Accounting: Memo on Inventory Methods

VerifiedAdded on 2023/01/16

|10

|2837

|89

AI Summary

This memo discusses the different methods of tracking inventory in accounting and their implications on cost of sales. It also explains the First in First out (FIFO) and weighted average methods of determining cost of sales.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: ACCOUNTING

ACCOUNTING

NAME OF STUDENT

NAME OF UNIVERSITY

ACCOUNTING

NAME OF STUDENT

NAME OF UNIVERSITY

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

ACCOUNTING

1. Memo on inventory methods

DATE 09/05/2019 Ref 10/1

From; Accountant Ltd.

To; Mr. & Mrs. Spottie

RE; BRIEF SUMMARY OF INVENTORY METHODS

The cost of sales is used to determine the gross profit of company during a period. However,

determining this cost is subject to interpretation as the stock sold and in hand must be valued

appropriately. The stock could have been acquired at different prices. Each purchase batch may have

incurred some costs which another similar batch in the same period did not incur. For example, one

bath may have a higher handling cost if it was delivered when there were some disruptions form

normal business.

We have two methods of tracking the quantity or stock of goods that are in stock, which are the

perpetual and periodic.

In perpetual method, there is a continuous update of the flow of stock in the company while the

periodic one requires that we do a physical count of what is in stock. The perpetual method requires a

lot of work in the form of continuously updating the records anytime a transaction is made.

For the periodic method one, physical stock state is done on a scheduled basis. The stock in hand is

then used to determine the cost of goods sold during the period. This is the most common method as it

is easier to perform periodic counts that perpetual stock counts (Bragg 2019).

The First in fist out (FIFO) inventory method of determining cost of sales where we assume the first

cost of goods purchased are those that are charged to the cost of sales when goods are sold (Valuing

Inventory | Boundless Accounting 2019). This is mainly used for fresh produce that may get spoilt

easily.

The weighted average method is used to determine the cost of ending inventory by using the weighted

average unit cost. This is mainly used for units which are the same.

Yours faithfully

Accountancy Ltd.

ACCOUNTING

1. Memo on inventory methods

DATE 09/05/2019 Ref 10/1

From; Accountant Ltd.

To; Mr. & Mrs. Spottie

RE; BRIEF SUMMARY OF INVENTORY METHODS

The cost of sales is used to determine the gross profit of company during a period. However,

determining this cost is subject to interpretation as the stock sold and in hand must be valued

appropriately. The stock could have been acquired at different prices. Each purchase batch may have

incurred some costs which another similar batch in the same period did not incur. For example, one

bath may have a higher handling cost if it was delivered when there were some disruptions form

normal business.

We have two methods of tracking the quantity or stock of goods that are in stock, which are the

perpetual and periodic.

In perpetual method, there is a continuous update of the flow of stock in the company while the

periodic one requires that we do a physical count of what is in stock. The perpetual method requires a

lot of work in the form of continuously updating the records anytime a transaction is made.

For the periodic method one, physical stock state is done on a scheduled basis. The stock in hand is

then used to determine the cost of goods sold during the period. This is the most common method as it

is easier to perform periodic counts that perpetual stock counts (Bragg 2019).

The First in fist out (FIFO) inventory method of determining cost of sales where we assume the first

cost of goods purchased are those that are charged to the cost of sales when goods are sold (Valuing

Inventory | Boundless Accounting 2019). This is mainly used for fresh produce that may get spoilt

easily.

The weighted average method is used to determine the cost of ending inventory by using the weighted

average unit cost. This is mainly used for units which are the same.

Yours faithfully

Accountancy Ltd.

