Inventory Valuation Methods in Accounting

VerifiedAdded on 2023/03/17

|27

|3113

|38

AI Summary

This article discusses the FIFO and weighted average methods of inventory valuation in accounting. It explains how these methods work and their impact on the value of inventory. The article also highlights the benefits of using cloud-based accounting software and the importance of internal controls in preventing fraud.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING 1

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING 2

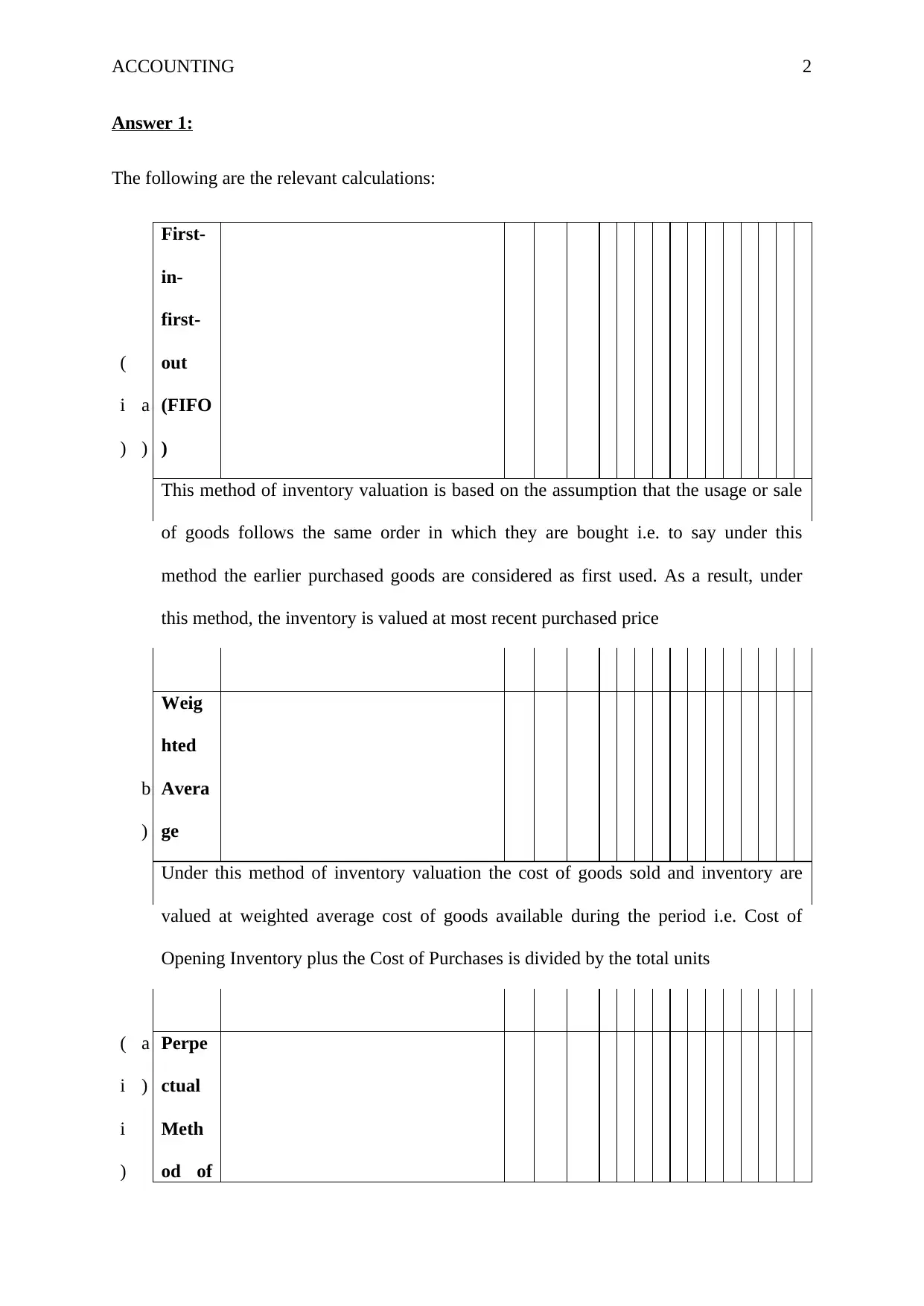

Answer 1:

The following are the relevant calculations:

(

i

)

a

)

First-

in-

first-

out

(FIFO

)

This method of inventory valuation is based on the assumption that the usage or sale

of goods follows the same order in which they are bought i.e. to say under this

method the earlier purchased goods are considered as first used. As a result, under

this method, the inventory is valued at most recent purchased price

b

)

Weig

hted

Avera

ge

Under this method of inventory valuation the cost of goods sold and inventory are

valued at weighted average cost of goods available during the period i.e. Cost of

Opening Inventory plus the Cost of Purchases is divided by the total units

(

i

i

)

a

)

Perpe

ctual

Meth

od of

Answer 1:

The following are the relevant calculations:

(

i

)

a

)

First-

in-

first-

out

(FIFO

)

This method of inventory valuation is based on the assumption that the usage or sale

of goods follows the same order in which they are bought i.e. to say under this

method the earlier purchased goods are considered as first used. As a result, under

this method, the inventory is valued at most recent purchased price

b

)

Weig

hted

Avera

ge

Under this method of inventory valuation the cost of goods sold and inventory are

valued at weighted average cost of goods available during the period i.e. Cost of

Opening Inventory plus the Cost of Purchases is divided by the total units

(

i

i

)

a

)

Perpe

ctual

Meth

od of

ACCOUNTING 3

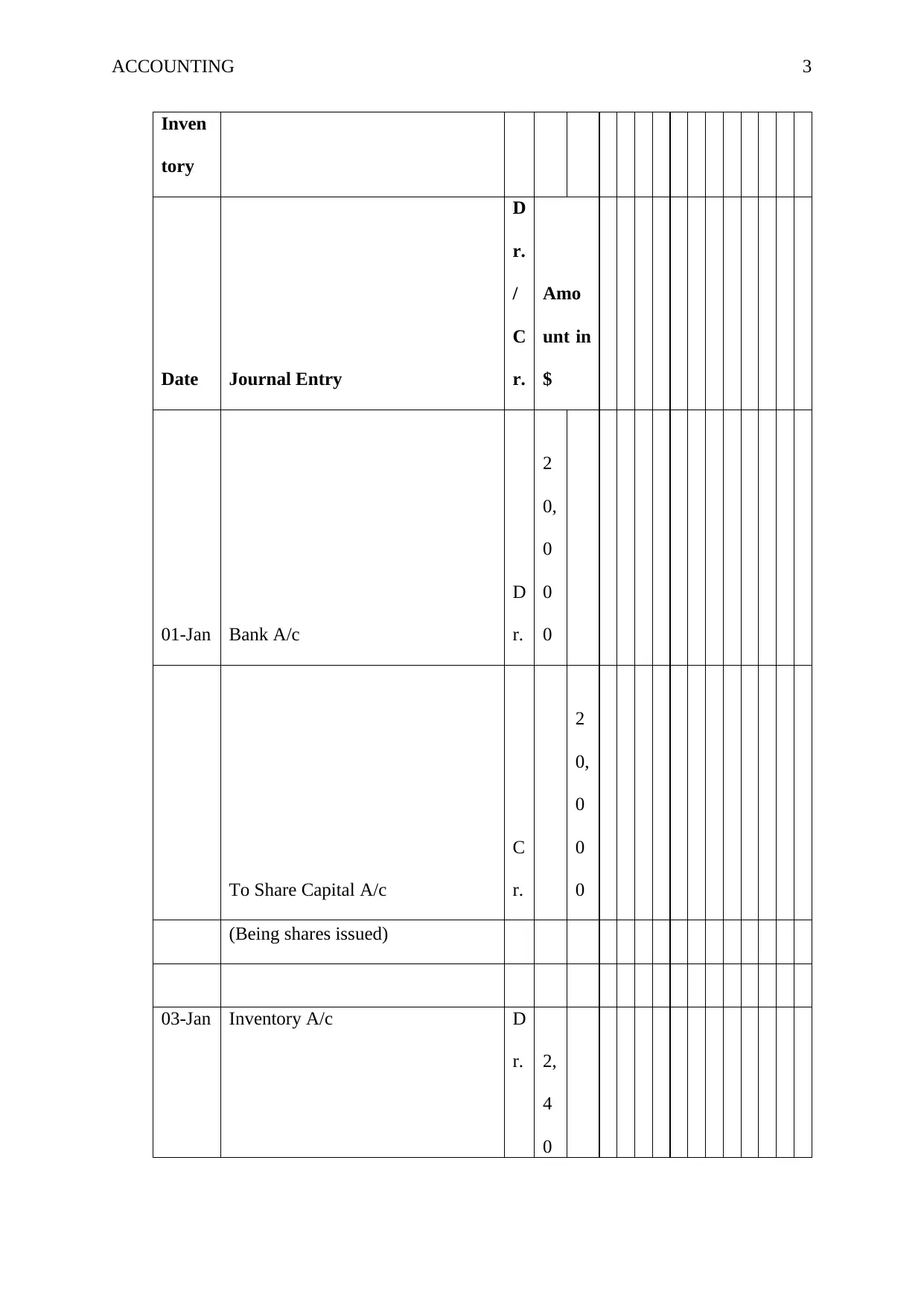

Inven

tory

Date Journal Entry

D

r.

/

C

r.

Amo

unt in

$

01-Jan Bank A/c

D

r.

2

0,

0

0

0

To Share Capital A/c

C

r.

2

0,

0

0

0

(Being shares issued)

03-Jan Inventory A/c D

r. 2,

4

0

Inven

tory

Date Journal Entry

D

r.

/

C

r.

Amo

unt in

$

01-Jan Bank A/c

D

r.

2

0,

0

0

0

To Share Capital A/c

C

r.

2

0,

0

0

0

(Being shares issued)

03-Jan Inventory A/c D

r. 2,

4

0

ACCOUNTING 4

0

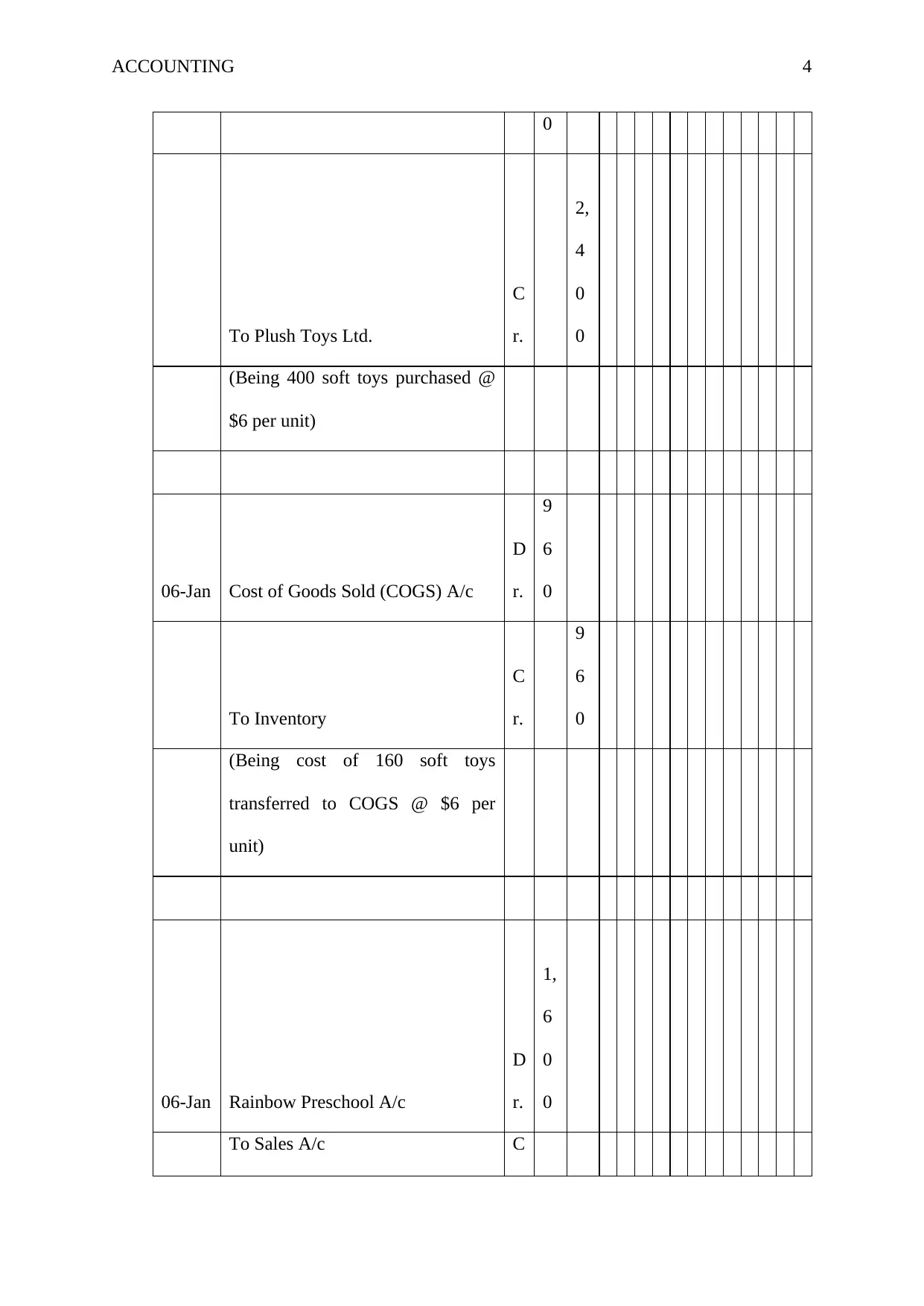

To Plush Toys Ltd.

