Analysis of Goodwill Calculation Methods: Expander & Target

VerifiedAdded on 2020/06/06

|11

|2994

|218

Report

AI Summary

This report provides a comprehensive analysis of goodwill calculations in the context of a business combination, specifically focusing on the acquisition of Target plc by Expander plc. It explores the impact of different types of consideration, including cash, deferred consideration, and contingent shares, on goodwill valuation. The report delves into the full goodwill method, contrasting it with the proportion of net asset method (partial goodwill). It explains the treatment of non-controlling interests (NCI) under both approaches and provides detailed calculations to illustrate the differences in goodwill amounts. The report highlights the effects of each method on the balance sheet and overall financial reporting, offering valuable insights into the practical application of IFRS 3 in accounting for business combinations.

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

a) Affects of nature of consideration on the calculation of goodwill..........................................1

b) Discussion of the concept full goodwill.................................................................................3

c) Effect of selecting the full goodwill method rather than the proportion of net asset method.3

d) Appropriate accounting policy to adopt in respect of measuring non-controlling interest at

acquisition...................................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

.........................................................................................................................................................7

INTRODUCTION...........................................................................................................................1

a) Affects of nature of consideration on the calculation of goodwill..........................................1

b) Discussion of the concept full goodwill.................................................................................3

c) Effect of selecting the full goodwill method rather than the proportion of net asset method.3

d) Appropriate accounting policy to adopt in respect of measuring non-controlling interest at

acquisition...................................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

.........................................................................................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

IFRS 3 provides informations to improve the relevance, reliability and comparability of

data provided for business combinations like acquisitions and mergers. It also describes about

their effects on calculations of goodwill. It regulates and frames the principles on the recognition

and measurement of assets and liabilities which is acquired by parent company.

In this assignment, the present scenario's indicates that there are two companies Expander

plc and Target plc, in which Expander plc is going to acquire 70% stake in Target plc. Hence,

through this assignment, calculation of goodwill both measuring non-controlling interest and full

goodwill methods will be done.

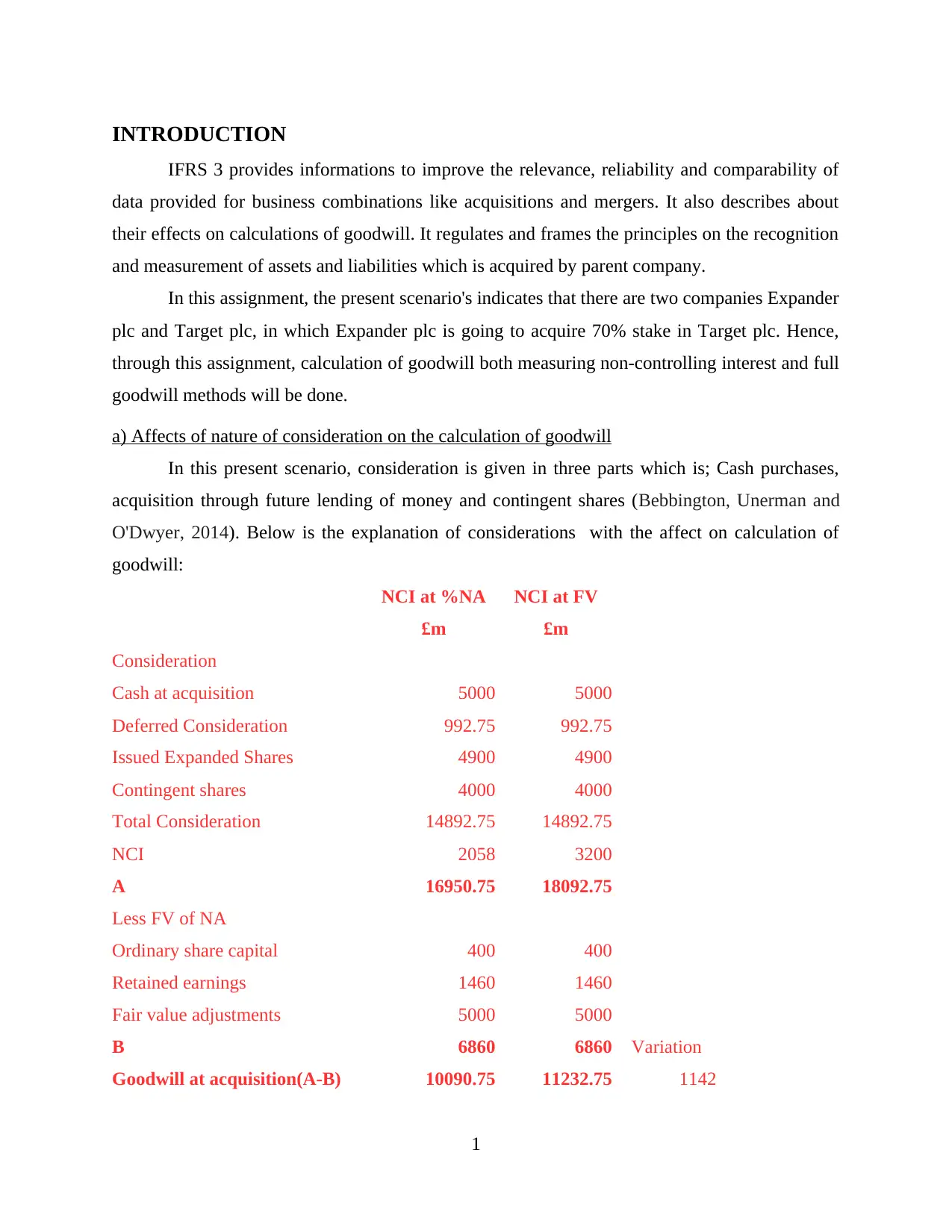

a) Affects of nature of consideration on the calculation of goodwill

In this present scenario, consideration is given in three parts which is; Cash purchases,

acquisition through future lending of money and contingent shares (Bebbington, Unerman and

