Theory and Current Issues in Accounting - AASB Framework

VerifiedAdded on 2023/06/07

|17

|3251

|127

AI Summary

This article discusses the AASB framework for financial statements and the issues related to it. It covers the elements of financial statements, recognition and measurement criteria, and the controversy around disclosure requirements. The article also includes a comparison of the essential characteristics of an asset, the fair value measurement approach, and the historical costing approach. Finally, it discusses the issue of disclosure overload and provides an example from BHP Billiton Ltd's annual report.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

THEORY AND CURRENT ISSUES IN ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

EXECUTIVE SUMMARY

Australian Accounting Standards Board (AASB), in December 2013, incorporated certain

changes in the AASB framework for the presentation and preparation of financial statements.

Such changes included chapter 1 and 3 of the international accounting standard board's

(IASB) conceptual framework for financial reporting (September, 2010). When further

changes were made in IASB's standards, the AASB decided to make change in the AASB

framework to the extent of chapter 1 and 3 as necessary and retain the existing framework.

The Exposure Draft was made to include more areas than the existing one and a more

detailed description of such areas, disclosure requirements, and recognition and

derecognition, measurement financial performance, introduction of other comprehensive

income and the financial reporting entity.

Australian Accounting Standards Board (AASB), in December 2013, incorporated certain

changes in the AASB framework for the presentation and preparation of financial statements.

Such changes included chapter 1 and 3 of the international accounting standard board's

(IASB) conceptual framework for financial reporting (September, 2010). When further

changes were made in IASB's standards, the AASB decided to make change in the AASB

framework to the extent of chapter 1 and 3 as necessary and retain the existing framework.

The Exposure Draft was made to include more areas than the existing one and a more

detailed description of such areas, disclosure requirements, and recognition and

derecognition, measurement financial performance, introduction of other comprehensive

income and the financial reporting entity.

Contents

INTRODUCTION......................................................................................................................3

Solution 1...................................................................................................................................4

Solution 2:..................................................................................................................................5

Solution 3:..................................................................................................................................7

Solution 4...................................................................................................................................8

Solution 5:..................................................................................................................................9

Solution 6:................................................................................................................................10

Solution 7:................................................................................................................................11

CONCLUSION........................................................................................................................12

Bibliography.............................................................................................................................13

INTRODUCTION......................................................................................................................3

Solution 1...................................................................................................................................4

Solution 2:..................................................................................................................................5

Solution 3:..................................................................................................................................7

Solution 4...................................................................................................................................8

Solution 5:..................................................................................................................................9

Solution 6:................................................................................................................................10

Solution 7:................................................................................................................................11

CONCLUSION........................................................................................................................12

Bibliography.............................................................................................................................13

INTRODUCTION

The current assignment is about AASB's accounting conceptual framework, 2014 that has

been applied upon financial reports prepared on or after July 1, 2014. It is expected by the

accounting industry to account for transactions in such a way that a qualitative report is being

made. Company accountants are expected to address the information which are critical in

nature for developing the appropriate accounting standard. The four fundamental issues are

definition of the element of financial statement, recognition and measurement of such

elements and appropriate disclosures related to that. The AASB has to consider the above

stated issues while presenting a framework for preparation and presentation of financial

statements (Atkinson, 2012).

However, controversies arises in relation to the fourth issue, that is, disclosure requirements.

The AASB framework of 2014 is criticized on this ground that proper guidance aren't

provided as to what disclosures should be made and not. The principles and practices

regarding disclosures are not clearly stated by AASB.

The current assignment is about AASB's accounting conceptual framework, 2014 that has

been applied upon financial reports prepared on or after July 1, 2014. It is expected by the

accounting industry to account for transactions in such a way that a qualitative report is being

made. Company accountants are expected to address the information which are critical in

nature for developing the appropriate accounting standard. The four fundamental issues are

definition of the element of financial statement, recognition and measurement of such

elements and appropriate disclosures related to that. The AASB has to consider the above

stated issues while presenting a framework for preparation and presentation of financial

statements (Atkinson, 2012).

However, controversies arises in relation to the fourth issue, that is, disclosure requirements.