C

r.

2,

4

0

0

(Being 400 soft toys purchased @

$6 per unit)

06-Jan Cost of Goods Sold (COGS) A/c

D

r.

9

6

0

To Inventory

C

r.

9

6

0

(Being cost of 160 soft toys

transferred to COGS @ $6 per

unit)

06-Jan Rainbow Preschool A/c

D

r.

1,

6

0

0

To Sales A/c C

0

To Plush Toys Ltd.

C

r.

2,

4

0

0

(Being 400 soft toys purchased @

$6 per unit)

06-Jan Cost of Goods Sold (COGS) A/c

D

r.

9

6

0

To Inventory

C

r.

9

6

0

(Being cost of 160 soft toys

transferred to COGS @ $6 per

unit)

06-Jan Rainbow Preschool A/c

D

r.

1,

6

0

0

To Sales A/c C

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

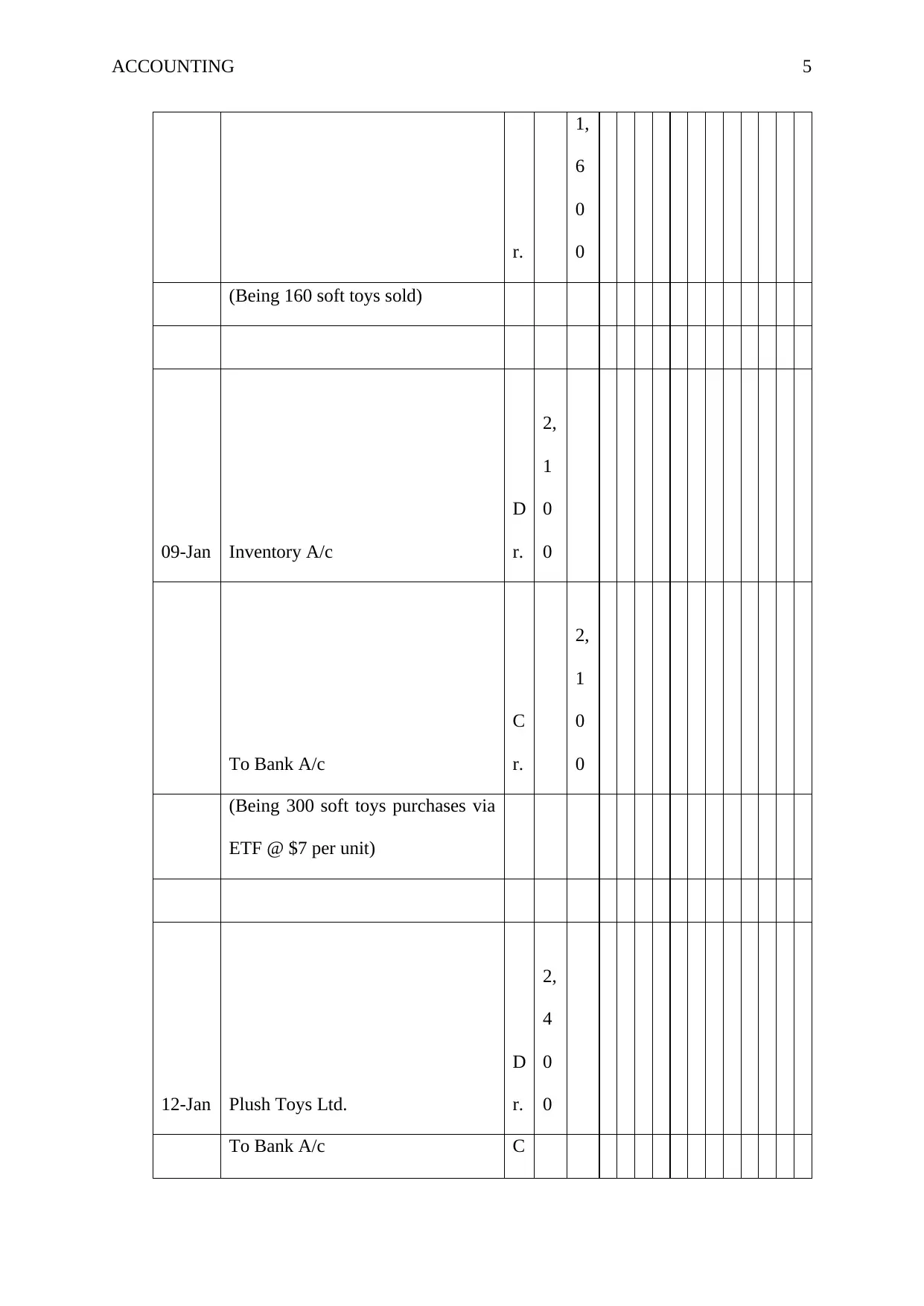

ACCOUNTING 5

r.

1,

6

0

0

(Being 160 soft toys sold)

09-Jan Inventory A/c

D

r.

2,

1

0

0

To Bank A/c

C

r.

2,

1

0

0

(Being 300 soft toys purchases via

ETF @ $7 per unit)

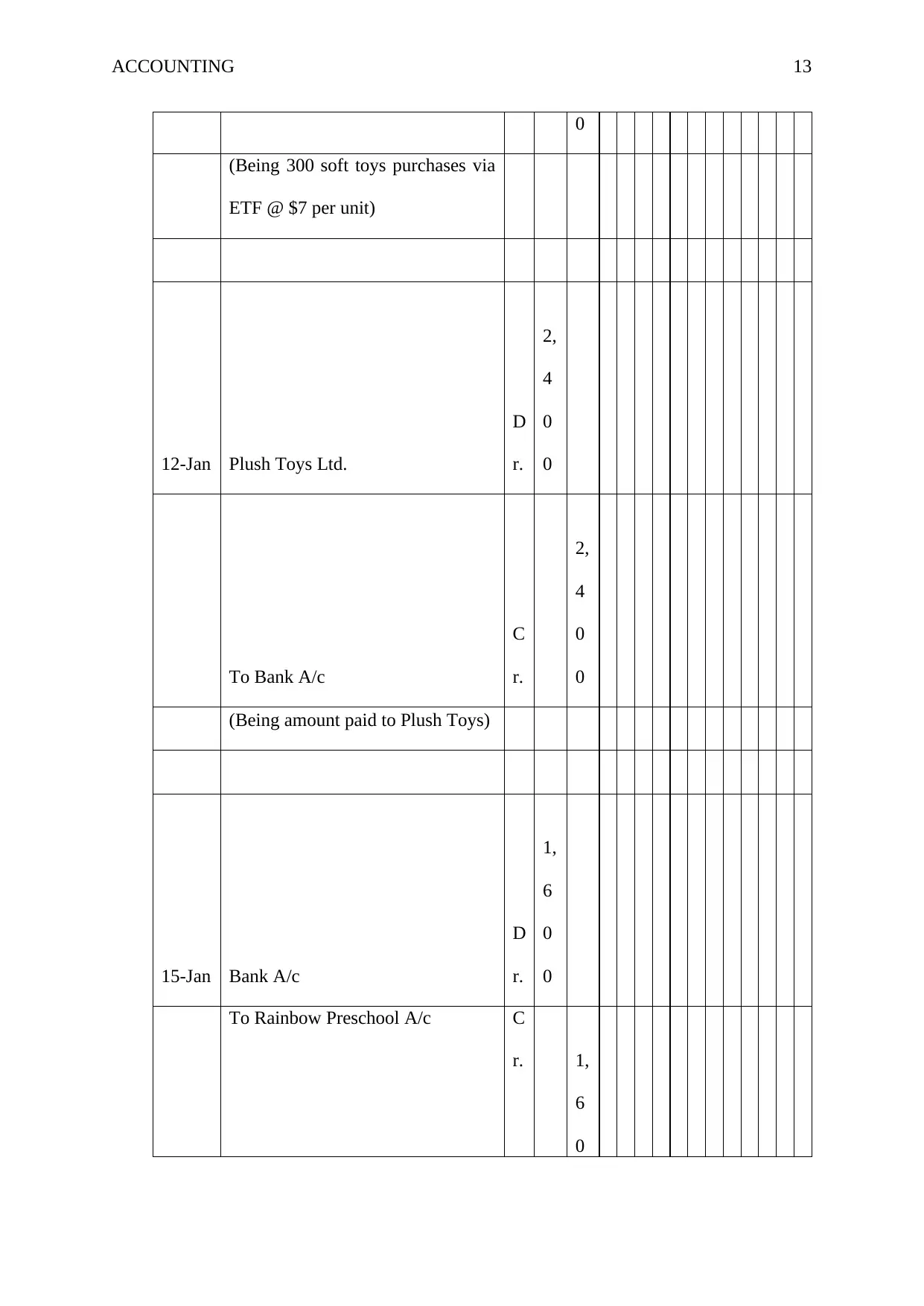

12-Jan Plush Toys Ltd.

D

r.

2,

4

0

0

To Bank A/c C

r.

1,

6

0

0

(Being 160 soft toys sold)

09-Jan Inventory A/c

D

r.

2,

1

0

0

To Bank A/c

C

r.

2,

1

0

0

(Being 300 soft toys purchases via

ETF @ $7 per unit)

12-Jan Plush Toys Ltd.

D

r.

2,

4

0

0

To Bank A/c C

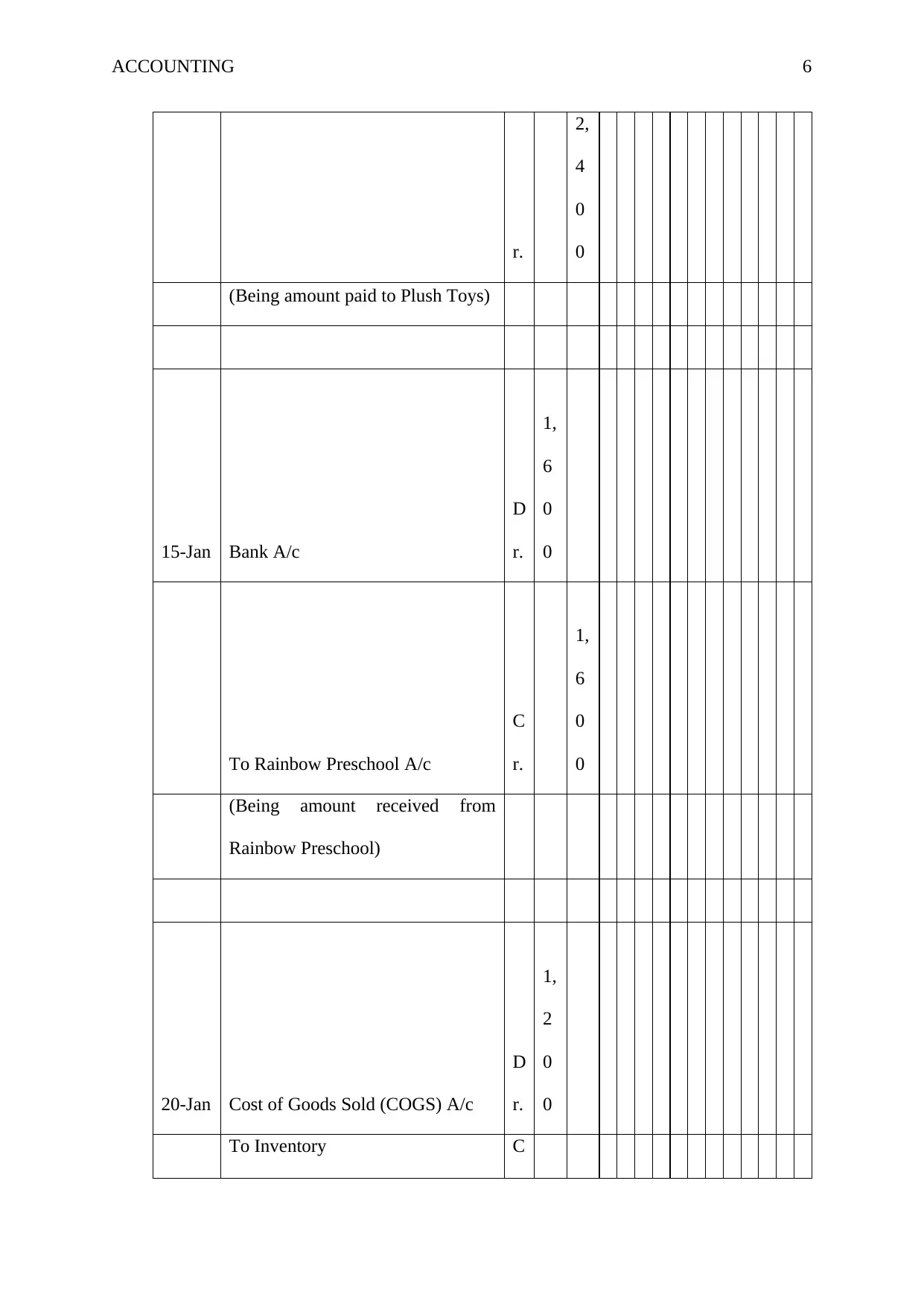

ACCOUNTING 6

r.

