AASB 138 and IAS 38: Technology Enterprises Ltd. Financial Report

VerifiedAdded on 2020/10/22

|10

|2561

|80

Report

AI Summary

This report examines Technology Enterprises Ltd.'s accounting practices concerning intangible assets, specifically focusing on a new battery charging design. It analyzes the application of AASB 138/IAS 38 to determine the appropriate treatment of the design within the financial statements. The report details the accounting procedures, including the allocation of research and development costs, and addresses the rules and restrictions imposed by AASB 138/IAS 38, and their impact on financial statement comparability. Furthermore, the report provides a response to the CEO's concerns regarding investor interpretation of the financial data, including the application of the efficient market hypothesis. Recommendations are offered to mitigate these concerns, emphasizing compliance with AASB 138 and the importance of detailed financial disclosures. The conclusion summarizes the findings and emphasizes the significance of accurate intangible asset accounting for the company's financial health and investor confidence.

Research Individual

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This report is mainly based upon Technology Enterprises Ltd. which is planning to

modify its design of charging batteries. AASB 138/ IAS 38 which are mainly related to treatment

of intangible assets are used to analyse nature of the design. It is vital for the company to fulfil

all the requirements of AASB in order to record new design in intangible assets.

Recommendation regarding complying with all the AASB standards is also provided to the

company so that it can mitigate its concerns regarding investor's interpretation of information

recorded in final accounts.

This report is mainly based upon Technology Enterprises Ltd. which is planning to

modify its design of charging batteries. AASB 138/ IAS 38 which are mainly related to treatment

of intangible assets are used to analyse nature of the design. It is vital for the company to fulfil

all the requirements of AASB in order to record new design in intangible assets.

Recommendation regarding complying with all the AASB standards is also provided to the

company so that it can mitigate its concerns regarding investor's interpretation of information

recorded in final accounts.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

The way in which project should be accounted in financial statement........................................1

TASK 2............................................................................................................................................3

To what extend might the rules or restrictions in AASB 138/IAS 38 reduce the comparability

of financial statements.................................................................................................................3

TASK 3............................................................................................................................................4

Response to the CEO and recommendation regarding concern about investor's interpretation. .4

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

The way in which project should be accounted in financial statement........................................1

TASK 2............................................................................................................................................3

To what extend might the rules or restrictions in AASB 138/IAS 38 reduce the comparability

of financial statements.................................................................................................................3

TASK 3............................................................................................................................................4

Response to the CEO and recommendation regarding concern about investor's interpretation. .4

