Accounting Theory Contemporary Issues PDF

VerifiedAdded on 2021/06/14

|13

|1919

|19

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Executive Summary

The report has been prepared on the acquisition made by Tuna Ltd. of the tarhet company Brim

Limited. Various inputs have been given and purchase consideration and acquisition analysis has

been made using the given data. Furthermore, the consolidation entries for the company Tuna

Limited has been shown in the given assignment. Finally, the consolidated set of financial

statements has been prepared for the group considering the format and the inputs given in the

question for Tuna and Brim Limited.

2 | P a g e

Executive Summary

The report has been prepared on the acquisition made by Tuna Ltd. of the tarhet company Brim

Limited. Various inputs have been given and purchase consideration and acquisition analysis has

been made using the given data. Furthermore, the consolidation entries for the company Tuna

Limited has been shown in the given assignment. Finally, the consolidated set of financial

statements has been prepared for the group considering the format and the inputs given in the

question for Tuna and Brim Limited.

2 | P a g e

3

Contents

Executive Summary.....................................................................................................................................2

ACQUISITION ANALYSIS OF TUNA LTD.........................................................................................................4

CONSOLIDATION JOURNAL ENTRIES OF TUNA LTD.....................................................................................5

CONSOLIDATED SET OF FINANCIAL STATEMENTS.......................................................................................8

References.................................................................................................................................................12

3 | P a g e

Contents

Executive Summary.....................................................................................................................................2

ACQUISITION ANALYSIS OF TUNA LTD.........................................................................................................4

CONSOLIDATION JOURNAL ENTRIES OF TUNA LTD.....................................................................................5

CONSOLIDATED SET OF FINANCIAL STATEMENTS.......................................................................................8

References.................................................................................................................................................12

3 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

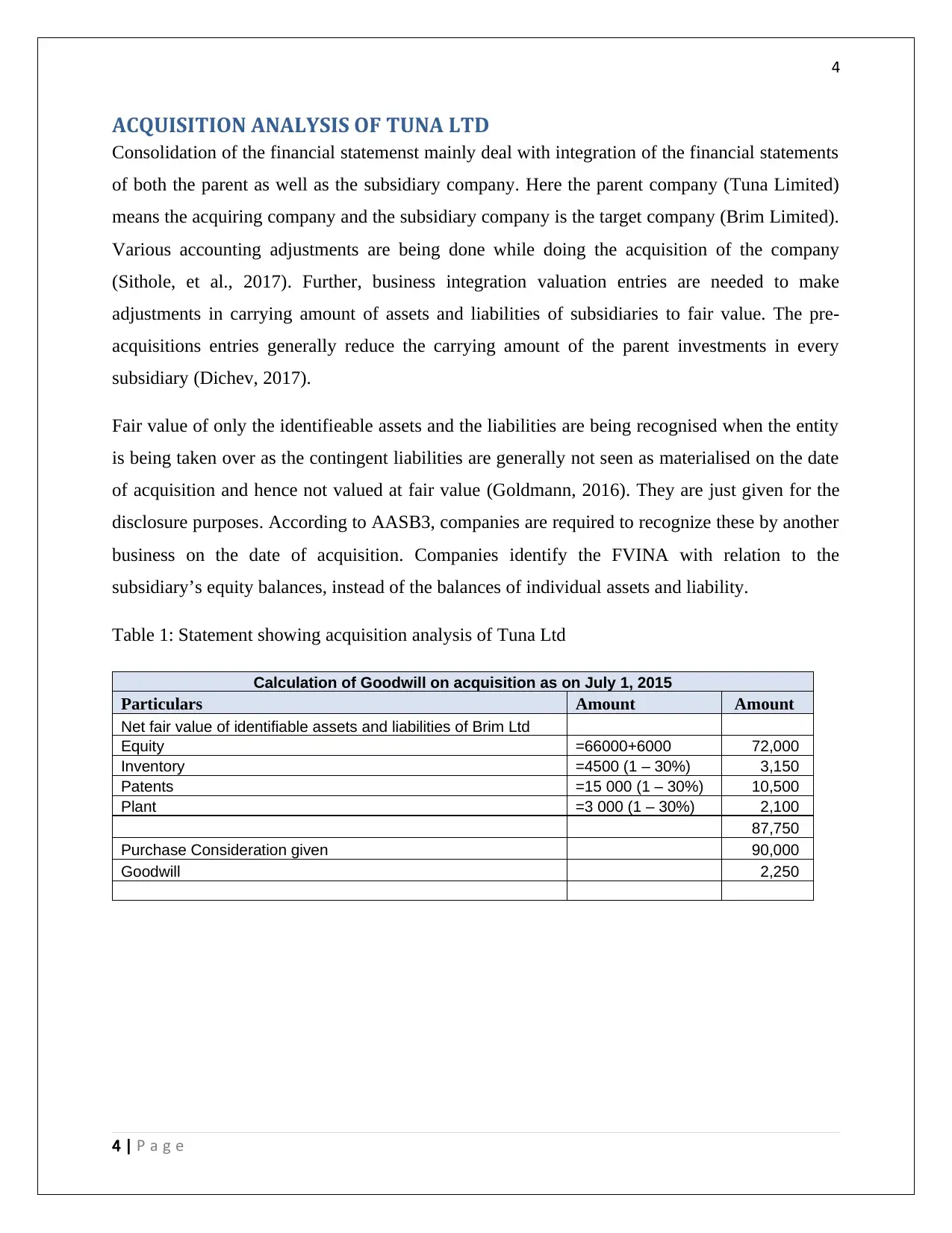

ACQUISITION ANALYSIS OF TUNA LTD

Consolidation of the financial statemenst mainly deal with integration of the financial statements

of both the parent as well as the subsidiary company. Here the parent company (Tuna Limited)

means the acquiring company and the subsidiary company is the target company (Brim Limited).

Various accounting adjustments are being done while doing the acquisition of the company

(Sithole, et al., 2017). Further, business integration valuation entries are needed to make

adjustments in carrying amount of assets and liabilities of subsidiaries to fair value. The pre-

acquisitions entries generally reduce the carrying amount of the parent investments in every

subsidiary (Dichev, 2017).