3

ACCOUNTING

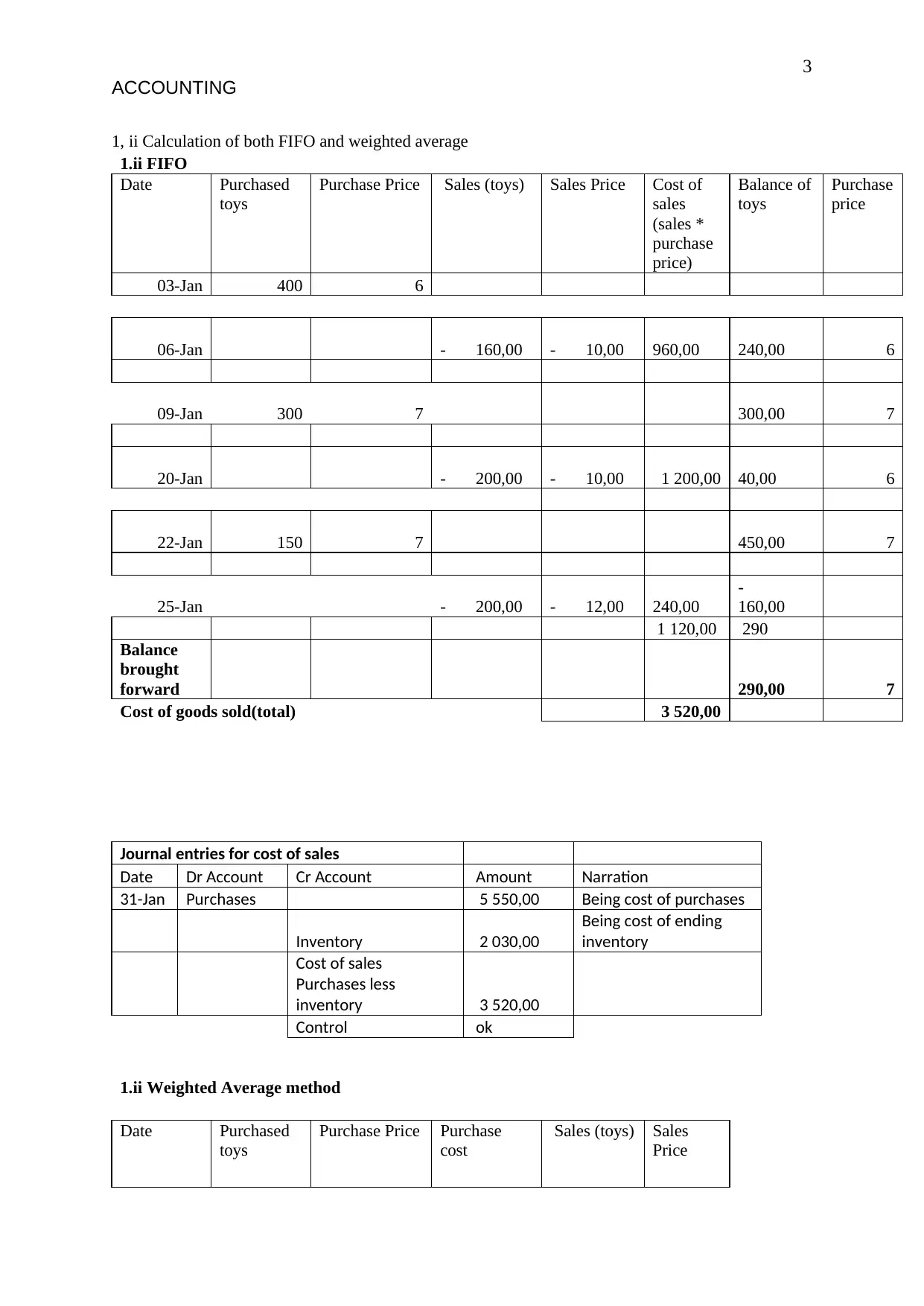

1, ii Calculation of both FIFO and weighted average

1.ii FIFO

Date Purchased

toys

Purchase Price Sales (toys) Sales Price Cost of

sales

(sales *

purchase

price)

Balance of

toys

Purchase

price

03-Jan 400 6

06-Jan - 160,00 - 10,00 960,00 240,00 6

09-Jan 300 7 300,00 7

20-Jan - 200,00 - 10,00 1 200,00 40,00 6

22-Jan 150 7 450,00 7

25-Jan - 200,00 - 12,00 240,00

-

160,00

1 120,00 290

Balance

brought

forward 290,00 7

Cost of goods sold(total) 3 520,00

Journal entries for cost of sales

Date Dr Account Cr Account Amount Narration

31-Jan Purchases 5 550,00 Being cost of purchases

Inventory 2 030,00

Being cost of ending

inventory

Cost of sales

Purchases less

inventory 3 520,00

Control ok

1.ii Weighted Average method

Date Purchased

toys

Purchase Price Purchase

cost

Sales (toys) Sales

Price

ACCOUNTING

1, ii Calculation of both FIFO and weighted average

1.ii FIFO

Date Purchased

toys

Purchase Price Sales (toys) Sales Price Cost of

sales

(sales *

purchase

price)