The AASB framework of 2014 is criticized on this ground that proper guidance aren't

provided as to what disclosures should be made and not. The principles and practices

regarding disclosures are not clearly stated by AASB.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Solution 1.

Chapter 3 enumerates the role of financial reports. It :

Tells us that financial statements are prepared using the perception of the organization

as a whole, instead of the perception of dependent stakeholders such as lenders,

investors or shareholders or other creditors.

Follows the assumption of going concern which is brought forward from the existing

conceptual framework.

Chapter 4 discusses the elements of financial statements. Elements of financial statements are

described as such important elements that has to be a part of entities or upon which the entity

depends. Such elements need to be presented in the most appropriate manner in the balance

sheet along with required disclosures in the notes. Balance sheet or revenue statement

presentation means presenting such elements (Berry, 2009). The elements of financial

statements si stated and discussed in brief below:

1. Assets: An asset is considered as an economic resource which is a result of past actions

and is controlled by the organization. The term economic resource is defined as the

capability to produce economic benefits for the company.

2. Liability: a liability is an obligation over the company in the present which requires the

transferring of economic resource and has occurred due to past events.

3. Equity: Equity is defined as the financial strength of an entity as it shows the interests of

the owners in the assets of the organization after removing the liabilities in terms of

values (Boyd, 2013).

4. Income: As the name suggests, it is the increase in the equity value of the owners due to

either there is an increase in the assets or decrease in the liabilities and is totally different

from the investments made by the equity holders.

5. Expenses: Expenses are totally an opposite of incomes. It results in the decrease of equity

value if there is a decrease in assets or increase in liabilities and is totally different from

distributions made to the equity holders voluntarily.

Chapter 3 enumerates the role of financial reports. It :

Tells us that financial statements are prepared using the perception of the organization

as a whole, instead of the perception of dependent stakeholders such as lenders,

investors or shareholders or other creditors.

Follows the assumption of going concern which is brought forward from the existing

conceptual framework.

Chapter 4 discusses the elements of financial statements. Elements of financial statements are

described as such important elements that has to be a part of entities or upon which the entity

depends. Such elements need to be presented in the most appropriate manner in the balance

sheet along with required disclosures in the notes. Balance sheet or revenue statement

presentation means presenting such elements (Berry, 2009). The elements of financial

statements si stated and discussed in brief below:

1. Assets: An asset is considered as an economic resource which is a result of past actions

and is controlled by the organization. The term economic resource is defined as the

capability to produce economic benefits for the company.

2. Liability: a liability is an obligation over the company in the present which requires the

transferring of economic resource and has occurred due to past events.

3. Equity: Equity is defined as the financial strength of an entity as it shows the interests of

the owners in the assets of the organization after removing the liabilities in terms of

values (Boyd, 2013).

4. Income: As the name suggests, it is the increase in the equity value of the owners due to

either there is an increase in the assets or decrease in the liabilities and is totally different

from the investments made by the equity holders.

5. Expenses: Expenses are totally an opposite of incomes. It results in the decrease of equity

value if there is a decrease in assets or increase in liabilities and is totally different from

distributions made to the equity holders voluntarily.

Solution 2:

The stated elements of financial statements are required to be compared on the basis of

definition and recognition. Such comparison can be explained with the help of the following

table:

Elements of

financial statements

Definition Criteria for Recognition

Assets Assets are the resources through which

an entity derives economic benefits.

Such assets are under the control of the

entity.

An asset is required to be

recognized only when :

It is probable that

economic benefits

would occur in the

future ;

The asset has a cost

or can be measured

in values reliably.

Liabilities Liabilities are an obligation on the

entity that it has to pay back and would

be satisfied by using the economic

benefits. It is a result of past

transactions of the company.

A liability is required to be

recognized only when :

It is probable that

such liabilities have

to satisfy through a

sacrifice from the

economic benefits of

the company.

The value of the

liabilities is

measurable in terms

of value.

Equity It is the net assets after deduction of

liabilities which represents the interests

of the company owners.

There are no such criteria as

it is simply a deduction of

liabilities from the assets.

