Financial Performance Analysis of Easy Jet Airways (AC4410)

VerifiedAdded on 2023/04/21

|18

|2744

|424

Report

AI Summary

This report provides a comprehensive financial analysis of Easy Jet Airways, a British low-cost airline carrier listed on the London Stock Exchange, examining its financial performance from 2015 to 2018. The analysis begins with an executive summary and an introduction to the company, followed by a detailed exploration of ratio analysis, including its benefits and limitations. The core of the report focuses on calculating and interpreting various financial ratios, including profitability ratios like ROCE, gross profit margin, and operating profit ratio; liquidity ratios such as the current ratio and acid-test ratio; and gearing ratios, specifically the gearing ratio and interest cover ratio. The report presents the calculations for each ratio over the four-year period, along with interpretations of the trends and implications for Easy Jet Airways' financial health and performance. The conclusion summarizes the key findings, highlighting the company's debt levels, profitability, and liquidity, and suggests the need for comparative analysis with industry peers. Appendices provide supporting financial information, including ratio summaries and extracts from annual reports.

Running head: ACCOUNTING AND FINANCE

Accounting and Finance

Name of the Student

Name of the University

Authors Note

Course ID

Accounting and Finance

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING AND FINANCE

Executive Summary:

The present report is aimed at reviewing the ratios of Easy Jet Airways. Initially the report

would assess the benefits and limitations of accounting ratios. In the later part the

profitability, liquidity and interest cover ratios would be computed to assess the financial

position of Easy Jet Airways. The computation of financial ratios would be based from the

financial year of 2015 to 2018. Easy Jet Airways is an established british low cost airline

carrier which is listed in the London stock exchange under the FTSE Index 100.

Executive Summary:

The present report is aimed at reviewing the ratios of Easy Jet Airways. Initially the report

would assess the benefits and limitations of accounting ratios. In the later part the

profitability, liquidity and interest cover ratios would be computed to assess the financial

position of Easy Jet Airways. The computation of financial ratios would be based from the

financial year of 2015 to 2018. Easy Jet Airways is an established british low cost airline

carrier which is listed in the London stock exchange under the FTSE Index 100.

2ACCOUNTING AND FINANCE

Table of Contents

Introduction................................................................................................................................4

Ratio Analysis:...........................................................................................................................4

Benefits of Ratio Analysis:....................................................................................................4

Limitations of Ratio Analysis:...............................................................................................5

Profitability Ratios:....................................................................................................................6

ROCE ratio:............................................................................................................................6

Gross Profit Margin:..............................................................................................................6

Operating Profit Ratio:...........................................................................................................7

Liquidity Ratios:.........................................................................................................................7

Current Ratio:.........................................................................................................................8

Acid Test Ratio:.....................................................................................................................8

Gearing/Capital Structure Ratios:..............................................................................................9

Gearing Ratio:........................................................................................................................9

Interest Cover Ratio:..............................................................................................................9

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

Appendices:..............................................................................................................................13

Appendix 1: Ratio Summary................................................................................................13

Appendix 2: Easy Jet Airways Financial Information Summary:.......................................13

Appendix 3: Annual Report Extracts:..................................................................................14

Table of Contents

Introduction................................................................................................................................4

Ratio Analysis:...........................................................................................................................4

Benefits of Ratio Analysis:....................................................................................................4

Limitations of Ratio Analysis:...............................................................................................5

Profitability Ratios:....................................................................................................................6

ROCE ratio:............................................................................................................................6

Gross Profit Margin:..............................................................................................................6

Operating Profit Ratio:...........................................................................................................7

Liquidity Ratios:.........................................................................................................................7

Current Ratio:.........................................................................................................................8

Acid Test Ratio:.....................................................................................................................8

Gearing/Capital Structure Ratios:..............................................................................................9

Gearing Ratio:........................................................................................................................9

Interest Cover Ratio:..............................................................................................................9

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

Appendices:..............................................................................................................................13

Appendix 1: Ratio Summary................................................................................................13

Appendix 2: Easy Jet Airways Financial Information Summary:.......................................13

Appendix 3: Annual Report Extracts:..................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING AND FINANCE

Introduction

Easy Jet Airline is the British low cost airline carrier that has its headquarter in

London Luton Airport. The company operates both the international and domestic services in

more than 820 routes to more than 30 nations. The company is listed on the FTSE 100 index

and has the largest shareholders stake of 34.62% (Corporate.easyjet.com 2019). The company

employs more than 11,000 employees that is based through Europe large part of the

employees are based in UK.

Easy Jet has witnessed expansion from the day it was established in 1995. Easy Jet

has growth through the combination of acquisition and the base opening is boosted by

customer demands for lost cost transportation. Easy Jet together with its associate company

Easy Jet Europe and Easy Jet Switzerland operates greater than 200 carriers with majority are

Airbus A320 (Corporate.easyjet.com 2019). During the year 2007 Easy Jet acquired the

entire share of GB Airways from the Bland Group. While in 2011 Easy Jet opened its

eleventh British airline base at London Southend Airport.

Ratio Analysis:

According to (_) ratio analysis is defined as the analysis and interpretation of the

figures that appears on the financial reports. Ratio analysis is regarded as the procedure of

comparing the figures of one year against another year. Ratio analysis provides the users of

financial report such as government, shareholders, creditor and investors to better understand

the financial reports.

Benefits of Ratio Analysis:

The benefits of ratio analysis are as follows;

Introduction

Easy Jet Airline is the British low cost airline carrier that has its headquarter in

London Luton Airport. The company operates both the international and domestic services in

more than 820 routes to more than 30 nations. The company is listed on the FTSE 100 index

and has the largest shareholders stake of 34.62% (Corporate.easyjet.com 2019). The company

employs more than 11,000 employees that is based through Europe large part of the

employees are based in UK.