2,

4

0

0

(Being amount paid to Plush Toys)

15-Jan Bank A/c

D

r.

1,

6

0

0

To Rainbow Preschool A/c

C

r.

1,

6

0

0

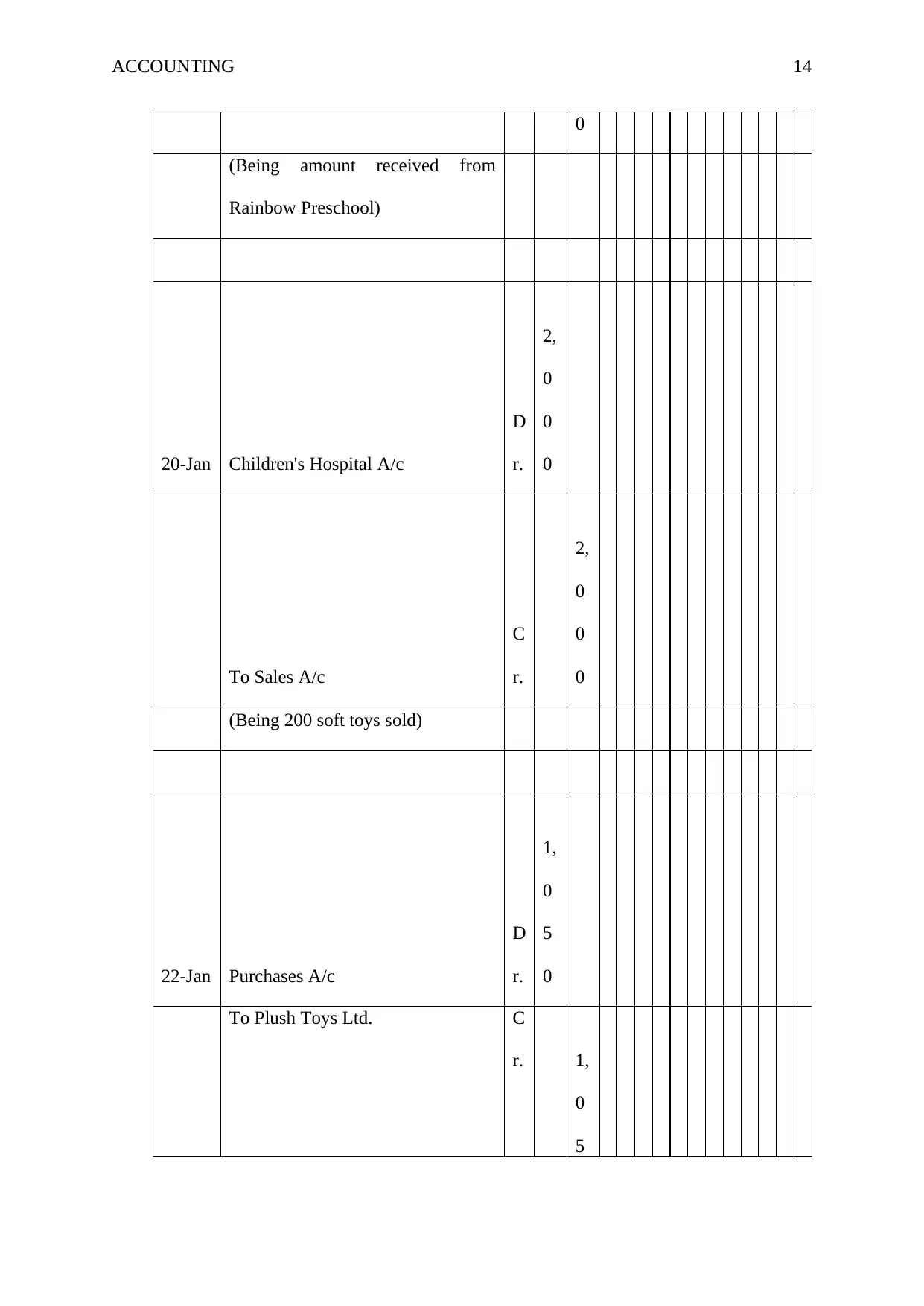

(Being amount received from

Rainbow Preschool)

20-Jan Cost of Goods Sold (COGS) A/c

D

r.

1,

2

0

0

To Inventory C

r.

2,

4

0

0

(Being amount paid to Plush Toys)

15-Jan Bank A/c

D

r.

1,

6

0

0

To Rainbow Preschool A/c

C

r.

1,

6

0

0

(Being amount received from

Rainbow Preschool)

20-Jan Cost of Goods Sold (COGS) A/c

D

r.

1,

2

0

0

To Inventory C

ACCOUNTING 7

r.

1,

2

0

0

(Being cost of 200 soft toys

transferred to COGS @ $6 per unit

from purchase of 3rd January)

20-Jan Children's Hospital A/c

D

r.

2,

0

0

0

To Sales A/c

C

r.

2,

0

0

0

(Being 200 soft toys sold)

22-Jan Inventory A/c

D

r.

1,

0

5

0

r.

1,

2

0

0

(Being cost of 200 soft toys

transferred to COGS @ $6 per unit

from purchase of 3rd January)

20-Jan Children's Hospital A/c

D

r.

2,

0

0

0

To Sales A/c

C

r.

2,

0

0

0

(Being 200 soft toys sold)

22-Jan Inventory A/c

D

r.

1,

0

5

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 8

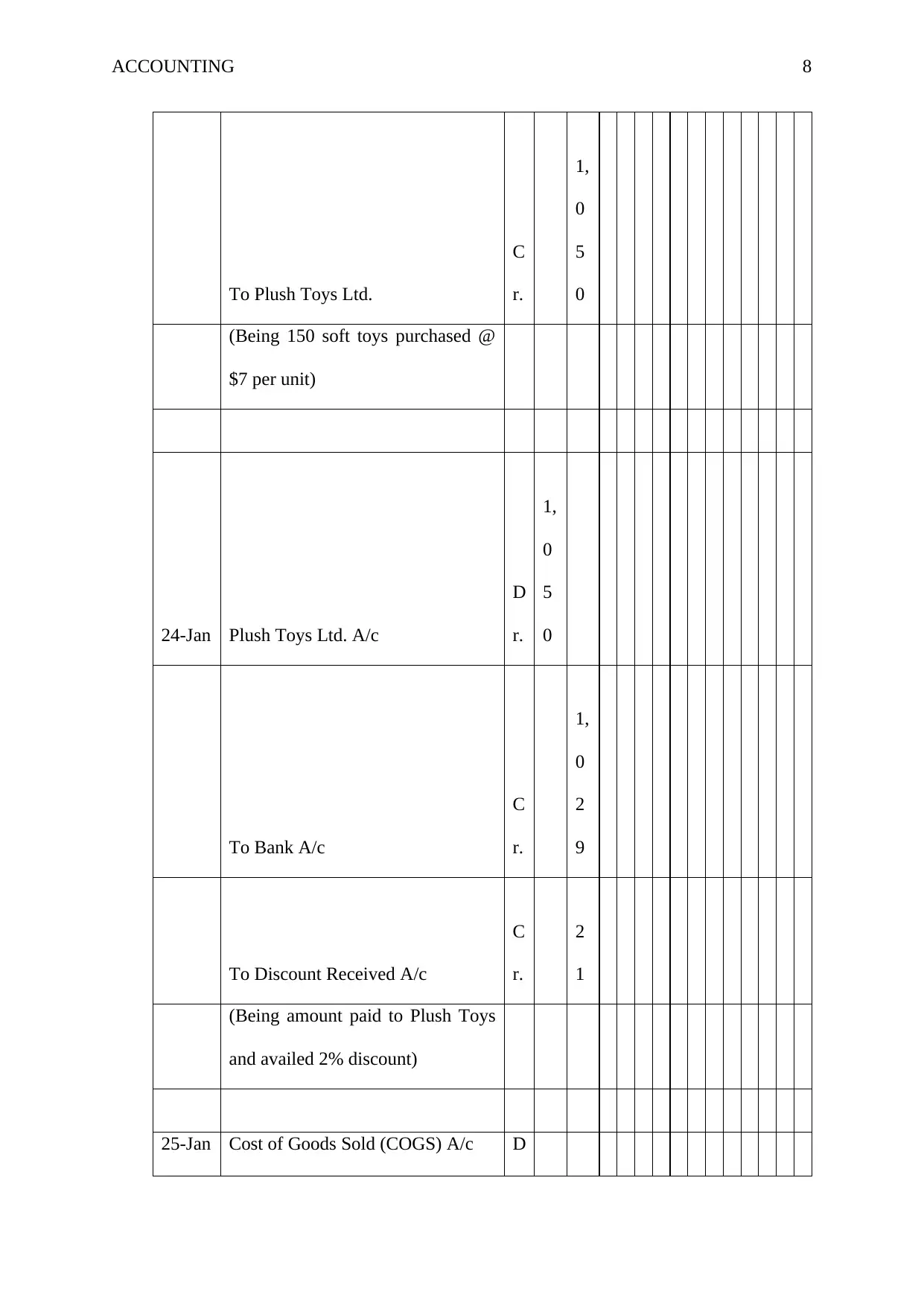

To Plush Toys Ltd.

C

r.

1,

0

5

0

(Being 150 soft toys purchased @

$7 per unit)

24-Jan Plush Toys Ltd. A/c

D

r.

1,

0

5

0

To Bank A/c

C

r.

1,

0

2

9

To Discount Received A/c

C

r.

2

1

(Being amount paid to Plush Toys

and availed 2% discount)

25-Jan Cost of Goods Sold (COGS) A/c D

To Plush Toys Ltd.

C

r.

1,

0

5

0

(Being 150 soft toys purchased @

$7 per unit)

24-Jan Plush Toys Ltd. A/c

D

r.

1,

0

5

0

To Bank A/c

C

r.

1,

0

2

9

To Discount Received A/c

C

r.

2

1

(Being amount paid to Plush Toys

and availed 2% discount)

25-Jan Cost of Goods Sold (COGS) A/c D

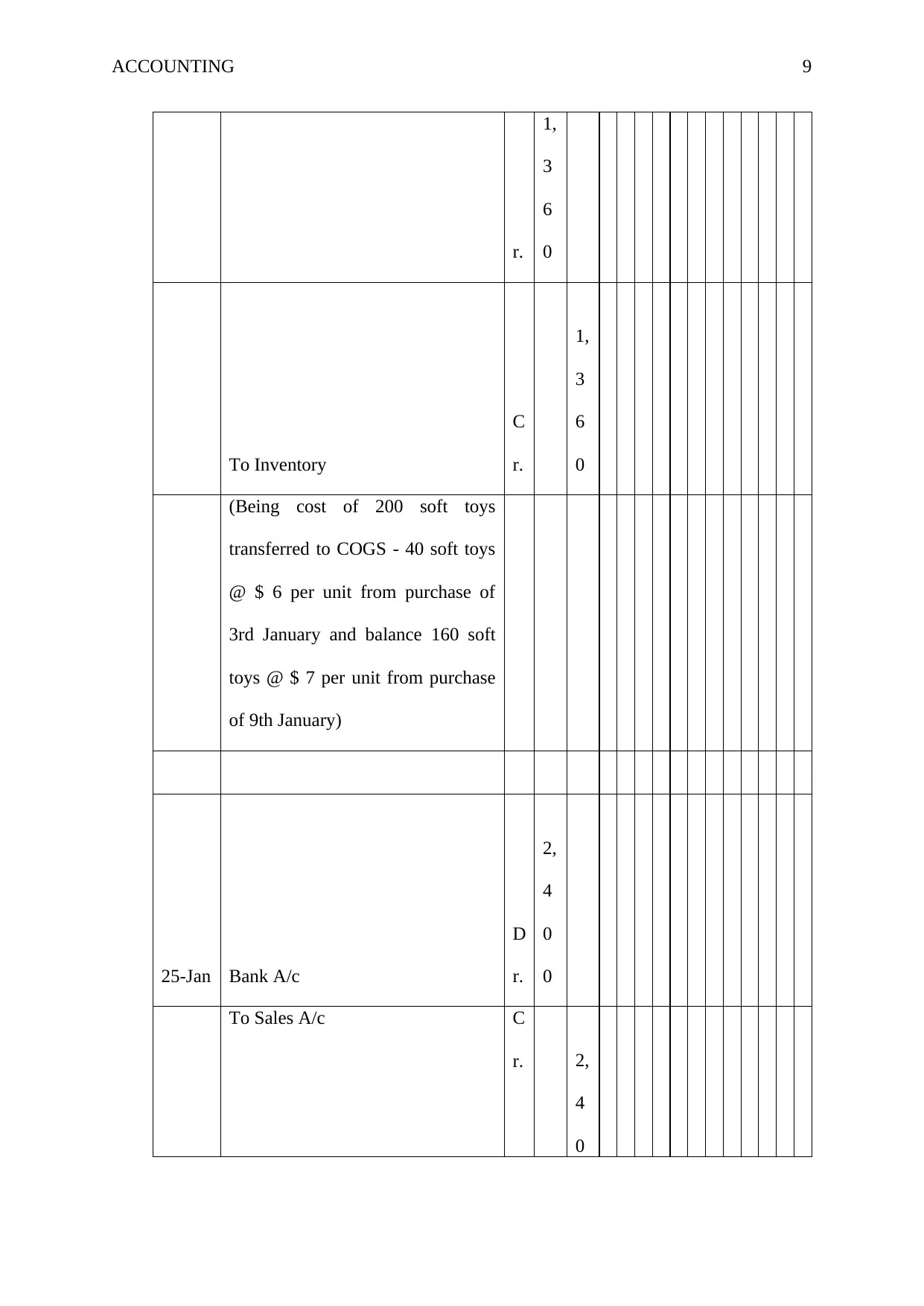

ACCOUNTING 9

r.

