A Study on the Dimensions of Service Quality in Banking Sector and CS

VerifiedAdded on 2021/04/23

|31

|10264

|124

Project

AI Summary

This project investigates the critical role of service quality in the banking sector and its impact on customer satisfaction. Utilizing the SERVQUAL model, the study analyzes the dimensions of service quality, including tangibility, reliability, responsiveness, assurance, and empathy, and their effects on customer satisfaction and retention. The research explores the relationship between service quality and customer satisfaction, highlighting how banks can improve service delivery to meet and exceed customer expectations. The project also addresses the strategic importance of service quality in building customer loyalty and achieving a competitive advantage within the banking industry. The study examines the impact of both human and non-human related factors of service quality on customer satisfaction. The project provides a comprehensive literature review, a detailed introduction, and a conclusion, along with tables and figures to support the analysis. The findings of this project can support banks to recognize service quality dimensions that greatest predict customers’ satisfaction.

Abstract

Service Quality in the banking sector is one of the most important criteria and an asset in measuring and

evaluating customer satisfaction thereby satisfying the customer with improved service quality will lead to high

amount of customer retention. In order to measure the service quality, SERVQUAL model was adopted.

Owing to the belief that improved service quality is a must in attaining customer satisfaction,

determinants such as tangibility and empathy plays a pivotal role. Recent academics have incensed a flurry of

different studies exploring the relationship between service quality and the customer satisfaction in the banking

sector.

This study examines how service quality dimensions effects the customer satisfaction in the banking

sector, whereby realizing the gap expectations, quality can be improved in order to satisfy the customer.

Key words: Service Quality, Service Quality Dimensions, Customer Satisfaction, SERVQUAL, Banks

Service Quality in the banking sector is one of the most important criteria and an asset in measuring and

evaluating customer satisfaction thereby satisfying the customer with improved service quality will lead to high

amount of customer retention. In order to measure the service quality, SERVQUAL model was adopted.

Owing to the belief that improved service quality is a must in attaining customer satisfaction,

determinants such as tangibility and empathy plays a pivotal role. Recent academics have incensed a flurry of

different studies exploring the relationship between service quality and the customer satisfaction in the banking

sector.

This study examines how service quality dimensions effects the customer satisfaction in the banking

sector, whereby realizing the gap expectations, quality can be improved in order to satisfy the customer.

Key words: Service Quality, Service Quality Dimensions, Customer Satisfaction, SERVQUAL, Banks

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Acknowledgement

Thank you!

Thank you!

Table of Contents

1.0 Introduction......................................................................................................................................................1

1.1 Background of the study.............................................................................................................................1

1.2 Problem Statement......................................................................................................................................2

1.3 Problem Justification...................................................................................................................................2

1.4 Research Questions......................................................................................................................................4

1.5 Research Objectives.....................................................................................................................................4

1.6 Significance of the study..............................................................................................................................4

2.0 Literature Review............................................................................................................................................5

2.1 Service Quality and its Conceptual roots..................................................................................................5

3.0 Service Quality and Customer Satisfaction in the banking Sector...........................................................16

3.1 Reliability and Customer Satisfaction.....................................................................................................17

3.2 Assurance and Customer Satisfaction.....................................................................................................17

3.3 Tangibility and Customer Satisfaction....................................................................................................17

3.4 Empathy and Customer Satisfaction.......................................................................................................18

3.5 Responsiveness and Customer Satisfaction.............................................................................................18

6.0 Conclusion......................................................................................................................................................20

5.0 References.......................................................................................................................................................21

1.0 Introduction......................................................................................................................................................1

1.1 Background of the study.............................................................................................................................1

1.2 Problem Statement......................................................................................................................................2

1.3 Problem Justification...................................................................................................................................2

1.4 Research Questions......................................................................................................................................4

1.5 Research Objectives.....................................................................................................................................4

1.6 Significance of the study..............................................................................................................................4

2.0 Literature Review............................................................................................................................................5

2.1 Service Quality and its Conceptual roots..................................................................................................5

3.0 Service Quality and Customer Satisfaction in the banking Sector...........................................................16

3.1 Reliability and Customer Satisfaction.....................................................................................................17

3.2 Assurance and Customer Satisfaction.....................................................................................................17

3.3 Tangibility and Customer Satisfaction....................................................................................................17

3.4 Empathy and Customer Satisfaction.......................................................................................................18

3.5 Responsiveness and Customer Satisfaction.............................................................................................18

6.0 Conclusion......................................................................................................................................................20

5.0 References.......................................................................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

List of Tables

Table 1.0..................................................................................................................................................................4

Table 2.0..................................................................................................................................................................4

Table 3.0................................................................................................................................................................12

Table 4.0................................................................................................................................................................13

Table 5.0................................................................................................................................................................14

Table 6.0................................................................................................................................................................19

List of Figures

Figure 1.0................................................................................................................................................................3

Figure 2.0................................................................................................................................................................6

Figure 3.0................................................................................................................................................................6

Figure 4.0................................................................................................................................................................7

Figure 5.0................................................................................................................................................................8