Easy Jet has witnessed expansion from the day it was established in 1995. Easy Jet

has growth through the combination of acquisition and the base opening is boosted by

customer demands for lost cost transportation. Easy Jet together with its associate company

Easy Jet Europe and Easy Jet Switzerland operates greater than 200 carriers with majority are

Airbus A320 (Corporate.easyjet.com 2019). During the year 2007 Easy Jet acquired the

entire share of GB Airways from the Bland Group. While in 2011 Easy Jet opened its

eleventh British airline base at London Southend Airport.

Ratio Analysis:

According to (_) ratio analysis is defined as the analysis and interpretation of the

figures that appears on the financial reports. Ratio analysis is regarded as the procedure of

comparing the figures of one year against another year. Ratio analysis provides the users of

financial report such as government, shareholders, creditor and investors to better understand

the financial reports.

Benefits of Ratio Analysis:

The benefits of ratio analysis are as follows;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING AND FINANCE

Forecasting and Planning: Ratio analysis helps in computing the trend of cost, sales and

profits. Ratio analysis facilitates trend analysis for better forecasting and future planning of

the business.

Budgeting: Budgets refers to the estimation of future activities based on the historical

understanding (Deegan 2014). The accounting ratios are helpful in projecting the budget

figures.

Inter-Firm Comparison: Ratio analysis facilitates inter-firm comparison based on the

average ratios of the industry. It helps in comparative performance of two firms to disclose

the effective and non-competent firms.

Limitations of Ratio Analysis:

In spite of the benefits of ratio analysis it suffers from the following limitations;

Limitation of financial reports: Accounting ratios are computed based on the information

presented in the financial reports (Khan 2015). However, financial statements suffers from

certain limitations that may hamper the quality of ratio analysis.

Historical information: The financial reports does not reflect the present state of affairs as

they are based on the historical information. Therefore, accounting ratios are not helpful in

determining the future.

Changes in level of price: In the financial statement fixed asset are shown only at cost and

does not provides the changes in level of price. This makes difficulty in comparison.

Ratios account for only one variable: As ratio only accounts for one variable therefore, it

cannot regularly provide the accurate picture because other variance namely economic

situations, government policies and resource availability must be kept in mind while

interpreting ratios.

Forecasting and Planning: Ratio analysis helps in computing the trend of cost, sales and

profits. Ratio analysis facilitates trend analysis for better forecasting and future planning of

the business.

Budgeting: Budgets refers to the estimation of future activities based on the historical

understanding (Deegan 2014). The accounting ratios are helpful in projecting the budget

figures.

Inter-Firm Comparison: Ratio analysis facilitates inter-firm comparison based on the

average ratios of the industry. It helps in comparative performance of two firms to disclose

the effective and non-competent firms.

Limitations of Ratio Analysis:

In spite of the benefits of ratio analysis it suffers from the following limitations;

Limitation of financial reports: Accounting ratios are computed based on the information

presented in the financial reports (Khan 2015). However, financial statements suffers from

certain limitations that may hamper the quality of ratio analysis.

Historical information: The financial reports does not reflect the present state of affairs as

they are based on the historical information. Therefore, accounting ratios are not helpful in

determining the future.

Changes in level of price: In the financial statement fixed asset are shown only at cost and

does not provides the changes in level of price. This makes difficulty in comparison.

Ratios account for only one variable: As ratio only accounts for one variable therefore, it

cannot regularly provide the accurate picture because other variance namely economic

situations, government policies and resource availability must be kept in mind while

interpreting ratios.

