Accounting: Liability, Bad Debts, Taxes, Repairs

Added on 2023-03-17

26 Pages2344 Words100 Views

ACCOUNTING 1

ACCOUNTING

ACCOUNTING

ACCOUNTING 2

Answer 1:

Part 1:

A liability is something which has some present obligation for the company and which also

entails an outflow of the resources. This are connected with the future economic benefits that

flow out of the company. A liability would be recorded in the books of accounts in case there

is a probability of an event to take place and it is more than probable that the event would

happen. In the case, wherein there is no existence of the present obligation, then the company

shall record that expense as a contingent liability. In the cases, wherein there are some similar

obligations of an outflow if the expenses such as the product warranties or such similar

obligations, then the company shall keep a provision for them. The company shall record the

expense as provision when there is a probability that there should be an outflow of the money

for the company in future (AASB, 2019).

Hence, in such a case the warranty expense shall be provided for in the financial statements.

The accounting entry for it would be credit profit and loss account and debit provision for

warranty with an amount of $34,400. The disclosure for this would be the provision for

warranty amount in the notes to the financial statements.

Part 2:

The company would always create a provision for the bad debts out of its total amount of the

accounts receivables. The provision for doubtful expense would be debited if there is any

actual bad debt expense which occurs. Hence, in such a case the entry would be debit

provision for doubtful debts and credit bad debt expense with an amount of $380,000. The

disclosure would be the fact of the actual bad debt loss that the company has suffered during

the year.

Part 3:

Answer 1:

Part 1:

A liability is something which has some present obligation for the company and which also

entails an outflow of the resources. This are connected with the future economic benefits that

flow out of the company. A liability would be recorded in the books of accounts in case there

is a probability of an event to take place and it is more than probable that the event would

happen. In the case, wherein there is no existence of the present obligation, then the company

shall record that expense as a contingent liability. In the cases, wherein there are some similar

obligations of an outflow if the expenses such as the product warranties or such similar

obligations, then the company shall keep a provision for them. The company shall record the

expense as provision when there is a probability that there should be an outflow of the money

for the company in future (AASB, 2019).

Hence, in such a case the warranty expense shall be provided for in the financial statements.

The accounting entry for it would be credit profit and loss account and debit provision for

warranty with an amount of $34,400. The disclosure for this would be the provision for

warranty amount in the notes to the financial statements.

Part 2:

The company would always create a provision for the bad debts out of its total amount of the

accounts receivables. The provision for doubtful expense would be debited if there is any

actual bad debt expense which occurs. Hence, in such a case the entry would be debit

provision for doubtful debts and credit bad debt expense with an amount of $380,000. The

disclosure would be the fact of the actual bad debt loss that the company has suffered during

the year.

Part 3:

ACCOUNTING 3

If the government of the country in which the company operates goes inti change the rate at

which the taxes are paid, then there would be disclosure requirement for the company. This is

mainly due to the fact that the company would have the pay the taxes at the changed tax rate

and that would be done in the end of the year. The company could though reduce its

provision for taxes as per the amended tax rate. In the given case, the company would reduce

its provision as per the changed tax rate from 30 to 28%.

There is no requirement of any additional disclosure for the company.

Part 4:

Whenever any amount of expense is incurred for an asset, then it has to be determined if that

expense would go on to increase the productivity or the life of the asset. In case, as the result

of those repairs, the life of the asset or its productivity improves, then that would be

capitalised in the cost of the asset. This means that on that expense, the company shall charge

depreciation. But if that expense merely provides some minor changes in the machine, then

that would be charged as against the profit and loss in the current month. The expense shall

be considered as repairs. The relevant disclosure in this case shall be the amount charged as

an expense or the capitalised amount. The relevant journal entry shall be repairs expense

debit with profit and loss credit and in case of capitalisation, machine or asset account debit

with profit and cash credit (IAS plus, 2019).

Journal entries:

Repairs expense Dr 22,000

To Trailer 22,000

Income tax receivable Dr 6,300

To Income tax 6,300

If the government of the country in which the company operates goes inti change the rate at

which the taxes are paid, then there would be disclosure requirement for the company. This is

mainly due to the fact that the company would have the pay the taxes at the changed tax rate

and that would be done in the end of the year. The company could though reduce its

provision for taxes as per the amended tax rate. In the given case, the company would reduce

its provision as per the changed tax rate from 30 to 28%.

There is no requirement of any additional disclosure for the company.

Part 4:

Whenever any amount of expense is incurred for an asset, then it has to be determined if that

expense would go on to increase the productivity or the life of the asset. In case, as the result

of those repairs, the life of the asset or its productivity improves, then that would be

capitalised in the cost of the asset. This means that on that expense, the company shall charge

depreciation. But if that expense merely provides some minor changes in the machine, then

that would be charged as against the profit and loss in the current month. The expense shall

be considered as repairs. The relevant disclosure in this case shall be the amount charged as

an expense or the capitalised amount. The relevant journal entry shall be repairs expense

debit with profit and loss credit and in case of capitalisation, machine or asset account debit

with profit and cash credit (IAS plus, 2019).