Figure 6.0................................................................................................................................................................8

Figure 7.0................................................................................................................................................................9

Figure 8.0................................................................................................................................................................9

Figure 9.0..............................................................................................................................................................10

Figure 10.0............................................................................................................................................................11

Figure 11.0............................................................................................................................................................13

Figure 12.0............................................................................................................................................................16

P a g e 4 | 32

Table 1.0..................................................................................................................................................................4

Table 2.0..................................................................................................................................................................4

Table 3.0................................................................................................................................................................12

Table 4.0................................................................................................................................................................13

Table 5.0................................................................................................................................................................14

Table 6.0................................................................................................................................................................19

List of Figures

Figure 1.0................................................................................................................................................................3

Figure 2.0................................................................................................................................................................6

Figure 3.0................................................................................................................................................................6

Figure 4.0................................................................................................................................................................7

Figure 5.0................................................................................................................................................................8

Figure 6.0................................................................................................................................................................8

Figure 7.0................................................................................................................................................................9

Figure 8.0................................................................................................................................................................9

Figure 9.0..............................................................................................................................................................10

Figure 10.0............................................................................................................................................................11

Figure 11.0............................................................................................................................................................13

Figure 12.0............................................................................................................................................................16

P a g e 4 | 32

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Project

A study on the dimensions of service quality in the banking sector and its effect

on customer satisfaction.

A study on the dimensions of service quality in the banking sector and its effect

on customer satisfaction.

1.0 Introduction

1.1 Background of the study

The Banks of any country plays a key role in the economic development where the term banking and financial

services are vital for the advancement of any economy, moreover the banking procedures are progressively

becoming client oriented (Osman, Mohamad & Mohamad, 2015). Having said that, it is vital for banks to build

more unique relationships with customers, in this highly globalized and competitive environment, where it is a

common belief that the success of the market place is dependent on organization’s ability to create customers in

which the most valuable resource for a bank is their customers (Ghotbabadi, Feiz & Baharun, 2015). Many

banks have started to improve their service quality in order to face these challenges where service quality is the

major influence, to maintain the competitive advantage in the market place and it is one of the serious

components in satisfying the customer (Belas & Gabcova, 2016).

Banking industry players that are flourishing in the novel global economy identifies measuring service quality

towards customer satisfaction as a key aspect, particularly when there is endlessly increasing pressure from

other organizations in the same industry and demanding client necessities (Dewan, 2014). Currently it is a rising

trend in banks to exercise, relationship based approach and to move away from transactional based marketing in

which they have identified the lifetime values of clients which is having the core in offering high quality

services (Banerjee and Sah, 2012). Therefore, service quality is a strategic tool that reinforces the competitive

advantage where it is determined by the customer satisfaction and vice versa (Banerjee and Sah, 2012). As per

Felix (2017) customer expectations are always very high and service provided by banks are low where service

quality can act as the mediator that bridges gaps between banks profitability and the customer satisfaction.

Therefore, to deliver greater services to the customers, firstly banks should recognize how customers perceive

and evaluate their services, in the case of banking industry, customers are attracted towards high quality

services (Masukujjaman & Akter, 2012). Banks have already understood the notion that, customers are the main

drivers for their place on the profitability ladder (Shahin & Samea, 2010). Banks differentiate their services,

operations from its opponents by implementing service quality dimensions as strategic options, notably to

satisfy customers, banks offer a prominent level of service quality that delivers a significant level of customer

satisfaction along with conquering sustainable competitive advantage (Terefe & Singh, 2016). For this, bankers

are adopting elevated level customer oriented services via service quality dimensions (SERVQUAL

dimensions) like empathy, assurance, responsiveness, tangibles and reliability (Parasuraman, Valarie &

Leonard, 1985). In this report, author has made an attempt to use the SERVQUAL model to understand the

P a g e 1 | 32

1.1 Background of the study

The Banks of any country plays a key role in the economic development where the term banking and financial

services are vital for the advancement of any economy, moreover the banking procedures are progressively

becoming client oriented (Osman, Mohamad & Mohamad, 2015). Having said that, it is vital for banks to build

more unique relationships with customers, in this highly globalized and competitive environment, where it is a

common belief that the success of the market place is dependent on organization’s ability to create customers in

which the most valuable resource for a bank is their customers (Ghotbabadi, Feiz & Baharun, 2015). Many

banks have started to improve their service quality in order to face these challenges where service quality is the

major influence, to maintain the competitive advantage in the market place and it is one of the serious

components in satisfying the customer (Belas & Gabcova, 2016).

Banking industry players that are flourishing in the novel global economy identifies measuring service quality

towards customer satisfaction as a key aspect, particularly when there is endlessly increasing pressure from

other organizations in the same industry and demanding client necessities (Dewan, 2014). Currently it is a rising

trend in banks to exercise, relationship based approach and to move away from transactional based marketing in

which they have identified the lifetime values of clients which is having the core in offering high quality

services (Banerjee and Sah, 2012). Therefore, service quality is a strategic tool that reinforces the competitive

advantage where it is determined by the customer satisfaction and vice versa (Banerjee and Sah, 2012). As per

Felix (2017) customer expectations are always very high and service provided by banks are low where service

quality can act as the mediator that bridges gaps between banks profitability and the customer satisfaction.