5ACCOUNTING AND FINANCE

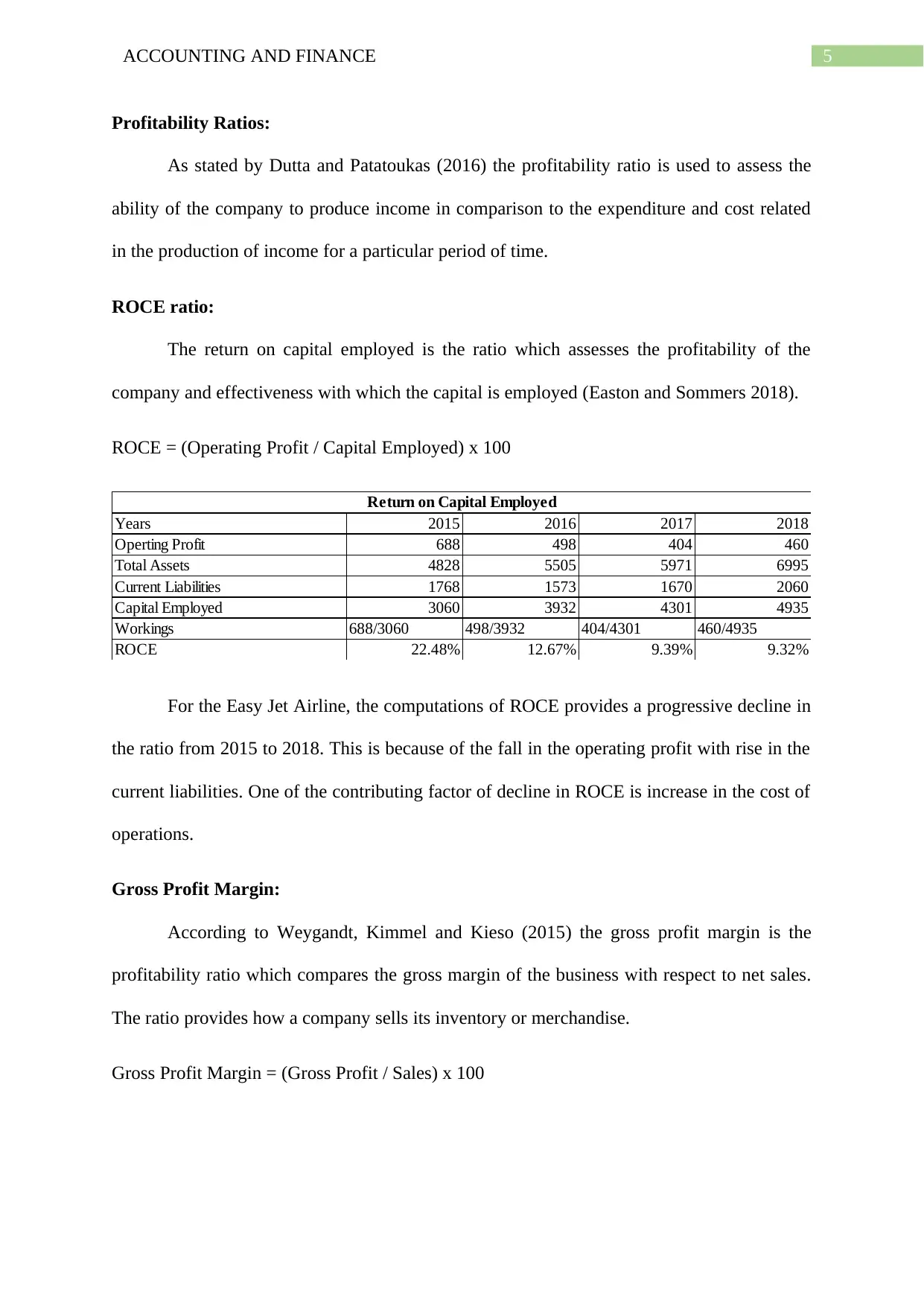

Profitability Ratios:

As stated by Dutta and Patatoukas (2016) the profitability ratio is used to assess the

ability of the company to produce income in comparison to the expenditure and cost related

in the production of income for a particular period of time.

ROCE ratio:

The return on capital employed is the ratio which assesses the profitability of the

company and effectiveness with which the capital is employed (Easton and Sommers 2018).

ROCE = (Operating Profit / Capital Employed) x 100

Years 2015 2016 2017 2018

Operting Profit 688 498 404 460

Total Assets 4828 5505 5971 6995

Current Liabilities 1768 1573 1670 2060

Capital Employed 3060 3932 4301 4935

Workings 688/3060 498/3932 404/4301 460/4935

ROCE 22.48% 12.67% 9.39% 9.32%

Return on Capital Employed

For the Easy Jet Airline, the computations of ROCE provides a progressive decline in

the ratio from 2015 to 2018. This is because of the fall in the operating profit with rise in the

current liabilities. One of the contributing factor of decline in ROCE is increase in the cost of

operations.

Gross Profit Margin:

According to Weygandt, Kimmel and Kieso (2015) the gross profit margin is the

profitability ratio which compares the gross margin of the business with respect to net sales.

The ratio provides how a company sells its inventory or merchandise.

Gross Profit Margin = (Gross Profit / Sales) x 100

Profitability Ratios:

As stated by Dutta and Patatoukas (2016) the profitability ratio is used to assess the

ability of the company to produce income in comparison to the expenditure and cost related

in the production of income for a particular period of time.

ROCE ratio:

The return on capital employed is the ratio which assesses the profitability of the

company and effectiveness with which the capital is employed (Easton and Sommers 2018).

ROCE = (Operating Profit / Capital Employed) x 100

Years 2015 2016 2017 2018

Operting Profit 688 498 404 460

Total Assets 4828 5505 5971 6995

Current Liabilities 1768 1573 1670 2060

Capital Employed 3060 3932 4301 4935

Workings 688/3060 498/3932 404/4301 460/4935

ROCE 22.48% 12.67% 9.39% 9.32%

Return on Capital Employed

For the Easy Jet Airline, the computations of ROCE provides a progressive decline in

the ratio from 2015 to 2018. This is because of the fall in the operating profit with rise in the

current liabilities. One of the contributing factor of decline in ROCE is increase in the cost of

operations.

Gross Profit Margin:

According to Weygandt, Kimmel and Kieso (2015) the gross profit margin is the

profitability ratio which compares the gross margin of the business with respect to net sales.

The ratio provides how a company sells its inventory or merchandise.

Gross Profit Margin = (Gross Profit / Sales) x 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING AND FINANCE

