Comprehensive Analysis: Accounting for Managers Assignment - Finance

VerifiedAdded on 2020/02/24

|7

|1544

|104

Homework Assignment

AI Summary

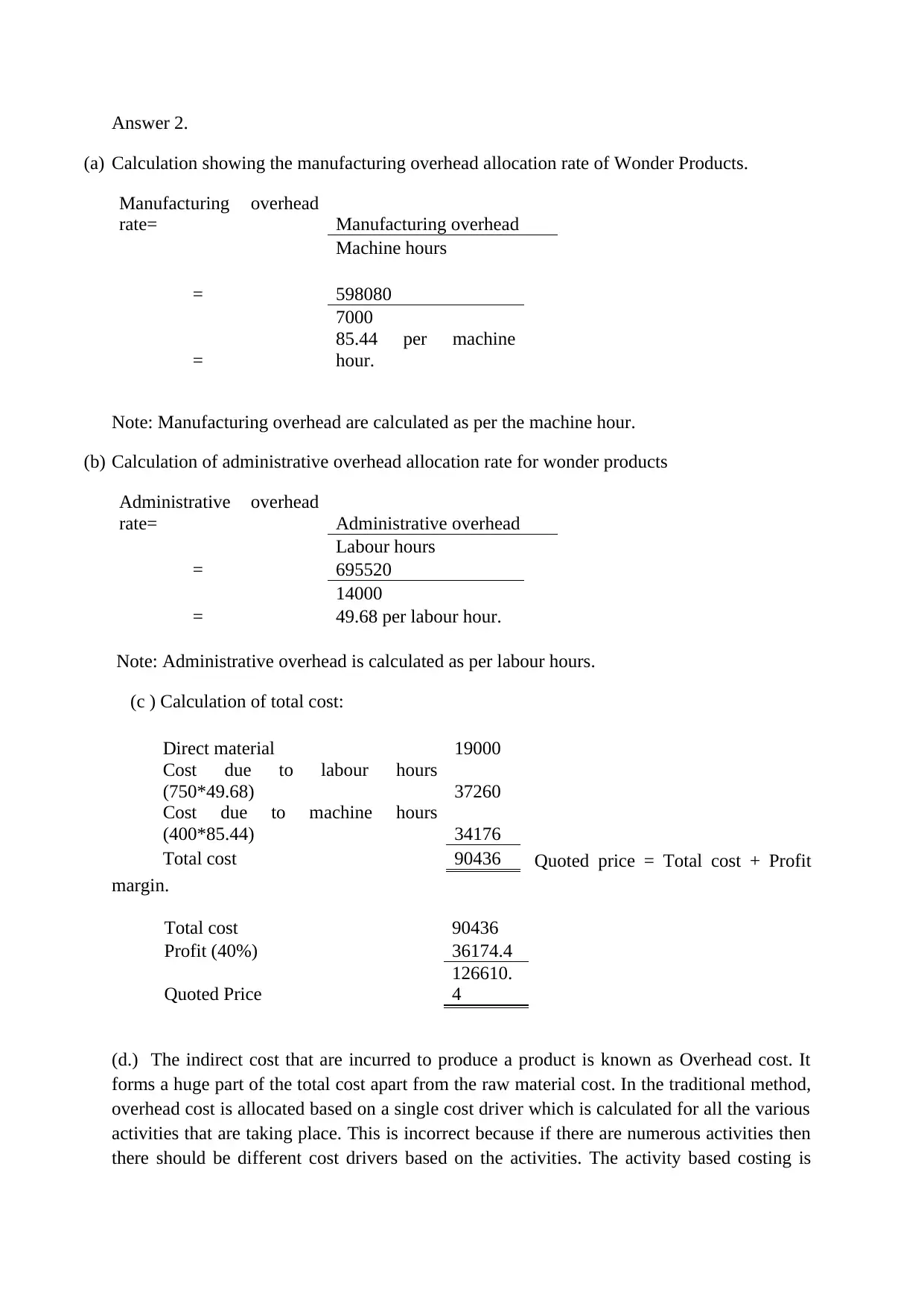

This assignment solution for Accounting for Managers delves into various aspects of financial and cost accounting. It begins by explaining the importance of financial budgets, contrasting fixed and flexible budgets, and demonstrating their application with examples. The solution then explores cash budgets, sales, production, and raw material budgets, highlighting their significance in financial planning. It also discusses the cash cycle, operating cycle, and working capital ratios, emphasizing their role in financial management. Furthermore, the assignment addresses the importance of accounting in both private and government organizations. The solution also covers costing systems, overhead allocation, and the advantages of predetermined overhead rates, providing calculations and explanations to support the concepts discussed. The references include key accounting textbooks and resources.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.