Fair value of only the identifieable assets and the liabilities are being recognised when the entity

is being taken over as the contingent liabilities are generally not seen as materialised on the date

of acquisition and hence not valued at fair value (Goldmann, 2016). They are just given for the

disclosure purposes. According to AASB3, companies are required to recognize these by another

business on the date of acquisition. Companies identify the FVINA with relation to the

subsidiary’s equity balances, instead of the balances of individual assets and liability.

Table 1: Statement showing acquisition analysis of Tuna Ltd

Calculation of Goodwill on acquisition as on July 1, 2015

Particulars Amount Amount

Net fair value of identifiable assets and liabilities of Brim Ltd

Equity =66000+6000 72,000

Inventory =4500 (1 – 30%) 3,150

Patents =15 000 (1 – 30%) 10,500

Plant =3 000 (1 – 30%) 2,100

87,750

Purchase Consideration given 90,000

Goodwill 2,250

4 | P a g e

ACQUISITION ANALYSIS OF TUNA LTD

Consolidation of the financial statemenst mainly deal with integration of the financial statements

of both the parent as well as the subsidiary company. Here the parent company (Tuna Limited)

means the acquiring company and the subsidiary company is the target company (Brim Limited).

Various accounting adjustments are being done while doing the acquisition of the company

(Sithole, et al., 2017). Further, business integration valuation entries are needed to make

adjustments in carrying amount of assets and liabilities of subsidiaries to fair value. The pre-

acquisitions entries generally reduce the carrying amount of the parent investments in every

subsidiary (Dichev, 2017).

Fair value of only the identifieable assets and the liabilities are being recognised when the entity

is being taken over as the contingent liabilities are generally not seen as materialised on the date

of acquisition and hence not valued at fair value (Goldmann, 2016). They are just given for the

disclosure purposes. According to AASB3, companies are required to recognize these by another

business on the date of acquisition. Companies identify the FVINA with relation to the

subsidiary’s equity balances, instead of the balances of individual assets and liability.

Table 1: Statement showing acquisition analysis of Tuna Ltd

Calculation of Goodwill on acquisition as on July 1, 2015

Particulars Amount Amount

Net fair value of identifiable assets and liabilities of Brim Ltd

Equity =66000+6000 72,000

Inventory =4500 (1 – 30%) 3,150

Patents =15 000 (1 – 30%) 10,500

Plant =3 000 (1 – 30%) 2,100

87,750

Purchase Consideration given 90,000

Goodwill 2,250

4 | P a g e

5

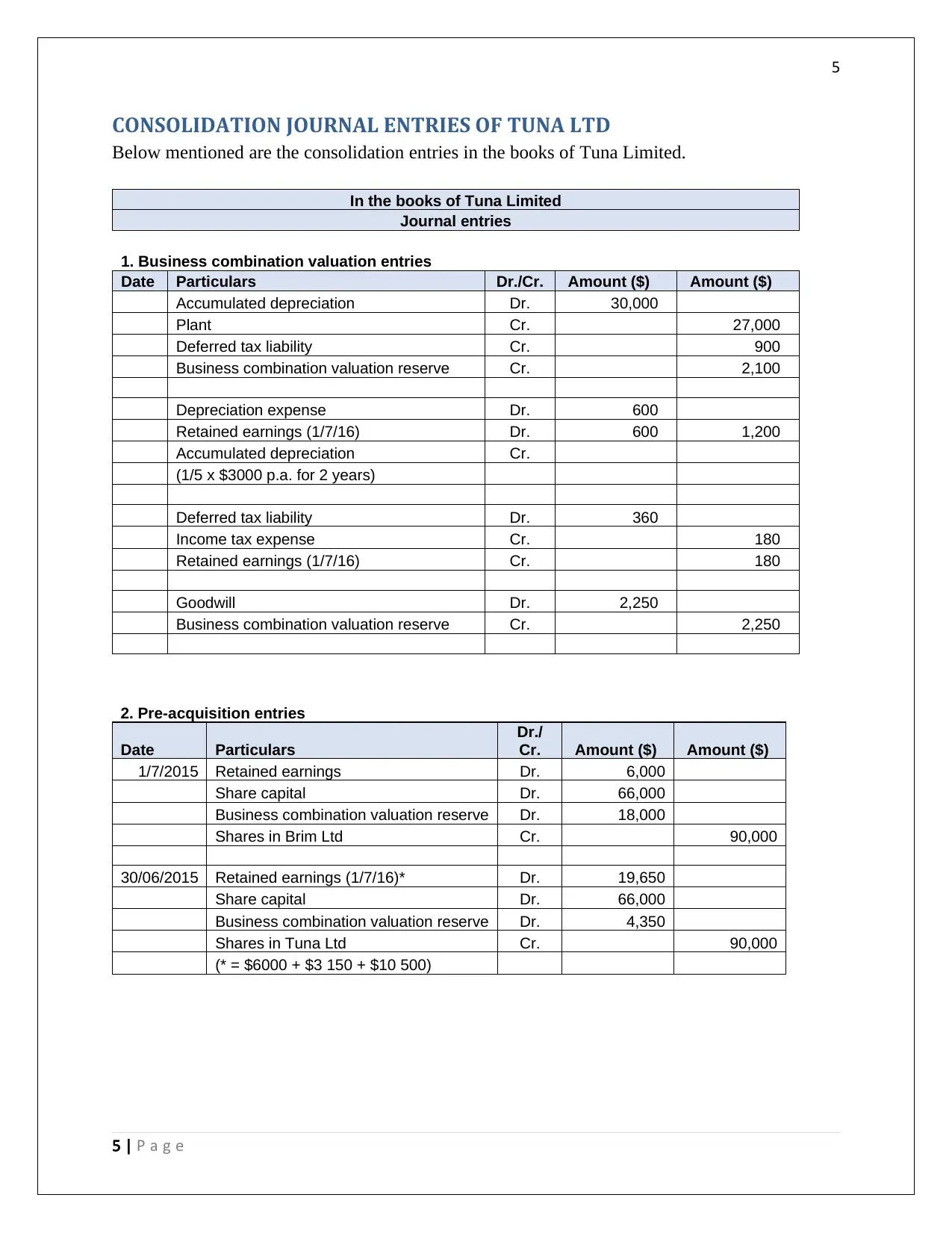

CONSOLIDATION JOURNAL ENTRIES OF TUNA LTD

Below mentioned are the consolidation entries in the books of Tuna Limited.

