Accounting & Financial Management - Desklib

VerifiedAdded on 2023/06/10

|12

|2413

|198

AI Summary

This article discusses the evaluation of projects using NPV and IRR, and their limitations. It includes a detailed analysis of two projects, their discount rates, cash flows, payback periods, and profitability index. The article also highlights the advantages and disadvantages of using IRR and NPV, and their suitability for different types of projects. The subject is Accounting & Financial Management, and the article is relevant for students pursuing courses in this field.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING & FINANCIAL MANAGEMENT

Accounting & Financial Management

Name of Student:

Name of University:

Author’s Note:

Accounting & Financial Management

Name of Student:

Name of University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ACCOUNTING & FINANCIAL MANAGEMENT

Table of Contents

Question 1........................................................................................................................................2

Answer to part a...............................................................................................................................2

Answer to part b...............................................................................................................................2

Answer to part c...............................................................................................................................3

Answer to part d...............................................................................................................................4

Answer to part e...............................................................................................................................5

Question 2........................................................................................................................................5

References......................................................................................................................................10

Table of Contents

Question 1........................................................................................................................................2

Answer to part a...............................................................................................................................2

Answer to part b...............................................................................................................................2

Answer to part c...............................................................................................................................3

Answer to part d...............................................................................................................................4

Answer to part e...............................................................................................................................5

Question 2........................................................................................................................................5

References......................................................................................................................................10