Balance of

toys

Purchase

price

03-Jan 400 6

06-Jan - 160,00 - 10,00 960,00 240,00 6

09-Jan 300 7 300,00 7

20-Jan - 200,00 - 10,00 1 200,00 40,00 6

22-Jan 150 7 450,00 7

25-Jan - 200,00 - 12,00 240,00

-

160,00

1 120,00 290

Balance

brought

forward 290,00 7

Cost of goods sold(total) 3 520,00

Journal entries for cost of sales

Date Dr Account Cr Account Amount Narration

31-Jan Purchases 5 550,00 Being cost of purchases

Inventory 2 030,00

Being cost of ending

inventory

Cost of sales

Purchases less

inventory 3 520,00

Control ok

1.ii Weighted Average method

Date Purchased

toys

Purchase Price Purchase

cost

Sales (toys) Sales

Price

4

ACCOUNTING

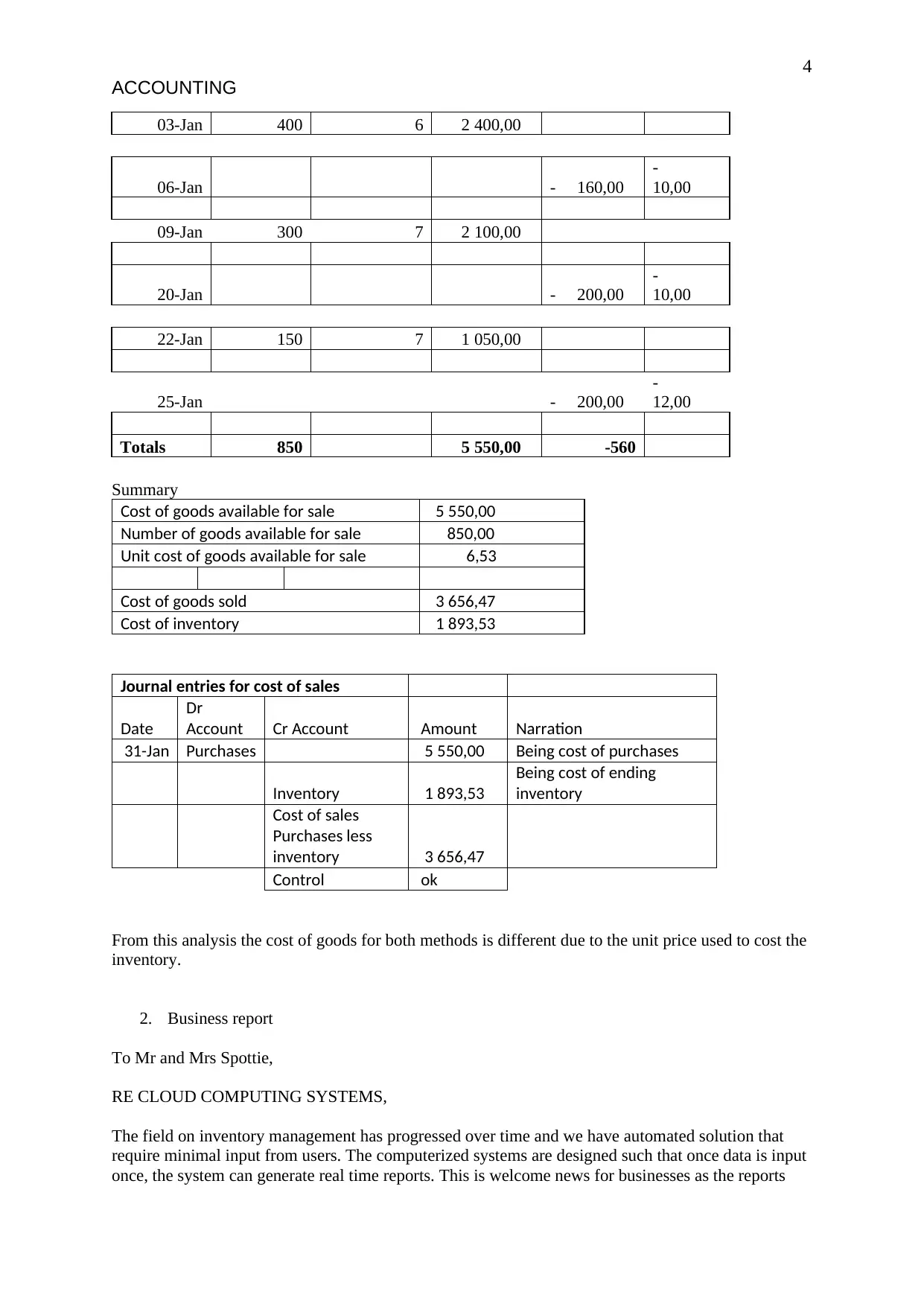

03-Jan 400 6 2 400,00

06-Jan - 160,00

-

10,00

09-Jan 300 7 2 100,00

20-Jan - 200,00

-

10,00

22-Jan 150 7 1 050,00

25-Jan - 200,00

-

12,00

Totals 850 5 550,00 -560

Summary

Cost of goods available for sale 5 550,00

Number of goods available for sale 850,00

Unit cost of goods available for sale 6,53

Cost of goods sold 3 656,47

Cost of inventory 1 893,53

Journal entries for cost of sales

Date

Dr

Account Cr Account Amount Narration

31-Jan Purchases 5 550,00 Being cost of purchases

Inventory 1 893,53

Being cost of ending

inventory

Cost of sales

Purchases less

inventory 3 656,47

Control ok

From this analysis the cost of goods for both methods is different due to the unit price used to cost the

inventory.

2. Business report

To Mr and Mrs Spottie,

RE CLOUD COMPUTING SYSTEMS,

The field on inventory management has progressed over time and we have automated solution that

require minimal input from users. The computerized systems are designed such that once data is input

once, the system can generate real time reports. This is welcome news for businesses as the reports

ACCOUNTING

03-Jan 400 6 2 400,00

06-Jan - 160,00

-

10,00

09-Jan 300 7 2 100,00

20-Jan - 200,00

-

10,00

22-Jan 150 7 1 050,00

25-Jan - 200,00

-

12,00

Totals 850 5 550,00 -560

Summary

Cost of goods available for sale 5 550,00

Number of goods available for sale 850,00

Unit cost of goods available for sale 6,53

Cost of goods sold 3 656,47

Cost of inventory 1 893,53

Journal entries for cost of sales

Date

Dr

Account Cr Account Amount Narration

31-Jan Purchases 5 550,00 Being cost of purchases

Inventory 1 893,53

Being cost of ending

inventory

Cost of sales

Purchases less

inventory 3 656,47

Control ok

From this analysis the cost of goods for both methods is different due to the unit price used to cost the

inventory.

2. Business report

To Mr and Mrs Spottie,

RE CLOUD COMPUTING SYSTEMS,

The field on inventory management has progressed over time and we have automated solution that

require minimal input from users. The computerized systems are designed such that once data is input

once, the system can generate real time reports. This is welcome news for businesses as the reports

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

ACCOUNTING

can be accessed in a timely manner and errors can be recognized early. Automation has the benefit of

remote access. You can also set limits on to what various staff members can do on the system. It can

also show you an audit trail. The audit trail can tell you who was doing what and when they were

doing it. The system can also be set to send you triggers once the thresholds that have been set are

breached. This access to the system removes the dependency on the accountants for some roles.

One of the computerized system in the market is “XERO”. This is cloud-based accounting solution

that compares well with the completion in the market (Krause 2019). For starter it is cloud based

which means that it is accessible over the internet. It is not restricted to a workstation but can be

accessed everywhere there is internet connection. This availability is very key for travelling users as

they can log in and attend to their duties. It can also can accommodate very many users. This means

that as the business expands, the system will be able to accommodate the many users that will require

access. The system is also compatible with mobile phones browsers, Macs and iPhone. This

compatibility is without any loss of features (Fairbanks 2019)

This system has many reports that are typically required from accountants. These range from income

statement, inventory analysis, debtors and creditors listing including aging, financial ratios and the

balance sheet. Inventory tracking is very critical for your company. Xero will give real time reports on

stock levels, sales and purchases. It can be configured to send alerts when reorder levels are reached.

The system will also give reports on the sales and stock level s per items and category. It will be easy

to make decisions concerning stock levels and mix due to the level of detail of this system. It will be

easy to see the fast-moving items and your top buyers and suppliers. It can host 4,000 different items.

The reports are also presented as dashboard for ease of presentation. It can run 50 different reports.

Many of those reports can be customised like sorting, filtering, rearranging columns, set charts and

edit titles. The printing of the reports is also available including exporting to email, PDF, Excel or

Google sheets. Another feature is the archiving of reports for future use.

This system can also be integrated with other peripheral systems such that the systems can update the

Xero reports. This integration also extends to linking of email. It can be programmed to be sending

scheduled reports to emails. This functionality is mainly used by companies who may not wish to

abandon their peripheral systems in favour of an existing functionality in Xero. This seam less

integration will ensure minimal interruptions to its uptake. It can be integrated with over 700

applications. It can integrate with your bank account where you can receive real time updates.

Xero also supports multi-currency prices. This function is a game changer for companies dealing in

many currencies and in more than one country.

Cloud computing saves a lot of time in terms of time, money and personnel to host and support

databases and the system itself. These cost saving can be significant for a typical business.