1,

3

6

0

To Inventory

C

r.

1,

3

6

0

(Being cost of 200 soft toys

transferred to COGS - 40 soft toys

@ $ 6 per unit from purchase of

3rd January and balance 160 soft

toys @ $ 7 per unit from purchase

of 9th January)

25-Jan Bank A/c

D

r.

2,

4

0

0

To Sales A/c C

r. 2,

4

0

r.

1,

3

6

0

To Inventory

C

r.

1,

3

6

0

(Being cost of 200 soft toys

transferred to COGS - 40 soft toys

@ $ 6 per unit from purchase of

3rd January and balance 160 soft

toys @ $ 7 per unit from purchase

of 9th January)

25-Jan Bank A/c

D

r.

2,

4

0

0

To Sales A/c C

r. 2,

4

0

ACCOUNTING 10

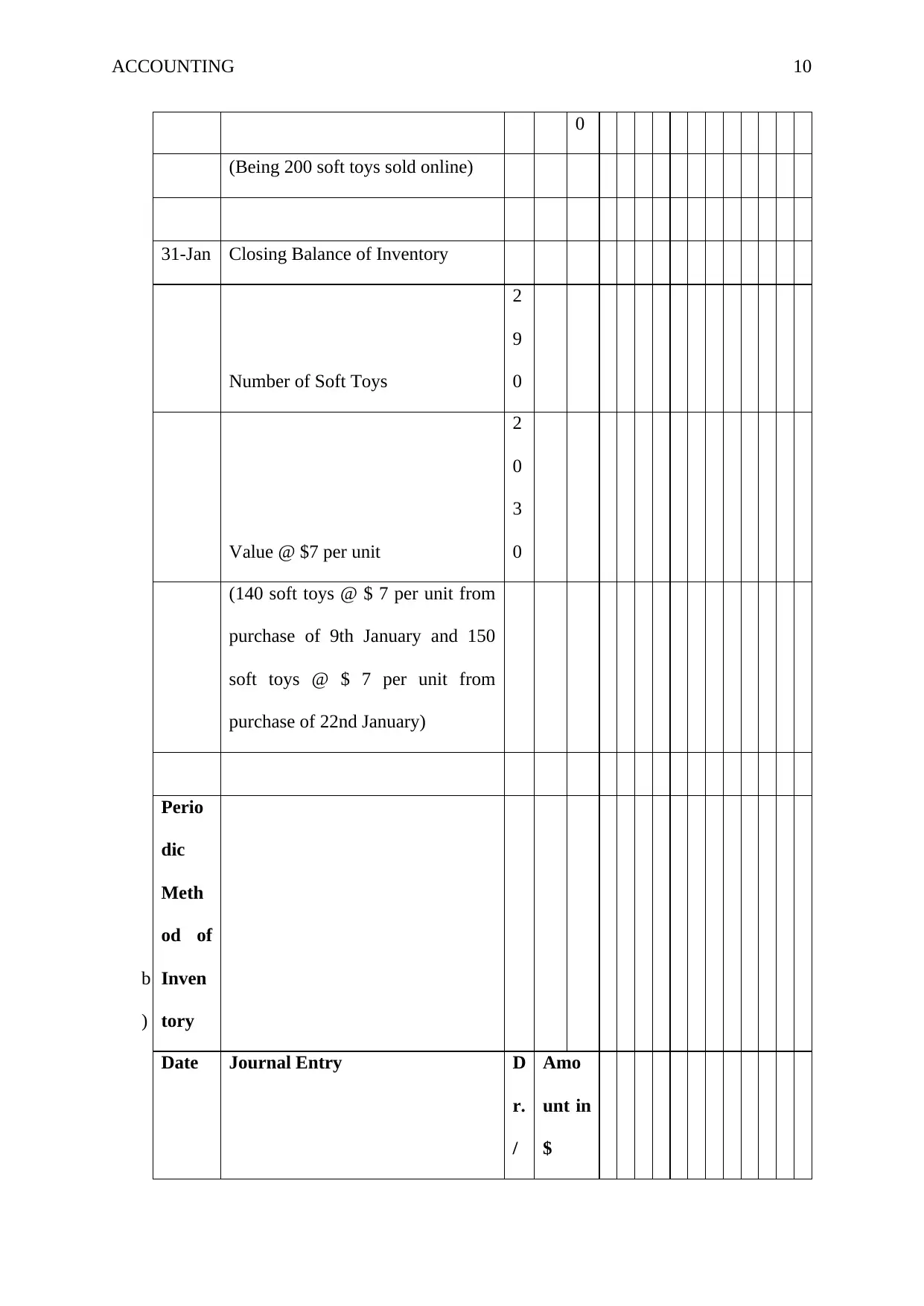

0

(Being 200 soft toys sold online)

31-Jan Closing Balance of Inventory

Number of Soft Toys

2

9

0

Value @ $7 per unit

2

0

3

0

(140 soft toys @ $ 7 per unit from

purchase of 9th January and 150

soft toys @ $ 7 per unit from

purchase of 22nd January)

b

)

Perio

dic

Meth

od of

Inven

tory

Date Journal Entry D

r.

/

Amo

unt in

$

0

(Being 200 soft toys sold online)

31-Jan Closing Balance of Inventory

Number of Soft Toys

2

9

0

Value @ $7 per unit

2

0

3

0

(140 soft toys @ $ 7 per unit from

purchase of 9th January and 150

soft toys @ $ 7 per unit from

purchase of 22nd January)

b

)

Perio

dic

Meth

od of

Inven

tory

Date Journal Entry D

r.

/

Amo

unt in

$

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING 11

C

r.

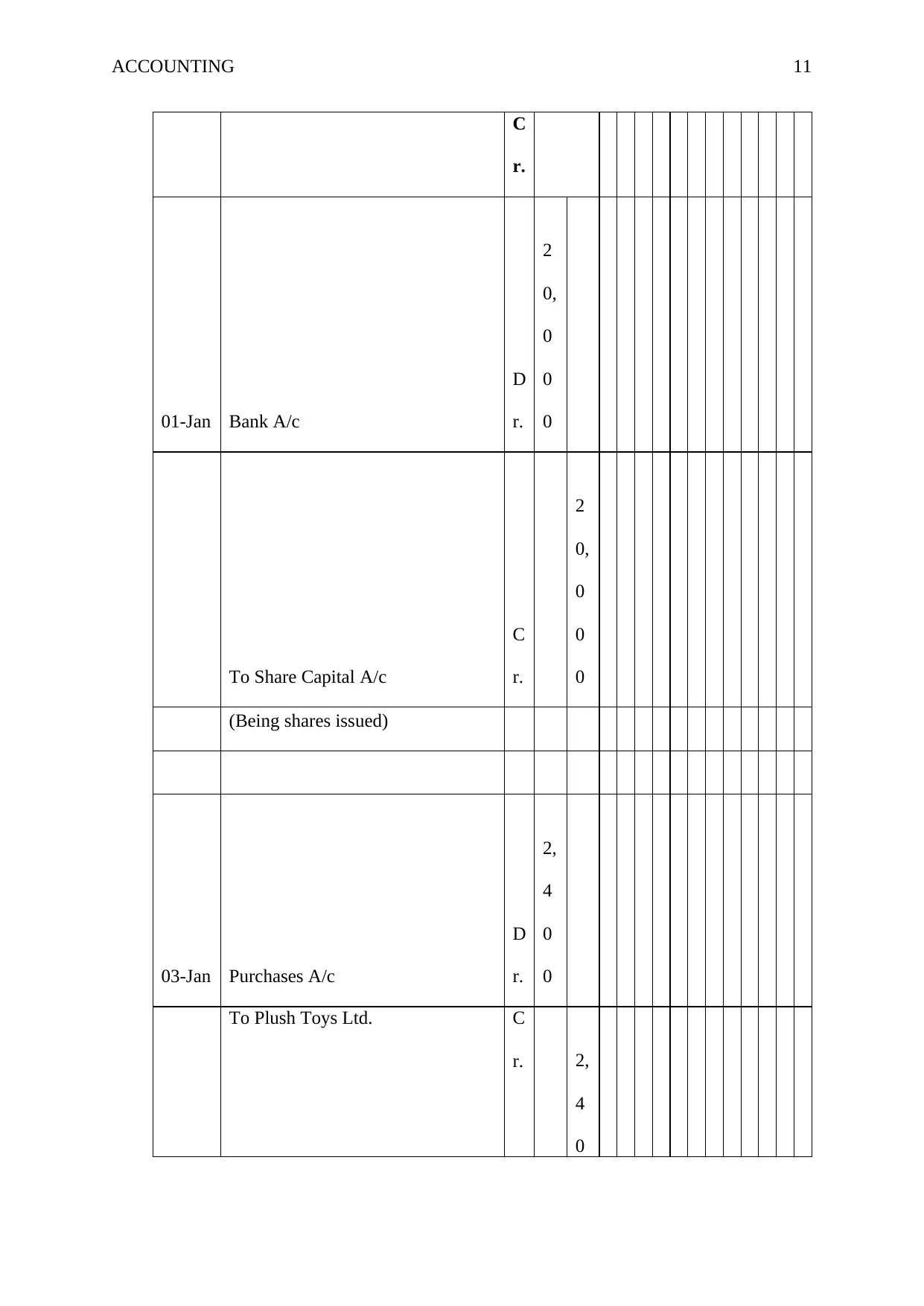

01-Jan Bank A/c

D

r.

2

0,

0

0

0

To Share Capital A/c

C

r.

2

0,

0

0

0

(Being shares issued)

03-Jan Purchases A/c

D

r.

2,

4

0

0

To Plush Toys Ltd. C

r. 2,

4

0

C

r.

01-Jan Bank A/c

D

r.

2

0,

0

0

0

To Share Capital A/c

C

r.

2

0,

0

0

0

(Being shares issued)

03-Jan Purchases A/c

D

r.

2,

4

0

0

To Plush Toys Ltd. C

r. 2,

4

0

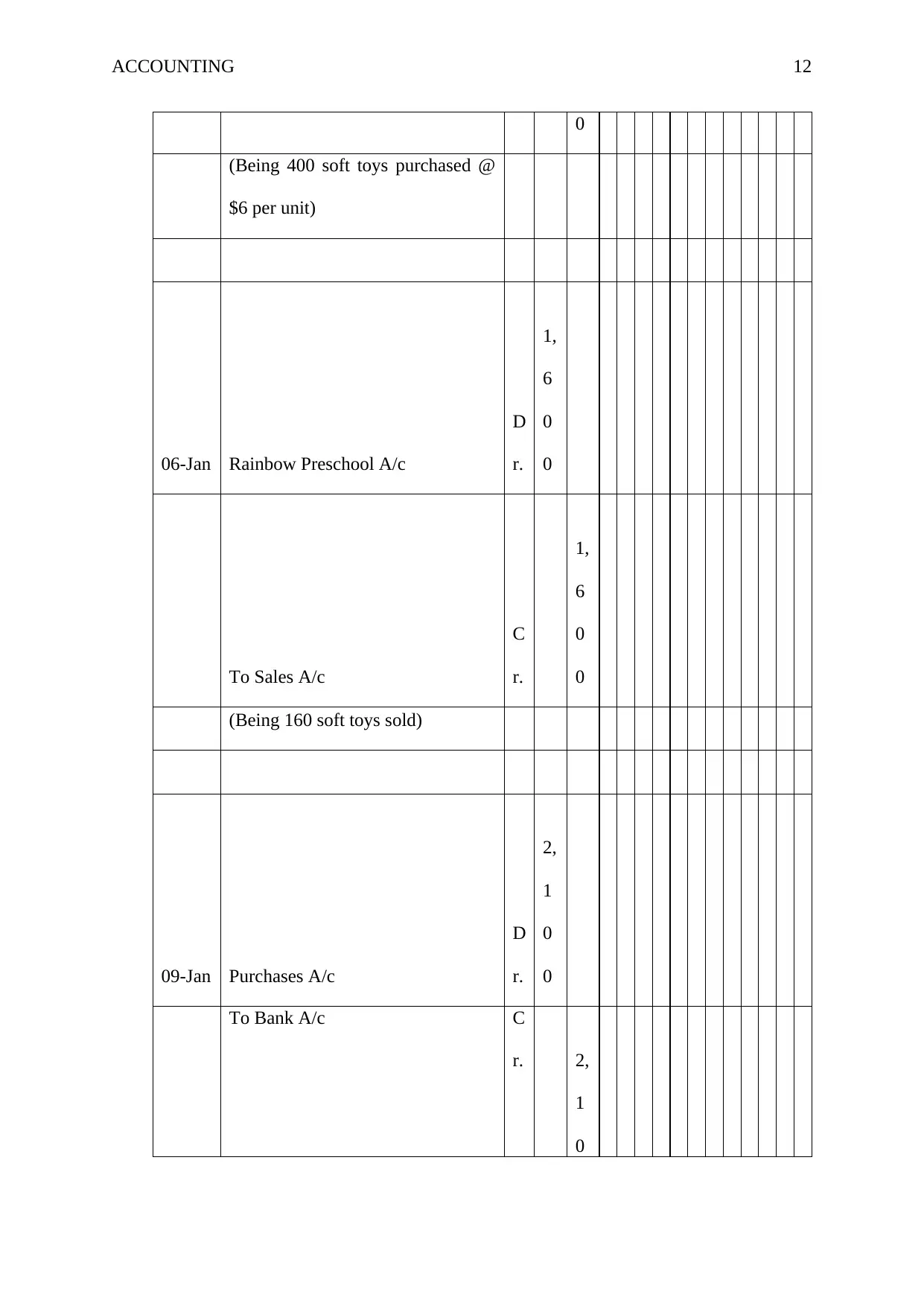

ACCOUNTING 12

0

(Being 400 soft toys purchased @

$6 per unit)

06-Jan Rainbow Preschool A/c

D

r.