O'Dwyer, 2014). Below is the explanation of considerations with the affect on calculation of

goodwill:

NCI at %NA NCI at FV

£m £m

Consideration

Cash at acquisition 5000 5000

Deferred Consideration 992.75 992.75

Issued Expanded Shares 4900 4900

Contingent shares 4000 4000

Total Consideration 14892.75 14892.75

NCI 2058 3200

A 16950.75 18092.75

Less FV of NA

Ordinary share capital 400 400

Retained earnings 1460 1460

Fair value adjustments 5000 5000

B 6860 6860 Variation

Goodwill at acquisition(A-B) 10090.75 11232.75 1142

1

IFRS 3 provides informations to improve the relevance, reliability and comparability of

data provided for business combinations like acquisitions and mergers. It also describes about

their effects on calculations of goodwill. It regulates and frames the principles on the recognition

and measurement of assets and liabilities which is acquired by parent company.

In this assignment, the present scenario's indicates that there are two companies Expander

plc and Target plc, in which Expander plc is going to acquire 70% stake in Target plc. Hence,

through this assignment, calculation of goodwill both measuring non-controlling interest and full

goodwill methods will be done.

a) Affects of nature of consideration on the calculation of goodwill

In this present scenario, consideration is given in three parts which is; Cash purchases,

acquisition through future lending of money and contingent shares (Bebbington, Unerman and

O'Dwyer, 2014). Below is the explanation of considerations with the affect on calculation of

goodwill:

NCI at %NA NCI at FV

£m £m

Consideration

Cash at acquisition 5000 5000

Deferred Consideration 992.75 992.75

Issued Expanded Shares 4900 4900

Contingent shares 4000 4000

Total Consideration 14892.75 14892.75

NCI 2058 3200

A 16950.75 18092.75

Less FV of NA

Ordinary share capital 400 400

Retained earnings 1460 1460

Fair value adjustments 5000 5000

B 6860 6860 Variation

Goodwill at acquisition(A-B) 10090.75 11232.75 1142

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash at acquisition: In the above calculation of total purchasing cost of 70% stake of

Target plc, cash purchases indicates instant payment of £5000 million at the time of acquiring

stakes. This consideration doesn't carry any future value or discounted value, as there's

immediate payment done by Expander plc at the time of acquiring such assets.

Issued Expander Shares: Expander plc has issued 1 shares for every 2 shares acquired

by the company. So, it has acquired 280 million shares of Target plc having value of £1 per

share. In this method, Expander has acquired the 70% stake in exchange of 140 million (280

million/2) shares having face value £35 per share. The total value of this share is around 140

million shares * £35 per share = £4900 million.

Deferred consideration for two years: In this consideration, Expander plc has promise

Target plc to pay £1100 after two years. But after discounting this amount @5% for two years,

the actual identified is £992.75 million. Deferred consideration should be measured at fair value

at the date of the acquisition, like for example it is a promise to pay an agreed sum on a

predetermined date in the future taking into account the time value of money with given

formulae:

Future value of Deferred Consideration = £1100 * (1 - 0.05)2 = £1100 * (.95)2 = £992.75

Discounting of cash payment is done to know accurate value of the investment. Because

according IFRS 3, present value should be included while calculating purchasing cost of

acquisition (IFRS 3 and IAS 27, 2009).

Contingent Shares: Contingent consideration should be measured at reasonable prices

during practical combinations and kept in mind in determining goodwill (Chaney, Faccio and

Parsley, 2011). If, after the acquisition, the number of contingency consideration changes as a

result of meeting an earnings target. The contingent shares of amount £4000 million is given.

These changes is dependent on whether the additional consideration is described as an equity or

an asset or liability.

Below is the calculation of Goodwill:

Partial Goodwill Calculation:

Amount £ Million

Cash at acquisition 5000

Deferred Consideration 992.75

2

Target plc, cash purchases indicates instant payment of £5000 million at the time of acquiring

stakes. This consideration doesn't carry any future value or discounted value, as there's

immediate payment done by Expander plc at the time of acquiring such assets.

Issued Expander Shares: Expander plc has issued 1 shares for every 2 shares acquired

by the company. So, it has acquired 280 million shares of Target plc having value of £1 per

share. In this method, Expander has acquired the 70% stake in exchange of 140 million (280

million/2) shares having face value £35 per share. The total value of this share is around 140

million shares * £35 per share = £4900 million.

Deferred consideration for two years: In this consideration, Expander plc has promise

Target plc to pay £1100 after two years. But after discounting this amount @5% for two years,

the actual identified is £992.75 million. Deferred consideration should be measured at fair value

at the date of the acquisition, like for example it is a promise to pay an agreed sum on a

predetermined date in the future taking into account the time value of money with given

formulae:

Future value of Deferred Consideration = £1100 * (1 - 0.05)2 = £1100 * (.95)2 = £992.75

Discounting of cash payment is done to know accurate value of the investment. Because

according IFRS 3, present value should be included while calculating purchasing cost of

acquisition (IFRS 3 and IAS 27, 2009).