2ACCOUNTING & FINANCIAL MANAGEMENT

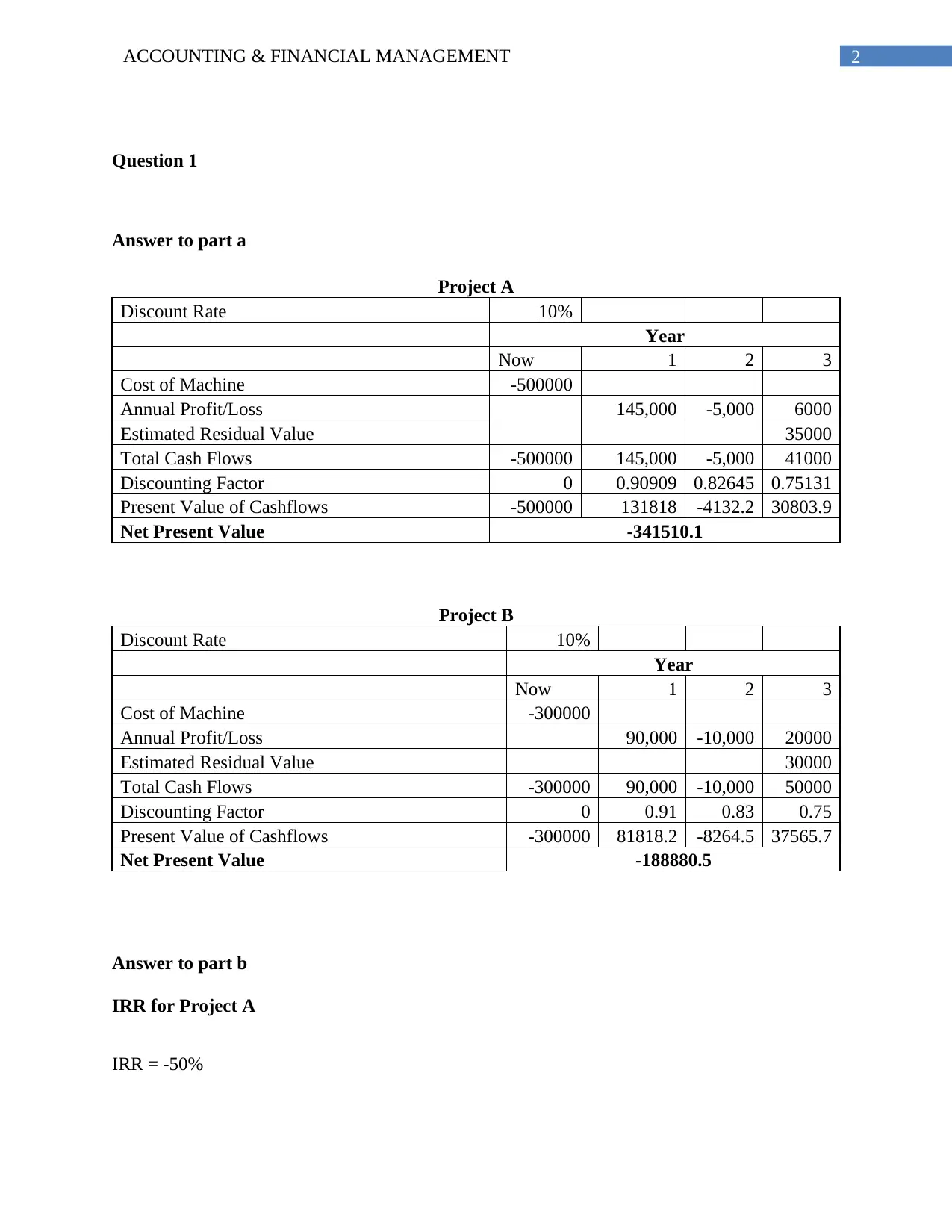

Question 1

Answer to part a

Project A

Discount Rate 10%

Year

Now 1 2 3

Cost of Machine -500000

Annual Profit/Loss 145,000 -5,000 6000

Estimated Residual Value 35000

Total Cash Flows -500000 145,000 -5,000 41000

Discounting Factor 0 0.90909 0.82645 0.75131

Present Value of Cashflows -500000 131818 -4132.2 30803.9

Net Present Value -341510.1

Project B

Discount Rate 10%

Year

Now 1 2 3

Cost of Machine -300000

Annual Profit/Loss 90,000 -10,000 20000

Estimated Residual Value 30000

Total Cash Flows -300000 90,000 -10,000 50000

Discounting Factor 0 0.91 0.83 0.75

Present Value of Cashflows -300000 81818.2 -8264.5 37565.7

Net Present Value -188880.5

Answer to part b

IRR for Project A

IRR = -50%

Question 1

Answer to part a

Project A

Discount Rate 10%

Year

Now 1 2 3

Cost of Machine -500000

Annual Profit/Loss 145,000 -5,000 6000

Estimated Residual Value 35000