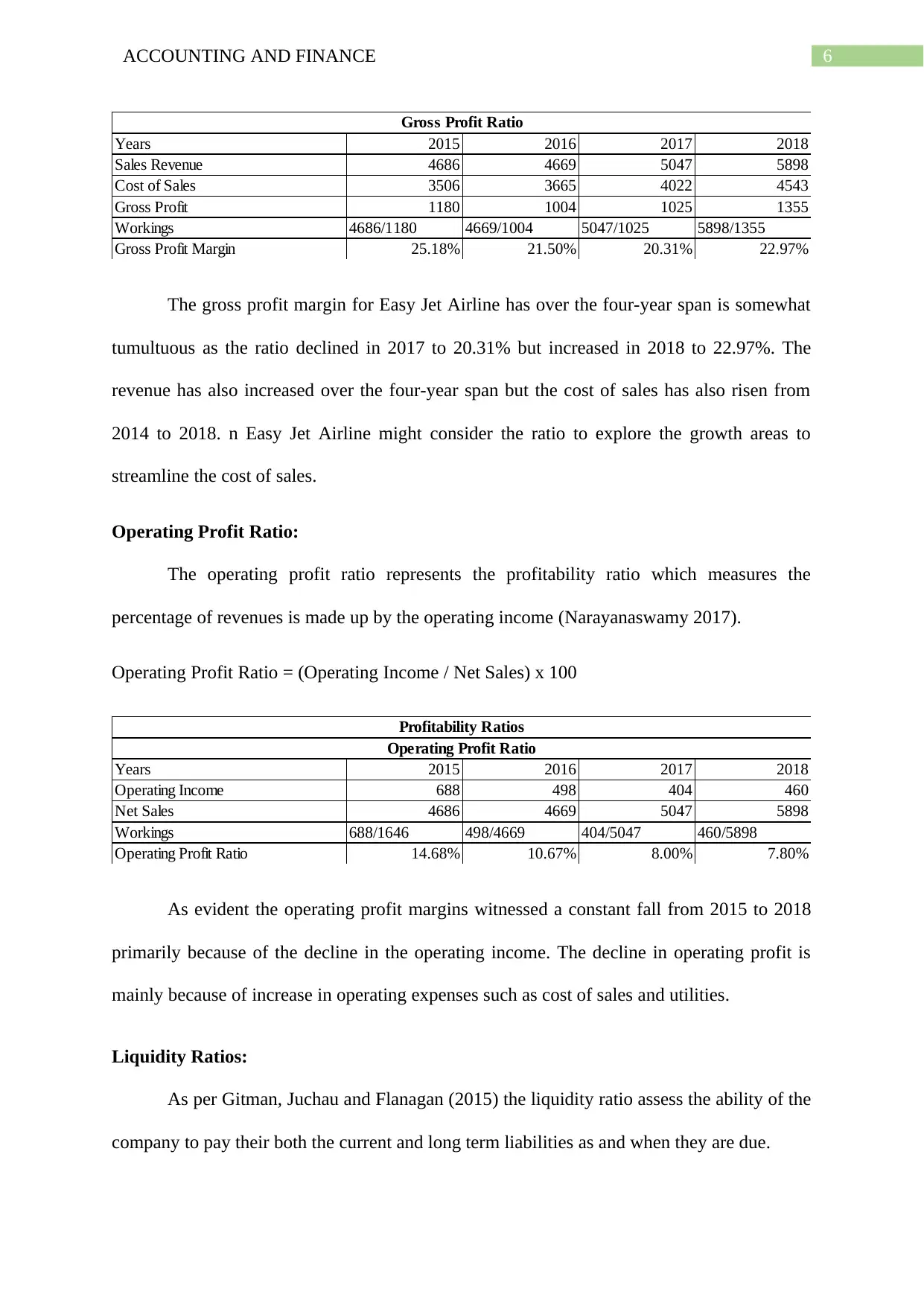

Years 2015 2016 2017 2018

Sales Revenue 4686 4669 5047 5898

Cost of Sales 3506 3665 4022 4543

Gross Profit 1180 1004 1025 1355

Workings 4686/1180 4669/1004 5047/1025 5898/1355

Gross Profit Margin 25.18% 21.50% 20.31% 22.97%

Gross Profit Ratio

The gross profit margin for Easy Jet Airline has over the four-year span is somewhat

tumultuous as the ratio declined in 2017 to 20.31% but increased in 2018 to 22.97%. The

revenue has also increased over the four-year span but the cost of sales has also risen from

2014 to 2018. n Easy Jet Airline might consider the ratio to explore the growth areas to

streamline the cost of sales.

Operating Profit Ratio:

The operating profit ratio represents the profitability ratio which measures the

percentage of revenues is made up by the operating income (Narayanaswamy 2017).

Operating Profit Ratio = (Operating Income / Net Sales) x 100

Years 2015 2016 2017 2018

Operating Income 688 498 404 460

Net Sales 4686 4669 5047 5898

Workings 688/1646 498/4669 404/5047 460/5898

Operating Profit Ratio 14.68% 10.67% 8.00% 7.80%

Profitability Ratios

Operating Profit Ratio

As evident the operating profit margins witnessed a constant fall from 2015 to 2018

primarily because of the decline in the operating income. The decline in operating profit is

mainly because of increase in operating expenses such as cost of sales and utilities.

Liquidity Ratios:

As per Gitman, Juchau and Flanagan (2015) the liquidity ratio assess the ability of the

company to pay their both the current and long term liabilities as and when they are due.

Years 2015 2016 2017 2018

Sales Revenue 4686 4669 5047 5898

Cost of Sales 3506 3665 4022 4543

Gross Profit 1180 1004 1025 1355

Workings 4686/1180 4669/1004 5047/1025 5898/1355

Gross Profit Margin 25.18% 21.50% 20.31% 22.97%

Gross Profit Ratio

The gross profit margin for Easy Jet Airline has over the four-year span is somewhat

tumultuous as the ratio declined in 2017 to 20.31% but increased in 2018 to 22.97%. The

revenue has also increased over the four-year span but the cost of sales has also risen from

2014 to 2018. n Easy Jet Airline might consider the ratio to explore the growth areas to

streamline the cost of sales.

Operating Profit Ratio:

The operating profit ratio represents the profitability ratio which measures the

percentage of revenues is made up by the operating income (Narayanaswamy 2017).

Operating Profit Ratio = (Operating Income / Net Sales) x 100

Years 2015 2016 2017 2018

Operating Income 688 498 404 460

Net Sales 4686 4669 5047 5898

Workings 688/1646 498/4669 404/5047 460/5898

Operating Profit Ratio 14.68% 10.67% 8.00% 7.80%

Profitability Ratios

Operating Profit Ratio

As evident the operating profit margins witnessed a constant fall from 2015 to 2018

primarily because of the decline in the operating income. The decline in operating profit is

mainly because of increase in operating expenses such as cost of sales and utilities.