Contingent Shares: Contingent consideration should be measured at reasonable prices

during practical combinations and kept in mind in determining goodwill (Chaney, Faccio and

Parsley, 2011). If, after the acquisition, the number of contingency consideration changes as a

result of meeting an earnings target. The contingent shares of amount £4000 million is given.

These changes is dependent on whether the additional consideration is described as an equity or

an asset or liability.

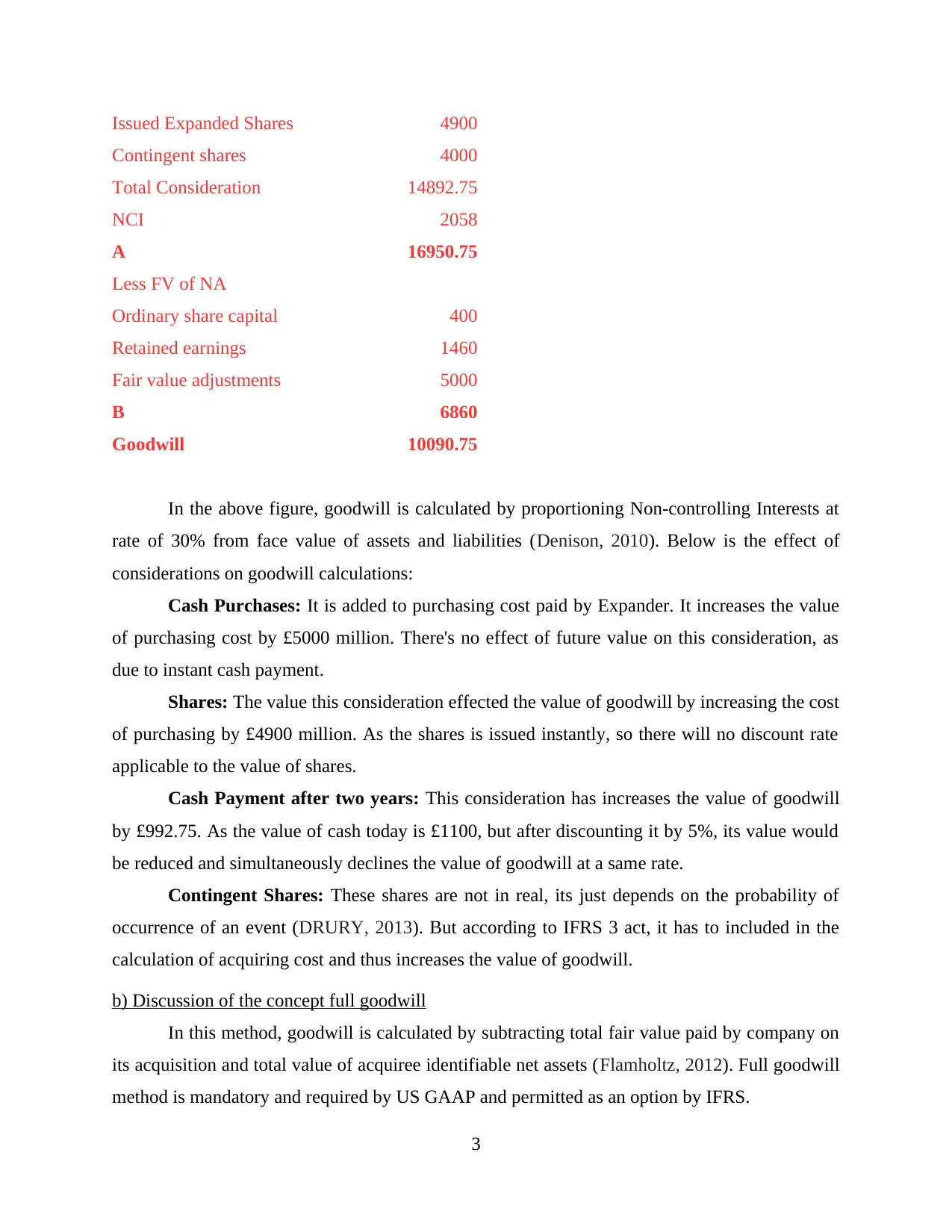

Below is the calculation of Goodwill:

Partial Goodwill Calculation:

Amount £ Million

Cash at acquisition 5000

Deferred Consideration 992.75

2

Issued Expanded Shares 4900

Contingent shares 4000

Total Consideration 14892.75

NCI 2058

A 16950.75

Less FV of NA

Ordinary share capital 400

Retained earnings 1460

Fair value adjustments 5000

B 6860

Goodwill 10090.75

In the above figure, goodwill is calculated by proportioning Non-controlling Interests at

rate of 30% from face value of assets and liabilities (Denison, 2010). Below is the effect of

considerations on goodwill calculations:

Cash Purchases: It is added to purchasing cost paid by Expander. It increases the value

of purchasing cost by £5000 million. There's no effect of future value on this consideration, as

due to instant cash payment.

Shares: The value this consideration effected the value of goodwill by increasing the cost

of purchasing by £4900 million. As the shares is issued instantly, so there will no discount rate

applicable to the value of shares.