In the books of Tuna Limited

Journal entries

1. Business combination valuation entries

Date Particulars Dr./Cr. Amount ($) Amount ($)

Accumulated depreciation Dr. 30,000

Plant Cr. 27,000

Deferred tax liability Cr. 900

Business combination valuation reserve Cr. 2,100

Depreciation expense Dr. 600

Retained earnings (1/7/16) Dr. 600 1,200

Accumulated depreciation Cr.

(1/5 x $3000 p.a. for 2 years)

Deferred tax liability Dr. 360

Income tax expense Cr. 180

Retained earnings (1/7/16) Cr. 180

Goodwill Dr. 2,250

Business combination valuation reserve Cr. 2,250

2. Pre-acquisition entries

Date Particulars

Dr./

Cr. Amount ($) Amount ($)

1/7/2015 Retained earnings Dr. 6,000

Share capital Dr. 66,000

Business combination valuation reserve Dr. 18,000

Shares in Brim Ltd Cr. 90,000

30/06/2015 Retained earnings (1/7/16)* Dr. 19,650

Share capital Dr. 66,000

Business combination valuation reserve Dr. 4,350

Shares in Tuna Ltd Cr. 90,000

(* = $6000 + $3 150 + $10 500)

5 | P a g e

CONSOLIDATION JOURNAL ENTRIES OF TUNA LTD

Below mentioned are the consolidation entries in the books of Tuna Limited.

In the books of Tuna Limited

Journal entries

1. Business combination valuation entries

Date Particulars Dr./Cr. Amount ($) Amount ($)

Accumulated depreciation Dr. 30,000

Plant Cr. 27,000

Deferred tax liability Cr. 900

Business combination valuation reserve Cr. 2,100

Depreciation expense Dr. 600

Retained earnings (1/7/16) Dr. 600 1,200

Accumulated depreciation Cr.

(1/5 x $3000 p.a. for 2 years)

Deferred tax liability Dr. 360

Income tax expense Cr. 180

Retained earnings (1/7/16) Cr. 180

Goodwill Dr. 2,250

Business combination valuation reserve Cr. 2,250

2. Pre-acquisition entries

Date Particulars

Dr./

Cr. Amount ($) Amount ($)

1/7/2015 Retained earnings Dr. 6,000

Share capital Dr. 66,000

Business combination valuation reserve Dr. 18,000

Shares in Brim Ltd Cr. 90,000

30/06/2015 Retained earnings (1/7/16)* Dr. 19,650

Share capital Dr. 66,000

Business combination valuation reserve Dr. 4,350

Shares in Tuna Ltd Cr. 90,000

(* = $6000 + $3 150 + $10 500)