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

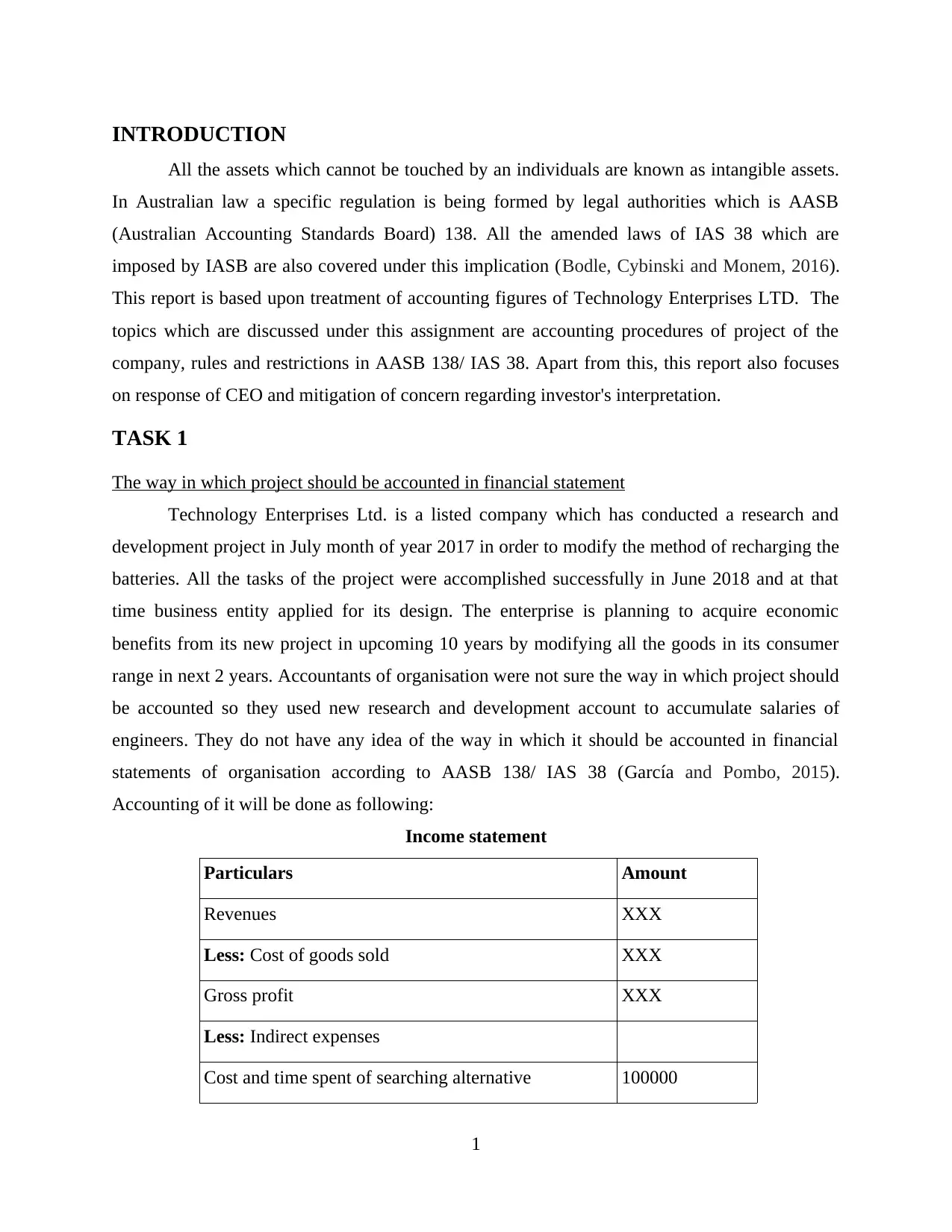

INTRODUCTION

All the assets which cannot be touched by an individuals are known as intangible assets.

In Australian law a specific regulation is being formed by legal authorities which is AASB

(Australian Accounting Standards Board) 138. All the amended laws of IAS 38 which are

imposed by IASB are also covered under this implication (Bodle, Cybinski and Monem, 2016).

This report is based upon treatment of accounting figures of Technology Enterprises LTD. The

topics which are discussed under this assignment are accounting procedures of project of the

company, rules and restrictions in AASB 138/ IAS 38. Apart from this, this report also focuses

on response of CEO and mitigation of concern regarding investor's interpretation.

TASK 1

The way in which project should be accounted in financial statement

Technology Enterprises Ltd. is a listed company which has conducted a research and

development project in July month of year 2017 in order to modify the method of recharging the

batteries. All the tasks of the project were accomplished successfully in June 2018 and at that

time business entity applied for its design. The enterprise is planning to acquire economic

benefits from its new project in upcoming 10 years by modifying all the goods in its consumer

range in next 2 years. Accountants of organisation were not sure the way in which project should

be accounted so they used new research and development account to accumulate salaries of

engineers. They do not have any idea of the way in which it should be accounted in financial

statements of organisation according to AASB 138/ IAS 38 (García and Pombo, 2015).

Accounting of it will be done as following:

Income statement

Particulars Amount

Revenues XXX

Less: Cost of goods sold XXX

Gross profit XXX

Less: Indirect expenses

Cost and time spent of searching alternative 100000

1

All the assets which cannot be touched by an individuals are known as intangible assets.