Reconciliations is also one of the most tedious tasks in accounting. There might be some initial cost to

upskill to the level of a comfortable user. This may require engaging professionals who are conversant

with this software. The first month is offered for free, so you can take advantage of this period to

familiarise yourself with the features. Pricing for similar solutions are based on the number of users.

However, for Xero it has three packages whose pricing is dependent on the number of features. All

plans can support unlimited number of users. Resources freed will be on the number of people

required to perform reconciliations, reporting and classification of financial data. There will be

savings in terms of paper work generated as a significant portion will be online. Retrieval of data and

documents will also be real-time. The released resources can then be channelled towards other

beneficial roles like business development.

Xero can be hosted on wide verity of browsers from Google Chrome, Internet explorer to Safari.

This system can also invoice and bill clients. This functionality is one of the most sought solutions for

solving problems. In addition, it can also generate quotes for customers who may be enquiring on

your items. This is enhanced where clients can interact with the quotes and invoices and accept, reject

and pay for them. On this, it is also possible to add discounts to the clients. It can also support

recurring invoices and billings. You can also attach documents or other items like photos to the

invoices. The system can host your banking statements and perform reconciliations for you.

ACCOUNTING

can be accessed in a timely manner and errors can be recognized early. Automation has the benefit of

remote access. You can also set limits on to what various staff members can do on the system. It can

also show you an audit trail. The audit trail can tell you who was doing what and when they were

doing it. The system can also be set to send you triggers once the thresholds that have been set are

breached. This access to the system removes the dependency on the accountants for some roles.

One of the computerized system in the market is “XERO”. This is cloud-based accounting solution

that compares well with the completion in the market (Krause 2019). For starter it is cloud based

which means that it is accessible over the internet. It is not restricted to a workstation but can be

accessed everywhere there is internet connection. This availability is very key for travelling users as

they can log in and attend to their duties. It can also can accommodate very many users. This means

that as the business expands, the system will be able to accommodate the many users that will require

access. The system is also compatible with mobile phones browsers, Macs and iPhone. This

compatibility is without any loss of features (Fairbanks 2019)

This system has many reports that are typically required from accountants. These range from income

statement, inventory analysis, debtors and creditors listing including aging, financial ratios and the

balance sheet. Inventory tracking is very critical for your company. Xero will give real time reports on

stock levels, sales and purchases. It can be configured to send alerts when reorder levels are reached.

The system will also give reports on the sales and stock level s per items and category. It will be easy

to make decisions concerning stock levels and mix due to the level of detail of this system. It will be

easy to see the fast-moving items and your top buyers and suppliers. It can host 4,000 different items.

The reports are also presented as dashboard for ease of presentation. It can run 50 different reports.

Many of those reports can be customised like sorting, filtering, rearranging columns, set charts and

edit titles. The printing of the reports is also available including exporting to email, PDF, Excel or

Google sheets. Another feature is the archiving of reports for future use.

This system can also be integrated with other peripheral systems such that the systems can update the

Xero reports. This integration also extends to linking of email. It can be programmed to be sending

scheduled reports to emails. This functionality is mainly used by companies who may not wish to

abandon their peripheral systems in favour of an existing functionality in Xero. This seam less

integration will ensure minimal interruptions to its uptake. It can be integrated with over 700

applications. It can integrate with your bank account where you can receive real time updates.

Xero also supports multi-currency prices. This function is a game changer for companies dealing in

many currencies and in more than one country.

Cloud computing saves a lot of time in terms of time, money and personnel to host and support

databases and the system itself. These cost saving can be significant for a typical business.

Reconciliations is also one of the most tedious tasks in accounting. There might be some initial cost to

upskill to the level of a comfortable user. This may require engaging professionals who are conversant

with this software. The first month is offered for free, so you can take advantage of this period to

familiarise yourself with the features. Pricing for similar solutions are based on the number of users.

However, for Xero it has three packages whose pricing is dependent on the number of features. All

plans can support unlimited number of users. Resources freed will be on the number of people

required to perform reconciliations, reporting and classification of financial data. There will be

savings in terms of paper work generated as a significant portion will be online. Retrieval of data and

documents will also be real-time. The released resources can then be channelled towards other

beneficial roles like business development.

Xero can be hosted on wide verity of browsers from Google Chrome, Internet explorer to Safari.

This system can also invoice and bill clients. This functionality is one of the most sought solutions for

solving problems. In addition, it can also generate quotes for customers who may be enquiring on

your items. This is enhanced where clients can interact with the quotes and invoices and accept, reject

and pay for them. On this, it is also possible to add discounts to the clients. It can also support

recurring invoices and billings. You can also attach documents or other items like photos to the

invoices. The system can host your banking statements and perform reconciliations for you.

6

ACCOUNTING

Other features that make it easy to use are; history where in the example of an invoice, you can from

which quote it was quoted from, who edited it and who it was sent to.

You can copy bills and edit them instead of creating new bills. The interface is easy to use and has

many “how to guides” including videos. It even has a demo company to get you started.

All in all, Xero cloud-based accounting system has many benefits. The benefits will go a long way in

freeing up your time so that you can dedicate it in business management and more precise on

analysing the accounting data. The benefits will far outweigh the costs incurred to use the system.

References

Krause, C. (2019). Xero Review 2019 | Reviews, Ratings, Complaints, Comparisons. Retrieved from

https://www.merchantmaverick.com/reviews/xero-review/

FAIRBANKS, L. (2019). Xero Review 2019 | Accounting Software Reviews. Retrieved from

https://www.business.com/reviews/xero-accounting-software/

3. Suggestion of improvement in internal controls

To Mr and Mrs Spottie,

RE REVIEW OF CONTROLS OVER CASH PAYMENTS AND RECIEPTS

Considering increasing cases of staff fraud across the country and the fact that your business is

expanding fast, I urge you to review your controls over cash payments and receipts. Even if you have

not experienced any issues with this item, it is my opinion that it poses a significant risk to your

business. I note that your cash payments and receipts more than doubled over the previous year. Cash

in hand may present temptation to staff to steal. You may not know when a staff decides to go rogue.

