Financial Performance Analysis of Pharmaceutical Companies: A Report

VerifiedAdded on 2021/02/18

|31

|5889

|18

Report

AI Summary

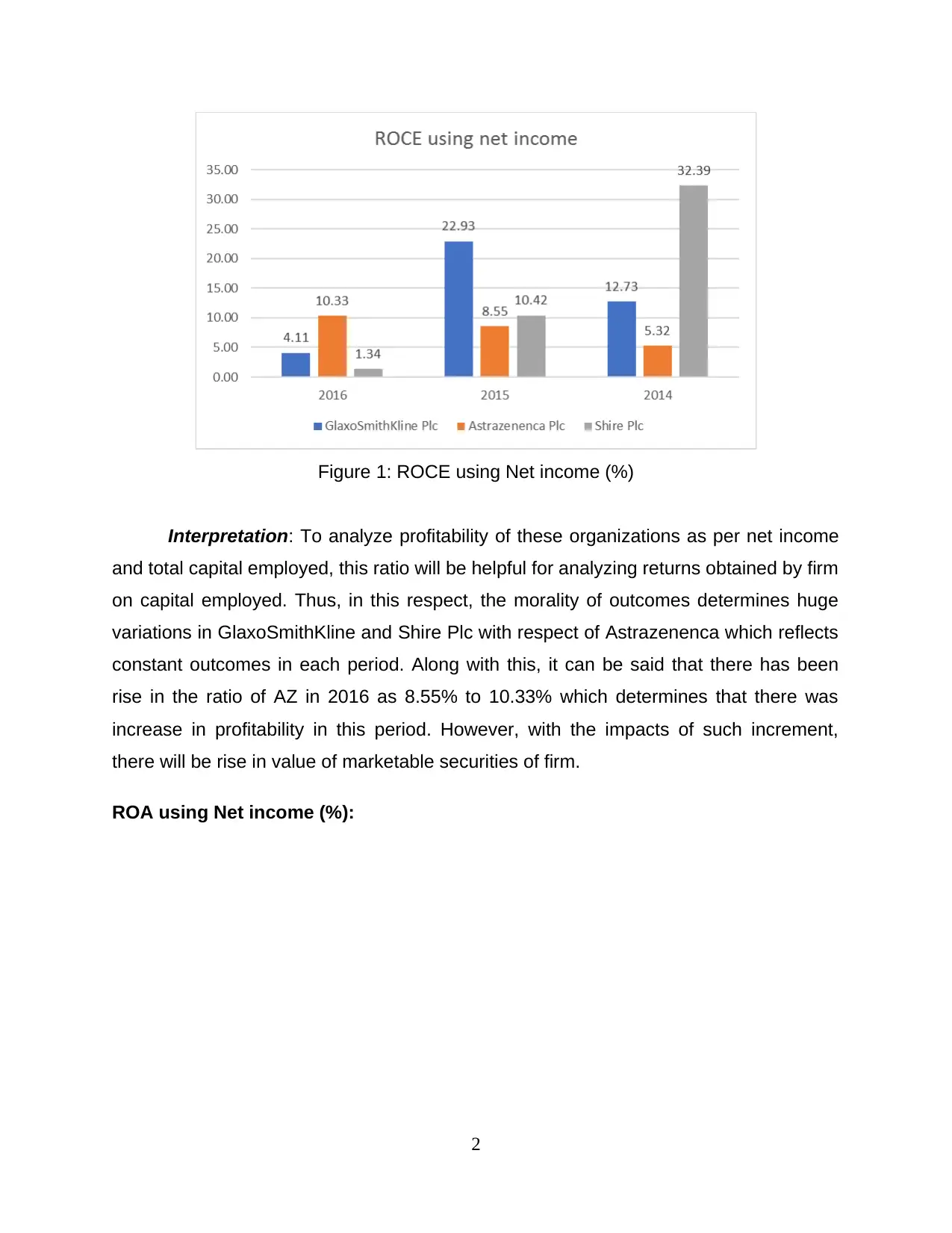

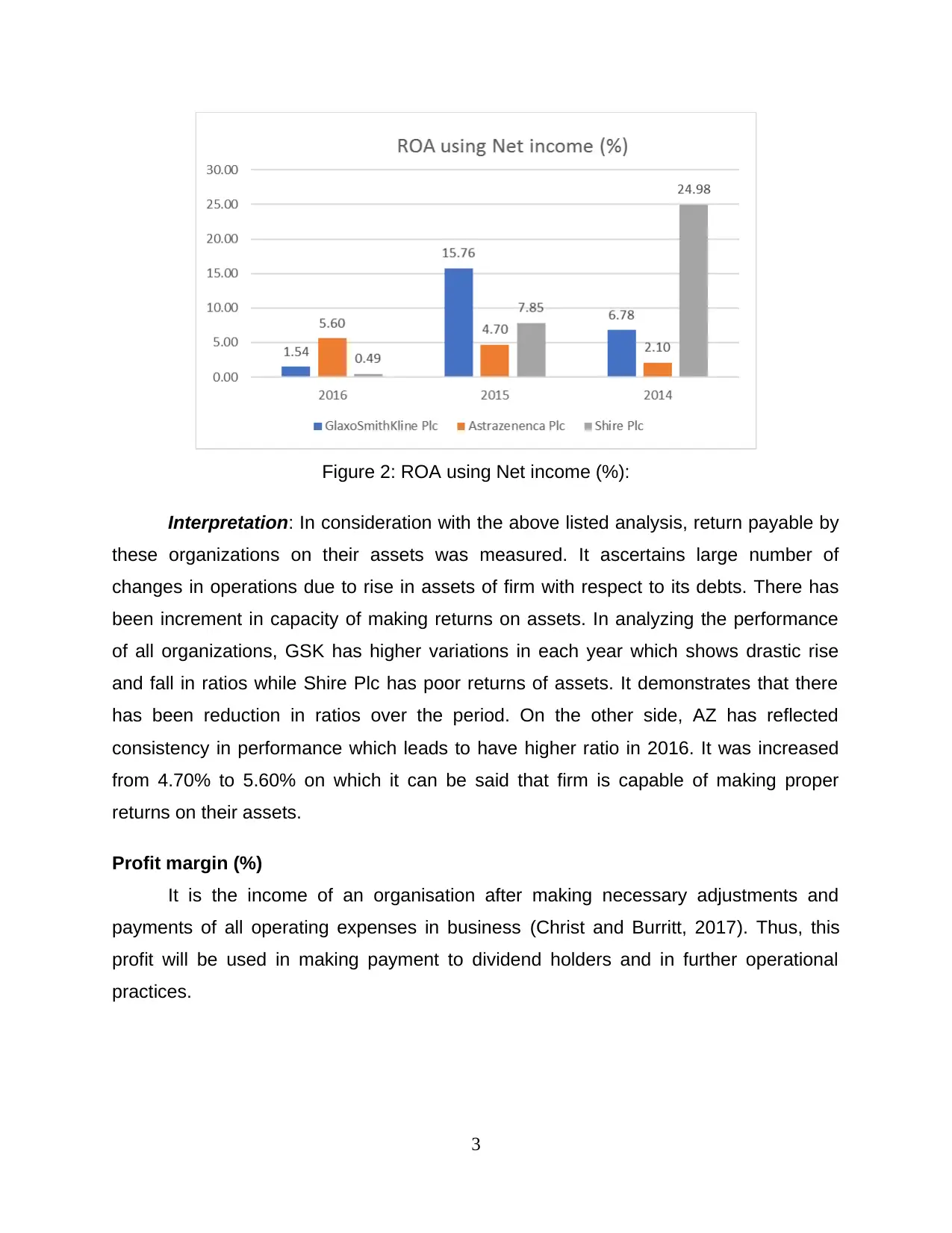

