Accounting Assignment 8 - Cost Accounting System, Manufacturing Costs, Budgets, and Variance Analysis

VerifiedAdded on 2023/06/04

|26

|2345

|357

AI Summary

This assignment covers various topics related to cost accounting system, manufacturing and product costs, budgets, variance analysis, and more. It includes answers to various questions related to accounting and also provides a production budget, direct materials budget, and direct labor budget.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING ASSIGNMENT 8

Accounting Assignment 8

Name of the Student:

Name of the University:

Authors Note:

Accounting Assignment 8

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ACCOUNTING ASSIGNMENT 8

Contents

Task 1:.............................................................................................................................................2

Task 2:.............................................................................................................................................4

References:....................................................................................................................................25

Contents

Task 1:.............................................................................................................................................2

Task 2:.............................................................................................................................................4

References:....................................................................................................................................25

2ACCOUNTING ASSIGNMENT 8

Task 1:

Answers:

1. The data in a cost accounting system must be stored properly from the source document

such as suppliers invoice bills and other supporting documents by a professional

adequately qualified for the job. Access to the cost accounting system should be

restricted. Only the accountant should be allowed access to the system.

2. Information about manufacturing and product costs are necessary to ascertain the cost of

production properly and take informed decision about the business.

3. The manufacturing entities in Australia are under compulsion to follow the standard in

maintaining and managing accounting information.

4. The financial systems generally have inbuilt system to check and compare the invoices

and purchase orders. In case of discrepancies, the financial system outlines those

discrepancies.

5. In case based system GSTs are reconciled to determine the net GST liability (payable) or

net GST asset (receivable) as the case may be. In case of accrual basis of accounting

adjustments are made to determine GST payable and GST receivable both to make

payment accordingly.

6. Variance analysis helps the management to identify the possible area of lack of efficiency

in the production or manufacturing process. Necessary changes shall be made in these

areas by the management to improve the efficiency of the overall production process.

7. The reliability of variance analysis techniques would be improved significantly if the

integrity in the costing system is intact. The data recorded in costing system if correctly

processed without any manipulation then the resultant information will reflect the actual

Task 1:

Answers:

1. The data in a cost accounting system must be stored properly from the source document

such as suppliers invoice bills and other supporting documents by a professional

adequately qualified for the job. Access to the cost accounting system should be

restricted. Only the accountant should be allowed access to the system.

2. Information about manufacturing and product costs are necessary to ascertain the cost of

production properly and take informed decision about the business.

3. The manufacturing entities in Australia are under compulsion to follow the standard in

maintaining and managing accounting information.

4. The financial systems generally have inbuilt system to check and compare the invoices

and purchase orders. In case of discrepancies, the financial system outlines those

discrepancies.

5. In case based system GSTs are reconciled to determine the net GST liability (payable) or

net GST asset (receivable) as the case may be. In case of accrual basis of accounting

adjustments are made to determine GST payable and GST receivable both to make

payment accordingly.

6. Variance analysis helps the management to identify the possible area of lack of efficiency

in the production or manufacturing process. Necessary changes shall be made in these

areas by the management to improve the efficiency of the overall production process.

7. The reliability of variance analysis techniques would be improved significantly if the

integrity in the costing system is intact. The data recorded in costing system if correctly

processed without any manipulation then the resultant information will reflect the actual

3ACCOUNTING ASSIGNMENT 8

costing of a manufacturing and production organization. Thus the variance analysis will

also be improved as the data will be authentic and correct (Dekker, 2016).

8. Budgets are prepared to achieve organization objectives. Comparison of actual financial

performance of an organization with its budgeted performance further helps the

management to evaluate the efficiency of an organization in achieving its objectives.

9. Three objectives of budgets are as following:

a. Evaluation of performance.

b. Optimum utilization of resources.

c. Minimizing cost of productions.

10. Three sources to gather information are as following:

a. Historic financial statements.

b. Board of directors’ report.

c. Proposed agreement documents.

11. The principle of double entry system of accounting is that there would be equal liabilities

and assets after each financial transaction as there is always compensating effects on

wealth and liabilities for the double entry system of accounting of each and every

financial transaction.

Accrual based accounting is on the basis of earning and incurred concept rather

than receipts and payments. Thus, revenue is recognized when earned even if not

received and expenditures are recognized when incurred even if not paid (Otley,

2016).

12. The following is on the basis of actual components:

a. Raw materials.

costing of a manufacturing and production organization. Thus the variance analysis will

also be improved as the data will be authentic and correct (Dekker, 2016).

8. Budgets are prepared to achieve organization objectives. Comparison of actual financial

performance of an organization with its budgeted performance further helps the

management to evaluate the efficiency of an organization in achieving its objectives.

9. Three objectives of budgets are as following:

a. Evaluation of performance.

b. Optimum utilization of resources.

c. Minimizing cost of productions.

10. Three sources to gather information are as following:

a. Historic financial statements.

b. Board of directors’ report.

c. Proposed agreement documents.

11. The principle of double entry system of accounting is that there would be equal liabilities

and assets after each financial transaction as there is always compensating effects on

wealth and liabilities for the double entry system of accounting of each and every

financial transaction.

Accrual based accounting is on the basis of earning and incurred concept rather

than receipts and payments. Thus, revenue is recognized when earned even if not

received and expenditures are recognized when incurred even if not paid (Otley,

2016).

12. The following is on the basis of actual components:

a. Raw materials.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ACCOUNTING ASSIGNMENT 8

b. Direct labor.

c. Factory overhead both fixed and variable.

However, there are the following which can also be referred to as components of finished

products:

I. Upstream of raw materials.

II. Raw materials.

III. Secondary products.

IV. Intermediate products (Fullerton, Kennedy & Widener, 2014).

Task 2:

Question 1:

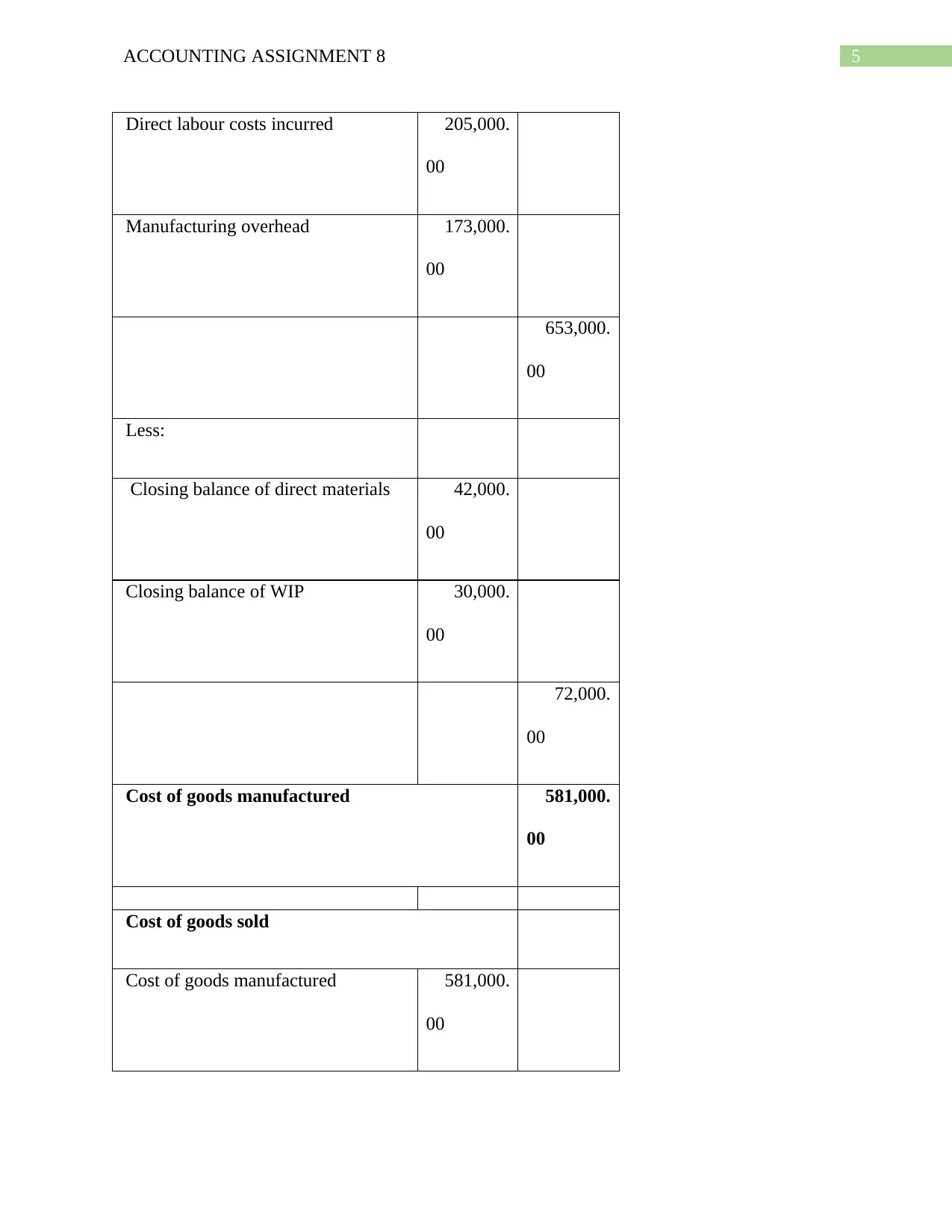

Particulars Amount

($)

Amount

($)

Cost of goods manufactured

Opening balance of direct materials 49,000.

00

Opening WIP 28,000.

00

Purchases during the year 198,000.

00

b. Direct labor.

c. Factory overhead both fixed and variable.

However, there are the following which can also be referred to as components of finished

products:

I. Upstream of raw materials.

II. Raw materials.

III. Secondary products.

IV. Intermediate products (Fullerton, Kennedy & Widener, 2014).

Task 2:

Question 1:

Particulars Amount

($)

Amount

($)

Cost of goods manufactured

Opening balance of direct materials 49,000.

00

Opening WIP 28,000.

00

Purchases during the year 198,000.

00

5ACCOUNTING ASSIGNMENT 8

Direct labour costs incurred 205,000.

00

Manufacturing overhead 173,000.

00

653,000.

00

Less:

Closing balance of direct materials 42,000.

00

Closing balance of WIP 30,000.

00

72,000.

00

Cost of goods manufactured 581,000.

00

Cost of goods sold

Cost of goods manufactured 581,000.

00

Direct labour costs incurred 205,000.

00

Manufacturing overhead 173,000.

00

653,000.

00

Less:

Closing balance of direct materials 42,000.

00

Closing balance of WIP 30,000.

00

72,000.

00

Cost of goods manufactured 581,000.

00

Cost of goods sold

Cost of goods manufactured 581,000.