5 | P a g e

6

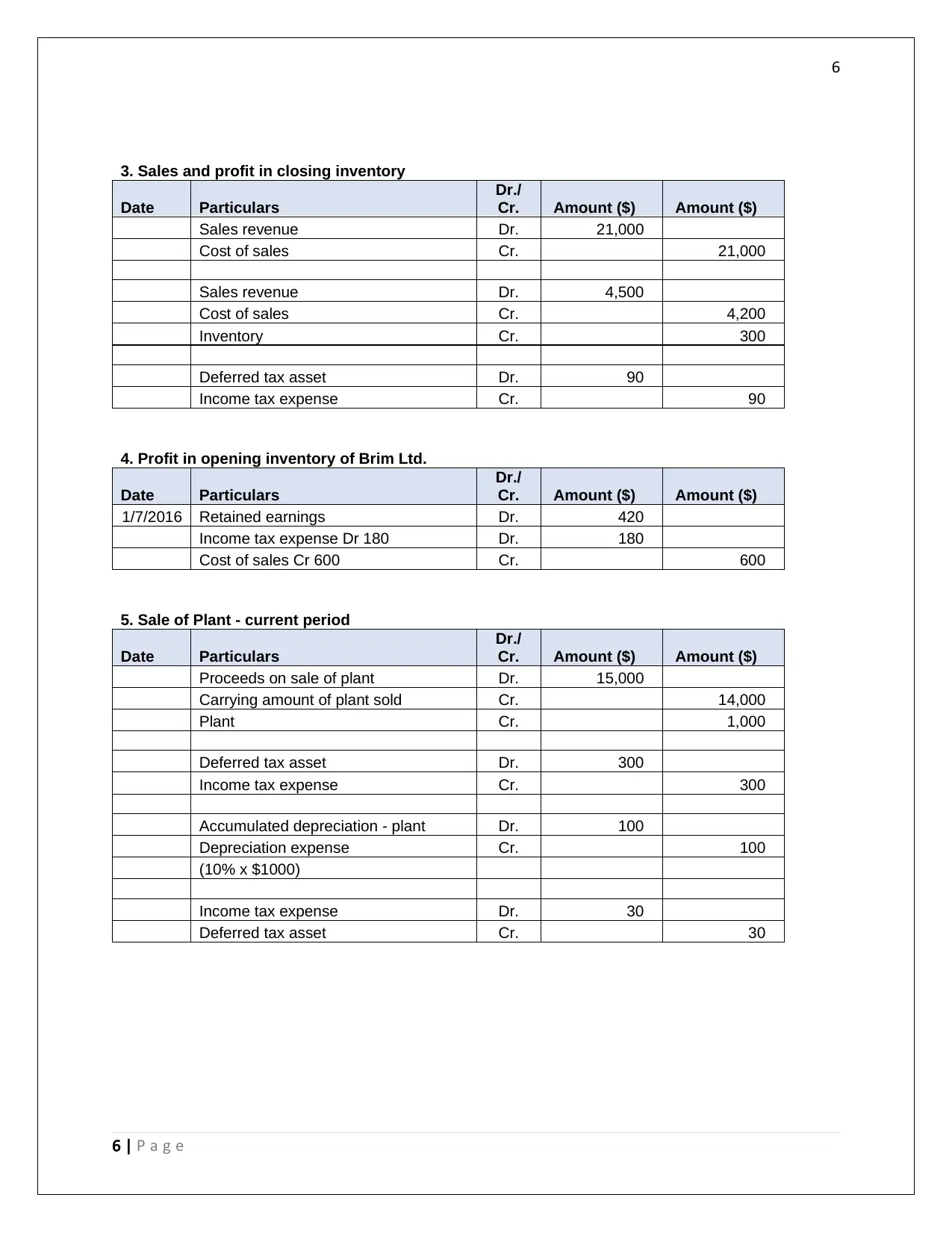

3. Sales and profit in closing inventory

Date Particulars

Dr./

Cr. Amount ($) Amount ($)

Sales revenue Dr. 21,000

Cost of sales Cr. 21,000

Sales revenue Dr. 4,500

Cost of sales Cr. 4,200

Inventory Cr. 300

Deferred tax asset Dr. 90

Income tax expense Cr. 90

4. Profit in opening inventory of Brim Ltd.

Date Particulars

Dr./

Cr. Amount ($) Amount ($)

1/7/2016 Retained earnings Dr. 420

Income tax expense Dr 180 Dr. 180

Cost of sales Cr 600 Cr. 600

5. Sale of Plant - current period

Date Particulars

Dr./

Cr. Amount ($) Amount ($)

Proceeds on sale of plant Dr. 15,000

Carrying amount of plant sold Cr. 14,000

Plant Cr. 1,000

Deferred tax asset Dr. 300

Income tax expense Cr. 300

Accumulated depreciation - plant Dr. 100

Depreciation expense Cr. 100

(10% x $1000)

Income tax expense Dr. 30

Deferred tax asset Cr. 30

6 | P a g e

3. Sales and profit in closing inventory

Date Particulars

Dr./

Cr. Amount ($) Amount ($)

Sales revenue Dr. 21,000

Cost of sales Cr. 21,000

Sales revenue Dr. 4,500

Cost of sales Cr. 4,200

Inventory Cr. 300

Deferred tax asset Dr. 90

Income tax expense Cr. 90

4. Profit in opening inventory of Brim Ltd.

Date Particulars

Dr./

Cr. Amount ($) Amount ($)

1/7/2016 Retained earnings Dr. 420

Income tax expense Dr 180 Dr. 180

Cost of sales Cr 600 Cr. 600

5. Sale of Plant - current period

Date Particulars

Dr./

Cr. Amount ($) Amount ($)

Proceeds on sale of plant Dr. 15,000

Carrying amount of plant sold Cr. 14,000

Plant Cr. 1,000

Deferred tax asset Dr. 300

Income tax expense Cr. 300

Accumulated depreciation - plant Dr. 100

Depreciation expense Cr. 100

(10% x $1000)