In Australian law a specific regulation is being formed by legal authorities which is AASB

(Australian Accounting Standards Board) 138. All the amended laws of IAS 38 which are

imposed by IASB are also covered under this implication (Bodle, Cybinski and Monem, 2016).

This report is based upon treatment of accounting figures of Technology Enterprises LTD. The

topics which are discussed under this assignment are accounting procedures of project of the

company, rules and restrictions in AASB 138/ IAS 38. Apart from this, this report also focuses

on response of CEO and mitigation of concern regarding investor's interpretation.

TASK 1

The way in which project should be accounted in financial statement

Technology Enterprises Ltd. is a listed company which has conducted a research and

development project in July month of year 2017 in order to modify the method of recharging the

batteries. All the tasks of the project were accomplished successfully in June 2018 and at that

time business entity applied for its design. The enterprise is planning to acquire economic

benefits from its new project in upcoming 10 years by modifying all the goods in its consumer

range in next 2 years. Accountants of organisation were not sure the way in which project should

be accounted so they used new research and development account to accumulate salaries of

engineers. They do not have any idea of the way in which it should be accounted in financial

statements of organisation according to AASB 138/ IAS 38 (García and Pombo, 2015).

Accounting of it will be done as following:

Income statement

Particulars Amount

Revenues XXX

Less: Cost of goods sold XXX

Gross profit XXX

Less: Indirect expenses

Cost and time spent of searching alternative 100000

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

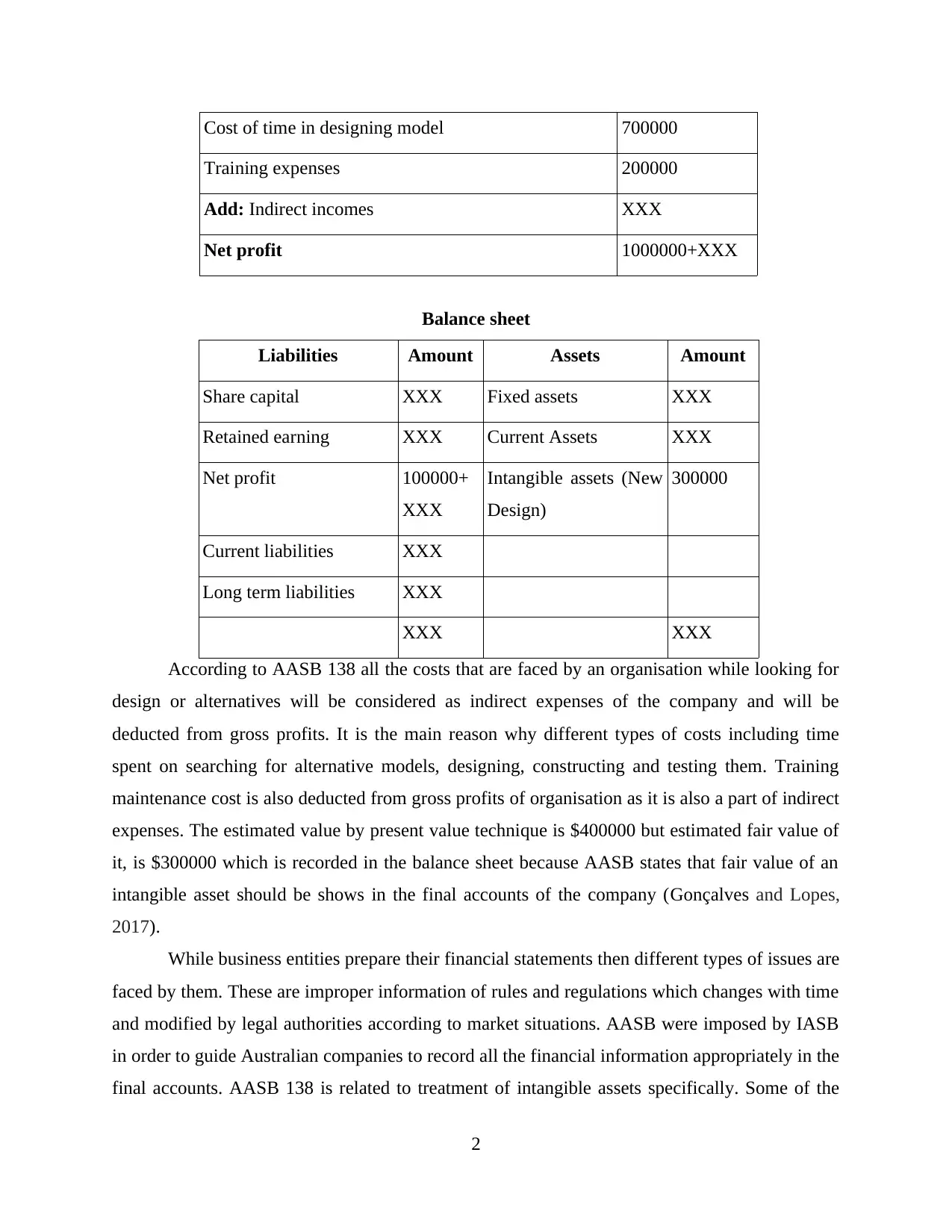

Cost of time in designing model 700000

Training expenses 200000

Add: Indirect incomes XXX

Net profit 1000000+XXX

Balance sheet

Liabilities Amount Assets Amount

Share capital XXX Fixed assets XXX

Retained earning XXX Current Assets XXX

Net profit 100000+

XXX

Intangible assets (New

Design)

300000

Current liabilities XXX

Long term liabilities XXX

XXX XXX

According to AASB 138 all the costs that are faced by an organisation while looking for

