Information about Inventory Methods and Cost Flow Assumption

Added on 2023-03-21

9 Pages1950 Words38 Views

ACCOUNTING 1

Accounting

[Name of Writer]

[Name of Institution]

Accounting

[Name of Writer]

[Name of Institution]

ACCOUNTING 2

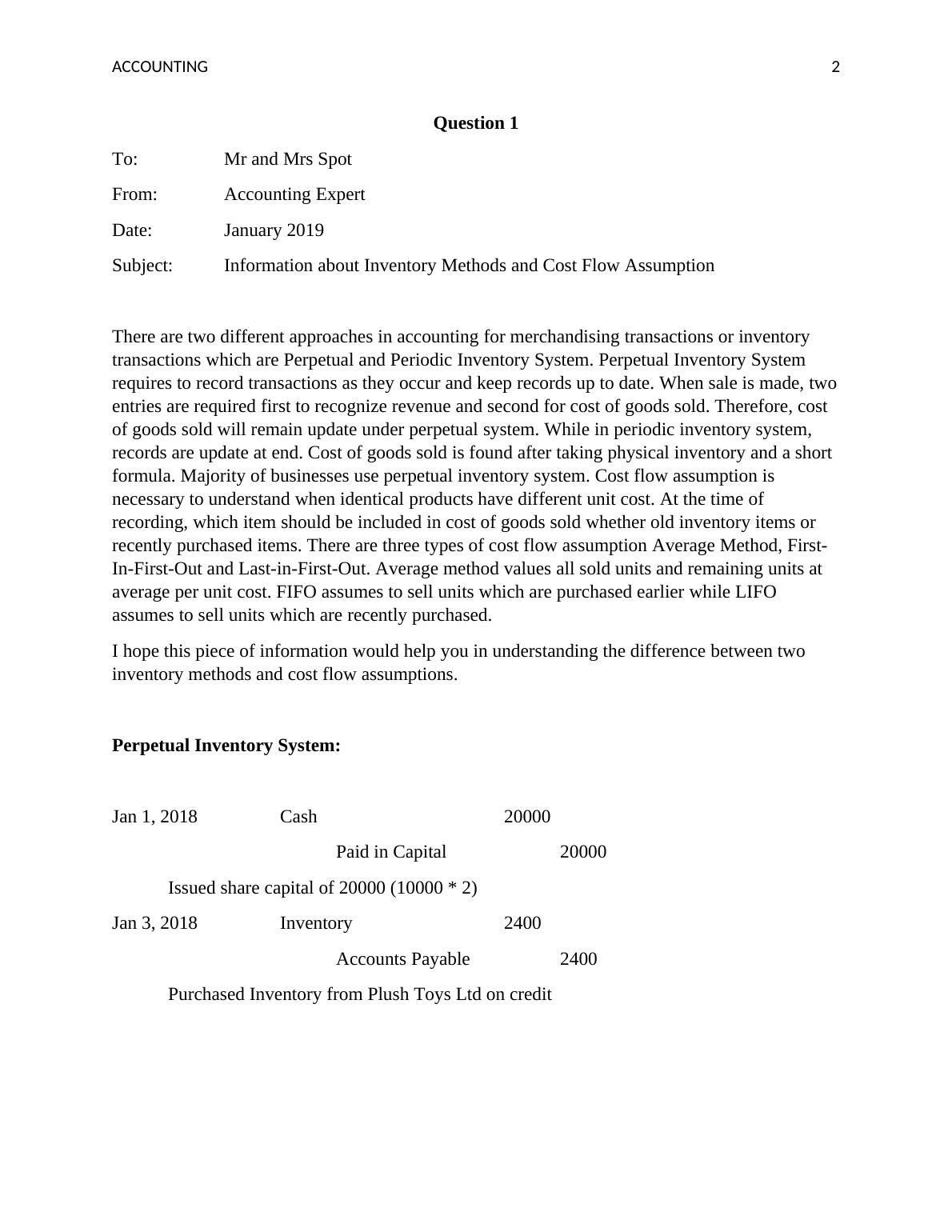

Question 1

To: Mr and Mrs Spot

From: Accounting Expert

Date: January 2019

Subject: Information about Inventory Methods and Cost Flow Assumption

There are two different approaches in accounting for merchandising transactions or inventory

transactions which are Perpetual and Periodic Inventory System. Perpetual Inventory System

requires to record transactions as they occur and keep records up to date. When sale is made, two

entries are required first to recognize revenue and second for cost of goods sold. Therefore, cost

of goods sold will remain update under perpetual system. While in periodic inventory system,

records are update at end. Cost of goods sold is found after taking physical inventory and a short

formula. Majority of businesses use perpetual inventory system. Cost flow assumption is

necessary to understand when identical products have different unit cost. At the time of

recording, which item should be included in cost of goods sold whether old inventory items or

recently purchased items. There are three types of cost flow assumption Average Method, First-