Cash Payment after two years: This consideration has increases the value of goodwill

by £992.75. As the value of cash today is £1100, but after discounting it by 5%, its value would

be reduced and simultaneously declines the value of goodwill at a same rate.

Contingent Shares: These shares are not in real, its just depends on the probability of

occurrence of an event (DRURY, 2013). But according to IFRS 3 act, it has to included in the

calculation of acquiring cost and thus increases the value of goodwill.

b) Discussion of the concept full goodwill

In this method, goodwill is calculated by subtracting total fair value paid by company on

its acquisition and total value of acquiree identifiable net assets (Flamholtz, 2012). Full goodwill

method is mandatory and required by US GAAP and permitted as an option by IFRS.

3

Contingent shares 4000

Total Consideration 14892.75

NCI 2058

A 16950.75

Less FV of NA

Ordinary share capital 400

Retained earnings 1460

Fair value adjustments 5000

B 6860

Goodwill 10090.75

In the above figure, goodwill is calculated by proportioning Non-controlling Interests at

rate of 30% from face value of assets and liabilities (Denison, 2010). Below is the effect of

considerations on goodwill calculations:

Cash Purchases: It is added to purchasing cost paid by Expander. It increases the value

of purchasing cost by £5000 million. There's no effect of future value on this consideration, as

due to instant cash payment.

Shares: The value this consideration effected the value of goodwill by increasing the cost

of purchasing by £4900 million. As the shares is issued instantly, so there will no discount rate

applicable to the value of shares.

Cash Payment after two years: This consideration has increases the value of goodwill

by £992.75. As the value of cash today is £1100, but after discounting it by 5%, its value would

be reduced and simultaneously declines the value of goodwill at a same rate.

Contingent Shares: These shares are not in real, its just depends on the probability of

occurrence of an event (DRURY, 2013). But according to IFRS 3 act, it has to included in the

calculation of acquiring cost and thus increases the value of goodwill.

b) Discussion of the concept full goodwill

In this method, goodwill is calculated by subtracting total fair value paid by company on

its acquisition and total value of acquiree identifiable net assets (Flamholtz, 2012). Full goodwill

method is mandatory and required by US GAAP and permitted as an option by IFRS.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

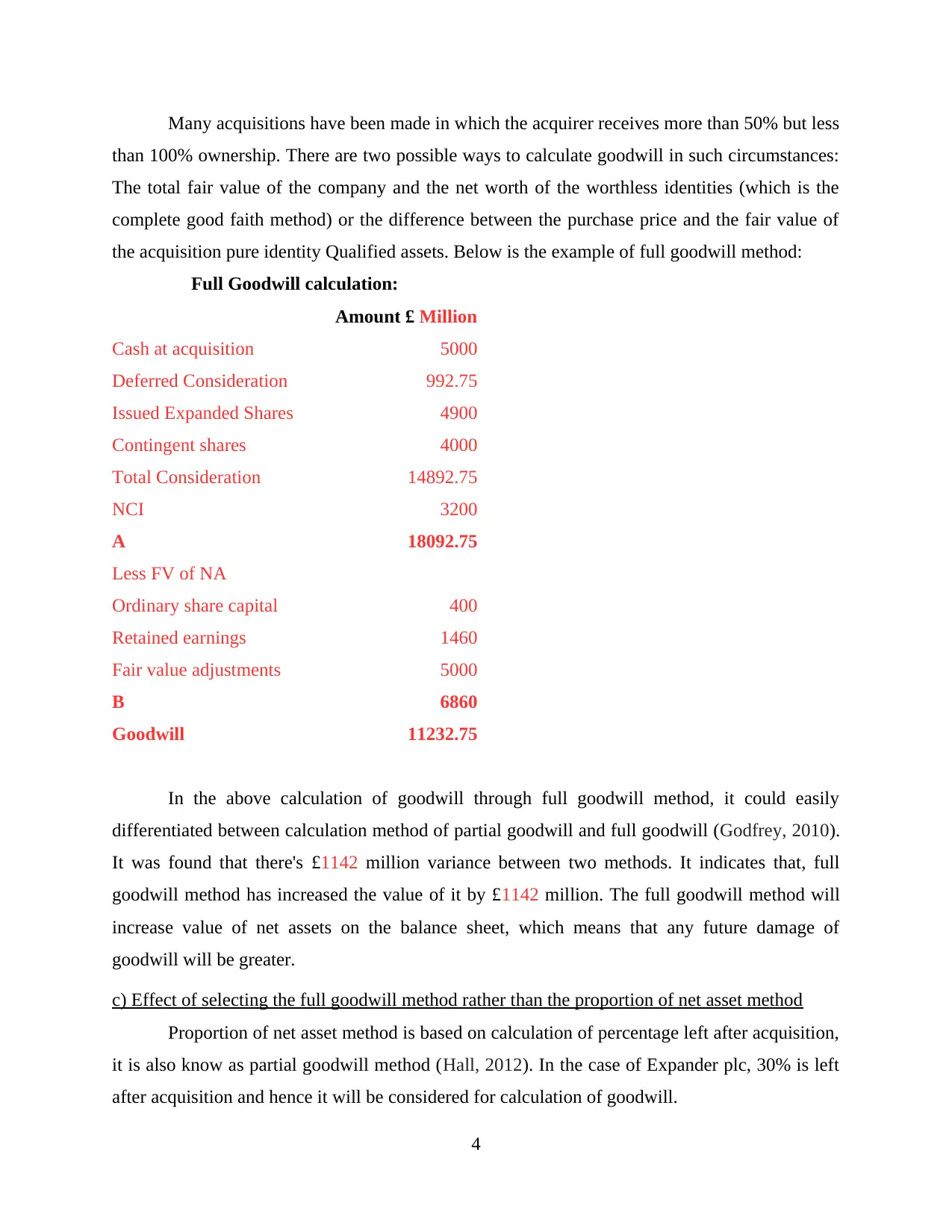

Many acquisitions have been made in which the acquirer receives more than 50% but less

than 100% ownership. There are two possible ways to calculate goodwill in such circumstances:

