Management Accounting: Cost Analysis and Inventory Valuation

Added on 2023-04-04

23 Pages4654 Words63 Views

Management

accounting

accounting

Table of Contents

INTRODUCTION...........................................................................................................................................4

Question 1...............................................................................................................................................4

a. Distinguishing various costs incurred by Smart looks..........................................................................4

b. Presenting different types of cost related to clothing retail firm.........................................................4

Q.2...........................................................................................................................................................6

(A) Calculation of total cost (TC) and unit cost (UC).................................................................................6

(B) Cost data analysis...............................................................................................................................7

Q.3 Inventory valuation...........................................................................................................................8

(1) First-in, first-out.................................................................................................................................8

(2) Last-in, First-out.................................................................................................................................8

(3) Average costs.....................................................................................................................................9

Q.4. Calculation of cost of goods sold under FIFO, LIFO and average cost method...............................10

Question 5.............................................................................................................................................10

A. Identifying critical success factors and performance indicators........................................................10

B............................................................................................................................................................11

1. Identifying the ways through which cost level can be reduced.........................................................11

2. Assessing the manner in which quality can be enhanced..................................................................12

TASK 2........................................................................................................................................................12

Q.6.........................................................................................................................................................12

(A). Meaning of budget..........................................................................................................................12

(B). Purpose or objectives of budgetary planning..................................................................................12

(C) Different methods of budget prearation for Smart Looks................................................................13

Question7..............................................................................................................................................14

a. Sales budget.......................................................................................................................................14

b. Production budget.............................................................................................................................15

c. Raw material budgets........................................................................................................................15

d. Labor budgets....................................................................................................................................15

e. Total overhead budget......................................................................................................................16

Q.8. Preparing cash budget and its analysis..........................................................................................16

INTRODUCTION...........................................................................................................................................4

Question 1...............................................................................................................................................4

a. Distinguishing various costs incurred by Smart looks..........................................................................4

b. Presenting different types of cost related to clothing retail firm.........................................................4

Q.2...........................................................................................................................................................6

(A) Calculation of total cost (TC) and unit cost (UC).................................................................................6

(B) Cost data analysis...............................................................................................................................7

Q.3 Inventory valuation...........................................................................................................................8

(1) First-in, first-out.................................................................................................................................8

(2) Last-in, First-out.................................................................................................................................8

(3) Average costs.....................................................................................................................................9

Q.4. Calculation of cost of goods sold under FIFO, LIFO and average cost method...............................10

Question 5.............................................................................................................................................10

A. Identifying critical success factors and performance indicators........................................................10

B............................................................................................................................................................11

1. Identifying the ways through which cost level can be reduced.........................................................11

2. Assessing the manner in which quality can be enhanced..................................................................12

TASK 2........................................................................................................................................................12

Q.6.........................................................................................................................................................12

(A). Meaning of budget..........................................................................................................................12

(B). Purpose or objectives of budgetary planning..................................................................................12

(C) Different methods of budget prearation for Smart Looks................................................................13

Question7..............................................................................................................................................14

a. Sales budget.......................................................................................................................................14

b. Production budget.............................................................................................................................15

c. Raw material budgets........................................................................................................................15

d. Labor budgets....................................................................................................................................15

e. Total overhead budget......................................................................................................................16

Q.8. Preparing cash budget and its analysis..........................................................................................16

TASK 3........................................................................................................................................................18

Question 9.............................................................................................................................................18

a. Computation of planned margin for March 2017..............................................................................18

b. Calculation of actual profit................................................................................................................18

c. Computation of material and labor variances....................................................................................19

d. Preparing reconciliation profit...........................................................................................................20

Question 10...........................................................................................................................................20

Finding causes of deviations and taking correction actions for improvement.......................................20

CONCLUSION.............................................................................................................................................21

REFERENCES..............................................................................................................................................22

Question 9.............................................................................................................................................18

a. Computation of planned margin for March 2017..............................................................................18

b. Calculation of actual profit................................................................................................................18

c. Computation of material and labor variances....................................................................................19

d. Preparing reconciliation profit...........................................................................................................20

Question 10...........................................................................................................................................20

Finding causes of deviations and taking correction actions for improvement.......................................20

CONCLUSION.............................................................................................................................................21

REFERENCES..............................................................................................................................................22

INTRODUCTION

Management accounting includes several tools and techniques which in turn help in

preparing suitable reports for decision making. In the present times, each business unit lays

emphasis on employing varied tools for getting information about the extent to which each

business unit is performing in a well manner. Moreover, managerial reporting provides deeper

insight to the firm about the area which requires improvement. Thus, management accounting

system aids in the growth and profitability aspect of firm to a great extent. The present report is

based on Smart Looks which is the clothing retailer of UK. It provides customers with high

quality fashion apparel at affordable prices. In this, report will furnish information regarding the

different types of cost associated with the manufacturing of clothes. Further, it will also provide

understanding about the manner in which suitable plan can be developed in monetary terms.

Besides this, report will help in understanding the manner in which variance analysis technique

helps in taking strategic action for the purpose of improvement.