In-First-Out and Last-in-First-Out. Average method values all sold units and remaining units at

average per unit cost. FIFO assumes to sell units which are purchased earlier while LIFO

assumes to sell units which are recently purchased.

I hope this piece of information would help you in understanding the difference between two

inventory methods and cost flow assumptions.

Perpetual Inventory System:

Jan 1, 2018 Cash 20000

Paid in Capital 20000

Issued share capital of 20000 (10000 * 2)

Jan 3, 2018 Inventory 2400

Accounts Payable 2400

Purchased Inventory from Plush Toys Ltd on credit

Question 1

To: Mr and Mrs Spot

From: Accounting Expert

Date: January 2019

Subject: Information about Inventory Methods and Cost Flow Assumption

There are two different approaches in accounting for merchandising transactions or inventory

transactions which are Perpetual and Periodic Inventory System. Perpetual Inventory System

requires to record transactions as they occur and keep records up to date. When sale is made, two

entries are required first to recognize revenue and second for cost of goods sold. Therefore, cost

of goods sold will remain update under perpetual system. While in periodic inventory system,

records are update at end. Cost of goods sold is found after taking physical inventory and a short

formula. Majority of businesses use perpetual inventory system. Cost flow assumption is

necessary to understand when identical products have different unit cost. At the time of

recording, which item should be included in cost of goods sold whether old inventory items or

recently purchased items. There are three types of cost flow assumption Average Method, First-

In-First-Out and Last-in-First-Out. Average method values all sold units and remaining units at

average per unit cost. FIFO assumes to sell units which are purchased earlier while LIFO

assumes to sell units which are recently purchased.

I hope this piece of information would help you in understanding the difference between two

inventory methods and cost flow assumptions.

Perpetual Inventory System:

Jan 1, 2018 Cash 20000

Paid in Capital 20000

Issued share capital of 20000 (10000 * 2)