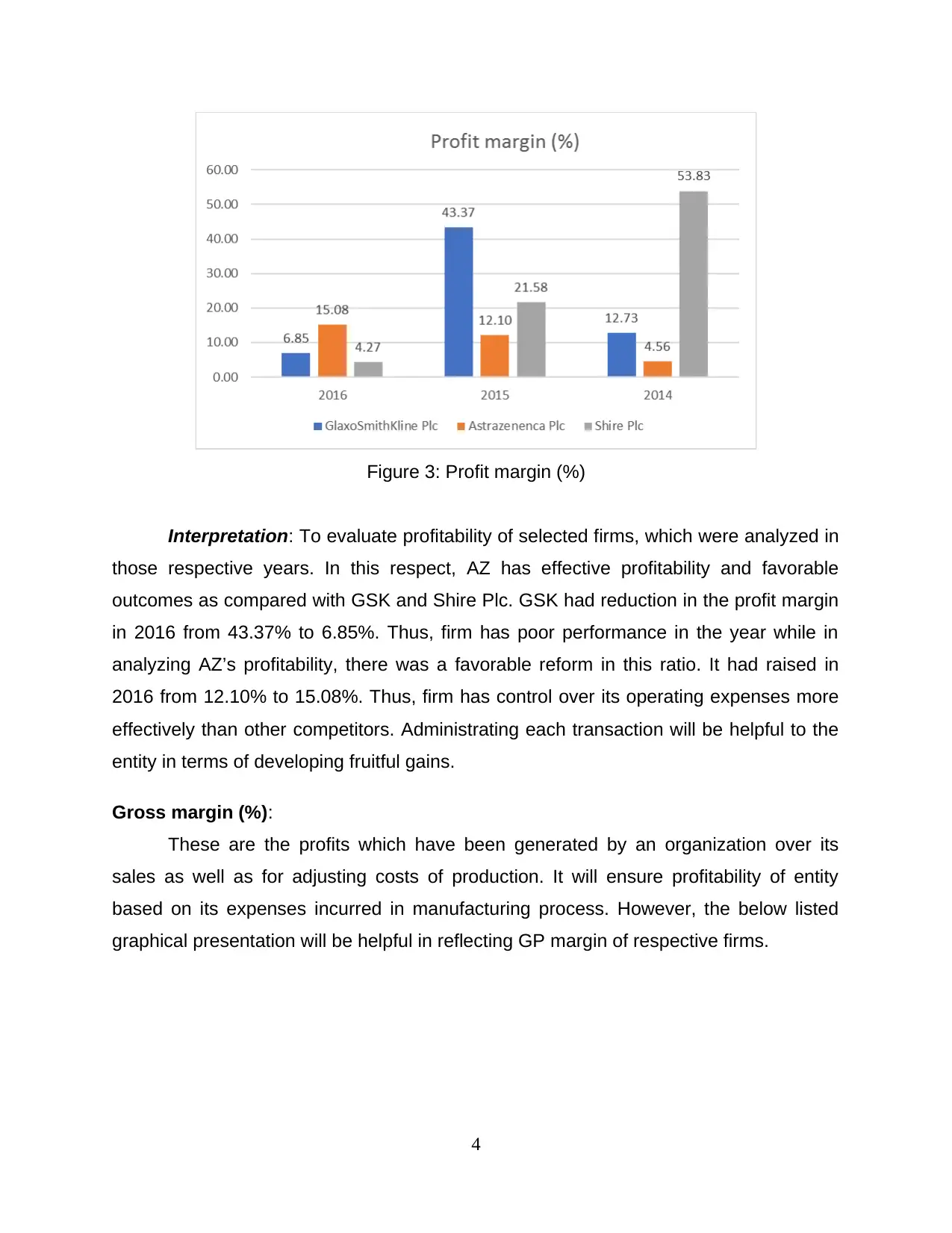

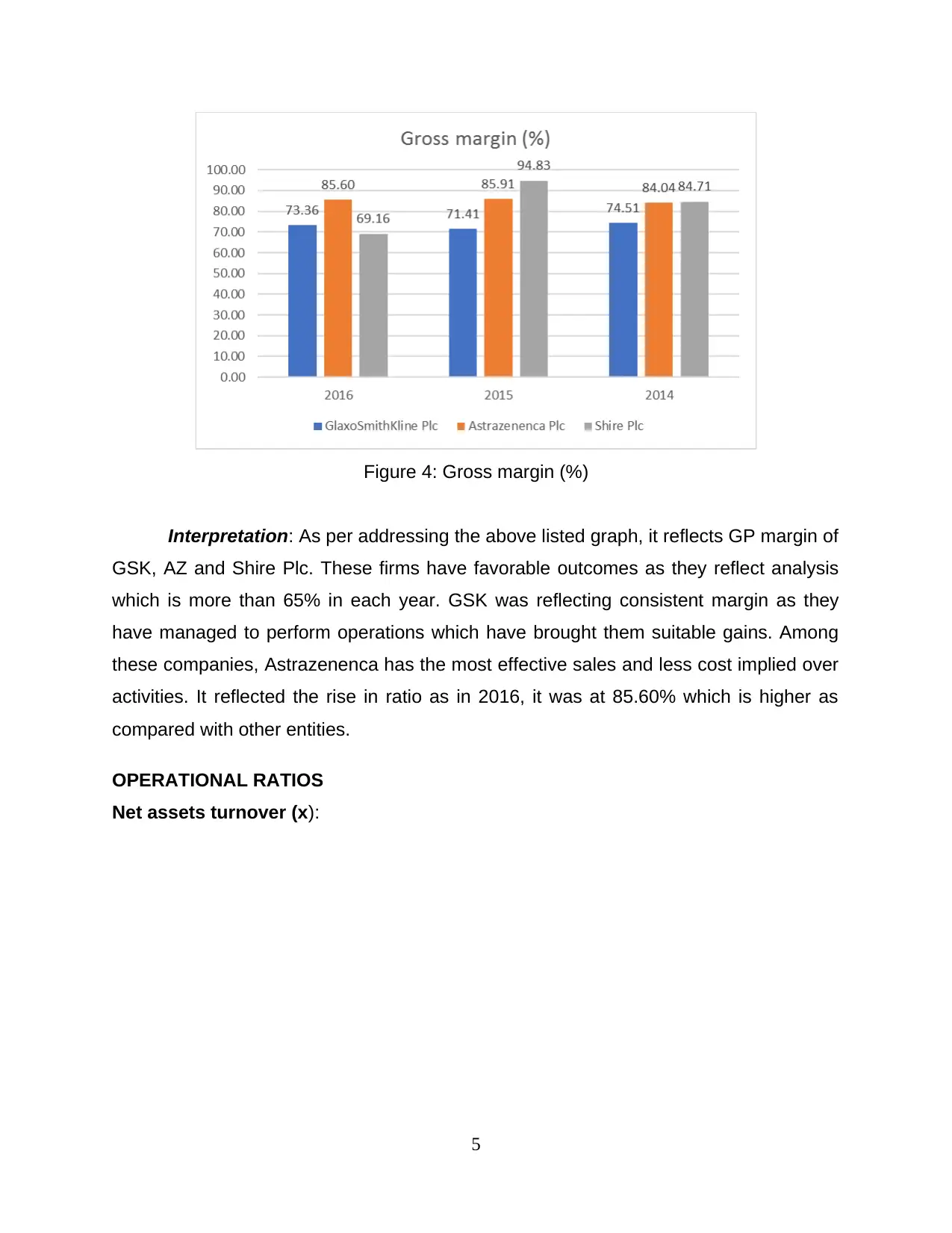

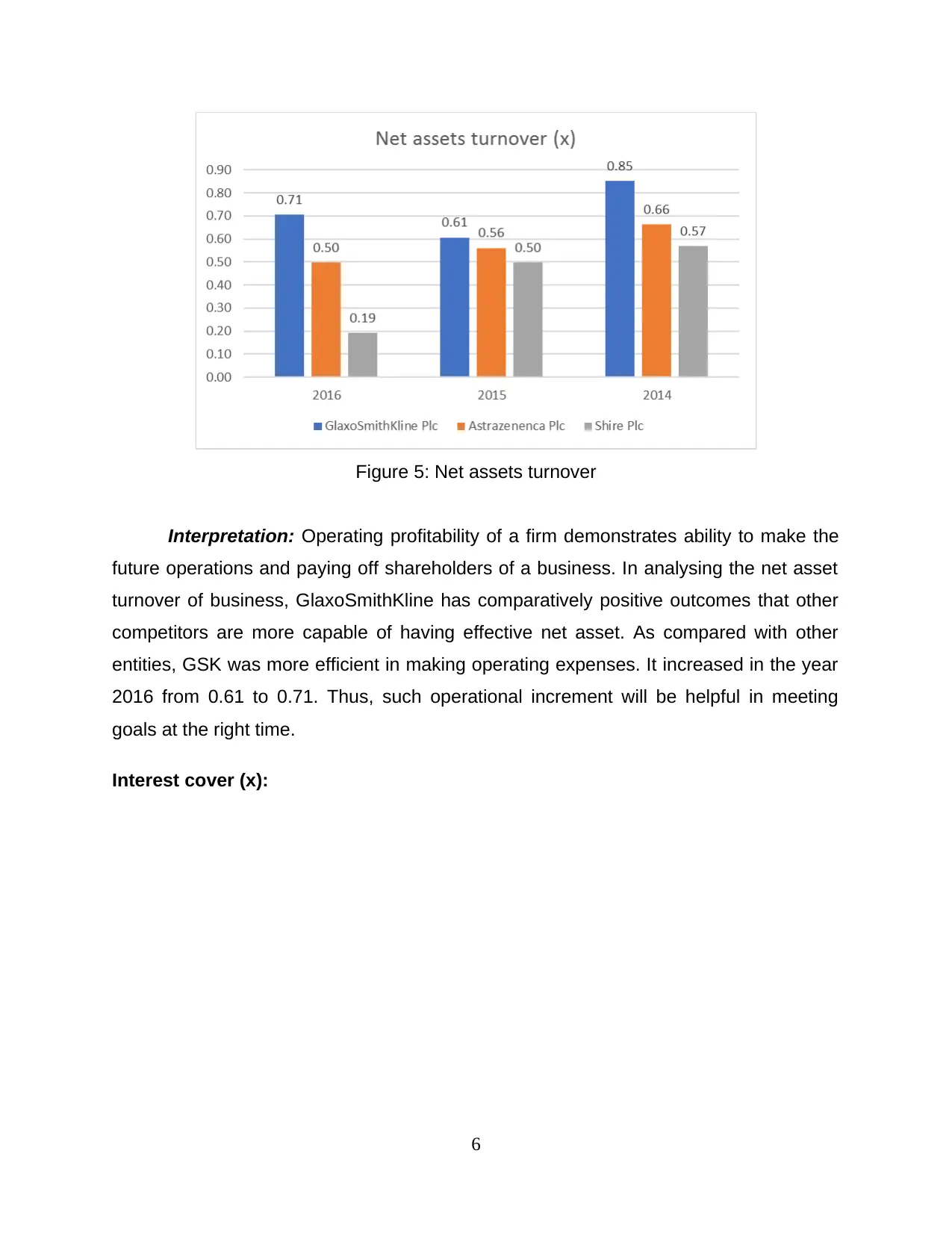

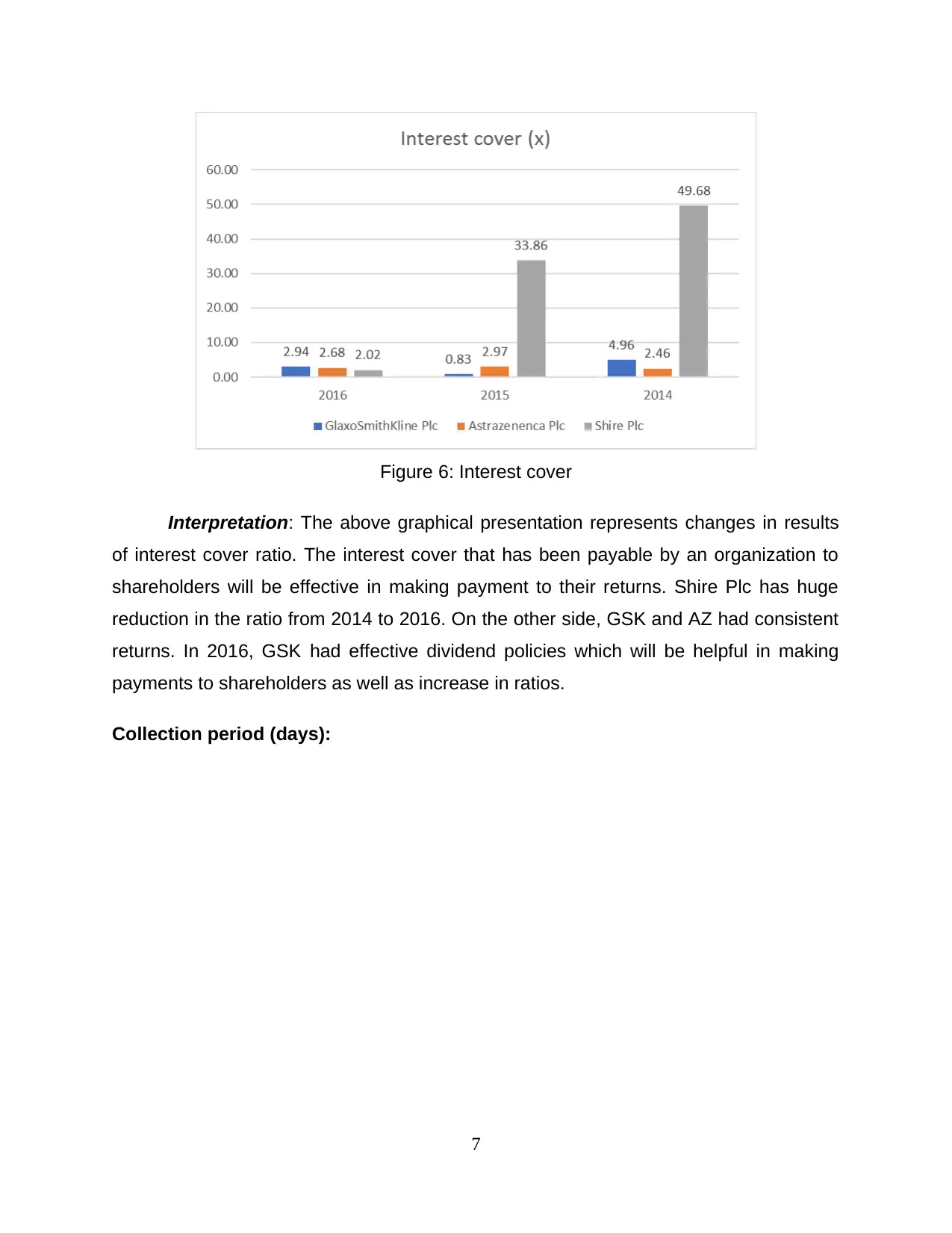

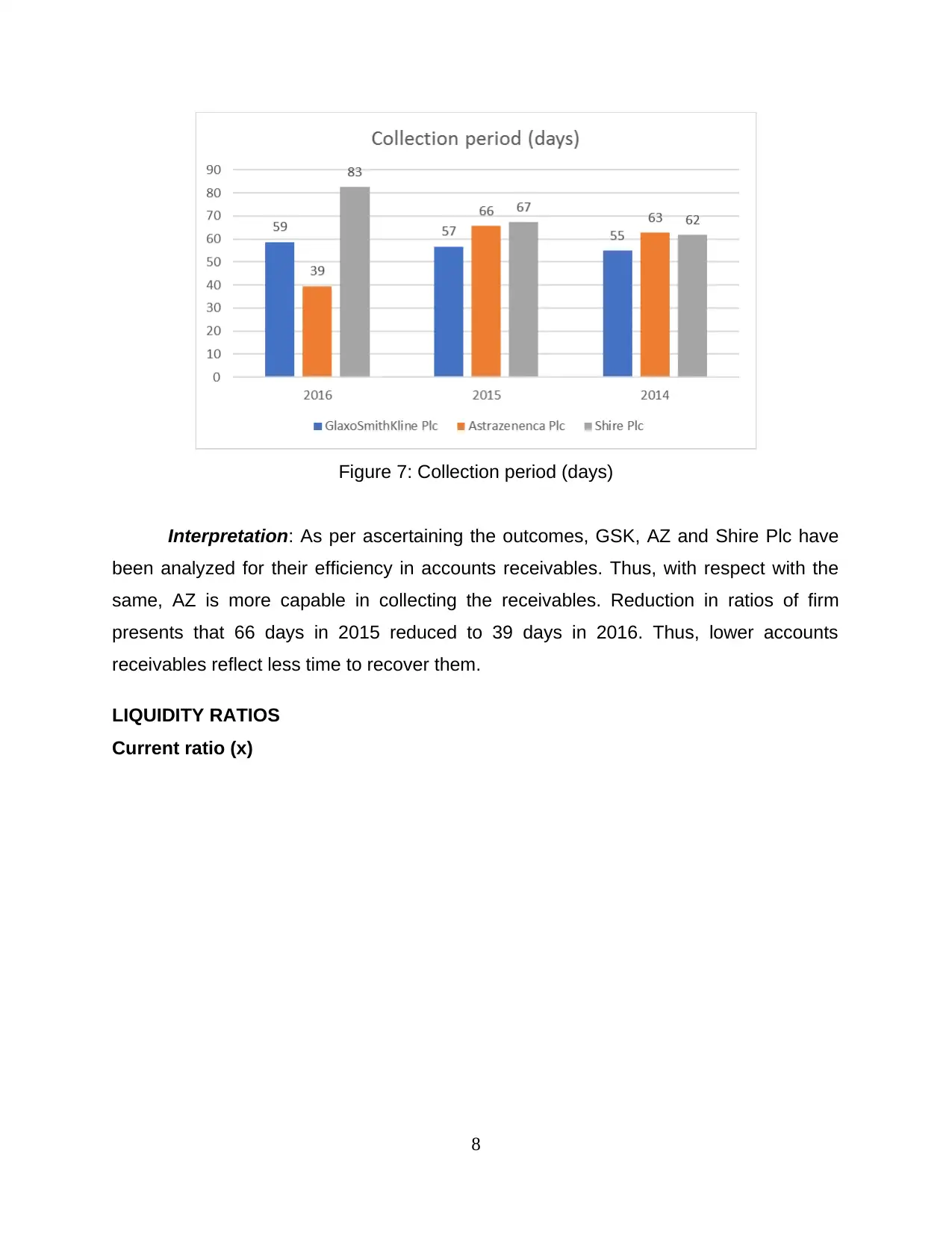

