ABC Ltd Case Study

Added on 2023-01-20

7 Pages1676 Words39 Views

Running Head: ABC LTD CASE STUDY

1

BUSINESS ANALYSIS CASE STUDY (SL- CONTROL COMPANY)

Name of Student:

Name of Institution:

Date:

1

BUSINESS ANALYSIS CASE STUDY (SL- CONTROL COMPANY)

Name of Student:

Name of Institution:

Date:

ABC LTD CASE STUDY

2

Purpose of the Report

The company called ABC Ltd requires viable production recommendations based on

expert analysis. The recommendations that are required are based on the required number of

balls they should manufacture in order to get optimal profits. Therefore, the analysis involved is

meant to ensure that ABC will obtain maximum net profits from the manufacture and sell of

footballs and basketballs.

The decision to obtain the optimal number of balls that will ensure that the company

gains maximum net profit will be arrived at based on the constraints that the company has. The

constraints include: The capacity of the production, the material costs, the labor costs and the

time available for manufacturing. Constrains are allocated based on the decision variables. The

decision variables are the number of footballs and the number of basketballs that the company

manufactures. Therefore, the report seeks to help ABC Ltd. Improve their resource allocation

processes and decisions.

Description of the Problem

The problem that is being solved in this report is a case study of a production company.

The company is in a dilemma of the optimal units to produce in order get a maximum net profit.

The sporting company has a set of constraints and decision variables that should be used in

making the decision. The description of the scenario is provided in the paragraph that follows.

Methodology

Method that was used to solve the problem is the linear programming method. Linear

programming is a mathematical technique of maximizing variables based on certain constrains.

The maximization is meant to aid decision-making process (Mahmoudi, et al., 2019). The

2

Purpose of the Report

The company called ABC Ltd requires viable production recommendations based on

expert analysis. The recommendations that are required are based on the required number of

balls they should manufacture in order to get optimal profits. Therefore, the analysis involved is

meant to ensure that ABC will obtain maximum net profits from the manufacture and sell of

footballs and basketballs.

The decision to obtain the optimal number of balls that will ensure that the company

gains maximum net profit will be arrived at based on the constraints that the company has. The

constraints include: The capacity of the production, the material costs, the labor costs and the

time available for manufacturing. Constrains are allocated based on the decision variables. The

decision variables are the number of footballs and the number of basketballs that the company

manufactures. Therefore, the report seeks to help ABC Ltd. Improve their resource allocation

processes and decisions.

Description of the Problem

The problem that is being solved in this report is a case study of a production company.

The company is in a dilemma of the optimal units to produce in order get a maximum net profit.

The sporting company has a set of constraints and decision variables that should be used in

making the decision. The description of the scenario is provided in the paragraph that follows.

Methodology

Method that was used to solve the problem is the linear programming method. Linear

programming is a mathematical technique of maximizing variables based on certain constrains.

The maximization is meant to aid decision-making process (Mahmoudi, et al., 2019). The

ABC LTD CASE STUDY

3

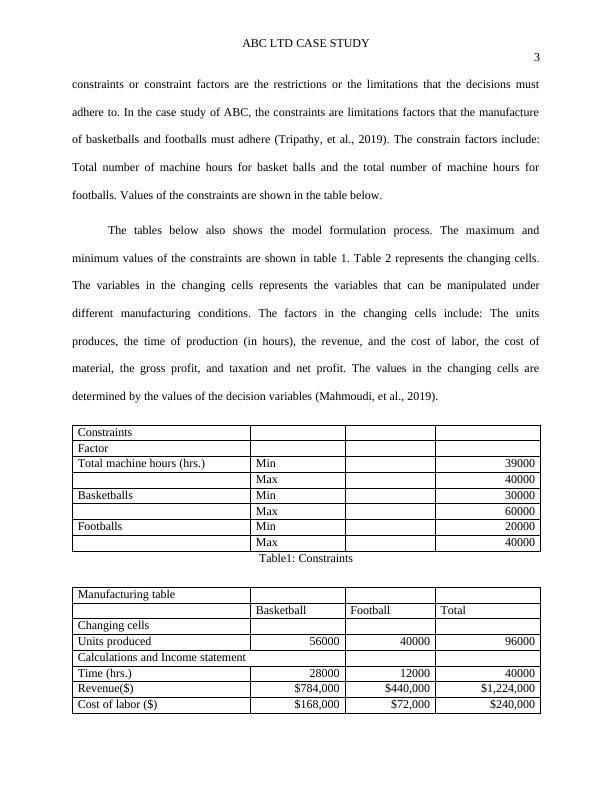

constraints or constraint factors are the restrictions or the limitations that the decisions must

adhere to. In the case study of ABC, the constraints are limitations factors that the manufacture

of basketballs and footballs must adhere (Tripathy, et al., 2019). The constrain factors include:

Total number of machine hours for basket balls and the total number of machine hours for

footballs. Values of the constraints are shown in the table below.

The tables below also shows the model formulation process. The maximum and

minimum values of the constraints are shown in table 1. Table 2 represents the changing cells.

The variables in the changing cells represents the variables that can be manipulated under

different manufacturing conditions. The factors in the changing cells include: The units

produces, the time of production (in hours), the revenue, and the cost of labor, the cost of

material, the gross profit, and taxation and net profit. The values in the changing cells are

determined by the values of the decision variables (Mahmoudi, et al., 2019).

Constraints

Factor

Total machine hours (hrs.) Min 39000

Max 40000

Basketballs Min 30000

Max 60000

Footballs Min 20000

Max 40000

Table1: Constraints

Manufacturing table

Basketball Football Total

Changing cells

Units produced 56000 40000 96000

Calculations and Income statement

Time (hrs.) 28000 12000 40000

Revenue($) $784,000 $440,000 $1,224,000

Cost of labor ($) $168,000 $72,000 $240,000

3

constraints or constraint factors are the restrictions or the limitations that the decisions must

adhere to. In the case study of ABC, the constraints are limitations factors that the manufacture

of basketballs and footballs must adhere (Tripathy, et al., 2019). The constrain factors include:

Total number of machine hours for basket balls and the total number of machine hours for

footballs. Values of the constraints are shown in the table below.

The tables below also shows the model formulation process. The maximum and

minimum values of the constraints are shown in table 1. Table 2 represents the changing cells.

The variables in the changing cells represents the variables that can be manipulated under

different manufacturing conditions. The factors in the changing cells include: The units

produces, the time of production (in hours), the revenue, and the cost of labor, the cost of

material, the gross profit, and taxation and net profit. The values in the changing cells are

determined by the values of the decision variables (Mahmoudi, et al., 2019).

Constraints

Factor

Total machine hours (hrs.) Min 39000

Max 40000

Basketballs Min 30000

Max 60000

Footballs Min 20000

Max 40000

Table1: Constraints

Manufacturing table

Basketball Football Total

Changing cells

Units produced 56000 40000 96000

Calculations and Income statement

Time (hrs.) 28000 12000 40000

Revenue($) $784,000 $440,000 $1,224,000

Cost of labor ($) $168,000 $72,000 $240,000

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Business Decision Analysis - Case Studylg...

|8

|888

|333

Report on Business Decision Making in Organizationlg...

|6

|1896

|63

Supply Chain and Design Analysis Case Studylg...

|15

|792

|64