00

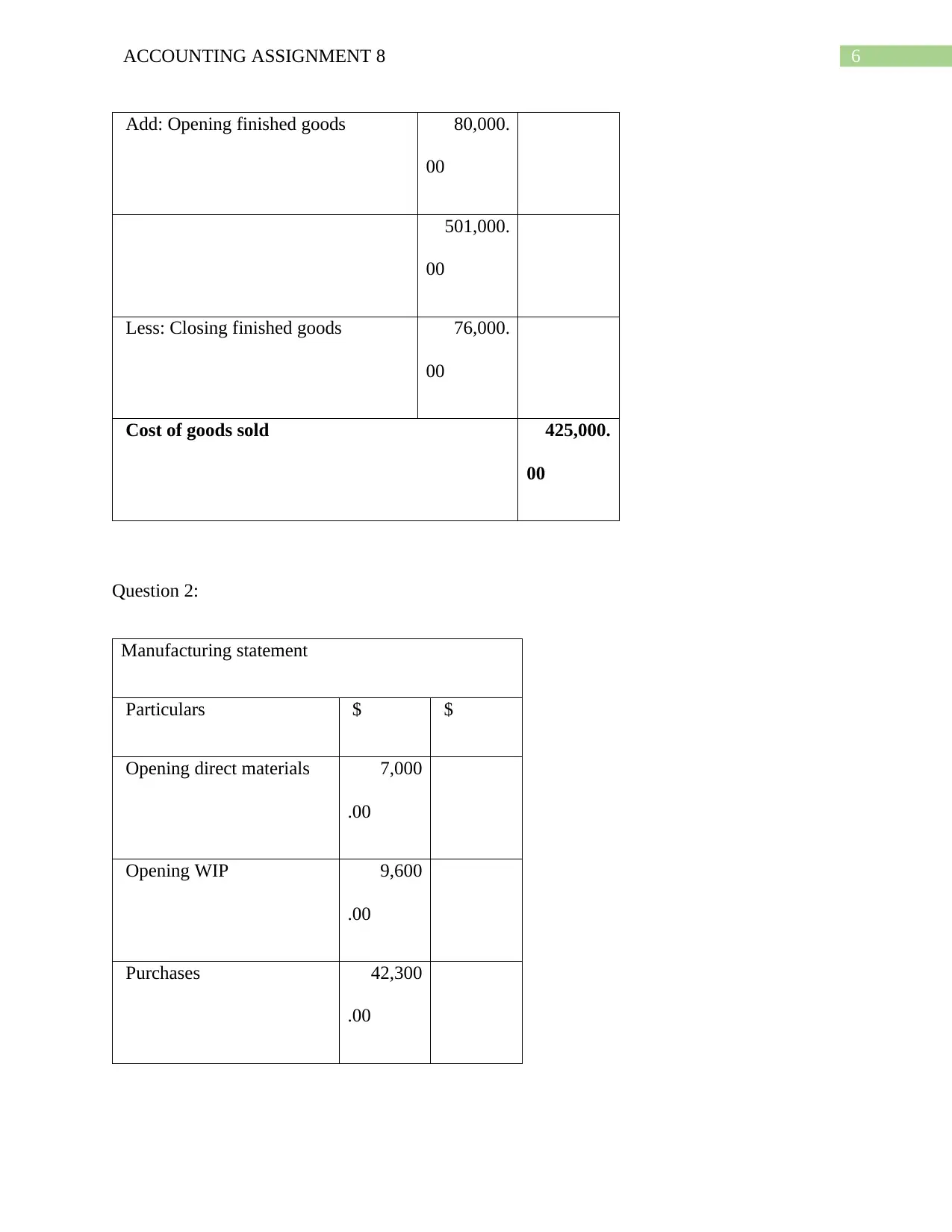

6ACCOUNTING ASSIGNMENT 8

Add: Opening finished goods 80,000.

00

501,000.

00

Less: Closing finished goods 76,000.

00

Cost of goods sold 425,000.

00

Question 2:

Manufacturing statement

Particulars $ $

Opening direct materials 7,000

.00

Opening WIP 9,600

.00

Purchases 42,300

.00

Add: Opening finished goods 80,000.

00

501,000.

00

Less: Closing finished goods 76,000.

00

Cost of goods sold 425,000.

00

Question 2:

Manufacturing statement

Particulars $ $

Opening direct materials 7,000

.00

Opening WIP 9,600

.00

Purchases 42,300

.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING ASSIGNMENT 8

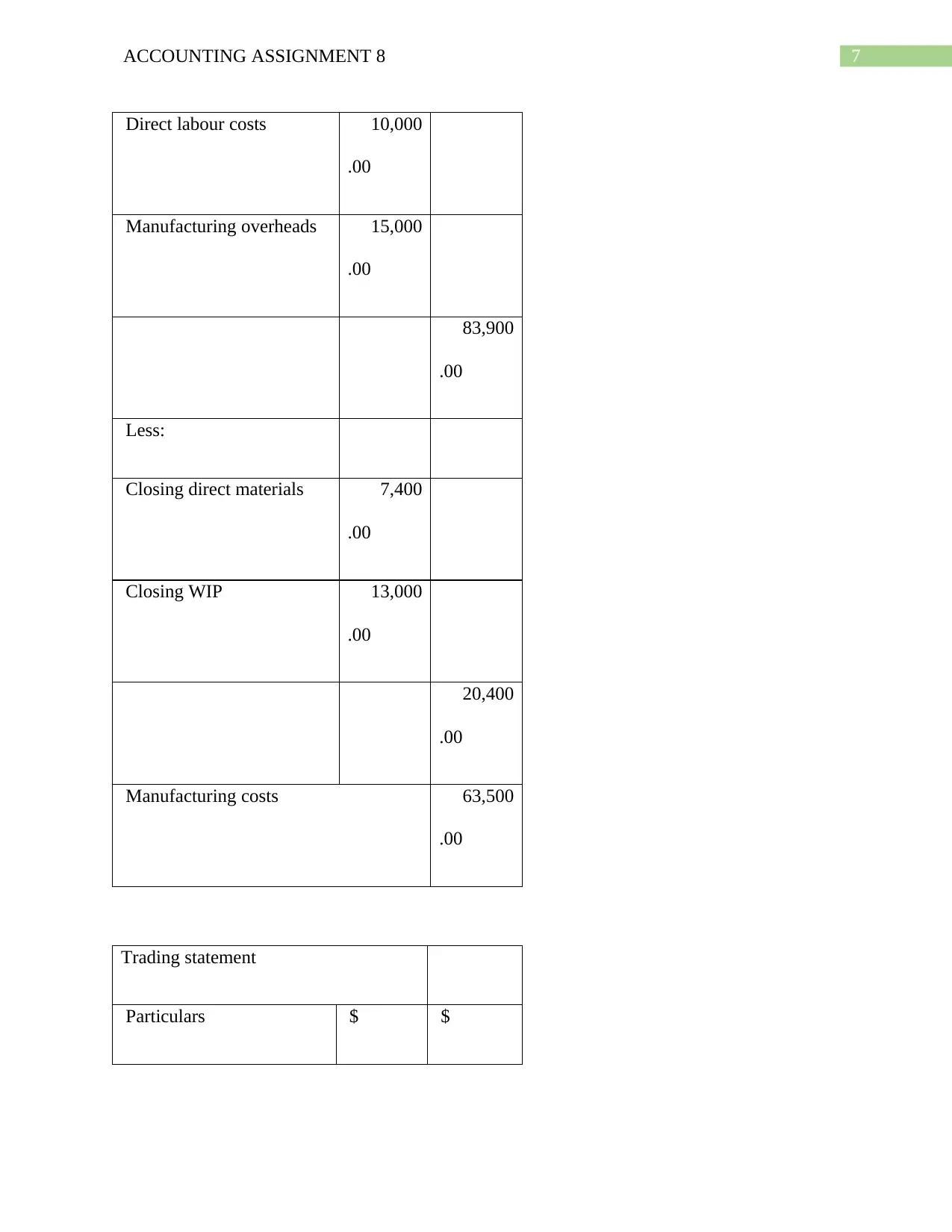

Direct labour costs 10,000

.00

Manufacturing overheads 15,000

.00

83,900

.00

Less:

Closing direct materials 7,400

.00

Closing WIP 13,000

.00

20,400

.00

Manufacturing costs 63,500

.00

Trading statement

Particulars $ $

Direct labour costs 10,000

.00

Manufacturing overheads 15,000

.00

83,900

.00

Less:

Closing direct materials 7,400

.00

Closing WIP 13,000

.00

20,400

.00

Manufacturing costs 63,500

.00

Trading statement

Particulars $ $

8ACCOUNTING ASSIGNMENT 8

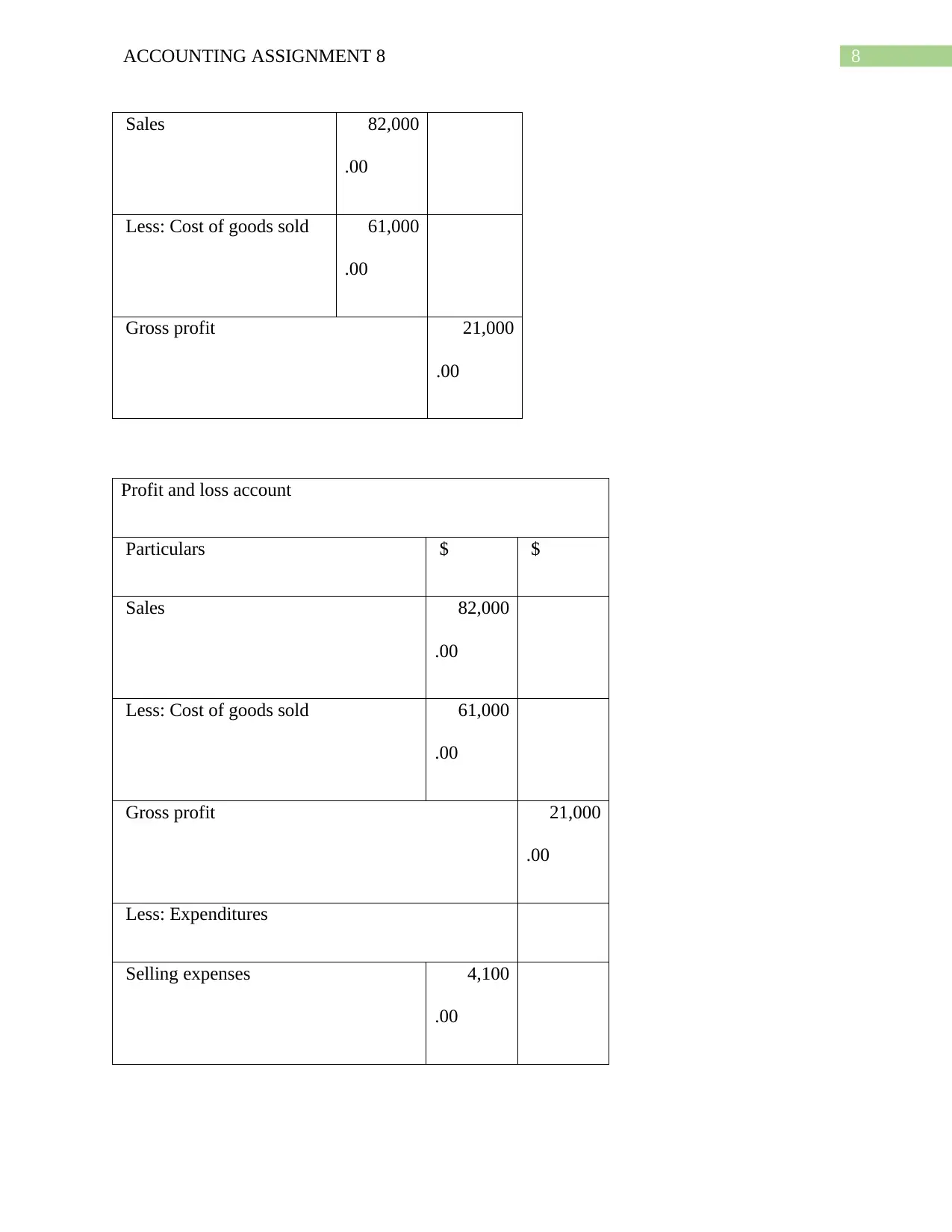

Sales 82,000

.00

Less: Cost of goods sold 61,000

.00

Gross profit 21,000

.00

Profit and loss account

Particulars $ $

Sales 82,000

.00

Less: Cost of goods sold 61,000

.00

Gross profit 21,000

.00

Less: Expenditures

Selling expenses 4,100

.00

Sales 82,000

.00

Less: Cost of goods sold 61,000

.00

Gross profit 21,000

.00

Profit and loss account

Particulars $ $

Sales 82,000

.00

Less: Cost of goods sold 61,000

.00

Gross profit 21,000

.00

Less: Expenditures

Selling expenses 4,100

.00

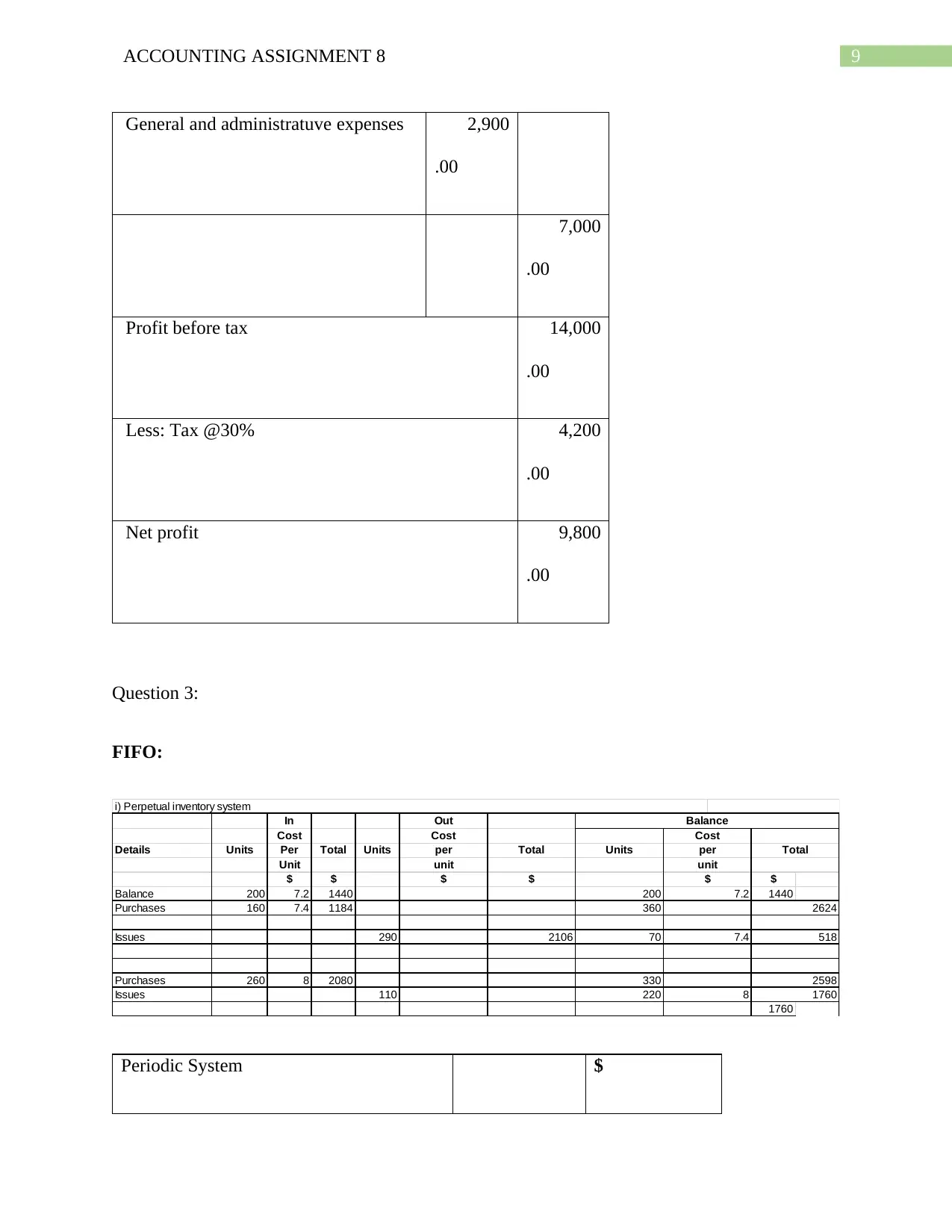

9ACCOUNTING ASSIGNMENT 8

General and administratuve expenses 2,900

.00

7,000

.00

Profit before tax 14,000

.00

Less: Tax @30% 4,200

.00

Net profit 9,800

.00

Question 3:

FIFO:

In

Cost

Units Per Total Units

Unit

$ $ $

200 7.2 1440 1440

160 7.4 1184

290

260 8 2080

110

1760

Issues 220 8 1760

Purchases 330 2598

Issues 2106 70 7.4 518

Purchases 360 2624

$ $ $

Balance 200 7.2

unit unit

Details per Total Units per Total

Cost Cost

i) Perpetual inventory system

Out Balance

Periodic System $

General and administratuve expenses 2,900

.00

7,000

.00

Profit before tax 14,000

.00

Less: Tax @30% 4,200

.00

Net profit 9,800

.00

Question 3:

FIFO:

In

Cost

Units Per Total Units

Unit

$ $ $

200 7.2 1440 1440

160 7.4 1184

290

260 8 2080

110

1760

Issues 220 8 1760

Purchases 330 2598

Issues 2106 70 7.4 518

Purchases 360 2624

$ $ $

Balance 200 7.2

unit unit

Details per Total Units per Total

Cost Cost

i) Perpetual inventory system

Out Balance

Periodic System $

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

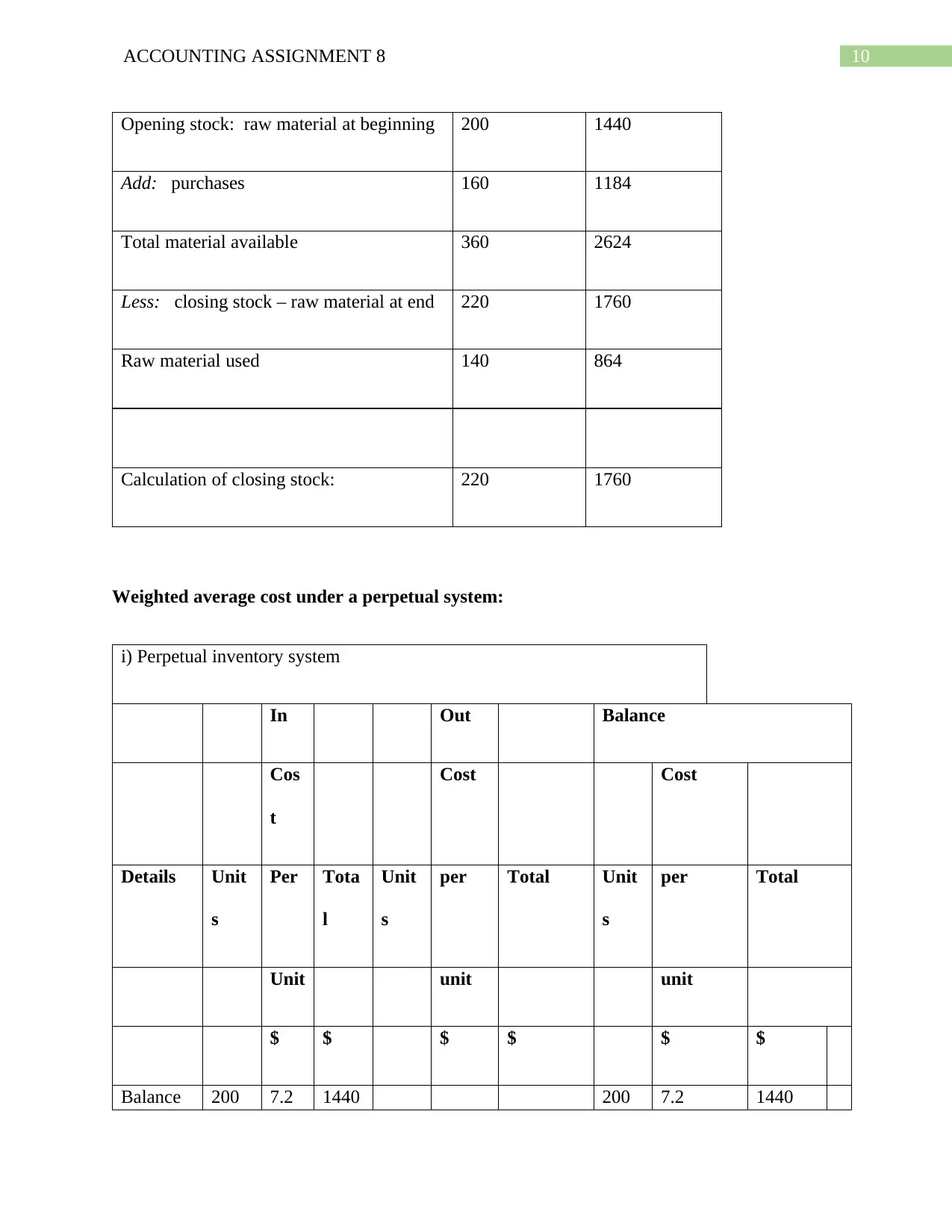

10ACCOUNTING ASSIGNMENT 8

Opening stock: raw material at beginning 200 1440

Add: purchases 160 1184

Total material available 360 2624

Less: closing stock – raw material at end 220 1760

Raw material used 140 864

Calculation of closing stock: 220 1760

Weighted average cost under a perpetual system:

i) Perpetual inventory system

In Out Balance

Cos

t

Cost Cost

Details Unit

s

Per Tota

l

Unit

s

per Total Unit

s

per Total

Unit unit unit

$ $ $ $ $ $

Balance 200 7.2 1440 200 7.2 1440

Opening stock: raw material at beginning 200 1440

Add: purchases 160 1184

Total material available 360 2624

Less: closing stock – raw material at end 220 1760

Raw material used 140 864

Calculation of closing stock: 220 1760

Weighted average cost under a perpetual system:

i) Perpetual inventory system

In Out Balance

Cos

t

Cost Cost

Details Unit

s

Per Tota

l

Unit

s

per Total Unit

s

per Total

Unit unit unit

$ $ $ $ $ $

Balance 200 7.2 1440 200 7.2 1440

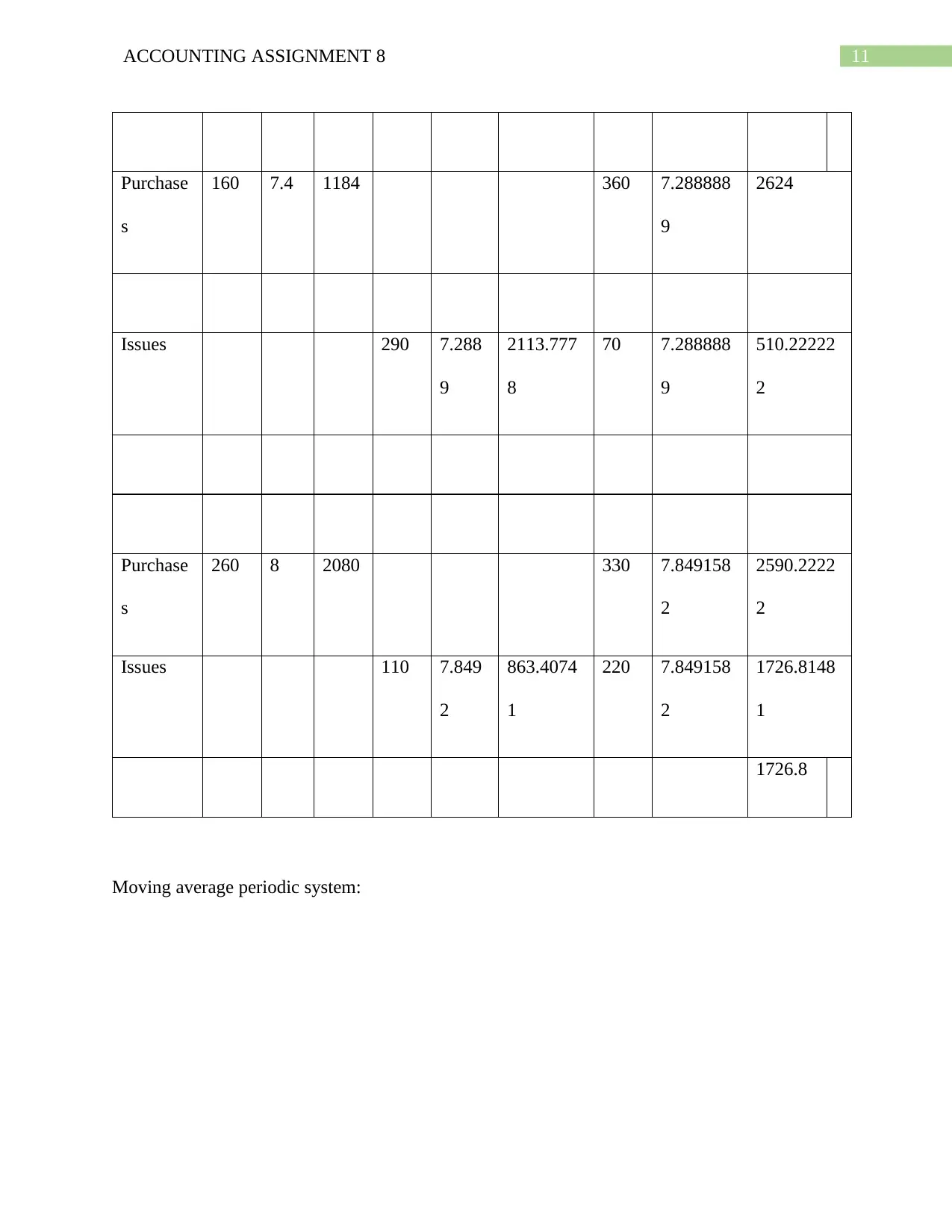

11ACCOUNTING ASSIGNMENT 8

Purchase

s

160 7.4 1184 360 7.288888

9

2624

Issues 290 7.288

9

2113.777

8

70 7.288888

9

510.22222

2

Purchase

s

260 8 2080 330 7.849158

2

2590.2222

2

Issues 110 7.849

2

863.4074

1

220 7.849158

2

1726.8148

1

1726.8

Moving average periodic system:

Purchase

s

160 7.4 1184 360 7.288888

9

2624

Issues 290 7.288

9

2113.777

8

70 7.288888

9

510.22222

2

Purchase

s

260 8 2080 330 7.849158

2

2590.2222

2

Issues 110 7.849

2

863.4074

1

220 7.849158

2

1726.8148

1

1726.8

Moving average periodic system:

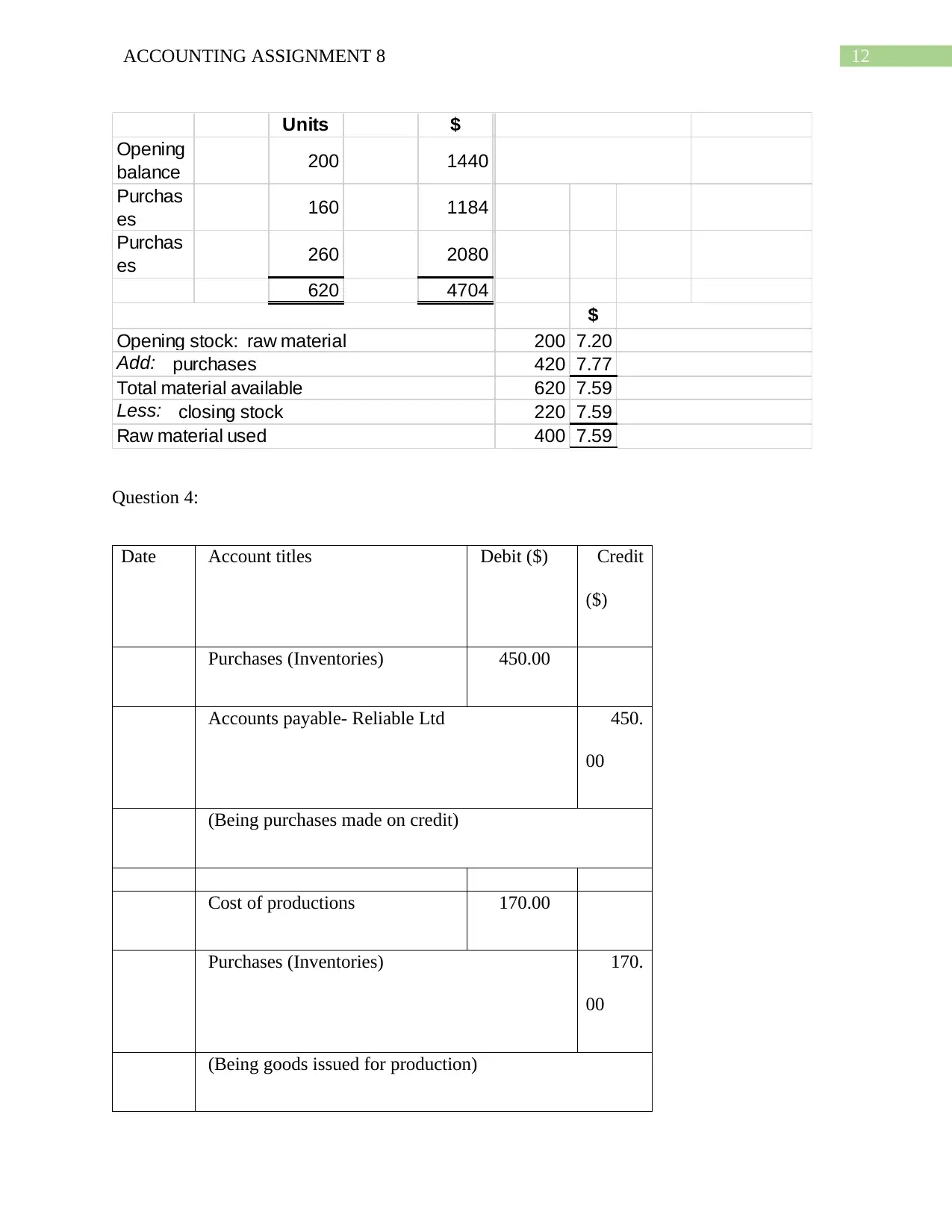

12ACCOUNTING ASSIGNMENT 8

Units $

Opening

balance 200 1440

Purchas

es 160 1184

Purchas

es 260 2080

620 4704

$

200 7.20

420 7.77

620 7.59

220 7.59

400 7.59

Less: closing stock

Raw material used

Opening stock: raw material

Add: purchases

Total material available

Question 4:

Date Account titles Debit ($) Credit

($)

Purchases (Inventories) 450.00

Accounts payable- Reliable Ltd 450.

00

(Being purchases made on credit)

Cost of productions 170.00

Purchases (Inventories) 170.

00

(Being goods issued for production)

Units $

Opening

balance 200 1440

Purchas

es 160 1184

Purchas

es 260 2080

620 4704

$

200 7.20

420 7.77

620 7.59

220 7.59

400 7.59

Less: closing stock

Raw material used

Opening stock: raw material

Add: purchases

Total material available

Question 4:

Date Account titles Debit ($) Credit

($)

Purchases (Inventories) 450.00

Accounts payable- Reliable Ltd 450.

00

(Being purchases made on credit)

Cost of productions 170.00

Purchases (Inventories) 170.

00

(Being goods issued for production)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

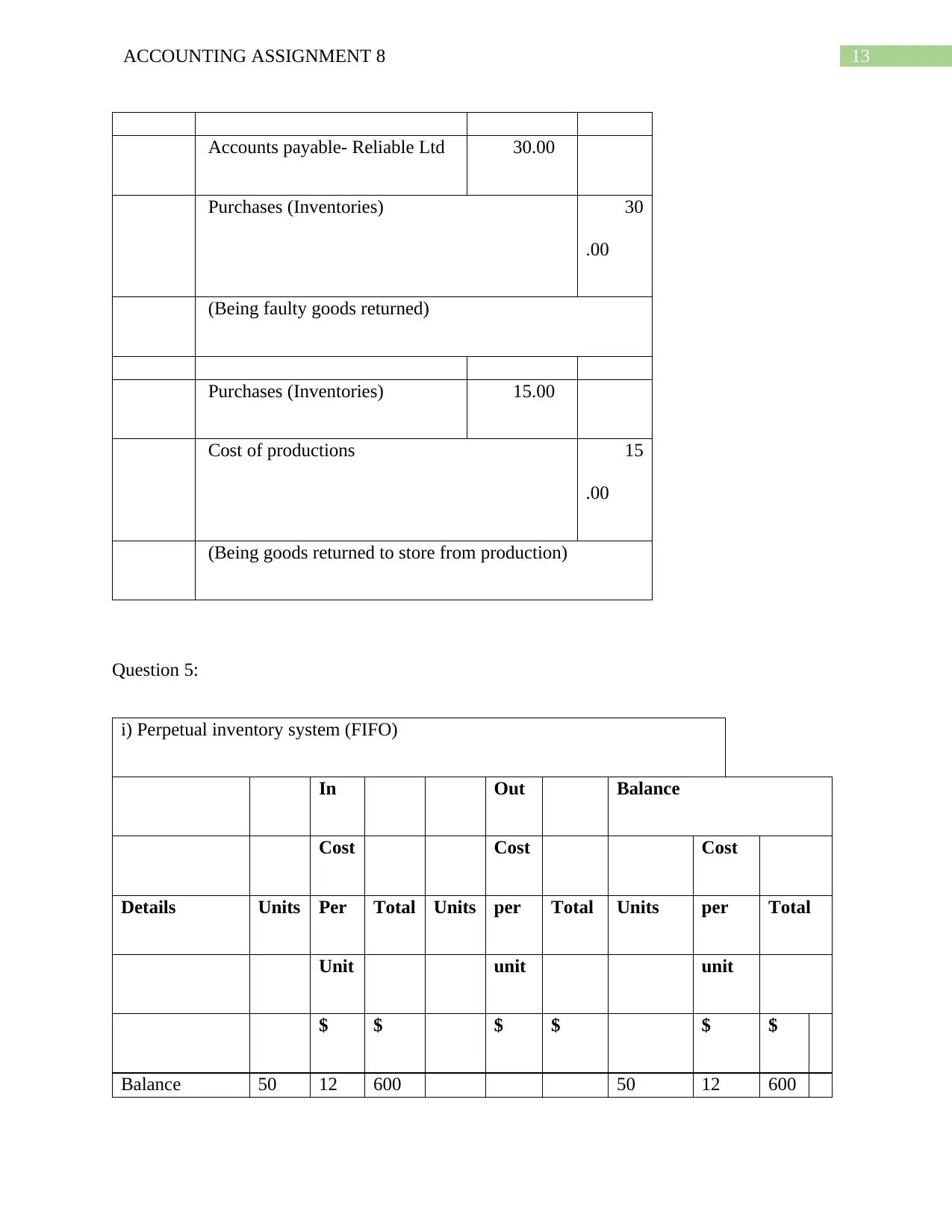

13ACCOUNTING ASSIGNMENT 8

Accounts payable- Reliable Ltd 30.00

Purchases (Inventories) 30

.00

(Being faulty goods returned)

Purchases (Inventories) 15.00

Cost of productions 15

.00

(Being goods returned to store from production)