The stated elements of financial statements are required to be compared on the basis of

definition and recognition. Such comparison can be explained with the help of the following

table:

Elements of

financial statements

Definition Criteria for Recognition

Assets Assets are the resources through which

an entity derives economic benefits.

Such assets are under the control of the

entity.

An asset is required to be

recognized only when :

It is probable that

economic benefits

would occur in the

future ;

The asset has a cost

or can be measured

in values reliably.

Liabilities Liabilities are an obligation on the

entity that it has to pay back and would

be satisfied by using the economic

benefits. It is a result of past

transactions of the company.

A liability is required to be

recognized only when :

It is probable that

such liabilities have

to satisfy through a

sacrifice from the

economic benefits of

the company.

The value of the

liabilities is

measurable in terms

of value.

Equity It is the net assets after deduction of

liabilities which represents the interests

of the company owners.

There are no such criteria as

it is simply a deduction of

liabilities from the assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

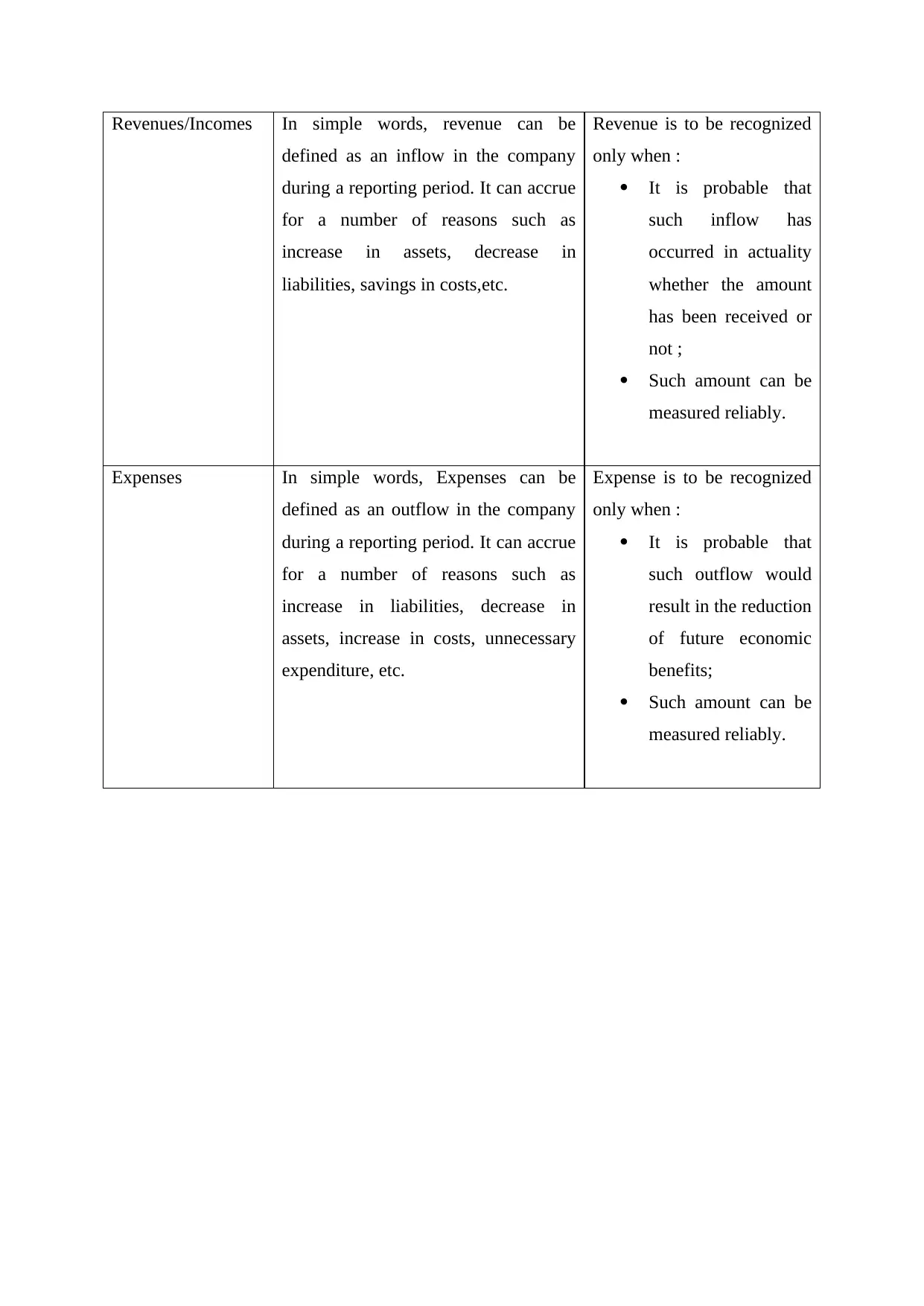

Revenues/Incomes In simple words, revenue can be

defined as an inflow in the company

during a reporting period. It can accrue

for a number of reasons such as

increase in assets, decrease in

liabilities, savings in costs,etc.

Revenue is to be recognized

only when :

It is probable that

such inflow has

occurred in actuality

whether the amount

has been received or

not ;

Such amount can be

measured reliably.

Expenses In simple words, Expenses can be

defined as an outflow in the company

during a reporting period. It can accrue

for a number of reasons such as

increase in liabilities, decrease in

assets, increase in costs, unnecessary

expenditure, etc.

Expense is to be recognized

only when :

It is probable that

such outflow would

result in the reduction

of future economic

benefits;

Such amount can be

measured reliably.

defined as an inflow in the company

during a reporting period. It can accrue

for a number of reasons such as

increase in assets, decrease in

liabilities, savings in costs,etc.

Revenue is to be recognized

only when :

It is probable that

such inflow has

occurred in actuality

whether the amount

has been received or

not ;

Such amount can be

measured reliably.

Expenses In simple words, Expenses can be

defined as an outflow in the company

during a reporting period. It can accrue

for a number of reasons such as

increase in liabilities, decrease in

assets, increase in costs, unnecessary

expenditure, etc.

Expense is to be recognized

only when :

It is probable that

such outflow would

result in the reduction

of future economic

benefits;

Such amount can be

measured reliably.

Solution 3:

As already discussed above regarding what an asset is, we would be here discussing the