Question 1

a. Distinguishing various costs incurred by Smart looks

Cited case situation presents that Smart Looks has incurred following expenses which fall

in the category of either fixed, semi-variable or variable. Hence, category of cost incurred is

enumerated below:

Material for clothes: Variable cost

Factory rent: Fixed cost

Power of sewing machines: Semi-variable cost

Telephone expenses: semi-variable cost

Office rates: Fixed cost

Delivery drivers: Semi-variable cost

Factory heating: Variable cost

b. Presenting different types of cost related to clothing retail firm

Cost may be defined as a sum of all the expenses which are incurred by firm to

manufacture clothes. In the business organization, firm has to incur several costs which in turn

Management accounting includes several tools and techniques which in turn help in

preparing suitable reports for decision making. In the present times, each business unit lays

emphasis on employing varied tools for getting information about the extent to which each

business unit is performing in a well manner. Moreover, managerial reporting provides deeper

insight to the firm about the area which requires improvement. Thus, management accounting

system aids in the growth and profitability aspect of firm to a great extent. The present report is

based on Smart Looks which is the clothing retailer of UK. It provides customers with high

quality fashion apparel at affordable prices. In this, report will furnish information regarding the

different types of cost associated with the manufacturing of clothes. Further, it will also provide

understanding about the manner in which suitable plan can be developed in monetary terms.

Besides this, report will help in understanding the manner in which variance analysis technique

helps in taking strategic action for the purpose of improvement.

Question 1

a. Distinguishing various costs incurred by Smart looks

Cited case situation presents that Smart Looks has incurred following expenses which fall

in the category of either fixed, semi-variable or variable. Hence, category of cost incurred is

enumerated below:

Material for clothes: Variable cost

Factory rent: Fixed cost

Power of sewing machines: Semi-variable cost

Telephone expenses: semi-variable cost

Office rates: Fixed cost

Delivery drivers: Semi-variable cost

Factory heating: Variable cost

b. Presenting different types of cost related to clothing retail firm

Cost may be defined as a sum of all the expenses which are incurred by firm to

manufacture clothes. In the business organization, firm has to incur several costs which in turn

place direct impact on the cost and profit level. From manufacturing to offering products or

services business entity has to incur several expenses which can be categorized in the following

manner:

Degree of Traceability

Direct expenses: It refers to those which are highly associated with the manufacturing of

product such as clothes. Hence, material, labor cost is the main examples of direct

expenditure.

Indirect expenses: Such category of expenses include selling and distribution,

administration expenses which business unit has to incur for offering high quality

products or services to the customers (Cost Classification, 2017). Hence, indirect

expenses are those which business unit to incur for ensuring the smooth functioning of

business operations.

Changes take place in activity or volume

Fixed cost: Factory rent, insurance, rent etc. comes under the category of fixed cost.

Thus, fixed costs are the one which remains unchanged irrespective the level of output

produced. Hence, per unit cost decreases when production level inclines and vice versa.

Variable cost: Such cost is directly associated with the number of unit produced. Variable

cost increases in line with the production level (Mohanty, 2014). Material, heating

expenses etc. are the main examples of variable cost.

Semi-variable cost: It may be served as those whose specific portion remains fixed to a

specific unit and balance portion considered as variable. Electricity, promotional are the

main examples of semi-variable cost which Smart Looks needs to incur.

Based on product

Direct material: In clothing business, retailer requires raw fabric to make finished

products. Hence, by multiplying the number of units manufacture with rate of per meter

direct material cost can be assessed.

Direct labor: This cost may be defined as wages which are paid by clothing retailer to the

labor on the basis of hours spend by them while manufacturing the apparels.

services business entity has to incur several expenses which can be categorized in the following

manner:

Degree of Traceability

Direct expenses: It refers to those which are highly associated with the manufacturing of

product such as clothes. Hence, material, labor cost is the main examples of direct

expenditure.

Indirect expenses: Such category of expenses include selling and distribution,

administration expenses which business unit has to incur for offering high quality

products or services to the customers (Cost Classification, 2017). Hence, indirect

expenses are those which business unit to incur for ensuring the smooth functioning of

business operations.

Changes take place in activity or volume

Fixed cost: Factory rent, insurance, rent etc. comes under the category of fixed cost.

Thus, fixed costs are the one which remains unchanged irrespective the level of output

produced. Hence, per unit cost decreases when production level inclines and vice versa.

Variable cost: Such cost is directly associated with the number of unit produced. Variable

cost increases in line with the production level (Mohanty, 2014). Material, heating

expenses etc. are the main examples of variable cost.

Semi-variable cost: It may be served as those whose specific portion remains fixed to a

specific unit and balance portion considered as variable. Electricity, promotional are the

main examples of semi-variable cost which Smart Looks needs to incur.

Based on product

Direct material: In clothing business, retailer requires raw fabric to make finished

products. Hence, by multiplying the number of units manufacture with rate of per meter

direct material cost can be assessed.