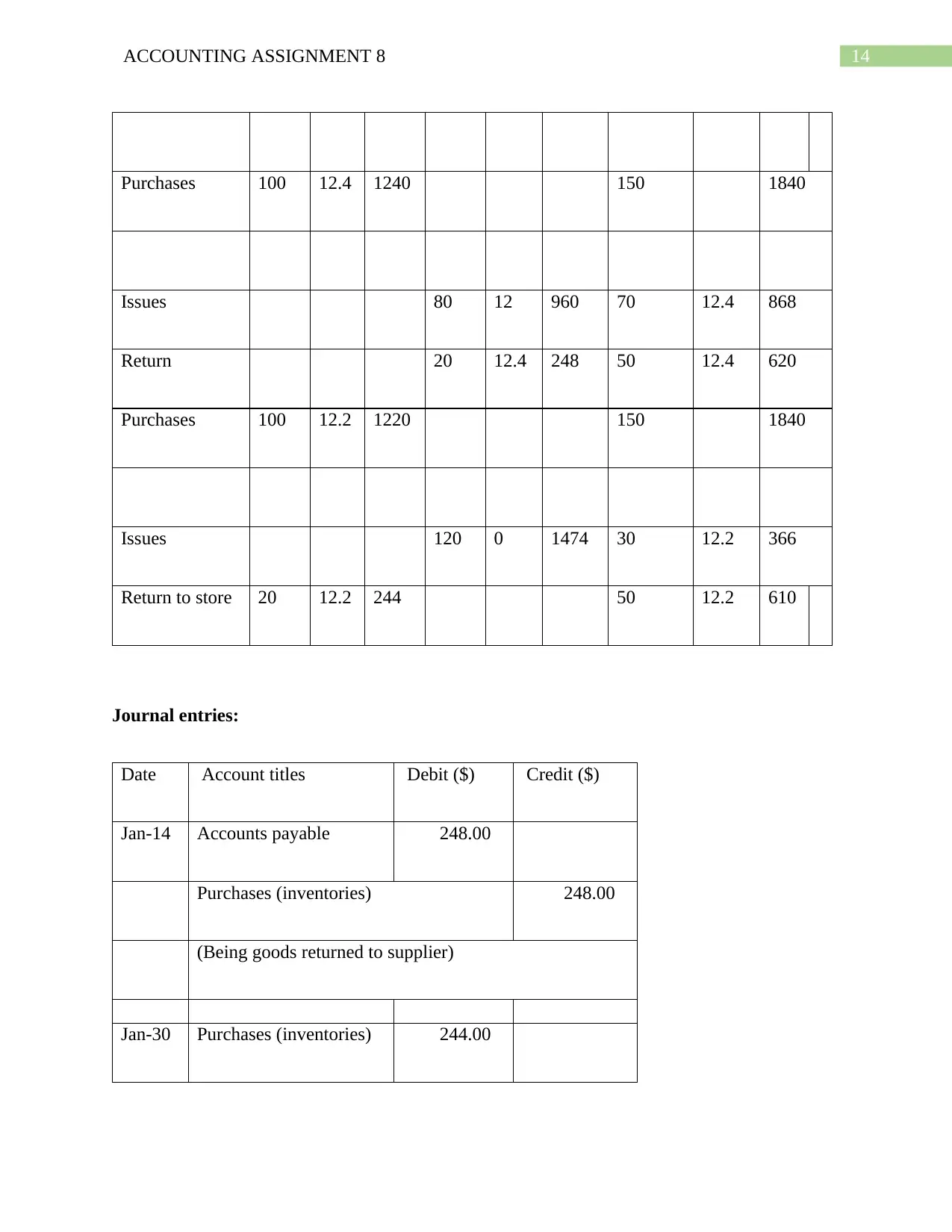

Question 5:

i) Perpetual inventory system (FIFO)

In Out Balance

Cost Cost Cost

Details Units Per Total Units per Total Units per Total

Unit unit unit

$ $ $ $ $ $

Balance 50 12 600 50 12 600

Accounts payable- Reliable Ltd 30.00

Purchases (Inventories) 30

.00

(Being faulty goods returned)

Purchases (Inventories) 15.00

Cost of productions 15

.00

(Being goods returned to store from production)

Question 5:

i) Perpetual inventory system (FIFO)

In Out Balance

Cost Cost Cost

Details Units Per Total Units per Total Units per Total

Unit unit unit

$ $ $ $ $ $

Balance 50 12 600 50 12 600

14ACCOUNTING ASSIGNMENT 8

Purchases 100 12.4 1240 150 1840

Issues 80 12 960 70 12.4 868

Return 20 12.4 248 50 12.4 620

Purchases 100 12.2 1220 150 1840

Issues 120 0 1474 30 12.2 366

Return to store 20 12.2 244 50 12.2 610

Journal entries:

Date Account titles Debit ($) Credit ($)

Jan-14 Accounts payable 248.00

Purchases (inventories) 248.00

(Being goods returned to supplier)

Jan-30 Purchases (inventories) 244.00

Purchases 100 12.4 1240 150 1840

Issues 80 12 960 70 12.4 868

Return 20 12.4 248 50 12.4 620

Purchases 100 12.2 1220 150 1840

Issues 120 0 1474 30 12.2 366

Return to store 20 12.2 244 50 12.2 610

Journal entries:

Date Account titles Debit ($) Credit ($)

Jan-14 Accounts payable 248.00

Purchases (inventories) 248.00

(Being goods returned to supplier)

Jan-30 Purchases (inventories) 244.00

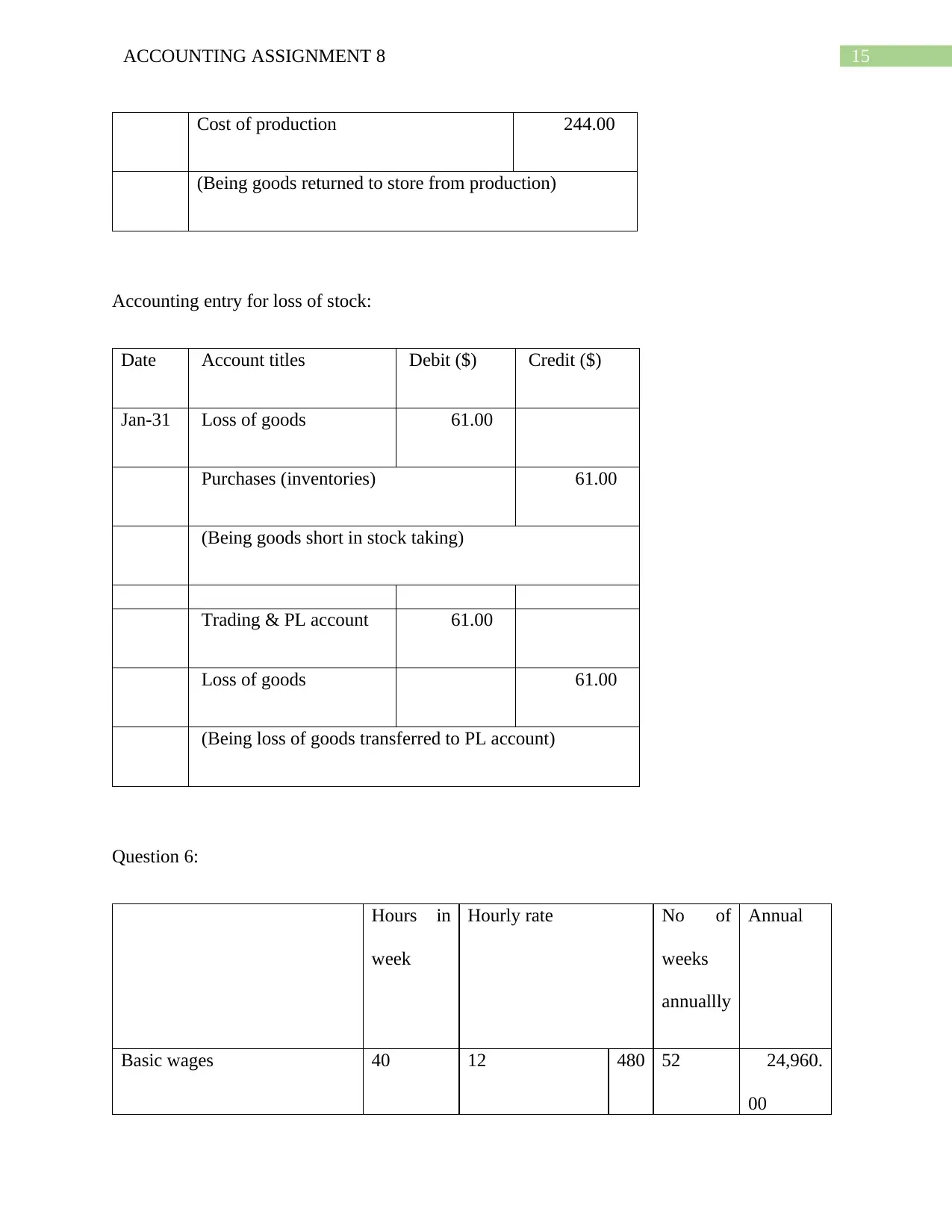

15ACCOUNTING ASSIGNMENT 8

Cost of production 244.00

(Being goods returned to store from production)

Accounting entry for loss of stock:

Date Account titles Debit ($) Credit ($)

Jan-31 Loss of goods 61.00

Purchases (inventories) 61.00

(Being goods short in stock taking)

Trading & PL account 61.00

Loss of goods 61.00

(Being loss of goods transferred to PL account)

Question 6:

Hours in

week

Hourly rate No of

weeks

annuallly

Annual

Basic wages 40 12 480 52 24,960.

00

Cost of production 244.00

(Being goods returned to store from production)

Accounting entry for loss of stock:

Date Account titles Debit ($) Credit ($)

Jan-31 Loss of goods 61.00

Purchases (inventories) 61.00

(Being goods short in stock taking)

Trading & PL account 61.00

Loss of goods 61.00

(Being loss of goods transferred to PL account)

Question 6:

Hours in

week

Hourly rate No of

weeks

annuallly

Annual

Basic wages 40 12 480 52 24,960.

00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

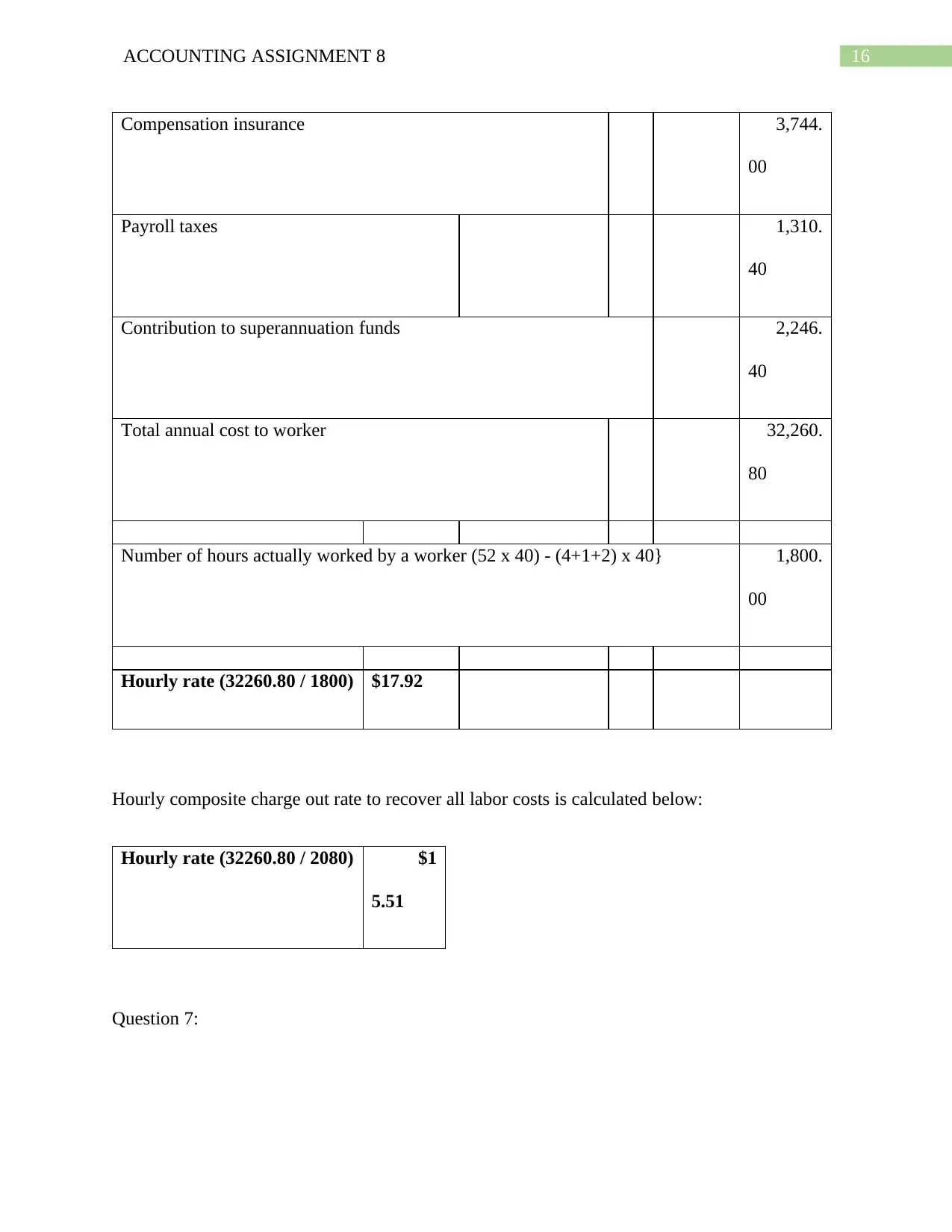

16ACCOUNTING ASSIGNMENT 8

Compensation insurance 3,744.