The total fair value of the company and the net worth of the worthless identities (which is the

complete good faith method) or the difference between the purchase price and the fair value of

the acquisition pure identity Qualified assets. Below is the example of full goodwill method:

Full Goodwill calculation:

Amount £ Million

Cash at acquisition 5000

Deferred Consideration 992.75

Issued Expanded Shares 4900

Contingent shares 4000

Total Consideration 14892.75

NCI 3200

A 18092.75

Less FV of NA

Ordinary share capital 400

Retained earnings 1460

Fair value adjustments 5000

B 6860

Goodwill 11232.75

In the above calculation of goodwill through full goodwill method, it could easily

differentiated between calculation method of partial goodwill and full goodwill (Godfrey, 2010).

It was found that there's £1142 million variance between two methods. It indicates that, full

goodwill method has increased the value of it by £1142 million. The full goodwill method will

increase value of net assets on the balance sheet, which means that any future damage of

goodwill will be greater.

c) Effect of selecting the full goodwill method rather than the proportion of net asset method

Proportion of net asset method is based on calculation of percentage left after acquisition,

it is also know as partial goodwill method (Hall, 2012). In the case of Expander plc, 30% is left

after acquisition and hence it will be considered for calculation of goodwill.

4

than 100% ownership. There are two possible ways to calculate goodwill in such circumstances:

The total fair value of the company and the net worth of the worthless identities (which is the

complete good faith method) or the difference between the purchase price and the fair value of

the acquisition pure identity Qualified assets. Below is the example of full goodwill method:

Full Goodwill calculation:

Amount £ Million

Cash at acquisition 5000

Deferred Consideration 992.75

Issued Expanded Shares 4900

Contingent shares 4000

Total Consideration 14892.75

NCI 3200

A 18092.75

Less FV of NA

Ordinary share capital 400

Retained earnings 1460

Fair value adjustments 5000

B 6860

Goodwill 11232.75

In the above calculation of goodwill through full goodwill method, it could easily

differentiated between calculation method of partial goodwill and full goodwill (Godfrey, 2010).

It was found that there's £1142 million variance between two methods. It indicates that, full

goodwill method has increased the value of it by £1142 million. The full goodwill method will

increase value of net assets on the balance sheet, which means that any future damage of

goodwill will be greater.

c) Effect of selecting the full goodwill method rather than the proportion of net asset method

Proportion of net asset method is based on calculation of percentage left after acquisition,

it is also know as partial goodwill method (Hall, 2012). In the case of Expander plc, 30% is left

after acquisition and hence it will be considered for calculation of goodwill.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