Total Cash Flows -500000 145,000 -5,000 41000

Discounting Factor 0 0.90909 0.82645 0.75131

Present Value of Cashflows -500000 131818 -4132.2 30803.9

Net Present Value -341510.1

Project B

Discount Rate 10%

Year

Now 1 2 3

Cost of Machine -300000

Annual Profit/Loss 90,000 -10,000 20000

Estimated Residual Value 30000

Total Cash Flows -300000 90,000 -10,000 50000

Discounting Factor 0 0.91 0.83 0.75

Present Value of Cashflows -300000 81818.2 -8264.5 37565.7

Net Present Value -188880.5

Answer to part b

IRR for Project A

IRR = -50%

3ACCOUNTING & FINANCIAL MANAGEMENT

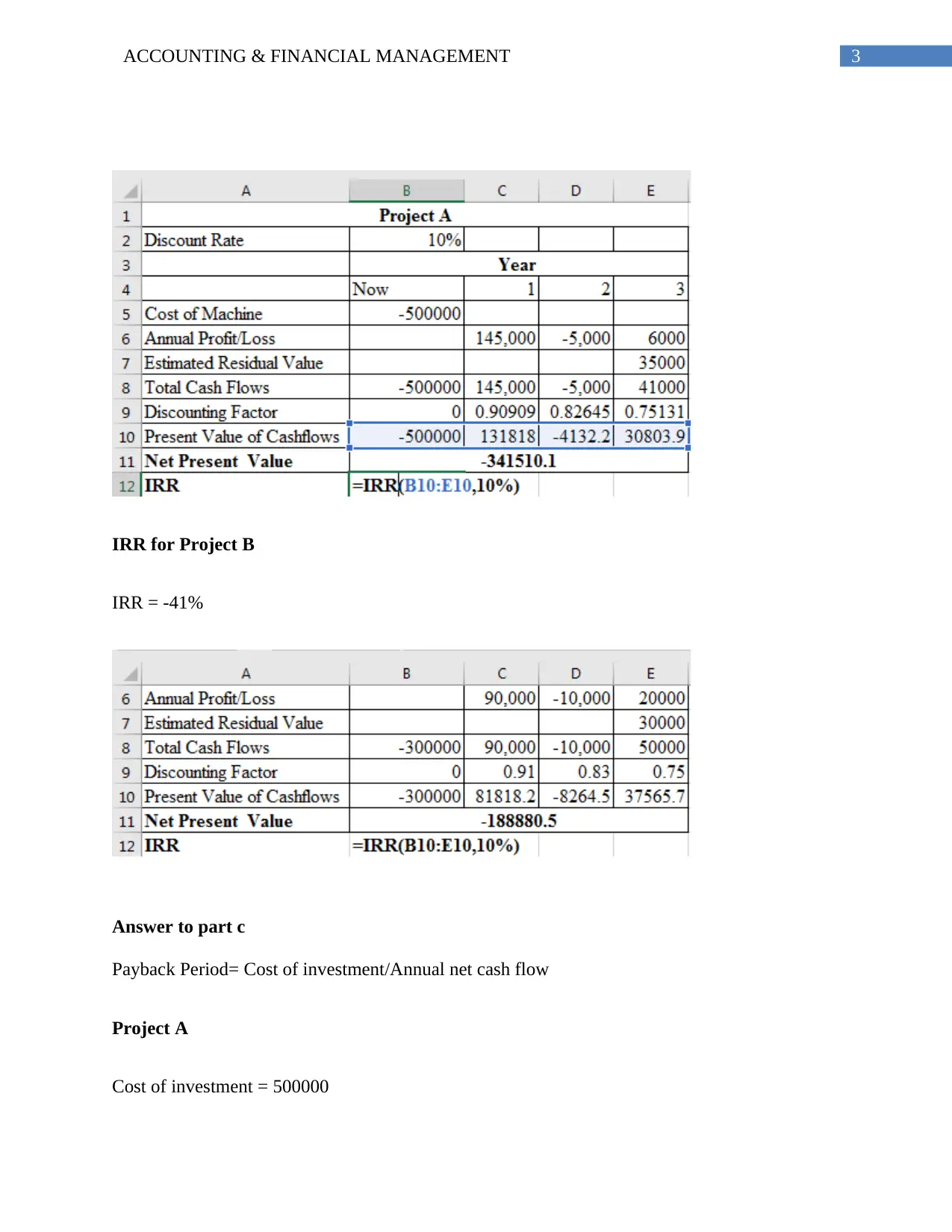

IRR for Project B

IRR = -41%

Answer to part c

Payback Period= Cost of investment/Annual net cash flow

Project A

Cost of investment = 500000

IRR for Project B

IRR = -41%

Answer to part c

Payback Period= Cost of investment/Annual net cash flow

Project A

Cost of investment = 500000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ACCOUNTING & FINANCIAL MANAGEMENT

