ACC 203 Assignment .

VerifiedAdded on 2023/05/29

|10

|1503

|213

AI Summary

This assignment covers topics like costing of products, variance analysis, financial analysis, and analysis with constraint financial resources. It includes calculations, journal entries, and financial analysis for decision making.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACC 203 ASSIGNMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Problem 1 – Costing of products.................................................................................................................2

Problem 2 – Variance analysis.....................................................................................................................4

Problem 3 – Financial Analysis.....................................................................................................................6

Problem 4 –Analysis with constraint financial resources.............................................................................8

Problem 1 – Costing of products.................................................................................................................2

Problem 2 – Variance analysis.....................................................................................................................4

Problem 3 – Financial Analysis.....................................................................................................................6

Problem 4 –Analysis with constraint financial resources.............................................................................8

Problem 1 – Costing of products

Problem 1 deals with costing. It includes calculating the cost per bottle and further journalizing

the transactions relating to production costs in the work in process inventory account. The

calculation of correct cost per unit produced is an important factor in the accounting, as the

selling price and profit margin are largely dependent on the cost of unit.

In the given case, Cool Brew Ltd has started producing breweries named “Cool Bay Draught” by

packaging them in bottles containing 300 milliliters. The company consists of two departments

named, mixing and bottling and has respective costs. During the period the company produced

48000 litres of product and bottled them.

The first requirement is to calculate the cost per bottle of Cool Bay Drought. For calculation of

cost per bottle, the total cost of both the departments is computed, which is $192,000 ($160,000

for mixing department + $32,000 for bottling department). The bifurcation of said cost is as

below:

Particulars Mixing Bottling

Direct materials $113,000 $17,000

Direct labour $15,000 $6,000

Manufacturing overhead $32,000 $9,000

Total $160,000 $32,000

Hence, the cost per bottle is total cost divided by number of bottles produced, which comes at

$1.20

Total cost / number of bottles

= 192000 / 160000

= $1.20

Hence, the cost of producing one bottle is $1.20.

The second requirement asks us to journalize the transactions. The journal entries are as below:

Particulars Dr./Cr.

Debit

Amount

Credit

Amount

WIP Inventory Dr. $130,000

Accounts payable A/c $130,000

(Direct materials charged to production)

WIP Inventory Dr. $21,000

Wages payable A/c $21,000

(Direct labour cost charged to production)

Problem 1 deals with costing. It includes calculating the cost per bottle and further journalizing

the transactions relating to production costs in the work in process inventory account. The

calculation of correct cost per unit produced is an important factor in the accounting, as the

selling price and profit margin are largely dependent on the cost of unit.

In the given case, Cool Brew Ltd has started producing breweries named “Cool Bay Draught” by

packaging them in bottles containing 300 milliliters. The company consists of two departments

named, mixing and bottling and has respective costs. During the period the company produced

48000 litres of product and bottled them.

The first requirement is to calculate the cost per bottle of Cool Bay Drought. For calculation of

cost per bottle, the total cost of both the departments is computed, which is $192,000 ($160,000

for mixing department + $32,000 for bottling department). The bifurcation of said cost is as

below:

Particulars Mixing Bottling

Direct materials $113,000 $17,000

Direct labour $15,000 $6,000

Manufacturing overhead $32,000 $9,000

Total $160,000 $32,000

Hence, the cost per bottle is total cost divided by number of bottles produced, which comes at

$1.20

Total cost / number of bottles

= 192000 / 160000

= $1.20

Hence, the cost of producing one bottle is $1.20.

The second requirement asks us to journalize the transactions. The journal entries are as below:

Particulars Dr./Cr.

Debit

Amount

Credit

Amount

WIP Inventory Dr. $130,000

Accounts payable A/c $130,000

(Direct materials charged to production)

WIP Inventory Dr. $21,000

Wages payable A/c $21,000

(Direct labour cost charged to production)

WIP Inventory Dr. $41,000

Manufacturing O/H payable A/c $41,000

(Overhead cost charged to production)

Manufacturing O/H payable A/c $41,000

(Overhead cost charged to production)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Problem 2 – Variance analysis

Variance analysis is the investigation of the differences between actual and budgeted values.

This analysis is important in controlling and maintaining the costs. As it helps in evaluating and

understanding the reasons of differences between actual and budgeted data and hence helps the

management in taking decisions for eliminating and controlling the irrelevant costs.

In the given case, the data has been given regarding actual and budgeted production of the output

and the question demands for calculation of variances.

The first variance is Direct Material Price Variance which reflects the variation between the

actual rate and standard rate.

