ACCG925: Audit Reporting Changes and Impact on Audit Practice

VerifiedAdded on 2019/11/12

|9

|1237

|277

Report

AI Summary

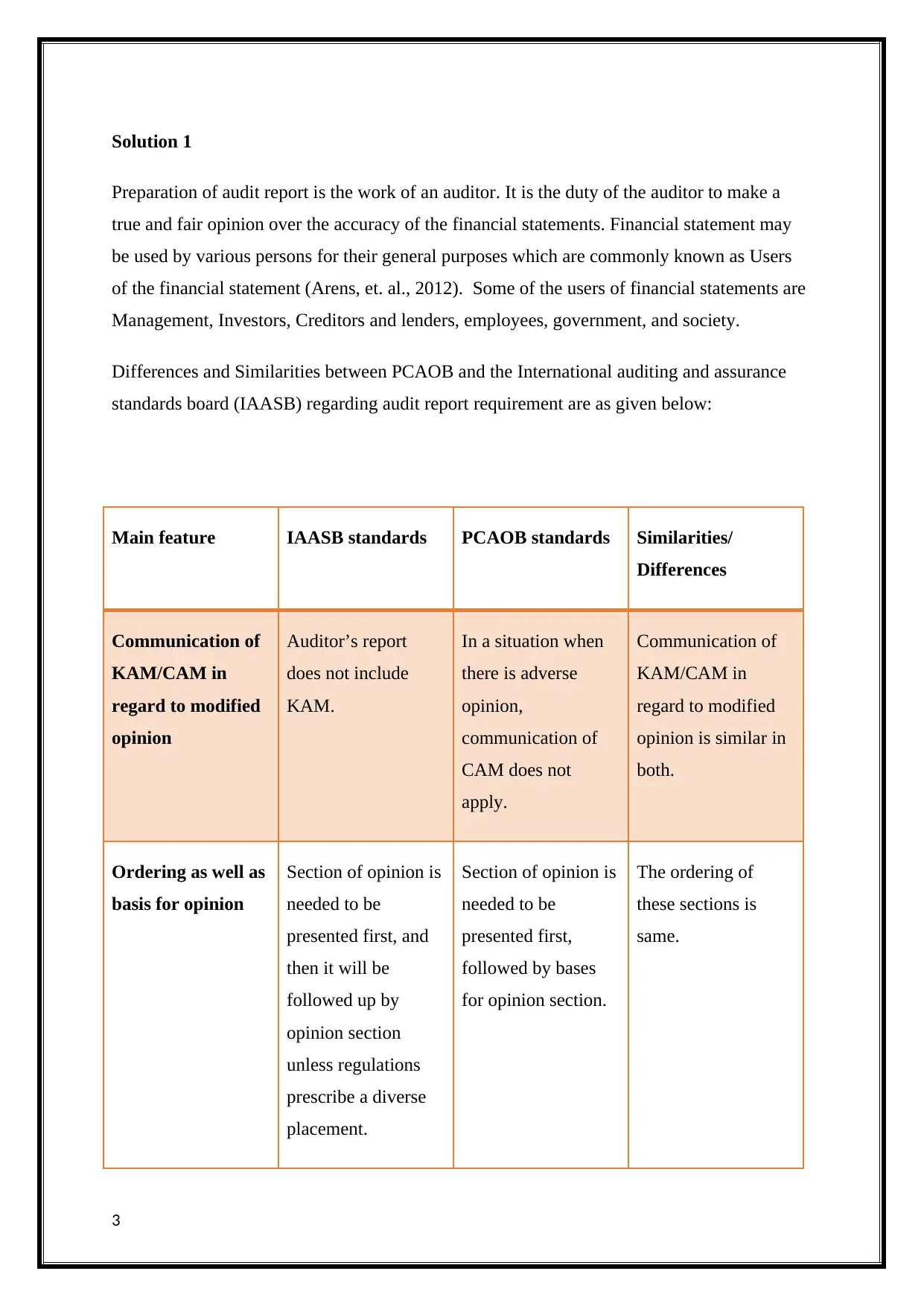

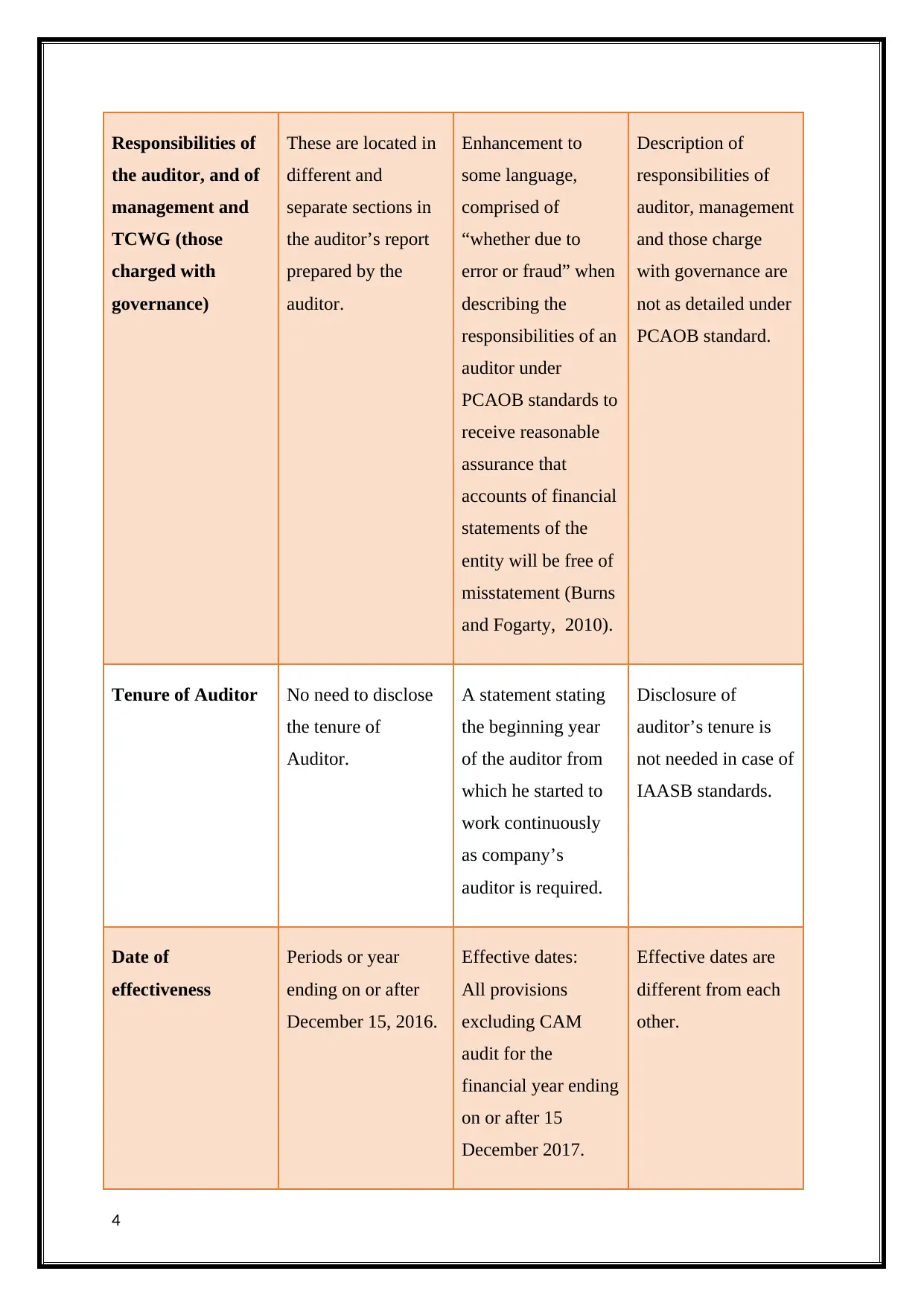

This individual assignment for ACCG925 analyzes the key changes in audit reporting, focusing on the similarities and differences between the Public Company Accounting Oversight Board (PCAOB) and the International Auditing and Assurance Standards Board (IAASB) auditing reporting requirements. The report examines the communication of Key Audit Matters (KAM) and Critical Audit Matters (CAM), the ordering of opinion sections, and the responsibilities of auditors, management, and those charged with governance. It explores the reasons behind the changes, including the going concern concept, and assesses their likely impact on audit practice. The assignment also highlights the effective dates of the changes and provides an overview of the auditor's responsibilities and the importance of audited financial statements for stakeholders. The report references several academic sources, including Arens et al. (2012), Burns and Fogarty (2010), Carson et al. (2012), Messier Jr. et al. (2015), and the PCAOB (2011) to support its analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.