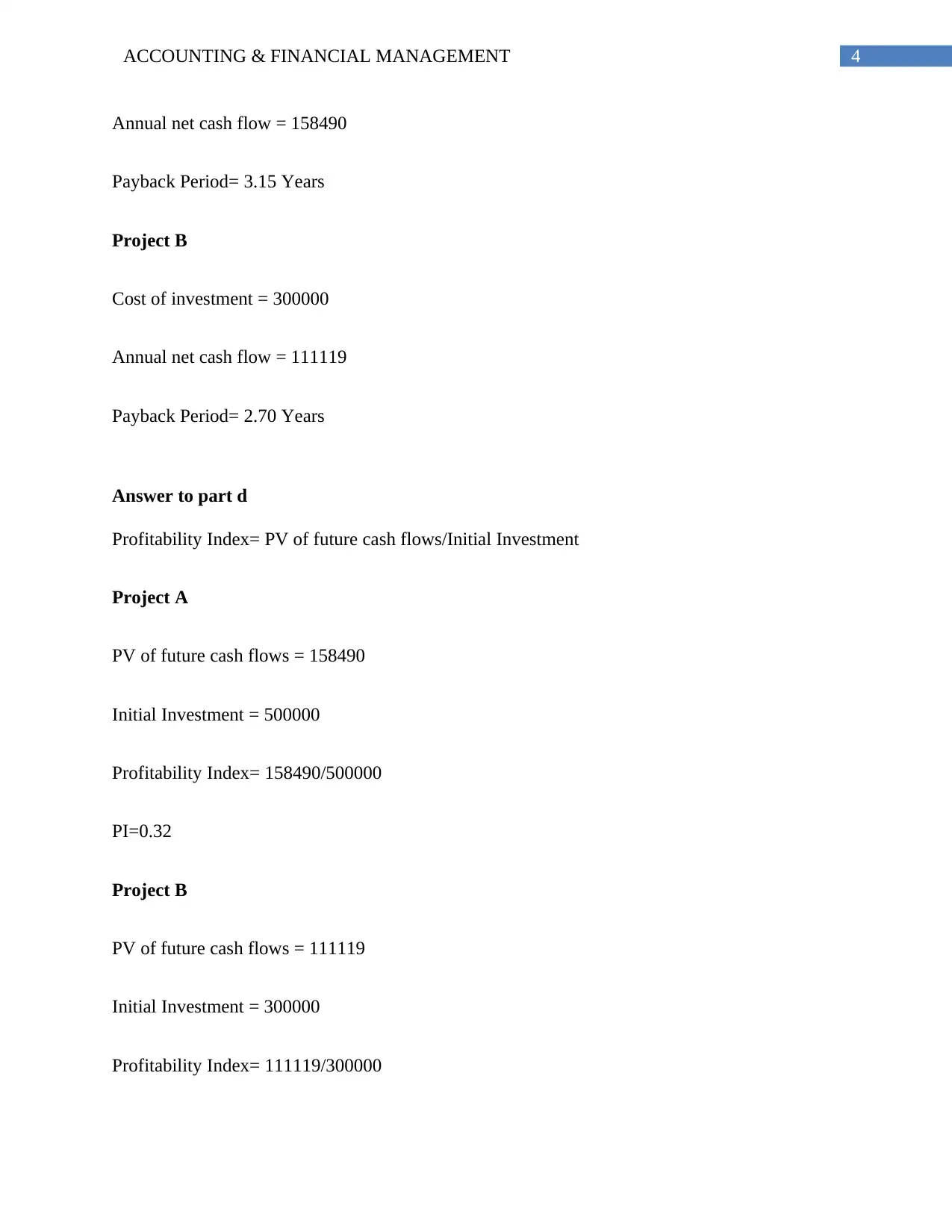

Annual net cash flow = 158490

Payback Period= 3.15 Years

Project B

Cost of investment = 300000

Annual net cash flow = 111119

Payback Period= 2.70 Years

Answer to part d

Profitability Index= PV of future cash flows/Initial Investment

Project A

PV of future cash flows = 158490

Initial Investment = 500000

Profitability Index= 158490/500000

PI=0.32

Project B

PV of future cash flows = 111119

Initial Investment = 300000

Profitability Index= 111119/300000

Annual net cash flow = 158490

Payback Period= 3.15 Years

Project B

Cost of investment = 300000

Annual net cash flow = 111119

Payback Period= 2.70 Years

Answer to part d

Profitability Index= PV of future cash flows/Initial Investment

Project A

PV of future cash flows = 158490

Initial Investment = 500000

Profitability Index= 158490/500000

PI=0.32

Project B

PV of future cash flows = 111119

Initial Investment = 300000

Profitability Index= 111119/300000

5ACCOUNTING & FINANCIAL MANAGEMENT

PI=0.37

Answer to part e

The management team of the Vina-Team Joint Ventures needs considered a total cash

flows of $ 131818 in year 1, $ -4132.231405 in year 2 and $ 30803 in year 3 for project B. In

addition to this, as per the NPV of the project A it is determined as $ -341510.1. This shows that

the negative value of the NPV is not favourable. The IRR of the project A is also -50% and

profitability index is less than 1. Henceforth, the management should not consider investing in

this project with a budget of $ 500000. Moreover, Vina-Team Joint Ventures needs to consider a

total cash flows of $ 81818 in year 1, $ -8264 in year 2 and $ 37565 in year 3 for project B. In

addition to this, as per the NPV of the project B it is determined as $ -188880.5. The IRR of the

project B is depicted as -41% along with a profitability index of 0.37. However, the payback

period is less that 3 years. Therefore, with the given budget of $ 500000, the project B is seen to

be more profitable in nature. It is recommended that the Vina-Team Joint Ventures needs to

proceed with Project B. The main rationale for such a recommendation is due to the fact that the

initial investment is low as well as the return is seen to be much more feasible in terms of the

project A. This is the main consideration which needs to be taken for the choice of Project B1.