Direct material price variance = (Standard price - Actual price) x Actual quantity

= (7.20 - 7.40) x 4200

= -$840 Unfavorable

Since, the actual price is more than the standard price, hence the direct material price variance is

unfavorable, which means that the company has procured the material at a higher cost than

budgeted.

Another variance is Direct Material Usage Variance which shows the variation between the

actual quantity used for producing one unit of product versus the budgeted quantity required for

production of one unit of product.

Direct material usage variances = (Standard quantity - Actual quantity) x Standard

price

= (4000 - 4200) x 7.20

= -$1,440 Unfavorable

From above, we found that the company has budgeted to consume 4000 kgs of material for

producing 2000 units whereas in actual the company has consumed 4200 kgs of material for

producing the 2000 units. Hence, the above variance is also unfavorable for the company.

The other variance is Direct Labor Rate variance which reflects the variation between the actual

rate paid to labor and the budgeted rate.

Direct labor rate variance = (Standard rate - Actual rate) x Actual hours worked

= (18 - 18.30) x 6450

= -$1,935 Unfavourable

Variance analysis is the investigation of the differences between actual and budgeted values.

This analysis is important in controlling and maintaining the costs. As it helps in evaluating and

understanding the reasons of differences between actual and budgeted data and hence helps the

management in taking decisions for eliminating and controlling the irrelevant costs.

In the given case, the data has been given regarding actual and budgeted production of the output

and the question demands for calculation of variances.

The first variance is Direct Material Price Variance which reflects the variation between the

actual rate and standard rate.

Direct material price variance = (Standard price - Actual price) x Actual quantity

= (7.20 - 7.40) x 4200

= -$840 Unfavorable

Since, the actual price is more than the standard price, hence the direct material price variance is

unfavorable, which means that the company has procured the material at a higher cost than

budgeted.

Another variance is Direct Material Usage Variance which shows the variation between the

actual quantity used for producing one unit of product versus the budgeted quantity required for

production of one unit of product.

Direct material usage variances = (Standard quantity - Actual quantity) x Standard

price

= (4000 - 4200) x 7.20

= -$1,440 Unfavorable

From above, we found that the company has budgeted to consume 4000 kgs of material for

producing 2000 units whereas in actual the company has consumed 4200 kgs of material for

producing the 2000 units. Hence, the above variance is also unfavorable for the company.

The other variance is Direct Labor Rate variance which reflects the variation between the actual

rate paid to labor and the budgeted rate.

Direct labor rate variance = (Standard rate - Actual rate) x Actual hours worked

= (18 - 18.30) x 6450

= -$1,935 Unfavourable

From above, we found that the company has budgeted to pay $18 per hour whereas in actual the

company has paid $18.30 per hour. Since, the company has paid more than the budgeted, hence

the said variance is unfavorable.

The last variance is Direct Labor Efficiency variance which reflects the variation between hours

taken by labor for producing one unit of product versus budgeted hours for producing one unit of

material.

Direct labor efficiency variance = (Standard hours - Actual hours) x Standard rate

= (7000 - 6450) x 18

= $9,900 Favorable

In the above variance, the actual hours taken is lower than the budgeted hours and hence the

variance is favorable.

company has paid $18.30 per hour. Since, the company has paid more than the budgeted, hence

the said variance is unfavorable.

The last variance is Direct Labor Efficiency variance which reflects the variation between hours

taken by labor for producing one unit of product versus budgeted hours for producing one unit of

material.

Direct labor efficiency variance = (Standard hours - Actual hours) x Standard rate

= (7000 - 6450) x 18

= $9,900 Favorable

In the above variance, the actual hours taken is lower than the budgeted hours and hence the

variance is favorable.

Problem 3 – Financial Analysis

Proper financial analysis is an key aspect for analysis the correct profitability and decision

making as regard to project continuity. In the given case, Sam has an ice cream shop and has

started selling fresh fruit juice as well. However, the Sam has found that the fruit juice business

is an loss making business as he included the fixed and sunk cost to its profitability. The

evaluation of Sam’s financial analysis is as below:

Particulars $ Amount ($)

Sales 67,500.00

Less: Cost of sales 30,000.00

Gross Profit 37,500.00

Less: Operating expenses:

Wages of counter staff 18,000.00

Consumables (e.g. cups and straws) 6,000.00

Utilities (allocated) 4,350.00

Depreciation of counter equipment and furnishings 3,750.00

Depreciation of building (allocated) 6,000.00

Super Scooper manager’s salary (allocated) 4,500.00 42,600.00

Net Profit / (Net Loss) (5,100.00)

Gross profit margin = Gross Profit / Sales

= 37500 / 67500

= 55.56%

Net Profit (loss) margin = Net Profit / Sales

= (5100) / 67500

= -7.56%

The above profit and loss shows that the company has a GP margin of 55.56%. Gross profit ratio

appears to be very high. However, indirect expenses are causing this profit to turn into losses.

