Taxation and Consolidation: Green Bay Ltd Analysis Assignment

VerifiedAdded on 2020/03/23

|11

|1807

|53

Homework Assignment

AI Summary

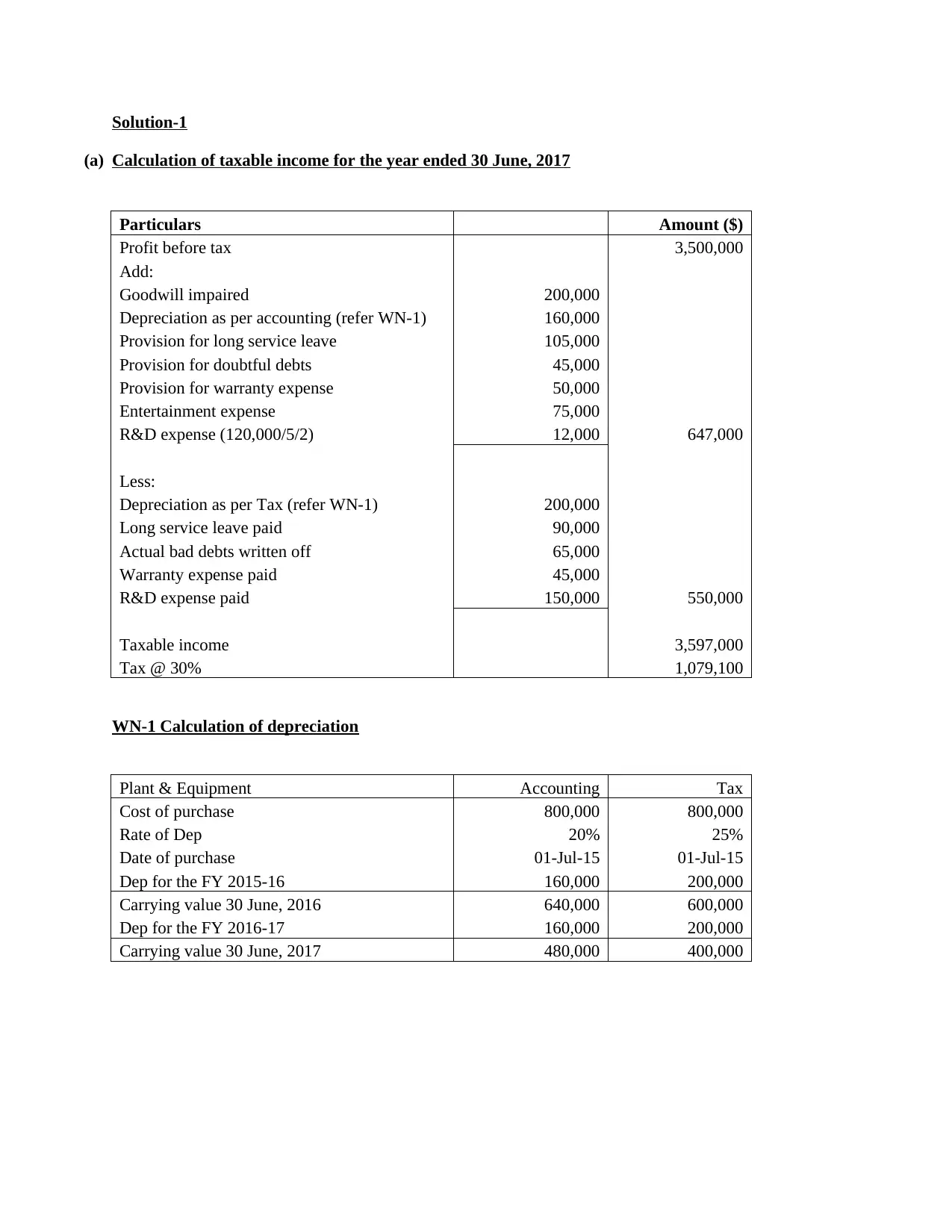

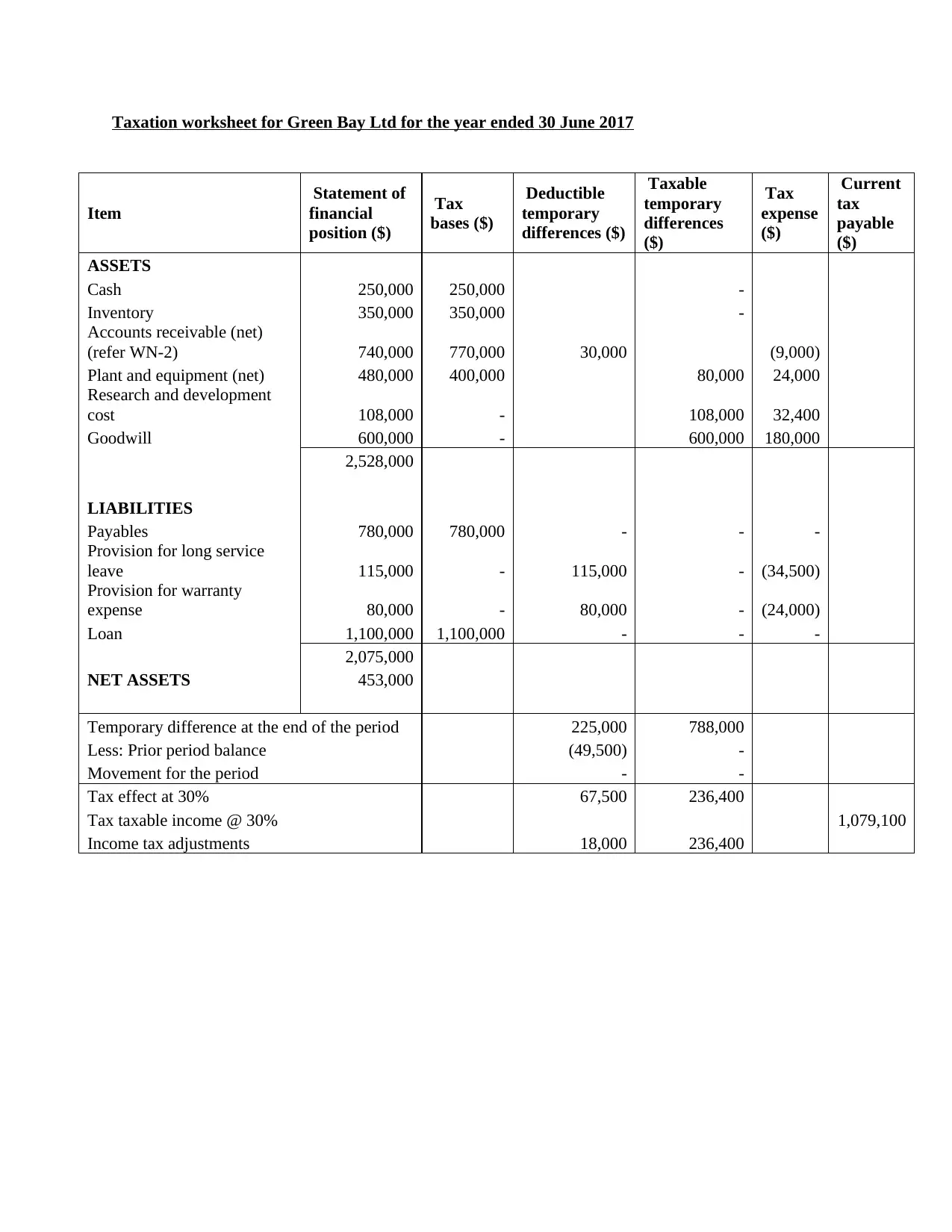

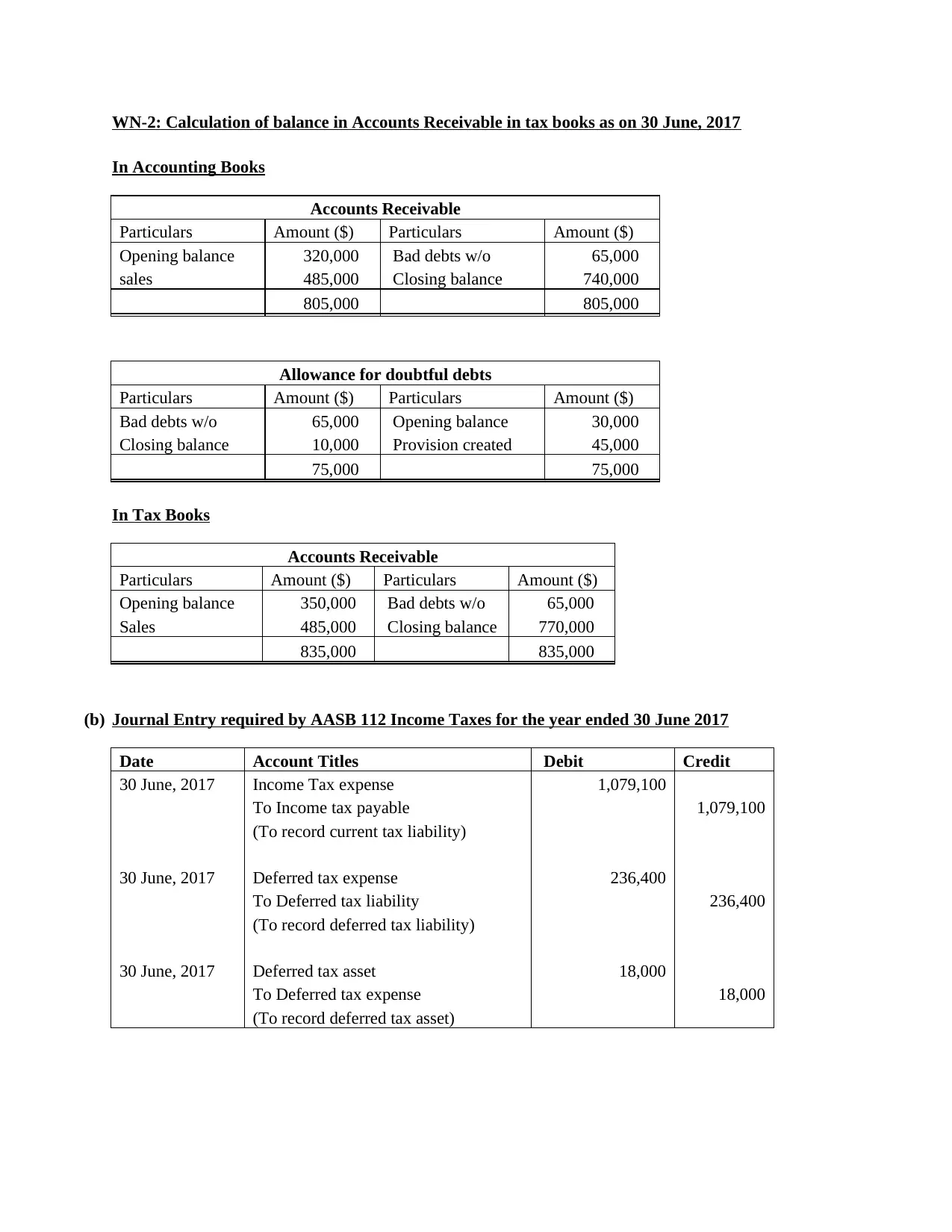