Question 2

NPV is considered as calculating the PV of the cash flows relating to the opportunity cost

of capital deriving the value of the wealth of the shareholders. On the contrary, IRR may not be

consistent to the shareholders’ wealth maximisation when compared to NPV. It is not seen to be

1 DeAngelo, Harry, and René M. Stulz. "Liquid-claim production, risk management, and bank capital structure: Why

high leverage is optimal for banks." Journal of Financial Economics116.2 (2015): 219-236.

PI=0.37

Answer to part e

The management team of the Vina-Team Joint Ventures needs considered a total cash

flows of $ 131818 in year 1, $ -4132.231405 in year 2 and $ 30803 in year 3 for project B. In

addition to this, as per the NPV of the project A it is determined as $ -341510.1. This shows that

the negative value of the NPV is not favourable. The IRR of the project A is also -50% and

profitability index is less than 1. Henceforth, the management should not consider investing in

this project with a budget of $ 500000. Moreover, Vina-Team Joint Ventures needs to consider a

total cash flows of $ 81818 in year 1, $ -8264 in year 2 and $ 37565 in year 3 for project B. In

addition to this, as per the NPV of the project B it is determined as $ -188880.5. The IRR of the

project B is depicted as -41% along with a profitability index of 0.37. However, the payback

period is less that 3 years. Therefore, with the given budget of $ 500000, the project B is seen to

be more profitable in nature. It is recommended that the Vina-Team Joint Ventures needs to

proceed with Project B. The main rationale for such a recommendation is due to the fact that the

initial investment is low as well as the return is seen to be much more feasible in terms of the

project A. This is the main consideration which needs to be taken for the choice of Project B1.

Question 2

NPV is considered as calculating the PV of the cash flows relating to the opportunity cost

of capital deriving the value of the wealth of the shareholders. On the contrary, IRR may not be

consistent to the shareholders’ wealth maximisation when compared to NPV. It is not seen to be

1 DeAngelo, Harry, and René M. Stulz. "Liquid-claim production, risk management, and bank capital structure: Why

high leverage is optimal for banks." Journal of Financial Economics116.2 (2015): 219-236.

6ACCOUNTING & FINANCIAL MANAGEMENT

as efficient with differentiating the two projects with the same IRR on the contrary, NPV is

consistent in nature. In addition to this, IRR considers the discounting and the reinvestment of

the cash flows at the same rate of discounting factor. Even if the IRR of a project is very good

like 35%, it is practically not possible to invest money at this rate. On the contrary, NPV assumes

the rate of borrowing along with the rate of borrowing along with the lending near the market

rate which are not impractical2.

The use of the IRR and NPV is used to evaluate the projects which are often seen to be

giving similar findings. Despite of this, there has been several numbers of the projects which has

stated that IRR is not as effective as the use of the NPV. The main limitation of the IRR is seen

with the consideration of the various types of the factors which was taken into account use of a

single discount rate for evaluating each investment. Despite of the simplicity of the one discount

rate there has been several numbers of issues relating to the cause of the problem for IRR3. In

case an analyst is evaluating two projects then it is seen to share a common discount rate along

with equal risk, predictability of the cash and shorter time horizon. In this case the IRR will be

suitable. However, the main catch is seen with the shorter time horizon for IRR to be a suitable

method and in general the over time, discount rates usually change substantially. For instance,

the rate of return on the T-Bill may last 20 years as a discount rate, but one-year T-Bill returns

between 1% and 12% may last for 20 years4.

2 Zeitun, Rami, and Gary Tian. "Capital structure and corporate performance: evidence from Jordan." (2014).

3 Ukhriyawati, Catur F., Tri Ratnawati, and Slamet Riyadi. "The Influence of Asset Structure, Capital Structure,

Risk Management and Good Corporate Governance on Financial Performance and Value of The Firm through

Earnings and Free Cash Flow As An Intervening Variable in Banking Companies Listed in Indonesia Stock

Exchange." International Journal of Business and Management 12.8 (2017): 249.

4 Graham, John R., Mark T. Leary, and Michael R. Roberts. "A century of capital structure: The leveraging of

corporate America." Journal of Financial Economics 118.3 (2015): 658-683.

as efficient with differentiating the two projects with the same IRR on the contrary, NPV is

consistent in nature. In addition to this, IRR considers the discounting and the reinvestment of

the cash flows at the same rate of discounting factor. Even if the IRR of a project is very good

like 35%, it is practically not possible to invest money at this rate. On the contrary, NPV assumes

the rate of borrowing along with the rate of borrowing along with the lending near the market

rate which are not impractical2.

