Assignment on Accounts - The Profit and Loss Statement

VerifiedAdded on 2022/08/24

|11

|2249

|20

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTS

Accounts

Name of the Student

Name of the University

Author Note

Accounts

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

ACCOUNTS

Table of Contents

Part A...............................................................................................................................................2

Balance Sheet as at October 31st 2019.............................................................................................3

Part B...............................................................................................................................................4

Cash Budget.....................................................................................................................................4

Part 3................................................................................................................................................5

Report Overview..........................................................................................................................5

Analysis of the cash flows...........................................................................................................5

Other Important Factors...............................................................................................................6

References........................................................................................................................................8

ACCOUNTS

Table of Contents

Part A...............................................................................................................................................2

Balance Sheet as at October 31st 2019.............................................................................................3

Part B...............................................................................................................................................4

Cash Budget.....................................................................................................................................4

Part 3................................................................................................................................................5

Report Overview..........................................................................................................................5

Analysis of the cash flows...........................................................................................................5

Other Important Factors...............................................................................................................6

References........................................................................................................................................8

2

ACCOUNTS

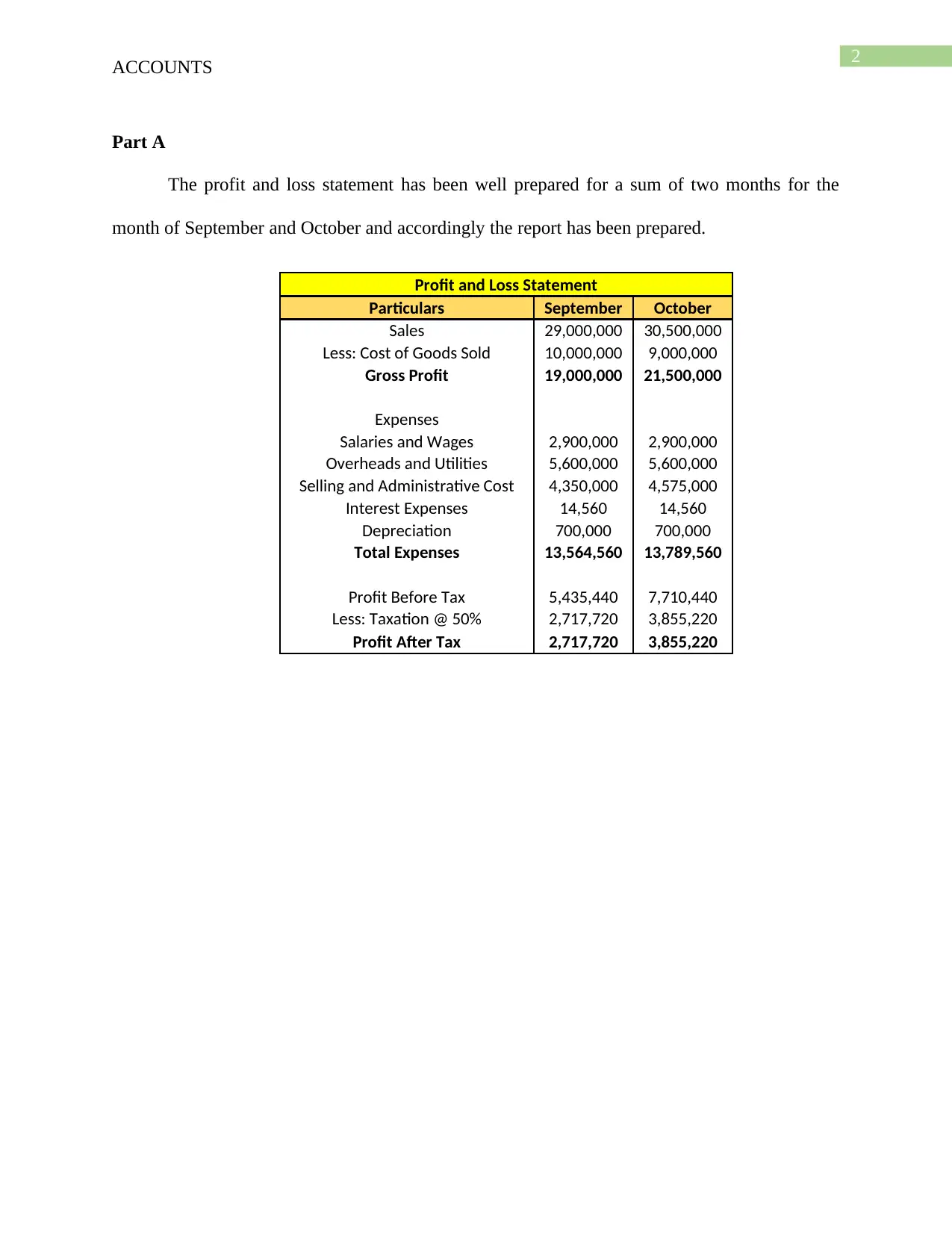

Part A

The profit and loss statement has been well prepared for a sum of two months for the

month of September and October and accordingly the report has been prepared.

Profit and Loss Statement

Particulars September October

Sales 29,000,000 30,500,000

Less: Cost of Goods Sold 10,000,000 9,000,000

Gross Profit 19,000,000 21,500,000

Expenses

Salaries and Wages 2,900,000 2,900,000

Overheads and Utilities 5,600,000 5,600,000

Selling and Administrative Cost 4,350,000 4,575,000

Interest Expenses 14,560 14,560

Depreciation 700,000 700,000

Total Expenses 13,564,560 13,789,560

Profit Before Tax 5,435,440 7,710,440

Less: Taxation @ 50% 2,717,720 3,855,220

Profit After Tax 2,717,720 3,855,220

ACCOUNTS

Part A

The profit and loss statement has been well prepared for a sum of two months for the

month of September and October and accordingly the report has been prepared.