00

Payroll taxes 1,310.

40

Contribution to superannuation funds 2,246.

40

Total annual cost to worker 32,260.

80

Number of hours actually worked by a worker (52 x 40) - (4+1+2) x 40} 1,800.

00

Hourly rate (32260.80 / 1800) $17.92

Hourly composite charge out rate to recover all labor costs is calculated below:

Hourly rate (32260.80 / 2080) $1

5.51

Question 7:

Compensation insurance 3,744.

00

Payroll taxes 1,310.

40

Contribution to superannuation funds 2,246.

40

Total annual cost to worker 32,260.

80

Number of hours actually worked by a worker (52 x 40) - (4+1+2) x 40} 1,800.

00

Hourly rate (32260.80 / 1800) $17.92

Hourly composite charge out rate to recover all labor costs is calculated below:

Hourly rate (32260.80 / 2080) $1

5.51

Question 7:

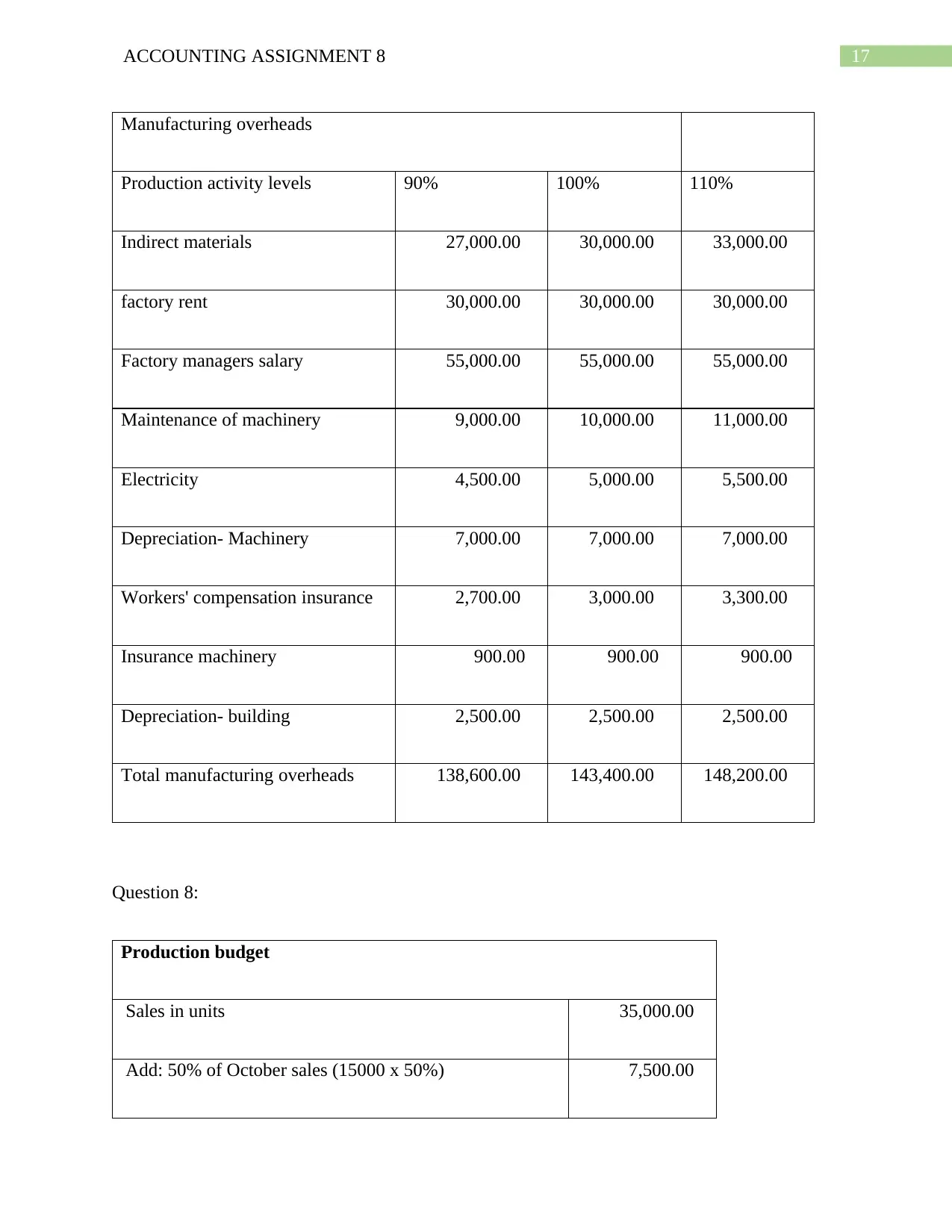

17ACCOUNTING ASSIGNMENT 8

Manufacturing overheads

Production activity levels 90% 100% 110%

Indirect materials 27,000.00 30,000.00 33,000.00

factory rent 30,000.00 30,000.00 30,000.00

Factory managers salary 55,000.00 55,000.00 55,000.00

Maintenance of machinery 9,000.00 10,000.00 11,000.00

Electricity 4,500.00 5,000.00 5,500.00

Depreciation- Machinery 7,000.00 7,000.00 7,000.00

Workers' compensation insurance 2,700.00 3,000.00 3,300.00

Insurance machinery 900.00 900.00 900.00

Depreciation- building 2,500.00 2,500.00 2,500.00

Total manufacturing overheads 138,600.00 143,400.00 148,200.00

Question 8:

Production budget

Sales in units 35,000.00

Add: 50% of October sales (15000 x 50%) 7,500.00

Manufacturing overheads

Production activity levels 90% 100% 110%

Indirect materials 27,000.00 30,000.00 33,000.00

factory rent 30,000.00 30,000.00 30,000.00

Factory managers salary 55,000.00 55,000.00 55,000.00

Maintenance of machinery 9,000.00 10,000.00 11,000.00

Electricity 4,500.00 5,000.00 5,500.00

Depreciation- Machinery 7,000.00 7,000.00 7,000.00

Workers' compensation insurance 2,700.00 3,000.00 3,300.00

Insurance machinery 900.00 900.00 900.00

Depreciation- building 2,500.00 2,500.00 2,500.00

Total manufacturing overheads 138,600.00 143,400.00 148,200.00

Question 8:

Production budget

Sales in units 35,000.00

Add: 50% of October sales (15000 x 50%) 7,500.00

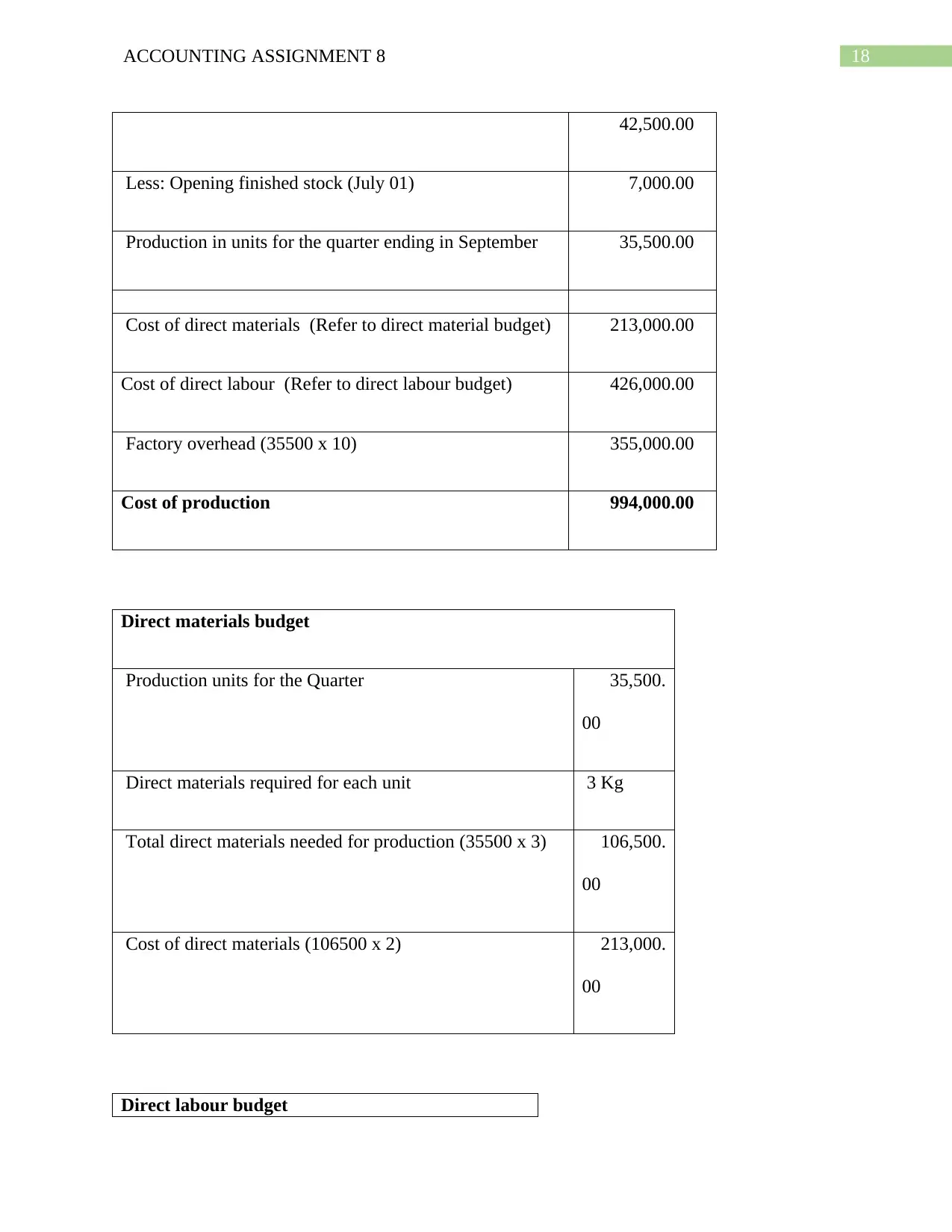

18ACCOUNTING ASSIGNMENT 8

42,500.00

Less: Opening finished stock (July 01) 7,000.00

Production in units for the quarter ending in September 35,500.00

Cost of direct materials (Refer to direct material budget) 213,000.00

Cost of direct labour (Refer to direct labour budget) 426,000.00

Factory overhead (35500 x 10) 355,000.00

Cost of production 994,000.00

Direct materials budget

Production units for the Quarter 35,500.

00

Direct materials required for each unit 3 Kg

Total direct materials needed for production (35500 x 3) 106,500.

00

Cost of direct materials (106500 x 2) 213,000.

00

Direct labour budget

42,500.00

Less: Opening finished stock (July 01) 7,000.00

Production in units for the quarter ending in September 35,500.00

Cost of direct materials (Refer to direct material budget) 213,000.00

Cost of direct labour (Refer to direct labour budget) 426,000.00

Factory overhead (35500 x 10) 355,000.00

Cost of production 994,000.00

Direct materials budget

Production units for the Quarter 35,500.

00

Direct materials required for each unit 3 Kg

Total direct materials needed for production (35500 x 3) 106,500.

00

Cost of direct materials (106500 x 2) 213,000.