Therefore, to deliver greater services to the customers, firstly banks should recognize how customers perceive

and evaluate their services, in the case of banking industry, customers are attracted towards high quality

services (Masukujjaman & Akter, 2012). Banks have already understood the notion that, customers are the main

drivers for their place on the profitability ladder (Shahin & Samea, 2010). Banks differentiate their services,

operations from its opponents by implementing service quality dimensions as strategic options, notably to

satisfy customers, banks offer a prominent level of service quality that delivers a significant level of customer

satisfaction along with conquering sustainable competitive advantage (Terefe & Singh, 2016). For this, bankers

are adopting elevated level customer oriented services via service quality dimensions (SERVQUAL

dimensions) like empathy, assurance, responsiveness, tangibles and reliability (Parasuraman, Valarie &

Leonard, 1985). In this report, author has made an attempt to use the SERVQUAL model to understand the

P a g e 1 | 32

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

service quality dimensions and its effect on customer satisfaction in the banking sector (Sangeetha &

Mahalingam, 2011).

1.2 Problem Statement

As per Quyet, Vinh & Chang (2017) many banks are lagging behind many areas such as the way employees

greeted customers, waiting time, time taken to answer calls or whether the clients received truthful and adequate

information and follow - ups from banks. Supporting that Muyeed (2012) have revealed shocking failures from

the banking industry, as per his study half of the customers from different banks around the world are unhappy

with how the complaints are dealt with. It is also evident that bad advices have led to serious financial losses

underpinning an average of 7, 143 complains per day (Jashireh, Slambolchi & Mobarakabadi, 2016).

Moreover, it is evident that majority (63%) of customers who do take time to complaint about the services they

got from the bank are not fully satisfied with the responses (Seth Deshmukh & Vrat, 2005). Above all different

practices among employees, poor work ethics, and poor working states have formed conspiracy on service

quality conveyed by the banks (Seth Deshmukh & Vrat, 2005). In this light, the topic of service quality needs a

renewed understanding in the contemporary industry situation where still there’s a gap that had not been

bridged where more strict banking regulations adjust how financial institutions do business.

Keeping in view the importance of service quality and customer satisfaction, this report is intended to study the

effects of service quality as an independent variable on the dependent variable, customer satisfaction.

1.3 Problem Justification

The crucial aim of this study is to evaluate and access how service quality affects the customer satisfaction in

the banking industry, where the practical insinuations that can be taken are to improve commercial bank service

quality. This study has also attempted to correlate the affiliation of customer satisfaction level and the success

of the banks through improved service quality with the assistance of other former literatures. The understanding

of the different dimensions of service quality towards customer satisfaction in different banks will improve the

understanding of the elements that effect on a profitable and a long-term connection with clients in the banking

industry. The study will provide significant evidence to the officials and supervisors/Managers of banks

This study then will eventually evaluate and disclose the solid views of how the dimensions of SERVQUAL

(reliability, responsiveness, assurance, empathy, and tangibility) influences the customer satisfaction and its

boundaries as how well a bank’s services meet or surpass customer expectations, thus to develop abilities and

attitudes of the staffs to offer an improved customer service to diminish the SERVQUAL gaps.

P a g e 2 | 32

Mahalingam, 2011).

1.2 Problem Statement

As per Quyet, Vinh & Chang (2017) many banks are lagging behind many areas such as the way employees

greeted customers, waiting time, time taken to answer calls or whether the clients received truthful and adequate

information and follow - ups from banks. Supporting that Muyeed (2012) have revealed shocking failures from

the banking industry, as per his study half of the customers from different banks around the world are unhappy

with how the complaints are dealt with. It is also evident that bad advices have led to serious financial losses

underpinning an average of 7, 143 complains per day (Jashireh, Slambolchi & Mobarakabadi, 2016).

Moreover, it is evident that majority (63%) of customers who do take time to complaint about the services they

got from the bank are not fully satisfied with the responses (Seth Deshmukh & Vrat, 2005). Above all different

practices among employees, poor work ethics, and poor working states have formed conspiracy on service

quality conveyed by the banks (Seth Deshmukh & Vrat, 2005). In this light, the topic of service quality needs a

renewed understanding in the contemporary industry situation where still there’s a gap that had not been

bridged where more strict banking regulations adjust how financial institutions do business.

Keeping in view the importance of service quality and customer satisfaction, this report is intended to study the

effects of service quality as an independent variable on the dependent variable, customer satisfaction.