It is better to be proactive than reactive.

I will give a review of two cases that were in our news recently to illustrate my concerns. The first one

is from https://www.abc.net.au/news/2018-10-25/worker-sentenced-over-1.2-million-dollar-fraud/

10428334. In this case it is simply a question of betrayal of trust by the employee. It seems the owners

placed trust on the employee and did not put controls to avert this situation. Lack of controls means

that this case of theft could not be arrested in time. The employee in question does not seem to have

criminal intent, she seems to have taken the money because it was there and there were weak controls.

Some of the controls that could have worked were on daily reconciliation of the cash receipts or

separation of her role with handling of cash.

The second case is taken from https://www.smh.com.au/national/electrical-store-20m-fraud-case-in-

court-20091218-l5vh.html. The employee, an accountant took advantage of the loophole of changing

beneficiary details of whoever was being paid. Like the first case, she did not have criminal intent but

was obsessed with being a winner in auctions. In this case we see an effort by the company to do

reconciliations, which uncovered this fraud. It seems if the reconciliations were being done in a

regular manner and by an independent person, this case could have been discovered earlier. Presence

of such controls can also hinder such a staff from conducting such frauds as they know they will be

caught.

In our case and considering the highlighted case examples, I suggest that you institute the following

controls in the cash payments;

a) All cash payments must have an acknowledgment like a receipt. At the very least there must

be an acknowledgement of the recipient of the cash and the details of the recipient captured.

b) Cash payments must be approved by the supervisor of the cashier.

ACCOUNTING

Other features that make it easy to use are; history where in the example of an invoice, you can from

which quote it was quoted from, who edited it and who it was sent to.

You can copy bills and edit them instead of creating new bills. The interface is easy to use and has

many “how to guides” including videos. It even has a demo company to get you started.

All in all, Xero cloud-based accounting system has many benefits. The benefits will go a long way in

freeing up your time so that you can dedicate it in business management and more precise on

analysing the accounting data. The benefits will far outweigh the costs incurred to use the system.

References

Krause, C. (2019). Xero Review 2019 | Reviews, Ratings, Complaints, Comparisons. Retrieved from

https://www.merchantmaverick.com/reviews/xero-review/

FAIRBANKS, L. (2019). Xero Review 2019 | Accounting Software Reviews. Retrieved from

https://www.business.com/reviews/xero-accounting-software/

3. Suggestion of improvement in internal controls

To Mr and Mrs Spottie,

RE REVIEW OF CONTROLS OVER CASH PAYMENTS AND RECIEPTS

Considering increasing cases of staff fraud across the country and the fact that your business is

expanding fast, I urge you to review your controls over cash payments and receipts. Even if you have

not experienced any issues with this item, it is my opinion that it poses a significant risk to your

business. I note that your cash payments and receipts more than doubled over the previous year. Cash

in hand may present temptation to staff to steal. You may not know when a staff decides to go rogue.

It is better to be proactive than reactive.

I will give a review of two cases that were in our news recently to illustrate my concerns. The first one

is from https://www.abc.net.au/news/2018-10-25/worker-sentenced-over-1.2-million-dollar-fraud/

10428334. In this case it is simply a question of betrayal of trust by the employee. It seems the owners

placed trust on the employee and did not put controls to avert this situation. Lack of controls means

that this case of theft could not be arrested in time. The employee in question does not seem to have

criminal intent, she seems to have taken the money because it was there and there were weak controls.

Some of the controls that could have worked were on daily reconciliation of the cash receipts or

separation of her role with handling of cash.

The second case is taken from https://www.smh.com.au/national/electrical-store-20m-fraud-case-in-

court-20091218-l5vh.html. The employee, an accountant took advantage of the loophole of changing

beneficiary details of whoever was being paid. Like the first case, she did not have criminal intent but

was obsessed with being a winner in auctions. In this case we see an effort by the company to do

reconciliations, which uncovered this fraud. It seems if the reconciliations were being done in a

regular manner and by an independent person, this case could have been discovered earlier. Presence

of such controls can also hinder such a staff from conducting such frauds as they know they will be

caught.

In our case and considering the highlighted case examples, I suggest that you institute the following

controls in the cash payments;

a) All cash payments must have an acknowledgment like a receipt. At the very least there must

be an acknowledgement of the recipient of the cash and the details of the recipient captured.

b) Cash payments must be approved by the supervisor of the cashier.

