Semester 1 ACT202 Assignment: Absorption vs. Activity Based Costing

VerifiedAdded on 2022/11/14

|15

|2569

|153

Homework Assignment

AI Summary

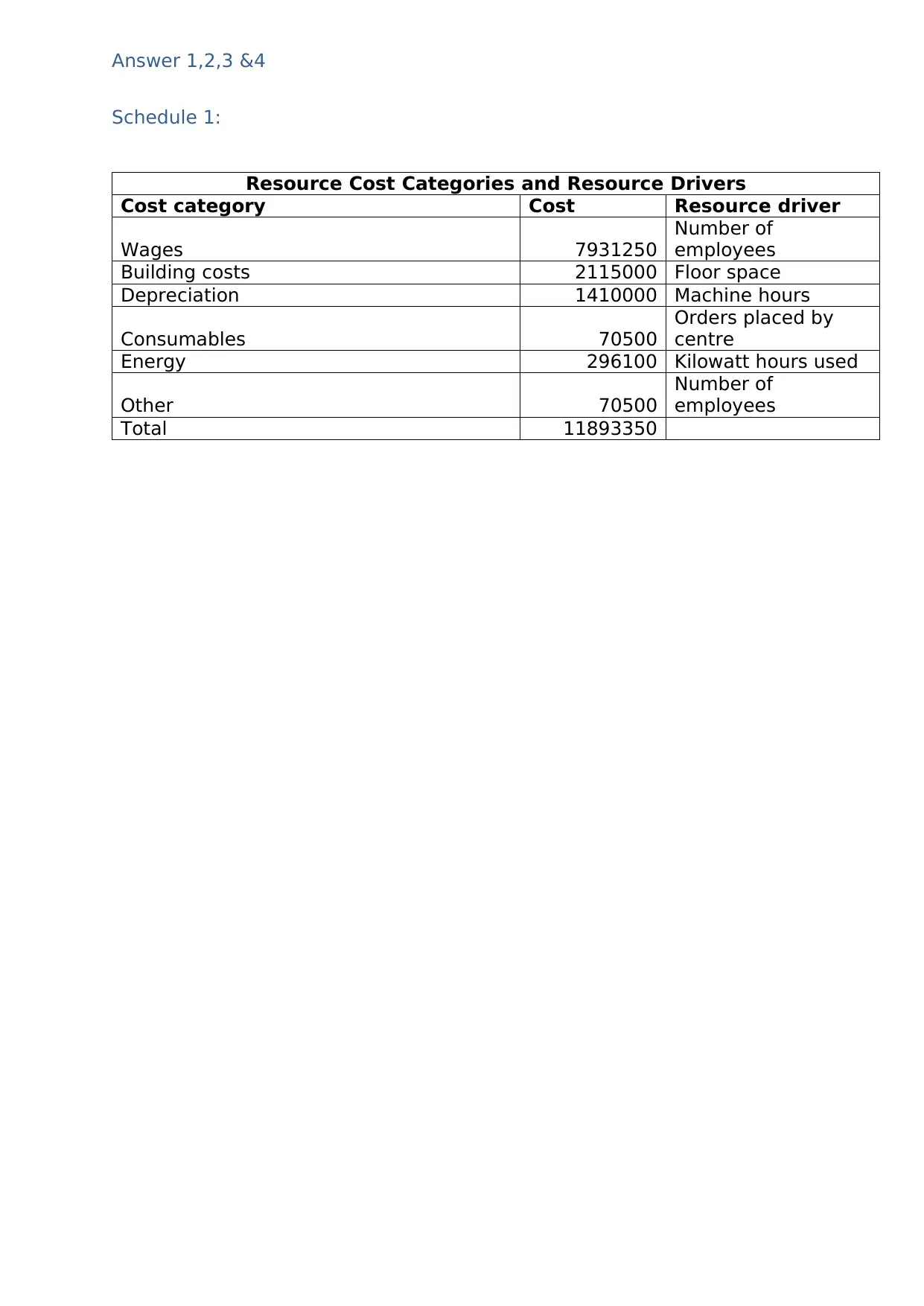

