Auditing and Assurance

Added on 2023-03-20

12 Pages4263 Words52 Views

Running head: Auditing and Assurance

Auditing and Assurance

Name of the Student

Name of the University

Author Note

Auditing and Assurance

Name of the Student

Name of the University

Author Note

1

Auditing and Assurance

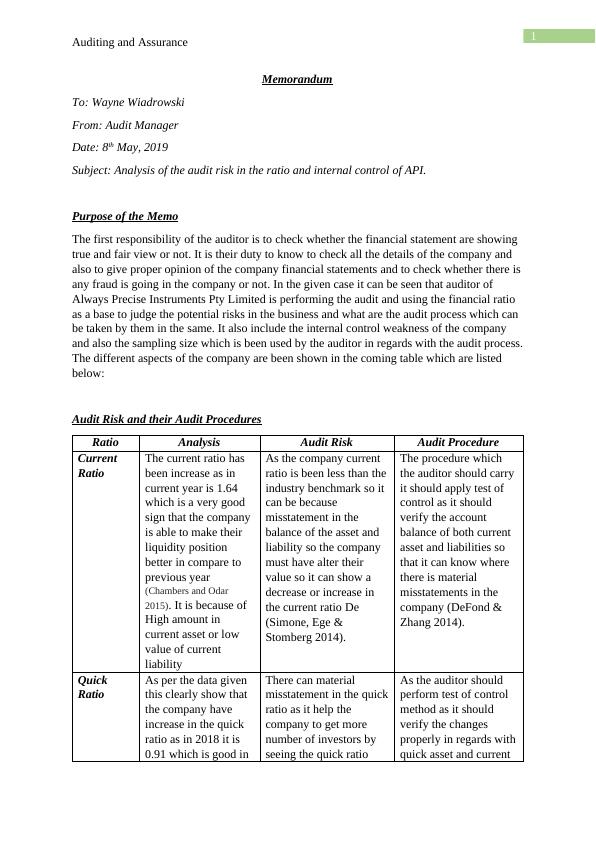

Memorandum

To: Wayne Wiadrowski

From: Audit Manager

Date: 8th May, 2019

Subject: Analysis of the audit risk in the ratio and internal control of API.

Purpose of the Memo

The first responsibility of the auditor is to check whether the financial statement are showing

true and fair view or not. It is their duty to know to check all the details of the company and

also to give proper opinion of the company financial statements and to check whether there is

any fraud is going in the company or not. In the given case it can be seen that auditor of

Always Precise Instruments Pty Limited is performing the audit and using the financial ratio

as a base to judge the potential risks in the business and what are the audit process which can

be taken by them in the same. It also include the internal control weakness of the company

and also the sampling size which is been used by the auditor in regards with the audit process.

The different aspects of the company are been shown in the coming table which are listed

below:

Audit Risk and their Audit Procedures

Ratio Analysis Audit Risk Audit Procedure

Current

Ratio

The current ratio has

been increase as in

current year is 1.64

which is a very good

sign that the company

is able to make their

liquidity position

better in compare to

previous year

(Chambers and Odar

2015). It is because of

High amount in

current asset or low

value of current

liability

As the company current

ratio is been less than the

industry benchmark so it

can be because

misstatement in the

balance of the asset and

liability so the company

must have alter their

value so it can show a

decrease or increase in

the current ratio De

(Simone, Ege &

Stomberg 2014).

The procedure which

the auditor should carry

it should apply test of

control as it should

verify the account

balance of both current

asset and liabilities so

that it can know where

there is material

misstatements in the

company (DeFond &

Zhang 2014).

Quick

Ratio

As per the data given

this clearly show that

the company have

increase in the quick

ratio as in 2018 it is

0.91 which is good in

There can material

misstatement in the quick

ratio as it help the

company to get more

number of investors by

seeing the quick ratio

As the auditor should

perform test of control

method as it should

verify the changes

properly in regards with

quick asset and current

Auditing and Assurance

Memorandum

To: Wayne Wiadrowski

From: Audit Manager

Date: 8th May, 2019

Subject: Analysis of the audit risk in the ratio and internal control of API.