1,

6

0

0

To Sales A/c

C

r.

1,

6

0

0

(Being 160 soft toys sold)

09-Jan Purchases A/c

D

r.

2,

1

0

0

To Bank A/c C

r. 2,

1

0

0

(Being 400 soft toys purchased @

$6 per unit)

06-Jan Rainbow Preschool A/c

D

r.

1,

6

0

0

To Sales A/c

C

r.

1,

6

0

0

(Being 160 soft toys sold)

09-Jan Purchases A/c

D

r.

2,

1

0

0

To Bank A/c C

r. 2,

1

0

ACCOUNTING 13

0

(Being 300 soft toys purchases via

ETF @ $7 per unit)

12-Jan Plush Toys Ltd.

D

r.

2,

4

0

0

To Bank A/c

C

r.

2,

4

0

0

(Being amount paid to Plush Toys)

15-Jan Bank A/c

D

r.

1,

6

0

0

To Rainbow Preschool A/c C

r. 1,

6

0

0

(Being 300 soft toys purchases via

ETF @ $7 per unit)

12-Jan Plush Toys Ltd.

D

r.

2,

4

0

0

To Bank A/c

C

r.

2,

4

0

0

(Being amount paid to Plush Toys)

15-Jan Bank A/c

D

r.

1,

6

0

0

To Rainbow Preschool A/c C

r. 1,

6

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 14

0

(Being amount received from

Rainbow Preschool)

20-Jan Children's Hospital A/c

D

r.

2,

0

0

0

To Sales A/c

C

r.

2,

0

0

0

(Being 200 soft toys sold)

22-Jan Purchases A/c

D

r.

1,

0

5

0

To Plush Toys Ltd. C

r. 1,

0

5

0

(Being amount received from

Rainbow Preschool)

20-Jan Children's Hospital A/c

D

r.

2,

0

0

0

To Sales A/c

C

r.

2,

0

0

0

(Being 200 soft toys sold)

22-Jan Purchases A/c

D

r.

1,

0

5

0

To Plush Toys Ltd. C

r. 1,

0

5

ACCOUNTING 15

0

(Being 150 soft toys purchased @

$7 per unit)

24-Jan Plush Toys Ltd. A/c

D

r.

1,

0

5

0

To Bank A/c

C

r.

1,

0

2

9

To Discount Received A/c

C

r.

2

1

(Being amount paid to Plush Toys

and availed 2% discount)

25-Jan Bank A/c

D

r.

2,

4

0

0

0

(Being 150 soft toys purchased @

$7 per unit)

24-Jan Plush Toys Ltd. A/c

D

r.

1,

0

5

0

To Bank A/c

C

r.

1,

0

2

9

To Discount Received A/c

C

r.

2

1

(Being amount paid to Plush Toys

and availed 2% discount)

25-Jan Bank A/c

D

r.

2,

4

0

0

ACCOUNTING 16

To Sales A/c

C

r.

2,

4

0

0

(Being 200 soft toys sold online)

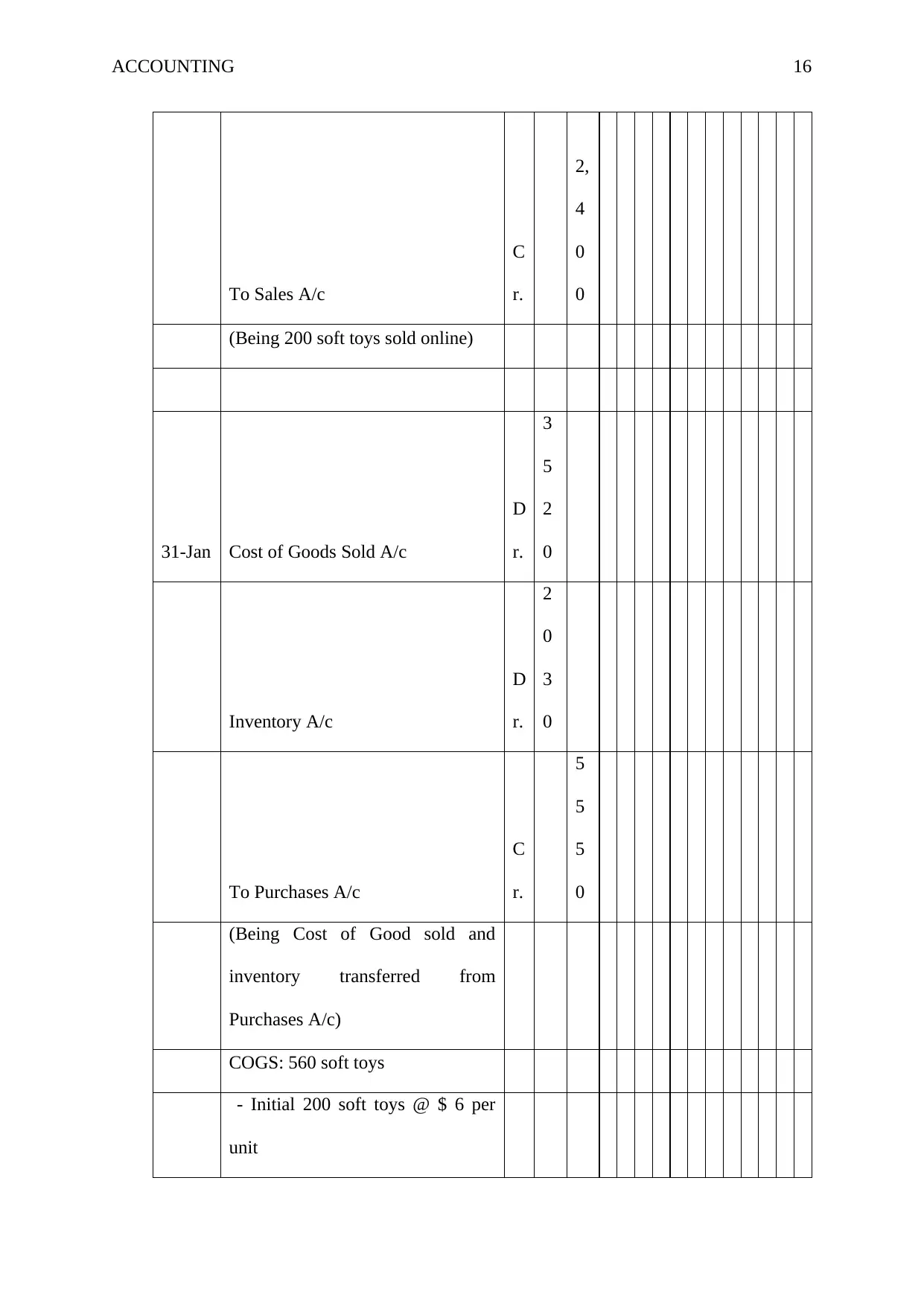

31-Jan Cost of Goods Sold A/c

D

r.

3

5

2

0

Inventory A/c

D

r.

2

0

3

0

To Purchases A/c

C

r.

5

5

5

0

(Being Cost of Good sold and

inventory transferred from

Purchases A/c)

COGS: 560 soft toys

- Initial 200 soft toys @ $ 6 per

unit

To Sales A/c

C

r.

2,

4

0

0

(Being 200 soft toys sold online)

31-Jan Cost of Goods Sold A/c

D

r.

3

5

2

0

Inventory A/c

D

r.

2

0

3

0

To Purchases A/c

C

r.

5

5

5

0

(Being Cost of Good sold and

inventory transferred from

Purchases A/c)

COGS: 560 soft toys

- Initial 200 soft toys @ $ 6 per

unit

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING 17

- Next 200 soft toys @ $ 6 per unit

- Last 160 soft toys @ $ 7 per unit

Inventory: 290 soft toys

- 290 soft toys @ $ 7 per unit

To: Mr and Mrs Spot

From: A

Re: Inventory method

Date: July 12, 2019

Question presented: Inventory methods

Under the FIFO method of inventory valuation is based on the assumption that the usage or

sale of goods follows the same order in which they are bought i.e. to say under this method

the earlier purchased goods are considered as first used. As a result, under this method, the

inventory is valued at most recent purchased price

Under the weighted average method of inventory valuation the cost of goods sold and

inventory are valued at weighted average cost of goods available during the period i.e. Cost

of Opening Inventory plus the Cost of Purchases is divided by the total units

Answer 2:

The following are the benefits if using the Xerox accounting software:

This is the type of an accounting in which the cloud book keeping and automation

goes side by side. The system allows the automating of all of the manual tasks and

this sort of the software is very important for the company. This helps in the scaling

of the business operations which the company did not have earlier. Plus the time spent

- Next 200 soft toys @ $ 6 per unit

- Last 160 soft toys @ $ 7 per unit

Inventory: 290 soft toys

- 290 soft toys @ $ 7 per unit

To: Mr and Mrs Spot

From: A

Re: Inventory method

Date: July 12, 2019

Question presented: Inventory methods

Under the FIFO method of inventory valuation is based on the assumption that the usage or

sale of goods follows the same order in which they are bought i.e. to say under this method

the earlier purchased goods are considered as first used. As a result, under this method, the

inventory is valued at most recent purchased price

Under the weighted average method of inventory valuation the cost of goods sold and

inventory are valued at weighted average cost of goods available during the period i.e. Cost

of Opening Inventory plus the Cost of Purchases is divided by the total units

Answer 2:

The following are the benefits if using the Xerox accounting software:

This is the type of an accounting in which the cloud book keeping and automation

goes side by side. The system allows the automating of all of the manual tasks and

this sort of the software is very important for the company. This helps in the scaling

of the business operations which the company did not have earlier. Plus the time spent

ACCOUNTING 18

by the book keepers and the accountants entering the data into the system could be

saved and the same could be used in something which is more fruitful. There are

many companies today that are using a larger accounting platform which have a

vibrant add on ecosystem. This software is the solution to each and very document,

workflow to the forecasting of the cash flows. Thee cloud book keeping helps in the

efficient management of the cash flows and this ensures support to an increased

number of clients. They could focus on higher paying work.

This software helps in the efficient management of the cash flows which makes sure

the financial success of the business owners. The owners of the company may not

always have an insight inti the finances if the company and even then they are duty

bound to manage the day to day operations of the business. It is the shortage of this

information that is capable of making or breaking the company. But cloud book

keeping helps in solving the issues like these. It puts the owners back on track and

helps them in an efficient management if the financial operations or the financial

health of the company. The company will have to no longer wait for the latest version

of the accounting software when it comes to the checking of the various incomes and

the expenses. The various owners of the business would be able to understand as to

where the money is going and from where it is coming. They would be able to control

the business transactions.

The owners of the business can access the information as and when they need it. This

helps then in accessing the information as and when they require and they are able to

know the exact movement of the business transactions. The advisors employed by the

company are today spending about 35% of the time in looking and in accessing of

their documents. With the adoption of this cloud based accounting software, they are

able to utilise that time in catering to the needs of the clients. The owners of the

by the book keepers and the accountants entering the data into the system could be

saved and the same could be used in something which is more fruitful. There are

many companies today that are using a larger accounting platform which have a

vibrant add on ecosystem. This software is the solution to each and very document,

workflow to the forecasting of the cash flows. Thee cloud book keeping helps in the

efficient management of the cash flows and this ensures support to an increased

number of clients. They could focus on higher paying work.