Liquidity Ratios:

As per Gitman, Juchau and Flanagan (2015) the liquidity ratio assess the ability of the

company to pay their both the current and long term liabilities as and when they are due.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING AND FINANCE

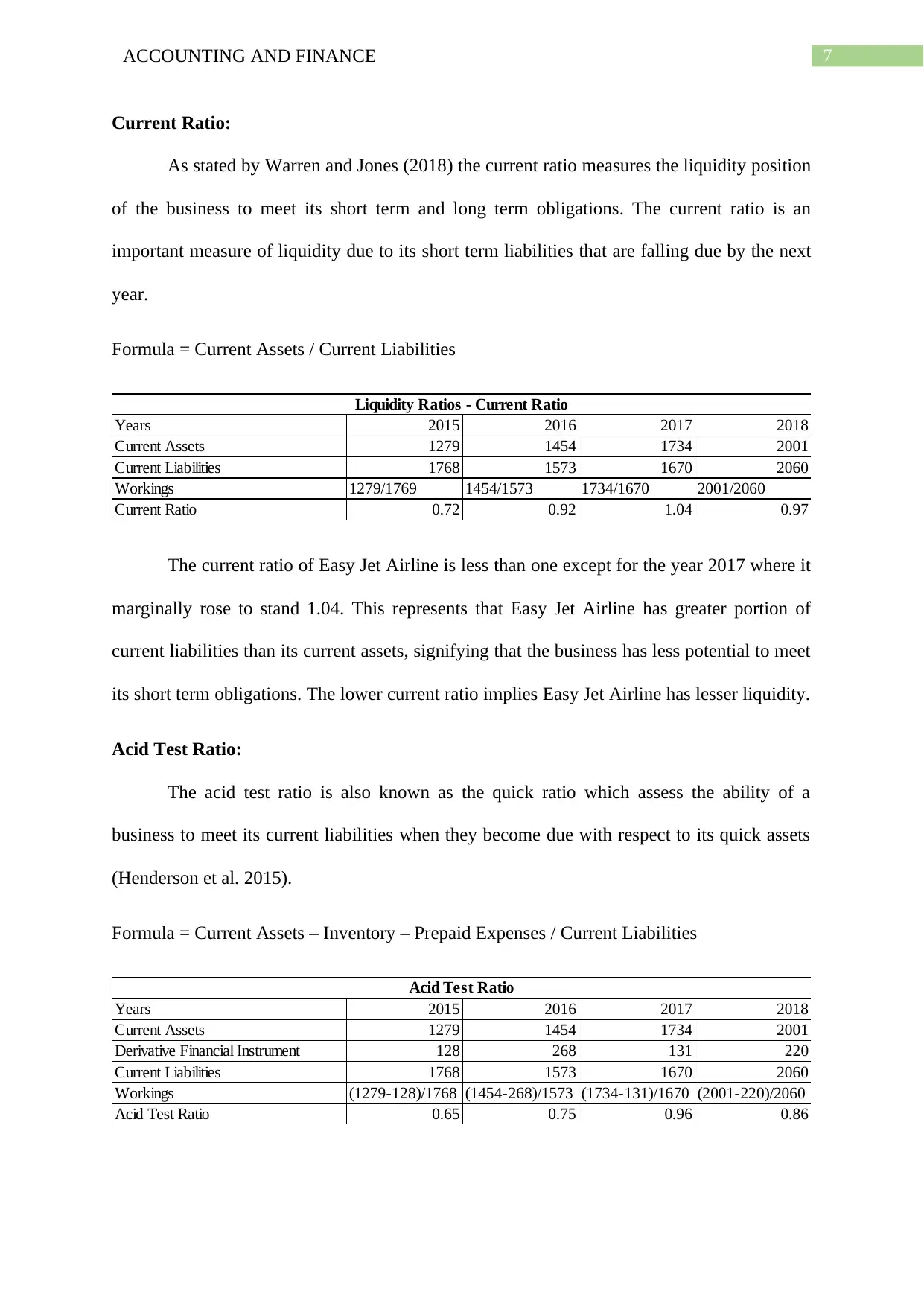

Current Ratio:

As stated by Warren and Jones (2018) the current ratio measures the liquidity position

of the business to meet its short term and long term obligations. The current ratio is an

important measure of liquidity due to its short term liabilities that are falling due by the next

year.

Formula = Current Assets / Current Liabilities

Years 2015 2016 2017 2018

Current Assets 1279 1454 1734 2001

Current Liabilities 1768 1573 1670 2060

Workings 1279/1769 1454/1573 1734/1670 2001/2060

Current Ratio 0.72 0.92 1.04 0.97

Liquidity Ratios - Current Ratio

The current ratio of Easy Jet Airline is less than one except for the year 2017 where it

marginally rose to stand 1.04. This represents that Easy Jet Airline has greater portion of

current liabilities than its current assets, signifying that the business has less potential to meet

its short term obligations. The lower current ratio implies Easy Jet Airline has lesser liquidity.

Acid Test Ratio:

The acid test ratio is also known as the quick ratio which assess the ability of a

business to meet its current liabilities when they become due with respect to its quick assets

(Henderson et al. 2015).

Formula = Current Assets – Inventory – Prepaid Expenses / Current Liabilities

Years 2015 2016 2017 2018

Current Assets 1279 1454 1734 2001

Derivative Financial Instrument 128 268 131 220

Current Liabilities 1768 1573 1670 2060

Workings (1279-128)/1768 (1454-268)/1573 (1734-131)/1670 (2001-220)/2060

Acid Test Ratio 0.65 0.75 0.96 0.86

Acid Test Ratio

Current Ratio:

As stated by Warren and Jones (2018) the current ratio measures the liquidity position

of the business to meet its short term and long term obligations. The current ratio is an

important measure of liquidity due to its short term liabilities that are falling due by the next

year.