Profit and Loss Statement

Particulars September October

Sales 29,000,000 30,500,000

Less: Cost of Goods Sold 10,000,000 9,000,000

Gross Profit 19,000,000 21,500,000

Expenses

Salaries and Wages 2,900,000 2,900,000

Overheads and Utilities 5,600,000 5,600,000

Selling and Administrative Cost 4,350,000 4,575,000

Interest Expenses 14,560 14,560

Depreciation 700,000 700,000

Total Expenses 13,564,560 13,789,560

Profit Before Tax 5,435,440 7,710,440

Less: Taxation @ 50% 2,717,720 3,855,220

Profit After Tax 2,717,720 3,855,220

3

ACCOUNTS

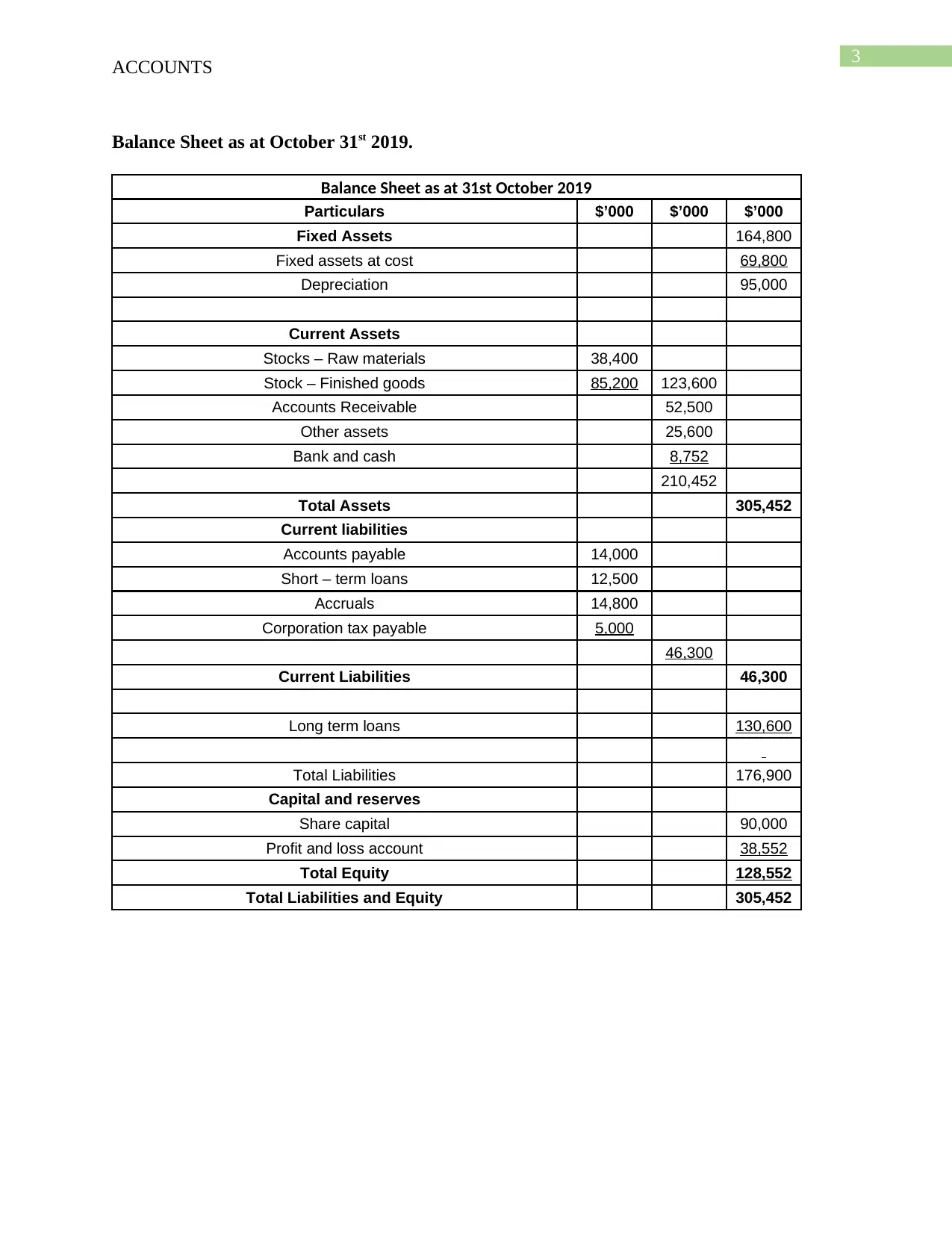

Balance Sheet as at October 31st 2019.

Balance Sheet as at 31st October 2019

Particulars $’000 $’000 $’000

Fixed Assets 164,800

Fixed assets at cost 69,800

Depreciation 95,000

Current Assets

Stocks – Raw materials 38,400

Stock – Finished goods 85,200 123,600

Accounts Receivable 52,500

Other assets 25,600

Bank and cash 8,752

210,452

Total Assets 305,452

Current liabilities

Accounts payable 14,000

Short – term loans 12,500

Accruals 14,800

Corporation tax payable 5,000

46,300

Current Liabilities 46,300

Long term loans 130,600

Total Liabilities 176,900

Capital and reserves

Share capital 90,000

Profit and loss account 38,552

Total Equity 128,552

Total Liabilities and Equity 305,452

ACCOUNTS

Balance Sheet as at October 31st 2019.