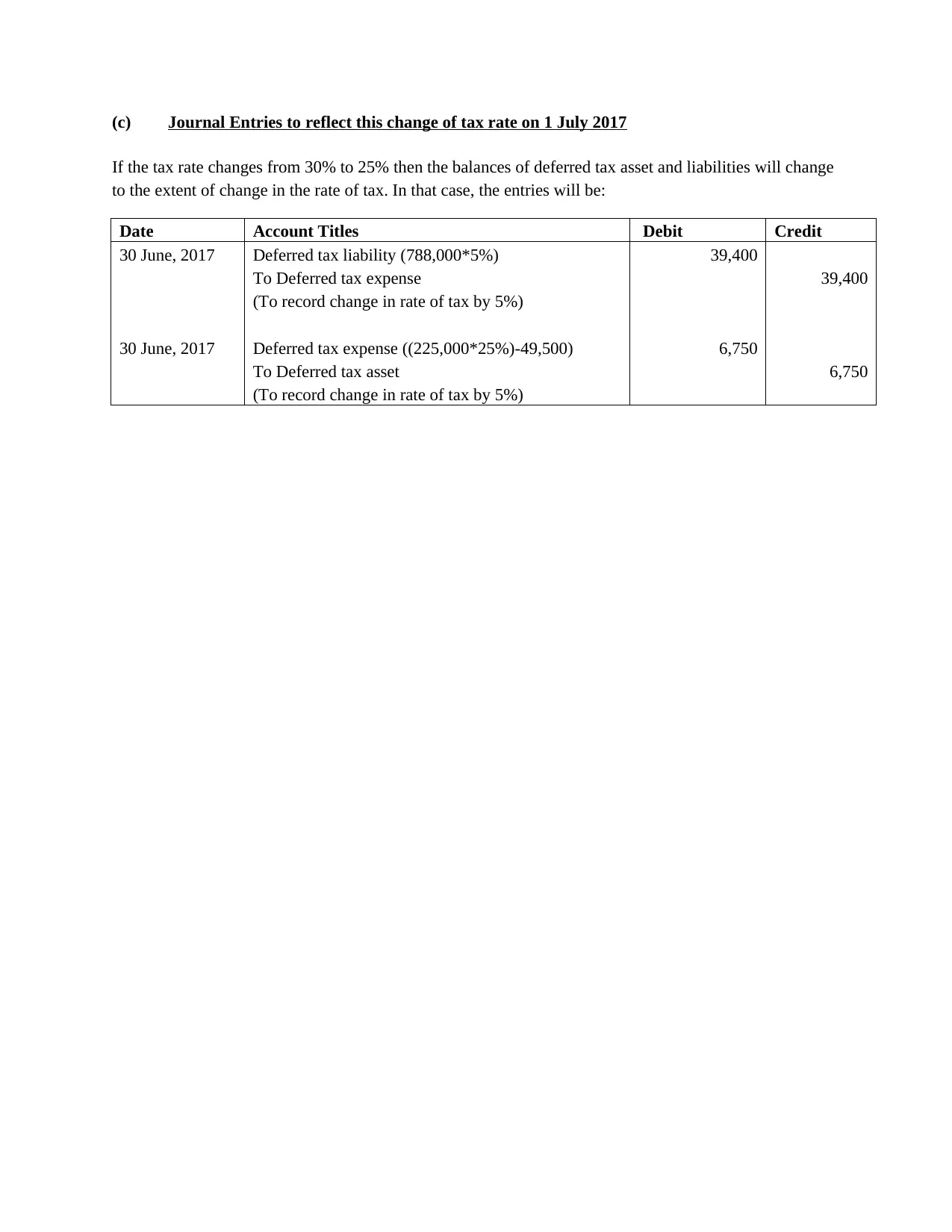

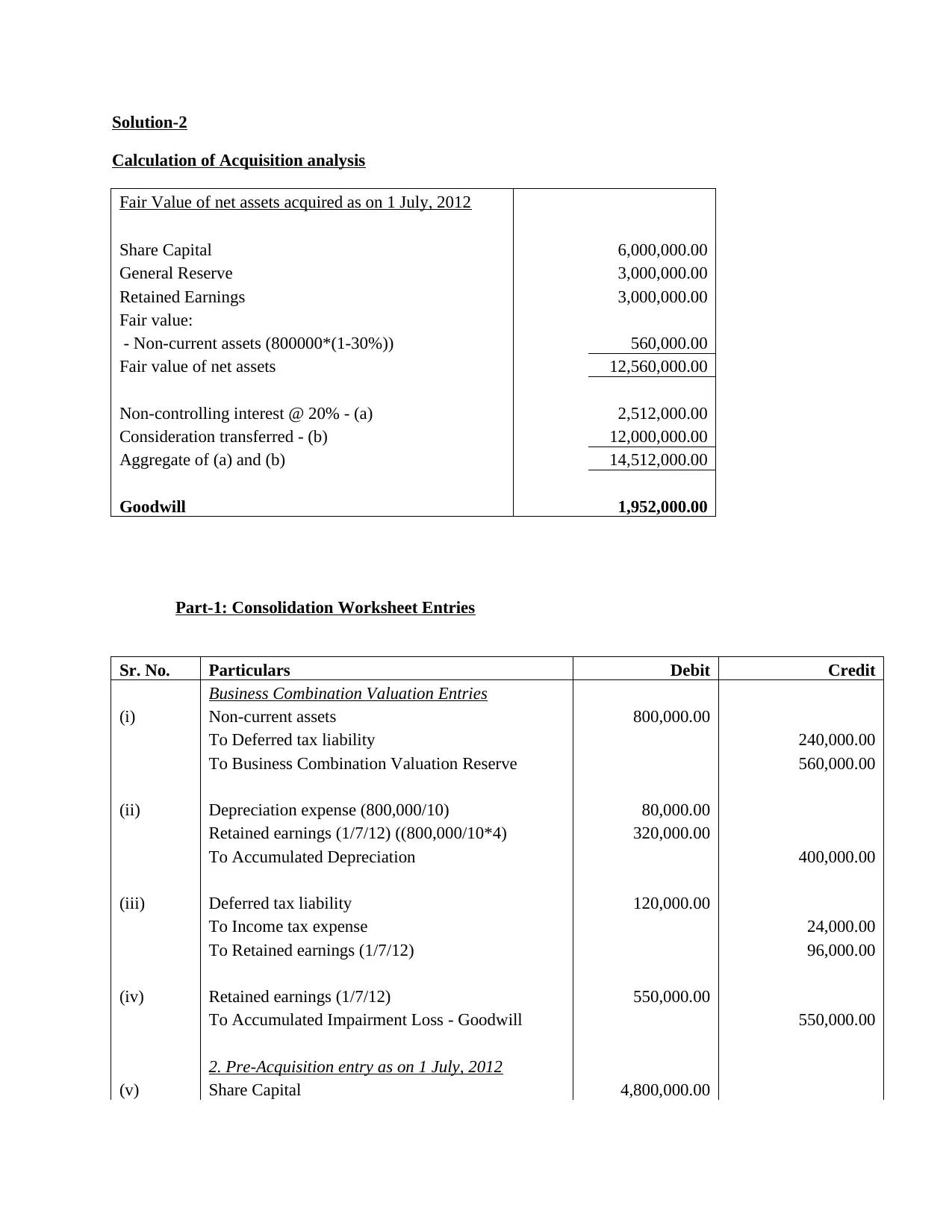

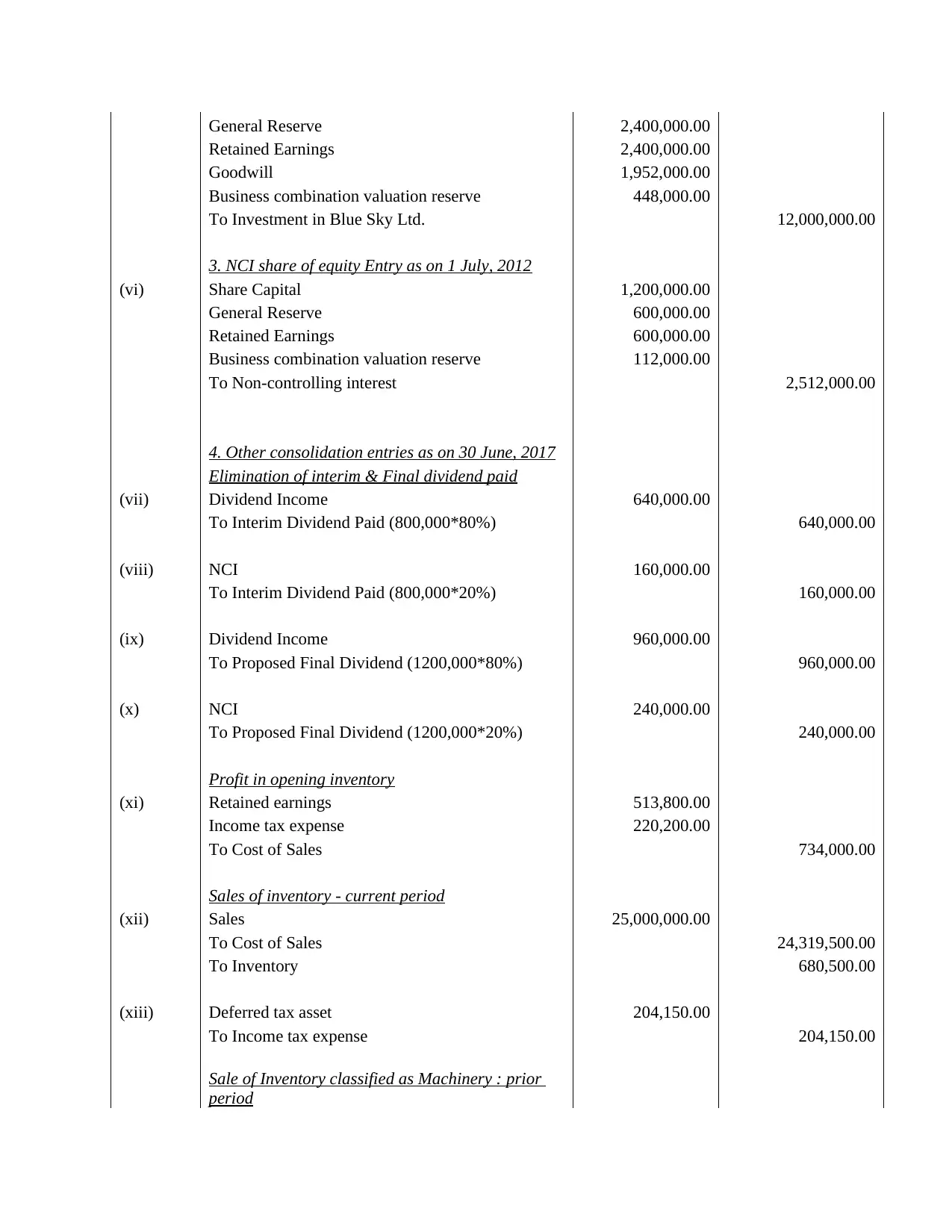

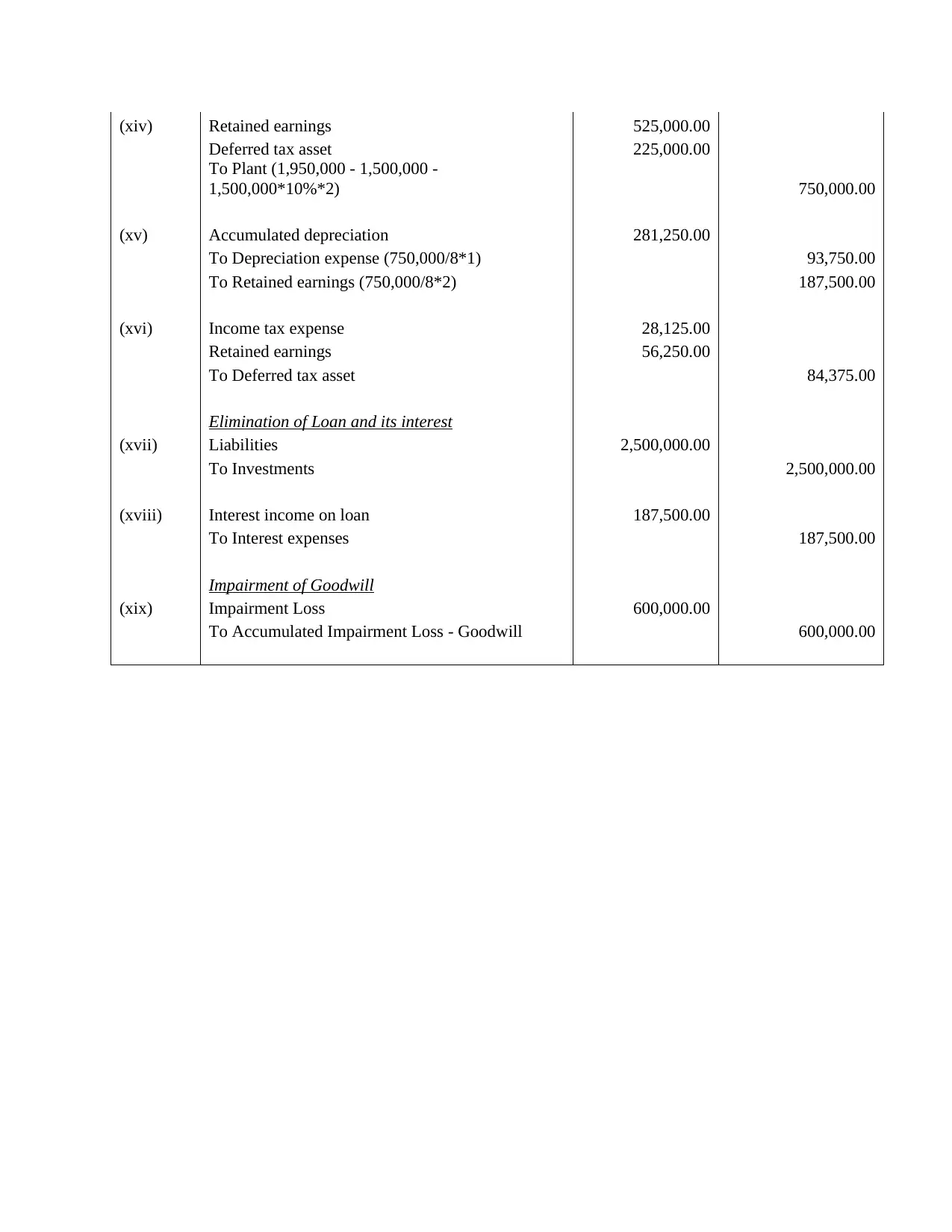

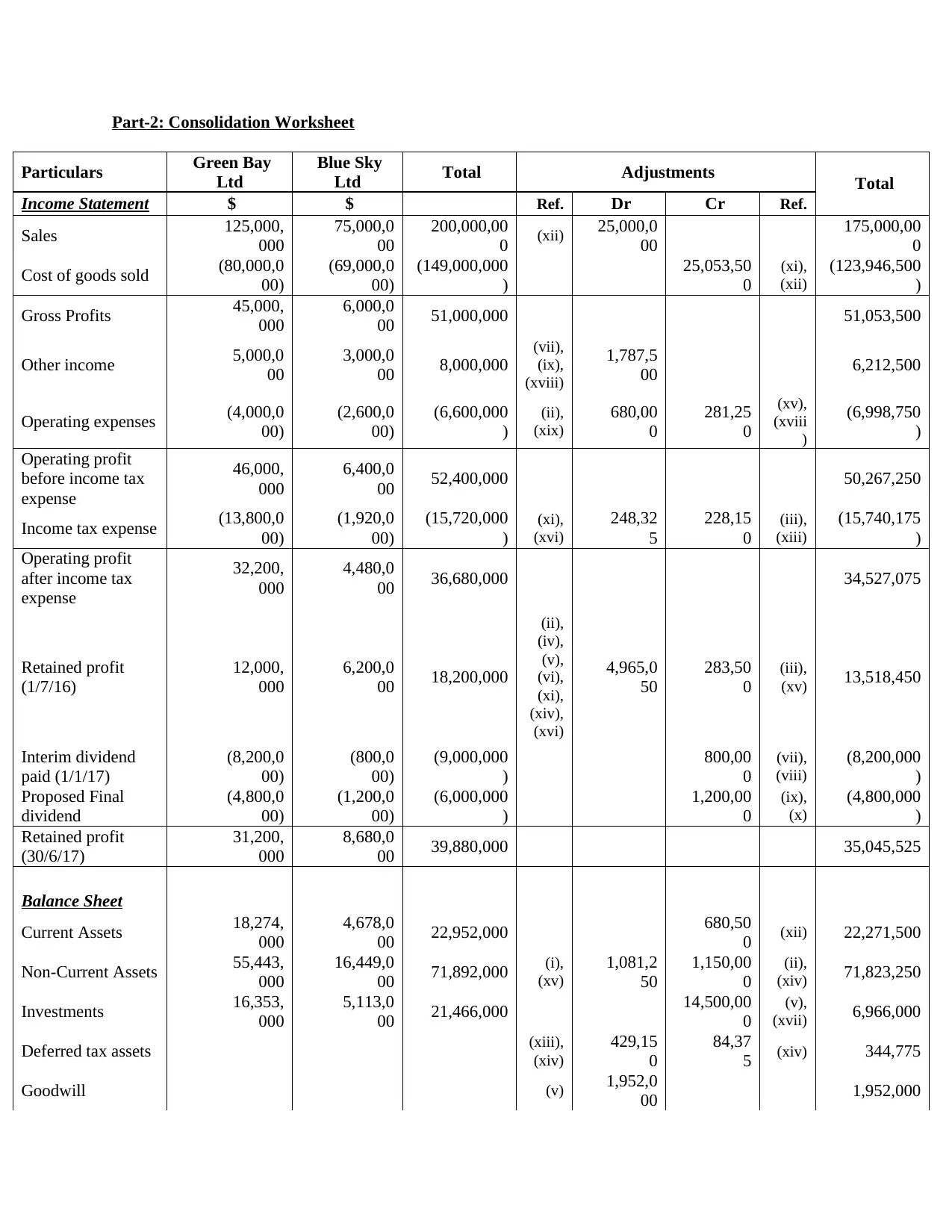

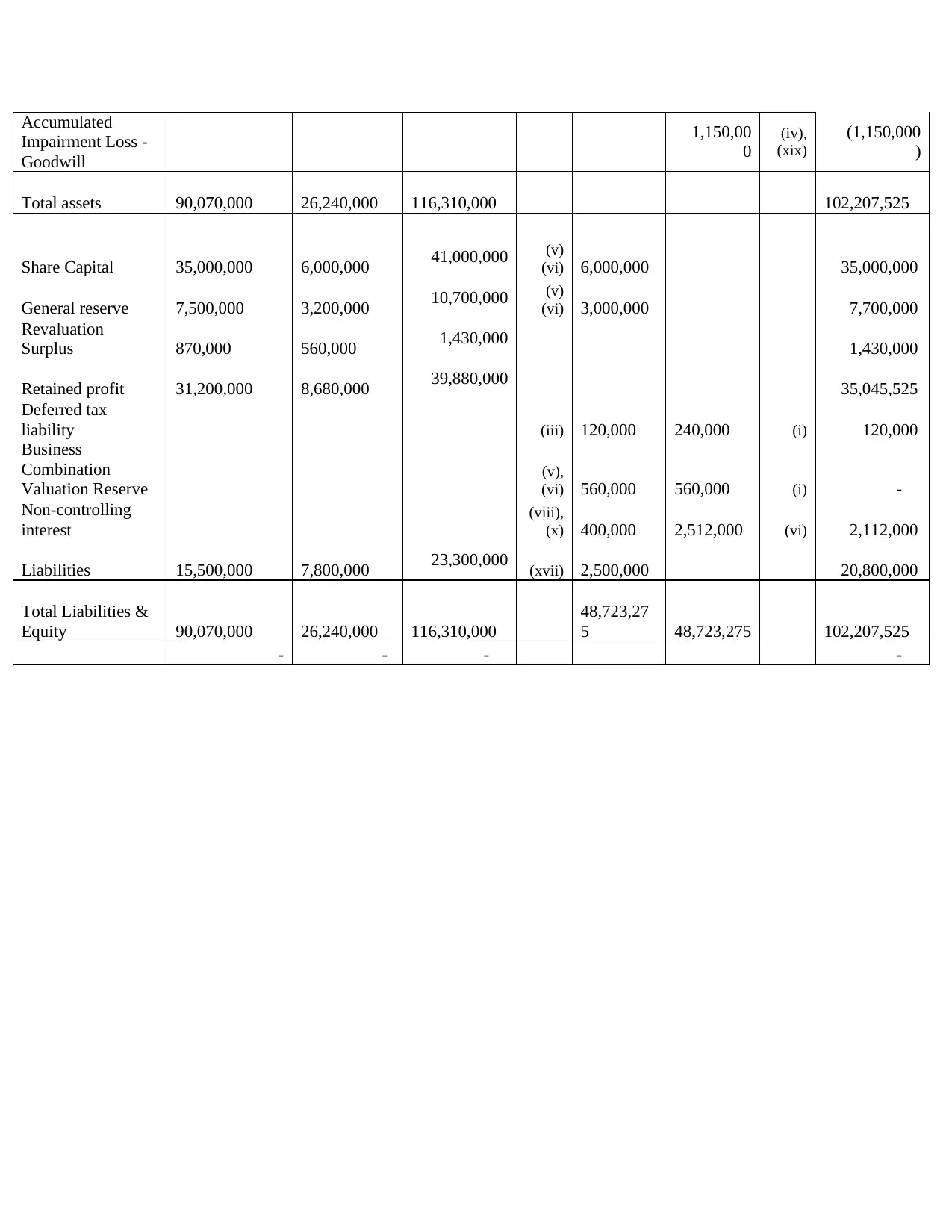