Formula = Current Assets / Current Liabilities

Years 2015 2016 2017 2018

Current Assets 1279 1454 1734 2001

Current Liabilities 1768 1573 1670 2060

Workings 1279/1769 1454/1573 1734/1670 2001/2060

Current Ratio 0.72 0.92 1.04 0.97

Liquidity Ratios - Current Ratio

The current ratio of Easy Jet Airline is less than one except for the year 2017 where it

marginally rose to stand 1.04. This represents that Easy Jet Airline has greater portion of

current liabilities than its current assets, signifying that the business has less potential to meet

its short term obligations. The lower current ratio implies Easy Jet Airline has lesser liquidity.

Acid Test Ratio:

The acid test ratio is also known as the quick ratio which assess the ability of a

business to meet its current liabilities when they become due with respect to its quick assets

(Henderson et al. 2015).

Formula = Current Assets – Inventory – Prepaid Expenses / Current Liabilities

Years 2015 2016 2017 2018

Current Assets 1279 1454 1734 2001

Derivative Financial Instrument 128 268 131 220

Current Liabilities 1768 1573 1670 2060

Workings (1279-128)/1768 (1454-268)/1573 (1734-131)/1670 (2001-220)/2060

Acid Test Ratio 0.65 0.75 0.96 0.86

Acid Test Ratio

8ACCOUNTING AND FINANCE

As evident from the computation the quick ratio for Easy Jet Airline for the four-year

span stood relatively low. similar to the current ratio the quick ratio for the company stood

less than one from 2011 to 2014. This signifies that the current assets do not covers the

current liabilities and this may a cause of concern for Easy Jet Airline as the current liabilities

stands greater than the current assets. Easy Jet Airline may suffer from the inability of paying

off their current liabilities with the current level of quick assets the business has presently.

Gearing/Capital Structure Ratios:

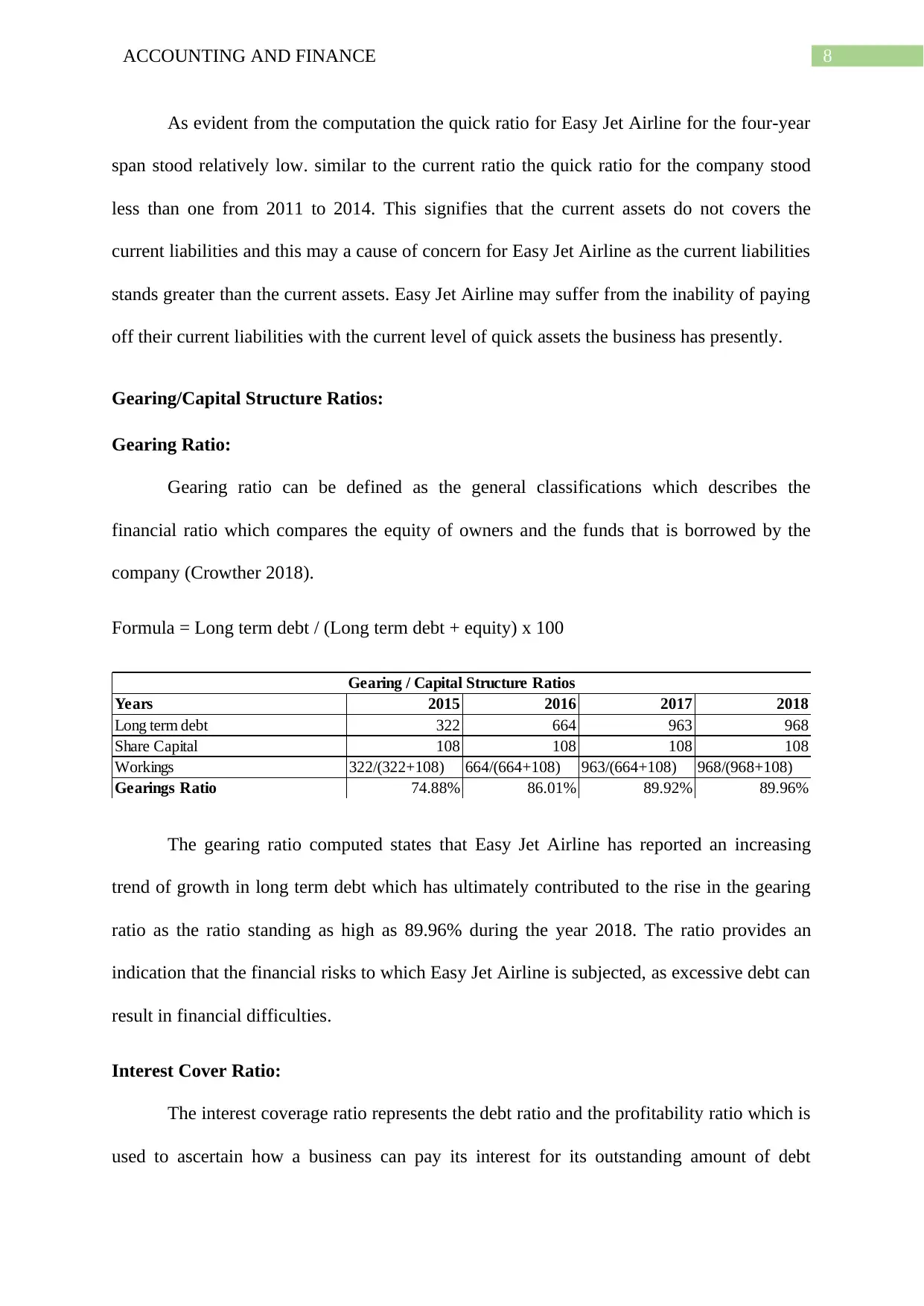

Gearing Ratio:

Gearing ratio can be defined as the general classifications which describes the

financial ratio which compares the equity of owners and the funds that is borrowed by the

company (Crowther 2018).