design or alternatives will be considered as indirect expenses of the company and will be

deducted from gross profits. It is the main reason why different types of costs including time

spent on searching for alternative models, designing, constructing and testing them. Training

maintenance cost is also deducted from gross profits of organisation as it is also a part of indirect

expenses. The estimated value by present value technique is $400000 but estimated fair value of

it, is $300000 which is recorded in the balance sheet because AASB states that fair value of an

intangible asset should be shows in the final accounts of the company (Gonçalves and Lopes,

2017).

While business entities prepare their financial statements then different types of issues are

faced by them. These are improper information of rules and regulations which changes with time

and modified by legal authorities according to market situations. AASB were imposed by IASB

in order to guide Australian companies to record all the financial information appropriately in the

final accounts. AASB 138 is related to treatment of intangible assets specifically. Some of the

2

Training expenses 200000

Add: Indirect incomes XXX

Net profit 1000000+XXX

Balance sheet

Liabilities Amount Assets Amount

Share capital XXX Fixed assets XXX

Retained earning XXX Current Assets XXX

Net profit 100000+

XXX

Intangible assets (New

Design)

300000

Current liabilities XXX

Long term liabilities XXX

XXX XXX

According to AASB 138 all the costs that are faced by an organisation while looking for

design or alternatives will be considered as indirect expenses of the company and will be

deducted from gross profits. It is the main reason why different types of costs including time

spent on searching for alternative models, designing, constructing and testing them. Training

maintenance cost is also deducted from gross profits of organisation as it is also a part of indirect

expenses. The estimated value by present value technique is $400000 but estimated fair value of

it, is $300000 which is recorded in the balance sheet because AASB states that fair value of an

intangible asset should be shows in the final accounts of the company (Gonçalves and Lopes,

2017).