7

ACCOUNTING

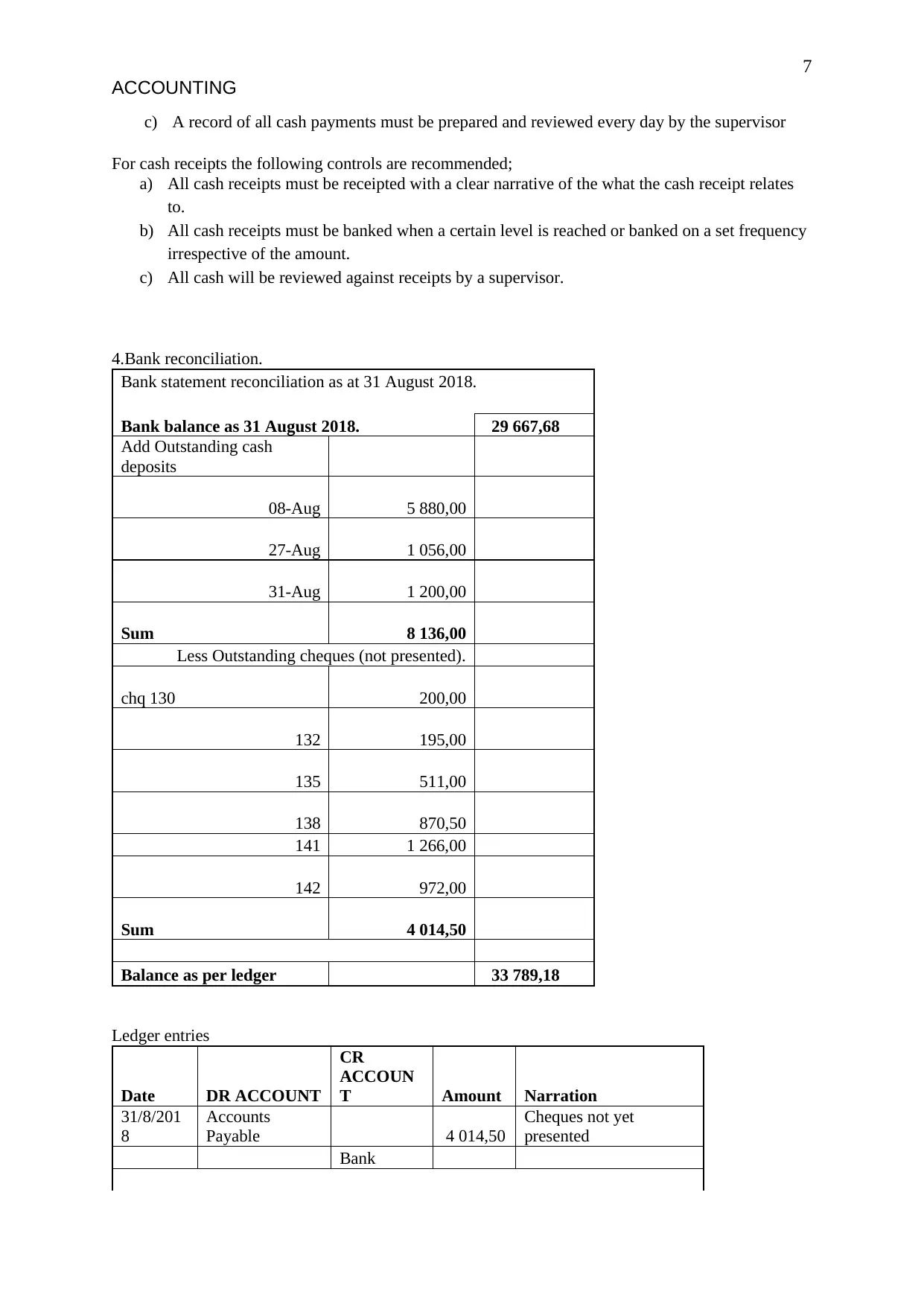

c) A record of all cash payments must be prepared and reviewed every day by the supervisor

For cash receipts the following controls are recommended;

a) All cash receipts must be receipted with a clear narrative of the what the cash receipt relates

to.

b) All cash receipts must be banked when a certain level is reached or banked on a set frequency

irrespective of the amount.

c) All cash will be reviewed against receipts by a supervisor.

4.Bank reconciliation.

Bank statement reconciliation as at 31 August 2018.

Bank balance as 31 August 2018. 29 667,68

Add Outstanding cash

deposits

08-Aug 5 880,00

27-Aug 1 056,00

31-Aug 1 200,00

Sum 8 136,00

Less Outstanding cheques (not presented).

chq 130 200,00

132 195,00

135 511,00

138 870,50

141 1 266,00

142 972,00

Sum 4 014,50

Balance as per ledger 33 789,18

Ledger entries

Date DR ACCOUNT

CR

ACCOUN

T Amount Narration

31/8/201

8

Accounts

Payable 4 014,50

Cheques not yet

presented

Bank

ACCOUNTING

c) A record of all cash payments must be prepared and reviewed every day by the supervisor

For cash receipts the following controls are recommended;

a) All cash receipts must be receipted with a clear narrative of the what the cash receipt relates

to.

b) All cash receipts must be banked when a certain level is reached or banked on a set frequency

irrespective of the amount.

c) All cash will be reviewed against receipts by a supervisor.

4.Bank reconciliation.

Bank statement reconciliation as at 31 August 2018.

Bank balance as 31 August 2018. 29 667,68

Add Outstanding cash

deposits

08-Aug 5 880,00

27-Aug 1 056,00

31-Aug 1 200,00

Sum 8 136,00

Less Outstanding cheques (not presented).

