, E. (2013) The Auditing Handbook 2013. Australia: Pearson.

Goergen , M. (2012). International Corporate Governance. Prentice Hall.

Goodstein, E. (2011) Ethics and Economics, Economics and the Environment. Wiley

Hoffelder, K. (2012). New Audit Standard Encourages More Talking. Harvard Press.

Lapsley, I. (2012). Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management, 9(3), pp. 291-292.

https://doi.org/10.1111/1468-0408.00081

Livne, G. (2015) Threats to Auditor Independence and Possible Remedies . Retrieved from:

http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full

Matthew, S. E. (2015). Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review, 90(2), 495-527. Doi:

https://doi.org/10.2308/accr-50871

Merchant, K. A. (2012). Making Management Accounting Research More Useful. Pacific

Accounting Review, 24(3), 1-34. Doi: https://doi.org/10.1108/01140581211283904

Mock, T. J., Bédard, J., Coram, P., Davis, S., Espahbodi, R. and Warne, R. (2013). The audit

reporting model: Current research synthesis and implications. Auditing: A Journal of

Practice and Theory, 32, 323-351. Doi: https://doi.org/10.2308/ajpt-50294

Niemi, L., and Sundgren, S. (2012). Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review, 21(4), 767-796.

Doi: https://doi.org/10.1080/09638180.2012.671465

Roach, L. (2010). Auditor Liability: Liability Limitation Agreements. Pearson.

16

References

Elder, J. R., Beasley S. M., & Arens A. A. (2010). Auditing and Assurance Services. Person

Education, New Jersey: USA

Gay, G., & Simnet, R. (2015). Auditing and Assurance Services. McGraw Hill

Geoffrey D. B., Joleen K., K. K.S., and David A. W. (2016). Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors.

Accounting Horizons. 30(1), p.143-156. DOI: https://doi.org/10.2308/acch-51309

Ghandar, A & Tsahuridu, E. (2013) The Auditing Handbook 2013. Australia: Pearson.

Goergen , M. (2012). International Corporate Governance. Prentice Hall.

Goodstein, E. (2011) Ethics and Economics, Economics and the Environment. Wiley

Hoffelder, K. (2012). New Audit Standard Encourages More Talking. Harvard Press.

Lapsley, I. (2012). Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management, 9(3), pp. 291-292.

https://doi.org/10.1111/1468-0408.00081

Livne, G. (2015) Threats to Auditor Independence and Possible Remedies . Retrieved from:

http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full

Matthew, S. E. (2015). Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review, 90(2), 495-527. Doi:

https://doi.org/10.2308/accr-50871

Merchant, K. A. (2012). Making Management Accounting Research More Useful. Pacific

Accounting Review, 24(3), 1-34. Doi: https://doi.org/10.1108/01140581211283904

Mock, T. J., Bédard, J., Coram, P., Davis, S., Espahbodi, R. and Warne, R. (2013). The audit

reporting model: Current research synthesis and implications. Auditing: A Journal of

Practice and Theory, 32, 323-351. Doi: https://doi.org/10.2308/ajpt-50294

Niemi, L., and Sundgren, S. (2012). Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review, 21(4), 767-796.

Doi: https://doi.org/10.1080/09638180.2012.671465

Roach, L. (2010). Auditor Liability: Liability Limitation Agreements. Pearson.

16

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.