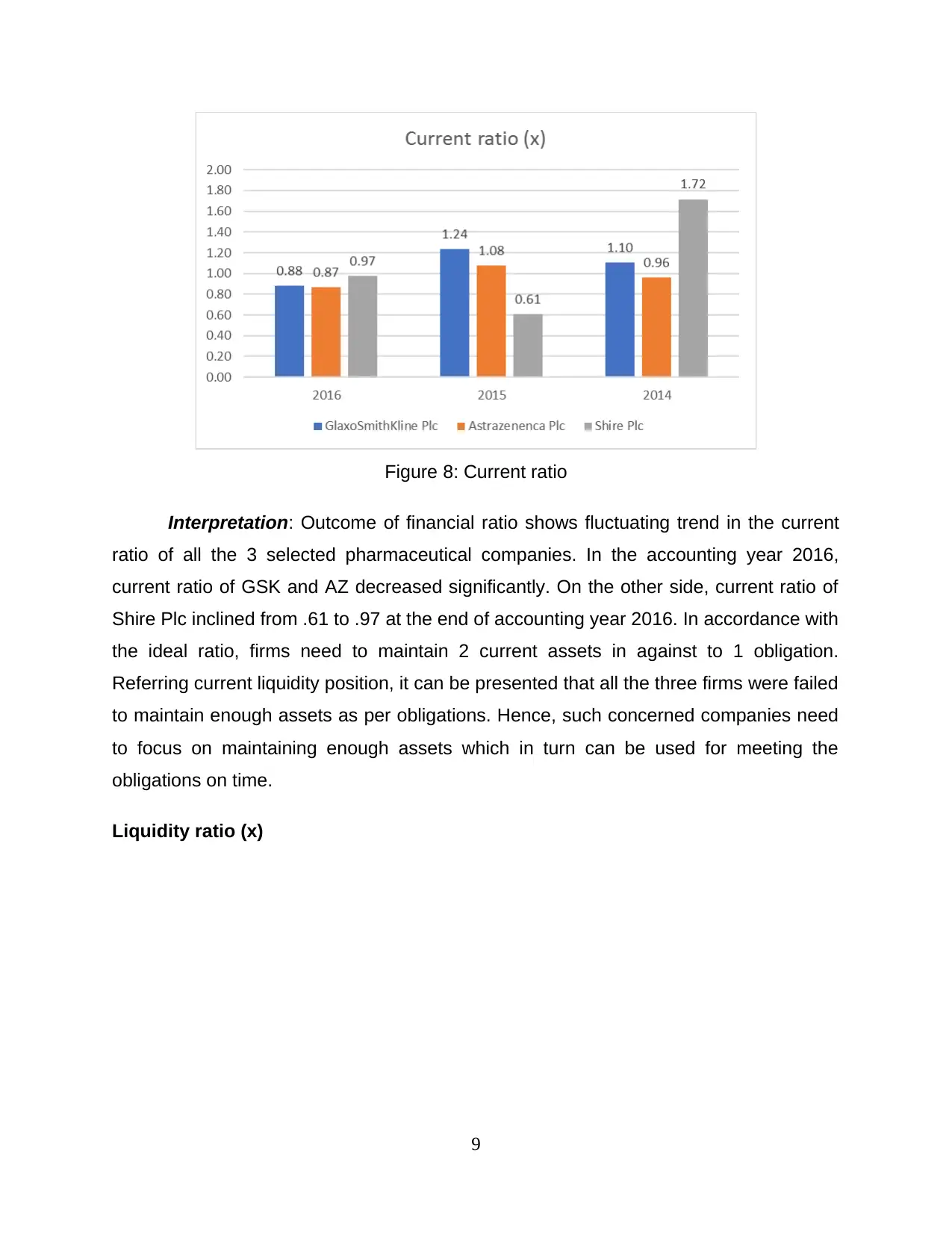

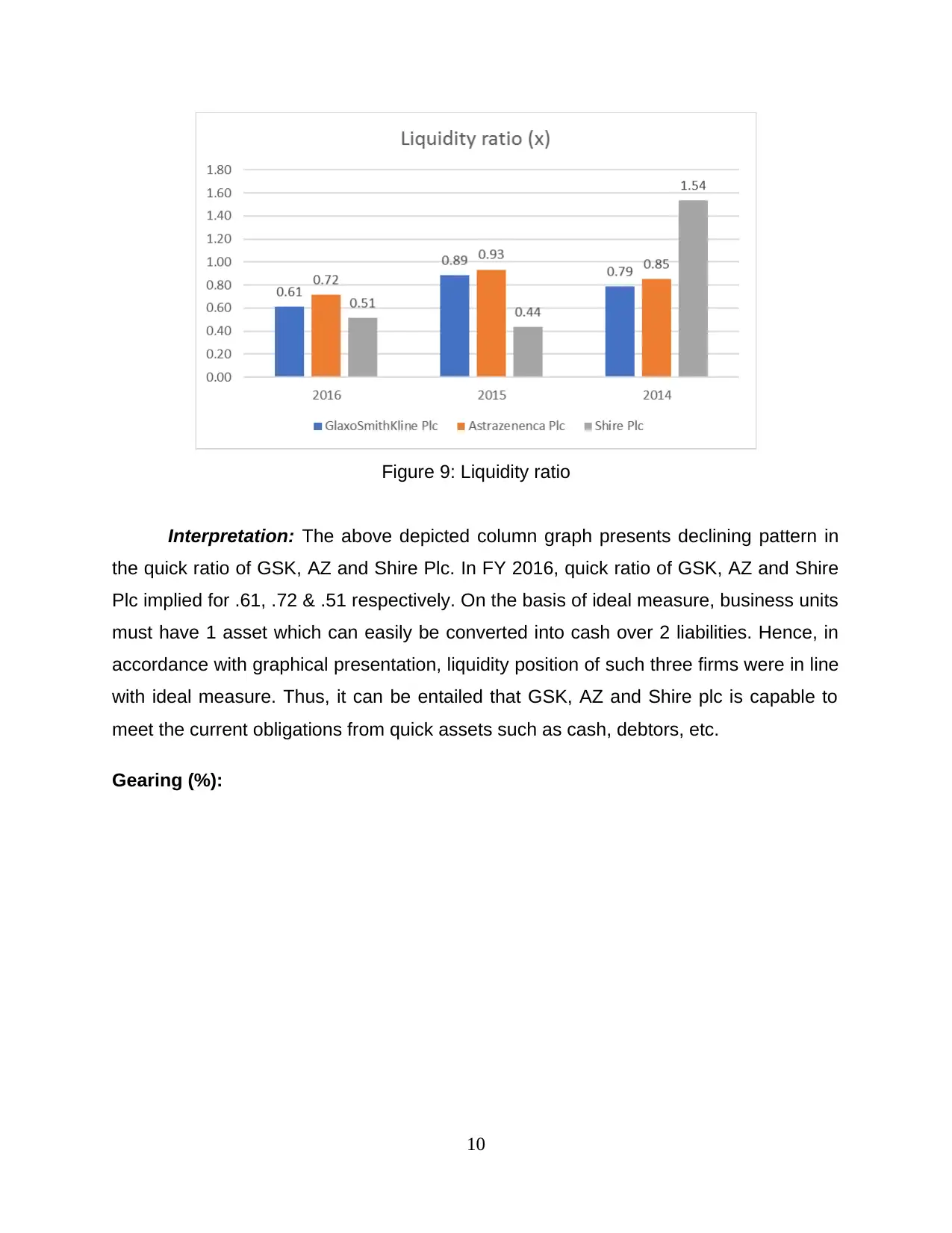

This report provides a detailed financial analysis of three pharmaceutical companies: GlaxoSmithKline, AstraZeneca Plc, and Shire Plc. It begins with an introduction to financial ratio analysis and its significance in assessing industry efficiency and capabilities. Section A focuses on the justification and selection of financial and non-financial ratios, including profitability, operational, and liquidity ratios, to evaluate the companies' performance. The report identifies the best-performing organization for investment and the worst-performing company, offering recommendations for financial improvement. Section B delves into the capital investment decision-making process, exploring investment appraisal methods. The analysis covers key financial ratios, including ROCE, ROA, profit margin, gross margin, net assets turnover, interest cover, collection period, current ratio, liquidity ratio, and gearing ratio. Non-financial ratios, such as profit per employee and costs of employees/operating revenue, are also assessed. The report concludes with a summary of findings and recommendations, offering valuable insights for investors and industry professionals.

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.