essential characteristics of an asset which can be explained as :

The definition of an asset outlines three characteristics. Firstly, there must occur economic

benefits in the future (Bragg, 2016). Secondly, the entity should have a strong control over

the benefits in a sense that it is able to derive such benefits by preventing others to have such

benefits. Thirdly, the entity’s control over such future benefits should have occurred as a

result of some happening of transactions or events. The other characteristics of an asset

include tangibility, acquisition of assets at cost, legal compliances, life of an asset, etc.

However, such characteristics are not essential in nature. Let us now discuss the nature of

such essential characteristics:

"Future Economic Benefits" is defined as the capacity of the entity to derive benefits

from the capacity of an asset whether in physical form or not. An entity creates a

value by utilizing these assets to produce such goods and services. Thus, assets serve

as means for the entity to justify their objectives (Dash, 2016).

The second essential characteristic revolves around the control of an entity which

defines the ability of the entity to derive the benefits from the assets. The "control"

can be defined as the right of the company to exchange the asset, or make use of it to

provide the goods or services, using it as securities, or to settle some liabilities over

the entity or for distribution to the entity's owners.

As discussed in the above point regarding the capability of the entity, such rights

arises from the legal rights and can be proved through documents of possession or

sanctions or such other documents that can be used as an evidence to protect the

interests of the entity.

In certain circumstances, the entity cannot deny the control to other entities to derive

future economic benefits. For example, a number of entities use highways for their

operations that represent future economic benefits but they cannot claim it as an asset

and can be qualified as an asset for entities responsible for its operation.

The third important characteristic include occurrence of past transactions. Assets can

be either obtained through cash or credit or exchange or on installment basis. Some

As already discussed above regarding what an asset is, we would be here discussing the

essential characteristics of an asset which can be explained as :

The definition of an asset outlines three characteristics. Firstly, there must occur economic

benefits in the future (Bragg, 2016). Secondly, the entity should have a strong control over

the benefits in a sense that it is able to derive such benefits by preventing others to have such

benefits. Thirdly, the entity’s control over such future benefits should have occurred as a

result of some happening of transactions or events. The other characteristics of an asset

include tangibility, acquisition of assets at cost, legal compliances, life of an asset, etc.