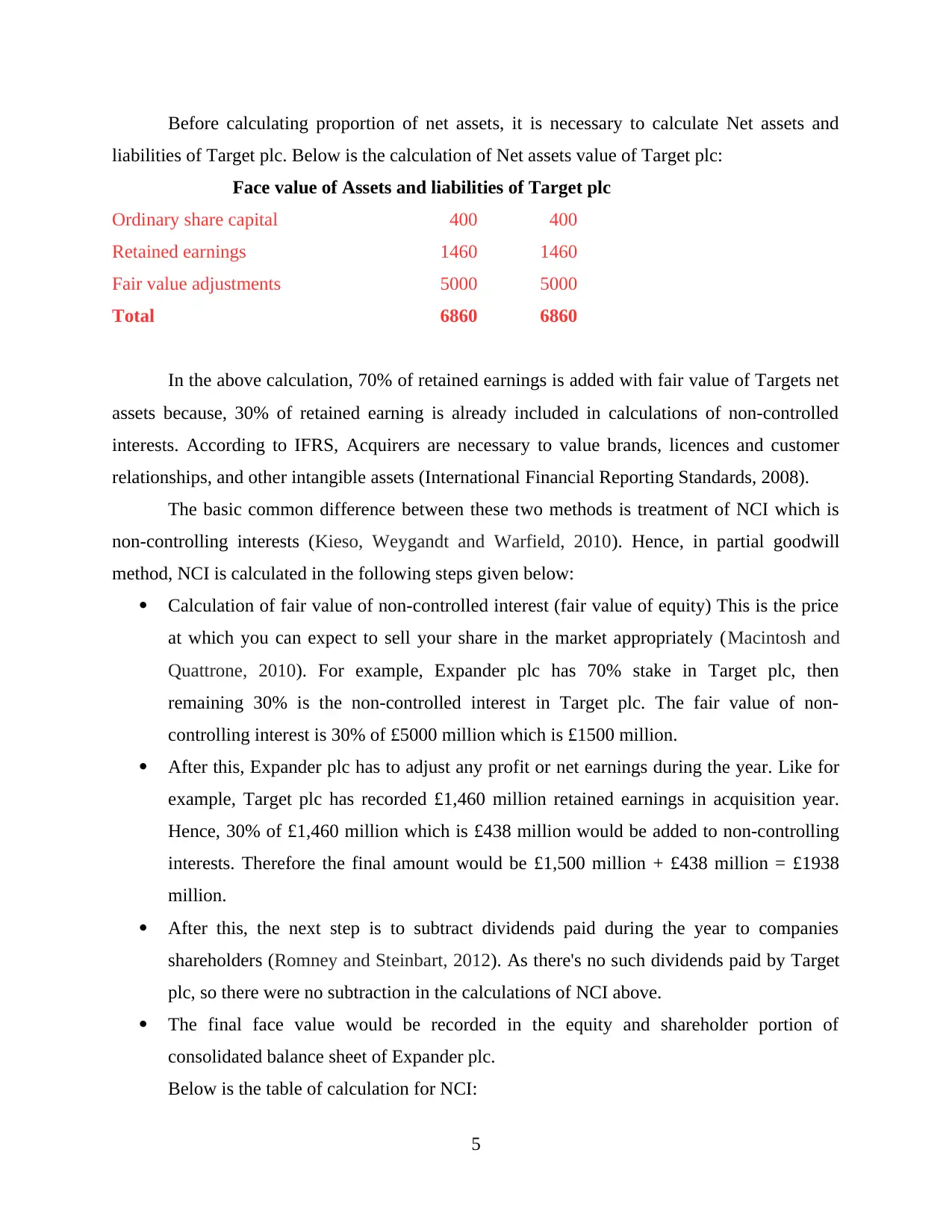

Before calculating proportion of net assets, it is necessary to calculate Net assets and

liabilities of Target plc. Below is the calculation of Net assets value of Target plc:

Face value of Assets and liabilities of Target plc

Ordinary share capital 400 400

Retained earnings 1460 1460

Fair value adjustments 5000 5000

Total 6860 6860

In the above calculation, 70% of retained earnings is added with fair value of Targets net

assets because, 30% of retained earning is already included in calculations of non-controlled

interests. According to IFRS, Acquirers are necessary to value brands, licences and customer

relationships, and other intangible assets (International Financial Reporting Standards, 2008).

The basic common difference between these two methods is treatment of NCI which is

non-controlling interests (Kieso, Weygandt and Warfield, 2010). Hence, in partial goodwill

method, NCI is calculated in the following steps given below:

Calculation of fair value of non-controlled interest (fair value of equity) This is the price

at which you can expect to sell your share in the market appropriately (Macintosh and

Quattrone, 2010). For example, Expander plc has 70% stake in Target plc, then

remaining 30% is the non-controlled interest in Target plc. The fair value of non-

controlling interest is 30% of £5000 million which is £1500 million.

After this, Expander plc has to adjust any profit or net earnings during the year. Like for

example, Target plc has recorded £1,460 million retained earnings in acquisition year.

Hence, 30% of £1,460 million which is £438 million would be added to non-controlling

interests. Therefore the final amount would be £1,500 million + £438 million = £1938

million.

After this, the next step is to subtract dividends paid during the year to companies

shareholders (Romney and Steinbart, 2012). As there's no such dividends paid by Target

plc, so there were no subtraction in the calculations of NCI above.

The final face value would be recorded in the equity and shareholder portion of

consolidated balance sheet of Expander plc.

Below is the table of calculation for NCI:

5

liabilities of Target plc. Below is the calculation of Net assets value of Target plc:

Face value of Assets and liabilities of Target plc

Ordinary share capital 400 400

Retained earnings 1460 1460

Fair value adjustments 5000 5000

Total 6860 6860

In the above calculation, 70% of retained earnings is added with fair value of Targets net

assets because, 30% of retained earning is already included in calculations of non-controlled

interests. According to IFRS, Acquirers are necessary to value brands, licences and customer

relationships, and other intangible assets (International Financial Reporting Standards, 2008).

The basic common difference between these two methods is treatment of NCI which is

non-controlling interests (Kieso, Weygandt and Warfield, 2010). Hence, in partial goodwill

method, NCI is calculated in the following steps given below:

Calculation of fair value of non-controlled interest (fair value of equity) This is the price

at which you can expect to sell your share in the market appropriately (Macintosh and

Quattrone, 2010). For example, Expander plc has 70% stake in Target plc, then

remaining 30% is the non-controlled interest in Target plc. The fair value of non-

controlling interest is 30% of £5000 million which is £1500 million.

After this, Expander plc has to adjust any profit or net earnings during the year. Like for

example, Target plc has recorded £1,460 million retained earnings in acquisition year.

Hence, 30% of £1,460 million which is £438 million would be added to non-controlling

interests. Therefore the final amount would be £1,500 million + £438 million = £1938

million.

After this, the next step is to subtract dividends paid during the year to companies

shareholders (Romney and Steinbart, 2012). As there's no such dividends paid by Target

plc, so there were no subtraction in the calculations of NCI above.

The final face value would be recorded in the equity and shareholder portion of

consolidated balance sheet of Expander plc.