While business entities prepare their financial statements then different types of issues are

faced by them. These are improper information of rules and regulations which changes with time

and modified by legal authorities according to market situations. AASB were imposed by IASB

in order to guide Australian companies to record all the financial information appropriately in the

final accounts. AASB 138 is related to treatment of intangible assets specifically. Some of the

2

requirements should be met to consider an asset intangible in nature (Requirements of AASB 138,

2019). All of them are as follows:

If an organisation is willing to treat an asset as an intangible one then it should be

distinct. On the other hand the asset should arise from sort of contract.

If the asset can be measured in monetary terms then it is not considered as intangible one

because business entity cannot purchase it from any other place.

The asset should not have any tangible feature which means it should not be touched by

individuals.

Sufficient control is also required to declare an asset as intangible one. For example, if an

organisation takes all the decisions regarding uses of logo or design then it has control

over the asset which can be treated as intangible.

If the asset is sold in future and economic benefits are received by company then it fulfils

the requirement of AASB.

Justification: All the above described requirements are fulfilled by Technology

Enterprises Ltd. for new design of charging the batteries which are used in its projects. Present

value of the design is $400000 and fair value if $300000 and if it is sold by company then

economic benefits of $100000 could be received by it. Organisation have sufficient control over

the asset and when it will be sold then potential buyer can modify the design according to their

requirements or needs (Grüber, 2014). It is the main reason why new design is treated as an

tangible assets.

TASK 2

To what extend might the rules or restrictions in AASB 138/IAS 38 reduce the comparability of

financial statements

AASB 138 stands for The Australian Accounting Standards Board which is commenced

on 15 July 2004, under 334 amendment of Corporation Act 2001. The main objective of this

standard is to dictate accounting treatment for an entity related to its intangible assets, which are

not dealt with specifically as per another Standard. Therefore, it assists a business entity for

recognising their intangible assets only in that condition, under which specified criteria are met.

It also specifies the organisations in way to measure carrying amount of such assets as well as

how to disclose the same. This law also covered amendments made by IASB in IAS 38. As per

3

2019). All of them are as follows:

If an organisation is willing to treat an asset as an intangible one then it should be

distinct. On the other hand the asset should arise from sort of contract.

If the asset can be measured in monetary terms then it is not considered as intangible one

because business entity cannot purchase it from any other place.

The asset should not have any tangible feature which means it should not be touched by

individuals.

Sufficient control is also required to declare an asset as intangible one. For example, if an

organisation takes all the decisions regarding uses of logo or design then it has control

over the asset which can be treated as intangible.

If the asset is sold in future and economic benefits are received by company then it fulfils

the requirement of AASB.

Justification: All the above described requirements are fulfilled by Technology

Enterprises Ltd. for new design of charging the batteries which are used in its projects. Present

value of the design is $400000 and fair value if $300000 and if it is sold by company then

economic benefits of $100000 could be received by it. Organisation have sufficient control over

the asset and when it will be sold then potential buyer can modify the design according to their

requirements or needs (Grüber, 2014). It is the main reason why new design is treated as an

tangible assets.

TASK 2

To what extend might the rules or restrictions in AASB 138/IAS 38 reduce the comparability of

financial statements

AASB 138 stands for The Australian Accounting Standards Board which is commenced

on 15 July 2004, under 334 amendment of Corporation Act 2001. The main objective of this

standard is to dictate accounting treatment for an entity related to its intangible assets, which are

not dealt with specifically as per another Standard. Therefore, it assists a business entity for

recognising their intangible assets only in that condition, under which specified criteria are met.

It also specifies the organisations in way to measure carrying amount of such assets as well as

how to disclose the same. This law also covered amendments made by IASB in IAS 38. As per

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this law, those assets of business are considered as intangible which needs to be identifiable,

must be non-monetary and more. It includes patents, licences, franchises, software, copyrights

etc. Therefore, if these assets are not recognised by corporations then the same have to be

expensed. This may affect bottom line of business and taxable profit as well.