Balance Sheet as at 31st October 2019

Particulars $’000 $’000 $’000

Fixed Assets 164,800

Fixed assets at cost 69,800

Depreciation 95,000

Current Assets

Stocks – Raw materials 38,400

Stock – Finished goods 85,200 123,600

Accounts Receivable 52,500

Other assets 25,600

Bank and cash 8,752

210,452

Total Assets 305,452

Current liabilities

Accounts payable 14,000

Short – term loans 12,500

Accruals 14,800

Corporation tax payable 5,000

46,300

Current Liabilities 46,300

Long term loans 130,600

Total Liabilities 176,900

Capital and reserves

Share capital 90,000

Profit and loss account 38,552

Total Equity 128,552

Total Liabilities and Equity 305,452

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

ACCOUNTS

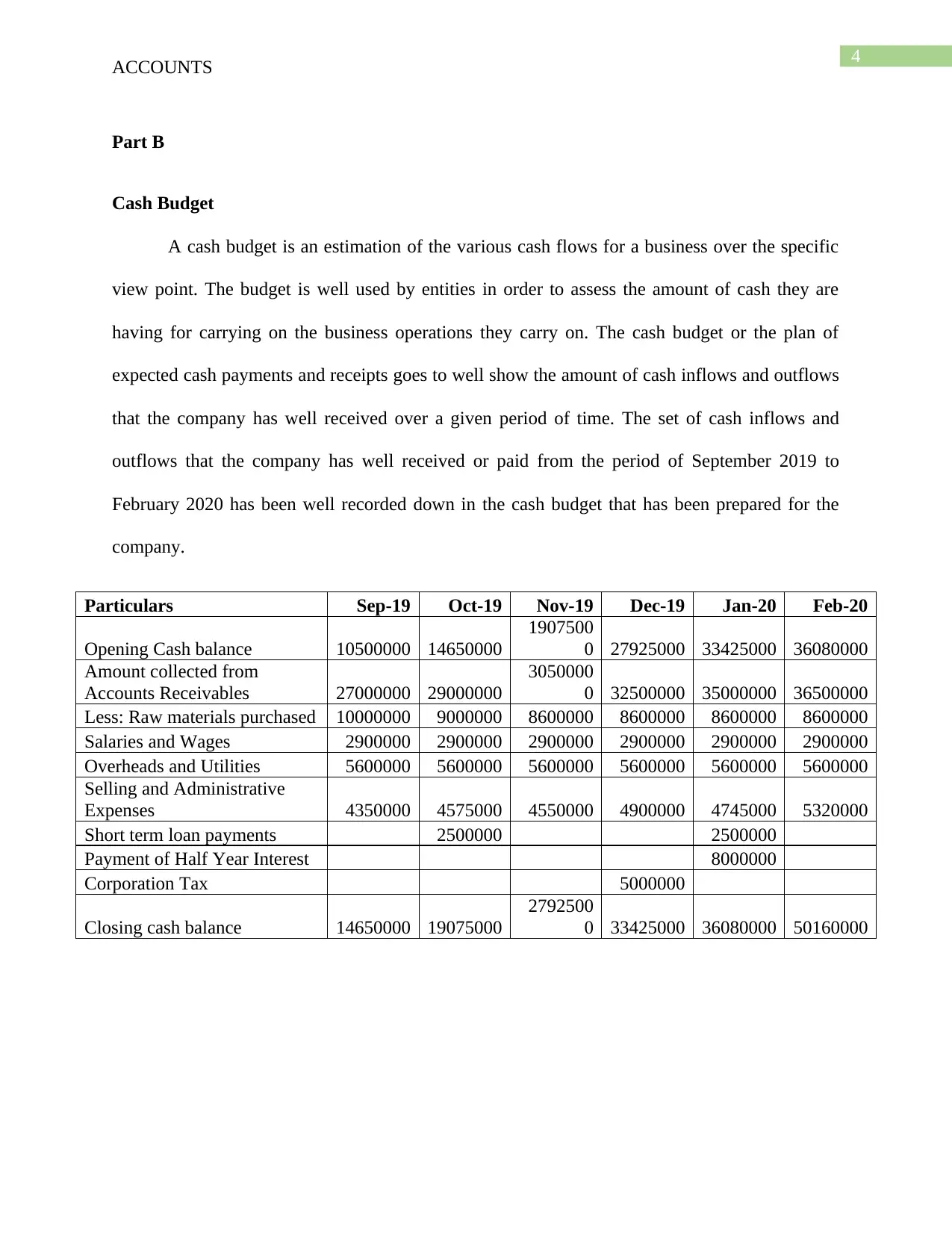

Part B

Cash Budget

A cash budget is an estimation of the various cash flows for a business over the specific

view point. The budget is well used by entities in order to assess the amount of cash they are

having for carrying on the business operations they carry on. The cash budget or the plan of

expected cash payments and receipts goes to well show the amount of cash inflows and outflows

that the company has well received over a given period of time. The set of cash inflows and

outflows that the company has well received or paid from the period of September 2019 to

February 2020 has been well recorded down in the cash budget that has been prepared for the

company.