Formula = Long term debt / (Long term debt + equity) x 100

Years 2015 2016 2017 2018

Long term debt 322 664 963 968

Share Capital 108 108 108 108

Workings 322/(322+108) 664/(664+108) 963/(664+108) 968/(968+108)

Gearings Ratio 74.88% 86.01% 89.92% 89.96%

Gearing / Capital Structure Ratios

The gearing ratio computed states that Easy Jet Airline has reported an increasing

trend of growth in long term debt which has ultimately contributed to the rise in the gearing

ratio as the ratio standing as high as 89.96% during the year 2018. The ratio provides an

indication that the financial risks to which Easy Jet Airline is subjected, as excessive debt can

result in financial difficulties.

Interest Cover Ratio:

The interest coverage ratio represents the debt ratio and the profitability ratio which is

used to ascertain how a business can pay its interest for its outstanding amount of debt

As evident from the computation the quick ratio for Easy Jet Airline for the four-year

span stood relatively low. similar to the current ratio the quick ratio for the company stood

less than one from 2011 to 2014. This signifies that the current assets do not covers the

current liabilities and this may a cause of concern for Easy Jet Airline as the current liabilities

stands greater than the current assets. Easy Jet Airline may suffer from the inability of paying

off their current liabilities with the current level of quick assets the business has presently.

Gearing/Capital Structure Ratios:

Gearing Ratio:

Gearing ratio can be defined as the general classifications which describes the

financial ratio which compares the equity of owners and the funds that is borrowed by the

company (Crowther 2018).

Formula = Long term debt / (Long term debt + equity) x 100

Years 2015 2016 2017 2018

Long term debt 322 664 963 968

Share Capital 108 108 108 108

Workings 322/(322+108) 664/(664+108) 963/(664+108) 968/(968+108)

Gearings Ratio 74.88% 86.01% 89.92% 89.96%

Gearing / Capital Structure Ratios

The gearing ratio computed states that Easy Jet Airline has reported an increasing

trend of growth in long term debt which has ultimately contributed to the rise in the gearing

ratio as the ratio standing as high as 89.96% during the year 2018. The ratio provides an

indication that the financial risks to which Easy Jet Airline is subjected, as excessive debt can

result in financial difficulties.

Interest Cover Ratio:

The interest coverage ratio represents the debt ratio and the profitability ratio which is

used to ascertain how a business can pay its interest for its outstanding amount of debt

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING AND FINANCE

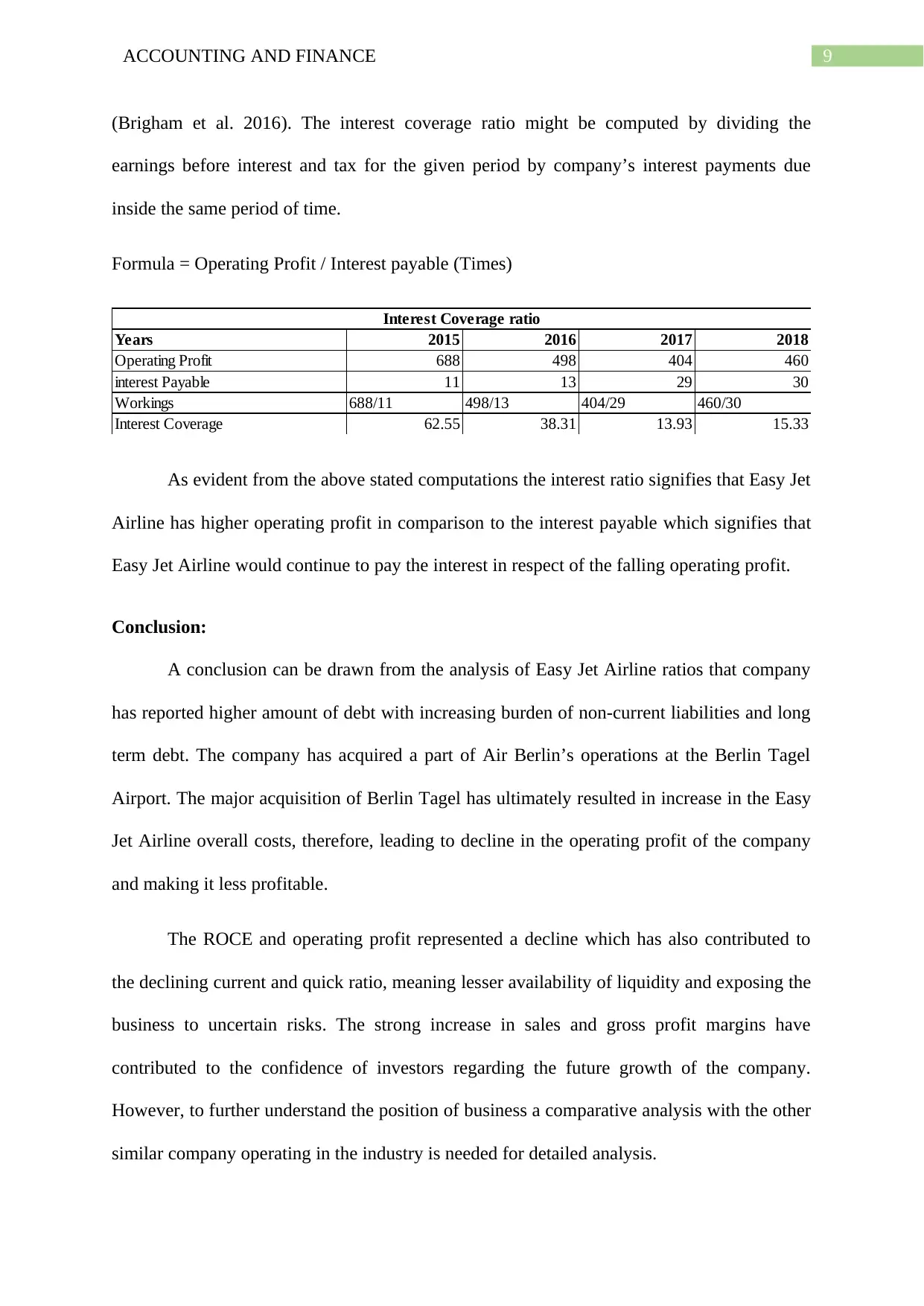

(Brigham et al. 2016). The interest coverage ratio might be computed by dividing the

earnings before interest and tax for the given period by company’s interest payments due

inside the same period of time.