In this regard, it is essential for entities to concern that when they organise their finance

then they must categorise the assets, which reflect value of business. For this purpose, they can

hire legal authorities at workplace who may help in categorising the assets as tangible and

intangible. Along with this, any items which are cannot classified in these two categorise can be

put as 'goodwill', so, it is not necessary to recognise them within financial statements. Hereby, it

has been evaluated that this AABS standards has covered entire ways in which entities have to

report their finances as per compliance with specifically standards, according to Corporations

Act (Hu, Percy and Yao, 2015). By breaching these requirements, business may be prosecuted,

therefore, organisations must ensure that their corporations are compliant with such give

financial reporting obligations. In context with financial statement, this standard does not apply

to:

Intangible assets which are held by an organisation for sale within an ordinary course of

business, as per AASB 111 Construction Contracts and AASB 111 Inventories

This standard is not applicable for deferred tax assets according to AASB 112 Income

Taxes

Leases which are included as scope of AASB 117 Leases

Assets which are arising from worker benefits as mentioned in AASB 119 Employee

Benefits

Financial assets as described in AASB 132.

Goodwill acquired in a business combination according to AASB 3 Business

Combinations

It is essential for organisation to apply AASB 138 Standard with their annual reporting

periods which are begun before 1 January 2009 and after 1 January 2005. While in context with

not-for-profit entities, this law can apply to annual reporting periods which begins on or after 1

January 2014. This would incorporates the reliable and relevant amendments that are contained

in other Standards of AASB made on and after 18 December 2012. Other than this, in context

4

must be non-monetary and more. It includes patents, licences, franchises, software, copyrights

etc. Therefore, if these assets are not recognised by corporations then the same have to be

expensed. This may affect bottom line of business and taxable profit as well.

In this regard, it is essential for entities to concern that when they organise their finance

then they must categorise the assets, which reflect value of business. For this purpose, they can

hire legal authorities at workplace who may help in categorising the assets as tangible and

intangible. Along with this, any items which are cannot classified in these two categorise can be

put as 'goodwill', so, it is not necessary to recognise them within financial statements. Hereby, it

has been evaluated that this AABS standards has covered entire ways in which entities have to

report their finances as per compliance with specifically standards, according to Corporations

Act (Hu, Percy and Yao, 2015). By breaching these requirements, business may be prosecuted,

therefore, organisations must ensure that their corporations are compliant with such give

financial reporting obligations. In context with financial statement, this standard does not apply

to:

Intangible assets which are held by an organisation for sale within an ordinary course of

business, as per AASB 111 Construction Contracts and AASB 111 Inventories

This standard is not applicable for deferred tax assets according to AASB 112 Income

Taxes

Leases which are included as scope of AASB 117 Leases

Assets which are arising from worker benefits as mentioned in AASB 119 Employee

Benefits

Financial assets as described in AASB 132.

Goodwill acquired in a business combination according to AASB 3 Business

Combinations

It is essential for organisation to apply AASB 138 Standard with their annual reporting

periods which are begun before 1 January 2009 and after 1 January 2005. While in context with

not-for-profit entities, this law can apply to annual reporting periods which begins on or after 1

January 2014. This would incorporates the reliable and relevant amendments that are contained

in other Standards of AASB made on and after 18 December 2012. Other than this, in context

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

with profit entities who are complying and amending with AASB 138, are also simultaneously

comes under compliance with IAS 38 also as amended (Ji and Lu, 2014).

TASK 3

Response to the CEO and recommendation regarding concern about investor's interpretation

According to CEO of organisation can show the asset at the value of $400000 in balance

sheet and add $300000 to the profits. AASB 138 states that only fair value of an intangible asset

should be recorded in the books of accounting because it can help to calculate economic benefits

which will be received by organisation in future. It is very important for organisations to measure

all the assets initially after recognising their nature according to requirements of AASB 138/ IAS

38. This law of IASB requires that business entities should disclose detained information of each

class of its intangible asset which helps to distinguish between these and other assets. If company

is not able to provide detailed information regarding an asset then it will be expensed for

organisation (AASB 138, 2019). It can leave negative impact upon profitability and taxation. It is

being suggested to the CEO that amount of $300000 for the design which is its fair value should

be recorded in balance sheet under intangible asset head. The way in which business entities such

as Technology Enterprises Ltd. classify their assets, affect value of whole business. Including

appropriate data in financial statements assures that value of the company will be increased in

future.