Particulars Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20

Opening Cash balance 10500000 14650000

1907500

0 27925000 33425000 36080000

Amount collected from

Accounts Receivables 27000000 29000000

3050000

0 32500000 35000000 36500000

Less: Raw materials purchased 10000000 9000000 8600000 8600000 8600000 8600000

Salaries and Wages 2900000 2900000 2900000 2900000 2900000 2900000

Overheads and Utilities 5600000 5600000 5600000 5600000 5600000 5600000

Selling and Administrative

Expenses 4350000 4575000 4550000 4900000 4745000 5320000

Short term loan payments 2500000 2500000

Payment of Half Year Interest 8000000

Corporation Tax 5000000

Closing cash balance 14650000 19075000

2792500

0 33425000 36080000 50160000

ACCOUNTS

Part B

Cash Budget

A cash budget is an estimation of the various cash flows for a business over the specific

view point. The budget is well used by entities in order to assess the amount of cash they are

having for carrying on the business operations they carry on. The cash budget or the plan of

expected cash payments and receipts goes to well show the amount of cash inflows and outflows

that the company has well received over a given period of time. The set of cash inflows and

outflows that the company has well received or paid from the period of September 2019 to

February 2020 has been well recorded down in the cash budget that has been prepared for the

company.

Particulars Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20

Opening Cash balance 10500000 14650000

1907500

0 27925000 33425000 36080000

Amount collected from

Accounts Receivables 27000000 29000000

3050000

0 32500000 35000000 36500000

Less: Raw materials purchased 10000000 9000000 8600000 8600000 8600000 8600000

Salaries and Wages 2900000 2900000 2900000 2900000 2900000 2900000

Overheads and Utilities 5600000 5600000 5600000 5600000 5600000 5600000

Selling and Administrative

Expenses 4350000 4575000 4550000 4900000 4745000 5320000

Short term loan payments 2500000 2500000

Payment of Half Year Interest 8000000

Corporation Tax 5000000

Closing cash balance 14650000 19075000

2792500

0 33425000 36080000 50160000

5

ACCOUNTS

Part 3

Report Overview

Working Capital is the amount of cash or cash equivalents that are available with the

company for the purpose of investment. The changes in the working capital is well determined

with the help of changes in the various cash flows that the company would be observing. These

changes can be in particular due to the change in the current assets or current liabilities of the

company. Thus it is important for the company to well analyse the various changes in the

working capital so that the business operations of the company in particular does not get

affected. In the case analysed for the company the company is well expecting to well

increase its payment receivable from its debtors from 30 days to 60 days. The steps are in turn

taken by the company to well increase the customer payment period so that they can well extend

their payment from a period of 30 days to 60 days this in turn would be well helping the

company offer a variable or increased set of payment period. The same would also allow the

company increase their credit sales, but at the same time slowdown the cash conversion cycle of

the company. The same should be well analysed from the cost benefit perspective that the

company would be undertaking. The decrease in the cash flows of the company should be well

compensated by a higher amount of cash or balance that they should keep in cash equivalents

form so that the regular business activities does not get interrupted. However, on the other hand,

if the company well tries to reduce the current liabilities/obligations or the payment time it takes

at the same time for paying off the liabilities from a period of 30 days to 60 days they can well

do the same for making the cash conversion cycle unchanged. The purpose of preparing this

report is to analyse the changes in the cash flows which are occurring in the entity due to the

changes in the collection terms from 60 days to 30 days. The main change in this case is related

ACCOUNTS

Part 3

Report Overview

Working Capital is the amount of cash or cash equivalents that are available with the

company for the purpose of investment. The changes in the working capital is well determined

with the help of changes in the various cash flows that the company would be observing. These

changes can be in particular due to the change in the current assets or current liabilities of the

company. Thus it is important for the company to well analyse the various changes in the

working capital so that the business operations of the company in particular does not get

affected. In the case analysed for the company the company is well expecting to well

increase its payment receivable from its debtors from 30 days to 60 days. The steps are in turn

taken by the company to well increase the customer payment period so that they can well extend

their payment from a period of 30 days to 60 days this in turn would be well helping the

company offer a variable or increased set of payment period. The same would also allow the

company increase their credit sales, but at the same time slowdown the cash conversion cycle of

the company. The same should be well analysed from the cost benefit perspective that the

company would be undertaking. The decrease in the cash flows of the company should be well

compensated by a higher amount of cash or balance that they should keep in cash equivalents

form so that the regular business activities does not get interrupted. However, on the other hand,

if the company well tries to reduce the current liabilities/obligations or the payment time it takes

at the same time for paying off the liabilities from a period of 30 days to 60 days they can well

do the same for making the cash conversion cycle unchanged. The purpose of preparing this

report is to analyse the changes in the cash flows which are occurring in the entity due to the

changes in the collection terms from 60 days to 30 days. The main change in this case is related