1.3 Problem Justification

The crucial aim of this study is to evaluate and access how service quality affects the customer satisfaction in

the banking industry, where the practical insinuations that can be taken are to improve commercial bank service

quality. This study has also attempted to correlate the affiliation of customer satisfaction level and the success

of the banks through improved service quality with the assistance of other former literatures. The understanding

of the different dimensions of service quality towards customer satisfaction in different banks will improve the

understanding of the elements that effect on a profitable and a long-term connection with clients in the banking

industry. The study will provide significant evidence to the officials and supervisors/Managers of banks

This study then will eventually evaluate and disclose the solid views of how the dimensions of SERVQUAL

(reliability, responsiveness, assurance, empathy, and tangibility) influences the customer satisfaction and its

boundaries as how well a bank’s services meet or surpass customer expectations, thus to develop abilities and

attitudes of the staffs to offer an improved customer service to diminish the SERVQUAL gaps.

P a g e 2 | 32

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

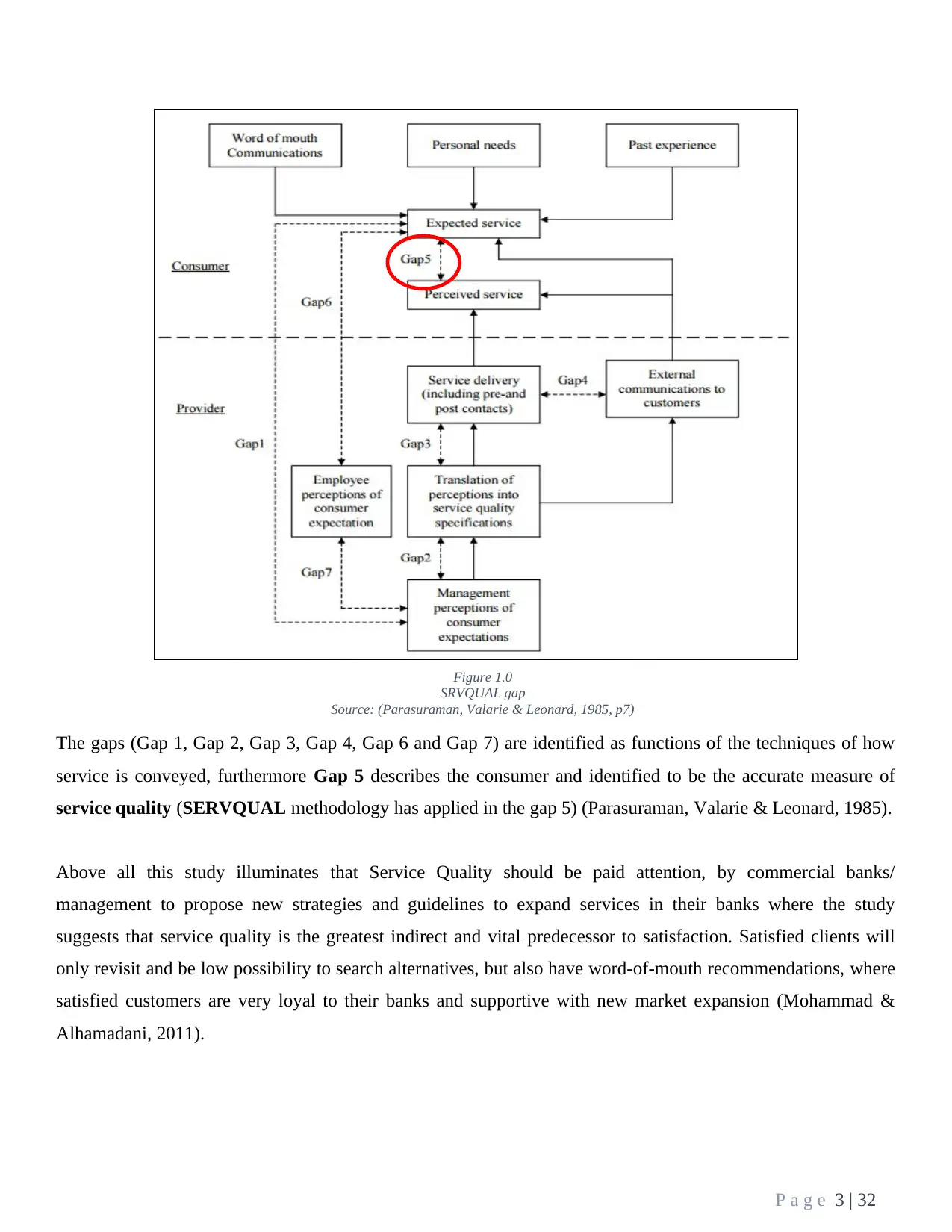

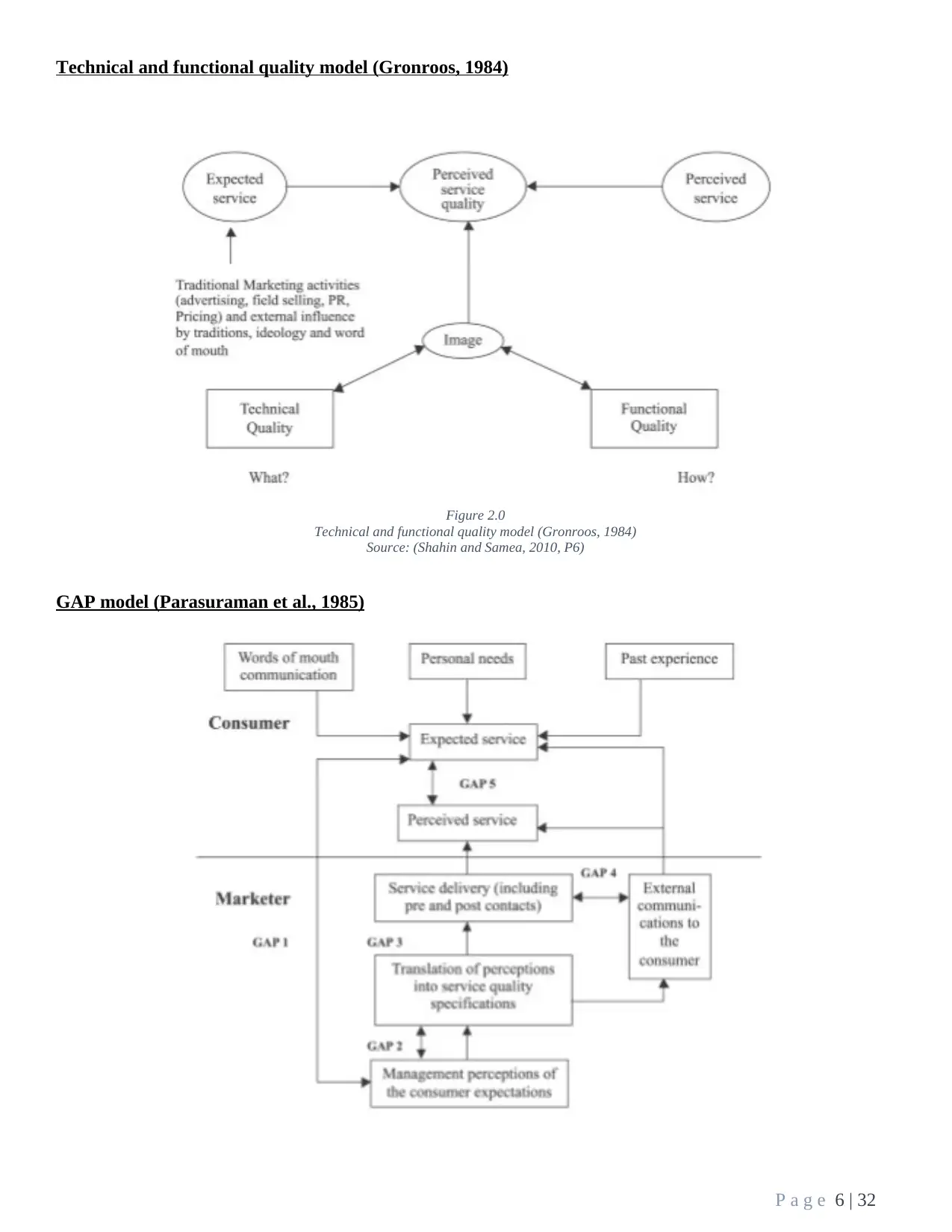

The gaps (Gap 1, Gap 2, Gap 3, Gap 4, Gap 6 and Gap 7) are identified as functions of the techniques of how

service is conveyed, furthermore Gap 5 describes the consumer and identified to be the accurate measure of

service quality (SERVQUAL methodology has applied in the gap 5) (Parasuraman, Valarie & Leonard, 1985).

Above all this study illuminates that Service Quality should be paid attention, by commercial banks/

management to propose new strategies and guidelines to expand services in their banks where the study