chq 130 200,00

132 195,00

135 511,00

138 870,50

141 1 266,00

142 972,00

Sum 4 014,50

Balance as per ledger 33 789,18

Ledger entries

Date DR ACCOUNT

CR

ACCOUN

T Amount Narration

31/8/201

8

Accounts

Payable 4 014,50

Cheques not yet

presented

Bank

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

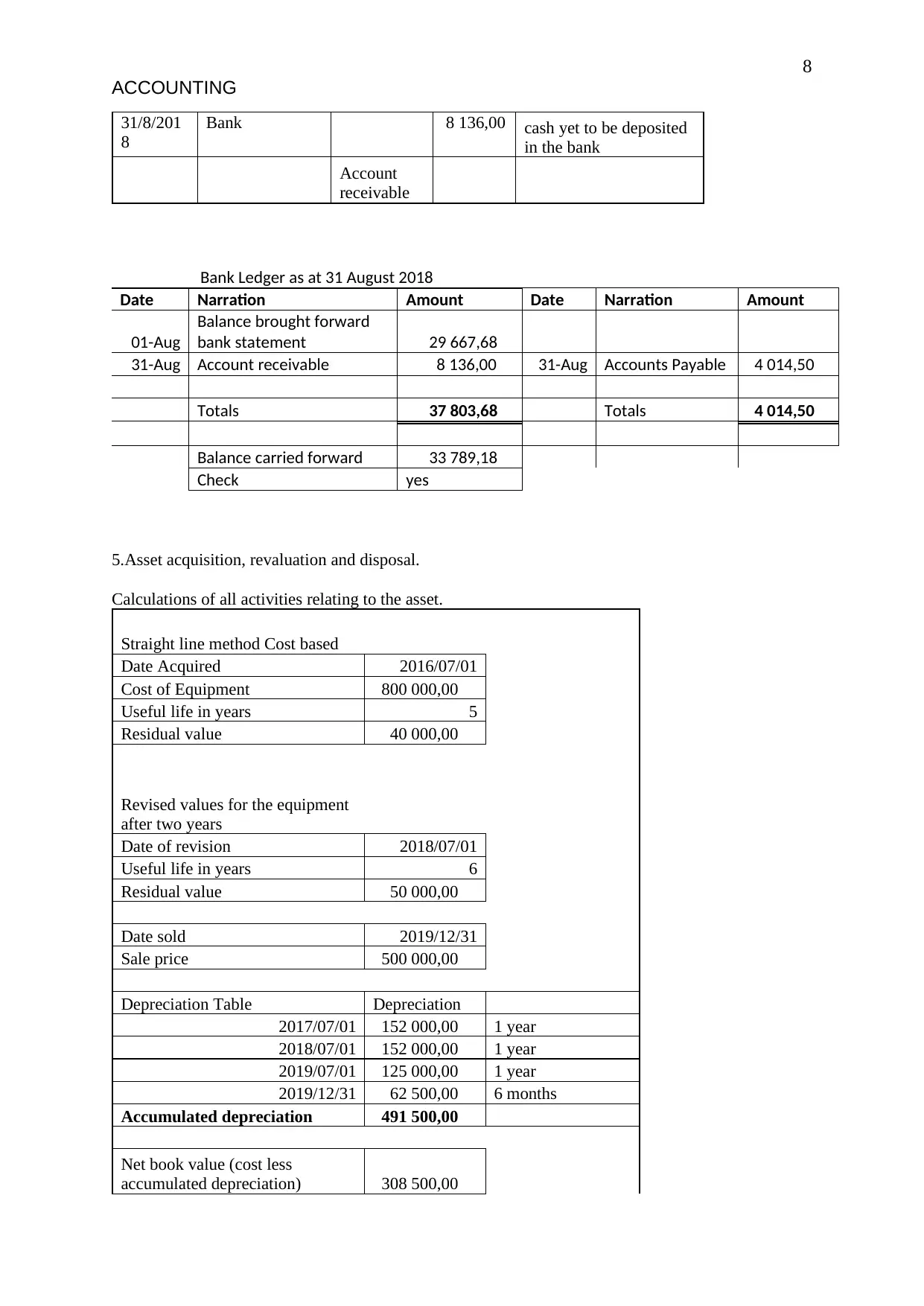

8

ACCOUNTING

31/8/201

8

Bank 8 136,00 cash yet to be deposited

in the bank

Account

receivable

Bank Ledger as at 31 August 2018

Date Narration Amount Date Narration Amount

01-Aug

Balance brought forward

bank statement 29 667,68

31-Aug Account receivable 8 136,00 31-Aug Accounts Payable 4 014,50

Totals 37 803,68 Totals 4 014,50

Balance carried forward 33 789,18

Check yes

5.Asset acquisition, revaluation and disposal.

Calculations of all activities relating to the asset.

Straight line method Cost based

Date Acquired 2016/07/01

Cost of Equipment 800 000,00

Useful life in years 5

Residual value 40 000,00

Revised values for the equipment

after two years

Date of revision 2018/07/01

Useful life in years 6

Residual value 50 000,00

Date sold 2019/12/31

Sale price 500 000,00

Depreciation Table Depreciation

2017/07/01 152 000,00 1 year

2018/07/01 152 000,00 1 year

2019/07/01 125 000,00 1 year

2019/12/31 62 500,00 6 months

Accumulated depreciation 491 500,00

Net book value (cost less

accumulated depreciation) 308 500,00

ACCOUNTING

31/8/201

8

Bank 8 136,00 cash yet to be deposited

in the bank

Account

receivable

Bank Ledger as at 31 August 2018

Date Narration Amount Date Narration Amount

01-Aug

Balance brought forward

bank statement 29 667,68

31-Aug Account receivable 8 136,00 31-Aug Accounts Payable 4 014,50

Totals 37 803,68 Totals 4 014,50

Balance carried forward 33 789,18

Check yes

5.Asset acquisition, revaluation and disposal.

Calculations of all activities relating to the asset.