However, such characteristics are not essential in nature. Let us now discuss the nature of

such essential characteristics:

"Future Economic Benefits" is defined as the capacity of the entity to derive benefits

from the capacity of an asset whether in physical form or not. An entity creates a

value by utilizing these assets to produce such goods and services. Thus, assets serve

as means for the entity to justify their objectives (Dash, 2016).

The second essential characteristic revolves around the control of an entity which

defines the ability of the entity to derive the benefits from the assets. The "control"

can be defined as the right of the company to exchange the asset, or make use of it to

provide the goods or services, using it as securities, or to settle some liabilities over

the entity or for distribution to the entity's owners.

As discussed in the above point regarding the capability of the entity, such rights

arises from the legal rights and can be proved through documents of possession or

sanctions or such other documents that can be used as an evidence to protect the

interests of the entity.

In certain circumstances, the entity cannot deny the control to other entities to derive

future economic benefits. For example, a number of entities use highways for their

operations that represent future economic benefits but they cannot claim it as an asset

and can be qualified as an asset for entities responsible for its operation.

The third important characteristic include occurrence of past transactions. Assets can

be either obtained through cash or credit or exchange or on installment basis. Some

transactions can be of non reciprocal nature such as donations, contributions,

government grants, etc. Assets may even result from discovery (Datar , 2015).

government grants, etc. Assets may even result from discovery (Datar , 2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Solution 4.

As discussed already, an asset is to be recognized only when it is probable that the future

economic benefits from an asset will occur and that the cost of the asset can be reliably

measured ( Datar ,2015).

For the sake of recognition in terms of value, it is important for an asset to possess a cost that

can be measured reliably. The term reliable is used in reference to the term 'reliability' used in

SAC 3 "Qualitative Characteristics Of Financial Information “The basis of measuring an

asset depends upon the accounting model used by the reporting entity. In most cases the

assets would already have a value or cost (Donanldson, 2012). However, in cases where the

cost cannot be identified, the item couldn't be recognized as an asset under any of the

accounting models. For example, a mining company might discover the existence of minerals

at one of its sites at some insignificant cost but couldn't report for the exact value.

AASB 113 requires fair value measurement of assets. Here, fair value refers to the market

value measurement. It defines a price at which a transaction might take place to sell off an

asset to other market participants under the present market conditions on a measurement date.

Where a price is not available in the market, the entity uses other valuation techniques.

The arguments to support the measurement of assets by fair value approach are because of

the following objectives:

Fair value measurement is considered as the most relevant approach for making

decisions. Such an amount is relevant for making decisions whether to sell it off or to

held it or to lease it out or for comparison purposes.

Fair value measurement is a determination in reference to the market price which is

determined by the external forces which are out of control of the entity. In this way,

the price wouldn't be regarded as biased and the same value couldn't be manipulated

or controlled by the entity (Edwards, 2014).

Such measurement would reveal the true capacity of an entity as the fair value

considers depreciation and in that way, the value of asset tends to decrease with every

year showing the true value. However, entities following historical costing would not

show a true measurement of assets as if an asset has a life of 10 years, suppose, it

As discussed already, an asset is to be recognized only when it is probable that the future

economic benefits from an asset will occur and that the cost of the asset can be reliably

measured ( Datar ,2015).

For the sake of recognition in terms of value, it is important for an asset to possess a cost that

can be measured reliably. The term reliable is used in reference to the term 'reliability' used in

SAC 3 "Qualitative Characteristics Of Financial Information “The basis of measuring an

asset depends upon the accounting model used by the reporting entity. In most cases the

assets would already have a value or cost (Donanldson, 2012). However, in cases where the

cost cannot be identified, the item couldn't be recognized as an asset under any of the

accounting models. For example, a mining company might discover the existence of minerals

at one of its sites at some insignificant cost but couldn't report for the exact value.

AASB 113 requires fair value measurement of assets. Here, fair value refers to the market

value measurement. It defines a price at which a transaction might take place to sell off an

asset to other market participants under the present market conditions on a measurement date.