Formula = Operating Profit / Interest payable (Times)

Years 2015 2016 2017 2018

Operating Profit 688 498 404 460

interest Payable 11 13 29 30

Workings 688/11 498/13 404/29 460/30

Interest Coverage 62.55 38.31 13.93 15.33

Interest Coverage ratio

As evident from the above stated computations the interest ratio signifies that Easy Jet

Airline has higher operating profit in comparison to the interest payable which signifies that

Easy Jet Airline would continue to pay the interest in respect of the falling operating profit.

Conclusion:

A conclusion can be drawn from the analysis of Easy Jet Airline ratios that company

has reported higher amount of debt with increasing burden of non-current liabilities and long

term debt. The company has acquired a part of Air Berlin’s operations at the Berlin Tagel

Airport. The major acquisition of Berlin Tagel has ultimately resulted in increase in the Easy

Jet Airline overall costs, therefore, leading to decline in the operating profit of the company

and making it less profitable.

The ROCE and operating profit represented a decline which has also contributed to

the declining current and quick ratio, meaning lesser availability of liquidity and exposing the

business to uncertain risks. The strong increase in sales and gross profit margins have

contributed to the confidence of investors regarding the future growth of the company.

However, to further understand the position of business a comparative analysis with the other

similar company operating in the industry is needed for detailed analysis.

(Brigham et al. 2016). The interest coverage ratio might be computed by dividing the

earnings before interest and tax for the given period by company’s interest payments due

inside the same period of time.

Formula = Operating Profit / Interest payable (Times)

Years 2015 2016 2017 2018

Operating Profit 688 498 404 460

interest Payable 11 13 29 30

Workings 688/11 498/13 404/29 460/30

Interest Coverage 62.55 38.31 13.93 15.33

Interest Coverage ratio

As evident from the above stated computations the interest ratio signifies that Easy Jet

Airline has higher operating profit in comparison to the interest payable which signifies that

Easy Jet Airline would continue to pay the interest in respect of the falling operating profit.

Conclusion:

A conclusion can be drawn from the analysis of Easy Jet Airline ratios that company

has reported higher amount of debt with increasing burden of non-current liabilities and long

term debt. The company has acquired a part of Air Berlin’s operations at the Berlin Tagel

Airport. The major acquisition of Berlin Tagel has ultimately resulted in increase in the Easy

Jet Airline overall costs, therefore, leading to decline in the operating profit of the company

and making it less profitable.

The ROCE and operating profit represented a decline which has also contributed to

the declining current and quick ratio, meaning lesser availability of liquidity and exposing the

business to uncertain risks. The strong increase in sales and gross profit margins have

contributed to the confidence of investors regarding the future growth of the company.

However, to further understand the position of business a comparative analysis with the other

similar company operating in the industry is needed for detailed analysis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING AND FINANCE

11ACCOUNTING AND FINANCE

References:

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment:

Theory And Practice, Canadian Edition. Nelson Education.

Corporate.easyjet.com. (2019). 2017. [online] Available at:

http://corporate.easyjet.com/investors/reports-and-presentations/2017 [Accessed 2 Jan. 2019].

Crowther, D., 2018. A Social Critique of Corporate Reporting: A Semiotic Analysis of

Corporate Financial and Environmental Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting. Routledge.

Deegan, C., 2014. Financial accounting theory. McGraw-Hill Education Australia.

Dutta, S. and Patatoukas, P.N., 2016. Identifying conditional conservatism in financial

accounting data: theory and evidence. The Accounting Review, 92(4), pp.191-216.

Easton, M. and Sommers, Z., 2018. Financial Statement Analysis & Valuation, 5e.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Khan, M., 2015. Accounting: Financial. In Encyclopedia of Public Administration and Public

Policy, Third Edition-5 Volume Set (pp. 1-6). Routledge.

Narayanaswamy, R., 2017. Financial Accounting: A Managerial Perspective. PHI Learning

Pvt. Ltd..

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

References:

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment:

Theory And Practice, Canadian Edition. Nelson Education.

Corporate.easyjet.com. (2019). 2017. [online] Available at:

http://corporate.easyjet.com/investors/reports-and-presentations/2017 [Accessed 2 Jan. 2019].

Crowther, D., 2018. A Social Critique of Corporate Reporting: A Semiotic Analysis of

Corporate Financial and Environmental Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting. Routledge.

Deegan, C., 2014. Financial accounting theory. McGraw-Hill Education Australia.

Dutta, S. and Patatoukas, P.N., 2016. Identifying conditional conservatism in financial

accounting data: theory and evidence. The Accounting Review, 92(4), pp.191-216.

Easton, M. and Sommers, Z., 2018. Financial Statement Analysis & Valuation, 5e.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Khan, M., 2015. Accounting: Financial. In Encyclopedia of Public Administration and Public

Policy, Third Edition-5 Volume Set (pp. 1-6). Routledge.

Narayanaswamy, R., 2017. Financial Accounting: A Managerial Perspective. PHI Learning

Pvt. Ltd..

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.