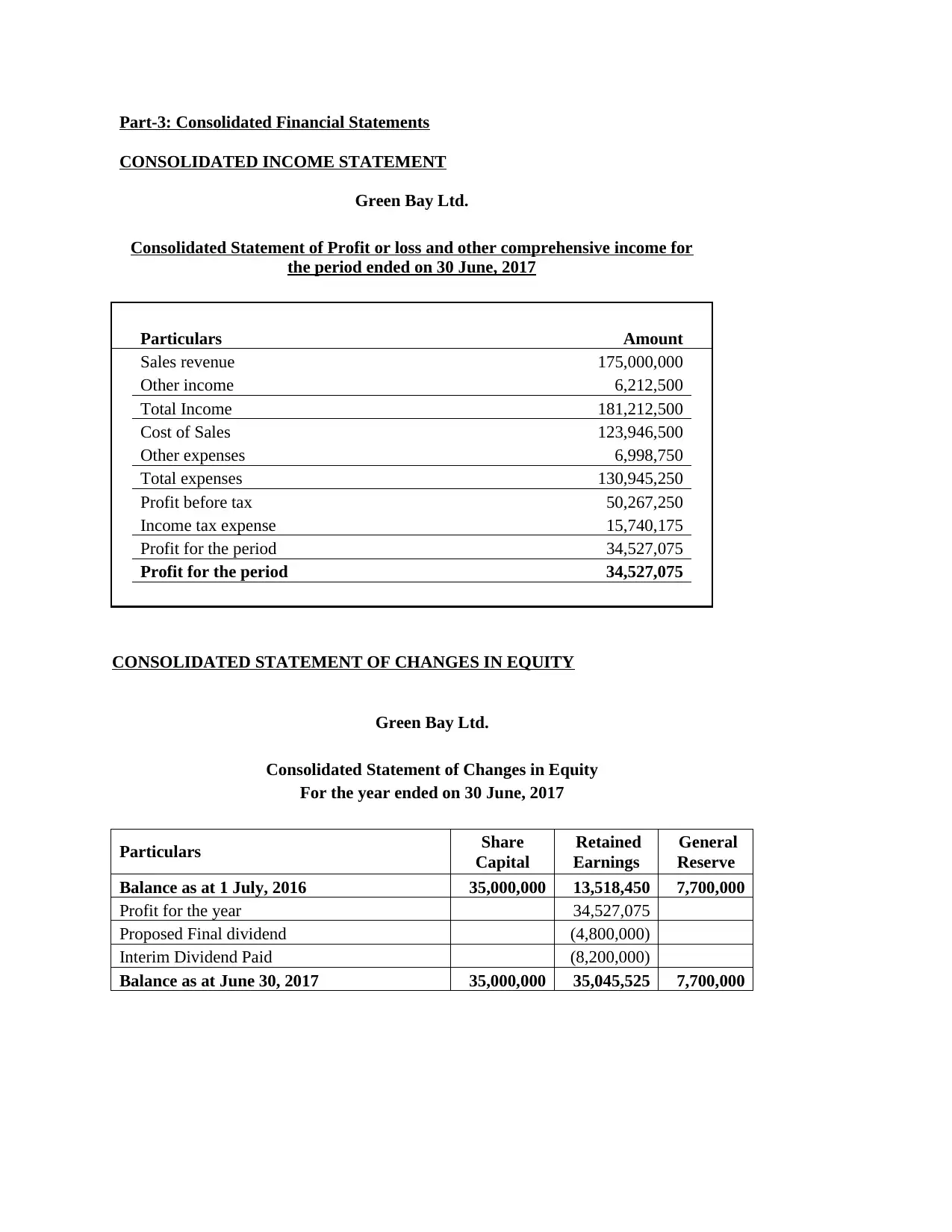

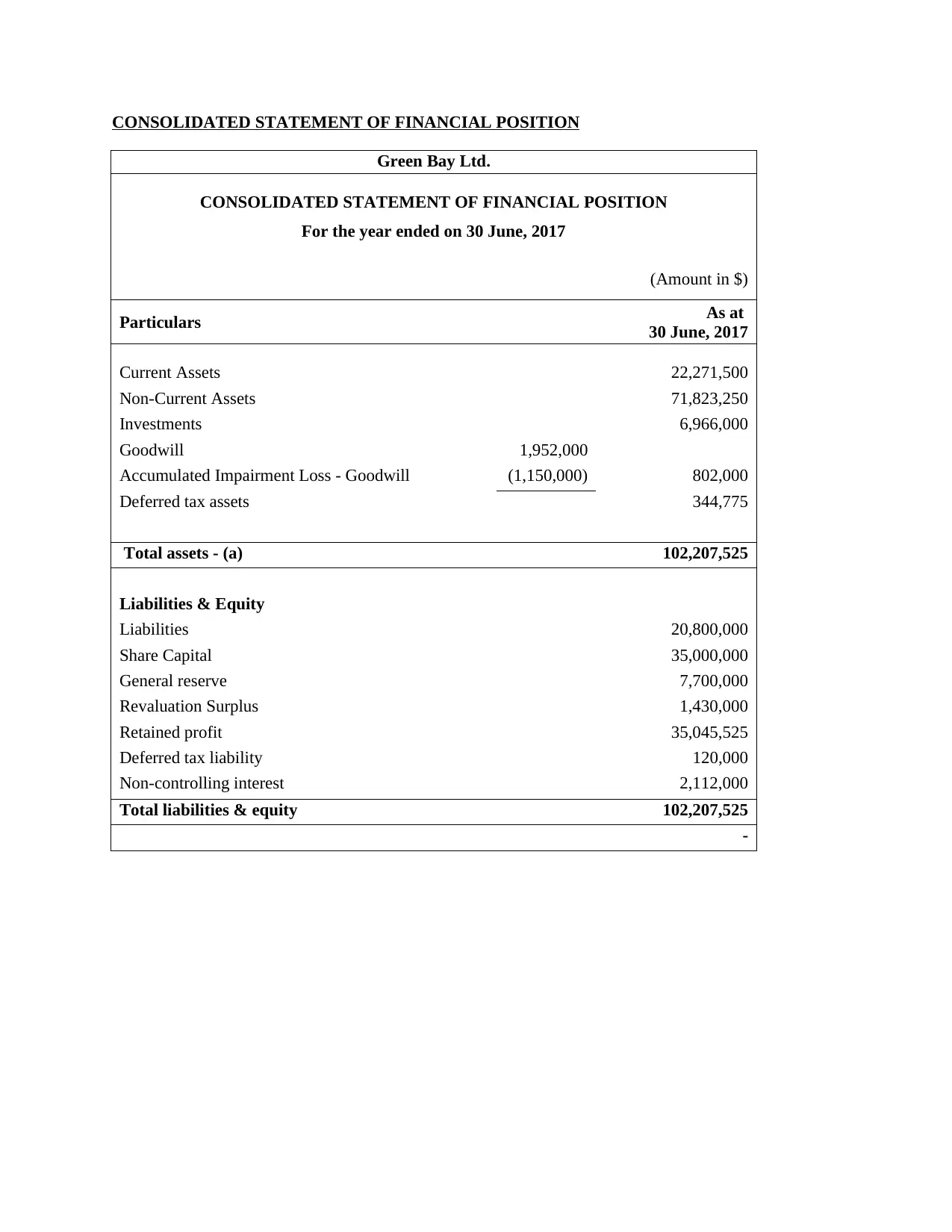

This assignment presents two comprehensive solutions. The first solution calculates the taxable income for Green Bay Ltd. for the year ended June 30, 2017. It meticulously adjusts the profit before tax by adding and subtracting various items such as depreciation, provisions, and research and development expenses to arrive at the final taxable income. The solution includes a detailed depreciation calculation worksheet and a taxation worksheet outlining temporary differences, tax bases, and tax expenses. It also provides the journal entries required by AASB 112 Income Taxes, including entries for current and deferred tax liabilities, and adjustments for a change in the tax rate. The second solution focuses on the acquisition analysis of Blue Sky Ltd. by Green Bay Ltd. as of July 1, 2012. It calculates the fair value of net assets acquired, goodwill, and non-controlling interest. The solution includes business combination valuation entries, pre-acquisition entries, and consolidation entries for dividends, inventory, and intercompany transactions. It also provides a consolidation worksheet and consolidated financial statements, including an income statement, statement of changes in equity, and statement of financial position. The analysis reflects adjustments for depreciation, impairment, and deferred tax, providing a complete picture of the consolidated financial position.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.