Efficient market hypothesis: It is an investment theory which helps to depict

information regarding share prices of an organisation. It helps investors to determine possible

returns which could be acquired by them on their money which will be invested by them in a

company. It suggests that investors can't generate returns above average of the market on

continual basis.

This theory can guide investors of Technology Enterprises Ltd. to analyse the situation in

which they will not be able to acquire higher returns on their investments on consistent basis.

With the help of it they can withdraw their money in order to ignore situation of losses which

may take place in future (Malone, Tarca and Wee, 2016).

Recommendation: CEO of Technology Enterprises Ltd. is worry about the way in which

organisation can mitigate its concerns regarding investor's interpretation of data accounted in

5

comes under compliance with IAS 38 also as amended (Ji and Lu, 2014).

TASK 3

Response to the CEO and recommendation regarding concern about investor's interpretation

According to CEO of organisation can show the asset at the value of $400000 in balance

sheet and add $300000 to the profits. AASB 138 states that only fair value of an intangible asset

should be recorded in the books of accounting because it can help to calculate economic benefits

which will be received by organisation in future. It is very important for organisations to measure

all the assets initially after recognising their nature according to requirements of AASB 138/ IAS

38. This law of IASB requires that business entities should disclose detained information of each

class of its intangible asset which helps to distinguish between these and other assets. If company

is not able to provide detailed information regarding an asset then it will be expensed for

organisation (AASB 138, 2019). It can leave negative impact upon profitability and taxation. It is

being suggested to the CEO that amount of $300000 for the design which is its fair value should

be recorded in balance sheet under intangible asset head. The way in which business entities such

as Technology Enterprises Ltd. classify their assets, affect value of whole business. Including

appropriate data in financial statements assures that value of the company will be increased in

future.

Efficient market hypothesis: It is an investment theory which helps to depict

information regarding share prices of an organisation. It helps investors to determine possible

returns which could be acquired by them on their money which will be invested by them in a

company. It suggests that investors can't generate returns above average of the market on

continual basis.

This theory can guide investors of Technology Enterprises Ltd. to analyse the situation in

which they will not be able to acquire higher returns on their investments on consistent basis.

With the help of it they can withdraw their money in order to ignore situation of losses which

may take place in future (Malone, Tarca and Wee, 2016).

Recommendation: CEO of Technology Enterprises Ltd. is worry about the way in which

organisation can mitigate its concerns regarding investor's interpretation of data accounted in

5

financial statements of company. Following recommendations are provided to CEO in order to

minimise it:

Efficient market hypothesis can be formulated by the company which can help it to

provide appropriate information regarding share price of the company and the level when

they will not be able to acquire consistent returns.

It is vital for Technology Enterprises Ltd. to comply with all the essential requirements of

AASB 138 which can help it to meet legal implications.

Detailed information in the financial statements can help investors to evaluate actual

position of company which can guide them to formulate strategic decisions regarding

making investment or withdrawing their money from organisation (Pacter, 2014).

CONCLUSION

From the above project report it has been concluded that various types of rules and

regulations are imposed by legal authorities which are required to be complied by organisations

in order to operate business in appropriate manner. One of them is AASB 138 which also covers

amendments made by IASB in IAS 38. It is focused with treatment of intangible assets which are

hold by companies. It guides them to fulfil requirements which are required to account an asset

as an intangible one. If enterprise is not able to adhere with them then it is not allowed to record

a asset under intangible asset head.