Journal entries:

Repairs expense Dr 22,000

To Trailer 22,000

Income tax receivable Dr 6,300

To Income tax 6,300

ACCOUNTING 4

Accumulated depreciation Dr 1,000

To Depreciation expense 1,000

Answer 2:

The following are the relevant calculations:

Date

31-Mar-19 Bank A/c

D

r.

1

6,

00

,0

00

To Preference Share Application A/c

Cr

.

16,

00,

000

(Being share application money received

on 800,000 shares @ $2 per share)

31-Mar-19 Bank A/c

D

r.

8

8,

00

,0

00

To Ordinary Share Application A/c Cr

. 88,

Accumulated depreciation Dr 1,000

To Depreciation expense 1,000

Answer 2:

The following are the relevant calculations:

Date

31-Mar-19 Bank A/c

D

r.

1

6,

00

,0

00

To Preference Share Application A/c

Cr

.

16,

00,

000

(Being share application money received

on 800,000 shares @ $2 per share)

31-Mar-19 Bank A/c

D

r.

8

8,

00

,0

00

To Ordinary Share Application A/c Cr

. 88,

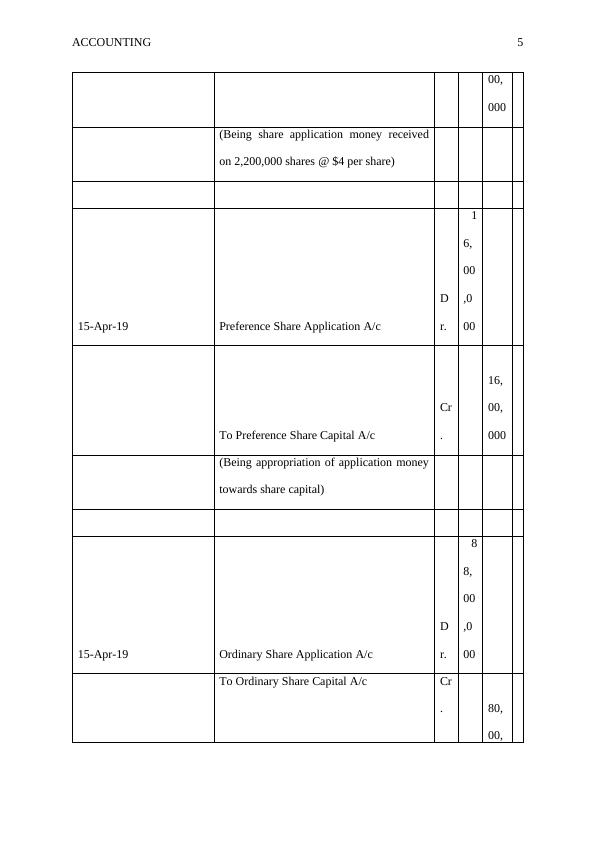

ACCOUNTING 5

00,

000

(Being share application money received

on 2,200,000 shares @ $4 per share)

15-Apr-19 Preference Share Application A/c

D

r.

1

6,

00

,0

00

To Preference Share Capital A/c

Cr

.

16,

00,

000

(Being appropriation of application money

towards share capital)

15-Apr-19 Ordinary Share Application A/c

D

r.

8

8,

00

,0

00

To Ordinary Share Capital A/c Cr

. 80,

00,

00,

000

(Being share application money received

on 2,200,000 shares @ $4 per share)

15-Apr-19 Preference Share Application A/c

D

r.

1

6,

00

,0

00

To Preference Share Capital A/c

Cr

.

16,

00,

000

(Being appropriation of application money

towards share capital)

15-Apr-19 Ordinary Share Application A/c

D

r.