6

ACCOUNTS

to the time period taken to collect the amount from the accounts receivables as a part of the

business (Flannery and Öztekin 2019). The reduction in the time period taken to collect the debts

results in the higher availability of the cash balances with the business. This improves the

liquidity position of the business and reduces the risk of bankruptcy for the business. Working

Capital is the key and prime concern which a company should well consider and the same would

be well helping the company in well maintain the liquidity that is associated for paying off the

current obligations of the company. Now it is important to note that if the credit terms of the

company well changes from a period to 60 days then this would be increasing the Cash

Conversion Cycle of the company. However, on the other hand, side if the period is allowed for a

sum of 30 days then the same would be reducing the Cash Conversion cycle of the company

whereby the management of the company would be having a wide access to a varied amount of

working capital (Shrotriya 2019).

Analysis of the cash flows

In the given situation, the changes have occurred in the overall cash balances of the entity

due to the changes in the collection terms of the customers. The opening cash balance available

with the entity was valued at $10500000 (Dixit and Dubey 2017). The change in the credit terms

gradually brought about a change in the total cash balances available with the entity. It increased

from $14650000 at the end of September 2019 to $50160000 at the end of February 2020. This is

a significant increase in the balances available with the entity. The main advantage of this change

is that the company can invest these funds in the business as they are readily available. The

previously existing 60 days terms resulted in the slow collection of funds from the accounts

receivable. This also adversely impacted the liquidity position of the business and ultimately its

ability to generate growth in a quicker manner (Baños-Caballero, García-Teruel and Martínez-

ACCOUNTS

to the time period taken to collect the amount from the accounts receivables as a part of the

business (Flannery and Öztekin 2019). The reduction in the time period taken to collect the debts

results in the higher availability of the cash balances with the business. This improves the

liquidity position of the business and reduces the risk of bankruptcy for the business. Working

Capital is the key and prime concern which a company should well consider and the same would

be well helping the company in well maintain the liquidity that is associated for paying off the

current obligations of the company. Now it is important to note that if the credit terms of the

company well changes from a period to 60 days then this would be increasing the Cash

Conversion Cycle of the company. However, on the other hand, side if the period is allowed for a

sum of 30 days then the same would be reducing the Cash Conversion cycle of the company

whereby the management of the company would be having a wide access to a varied amount of

working capital (Shrotriya 2019).

Analysis of the cash flows

In the given situation, the changes have occurred in the overall cash balances of the entity

due to the changes in the collection terms of the customers. The opening cash balance available

with the entity was valued at $10500000 (Dixit and Dubey 2017). The change in the credit terms

gradually brought about a change in the total cash balances available with the entity. It increased

from $14650000 at the end of September 2019 to $50160000 at the end of February 2020. This is

a significant increase in the balances available with the entity. The main advantage of this change

is that the company can invest these funds in the business as they are readily available. The

previously existing 60 days terms resulted in the slow collection of funds from the accounts

receivable. This also adversely impacted the liquidity position of the business and ultimately its

ability to generate growth in a quicker manner (Baños-Caballero, García-Teruel and Martínez-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTS

Solano 2016). As the terms of payments to the creditors are for 45 days, it is better to have the

funds available in a much quicker manner. Hence, the shifting in the collection period is also

helpful for the business. Any sudden changes in the business scenario like an emergency

situation or the timely payment of loans is only possible through the timely collection of funds

(Masri and Abdulla 2018).