suggests that service quality is the greatest indirect and vital predecessor to satisfaction. Satisfied clients will

only revisit and be low possibility to search alternatives, but also have word-of-mouth recommendations, where

satisfied customers are very loyal to their banks and supportive with new market expansion (Mohammad &

Alhamadani, 2011).

P a g e 3 | 32

Figure 1.0

SRVQUAL gap

Source: (Parasuraman, Valarie & Leonard, 1985, p7)

service is conveyed, furthermore Gap 5 describes the consumer and identified to be the accurate measure of

service quality (SERVQUAL methodology has applied in the gap 5) (Parasuraman, Valarie & Leonard, 1985).

Above all this study illuminates that Service Quality should be paid attention, by commercial banks/

management to propose new strategies and guidelines to expand services in their banks where the study

suggests that service quality is the greatest indirect and vital predecessor to satisfaction. Satisfied clients will

only revisit and be low possibility to search alternatives, but also have word-of-mouth recommendations, where

satisfied customers are very loyal to their banks and supportive with new market expansion (Mohammad &

Alhamadani, 2011).

P a g e 3 | 32

Figure 1.0

SRVQUAL gap

Source: (Parasuraman, Valarie & Leonard, 1985, p7)

1.4 Research Questions

How human related factors of service quality effects the customer satisfaction in the banking sector? ??

bbbbajhfndddsbankiswswsssectorsector? How non – human related factors of service quality effects the customer satisfaction in the banking sector?

bankisesector? Table 1.0

Research Objectives

Source: Authors work based on the study

1.5 Research Objectives

To recognize the impact of human related service quality factors towards the customer satisfaction in

the banking sector.