Below is the table of calculation for NCI:

5

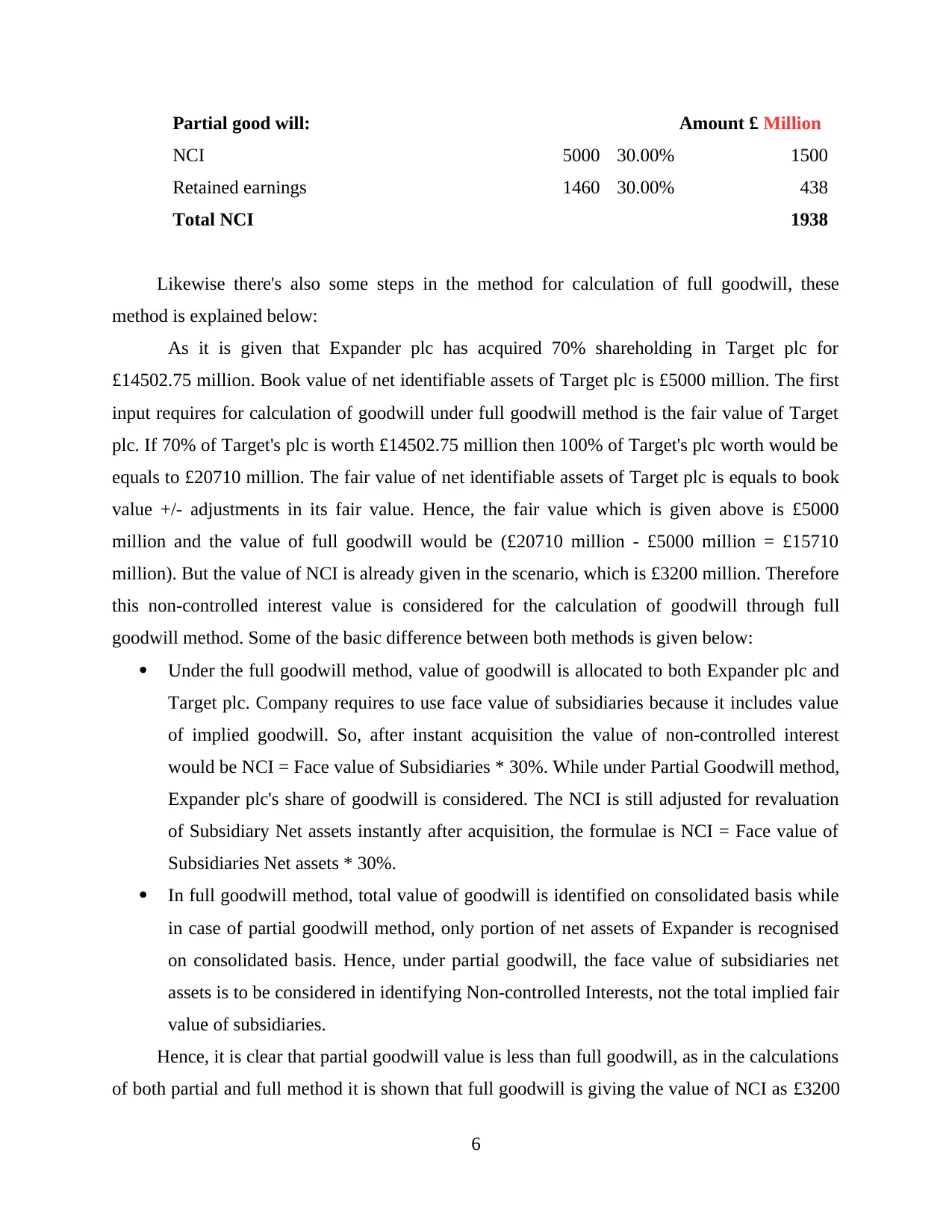

Partial good will: Amount £ Million

NCI 5000 30.00% 1500

Retained earnings 1460 30.00% 438

Total NCI 1938

Likewise there's also some steps in the method for calculation of full goodwill, these

method is explained below:

As it is given that Expander plc has acquired 70% shareholding in Target plc for

£14502.75 million. Book value of net identifiable assets of Target plc is £5000 million. The first

input requires for calculation of goodwill under full goodwill method is the fair value of Target

plc. If 70% of Target's plc is worth £14502.75 million then 100% of Target's plc worth would be

equals to £20710 million. The fair value of net identifiable assets of Target plc is equals to book

value +/- adjustments in its fair value. Hence, the fair value which is given above is £5000

million and the value of full goodwill would be (£20710 million - £5000 million = £15710

million). But the value of NCI is already given in the scenario, which is £3200 million. Therefore

this non-controlled interest value is considered for the calculation of goodwill through full

goodwill method. Some of the basic difference between both methods is given below:

Under the full goodwill method, value of goodwill is allocated to both Expander plc and

Target plc. Company requires to use face value of subsidiaries because it includes value

of implied goodwill. So, after instant acquisition the value of non-controlled interest

would be NCI = Face value of Subsidiaries * 30%. While under Partial Goodwill method,

Expander plc's share of goodwill is considered. The NCI is still adjusted for revaluation

of Subsidiary Net assets instantly after acquisition, the formulae is NCI = Face value of

Subsidiaries Net assets * 30%.

In full goodwill method, total value of goodwill is identified on consolidated basis while

in case of partial goodwill method, only portion of net assets of Expander is recognised

on consolidated basis. Hence, under partial goodwill, the face value of subsidiaries net

assets is to be considered in identifying Non-controlled Interests, not the total implied fair

value of subsidiaries.