This software helps in the efficient management of the cash flows which makes sure

the financial success of the business owners. The owners of the company may not

always have an insight inti the finances if the company and even then they are duty

bound to manage the day to day operations of the business. It is the shortage of this

information that is capable of making or breaking the company. But cloud book

keeping helps in solving the issues like these. It puts the owners back on track and

helps them in an efficient management if the financial operations or the financial

health of the company. The company will have to no longer wait for the latest version

of the accounting software when it comes to the checking of the various incomes and

the expenses. The various owners of the business would be able to understand as to

where the money is going and from where it is coming. They would be able to control

the business transactions.

The owners of the business can access the information as and when they need it. This

helps then in accessing the information as and when they require and they are able to

know the exact movement of the business transactions. The advisors employed by the

company are today spending about 35% of the time in looking and in accessing of

their documents. With the adoption of this cloud based accounting software, they are

able to utilise that time in catering to the needs of the clients. The owners of the

ACCOUNTING 19

company would be able to manage business and also leverage business solutions from

these financial documents if they are available online. The maintenance of these

documents are secure in the cloud and are accessible from anywhere in the world.

This merely means that these documents are readily available and can be accessed

whenever and wherever needed. This helps in a greater control over their time.

Another advantage of using this software is the fact that is available with the push

updates which means that it is very different from the desktop wherein there is a new

version that one would be stuck with. Further, the upgrades are only available when a

new version is purchased. This software would fly without incurring an extra cost for

the user. This software also seeks the feedback from their customers which means that

the customers are always kept in loop whenever any new improvement is to be made.

The manual backing up of the data is very much difficult and hence, when the backing

up is automated, it would prove to be less painful for the company. Hence, this is the

software that would lead to a deep integration between this book keeping software

and their add ons. This back up is something which is automatic.

Further, one just has to update the new numbers of the inventory, the rest of the work

is done by this software itself. All of the inventory records are updated automatically

which means hassle free updations and an error free and a more accurate book

keeping of all of the business transactions backed up by the relevant documents and

also the maintenance of the adequate inventory records (Xero, 2019).

In the nutshell, when a business is blooming, it is better to automate the financial records

since manual intervention can only lead to mistakes or errors. Also, the time spent in manual

intervention could be utilised to make the business more fruitful.

All the work is done automatically by the system.

company would be able to manage business and also leverage business solutions from

these financial documents if they are available online. The maintenance of these

documents are secure in the cloud and are accessible from anywhere in the world.

This merely means that these documents are readily available and can be accessed

whenever and wherever needed. This helps in a greater control over their time.

Another advantage of using this software is the fact that is available with the push

updates which means that it is very different from the desktop wherein there is a new

version that one would be stuck with. Further, the upgrades are only available when a

new version is purchased. This software would fly without incurring an extra cost for

the user. This software also seeks the feedback from their customers which means that

the customers are always kept in loop whenever any new improvement is to be made.

The manual backing up of the data is very much difficult and hence, when the backing

up is automated, it would prove to be less painful for the company. Hence, this is the

software that would lead to a deep integration between this book keeping software

and their add ons. This back up is something which is automatic.

Further, one just has to update the new numbers of the inventory, the rest of the work

is done by this software itself. All of the inventory records are updated automatically

which means hassle free updations and an error free and a more accurate book

keeping of all of the business transactions backed up by the relevant documents and

also the maintenance of the adequate inventory records (Xero, 2019).

In the nutshell, when a business is blooming, it is better to automate the financial records

since manual intervention can only lead to mistakes or errors. Also, the time spent in manual

intervention could be utilised to make the business more fruitful.

All the work is done automatically by the system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 20

Answer 3:

The main aim of the internal controls is to save the business from any sort of fraud that may

take place. And also, to ensure that all of the business activities show the correct and the true

picture of the financial position of the company.

The following are the 2 cases:

Mr Wilkinson from Employsure stated that one of his clients was operating a small

time business of importing the Italian coffee machines, he used to travel a lot and he

found that his money was being stolen. He then found out that one of his employees

was stealing from him and with the help of the evidence from the camera that he had

placed, he terminated his employment (The news, 2019).

In another case, the owner of the building supplies company was caught making the

refunds to the amount of $150,000 into their personal bank accounts. They were

trying to cover up these records with the help of forging stock records (ABC news,

2019).

The following are some of the internal controls that could be placed:

Separation of the people form the duties that include collection and keeping the cash

in safe custody

A limited amount of access should be given to the people to the assets that are critical

and that are important.

A physical audit of all of the assets must be done so that any irregular transaction

could easily and timely be uncovered.

Periodic reconciliations must be done so that anything which is irregular can be

uncovered and an appropriate action could be taken for the same (Small business

chron, 2019).

Answer 3:

The main aim of the internal controls is to save the business from any sort of fraud that may

take place. And also, to ensure that all of the business activities show the correct and the true

picture of the financial position of the company.

The following are the 2 cases:

Mr Wilkinson from Employsure stated that one of his clients was operating a small

time business of importing the Italian coffee machines, he used to travel a lot and he

found that his money was being stolen. He then found out that one of his employees

was stealing from him and with the help of the evidence from the camera that he had

placed, he terminated his employment (The news, 2019).

In another case, the owner of the building supplies company was caught making the

refunds to the amount of $150,000 into their personal bank accounts. They were

trying to cover up these records with the help of forging stock records (ABC news,

2019).

The following are some of the internal controls that could be placed:

Separation of the people form the duties that include collection and keeping the cash

in safe custody

A limited amount of access should be given to the people to the assets that are critical

and that are important.

A physical audit of all of the assets must be done so that any irregular transaction

could easily and timely be uncovered.

Periodic reconciliations must be done so that anything which is irregular can be

uncovered and an appropriate action could be taken for the same (Small business

chron, 2019).

ACCOUNTING 21

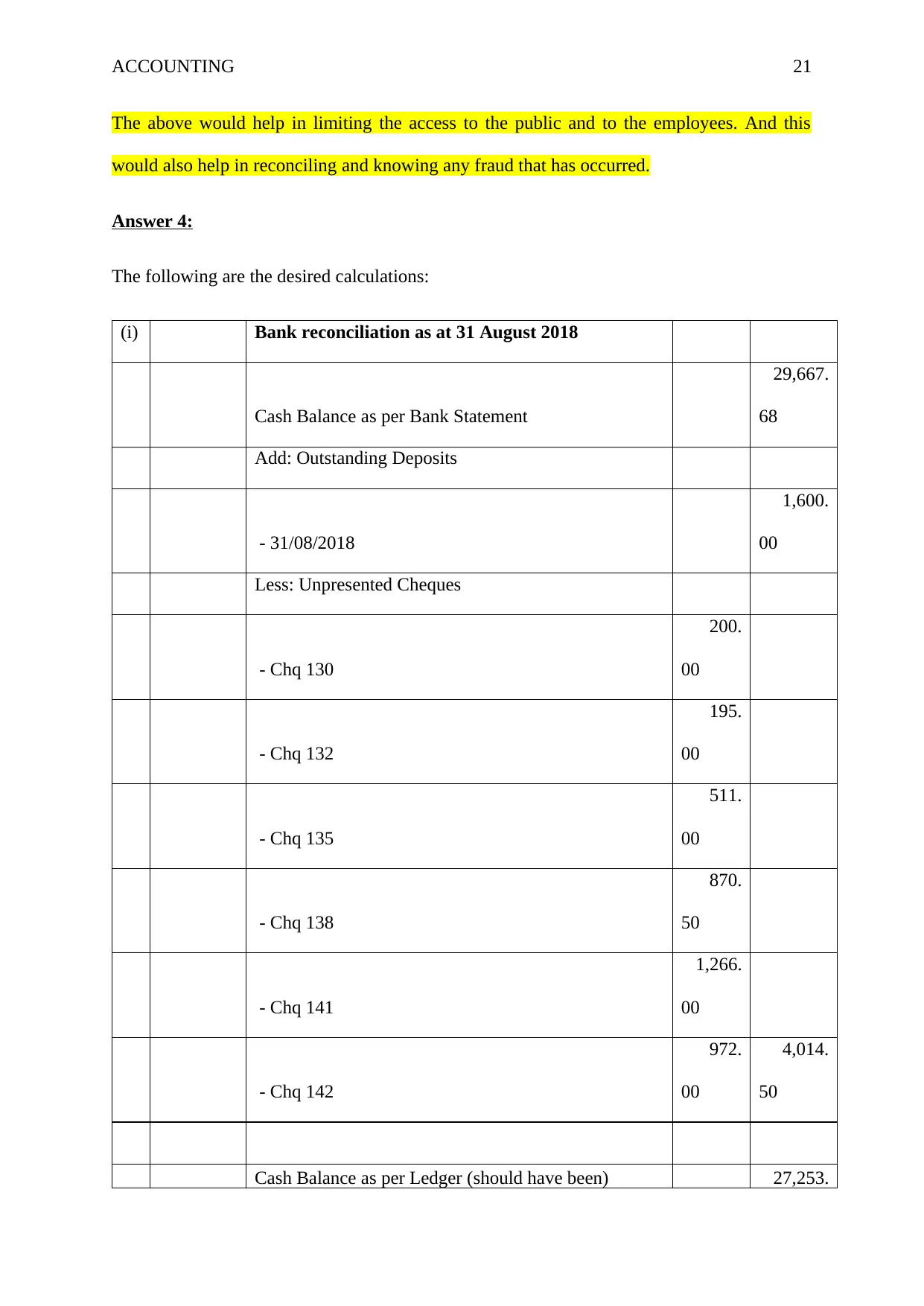

The above would help in limiting the access to the public and to the employees. And this

would also help in reconciling and knowing any fraud that has occurred.

Answer 4:

The following are the desired calculations:

(i) Bank reconciliation as at 31 August 2018

Cash Balance as per Bank Statement

29,667.

68

Add: Outstanding Deposits

- 31/08/2018

1,600.

00

Less: Unpresented Cheques

- Chq 130

200.

00

- Chq 132

195.

00

- Chq 135

511.

00

- Chq 138

870.

50

- Chq 141

1,266.

00

- Chq 142

972.

00

4,014.

50

Cash Balance as per Ledger (should have been) 27,253.

The above would help in limiting the access to the public and to the employees. And this

would also help in reconciling and knowing any fraud that has occurred.

Answer 4:

The following are the desired calculations:

(i) Bank reconciliation as at 31 August 2018

Cash Balance as per Bank Statement

29,667.

68

Add: Outstanding Deposits

- 31/08/2018

1,600.

00

Less: Unpresented Cheques

- Chq 130

200.

00

- Chq 132

195.

00

- Chq 135

511.

00

- Chq 138

870.

50

- Chq 141

1,266.

00

- Chq 142

972.

00

4,014.

50

Cash Balance as per Ledger (should have been) 27,253.