Purpose of the Memo

The first responsibility of the auditor is to check whether the financial statement are showing

true and fair view or not. It is their duty to know to check all the details of the company and

also to give proper opinion of the company financial statements and to check whether there is

any fraud is going in the company or not. In the given case it can be seen that auditor of

Always Precise Instruments Pty Limited is performing the audit and using the financial ratio

as a base to judge the potential risks in the business and what are the audit process which can

be taken by them in the same. It also include the internal control weakness of the company

and also the sampling size which is been used by the auditor in regards with the audit process.

The different aspects of the company are been shown in the coming table which are listed

below:

Audit Risk and their Audit Procedures

Ratio Analysis Audit Risk Audit Procedure

Current

Ratio

The current ratio has

been increase as in

current year is 1.64

which is a very good

sign that the company

is able to make their

liquidity position

better in compare to

previous year

(Chambers and Odar

2015). It is because of

High amount in

current asset or low

value of current

liability

As the company current

ratio is been less than the

industry benchmark so it

can be because

misstatement in the

balance of the asset and

liability so the company

must have alter their

value so it can show a

decrease or increase in

the current ratio De

(Simone, Ege &

Stomberg 2014).

The procedure which

the auditor should carry

it should apply test of

control as it should

verify the account

balance of both current

asset and liabilities so

that it can know where

there is material

misstatements in the

company (DeFond &

Zhang 2014).

Quick

Ratio

As per the data given

this clearly show that

the company have

increase in the quick

ratio as in 2018 it is

0.91 which is good in

There can material

misstatement in the quick

ratio as it help the

company to get more

number of investors by

seeing the quick ratio

As the auditor should

perform test of control

method as it should

verify the changes

properly in regards with

quick asset and current

2

Auditing and Assurance

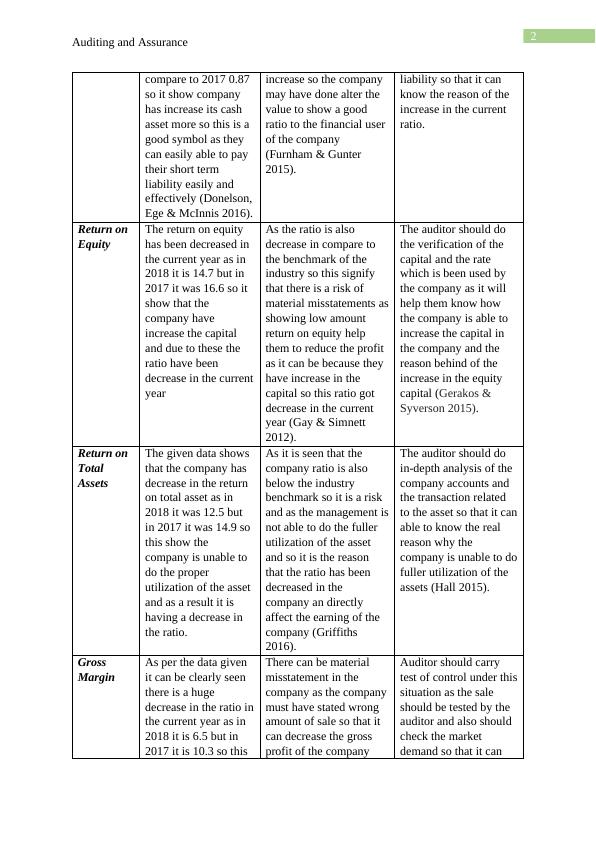

compare to 2017 0.87

so it show company

has increase its cash

asset more so this is a

good symbol as they

can easily able to pay

their short term

liability easily and

effectively (Donelson,

Ege & McInnis 2016).

increase so the company

may have done alter the

value to show a good

ratio to the financial user

of the company

(Furnham & Gunter

2015).

liability so that it can

know the reason of the

increase in the current

ratio.

Return on

Equity

The return on equity

has been decreased in

the current year as in

2018 it is 14.7 but in

2017 it was 16.6 so it

show that the

company have

increase the capital

and due to these the

ratio have been

decrease in the current

year

As the ratio is also

decrease in compare to

the benchmark of the

industry so this signify

that there is a risk of

material misstatements as

showing low amount

return on equity help

them to reduce the profit

as it can be because they

have increase in the

capital so this ratio got

decrease in the current

year (Gay & Simnett

2012).