We noticed there are some allocated costs which are not relevant for decision making.

The above profit and loss includes some relevant and sunk costs as well. The correct profit &

loss account is as under:

Particulars $ Amount ($)

Sales 67,500

Less: Cost of sales 30,000

Gross Profit 37,500

Proper financial analysis is an key aspect for analysis the correct profitability and decision

making as regard to project continuity. In the given case, Sam has an ice cream shop and has

started selling fresh fruit juice as well. However, the Sam has found that the fruit juice business

is an loss making business as he included the fixed and sunk cost to its profitability. The

evaluation of Sam’s financial analysis is as below:

Particulars $ Amount ($)

Sales 67,500.00

Less: Cost of sales 30,000.00

Gross Profit 37,500.00

Less: Operating expenses:

Wages of counter staff 18,000.00

Consumables (e.g. cups and straws) 6,000.00

Utilities (allocated) 4,350.00

Depreciation of counter equipment and furnishings 3,750.00

Depreciation of building (allocated) 6,000.00

Super Scooper manager’s salary (allocated) 4,500.00 42,600.00

Net Profit / (Net Loss) (5,100.00)

Gross profit margin = Gross Profit / Sales

= 37500 / 67500

= 55.56%

Net Profit (loss) margin = Net Profit / Sales

= (5100) / 67500

= -7.56%

The above profit and loss shows that the company has a GP margin of 55.56%. Gross profit ratio

appears to be very high. However, indirect expenses are causing this profit to turn into losses.

We noticed there are some allocated costs which are not relevant for decision making.

The above profit and loss includes some relevant and sunk costs as well. The correct profit &

loss account is as under:

Particulars $ Amount ($)