Other Important Factors

Some other factors which are essential in considering the reduction of the collection

period from 60 days to 30 days include the credit standards, credit period, collection effort and

cash discount. A period of 60 days would have resulted in a higher effort and greater cost of

collection of funds. Hence, the change in the credit policy is beneficial to the entity in reducing

these costs and improving the value of the money. Higher discounts may result in a quicker

collection of funds by the business (Filbeck, Zhao and Knoll 2017). However, this results in a

loss for the entity due to the value of the funds foregone by the business. Stiffer credit policies

also have other disadvantages. They tend to reduce the sales due to the dissatisfaction of the

customers. This may make it difficult for the business to compete with existing parties as the

preferences of the customers may change due to these credit policies. Some other limitations of

this decision include the fact that it is determined on the basis of the pattern of the sales. If the

sales are high, then reducing the collection period is not necessarily a cause of concern. If the

business is not able to sustain these levels, then the decision to reduce the collection period may

not seem too beneficial for the business. Hence, the most important factor to consider in reducing

the collection period is the payment behaviour of the customers and not the amount of sales

happening. Financial as well as non-financial factors, could be well analysed on the level of

changes that would be observed for the changes in the working capital that would be well

ACCOUNTS

Solano 2016). As the terms of payments to the creditors are for 45 days, it is better to have the

funds available in a much quicker manner. Hence, the shifting in the collection period is also

helpful for the business. Any sudden changes in the business scenario like an emergency

situation or the timely payment of loans is only possible through the timely collection of funds

(Masri and Abdulla 2018).

Other Important Factors

Some other factors which are essential in considering the reduction of the collection

period from 60 days to 30 days include the credit standards, credit period, collection effort and

cash discount. A period of 60 days would have resulted in a higher effort and greater cost of

collection of funds. Hence, the change in the credit policy is beneficial to the entity in reducing

these costs and improving the value of the money. Higher discounts may result in a quicker

collection of funds by the business (Filbeck, Zhao and Knoll 2017). However, this results in a

loss for the entity due to the value of the funds foregone by the business. Stiffer credit policies

also have other disadvantages. They tend to reduce the sales due to the dissatisfaction of the

customers. This may make it difficult for the business to compete with existing parties as the

preferences of the customers may change due to these credit policies. Some other limitations of

this decision include the fact that it is determined on the basis of the pattern of the sales. If the

sales are high, then reducing the collection period is not necessarily a cause of concern. If the

business is not able to sustain these levels, then the decision to reduce the collection period may

not seem too beneficial for the business. Hence, the most important factor to consider in reducing

the collection period is the payment behaviour of the customers and not the amount of sales

happening. Financial as well as non-financial factors, could be well analysed on the level of

changes that would be observed for the changes in the working capital that would be well

8

ACCOUNTS

observed as the cash conversion cycle of the company changes. It is crucial to note that the

working capital plays a predominant role and the CCC or the Cash Conversion Cycle is

particularly considered as the same would be helping the company determine the time it is taking

for the company to well recover its cash deployed in the business. Non-financial factors like

goodwill and overall risk of the company could be well affected as the company continues to

raise the time period of collecting the due amount. If the company increases the time period of

collecting its payment from 30 days to 60 days then there is a high possibility that the bad debts

that are associated with the company with respect to the overall payment increases. While at the

same time if 60 days are given it would be allowing the management of the company earn a

confidence of customer along with a wider scale of customer base who would be well willing to

purchase the goods from the company. Thus, it is necessary for the company to take a decision

that is well associated in the betterment of company and which in turn would be creating a better

set of opportunities for the company. The management of the company can do something that is

create or lookup the average amount of time that is well allowed by other companies operating in

the same industry and then accordingly work a plan out. The strategy would not only

management of the company address the financial risk or exposure to excess bad debt but at the

same time would allow the company to increase its business operations with a wider scale of

business operations.

ACCOUNTS

observed as the cash conversion cycle of the company changes. It is crucial to note that the

working capital plays a predominant role and the CCC or the Cash Conversion Cycle is

particularly considered as the same would be helping the company determine the time it is taking

for the company to well recover its cash deployed in the business. Non-financial factors like

goodwill and overall risk of the company could be well affected as the company continues to

raise the time period of collecting the due amount. If the company increases the time period of

collecting its payment from 30 days to 60 days then there is a high possibility that the bad debts

that are associated with the company with respect to the overall payment increases. While at the

same time if 60 days are given it would be allowing the management of the company earn a

confidence of customer along with a wider scale of customer base who would be well willing to

purchase the goods from the company. Thus, it is necessary for the company to take a decision

that is well associated in the betterment of company and which in turn would be creating a better

set of opportunities for the company. The management of the company can do something that is

create or lookup the average amount of time that is well allowed by other companies operating in

the same industry and then accordingly work a plan out. The strategy would not only

management of the company address the financial risk or exposure to excess bad debt but at the

same time would allow the company to increase its business operations with a wider scale of

business operations.