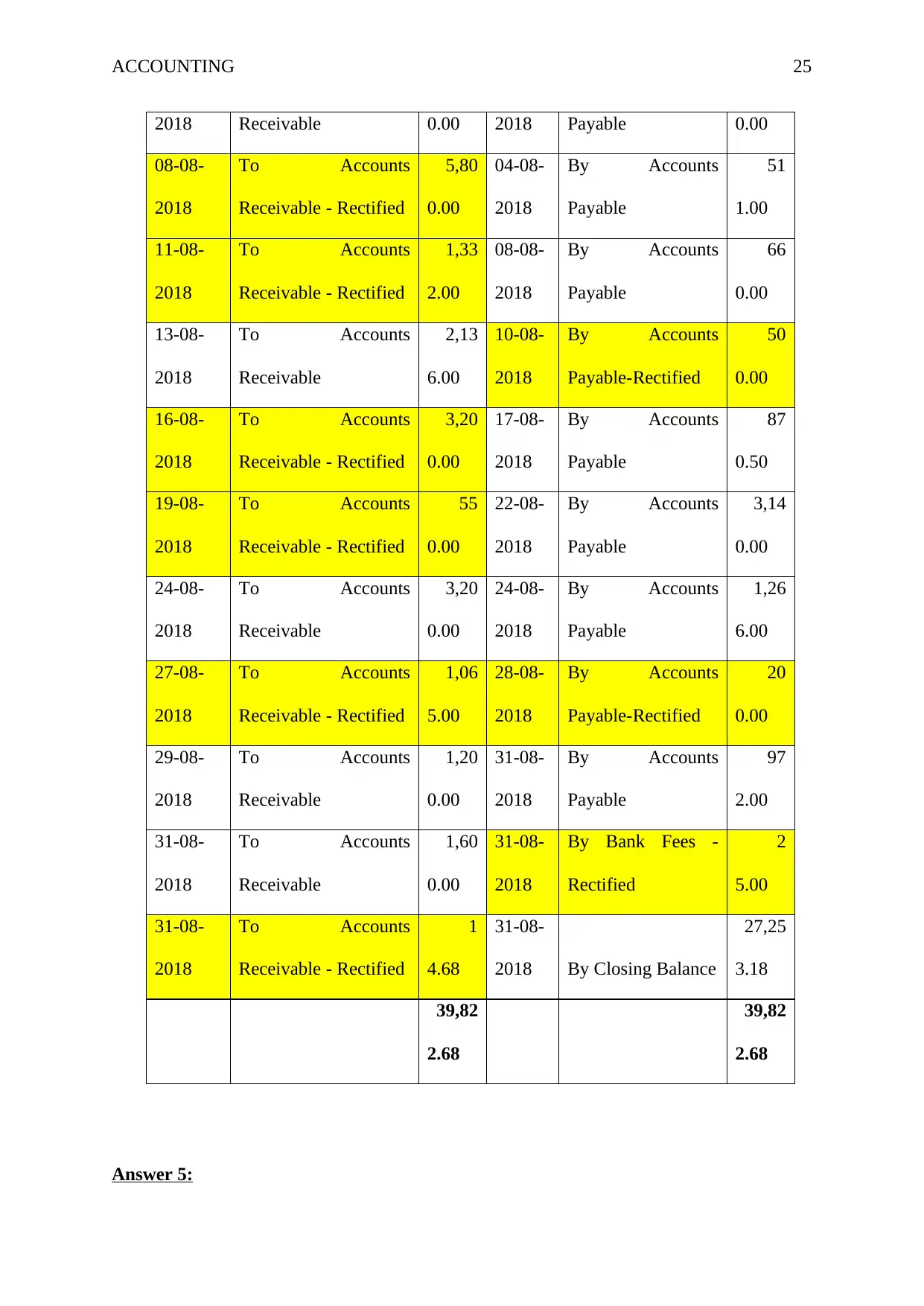

ACCOUNTING 22

18

(ii

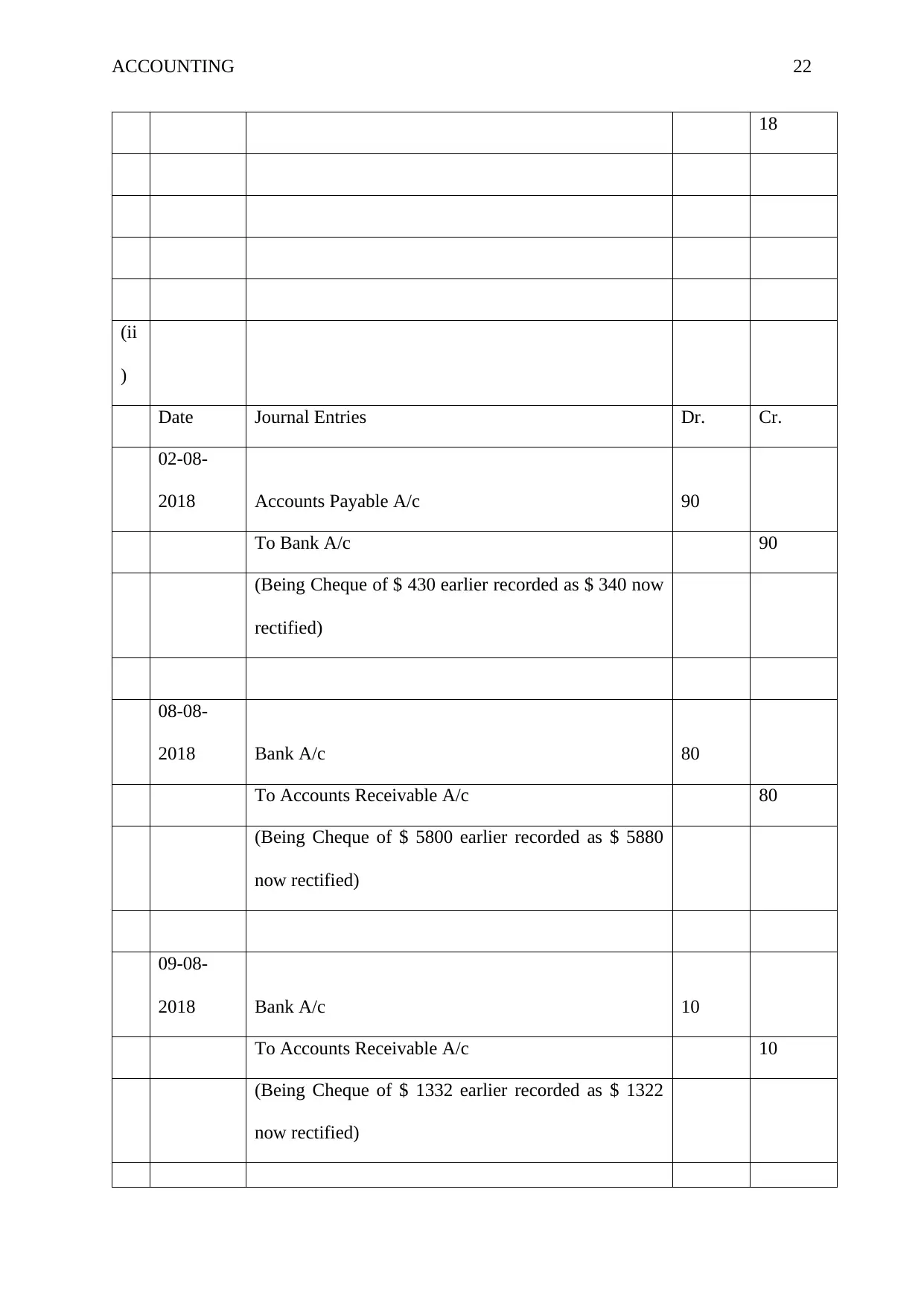

)

Date Journal Entries Dr. Cr.

02-08-

2018 Accounts Payable A/c 90

To Bank A/c 90

(Being Cheque of $ 430 earlier recorded as $ 340 now

rectified)

08-08-

2018 Bank A/c 80

To Accounts Receivable A/c 80

(Being Cheque of $ 5800 earlier recorded as $ 5880

now rectified)

09-08-

2018 Bank A/c 10

To Accounts Receivable A/c 10

(Being Cheque of $ 1332 earlier recorded as $ 1322

now rectified)

18

(ii

)

Date Journal Entries Dr. Cr.

02-08-

2018 Accounts Payable A/c 90

To Bank A/c 90

(Being Cheque of $ 430 earlier recorded as $ 340 now

rectified)

08-08-

2018 Bank A/c 80

To Accounts Receivable A/c 80

(Being Cheque of $ 5800 earlier recorded as $ 5880

now rectified)

09-08-

2018 Bank A/c 10

To Accounts Receivable A/c 10

(Being Cheque of $ 1332 earlier recorded as $ 1322

now rectified)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING 23

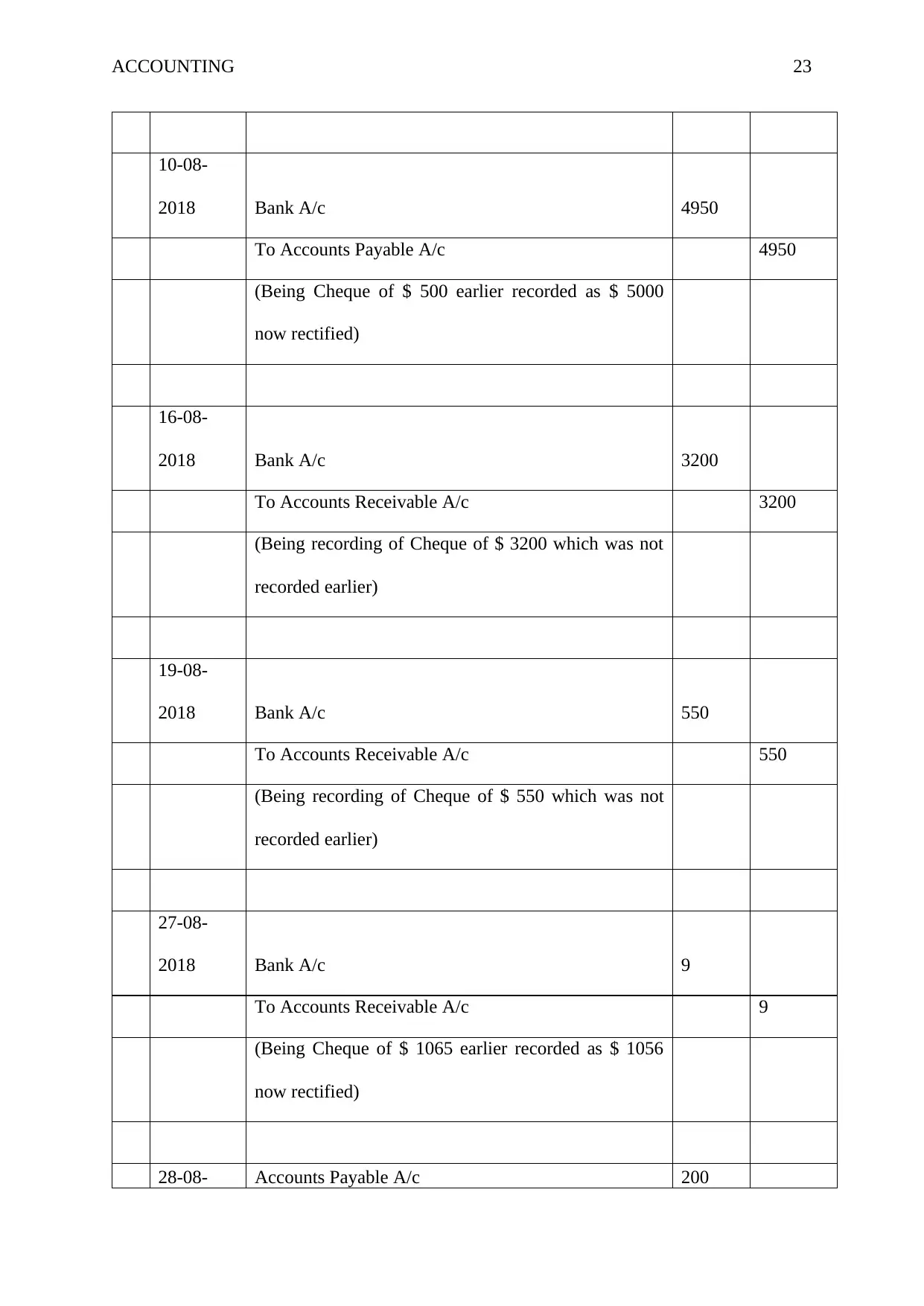

10-08-

2018 Bank A/c 4950

To Accounts Payable A/c 4950

(Being Cheque of $ 500 earlier recorded as $ 5000

now rectified)

16-08-

2018 Bank A/c 3200

To Accounts Receivable A/c 3200

(Being recording of Cheque of $ 3200 which was not

recorded earlier)

19-08-

2018 Bank A/c 550

To Accounts Receivable A/c 550

(Being recording of Cheque of $ 550 which was not

recorded earlier)

27-08-

2018 Bank A/c 9

To Accounts Receivable A/c 9

(Being Cheque of $ 1065 earlier recorded as $ 1056

now rectified)

28-08- Accounts Payable A/c 200

10-08-

2018 Bank A/c 4950

To Accounts Payable A/c 4950

(Being Cheque of $ 500 earlier recorded as $ 5000

now rectified)

16-08-

2018 Bank A/c 3200

To Accounts Receivable A/c 3200

(Being recording of Cheque of $ 3200 which was not

recorded earlier)

19-08-

2018 Bank A/c 550

To Accounts Receivable A/c 550

(Being recording of Cheque of $ 550 which was not

recorded earlier)

27-08-

2018 Bank A/c 9

To Accounts Receivable A/c 9

(Being Cheque of $ 1065 earlier recorded as $ 1056

now rectified)