To recognize the impact of non- human related service quality factors towards the customer

satisfaction in the banking sector.

To investigate the linkage between service quality and customer satisfaction and the methods through

which banks can develop and manage the process of providing quality standards to their customers.

Table 2.0

Research Objectives

Source: Authors work based on Study

1.6 Significance of the study

This study has a unique contribution, the findings of the study are likely to support banks to recognize service

quality dimensions that greatest predict customers’ satisfaction, to focus on them accordingly to their degree of

position, in this regard and more research can be done based on this research to study the effect of service

quality on customer satisfaction and will contribute for service organizations targeting to develop the quality

criterions to satisfy their prevailing and future customers. Moreover, this study will help bank managers/Policy

makers to well understand how to grasp loyal customers by satisfying their overall needs with prospects that

they will promote the bank, and hold their trust upon the bank which marks improved profit, and enhances

reputation as well. Studies have been done that evaluates the determinants of customer satisfaction. Thus, this

study seeks to investigate service quality as a determinant of customer satisfaction in banking sector.

P a g e 4 | 32

How human related factors of service quality effects the customer satisfaction in the banking sector? ??

bbbbajhfndddsbankiswswsssectorsector? How non – human related factors of service quality effects the customer satisfaction in the banking sector?

bankisesector? Table 1.0

Research Objectives

Source: Authors work based on the study

1.5 Research Objectives

To recognize the impact of human related service quality factors towards the customer satisfaction in

the banking sector.

To recognize the impact of non- human related service quality factors towards the customer

satisfaction in the banking sector.

To investigate the linkage between service quality and customer satisfaction and the methods through

which banks can develop and manage the process of providing quality standards to their customers.

Table 2.0

Research Objectives

Source: Authors work based on Study

1.6 Significance of the study

This study has a unique contribution, the findings of the study are likely to support banks to recognize service

quality dimensions that greatest predict customers’ satisfaction, to focus on them accordingly to their degree of

position, in this regard and more research can be done based on this research to study the effect of service

quality on customer satisfaction and will contribute for service organizations targeting to develop the quality

criterions to satisfy their prevailing and future customers. Moreover, this study will help bank managers/Policy

makers to well understand how to grasp loyal customers by satisfying their overall needs with prospects that

they will promote the bank, and hold their trust upon the bank which marks improved profit, and enhances

reputation as well. Studies have been done that evaluates the determinants of customer satisfaction. Thus, this

study seeks to investigate service quality as a determinant of customer satisfaction in banking sector.

P a g e 4 | 32

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.0 Literature Review

2.1 Service Quality and its Conceptual roots.

As per Jain & Gupta (2004) quality is the “consistency with fixed specifications”, supported by Ragavan

(2013), who defined Quality as anything which accords with the features of the service to reach the exterior

customers' requirements. Moreover, service and product quality differ from each other as earlier the tangible

and the latter is intangible where services are benefits or activities that delivered for sale or else that are

delivered for being to a specific product (Naeem, Akram, & Saif, 2009), furthermore, Bo (1998) demarcated

services as act or behavior created on an interaction between two parties. Above all service quality has been

conceptualized as the difference between the perceived services expected performance and the perceived service

actual performance in which it can be the performance that will give benefit to the customers.

To that end, since service quality has been considered as the essence or the core of strategic

competition, banks should always care about the service quality (Ilyas et al., 2013). In order to contribute for the

own success and the persistence in the international as well as national banking competitive environment banks

must possess a good knowledge of characteristics and advantages of service quality as a part of them which will

contribute positively in the rivalry (Ananth, Ramesh and Prabaharan, 2010; Magdy & Nevien, 2017). All things

considered it seems reasonable to assume that quality of the banking services which are offered to external

clients are an integrative assessment which they should have qualified employees to offer higher level of

services towards satisfying customers.

It is obvious that Service Quality is a critical dimension of competitiveness, where it is a crucial issue

and a challenge for the contemporary banking industry to provide excellent service quality and higher customer

satisfaction (Brady & Cronin, 2001; Cheserek, Kimwolo & Cherop, 2015). Service quality has been one of the

major topics during the past decades, for many managers, researchers, practitioners because of its affect to the

banking industry to lower costs, gain higher profits, customer loyalty and satisfaction, return of investment (Lau

et al., 2013; Ramachandran & Chidambaram, 2012). Significantly both developed and developing countries are

facing the rapid development and competition of the service quality where it had made important for banks to

evaluate and measure quality of service encounters (Shahin, 2017; Selvakumar, 2015).