9

ACCOUNTS

References

Adam, C.S. and Bevan, D.L., 2016. 8 The Cash-Budget as a Restraint: The

Experience. Investment and Risk in Africa, p.185.

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2016. Financing of working

capital requirement, financial flexibility and SME performance. Journal of Business Economics

and Management, 17(6), pp.1189-1204.

Dixit, M.S. and Dubey, M.P., 2017. Management of Working Capital. Management, 2(02).

Filbeck, G., Zhao, X. and Knoll, R., 2017. An analysis of working capital efficiency and

shareholder return. Review of Quantitative Finance and Accounting, 48(1), pp.265-288.

Flannery, M.J. and Öztekin, Ö., 2019. Working-Capital and Capital Structure. Available at SSRN

3479180.

Kookda, R.S. and Shukla, A., 2019. Is Working Capital Really Working in the Indian Cement

Industry. Our Heritage, 67(2), pp.1950-1959.

Kumaraswamy, S., 2016. Impact of working capital on financial performance of gulf cooperation

council firms. International Journal of Economics and Financial Issues, 6(3), pp.1136-1143.

Mariana, Z., 2018. THE CASH BUDGET–A SHORT-TERM FORECAST TOOL FOR THE

FINANCIAL STATEMENTS OF ECONOMIC ENTITIES. Ecoforum Journal, 7(2).

Masri, H. and Abdulla, Y., 2018. A multiple objective stochastic programming model for

working capital management. Technological Forecasting and Social Change, 131, pp.141-146.

ACCOUNTS

References

Adam, C.S. and Bevan, D.L., 2016. 8 The Cash-Budget as a Restraint: The

Experience. Investment and Risk in Africa, p.185.

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2016. Financing of working

capital requirement, financial flexibility and SME performance. Journal of Business Economics

and Management, 17(6), pp.1189-1204.

Dixit, M.S. and Dubey, M.P., 2017. Management of Working Capital. Management, 2(02).

Filbeck, G., Zhao, X. and Knoll, R., 2017. An analysis of working capital efficiency and

shareholder return. Review of Quantitative Finance and Accounting, 48(1), pp.265-288.

Flannery, M.J. and Öztekin, Ö., 2019. Working-Capital and Capital Structure. Available at SSRN

3479180.

Kookda, R.S. and Shukla, A., 2019. Is Working Capital Really Working in the Indian Cement

Industry. Our Heritage, 67(2), pp.1950-1959.

Kumaraswamy, S., 2016. Impact of working capital on financial performance of gulf cooperation

council firms. International Journal of Economics and Financial Issues, 6(3), pp.1136-1143.

Mariana, Z., 2018. THE CASH BUDGET–A SHORT-TERM FORECAST TOOL FOR THE

FINANCIAL STATEMENTS OF ECONOMIC ENTITIES. Ecoforum Journal, 7(2).

Masri, H. and Abdulla, Y., 2018. A multiple objective stochastic programming model for

working capital management. Technological Forecasting and Social Change, 131, pp.141-146.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

ACCOUNTS

Sarwat, S., Iqbal, D., Durrani, B.A., Shaikh, K.H. and Liaquat, F., 2017. Impact of working

capital management on the profitability of firms: Case of Pakistan’s cement sector. Journal of

Advanced Management Science Vol, 5(3).

Shrotriya, V., 2019. Analysis of Net Working Capital of Nestle India Limited.

ACCOUNTS

Sarwat, S., Iqbal, D., Durrani, B.A., Shaikh, K.H. and Liaquat, F., 2017. Impact of working

capital management on the profitability of firms: Case of Pakistan’s cement sector. Journal of

Advanced Management Science Vol, 5(3).

Shrotriya, V., 2019. Analysis of Net Working Capital of Nestle India Limited.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.