00

Direct labour budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

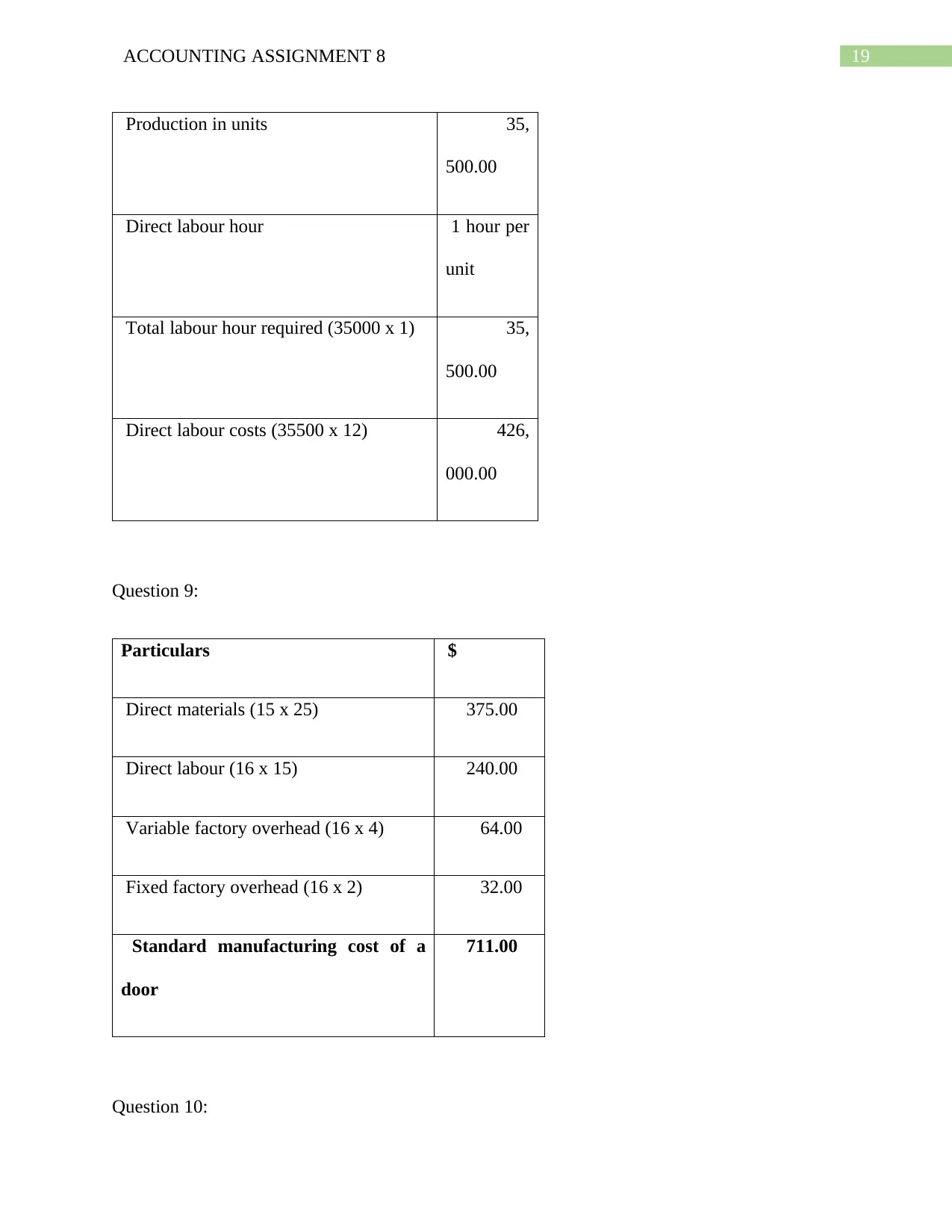

19ACCOUNTING ASSIGNMENT 8

Production in units 35,

500.00

Direct labour hour 1 hour per

unit

Total labour hour required (35000 x 1) 35,

500.00

Direct labour costs (35500 x 12) 426,

000.00

Question 9:

Particulars $

Direct materials (15 x 25) 375.00

Direct labour (16 x 15) 240.00

Variable factory overhead (16 x 4) 64.00

Fixed factory overhead (16 x 2) 32.00

Standard manufacturing cost of a

door

711.00

Question 10:

Production in units 35,

500.00

Direct labour hour 1 hour per

unit

Total labour hour required (35000 x 1) 35,

500.00

Direct labour costs (35500 x 12) 426,

000.00

Question 9:

Particulars $

Direct materials (15 x 25) 375.00

Direct labour (16 x 15) 240.00

Variable factory overhead (16 x 4) 64.00

Fixed factory overhead (16 x 2) 32.00

Standard manufacturing cost of a

door

711.00

Question 10:

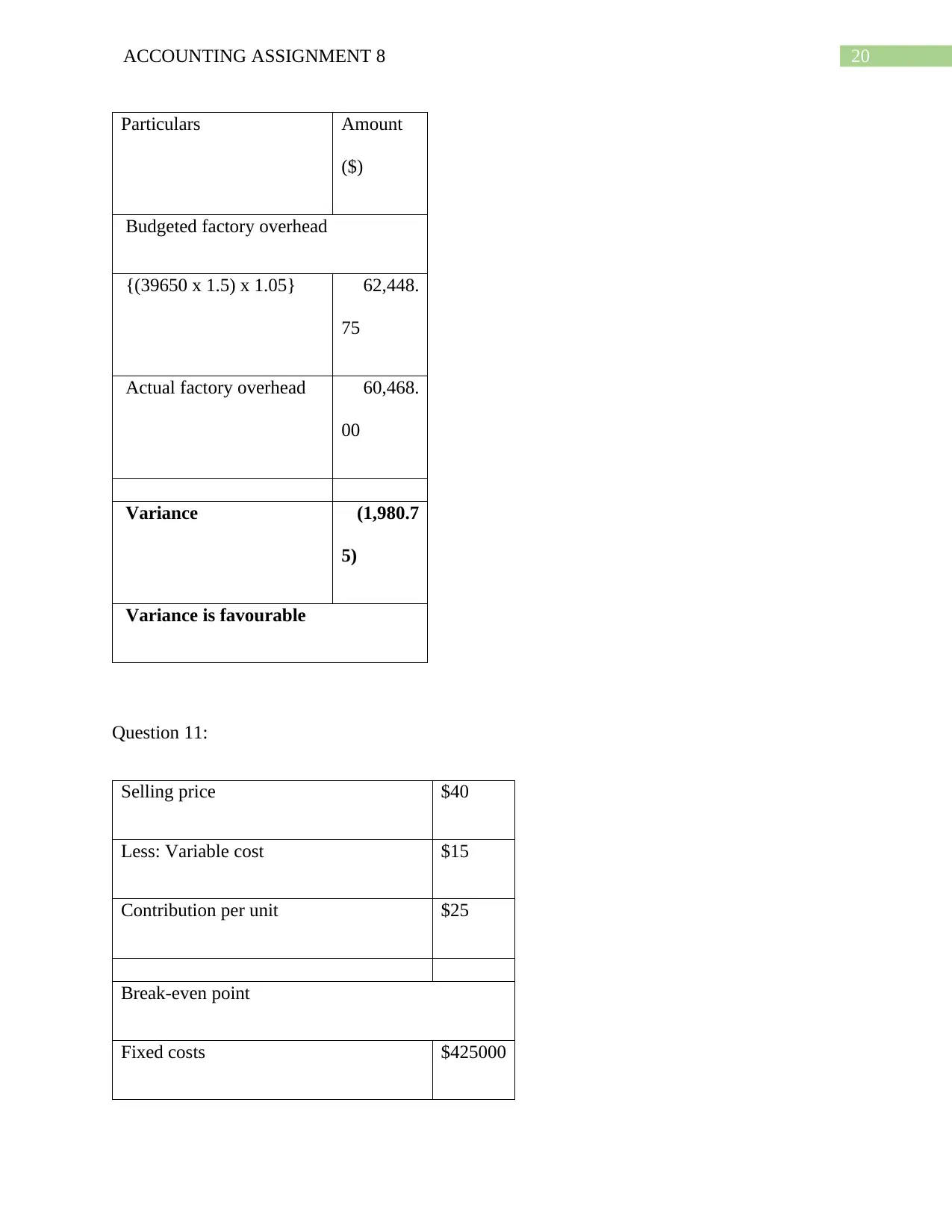

20ACCOUNTING ASSIGNMENT 8

Particulars Amount

($)

Budgeted factory overhead

{(39650 x 1.5) x 1.05} 62,448.

75

Actual factory overhead 60,468.

00

Variance (1,980.7

5)

Variance is favourable

Question 11:

Selling price $40

Less: Variable cost $15

Contribution per unit $25

Break-even point

Fixed costs $425000

Particulars Amount

($)

Budgeted factory overhead

{(39650 x 1.5) x 1.05} 62,448.

75

Actual factory overhead 60,468.

00

Variance (1,980.7

5)

Variance is favourable

Question 11:

Selling price $40

Less: Variable cost $15

Contribution per unit $25

Break-even point

Fixed costs $425000

21ACCOUNTING ASSIGNMENT 8

Contribution per unit $25

Break-even point in units (425000 /

25)

17000

Break-even point in sales (17000 x 40) 680000

0 . 5 1 1 . 5 2 2 . 5 3 3 . 5 4 4 . 5

0

100000

200000

300000

400000

500000

600000

700000

800000

Chart Title

Question 12:

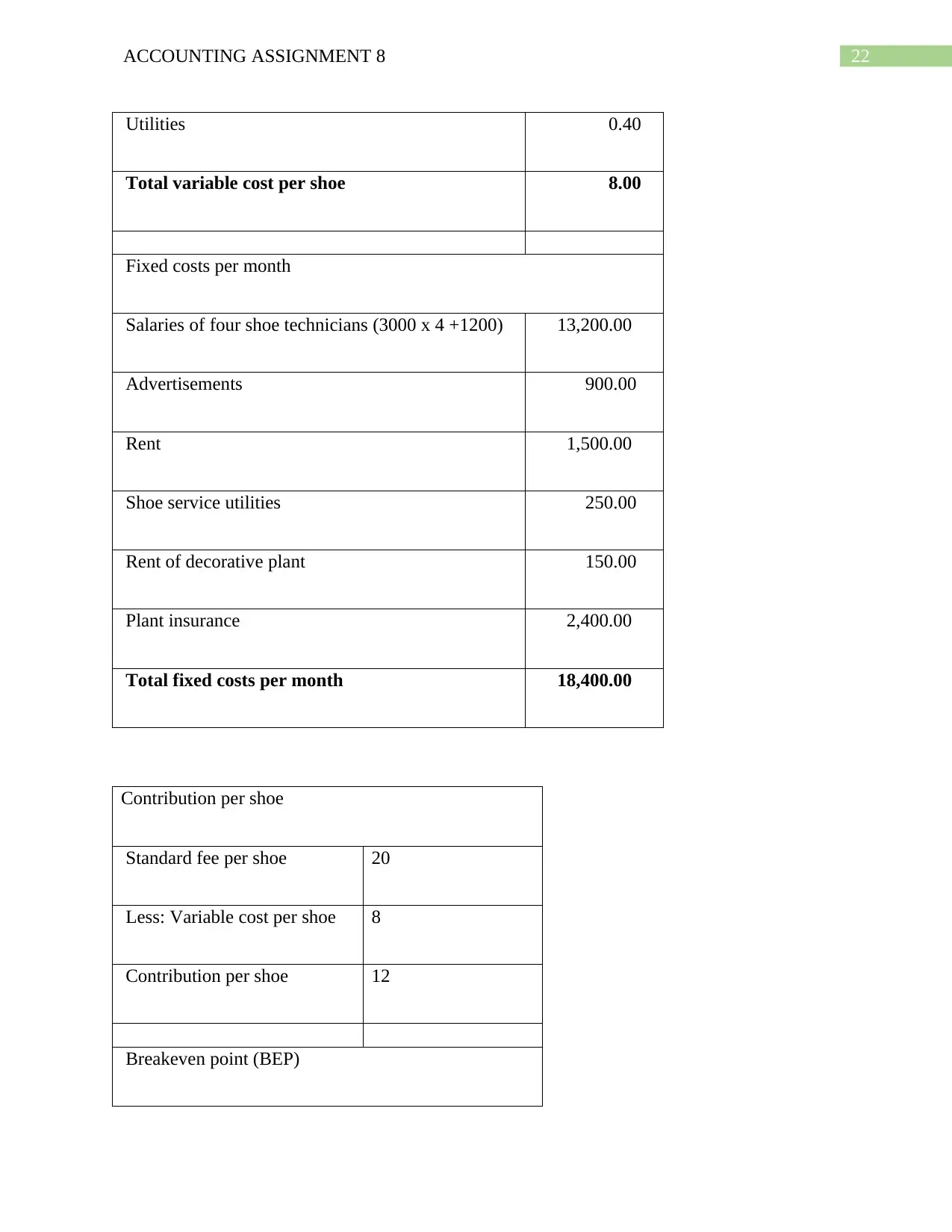

Variable costs

Particulars $

Commission on each shoe 7.00

Shoe service supplies 0.60

Contribution per unit $25

Break-even point in units (425000 /

25)