The auditor should do

the verification of the

capital and the rate

which is been used by

the company as it will

help them know how

the company is able to

increase the capital in

the company and the

reason behind of the

increase in the equity

capital (Gerakos &

Syverson 2015).

Return on

Total

Assets

The given data shows

that the company has

decrease in the return

on total asset as in

2018 it was 12.5 but

in 2017 it was 14.9 so

this show the

company is unable to

do the proper

utilization of the asset

and as a result it is

having a decrease in

the ratio.

As it is seen that the

company ratio is also

below the industry

benchmark so it is a risk

and as the management is

not able to do the fuller

utilization of the asset

and so it is the reason

that the ratio has been

decreased in the

company an directly

affect the earning of the

company (Griffiths

2016).

The auditor should do

in-depth analysis of the

company accounts and

the transaction related

to the asset so that it can

able to know the real

reason why the

company is unable to do

fuller utilization of the

assets (Hall 2015).

Gross

Margin

As per the data given

it can be clearly seen

there is a huge

decrease in the ratio in

the current year as in

2018 it is 6.5 but in

2017 it is 10.3 so this

There can be material

misstatement in the

company as the company

must have stated wrong

amount of sale so that it

can decrease the gross

profit of the company

Auditor should carry

test of control under this

situation as the sale

should be tested by the

auditor and also should

check the market

demand so that it can

Auditing and Assurance

compare to 2017 0.87

so it show company

has increase its cash

asset more so this is a

good symbol as they

can easily able to pay

their short term

liability easily and

effectively (Donelson,

Ege & McInnis 2016).

increase so the company

may have done alter the

value to show a good

ratio to the financial user

of the company

(Furnham & Gunter

2015).

liability so that it can

know the reason of the

increase in the current

ratio.

Return on

Equity

The return on equity

has been decreased in

the current year as in

2018 it is 14.7 but in

2017 it was 16.6 so it

show that the

company have

increase the capital

and due to these the

ratio have been

decrease in the current

year

As the ratio is also

decrease in compare to

the benchmark of the

industry so this signify

that there is a risk of

material misstatements as

showing low amount

return on equity help

them to reduce the profit

as it can be because they

have increase in the

capital so this ratio got

decrease in the current

year (Gay & Simnett

2012).

The auditor should do

the verification of the

capital and the rate

which is been used by

the company as it will

help them know how

the company is able to

increase the capital in

the company and the

reason behind of the

increase in the equity

capital (Gerakos &

Syverson 2015).

Return on

Total

Assets

The given data shows

that the company has

decrease in the return

on total asset as in

2018 it was 12.5 but

in 2017 it was 14.9 so

this show the

company is unable to

do the proper

utilization of the asset

and as a result it is

having a decrease in

the ratio.

As it is seen that the

company ratio is also

below the industry

benchmark so it is a risk

and as the management is

not able to do the fuller

utilization of the asset

and so it is the reason

that the ratio has been

decreased in the

company an directly

affect the earning of the

company (Griffiths

2016).

The auditor should do

in-depth analysis of the

company accounts and

the transaction related

to the asset so that it can

able to know the real

reason why the

company is unable to do

fuller utilization of the

assets (Hall 2015).

Gross

Margin

As per the data given

it can be clearly seen

there is a huge

decrease in the ratio in

the current year as in

2018 it is 6.5 but in

2017 it is 10.3 so this

There can be material

misstatement in the

company as the company

must have stated wrong

amount of sale so that it

can decrease the gross

profit of the company

Auditor should carry

test of control under this

situation as the sale

should be tested by the

auditor and also should

check the market

demand so that it can

3

Auditing and Assurance

show that the

company is unable to

get proper sale in the

current year and as a

result the ratio got

decrease. It is because

of low amount of sale

or high cost expenses.

and able to save amount

of tax from it

(He ,Zeadally & Wu

2018)

assume about the sale

amount which is there

in the financial

statement and can

conclude whether they

are any material

misstatement or not

Marketing

Expenses

There is high increase

in the marketing

expense of the

company as in 2018 it

is 4.4% but in 2017 it

is 3.8% so this is

increase and it will

directly affect the net

profit of the company.