Income tax expense Dr. 30

Deferred tax asset Cr. 30

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

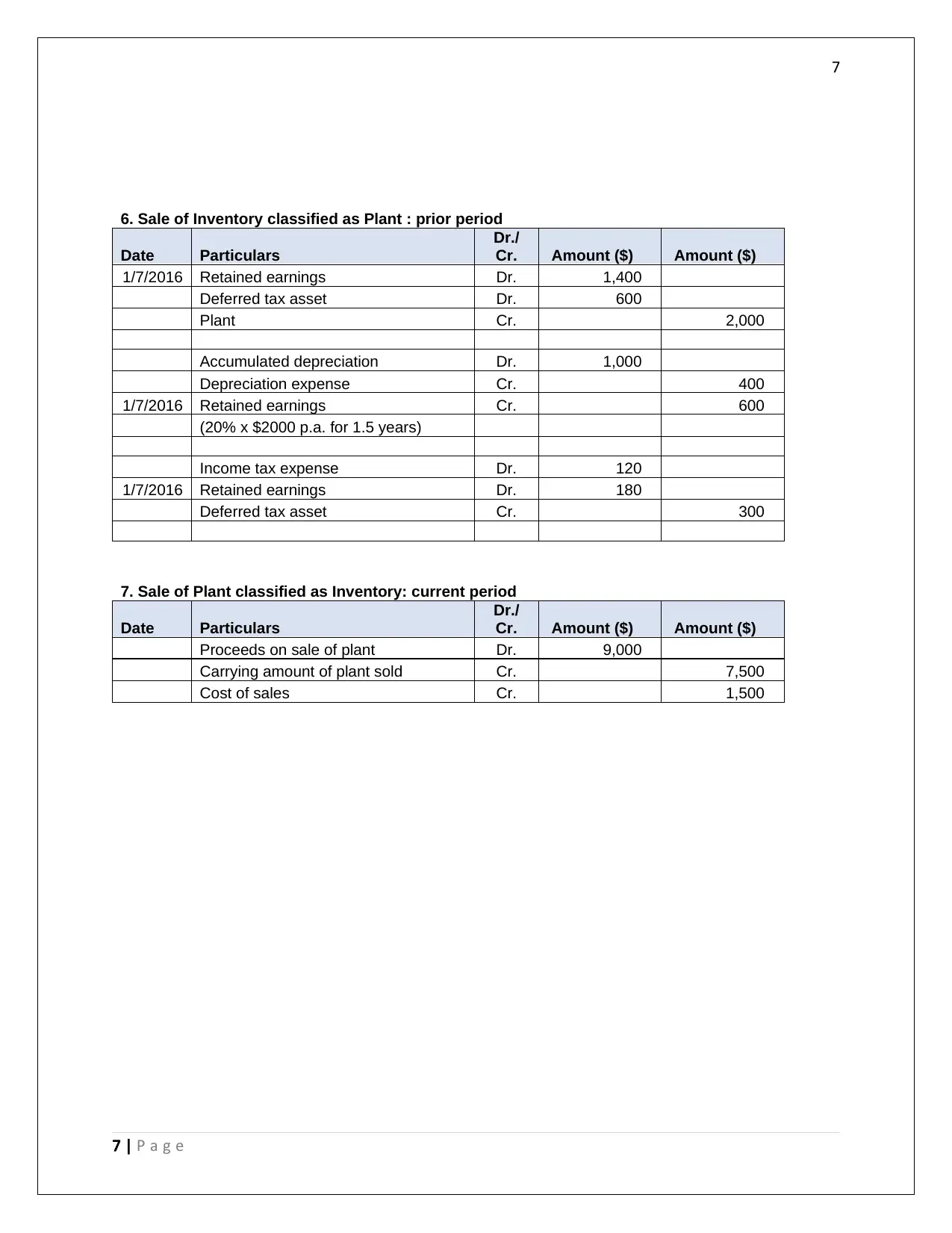

6. Sale of Inventory classified as Plant : prior period

Date Particulars

Dr./

Cr. Amount ($) Amount ($)

1/7/2016 Retained earnings Dr. 1,400

Deferred tax asset Dr. 600

Plant Cr. 2,000

Accumulated depreciation Dr. 1,000

Depreciation expense Cr. 400

1/7/2016 Retained earnings Cr. 600

(20% x $2000 p.a. for 1.5 years)

Income tax expense Dr. 120

1/7/2016 Retained earnings Dr. 180

Deferred tax asset Cr. 300

7. Sale of Plant classified as Inventory: current period

Date Particulars

Dr./

Cr. Amount ($) Amount ($)

Proceeds on sale of plant Dr. 9,000

Carrying amount of plant sold Cr. 7,500

Cost of sales Cr. 1,500

7 | P a g e

6. Sale of Inventory classified as Plant : prior period

Date Particulars

Dr./

Cr. Amount ($) Amount ($)

1/7/2016 Retained earnings Dr. 1,400

Deferred tax asset Dr. 600

Plant Cr. 2,000

Accumulated depreciation Dr. 1,000

Depreciation expense Cr. 400

1/7/2016 Retained earnings Cr. 600

(20% x $2000 p.a. for 1.5 years)

Income tax expense Dr. 120

1/7/2016 Retained earnings Dr. 180

Deferred tax asset Cr. 300

7. Sale of Plant classified as Inventory: current period

Date Particulars

Dr./

Cr. Amount ($) Amount ($)

Proceeds on sale of plant Dr. 9,000

Carrying amount of plant sold Cr. 7,500

Cost of sales Cr. 1,500

7 | P a g e

8

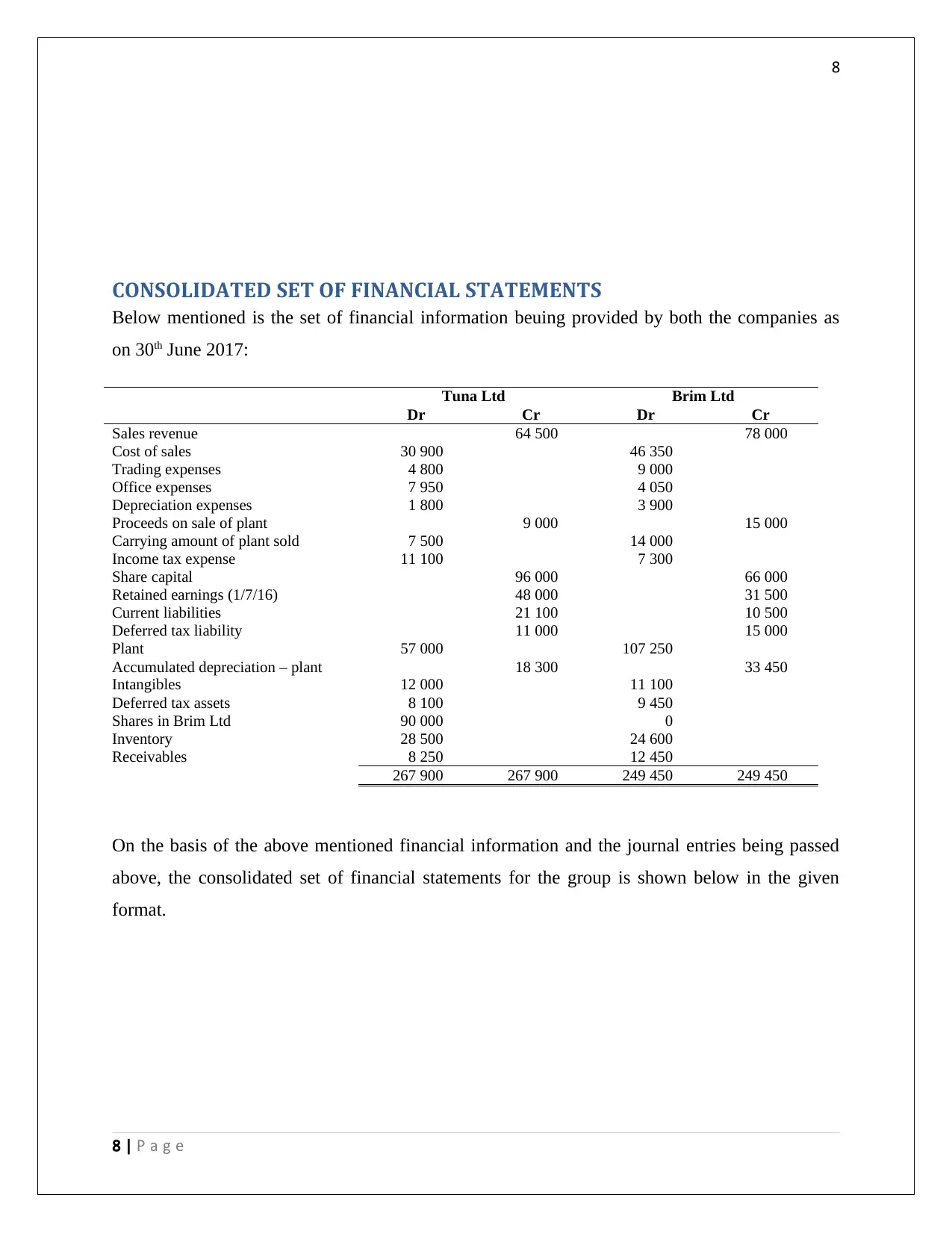

CONSOLIDATED SET OF FINANCIAL STATEMENTS

Below mentioned is the set of financial information beuing provided by both the companies as

on 30th June 2017:

Tuna Ltd Brim Ltd

Dr Cr Dr Cr

Sales revenue 64 500 78 000

Cost of sales 30 900 46 350

Trading expenses 4 800 9 000

Office expenses 7 950 4 050

Depreciation expenses 1 800 3 900

Proceeds on sale of plant 9 000 15 000

Carrying amount of plant sold 7 500 14 000

Income tax expense 11 100 7 300

Share capital 96 000 66 000

Retained earnings (1/7/16) 48 000 31 500

Current liabilities 21 100 10 500

Deferred tax liability 11 000 15 000

Plant 57 000 107 250

Accumulated depreciation – plant 18 300 33 450

Intangibles 12 000 11 100

Deferred tax assets 8 100 9 450

Shares in Brim Ltd 90 000 0

Inventory 28 500 24 600

Receivables 8 250 12 450

267 900 267 900 249 450 249 450

On the basis of the above mentioned financial information and the journal entries being passed

above, the consolidated set of financial statements for the group is shown below in the given

format.

8 | P a g e

CONSOLIDATED SET OF FINANCIAL STATEMENTS

Below mentioned is the set of financial information beuing provided by both the companies as

on 30th June 2017:

Tuna Ltd Brim Ltd

Dr Cr Dr Cr

Sales revenue 64 500 78 000

Cost of sales 30 900 46 350

Trading expenses 4 800 9 000

Office expenses 7 950 4 050

Depreciation expenses 1 800 3 900

Proceeds on sale of plant 9 000 15 000

Carrying amount of plant sold 7 500 14 000

Income tax expense 11 100 7 300

Share capital 96 000 66 000

Retained earnings (1/7/16) 48 000 31 500

Current liabilities 21 100 10 500

Deferred tax liability 11 000 15 000

Plant 57 000 107 250

Accumulated depreciation – plant 18 300 33 450

Intangibles 12 000 11 100

Deferred tax assets 8 100 9 450

Shares in Brim Ltd 90 000 0

Inventory 28 500 24 600

Receivables 8 250 12 450

267 900 267 900 249 450 249 450

On the basis of the above mentioned financial information and the journal entries being passed

above, the consolidated set of financial statements for the group is shown below in the given

format.