Sales 67,500

Less: Cost of sales 30,000

Gross Profit 37,500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

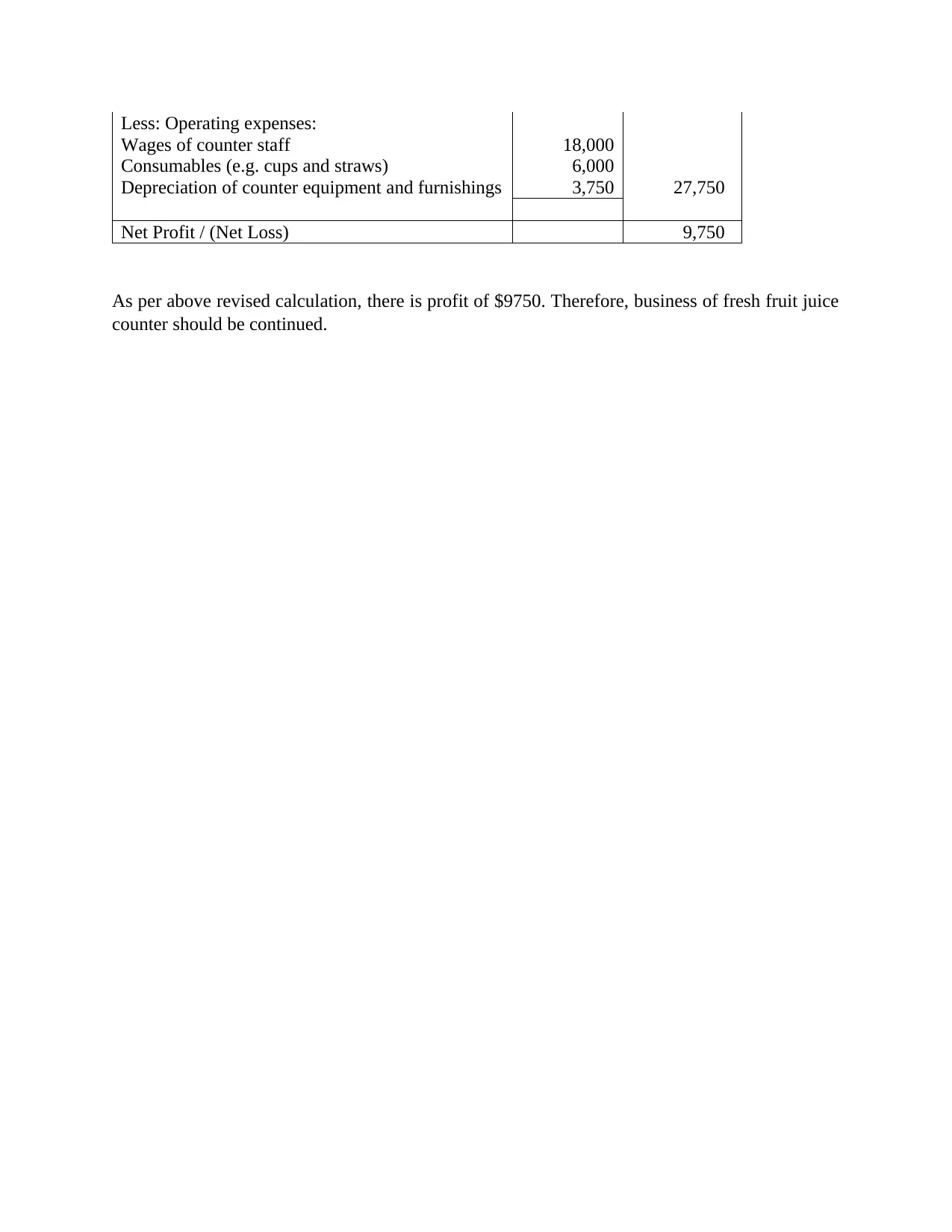

Less: Operating expenses:

Wages of counter staff 18,000

Consumables (e.g. cups and straws) 6,000

Depreciation of counter equipment and furnishings 3,750 27,750

Net Profit / (Net Loss) 9,750

As per above revised calculation, there is profit of $9750. Therefore, business of fresh fruit juice

counter should be continued.

Wages of counter staff 18,000

Consumables (e.g. cups and straws) 6,000

Depreciation of counter equipment and furnishings 3,750 27,750

Net Profit / (Net Loss) 9,750

As per above revised calculation, there is profit of $9750. Therefore, business of fresh fruit juice

counter should be continued.

Problem 4 –Analysis with constraint financial resources

Every business runs for profit and profit maximization is the main aim for any business to run.

Hence, the costing gives emphasizes on maximizing the profit by deciding which and how much

units should be produced when the resources are limited. In such a case, the product having

higher profit should be produced more as compared to one which has low profit margin.

The financial analysis when the machine hours are limited.

Particulars Standard ($) Deluxe ($)

Selling price 70.00 120.00

Direct material (15.00) (22.00)

Direct labour (10.00) (30.00)

Manufacturing overhead (30.00) (60.00)

Profit / unit 15.00 8.00

Add: Fixed costs 20.00 40.00

CM / unit 35.00 48.00

Machine hour required (in hours) 1 2

CM / machine hour 35.00 24.00

If machine hours are limited, product with higher CM per machine hour should be produced first.

Company should first allocate machine hours first towards Standard.

Number of units to be produced to maximize the ABC Ltd’s profitability.

Since maximum demand for Standard is 40,000 units, machine hours should be allocated to these

40,000 units.

Total machine hours available 60,000

Machine hours required for 40000 unit of Standard -40,000

Remaining machine hours for Deluxe 20,000

These remaining machine hours will now be allocated to Deluxe.

Remaining machine hours for Deluxe 20,000

Machine hours required per unit of deluxe 2

Number of units to be produced of Deluxe 10,000

Particulars Standard Deluxe

Contribution margin per unit $35 48

No. of units 40,000 10,000

Total contribution margin $1,400,000 $480,000

Less: Fixed costs $800,000 $400,000

Net Profit $600,000 $80,000

Every business runs for profit and profit maximization is the main aim for any business to run.

Hence, the costing gives emphasizes on maximizing the profit by deciding which and how much

units should be produced when the resources are limited. In such a case, the product having

higher profit should be produced more as compared to one which has low profit margin.

The financial analysis when the machine hours are limited.

Particulars Standard ($) Deluxe ($)

Selling price 70.00 120.00

Direct material (15.00) (22.00)

Direct labour (10.00) (30.00)

Manufacturing overhead (30.00) (60.00)

Profit / unit 15.00 8.00

Add: Fixed costs 20.00 40.00

CM / unit 35.00 48.00

Machine hour required (in hours) 1 2

CM / machine hour 35.00 24.00

If machine hours are limited, product with higher CM per machine hour should be produced first.

Company should first allocate machine hours first towards Standard.

Number of units to be produced to maximize the ABC Ltd’s profitability.

Since maximum demand for Standard is 40,000 units, machine hours should be allocated to these

40,000 units.

Total machine hours available 60,000

Machine hours required for 40000 unit of Standard -40,000

Remaining machine hours for Deluxe 20,000

These remaining machine hours will now be allocated to Deluxe.

Remaining machine hours for Deluxe 20,000

Machine hours required per unit of deluxe 2

Number of units to be produced of Deluxe 10,000

Particulars Standard Deluxe

Contribution margin per unit $35 48

No. of units 40,000 10,000

Total contribution margin $1,400,000 $480,000

Less: Fixed costs $800,000 $400,000

Net Profit $600,000 $80,000

Total profit in this case is $680,000.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.