Jan 3, 2018 Inventory 2400

Accounts Payable 2400

Purchased Inventory from Plush Toys Ltd on credit

ACCOUNTING 3

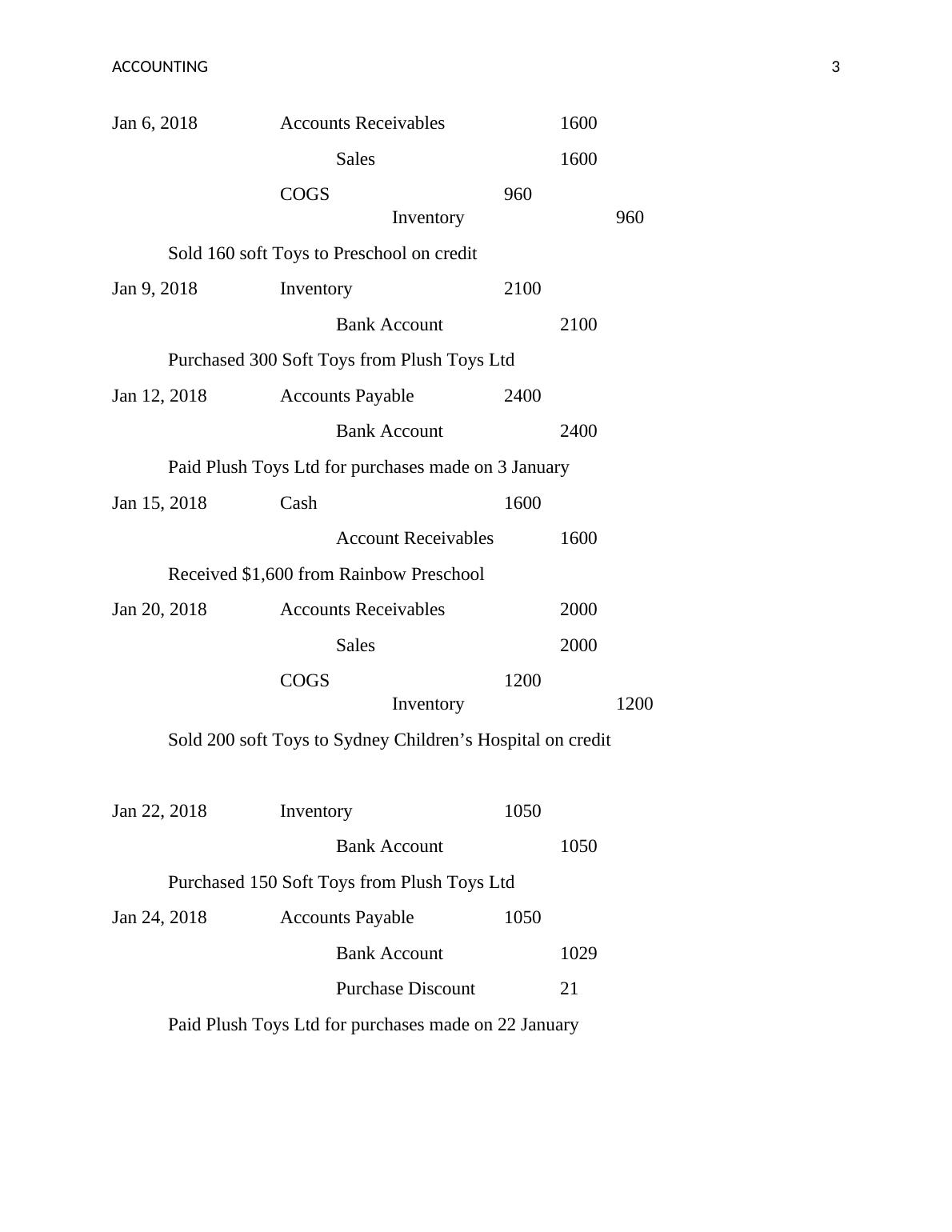

Jan 6, 2018 Accounts Receivables 1600

Sales 1600

COGS 960

Inventory 960

Sold 160 soft Toys to Preschool on credit

Jan 9, 2018 Inventory 2100

Bank Account 2100

Purchased 300 Soft Toys from Plush Toys Ltd

Jan 12, 2018 Accounts Payable 2400

Bank Account 2400

Paid Plush Toys Ltd for purchases made on 3 January

Jan 15, 2018 Cash 1600

Account Receivables 1600

Received $1,600 from Rainbow Preschool

Jan 20, 2018 Accounts Receivables 2000

Sales 2000

COGS 1200

Inventory 1200

Sold 200 soft Toys to Sydney Children’s Hospital on credit

Jan 22, 2018 Inventory 1050

Bank Account 1050

Purchased 150 Soft Toys from Plush Toys Ltd

Jan 24, 2018 Accounts Payable 1050

Bank Account 1029

Purchase Discount 21

Paid Plush Toys Ltd for purchases made on 22 January

Jan 6, 2018 Accounts Receivables 1600

Sales 1600

COGS 960

Inventory 960

Sold 160 soft Toys to Preschool on credit

Jan 9, 2018 Inventory 2100

Bank Account 2100

Purchased 300 Soft Toys from Plush Toys Ltd

Jan 12, 2018 Accounts Payable 2400

Bank Account 2400

Paid Plush Toys Ltd for purchases made on 3 January

Jan 15, 2018 Cash 1600

Account Receivables 1600

Received $1,600 from Rainbow Preschool

Jan 20, 2018 Accounts Receivables 2000

Sales 2000

COGS 1200

Inventory 1200

Sold 200 soft Toys to Sydney Children’s Hospital on credit

Jan 22, 2018 Inventory 1050

Bank Account 1050

Purchased 150 Soft Toys from Plush Toys Ltd

Jan 24, 2018 Accounts Payable 1050

Bank Account 1029

Purchase Discount 21

Paid Plush Toys Ltd for purchases made on 22 January

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Inventory Valuation Methods in Accountinglg...

|27

|3113

|38

Accounting: Memo on Inventory Methodslg...

|10

|2837

|89

Business Managementlg...

|9

|1460

|207

Accounting for Business: Sales, Financial Viability, Break-Even Analysislg...

|12

|1243

|232