17000

Break-even point in sales (17000 x 40) 680000

0 . 5 1 1 . 5 2 2 . 5 3 3 . 5 4 4 . 5

0

100000

200000

300000

400000

500000

600000

700000

800000

Chart Title

Question 12:

Variable costs

Particulars $

Commission on each shoe 7.00

Shoe service supplies 0.60

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22ACCOUNTING ASSIGNMENT 8

Utilities 0.40

Total variable cost per shoe 8.00

Fixed costs per month

Salaries of four shoe technicians (3000 x 4 +1200) 13,200.00

Advertisements 900.00

Rent 1,500.00

Shoe service utilities 250.00

Rent of decorative plant 150.00

Plant insurance 2,400.00

Total fixed costs per month 18,400.00

Contribution per shoe

Standard fee per shoe 20

Less: Variable cost per shoe 8

Contribution per shoe 12

Breakeven point (BEP)

Utilities 0.40

Total variable cost per shoe 8.00

Fixed costs per month

Salaries of four shoe technicians (3000 x 4 +1200) 13,200.00

Advertisements 900.00

Rent 1,500.00

Shoe service utilities 250.00

Rent of decorative plant 150.00

Plant insurance 2,400.00

Total fixed costs per month 18,400.00

Contribution per shoe

Standard fee per shoe 20

Less: Variable cost per shoe 8

Contribution per shoe 12

Breakeven point (BEP)

23ACCOUNTING ASSIGNMENT 8

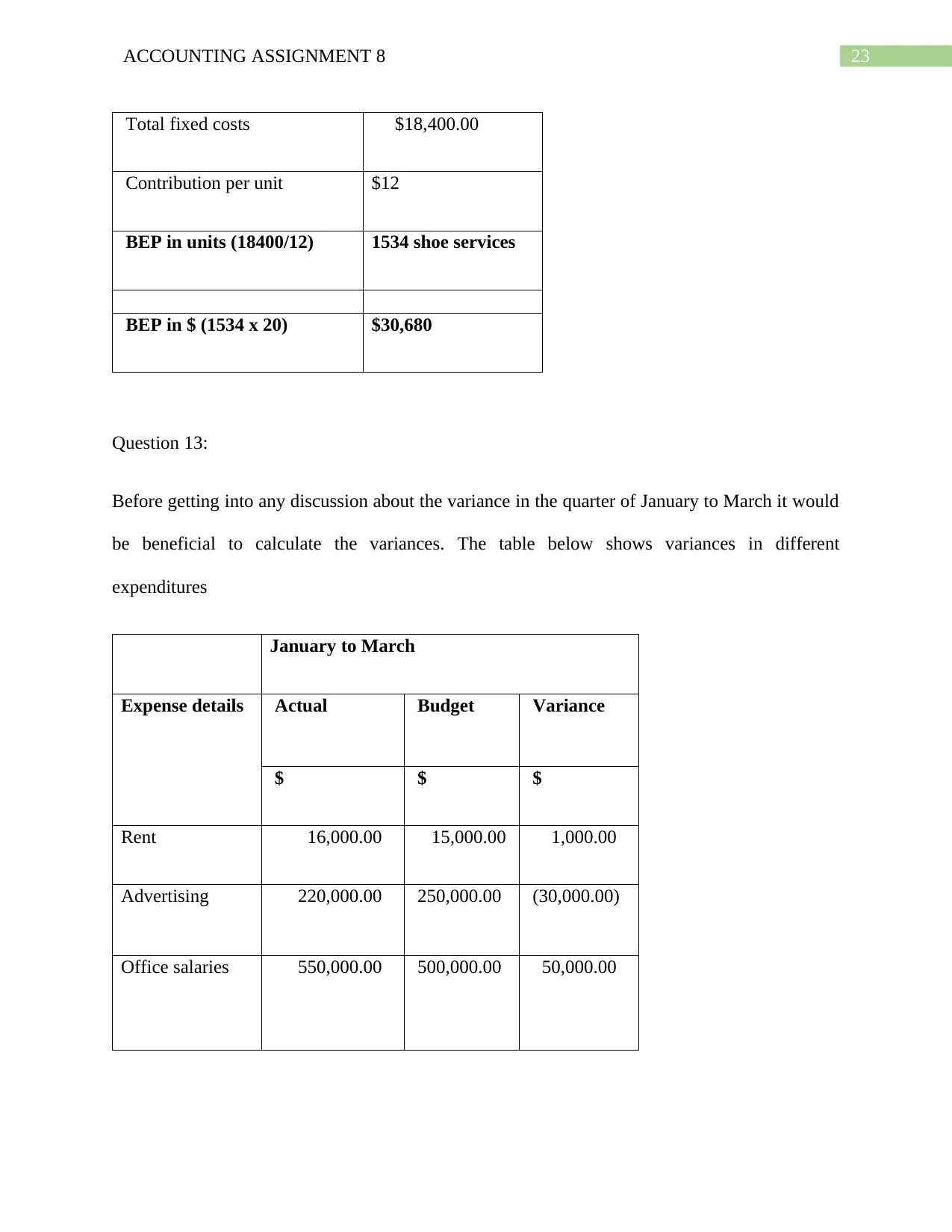

Total fixed costs $18,400.00

Contribution per unit $12

BEP in units (18400/12) 1534 shoe services

BEP in $ (1534 x 20) $30,680

Question 13:

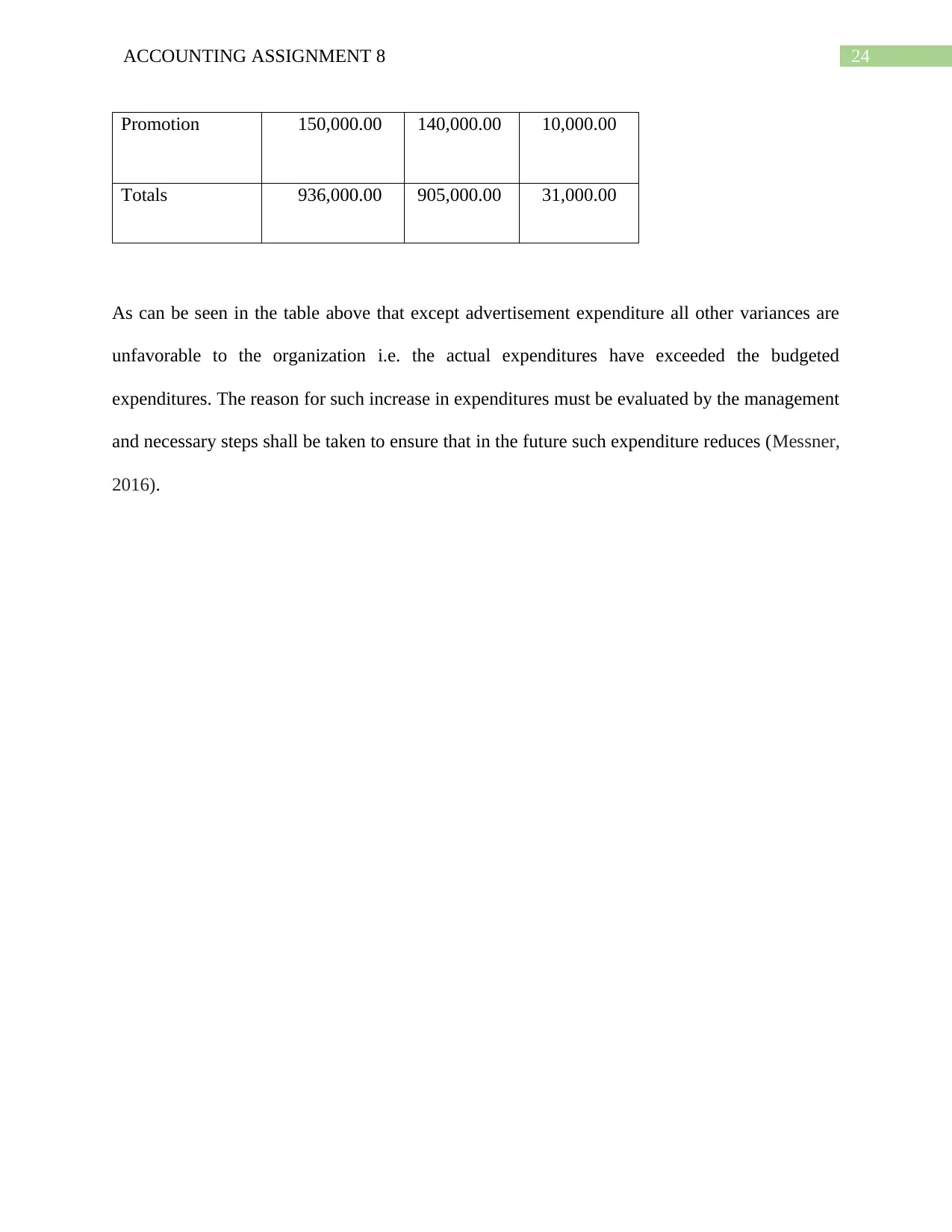

Before getting into any discussion about the variance in the quarter of January to March it would

be beneficial to calculate the variances. The table below shows variances in different

expenditures

January to March

Expense details Actual Budget Variance

$ $ $

Rent 16,000.00 15,000.00 1,000.00

Advertising 220,000.00 250,000.00 (30,000.00)

Office salaries 550,000.00 500,000.00 50,000.00

Total fixed costs $18,400.00

Contribution per unit $12

BEP in units (18400/12) 1534 shoe services

BEP in $ (1534 x 20) $30,680

Question 13:

Before getting into any discussion about the variance in the quarter of January to March it would

be beneficial to calculate the variances. The table below shows variances in different

expenditures

January to March

Expense details Actual Budget Variance

$ $ $

Rent 16,000.00 15,000.00 1,000.00

Advertising 220,000.00 250,000.00 (30,000.00)

Office salaries 550,000.00 500,000.00 50,000.00

24ACCOUNTING ASSIGNMENT 8

Promotion 150,000.00 140,000.00 10,000.00

Totals 936,000.00 905,000.00 31,000.00

As can be seen in the table above that except advertisement expenditure all other variances are

unfavorable to the organization i.e. the actual expenditures have exceeded the budgeted

expenditures. The reason for such increase in expenditures must be evaluated by the management

and necessary steps shall be taken to ensure that in the future such expenditure reduces (Messner,

2016).

Promotion 150,000.00 140,000.00 10,000.00

Totals 936,000.00 905,000.00 31,000.00

As can be seen in the table above that except advertisement expenditure all other variances are

unfavorable to the organization i.e. the actual expenditures have exceeded the budgeted

expenditures. The reason for such increase in expenditures must be evaluated by the management

and necessary steps shall be taken to ensure that in the future such expenditure reduces (Messner,

2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25ACCOUNTING ASSIGNMENT 8

References:

Dekker, H. C. (2016). On the boundaries between intrafirm and interfirm management

accounting research. Management Accounting Research, 31, 86-99.

Fullerton, R. R., Kennedy, F. A., & Widener, S. K. (2014). Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), 414-428.

Messner, M. (2016). Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research, 31, 103-111.

Otley, D. (2016). The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, 45-62.

References:

Dekker, H. C. (2016). On the boundaries between intrafirm and interfirm management

accounting research. Management Accounting Research, 31, 86-99.

Fullerton, R. R., Kennedy, F. A., & Widener, S. K. (2014). Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), 414-428.

Messner, M. (2016). Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research, 31, 103-111.

Otley, D. (2016). The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, 45-62.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.