As there is high amount

of marketing expenses is

there this signify that the

company must done

some material

misstatement in the

expenses it must have

overstated the expenses

as it is also increased in

compare to industry

benchmark so this show

company is able to get

high amount of the

expenses which not a

good sign in regards with

the net profit of the

company (King 2014).

The auditor should

carry test of control

methods as there is an

increase in the expenses

so the auditor should

verify the invoice and

also should check

whether the expenses

are done in some other

cases are not been

included in this

expenses.

Sales

Expenses

As per the data it is

clear that there is a

decrease in the ratio as

in 2018 it is 3.4% and

in 2017 it is 3.6% so

this the good sign that

the company is able to

control the expenses

and as a result it will

able to increase the

overall profit of the

company.

As the company expense

is even low compare to

the industry benchmark

so there can be a risk of

material misstatement in

the account and the

company may have

decrease the value of the

expenses so that it can

able to show an increase

in gross profit and can

misstated it to the

financial user of the

company (Knechel &

Salterio 2016).

Auditor should use test

of details method in this

scenario as it should

check the details of the

invoice of the sale so

that it can conclude

about the fairness of the

expenses and can check

the reason of material

misstatement.

Times

Interest

Earned

The data show that the

company have got a

decrease in the ratio as

in 2018 it is 3.6 but in

2017 it was 4.6 so this

show that the

As per the given scenario

it can be say that there is

material misstatement in

the ratio and as it help

the company to decrease

their borrowing cost and

Auditor should perform

different process in this

case as it should able to

check all the borrowing

details so that it can

know what are the

Auditing and Assurance

show that the

company is unable to

get proper sale in the

current year and as a

result the ratio got

decrease. It is because

of low amount of sale

or high cost expenses.

and able to save amount

of tax from it

(He ,Zeadally & Wu

2018)

assume about the sale

amount which is there

in the financial

statement and can

conclude whether they

are any material

misstatement or not

Marketing

Expenses

There is high increase

in the marketing

expense of the

company as in 2018 it

is 4.4% but in 2017 it

is 3.8% so this is

increase and it will

directly affect the net

profit of the company.

As there is high amount

of marketing expenses is

there this signify that the

company must done

some material

misstatement in the

expenses it must have

overstated the expenses

as it is also increased in

compare to industry

benchmark so this show

company is able to get

high amount of the

expenses which not a

good sign in regards with

the net profit of the

company (King 2014).

The auditor should

carry test of control

methods as there is an

increase in the expenses

so the auditor should

verify the invoice and

also should check

whether the expenses

are done in some other

cases are not been

included in this

expenses.

Sales

Expenses

As per the data it is

clear that there is a

decrease in the ratio as

in 2018 it is 3.4% and

in 2017 it is 3.6% so

this the good sign that

the company is able to

control the expenses

and as a result it will

able to increase the

overall profit of the

company.

As the company expense

is even low compare to

the industry benchmark

so there can be a risk of

material misstatement in

the account and the

company may have

decrease the value of the

expenses so that it can

able to show an increase

in gross profit and can

misstated it to the

financial user of the

company (Knechel &

Salterio 2016).

Auditor should use test

of details method in this

scenario as it should

check the details of the

invoice of the sale so

that it can conclude

about the fairness of the

expenses and can check

the reason of material

misstatement.

Times

Interest

Earned

The data show that the

company have got a

decrease in the ratio as

in 2018 it is 3.6 but in

2017 it was 4.6 so this

show that the

As per the given scenario

it can be say that there is

material misstatement in

the ratio and as it help

the company to decrease

their borrowing cost and

Auditor should perform

different process in this

case as it should able to

check all the borrowing

details so that it can

know what are the

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Audit and Assurancelg...

|15

|3782

|81

Addressing Specific Audit Situations in Auditing and Assurance in Australialg...

|16

|4293

|49

Analysis of Audit Risk in Always Precise Instruments Pty Ltdlg...

|15

|4227

|79

Audit Risks from Ratios and Internal Control and Sampling Method of APIlg...

|15

|4289

|34

Weaknesses in Inventory Internal Control, Audit Risk and Procedureslg...

|15

|3868

|48

Discussion Regarding Audit Risks of APIlg...

|15

|3872

|98