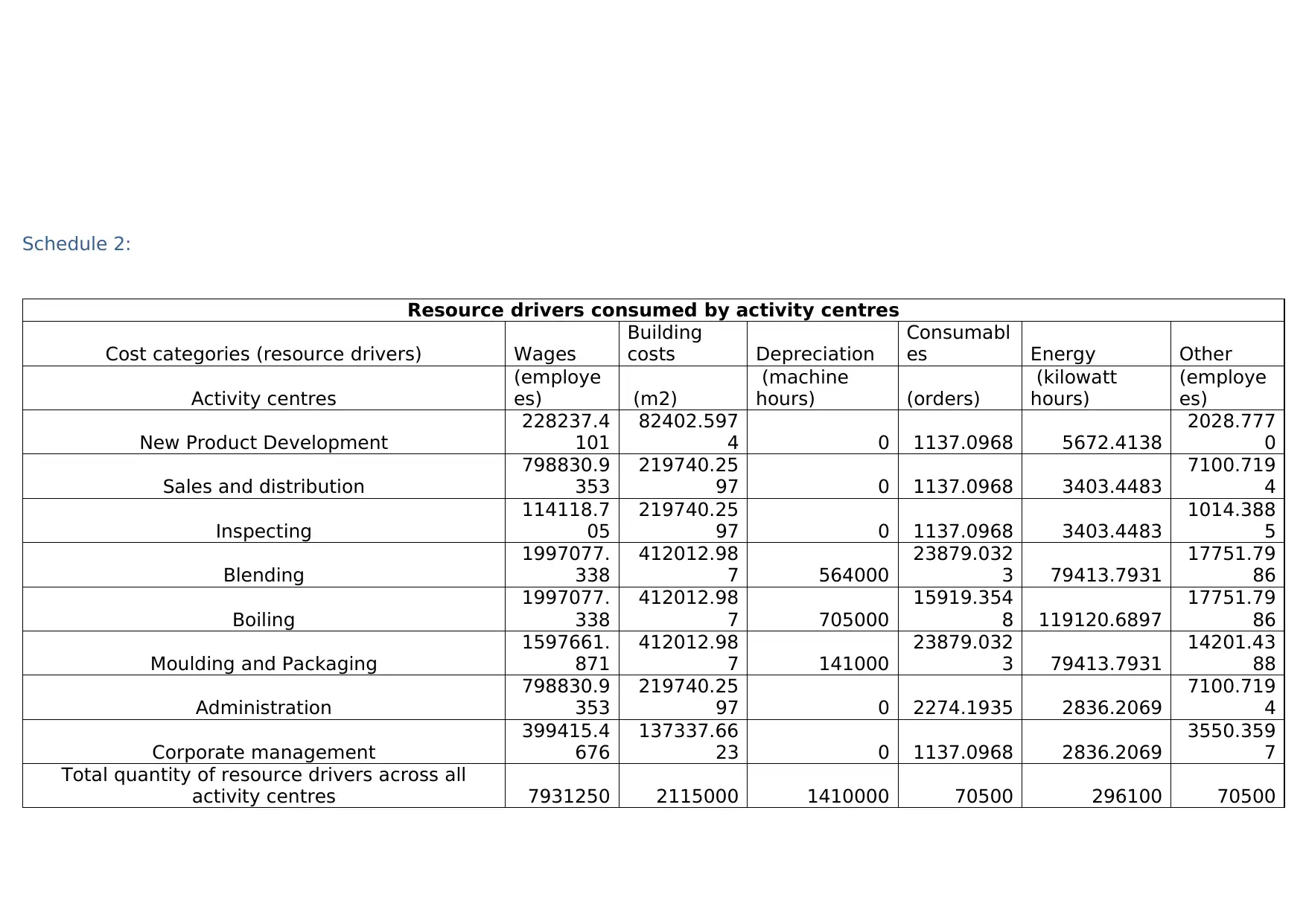

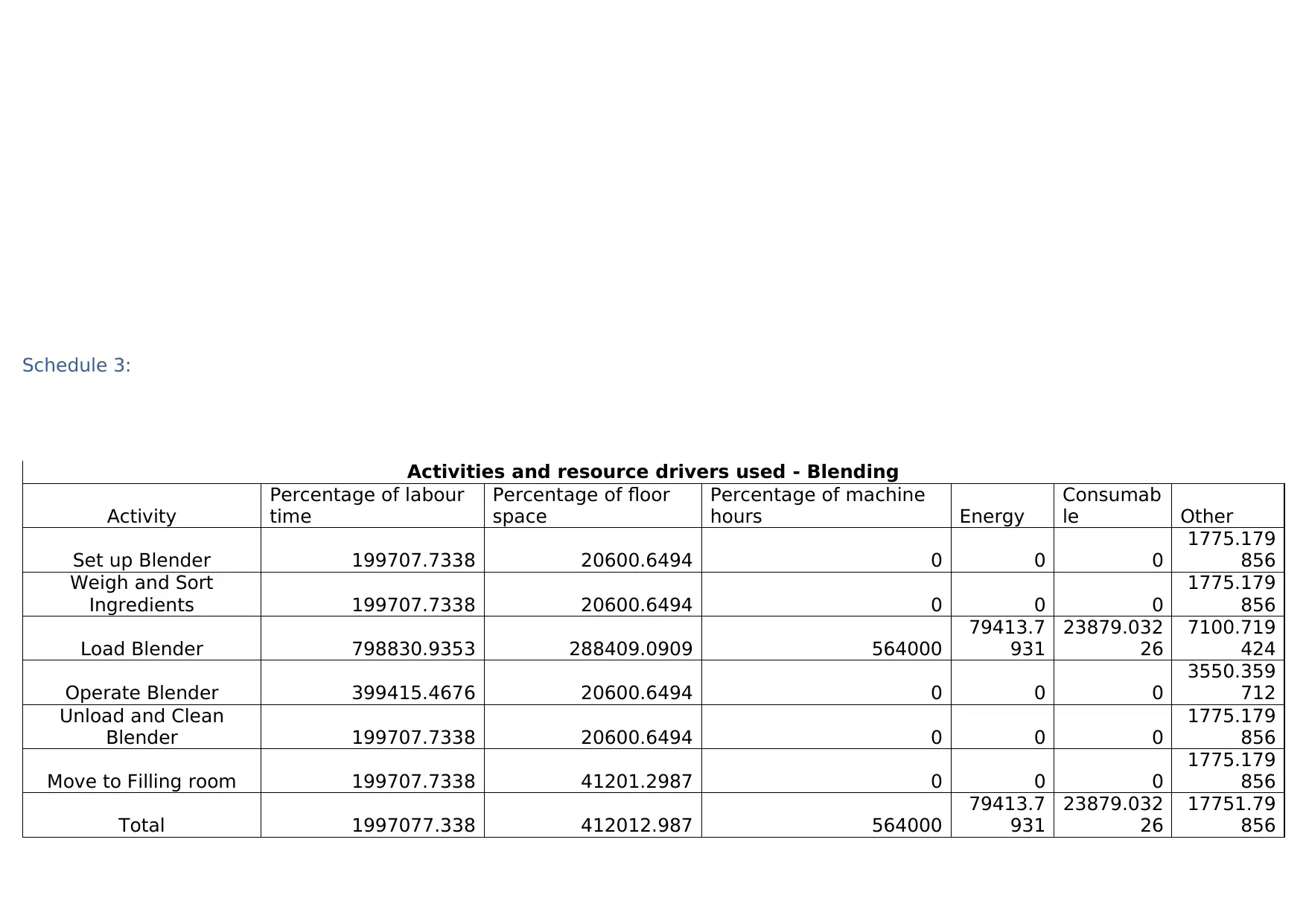

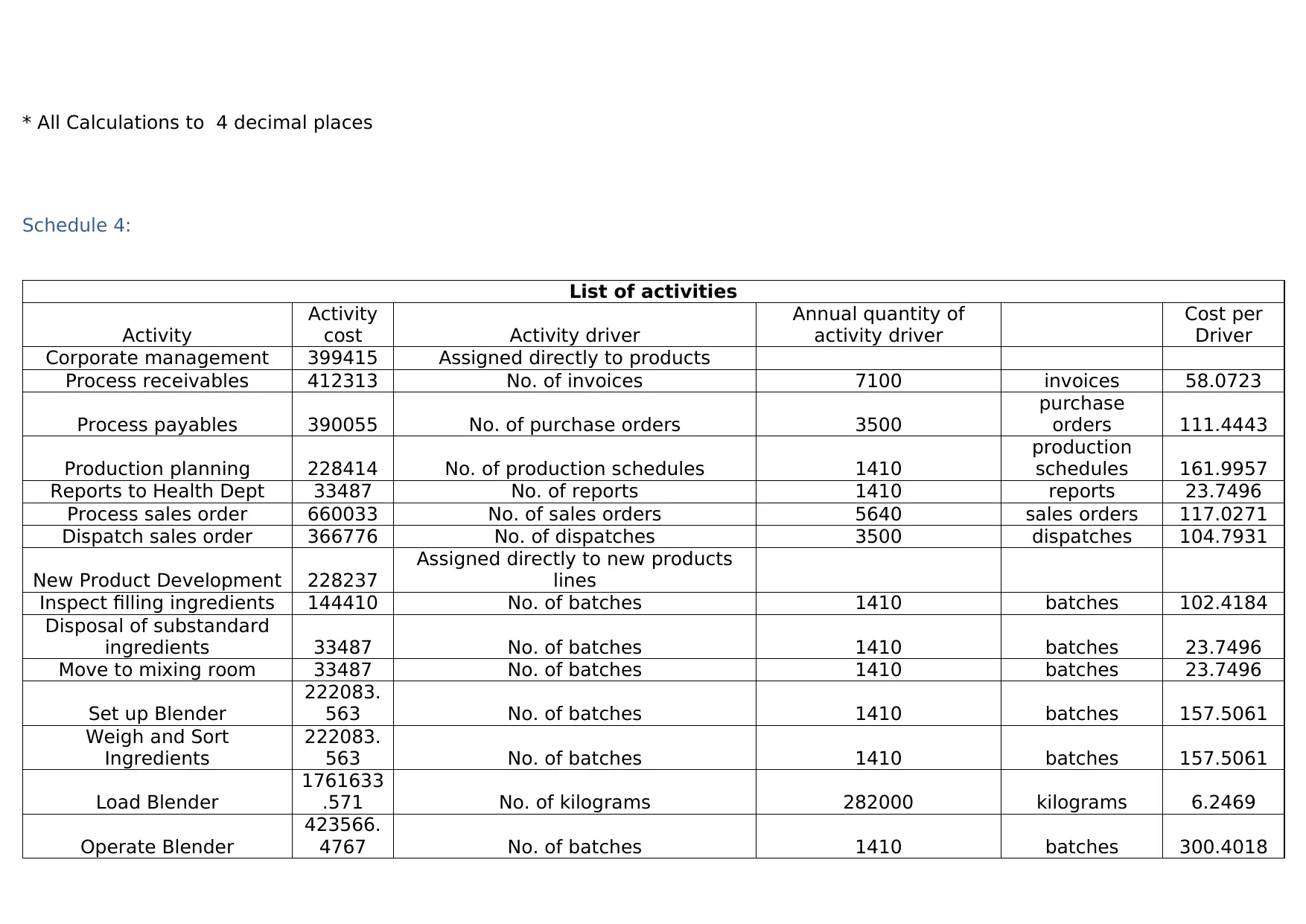

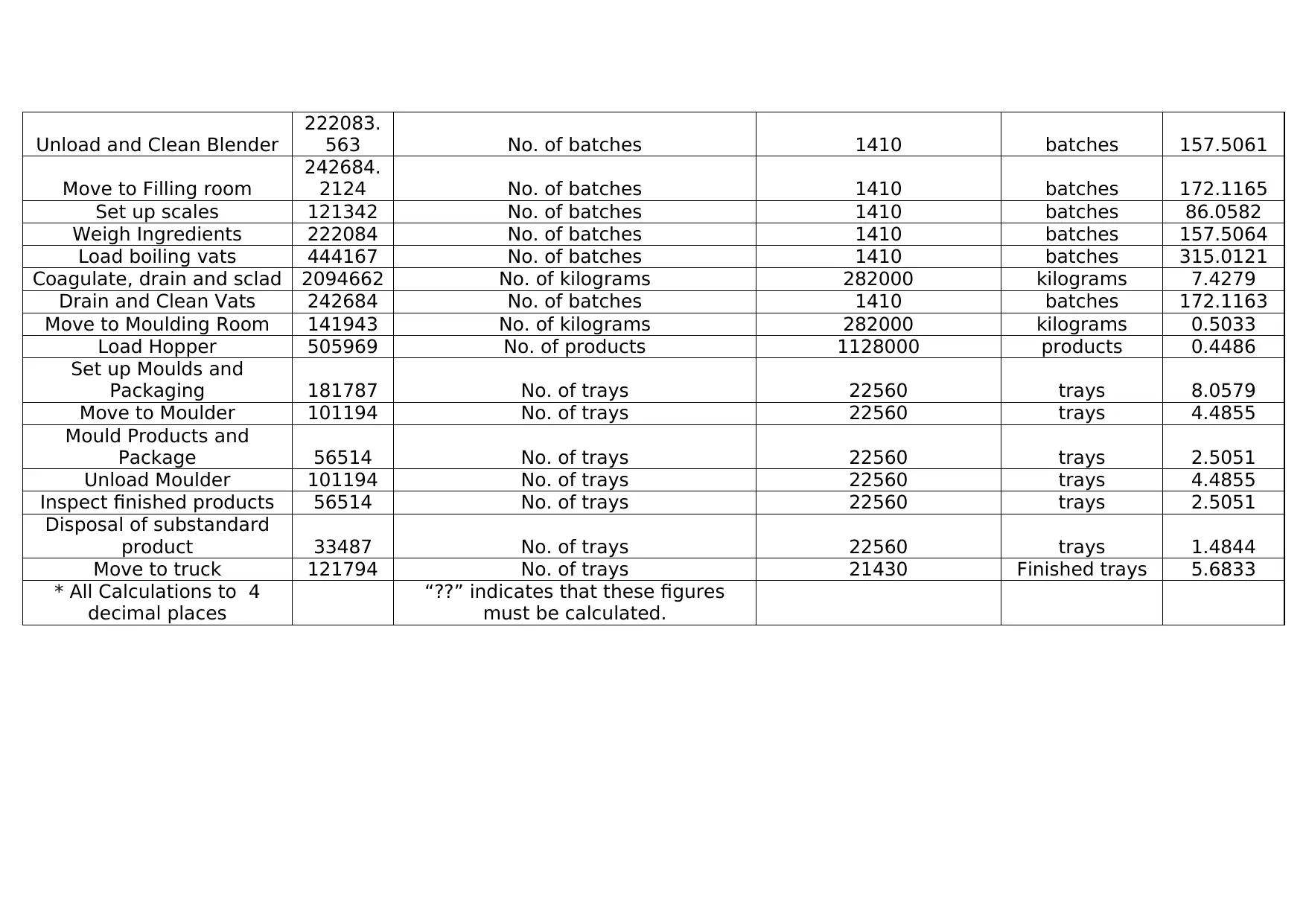