Where a price is not available in the market, the entity uses other valuation techniques.

The arguments to support the measurement of assets by fair value approach are because of

the following objectives:

Fair value measurement is considered as the most relevant approach for making

decisions. Such an amount is relevant for making decisions whether to sell it off or to

held it or to lease it out or for comparison purposes.

Fair value measurement is a determination in reference to the market price which is

determined by the external forces which are out of control of the entity. In this way,

the price wouldn't be regarded as biased and the same value couldn't be manipulated

or controlled by the entity (Edwards, 2014).

Such measurement would reveal the true capacity of an entity as the fair value

considers depreciation and in that way, the value of asset tends to decrease with every

year showing the true value. However, entities following historical costing would not

show a true measurement of assets as if an asset has a life of 10 years, suppose, it

would be showing the value of first year in the 10th year. Thus, unnecessarily the

asset side of a company would be more than its actual capacity or value.

Solution 5:

Historical costing is an uniform and simple accounting model that prefers using the original

cost of an asset (Girard, 2014). The reasons for using of historical costing by accountants in

spite of certain disagreement can be enumerated as :

1. Adopting fair value measurement is a subjective concept ad different person's can adopt

different methods of valuation. Due to fair value measurement, people would measure

their assets at a price higher than the actual cost so as to show a strong position of the

company. Also, they might use the market conditions of recession, decline, trade cycles,

etc so as to show a downward revaluation and charge it to profit and loss account, this

saving themselves from tax norms. Recording assets at their original cost helps in

eradicating the problem of window dressing.

2. FMV can lead to serious circumstances of not valuing an asset properly such as

volatility in market would change the value of an asset on a daily basis; companies

might use it to show favorable and desired results in their financial statements so as to

enjoy the benefits of strong creditworthiness. In the end, such companies are unable to

fulfill their credit pressure and end up being bankrupt (Gow, 2016).

Stewardship theory is entrusting the responsibility on the managers to take control of the

assets in a say to provide sufficient interests to its shareholders. Thus, stewardship

distinguishes between responsibility for actions and responsibility for managing where

responsibility of managing has the responsibility of decisions or actions that might take place

on the basis of that. Relating the historical approach with stewardship theory, it can be said

that the accountants are considering stewardship as a goal (Holtzman, 2013).

asset side of a company would be more than its actual capacity or value.

Solution 5:

Historical costing is an uniform and simple accounting model that prefers using the original

cost of an asset (Girard, 2014). The reasons for using of historical costing by accountants in

spite of certain disagreement can be enumerated as :

1. Adopting fair value measurement is a subjective concept ad different person's can adopt

different methods of valuation. Due to fair value measurement, people would measure

their assets at a price higher than the actual cost so as to show a strong position of the

company. Also, they might use the market conditions of recession, decline, trade cycles,

etc so as to show a downward revaluation and charge it to profit and loss account, this

saving themselves from tax norms. Recording assets at their original cost helps in

eradicating the problem of window dressing.

2. FMV can lead to serious circumstances of not valuing an asset properly such as

volatility in market would change the value of an asset on a daily basis; companies

might use it to show favorable and desired results in their financial statements so as to

enjoy the benefits of strong creditworthiness. In the end, such companies are unable to

fulfill their credit pressure and end up being bankrupt (Gow, 2016).

Stewardship theory is entrusting the responsibility on the managers to take control of the

assets in a say to provide sufficient interests to its shareholders. Thus, stewardship

distinguishes between responsibility for actions and responsibility for managing where

responsibility of managing has the responsibility of decisions or actions that might take place

on the basis of that. Relating the historical approach with stewardship theory, it can be said

that the accountants are considering stewardship as a goal (Holtzman, 2013).

Solution 6:

The term 'disclosure overload' became an issue in financial report that became one of the

topmost priorities of IASB or Board (Horngren, 2012). The reasons why there was no

reference to disclosures practices in financial reporting are:

The common format cannot be used for representing every kind of information.

Therefore, due to increase in volume of information and complex accounting

standards, use of different formats can be used to deliver a better understanding of the

financial reports (Mattessich, 2016).