6

minimise it:

Efficient market hypothesis can be formulated by the company which can help it to

provide appropriate information regarding share price of the company and the level when

they will not be able to acquire consistent returns.

It is vital for Technology Enterprises Ltd. to comply with all the essential requirements of

AASB 138 which can help it to meet legal implications.

Detailed information in the financial statements can help investors to evaluate actual

position of company which can guide them to formulate strategic decisions regarding

making investment or withdrawing their money from organisation (Pacter, 2014).

CONCLUSION

From the above project report it has been concluded that various types of rules and

regulations are imposed by legal authorities which are required to be complied by organisations

in order to operate business in appropriate manner. One of them is AASB 138 which also covers

amendments made by IASB in IAS 38. It is focused with treatment of intangible assets which are

hold by companies. It guides them to fulfil requirements which are required to account an asset

as an intangible one. If enterprise is not able to adhere with them then it is not allowed to record

a asset under intangible asset head.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Bodle, K. A., Cybinski, P. J. and Monem, R., 2016. Effect of IFRS adoption on financial

reporting quality: Evidence from bankruptcy prediction. Accounting Research Journal.

29(3). pp.292-312.

García, E. R. and Pombo, L. C., 2015. Valuación de Activos Intangibles de Propiedad

Intelectual: Fundamentos económicos, jurídicos, financieros y contables. U. Externado

de Colombia.

Gonçalves, R. and Lopes, P. T., 2017. Accounting for Biological Assets. Routledge.

Grüber, S., 2014. Intangible values in financial accounting and reporting: an analysis from the

perspective of financial analysts. Springer.

Hu, F., Percy, M. and Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control. 13(1). pp.930-939.

Ji, X. D. and Lu, W., 2014. The value relevance and reliability of intangible assets: Evidence

from Australia before and after adopting IFRS. Asian Review of Accounting. 22(3).

pp.182-216.

Malone, L., Tarca, A. and Wee, M., 2016. IFRS non‐GAAP earnings disclosures and fair value

measurement. Accounting & Finance. 56(1). pp.59-97.

Pacter, P., 2014. IFRS as global standards: A pocket guide. London: IFRS Foundation.

Online

AASB 138. 2019. [Online]. Available through:

<https://legalvision.com.au/aasb-138-intangible-assets-summary-for-businesses/>

Requirements of AASB 138. 2019. [Online]. Available through:

<https://lawpath.com.au/blog/aasb-138-intangible-assets>

7

Books and Journals:

Bodle, K. A., Cybinski, P. J. and Monem, R., 2016. Effect of IFRS adoption on financial

reporting quality: Evidence from bankruptcy prediction. Accounting Research Journal.

29(3). pp.292-312.

García, E. R. and Pombo, L. C., 2015. Valuación de Activos Intangibles de Propiedad

Intelectual: Fundamentos económicos, jurídicos, financieros y contables. U. Externado

de Colombia.

Gonçalves, R. and Lopes, P. T., 2017. Accounting for Biological Assets. Routledge.

Grüber, S., 2014. Intangible values in financial accounting and reporting: an analysis from the

perspective of financial analysts. Springer.

Hu, F., Percy, M. and Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control. 13(1). pp.930-939.

Ji, X. D. and Lu, W., 2014. The value relevance and reliability of intangible assets: Evidence

from Australia before and after adopting IFRS. Asian Review of Accounting. 22(3).

pp.182-216.

Malone, L., Tarca, A. and Wee, M., 2016. IFRS non‐GAAP earnings disclosures and fair value

measurement. Accounting & Finance. 56(1). pp.59-97.

Pacter, P., 2014. IFRS as global standards: A pocket guide. London: IFRS Foundation.

Online

AASB 138. 2019. [Online]. Available through:

<https://legalvision.com.au/aasb-138-intangible-assets-summary-for-businesses/>

Requirements of AASB 138. 2019. [Online]. Available through:

<https://lawpath.com.au/blog/aasb-138-intangible-assets>

7

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.