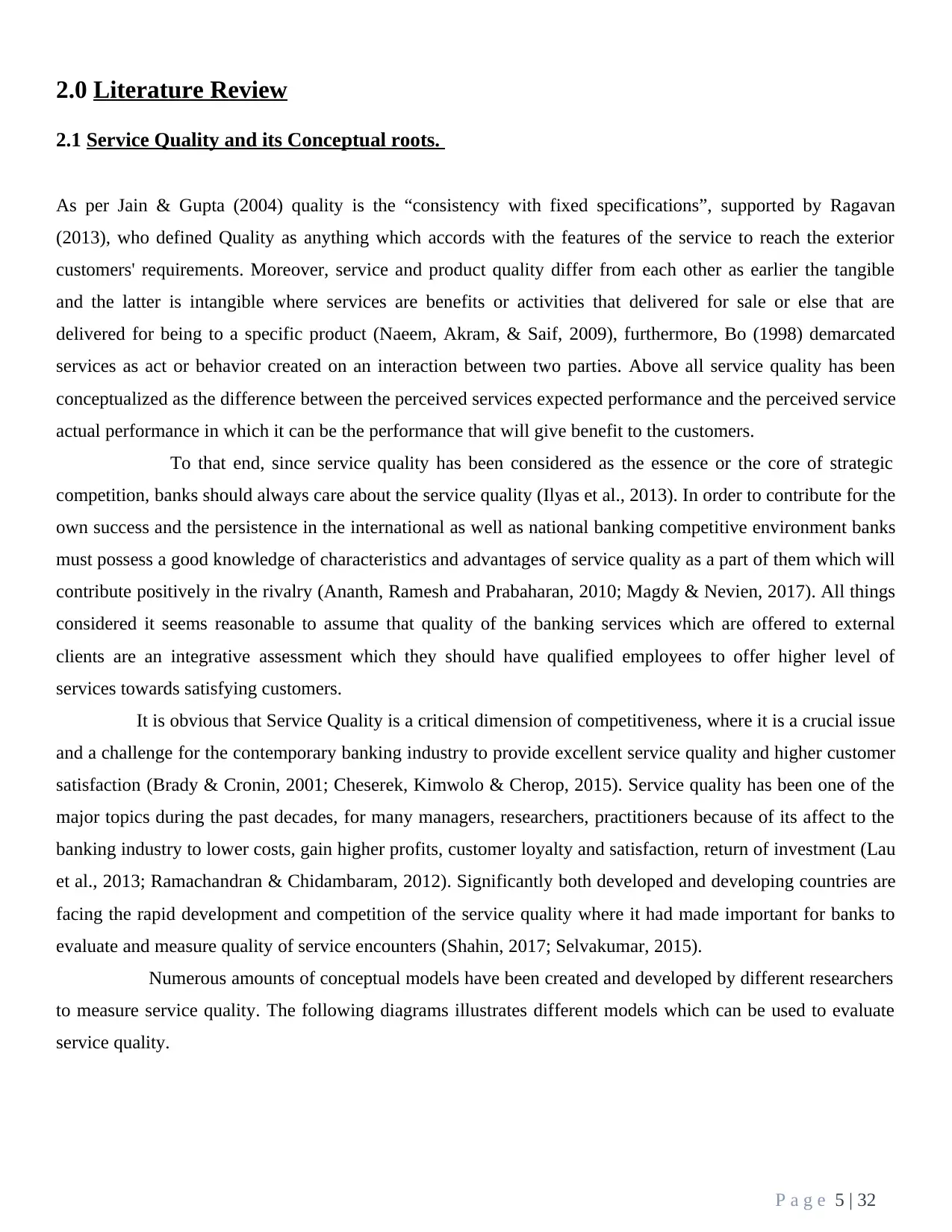

Numerous amounts of conceptual models have been created and developed by different researchers

to measure service quality. The following diagrams illustrates different models which can be used to evaluate

service quality.

P a g e 5 | 32

2.1 Service Quality and its Conceptual roots.

As per Jain & Gupta (2004) quality is the “consistency with fixed specifications”, supported by Ragavan

(2013), who defined Quality as anything which accords with the features of the service to reach the exterior

customers' requirements. Moreover, service and product quality differ from each other as earlier the tangible

and the latter is intangible where services are benefits or activities that delivered for sale or else that are

delivered for being to a specific product (Naeem, Akram, & Saif, 2009), furthermore, Bo (1998) demarcated

services as act or behavior created on an interaction between two parties. Above all service quality has been

conceptualized as the difference between the perceived services expected performance and the perceived service

actual performance in which it can be the performance that will give benefit to the customers.

To that end, since service quality has been considered as the essence or the core of strategic

competition, banks should always care about the service quality (Ilyas et al., 2013). In order to contribute for the

own success and the persistence in the international as well as national banking competitive environment banks

must possess a good knowledge of characteristics and advantages of service quality as a part of them which will

contribute positively in the rivalry (Ananth, Ramesh and Prabaharan, 2010; Magdy & Nevien, 2017). All things

considered it seems reasonable to assume that quality of the banking services which are offered to external

clients are an integrative assessment which they should have qualified employees to offer higher level of

services towards satisfying customers.

It is obvious that Service Quality is a critical dimension of competitiveness, where it is a crucial issue

and a challenge for the contemporary banking industry to provide excellent service quality and higher customer

satisfaction (Brady & Cronin, 2001; Cheserek, Kimwolo & Cherop, 2015). Service quality has been one of the

major topics during the past decades, for many managers, researchers, practitioners because of its affect to the

banking industry to lower costs, gain higher profits, customer loyalty and satisfaction, return of investment (Lau

et al., 2013; Ramachandran & Chidambaram, 2012). Significantly both developed and developing countries are

facing the rapid development and competition of the service quality where it had made important for banks to

evaluate and measure quality of service encounters (Shahin, 2017; Selvakumar, 2015).

