College of Admin: ACCT 301 Cost Accounting Assignment on Budgeting

VerifiedAdded on 2022/09/14

|10

|1364

|29

Homework Assignment

AI Summary

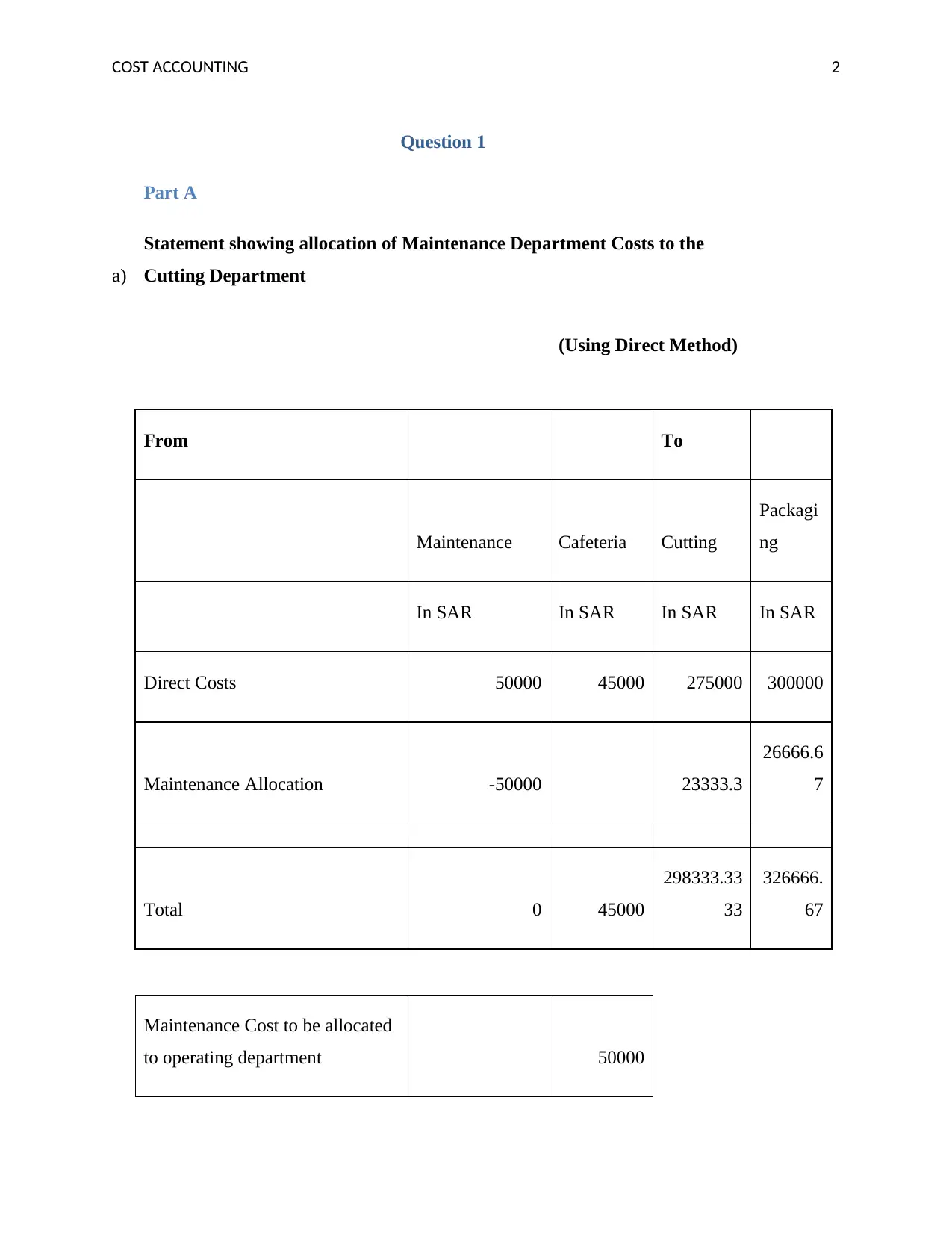

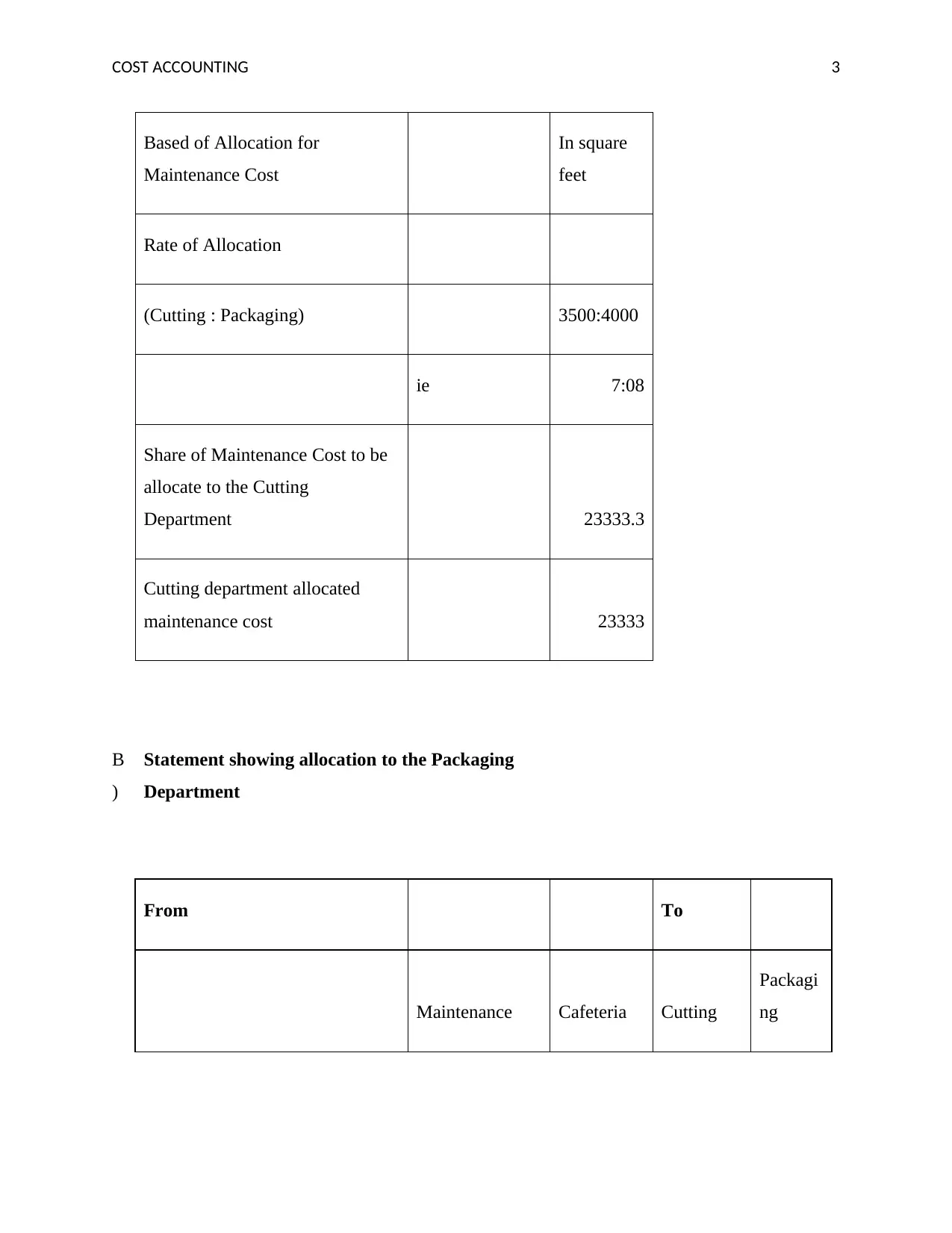

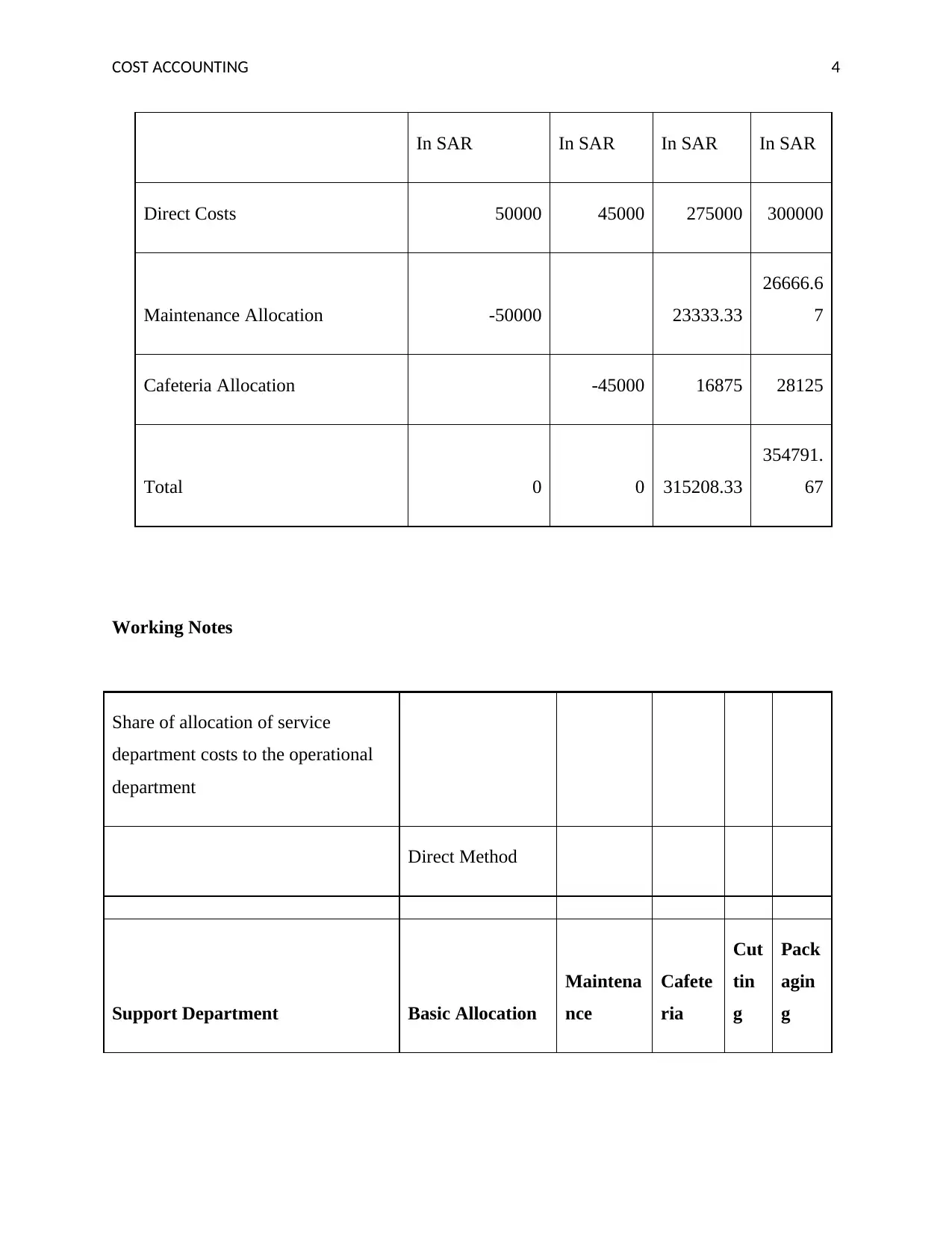

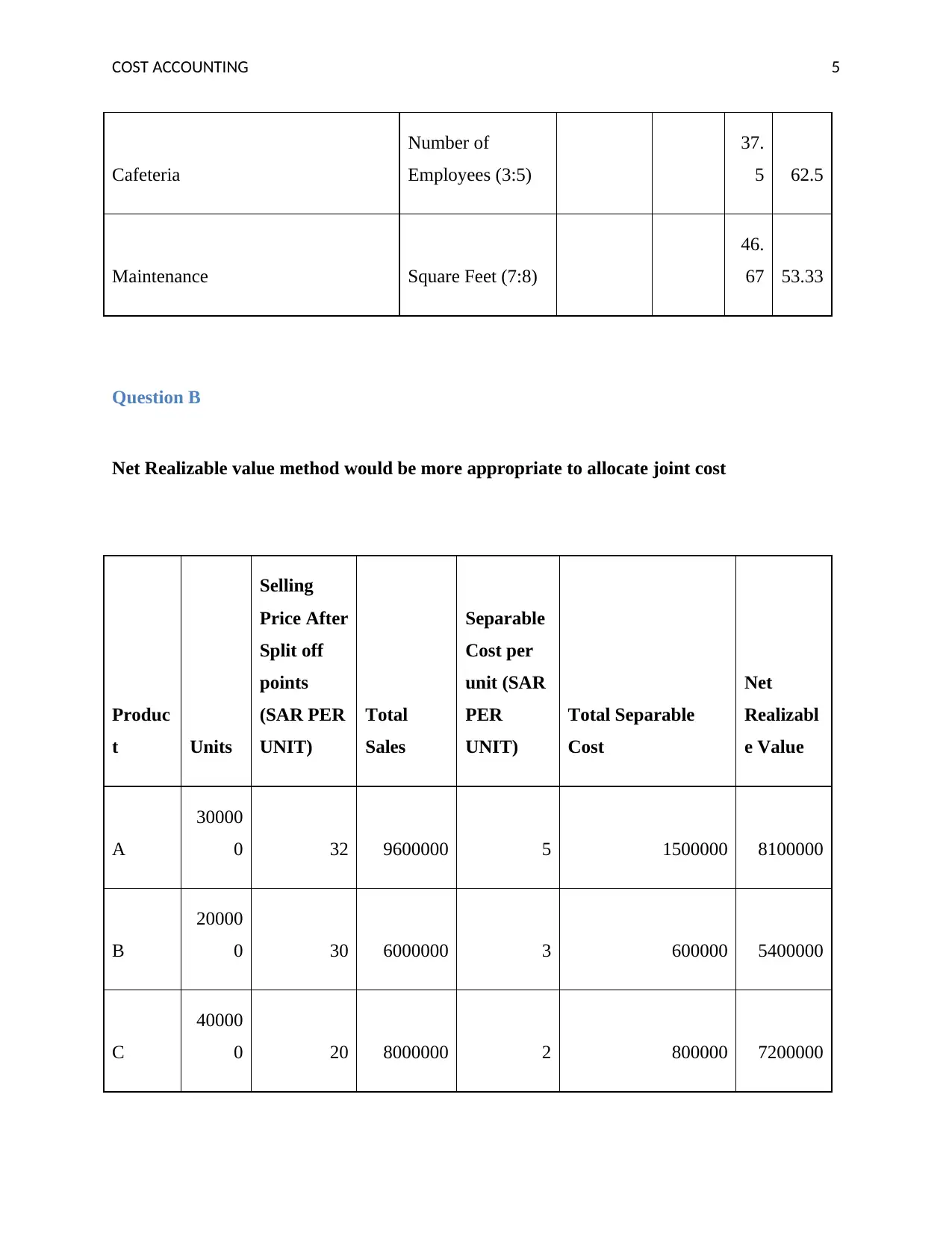

This assignment presents a comprehensive solution to a cost accounting problem. It begins with the allocation of maintenance department costs to the cutting and packaging departments using the direct method, providing detailed calculations. The assignment then explores the net realizable value method for allocating joint costs, offering a practical example. Furthermore, it delves into the comparison of different methods of allocating departmental support costs, specifically the direct, step, and reciprocal methods, with a preference for the reciprocal approach. The solution also explains unfavorable variances, outlining potential causes such as labor rate and efficiency variances, material variances, and overhead variances. Finally, it discusses the effects of budgeting, emphasizing its role in planning, performance evaluation, and employee engagement. The assignment is well-structured, offering a clear understanding of cost accounting concepts with relevant examples and explanations.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.