The users of financial reports find disclosures overlapping and therefore, they do not

find useful decision making information.

There is a little knowledge of deciding a fact as material or immaterial. Thus,

disclosure overload increases if the information disclosed are of immaterial nature

(McLaney & Adril, 2016).

The term 'disclosure overload' became an issue in financial report that became one of the

topmost priorities of IASB or Board (Horngren, 2012). The reasons why there was no

reference to disclosures practices in financial reporting are:

The common format cannot be used for representing every kind of information.

Therefore, due to increase in volume of information and complex accounting

standards, use of different formats can be used to deliver a better understanding of the

financial reports (Mattessich, 2016).

The users of financial reports find disclosures overlapping and therefore, they do not

find useful decision making information.

There is a little knowledge of deciding a fact as material or immaterial. Thus,

disclosure overload increases if the information disclosed are of immaterial nature

(McLaney & Adril, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Solution 7:

Let us consider the annual report of 2017 of BHP Billiton Ltd. In case of this company, the

noncurrent assets show a value of $80,497 million.

This property, plant and equipment is measured at cost after eliminating accumulated

depreciation and impairment charges (Rosenfield, 2009). Cost here represents the fair value

of the transaction undertaken before to own the asset at the time the asset was bought and

includes the costs directly associated with the asset such as installation costs, conditions

necessary for bringing the asset into operation and the provisions related to future closure

costs. In a similar way, leased assets which are recorded as property, plant and equipment are

recorded at the lower of the fair value or the estimated value of the minimum lease payments

currently. The basis of depreciating the leased assets is same as that of company's owned

assets (Schroeder, 2014).

In notes to accounts, after the actual fair value is obtained, the company just after that

represents the historical cost in one row and accumulated depreciation and impairments in

another row. In the following case, the cost is $157, 666 millions and accumulated

depreciation and impairments is $77,169 million. Thus presenting the fair value in the

balance sheet for the true and fair view condition and representing the cost and depreciation

amount in the disclosures so as to provide complete information to the users of the financial

reports (Scott, 2014).

Let us consider the annual report of 2017 of BHP Billiton Ltd. In case of this company, the

noncurrent assets show a value of $80,497 million.

This property, plant and equipment is measured at cost after eliminating accumulated

depreciation and impairment charges (Rosenfield, 2009). Cost here represents the fair value

of the transaction undertaken before to own the asset at the time the asset was bought and

includes the costs directly associated with the asset such as installation costs, conditions

necessary for bringing the asset into operation and the provisions related to future closure

costs. In a similar way, leased assets which are recorded as property, plant and equipment are

recorded at the lower of the fair value or the estimated value of the minimum lease payments

currently. The basis of depreciating the leased assets is same as that of company's owned

assets (Schroeder, 2014).

In notes to accounts, after the actual fair value is obtained, the company just after that

represents the historical cost in one row and accumulated depreciation and impairments in

another row. In the following case, the cost is $157, 666 millions and accumulated

depreciation and impairments is $77,169 million. Thus presenting the fair value in the

balance sheet for the true and fair view condition and representing the cost and depreciation

amount in the disclosures so as to provide complete information to the users of the financial

reports (Scott, 2014).

CONCLUSION

The conclusion of the following assignment understands the changes incorporated in

conceptual framework by adopting practices from IASB framework. The AASB practices of

not considering disclosure requirements have to be eliminated completely. Already, the

AASB is working towards providing necessary guidance to incorporate sufficient disclosure

requirements that fulfills the conditions of an unqualified financial report. It would take time

but it would deliver the best possible results and would improve the quality and quantity of

financial reports.

The conclusion of the following assignment understands the changes incorporated in

conceptual framework by adopting practices from IASB framework. The AASB practices of

not considering disclosure requirements have to be eliminated completely. Already, the

AASB is working towards providing necessary guidance to incorporate sufficient disclosure

requirements that fulfills the conditions of an unqualified financial report. It would take time

but it would deliver the best possible results and would improve the quality and quantity of

financial reports.

Bibliography

Atkinson, A. A. (2012). Management accounting. Upper Saddle River, N.J.: Paerson.