28-08- Accounts Payable A/c 200

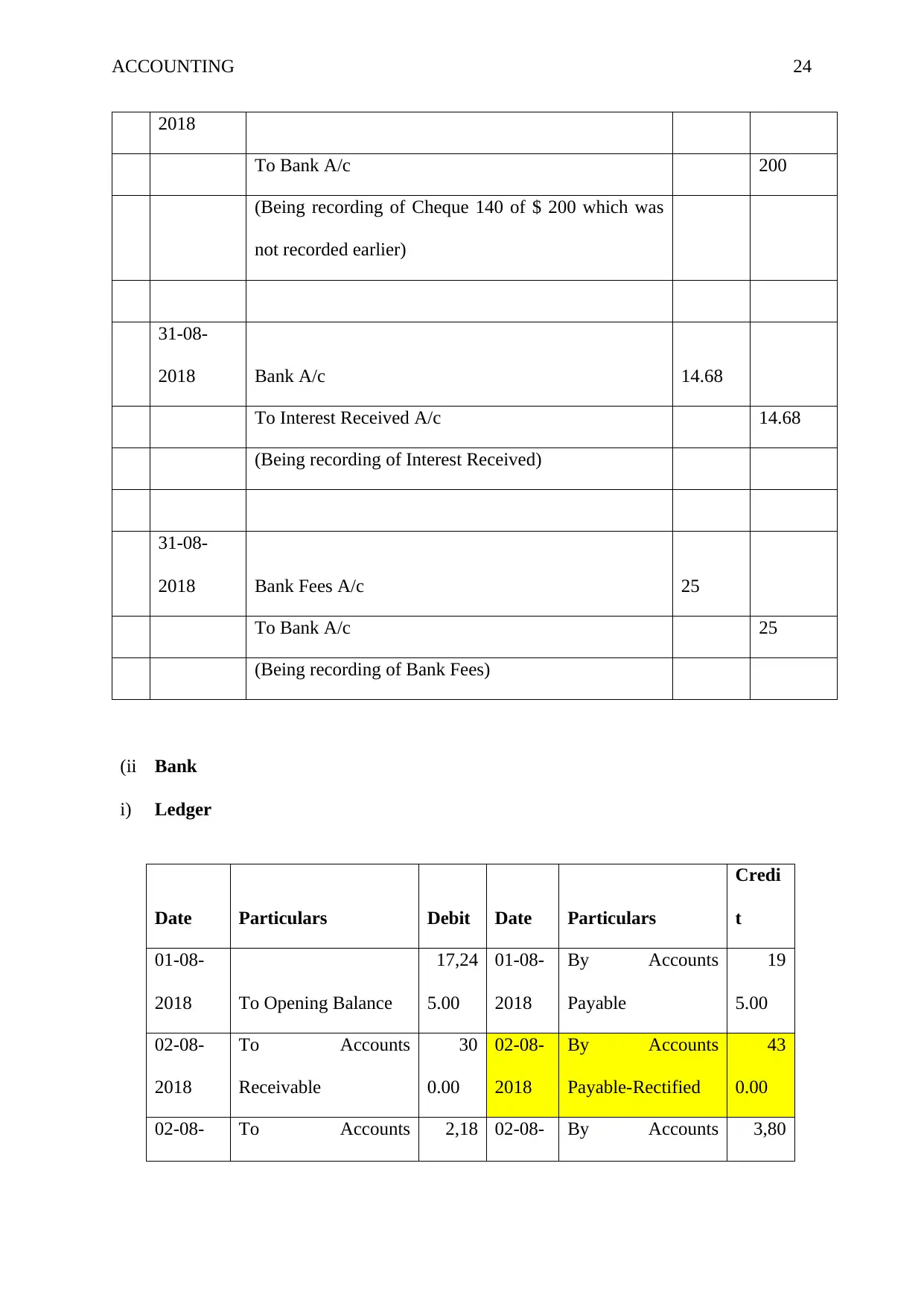

ACCOUNTING 24

2018

To Bank A/c 200

(Being recording of Cheque 140 of $ 200 which was

not recorded earlier)

31-08-

2018 Bank A/c 14.68

To Interest Received A/c 14.68

(Being recording of Interest Received)

31-08-

2018 Bank Fees A/c 25

To Bank A/c 25

(Being recording of Bank Fees)

(ii

i)

Bank

Ledger

Date Particulars Debit Date Particulars

Credi

t

01-08-

2018 To Opening Balance

17,24

5.00

01-08-

2018

By Accounts

Payable

19

5.00

02-08-

2018

To Accounts

Receivable

30

0.00

02-08-

2018

By Accounts

Payable-Rectified

43

0.00

02-08- To Accounts 2,18 02-08- By Accounts 3,80

2018

To Bank A/c 200

(Being recording of Cheque 140 of $ 200 which was

not recorded earlier)

31-08-

2018 Bank A/c 14.68

To Interest Received A/c 14.68

(Being recording of Interest Received)

31-08-

2018 Bank Fees A/c 25

To Bank A/c 25

(Being recording of Bank Fees)

(ii

i)

Bank

Ledger

Date Particulars Debit Date Particulars

Credi

t

01-08-

2018 To Opening Balance

17,24

5.00

01-08-

2018

By Accounts

Payable

19

5.00

02-08-

2018

To Accounts

Receivable

30

0.00

02-08-

2018

By Accounts

Payable-Rectified

43

0.00

02-08- To Accounts 2,18 02-08- By Accounts 3,80

ACCOUNTING 25

2018 Receivable 0.00 2018 Payable 0.00

08-08-

2018

To Accounts

Receivable - Rectified

5,80

0.00

04-08-

2018

By Accounts

Payable

51

1.00

11-08-

2018

To Accounts

Receivable - Rectified

1,33

2.00

08-08-

2018

By Accounts

Payable

66

0.00

13-08-

2018

To Accounts

Receivable

2,13

6.00

10-08-

2018

By Accounts

Payable-Rectified

50

0.00

16-08-

2018

To Accounts

Receivable - Rectified

3,20

0.00

17-08-

2018

By Accounts

Payable

87

0.50

19-08-

2018

To Accounts

Receivable - Rectified

55

0.00

22-08-

2018

By Accounts

Payable

3,14

0.00

24-08-

2018

To Accounts

Receivable

3,20

0.00

24-08-

2018

By Accounts

Payable

1,26

6.00

27-08-

2018

To Accounts

Receivable - Rectified

1,06

5.00

28-08-

2018

By Accounts

Payable-Rectified

20

0.00

29-08-

2018

To Accounts

Receivable

1,20

0.00

31-08-

2018

By Accounts

Payable

97

2.00

31-08-

2018

To Accounts

Receivable

1,60

0.00

31-08-

2018

By Bank Fees -

Rectified

2

5.00

31-08-

2018

To Accounts

Receivable - Rectified

1

4.68

31-08-

2018 By Closing Balance

27,25

3.18

39,82

2.68

39,82

2.68

Answer 5:

2018 Receivable 0.00 2018 Payable 0.00

08-08-

2018

To Accounts

Receivable - Rectified

5,80

0.00

04-08-

2018

By Accounts

Payable

51

1.00

11-08-

2018

To Accounts

Receivable - Rectified

1,33

2.00

08-08-

2018

By Accounts

Payable

66

0.00

13-08-

2018

To Accounts

Receivable

2,13

6.00

10-08-

2018

By Accounts

Payable-Rectified

50

0.00

16-08-

2018

To Accounts

Receivable - Rectified

3,20

0.00

17-08-

2018

By Accounts

Payable

87

0.50

19-08-

2018

To Accounts

Receivable - Rectified

55

0.00

22-08-

2018

By Accounts

Payable

3,14

0.00

24-08-

2018

To Accounts

Receivable

3,20

0.00

24-08-

2018

By Accounts

Payable

1,26

6.00

27-08-

2018

To Accounts

Receivable - Rectified

1,06

5.00

28-08-

2018

By Accounts

Payable-Rectified

20

0.00

29-08-

2018

To Accounts

Receivable

1,20

0.00

31-08-

2018

By Accounts

Payable

97

2.00

31-08-

2018

To Accounts

Receivable

1,60

0.00

31-08-

2018

By Bank Fees -

Rectified

2

5.00

31-08-

2018

To Accounts

Receivable - Rectified

1

4.68

31-08-

2018 By Closing Balance

27,25

3.18

39,82

2.68

39,82

2.68

Answer 5:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING 26

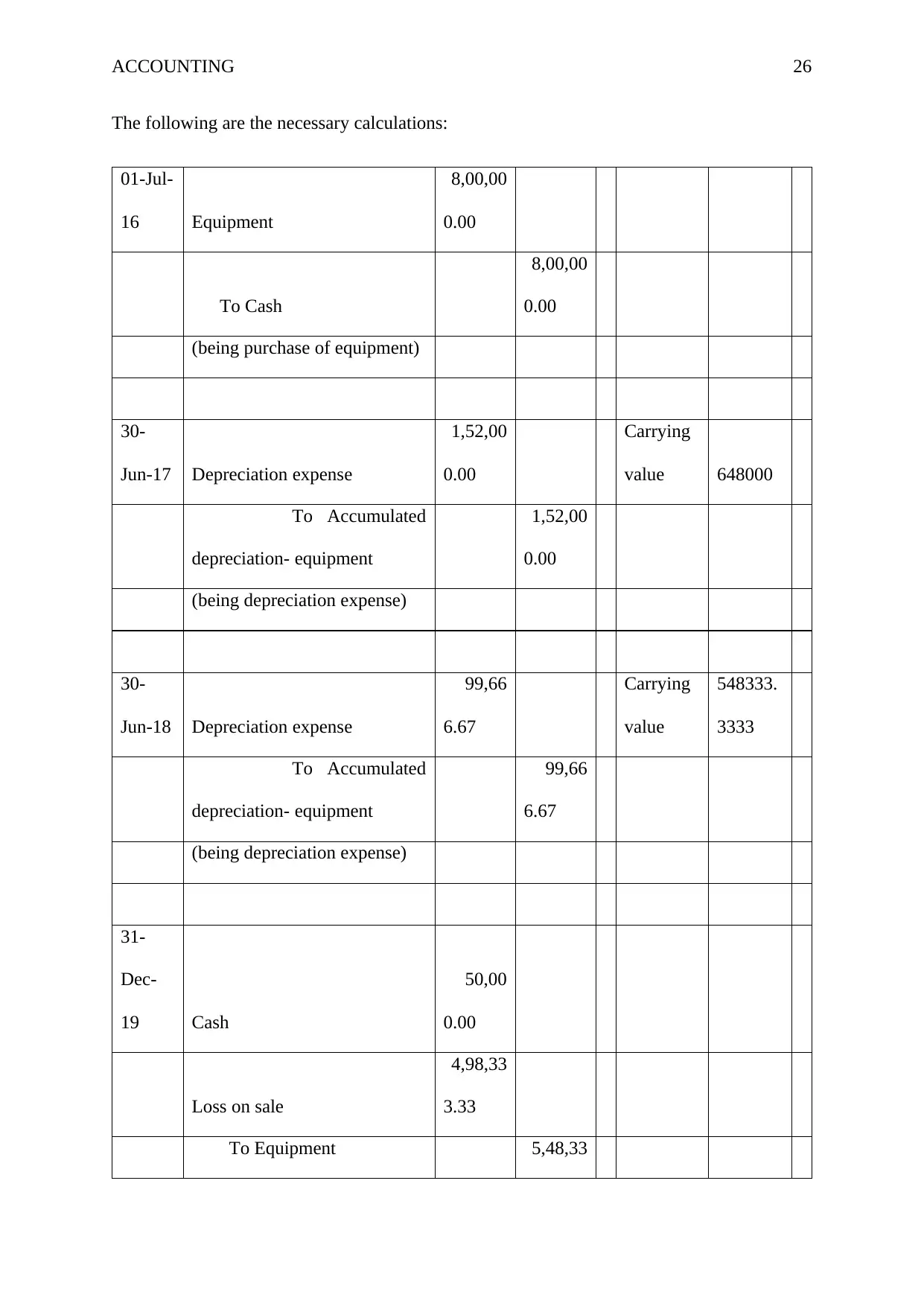

The following are the necessary calculations:

01-Jul-

16 Equipment

8,00,00

0.00

To Cash

8,00,00

0.00

(being purchase of equipment)

30-

Jun-17 Depreciation expense

1,52,00

0.00

Carrying

value 648000

To Accumulated

depreciation- equipment

1,52,00

0.00

(being depreciation expense)

30-

Jun-18 Depreciation expense

99,66

6.67

Carrying

value

548333.

3333

To Accumulated

depreciation- equipment

99,66

6.67

(being depreciation expense)

31-

Dec-

19 Cash

50,00

0.00

Loss on sale

4,98,33

3.33

To Equipment 5,48,33

The following are the necessary calculations:

01-Jul-

16 Equipment

8,00,00

0.00

To Cash

8,00,00

0.00

(being purchase of equipment)

30-

Jun-17 Depreciation expense

1,52,00

0.00

Carrying

value 648000

To Accumulated

depreciation- equipment

1,52,00

0.00

(being depreciation expense)

30-

Jun-18 Depreciation expense

99,66

6.67

Carrying

value

548333.

3333

To Accumulated

depreciation- equipment

99,66

6.67

(being depreciation expense)

31-

Dec-

19 Cash

50,00

0.00

Loss on sale

4,98,33

3.33

To Equipment 5,48,33

ACCOUNTING 27

3.33

(being sale of equipment)

References:

‘The employee strongly denied the evidence’. (2019). Retrieved from

https://www.news.com.au/finance/work/at-work/from-freebies-for-mates-to-150000-

fraud-employee-theft-costs-australian-business-billions/news-story/

ac7b41f93ace63b20ff99b5e3d1b712a

Internal Control Procedures for the Receipt of Cash. (2019). Retrieved from

https://work.chron.com/internal-control-procedures-receipt-cash-6735.html

'Serious breach of trust': Police arrest woman accused of fraud against NAB. (2019).

Retrieved from https://www.abc.net.au/news/2019-03-01/nsw-police-arrest-woman-

accused-of-nab-fraud/10861092

Why cloud accounting is good for business | Xero. (2019). Retrieved from

https://www.xero.com/id/resources/small-business-guides/cloud-accounting/cloud-

accounting-business/

3.33

(being sale of equipment)

References:

‘The employee strongly denied the evidence’. (2019). Retrieved from

https://www.news.com.au/finance/work/at-work/from-freebies-for-mates-to-150000-

fraud-employee-theft-costs-australian-business-billions/news-story/

ac7b41f93ace63b20ff99b5e3d1b712a

Internal Control Procedures for the Receipt of Cash. (2019). Retrieved from

https://work.chron.com/internal-control-procedures-receipt-cash-6735.html

'Serious breach of trust': Police arrest woman accused of fraud against NAB. (2019).

Retrieved from https://www.abc.net.au/news/2019-03-01/nsw-police-arrest-woman-

accused-of-nab-fraud/10861092

Why cloud accounting is good for business | Xero. (2019). Retrieved from

https://www.xero.com/id/resources/small-business-guides/cloud-accounting/cloud-

accounting-business/

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.