Hence, it is clear that partial goodwill value is less than full goodwill, as in the calculations

of both partial and full method it is shown that full goodwill is giving the value of NCI as £3200

6

NCI 5000 30.00% 1500

Retained earnings 1460 30.00% 438

Total NCI 1938

Likewise there's also some steps in the method for calculation of full goodwill, these

method is explained below:

As it is given that Expander plc has acquired 70% shareholding in Target plc for

£14502.75 million. Book value of net identifiable assets of Target plc is £5000 million. The first

input requires for calculation of goodwill under full goodwill method is the fair value of Target

plc. If 70% of Target's plc is worth £14502.75 million then 100% of Target's plc worth would be

equals to £20710 million. The fair value of net identifiable assets of Target plc is equals to book

value +/- adjustments in its fair value. Hence, the fair value which is given above is £5000

million and the value of full goodwill would be (£20710 million - £5000 million = £15710

million). But the value of NCI is already given in the scenario, which is £3200 million. Therefore

this non-controlled interest value is considered for the calculation of goodwill through full

goodwill method. Some of the basic difference between both methods is given below:

Under the full goodwill method, value of goodwill is allocated to both Expander plc and

Target plc. Company requires to use face value of subsidiaries because it includes value

of implied goodwill. So, after instant acquisition the value of non-controlled interest

would be NCI = Face value of Subsidiaries * 30%. While under Partial Goodwill method,

Expander plc's share of goodwill is considered. The NCI is still adjusted for revaluation

of Subsidiary Net assets instantly after acquisition, the formulae is NCI = Face value of

Subsidiaries Net assets * 30%.

In full goodwill method, total value of goodwill is identified on consolidated basis while

in case of partial goodwill method, only portion of net assets of Expander is recognised

on consolidated basis. Hence, under partial goodwill, the face value of subsidiaries net

assets is to be considered in identifying Non-controlled Interests, not the total implied fair

value of subsidiaries.

Hence, it is clear that partial goodwill value is less than full goodwill, as in the calculations

of both partial and full method it is shown that full goodwill is giving the value of NCI as £3200

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

million. As this would be calculated on the basis of those factors which are not mention in Assets

and liabilities side of Target plc, so it is mandatory to consider full goodwill methods for

calculating goodwill of the company.

d) Appropriate accounting policy to adopt in respect of measuring non-controlling interest at

acquisition

There are basically two ways to identify goodwill of the company, in a business

combination, Expander could calculate goodwill either by partial or full goodwill method:

Partial goodwill method: In this method, Expander would measure value of assets and

liabilities, it could only recognize these value of goodwill with controlling interest in Target plc.

Full goodwill method: This method is fundamentally same as partial method of

calculating goodwill, but there's mainly one difference which is non-controlling interests is

included in goodwill.

Both methods are advisable and the company might choose either methods depends on

different circumstances to keep consistency for every acquisition. It is also recommended to the

company, that it should calculate NCI by considering full goodwill method, because this method

recognises and allocated goodwill among Expander and Target plc both at a time.

The purchasing cost is simply based its value on market prices of the share which it

doesn't hold. When the market is not active, then it is suggested to Expander plc that it should

calculate its purchasing cost of a company to measure fair value through using other valuation

techniques such as:

A measurement of market that contains multiple of market for traded companies and

which is comparable to Target plc.

Valuation of income on the basis of future value analyses through discounted cash flow

analyses.

CONCLUSION

On the basis of all calculations and observations it could be concluded that IFRS 3 is

necessary to be considered, as it provides informations to improve the relevance, reliability and

comparability of data provided for business combinations like acquisitions and mergers. It also

describes about their effects on calculations of goodwill. There are basically two ways to identify

goodwill of the company in a business combination which is partial or full goodwill method. On

7

and liabilities side of Target plc, so it is mandatory to consider full goodwill methods for

calculating goodwill of the company.

d) Appropriate accounting policy to adopt in respect of measuring non-controlling interest at

acquisition

There are basically two ways to identify goodwill of the company, in a business

combination, Expander could calculate goodwill either by partial or full goodwill method:

Partial goodwill method: In this method, Expander would measure value of assets and

liabilities, it could only recognize these value of goodwill with controlling interest in Target plc.

Full goodwill method: This method is fundamentally same as partial method of

calculating goodwill, but there's mainly one difference which is non-controlling interests is

included in goodwill.

Both methods are advisable and the company might choose either methods depends on

different circumstances to keep consistency for every acquisition. It is also recommended to the

company, that it should calculate NCI by considering full goodwill method, because this method

recognises and allocated goodwill among Expander and Target plc both at a time.

The purchasing cost is simply based its value on market prices of the share which it

doesn't hold. When the market is not active, then it is suggested to Expander plc that it should

calculate its purchasing cost of a company to measure fair value through using other valuation

techniques such as:

A measurement of market that contains multiple of market for traded companies and

which is comparable to Target plc.

Valuation of income on the basis of future value analyses through discounted cash flow

analyses.

CONCLUSION

On the basis of all calculations and observations it could be concluded that IFRS 3 is

necessary to be considered, as it provides informations to improve the relevance, reliability and

comparability of data provided for business combinations like acquisitions and mergers. It also

describes about their effects on calculations of goodwill. There are basically two ways to identify

goodwill of the company in a business combination which is partial or full goodwill method. On

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the basis of all calculations and comparative analysis between these two methods, it is clear that

full goodwill method is good choice for Expander but at the same time company should consider

other alternative method also.

8

full goodwill method is good choice for Expander but at the same time company should consider

other alternative method also.

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.