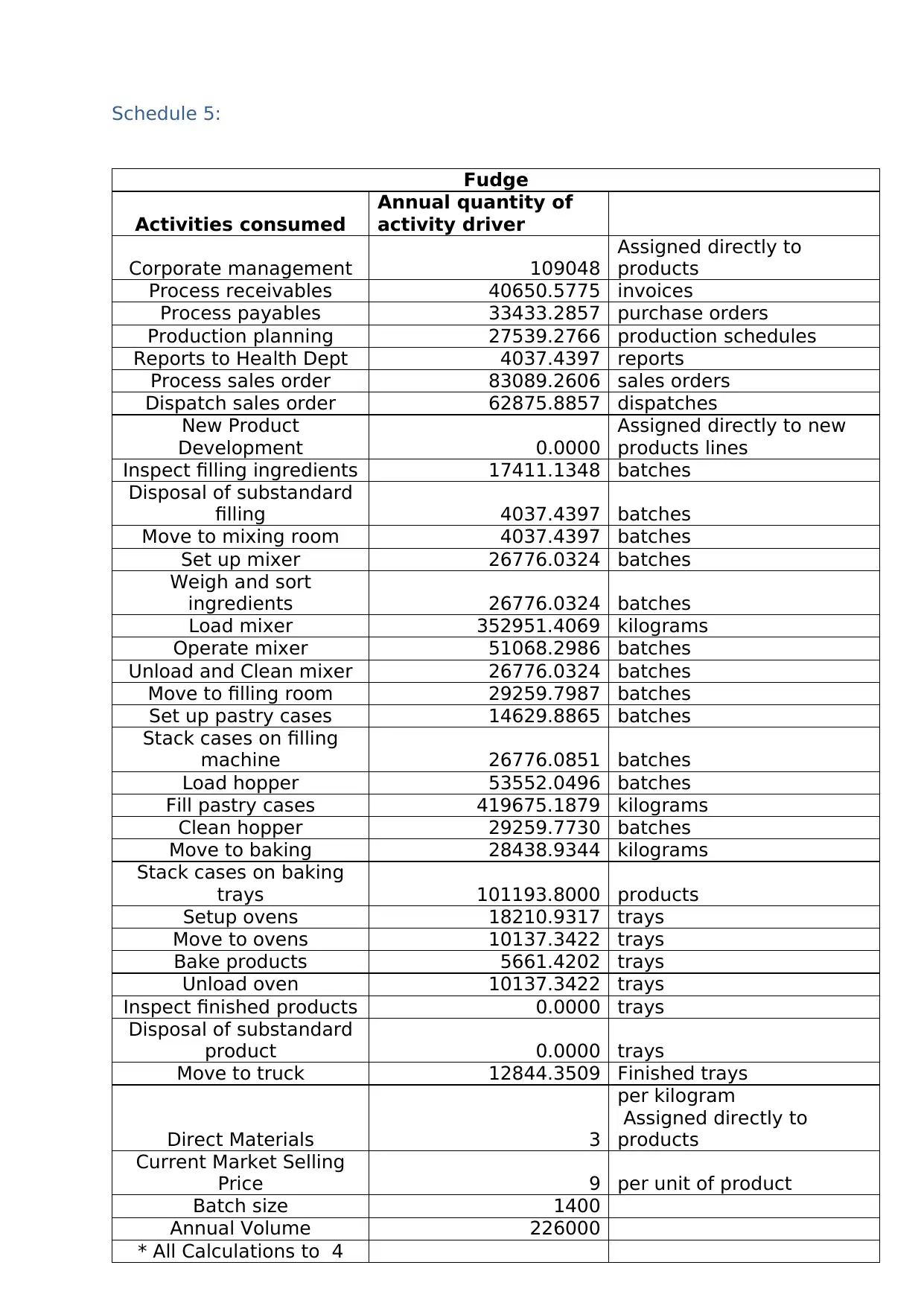

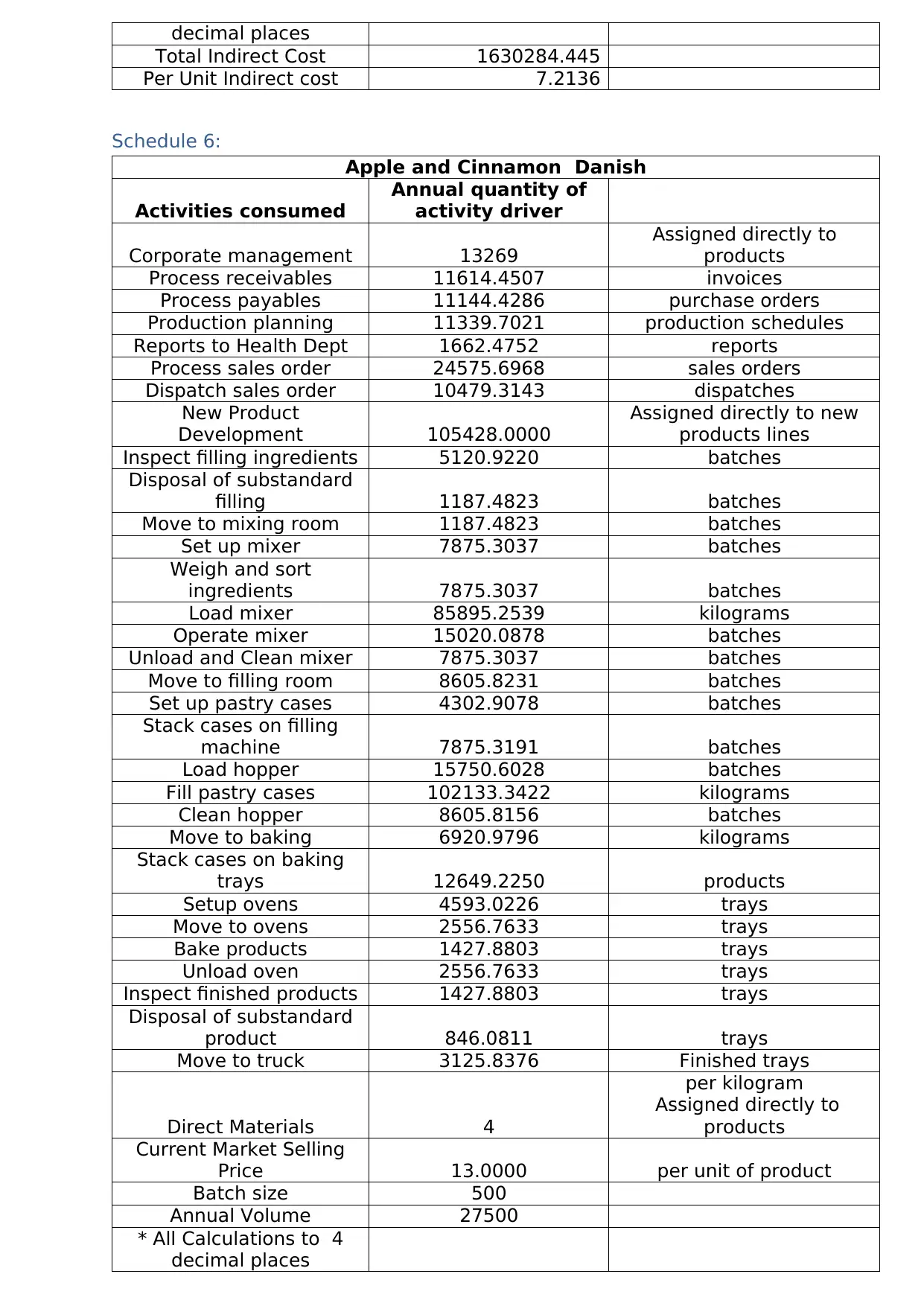

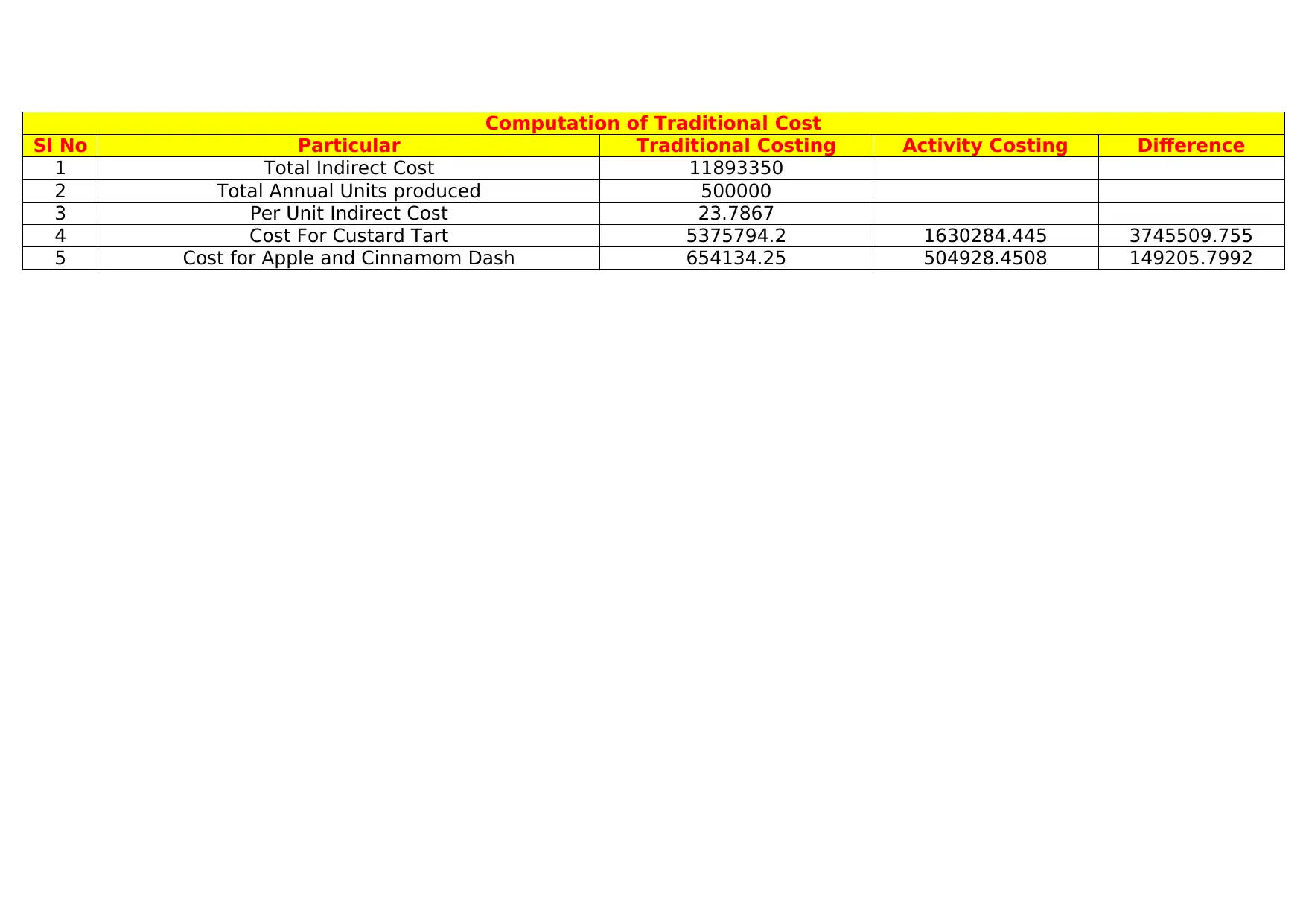

This assignment explores and compares absorption costing and activity-based costing (ABC) methods, crucial in management accounting for cost allocation and decision-making. The solution provided includes detailed schedules with resource drivers, activity centers, and activity costs, showcasing how overhead costs are allocated under both methodologies. It analyzes the differences in product costing, highlighting the impact of each method on cost determination and potential overstatement issues. The assignment also delves into the evolution of ABC, outlining its advantages and disadvantages alongside those of absorption costing. The analysis includes practical calculations and comparisons, offering insights into the application and implications of each costing approach, along with the reasons for cost variations and the importance of accurate cost allocation in production processes.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.