8 | P a g e

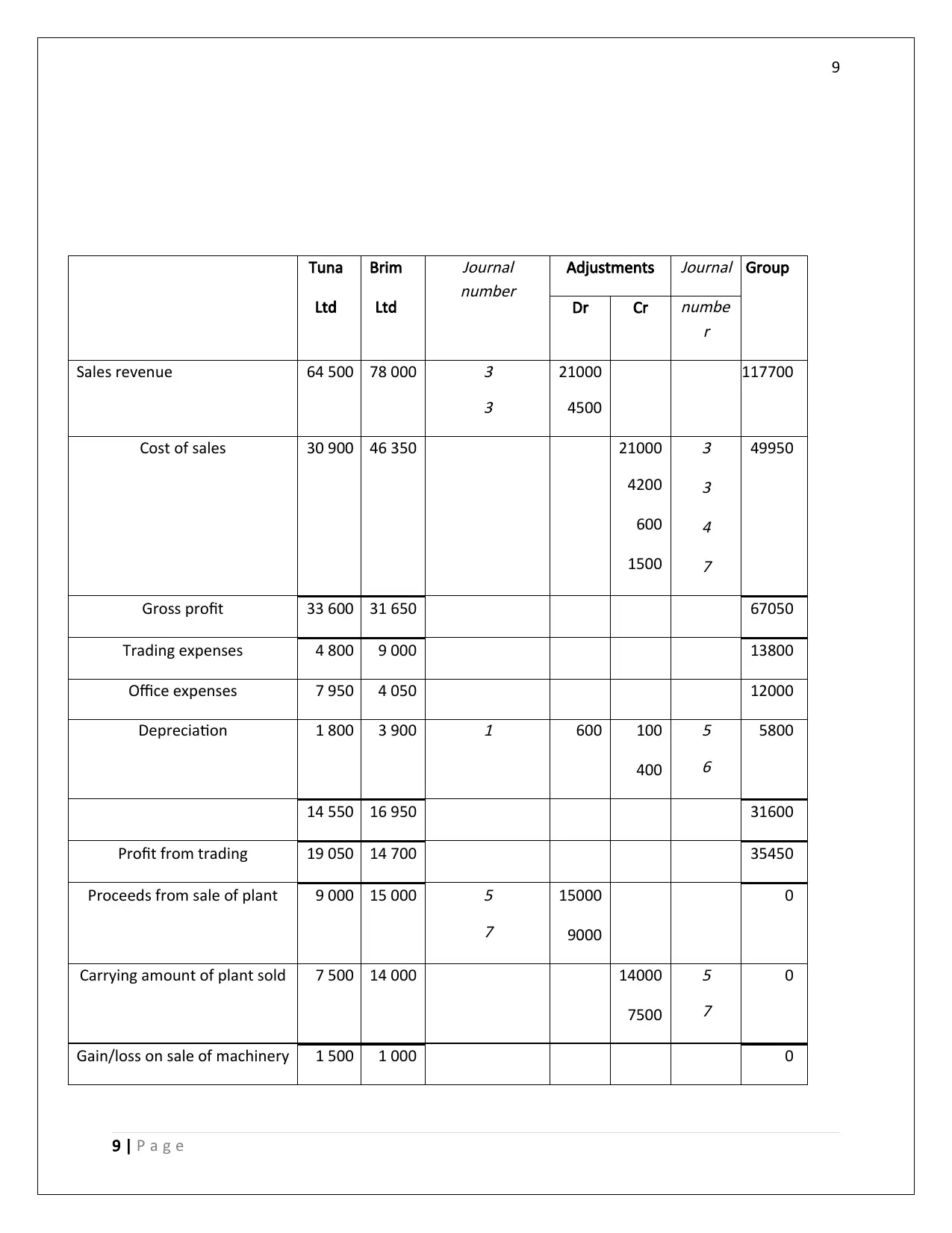

9

Tuna

Ltd

Brim

Ltd

Journal

number

Adjustments

Journal Group

Dr Cr

numbe

r

Sales revenue 64 500 78 000

3

3

21000

4500

117700

Cost of sales 30 900 46 350 21000

4200

600

1500

3

3

4

7

49950

Gross profit 33 600 31 650 67050

Trading expenses 4 800 9 000 13800

Office expenses 7 950 4 050 12000

Depreciation 1 800 3 900

1 600 100

400

5

6

5800

14 550 16 950 31600

Profit from trading 19 050 14 700 35450

Proceeds from sale of plant 9 000 15 000

5

7

15000

9000

0

Carrying amount of plant sold 7 500 14 000 14000

7500

5

7

0

Gain/loss on sale of machinery 1 500 1 000 0

9 | P a g e

Tuna

Ltd

Brim

Ltd

Journal

number

Adjustments

Journal Group

Dr Cr

numbe

r

Sales revenue 64 500 78 000

3

3

21000

4500

117700

Cost of sales 30 900 46 350 21000

4200

600

1500

3

3

4

7

49950

Gross profit 33 600 31 650 67050

Trading expenses 4 800 9 000 13800

Office expenses 7 950 4 050 12000

Depreciation 1 800 3 900

1 600 100

400

5

6

5800

14 550 16 950 31600

Profit from trading 19 050 14 700 35450

Proceeds from sale of plant 9 000 15 000

5

7

15000

9000

0

Carrying amount of plant sold 7 500 14 000 14000

7500

5

7

0

Gain/loss on sale of machinery 1 500 1 000 0

9 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

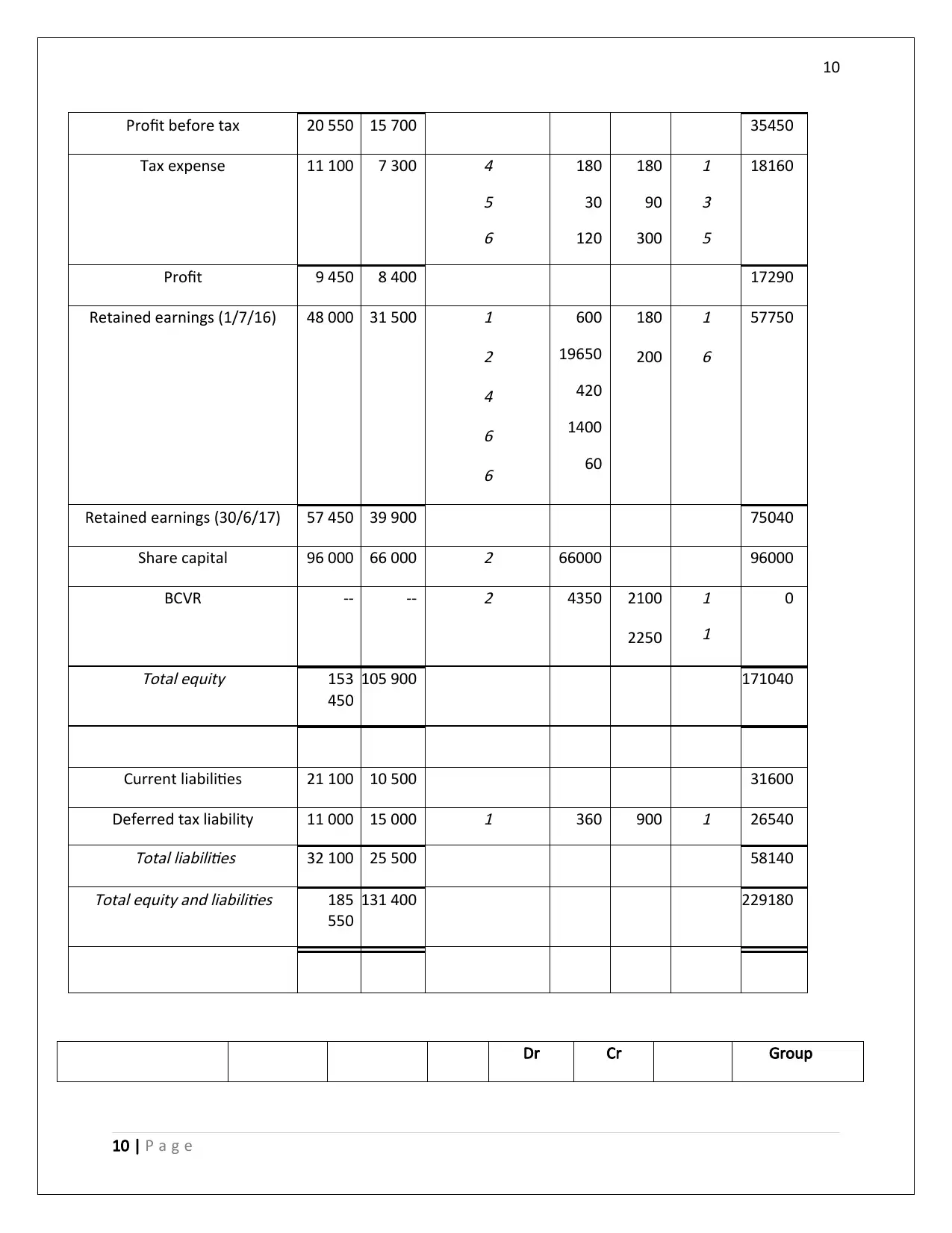

Profit before tax 20 550 15 700 35450

Tax expense 11 100 7 300

4

5

6

180

30

120

180

90

300

1

3

5

18160

Profit 9 450 8 400 17290

Retained earnings (1/7/16) 48 000 31 500

1

2

4

6

6

600

19650

420

1400

60

180

200

1

6

57750

Retained earnings (30/6/17) 57 450 39 900 75040

Share capital 96 000 66 000

2 66000 96000

BCVR -- --

2 4350 2100

2250

1

1

0

Total equity 153

450

105 900 171040

Current liabilities 21 100 10 500 31600

Deferred tax liability 11 000 15 000

1 360 900

1 26540Total liabilities 32 100 25 500 58140

Total equity and liabilities 185

550

131 400 229180

Dr Cr Group

10 | P a g e

Profit before tax 20 550 15 700 35450

Tax expense 11 100 7 300

4

5

6

180

30

120

180

90

300

1

3

5

18160

Profit 9 450 8 400 17290

Retained earnings (1/7/16) 48 000 31 500

1

2

4

6

6

600

19650

420

1400

60

180

200

1

6

57750

Retained earnings (30/6/17) 57 450 39 900 75040

Share capital 96 000 66 000

2 66000 96000

BCVR -- --

2 4350 2100

2250

1

1

0

Total equity 153

450

105 900 171040

Current liabilities 21 100 10 500 31600

Deferred tax liability 11 000 15 000

1 360 900

1 26540Total liabilities 32 100 25 500 58140

Total equity and liabilities 185

550

131 400 229180

Dr Cr Group

10 | P a g e

11

Plant 57 000 107 250 27000

1000

2000

1

5

6

134250

Accumulated

depreciation

(18 300) (33 450)

1

5

6

30000

100

600

1200

1 (22250)

Intangibles 12 000 11 100 23100

Shares in Brim Ltd 90 000 - 90000

2 0

Deferred tax asset 8 100 9 450

3

5

6

90

300

600

30

180

5

6

18330

Inventory 28 500 24 600 300

3 52800

Receivables 8 250 12 450 20700

Goodwill 0 0

1 2250 2250

Total assets 185 550 131 400 177210 177210 229180

Notes on Accounts:

1. The total equity of the group is the sum total of the equity shares share capital), the

retained earnings, the net profit and the general reserves. It is the total capital formulation

of the company over the years put together. In short, it is equal to the net assets of the

company and the thereby both the sides of the balance sheet will be equal (Alexander,

2016).

2. Profit is generally the difference between the incomes and expenses for the year on which

the tax is being paid at 30% and the remainder is profit after tax. This is then being added

to the retained earnings and shown as part of the equity.

11 | P a g e

Plant 57 000 107 250 27000

1000

2000

1

5

6

134250

Accumulated

depreciation

(18 300) (33 450)

1

5

6

30000

100