Direct labor: This cost may be defined as wages which are paid by clothing retailer to the

labor on the basis of hours spend by them while manufacturing the apparels.

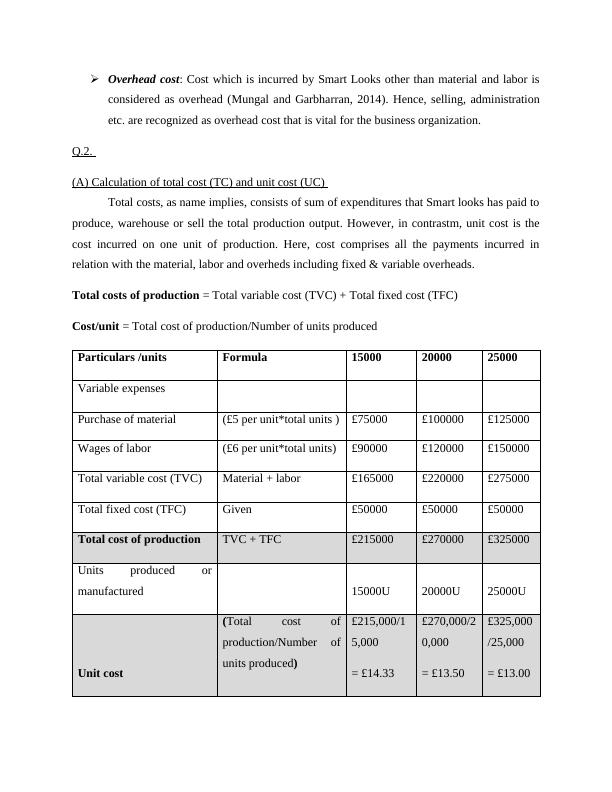

Overhead cost: Cost which is incurred by Smart Looks other than material and labor is

considered as overhead (Mungal and Garbharran, 2014). Hence, selling, administration

etc. are recognized as overhead cost that is vital for the business organization.

Q.2.

(A) Calculation of total cost (TC) and unit cost (UC)

Total costs, as name implies, consists of sum of expenditures that Smart looks has paid to

produce, warehouse or sell the total production output. However, in contrastm, unit cost is the

cost incurred on one unit of production. Here, cost comprises all the payments incurred in

relation with the material, labor and overheds including fixed & variable overheads.

Total costs of production = Total variable cost (TVC) + Total fixed cost (TFC)

Cost/unit = Total cost of production/Number of units produced

Particulars /units Formula 15000 20000 25000

Variable expenses

Purchase of material (£5 per unit*total units ) £75000 £100000 £125000

Wages of labor (£6 per unit*total units) £90000 £120000 £150000

Total variable cost (TVC) Material + labor £165000 £220000 £275000

Total fixed cost (TFC) Given £50000 £50000 £50000

Total cost of production TVC + TFC £215000 £270000 £325000

Units produced or

manufactured 15000U 20000U 25000U

Unit cost

(Total cost of

production/Number of

units produced)

£215,000/1

5,000

= £14.33

£270,000/2

0,000

= £13.50

£325,000

/25,000

= £13.00

considered as overhead (Mungal and Garbharran, 2014). Hence, selling, administration

etc. are recognized as overhead cost that is vital for the business organization.

Q.2.

(A) Calculation of total cost (TC) and unit cost (UC)

Total costs, as name implies, consists of sum of expenditures that Smart looks has paid to

produce, warehouse or sell the total production output. However, in contrastm, unit cost is the

cost incurred on one unit of production. Here, cost comprises all the payments incurred in

relation with the material, labor and overheds including fixed & variable overheads.

Total costs of production = Total variable cost (TVC) + Total fixed cost (TFC)

Cost/unit = Total cost of production/Number of units produced

Particulars /units Formula 15000 20000 25000

Variable expenses

Purchase of material (£5 per unit*total units ) £75000 £100000 £125000

Wages of labor (£6 per unit*total units) £90000 £120000 £150000

Total variable cost (TVC) Material + labor £165000 £220000 £275000

Total fixed cost (TFC) Given £50000 £50000 £50000

Total cost of production TVC + TFC £215000 £270000 £325000

Units produced or

manufactured 15000U 20000U 25000U

Unit cost

(Total cost of

production/Number of

units produced)

£215,000/1

5,000

= £14.33

£270,000/2

0,000

= £13.50

£325,000

/25,000

= £13.00

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Report on Strategic and Competent Policy Frameworklg...

|24

|5145

|60

Management Accounting Assignment tasklg...

|20

|4773

|101

Budget Statements of Smart Looks Limited- Reportlg...

|23

|4865

|64

Managing costs of goods sold under different inventory methodslg...

|19

|5696

|316

MANAGEMENT ACCOUNTING TABLE OF CONTENTSlg...

|27

|4551

|367

MANAGEMENT ACCOUNTING TABLE OF CONTENTS INTRODUCTION 5 Q1.5 a) Classification of cost 5 Q2.7 b) Analysis of inventory 7 Q3. Method 8lg...

|18

|3165

|106