Straight line method Cost based

Date Acquired 2016/07/01

Cost of Equipment 800 000,00

Useful life in years 5

Residual value 40 000,00

Revised values for the equipment

after two years

Date of revision 2018/07/01

Useful life in years 6

Residual value 50 000,00

Date sold 2019/12/31

Sale price 500 000,00

Depreciation Table Depreciation

2017/07/01 152 000,00 1 year

2018/07/01 152 000,00 1 year

2019/07/01 125 000,00 1 year

2019/12/31 62 500,00 6 months

Accumulated depreciation 491 500,00

Net book value (cost less

accumulated depreciation) 308 500,00

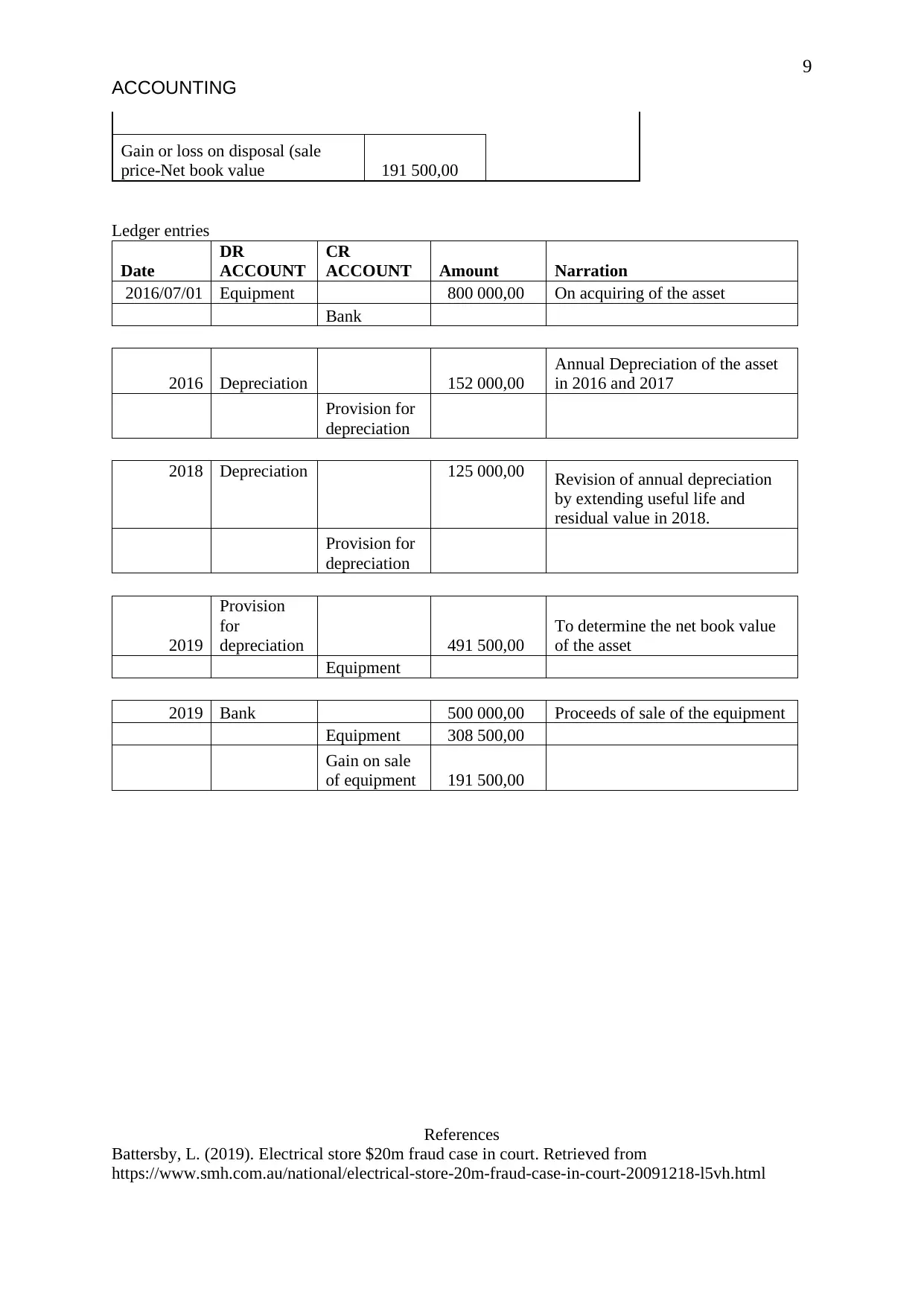

9

ACCOUNTING

Gain or loss on disposal (sale

price-Net book value 191 500,00

Ledger entries

Date

DR

ACCOUNT

CR

ACCOUNT Amount Narration

2016/07/01 Equipment 800 000,00 On acquiring of the asset

Bank

2016 Depreciation 152 000,00

Annual Depreciation of the asset

in 2016 and 2017

Provision for

depreciation

2018 Depreciation 125 000,00 Revision of annual depreciation

by extending useful life and

residual value in 2018.

Provision for

depreciation

2019

Provision

for

depreciation 491 500,00

To determine the net book value

of the asset

Equipment

2019 Bank 500 000,00 Proceeds of sale of the equipment

Equipment 308 500,00

Gain on sale

of equipment 191 500,00

References

Battersby, L. (2019). Electrical store $20m fraud case in court. Retrieved from

https://www.smh.com.au/national/electrical-store-20m-fraud-case-in-court-20091218-l5vh.html

ACCOUNTING

Gain or loss on disposal (sale

price-Net book value 191 500,00

Ledger entries

Date

DR

ACCOUNT

CR

ACCOUNT Amount Narration

2016/07/01 Equipment 800 000,00 On acquiring of the asset

Bank

2016 Depreciation 152 000,00

Annual Depreciation of the asset

in 2016 and 2017

Provision for

depreciation

2018 Depreciation 125 000,00 Revision of annual depreciation

by extending useful life and

residual value in 2018.

Provision for

depreciation

2019

Provision

for

depreciation 491 500,00

To determine the net book value

of the asset

Equipment

2019 Bank 500 000,00 Proceeds of sale of the equipment

Equipment 308 500,00

Gain on sale

of equipment 191 500,00

References

Battersby, L. (2019). Electrical store $20m fraud case in court. Retrieved from

https://www.smh.com.au/national/electrical-store-20m-fraud-case-in-court-20091218-l5vh.html

10

ACCOUNTING

Bragg, S. (2019). The difference between the periodic and perpetual inventory systems. Retrieved

from https://www.accountingtools.com/articles/what-is-the-difference-between-the-periodic-and-

perpetual-in.html

FAIRBANKS, L. (2019). Xero Review 2019 | Accounting Software Reviews. Retrieved from

https://www.business.com/reviews/xero-accounting-software/

Krause, C. (2019). Xero Review 2019 | Reviews, Ratings, Complaints, Comparisons. Retrieved from

https://www.merchantmaverick.com/reviews/xero-review/

Valuing Inventory | Boundless Accounting. (2019). Retrieved from

https://courses.lumenlearning.com/boundless-accounting/chapter/valuing-inventory/

Worker stole $1.2 million from employers so she could 'go shopping, have coffee'. (2019). Retrieved

from https://www.abc.net.au/news/2018-10-25/worker-sentenced-over-1.2-million-dollar-fraud/

10428334

ACCOUNTING

Bragg, S. (2019). The difference between the periodic and perpetual inventory systems. Retrieved

from https://www.accountingtools.com/articles/what-is-the-difference-between-the-periodic-and-

perpetual-in.html

FAIRBANKS, L. (2019). Xero Review 2019 | Accounting Software Reviews. Retrieved from

https://www.business.com/reviews/xero-accounting-software/

Krause, C. (2019). Xero Review 2019 | Reviews, Ratings, Complaints, Comparisons. Retrieved from

https://www.merchantmaverick.com/reviews/xero-review/

Valuing Inventory | Boundless Accounting. (2019). Retrieved from

https://courses.lumenlearning.com/boundless-accounting/chapter/valuing-inventory/

Worker stole $1.2 million from employers so she could 'go shopping, have coffee'. (2019). Retrieved

from https://www.abc.net.au/news/2018-10-25/worker-sentenced-over-1.2-million-dollar-fraud/

10428334

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.