Berry, L. E. (2009). Management accounting demystified. New York: McGraw-Hill.

Boyd, W. K. (2013). Cost Accounting For Dummies. Hoboken: Wiley.

Bragg, S. M. (2016). GAAP Guidebook. [S.I]: AccountingTools, Inc.

Dash, S. S. (2016). INSTITUTIONAL THEORY AND CSR. Retrieved from www.anzam.org:

https://www.anzam.org/wp-content/uploads/pdf-manager/2844_ANZAM-2016-407-

FILE001.PDF

Datar, M. S. (2015). Cost accounting. Boston: Pearson.

Datar, S. (2016). Horngren's Cost Accounting: A Managerial Emphasis. Hoboken: Wiley.

Donanldson, T. (2012). Ethical issues in business. New Jersey: Prentice Hall.

Edwards, M. (2014). Valuation for Financial Reporting: Fair Value Measurement in

Business Combinations, Early Stage Entities, Financial Instruments and Advanced

Topics . Hoboken: John Wiley & Sons Inc.

Girard, S. L. (2014). Business finance basics. Pompton Plains, NJ: Career Press.

Gow, I. D. (2016). Causal Inference in Accounting Research. Journal of Accounting Reseach

, 54 (2), 477-523.

Holtzman, M. (2013). Managerial Accounting For Dummies. Hoboken, NJ: Wiley.

Horngren, C. (2012). Cost accounting. Upper Saddle River, N.J.: Pearson/Prentice Hall.

Mattessich, R. (2016). Reality and accounting. [S.I.]: Routledge.

McLaney, E., & Adril, D. P. (2016). Accounting and Finance: An Introduction. United

Kingdom: Pearson.

Rosenfield, P. (2009). Contemporary Issues in Financial Reporting: A User-Oriented

Approach (Routledge New Works in Accounting History). [S.I.]: Wiley.

Atkinson, A. A. (2012). Management accounting. Upper Saddle River, N.J.: Paerson.

Berry, L. E. (2009). Management accounting demystified. New York: McGraw-Hill.

Boyd, W. K. (2013). Cost Accounting For Dummies. Hoboken: Wiley.

Bragg, S. M. (2016). GAAP Guidebook. [S.I]: AccountingTools, Inc.

Dash, S. S. (2016). INSTITUTIONAL THEORY AND CSR. Retrieved from www.anzam.org:

https://www.anzam.org/wp-content/uploads/pdf-manager/2844_ANZAM-2016-407-

FILE001.PDF

Datar, M. S. (2015). Cost accounting. Boston: Pearson.

Datar, S. (2016). Horngren's Cost Accounting: A Managerial Emphasis. Hoboken: Wiley.

Donanldson, T. (2012). Ethical issues in business. New Jersey: Prentice Hall.

Edwards, M. (2014). Valuation for Financial Reporting: Fair Value Measurement in

Business Combinations, Early Stage Entities, Financial Instruments and Advanced

Topics . Hoboken: John Wiley & Sons Inc.

Girard, S. L. (2014). Business finance basics. Pompton Plains, NJ: Career Press.

Gow, I. D. (2016). Causal Inference in Accounting Research. Journal of Accounting Reseach

, 54 (2), 477-523.

Holtzman, M. (2013). Managerial Accounting For Dummies. Hoboken, NJ: Wiley.

Horngren, C. (2012). Cost accounting. Upper Saddle River, N.J.: Pearson/Prentice Hall.

Mattessich, R. (2016). Reality and accounting. [S.I.]: Routledge.

McLaney, E., & Adril, D. P. (2016). Accounting and Finance: An Introduction. United

Kingdom: Pearson.

Rosenfield, P. (2009). Contemporary Issues in Financial Reporting: A User-Oriented

Approach (Routledge New Works in Accounting History). [S.I.]: Wiley.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Schroeder, R. G. (2014). Financial Accounting Theory and Analysis: Text and Cases.

Hoboken: John Wiley & Sons.

Scott, W. R. (2014). Financial Accounting Theory. Toronto: Pearson.

Hoboken: John Wiley & Sons.

Scott, W. R. (2014). Financial Accounting Theory. Toronto: Pearson.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.