Numerous amounts of conceptual models have been created and developed by different researchers

to measure service quality. The following diagrams illustrates different models which can be used to evaluate

service quality.

P a g e 5 | 32

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Technical and functional quality model (Gronroos, 1984)

GAP model (Parasuraman et al., 1985)

P a g e 6 | 32

Figure 2.0

Technical and functional quality model (Gronroos, 1984)

Source: (Shahin and Samea, 2010, P6)

GAP model (Parasuraman et al., 1985)

P a g e 6 | 32

Figure 2.0

Technical and functional quality model (Gronroos, 1984)

Source: (Shahin and Samea, 2010, P6)

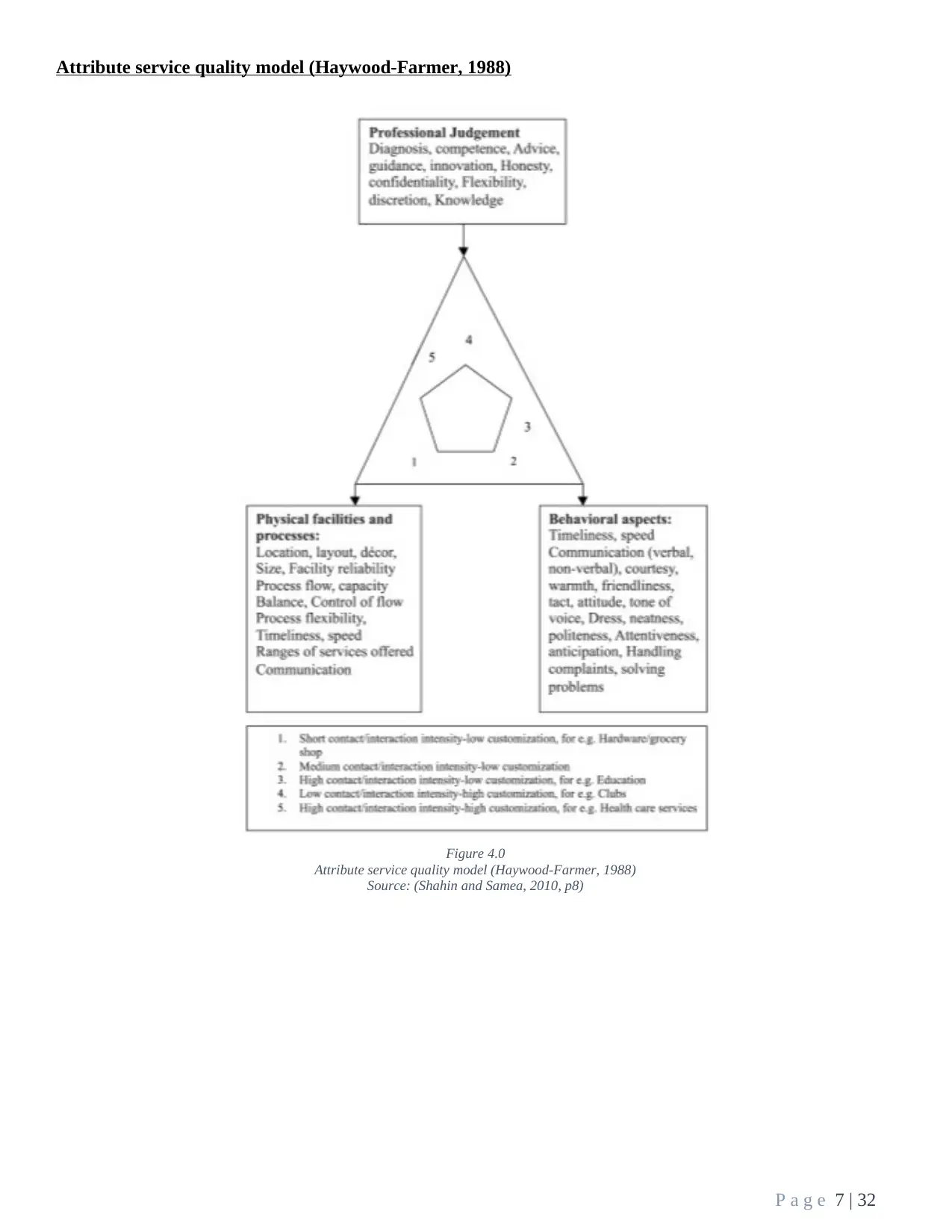

Attribute service quality model (Haywood-Farmer, 1988)

P a g e 7 | 32

Figure 4.0

Attribute service quality model (Haywood-Farmer, 1988)

Source: (Shahin and Samea, 2010, p8)

P a g e 7 | 32

Figure 4.0

Attribute service quality model (Haywood-Farmer, 1988)

Source: (Shahin and Samea, 2010, p8)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.