8

8,

00

,0

00

To Ordinary Share Capital A/c Cr

. 80,

00,

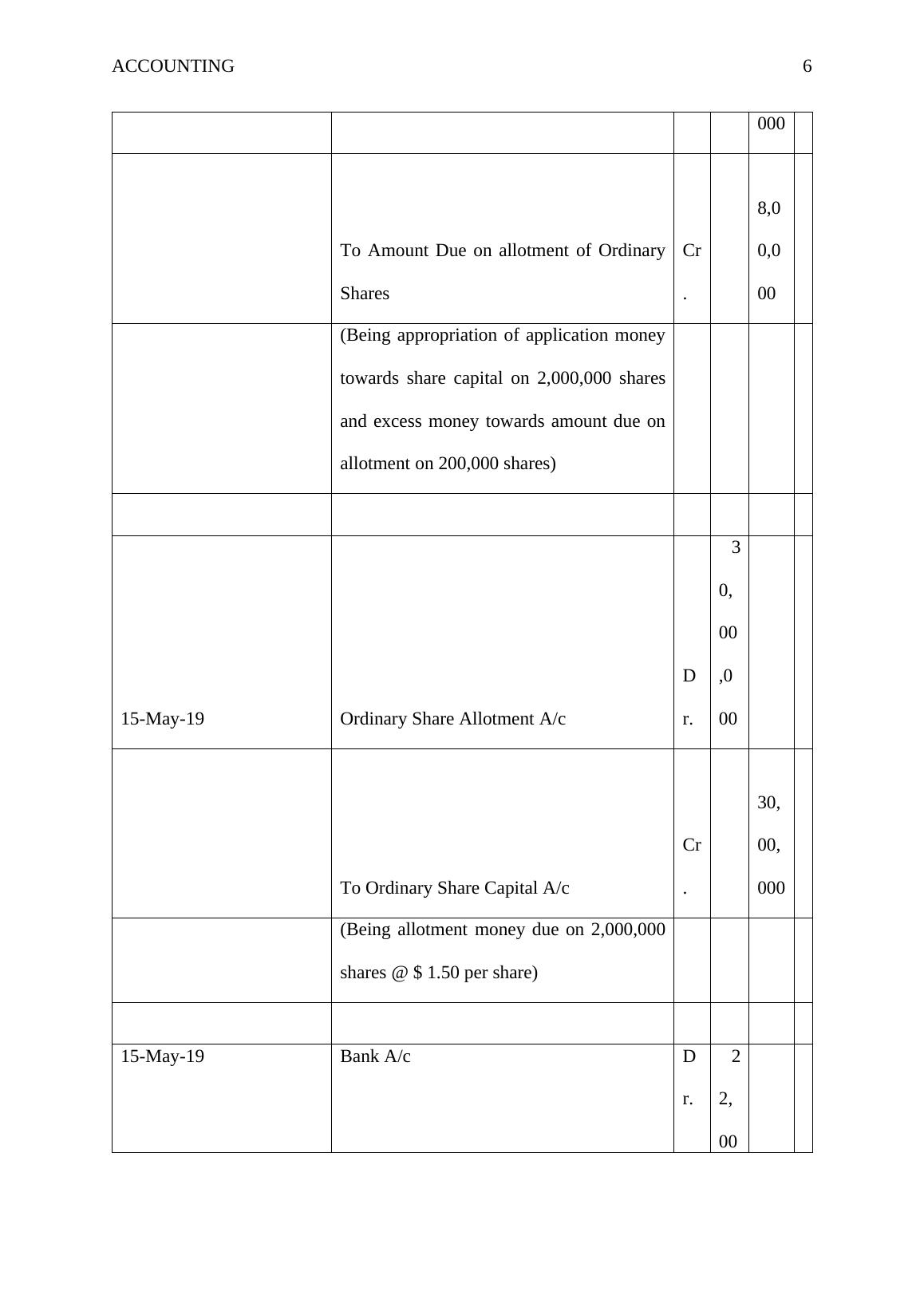

ACCOUNTING 6

000

To Amount Due on allotment of Ordinary

Shares

Cr

.

8,0

0,0

00

(Being appropriation of application money

towards share capital on 2,000,000 shares

and excess money towards amount due on

allotment on 200,000 shares)

15-May-19 Ordinary Share Allotment A/c

D

r.

3

0,

00

,0

00

To Ordinary Share Capital A/c

Cr

.

30,

00,

000

(Being allotment money due on 2,000,000

shares @ $ 1.50 per share)

15-May-19 Bank A/c D

r.

2

2,

00

000

To Amount Due on allotment of Ordinary

Shares

Cr

.

8,0

0,0

00

(Being appropriation of application money

towards share capital on 2,000,000 shares

and excess money towards amount due on

allotment on 200,000 shares)

15-May-19 Ordinary Share Allotment A/c

D

r.

3

0,

00

,0

00

To Ordinary Share Capital A/c

Cr

.

30,

00,

000

(Being allotment money due on 2,000,000

shares @ $ 1.50 per share)

15-May-19 Bank A/c D

r.

2

2,

00

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Accounting: Provision, Change in Accounting Estimate, Income Taxes, Fixed Assetslg...

|29

|2847

|478

Calculation of Taxable Incomelg...

|11

|1807

|53

Financial Accountinglg...

|13

|609

|67

Financial Accounting: Provisions, Contingent Liabilities, and Contingent Assetslg...

|11

|1388

|41

Corporate Accounting System Assignmentlg...

|16

|2650

|111

Assignment On Corporate Accounting of DJB limitedlg...

|15

|2434

|193