600

1200

1 (22250)

Intangibles 12 000 11 100 23100

Shares in Brim Ltd 90 000 - 90000

2 0

Deferred tax asset 8 100 9 450

3

5

6

90

300

600

30

180

5

6

18330

Inventory 28 500 24 600 300

3 52800

Receivables 8 250 12 450 20700

Goodwill 0 0

1 2250 2250

Total assets 185 550 131 400 177210 177210 229180

Notes on Accounts:

1. The total equity of the group is the sum total of the equity shares share capital), the

retained earnings, the net profit and the general reserves. It is the total capital formulation

of the company over the years put together. In short, it is equal to the net assets of the

company and the thereby both the sides of the balance sheet will be equal (Alexander,

2016).

2. Profit is generally the difference between the incomes and expenses for the year on which

the tax is being paid at 30% and the remainder is profit after tax. This is then being added

to the retained earnings and shown as part of the equity.

11 | P a g e

12

3. For the current assets like accounts receivables and inventory, the line by line item

consolidation takes place and the book value is added for both the entities while doing

consolidation (Das, 2017).

4. Similarly, for the current liabilities as well like the payables, the line by line item

consolidation takes place (Boccia & Leonardi, 2016).

5. Deferred tax asset or liability is created due to the timing differences. There are some line

items on which the tax is being paid as per taxation laws and the tax as per accounting

laws might need to be paid in the later years, thereby giving rise to the deffered tax asset

or liabilities.

References

Alexander, F., 2016. The Changing Face of Accountability.

The Journal of Higher Education, 71(4), pp.

411-431.

Boccia, F. & Leonardi, R., 2016.

The Challenge of the Digital Economy: Markets, Taxation and

Appropriate Economic Models. s.l.:Springer.

Das, P., 2017. Financing Pattern and Utilization of Fixed Assets - A Study.

Asian Journal of Social Science

Studies, 2(2), pp. 10-17.

Dichev, I., 2017. On the conceptual foundations of financial reporting.

Accounting and Business

Research, 47(6), pp. 617-632.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.Financial Environment and Business Development, Volume 4, pp. 103-112.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting.

Journal of Educational Psychology, 109(2), p. 220.

12 | P a g e

3. For the current assets like accounts receivables and inventory, the line by line item

consolidation takes place and the book value is added for both the entities while doing

consolidation (Das, 2017).

4. Similarly, for the current liabilities as well like the payables, the line by line item

consolidation takes place (Boccia & Leonardi, 2016).

5. Deferred tax asset or liability is created due to the timing differences. There are some line

items on which the tax is being paid as per taxation laws and the tax as per accounting

laws might need to be paid in the later years, thereby giving rise to the deffered tax asset

or liabilities.

References

Alexander, F., 2016. The Changing Face of Accountability.

The Journal of Higher Education, 71(4), pp.

411-431.

Boccia, F. & Leonardi, R., 2016.

The Challenge of the Digital Economy: Markets, Taxation and

Appropriate Economic Models. s.l.:Springer.

Das, P., 2017. Financing Pattern and Utilization of Fixed Assets - A Study.

Asian Journal of Social Science

Studies, 2(2), pp. 10-17.

Dichev, I., 2017. On the conceptual foundations of financial reporting.

Accounting and Business

Research, 47(6), pp. 617-632.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.Financial Environment and Business Development, Volume 4, pp. 103-112.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting.

Journal of Educational Psychology, 109(2), p. 220.

12 | P a g e

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.