The use of the IRR and NPV is used to evaluate the projects which are often seen to be

giving similar findings. Despite of this, there has been several numbers of the projects which has

stated that IRR is not as effective as the use of the NPV. The main limitation of the IRR is seen

with the consideration of the various types of the factors which was taken into account use of a

single discount rate for evaluating each investment. Despite of the simplicity of the one discount

rate there has been several numbers of issues relating to the cause of the problem for IRR3. In

case an analyst is evaluating two projects then it is seen to share a common discount rate along

with equal risk, predictability of the cash and shorter time horizon. In this case the IRR will be

suitable. However, the main catch is seen with the shorter time horizon for IRR to be a suitable

method and in general the over time, discount rates usually change substantially. For instance,

the rate of return on the T-Bill may last 20 years as a discount rate, but one-year T-Bill returns

between 1% and 12% may last for 20 years4.

2 Zeitun, Rami, and Gary Tian. "Capital structure and corporate performance: evidence from Jordan." (2014).

3 Ukhriyawati, Catur F., Tri Ratnawati, and Slamet Riyadi. "The Influence of Asset Structure, Capital Structure,

Risk Management and Good Corporate Governance on Financial Performance and Value of The Firm through

Earnings and Free Cash Flow As An Intervening Variable in Banking Companies Listed in Indonesia Stock

Exchange." International Journal of Business and Management 12.8 (2017): 249.

4 Graham, John R., Mark T. Leary, and Michael R. Roberts. "A century of capital structure: The leveraging of

corporate America." Journal of Financial Economics 118.3 (2015): 658-683.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING & FINANCIAL MANAGEMENT

IRR is not seen to be taking into account any changing discount rates without any

modification. Therefore, this is not seen to be suitable for the longer-term projects which are

expected to vary. A similar nature of the project for the basic IRR computation is ineffective

with the mixture of the multiple positive and negative cash flows. Moreover, a single IRR cannot

be used. On recalling the IRR is identified as the discount rate or the interest needed for a single

project to break given in the initial investment. In case of the chagrin market conditions there

may be multiple IRRs for a project. The projects with longer projects is susceptible to be having

additional investments of capital with distinct IRR values. The main form of the advantage for

using the NPV over IRR is seen with handling multiple discount rates without any major

concern.

It needs to be also seen that NPV includes the various types of the present values of the

stream of the cash flows at a discount rate. The IRR on the other hand, has been able to solve the

rate of return thereby setting to equal to zero5. The focus of the NPV is seen to be solving with a

present value of a stream of cash flows along with a definite discount rate. On the other hand,

IRR is depicted to consider the rate of return thereby setting the value of NPV equal to zero. It

needs to be understood that the IRR has been able to answer the questions like what is rate of the

return which can be achieved, whereas NPV is able to consider answering the question whether

stream of cash flows is worth at a particular discount rate as per the recent value of the dollar6.

The appropriateness of the IRR is depicted to be only valid whether to accept a project or

a particular investment plan in which the IRR is greater in compare to the cost of capital.

5 Serfling, Matthew. "Firing costs and capital structure decisions." The Journal of Finance 71.5 (2016): 2239-2286.

6 Robb, Alicia M., and David T. Robinson. "The capital structure decisions of new firms." The Review of Financial

Studies 27.1 (2014): 153-179.

IRR is not seen to be taking into account any changing discount rates without any

modification. Therefore, this is not seen to be suitable for the longer-term projects which are

expected to vary. A similar nature of the project for the basic IRR computation is ineffective

with the mixture of the multiple positive and negative cash flows. Moreover, a single IRR cannot

be used. On recalling the IRR is identified as the discount rate or the interest needed for a single

project to break given in the initial investment. In case of the chagrin market conditions there

may be multiple IRRs for a project. The projects with longer projects is susceptible to be having

additional investments of capital with distinct IRR values. The main form of the advantage for

using the NPV over IRR is seen with handling multiple discount rates without any major

concern.

It needs to be also seen that NPV includes the various types of the present values of the

stream of the cash flows at a discount rate. The IRR on the other hand, has been able to solve the

rate of return thereby setting to equal to zero5. The focus of the NPV is seen to be solving with a

present value of a stream of cash flows along with a definite discount rate. On the other hand,

IRR is depicted to consider the rate of return thereby setting the value of NPV equal to zero. It

needs to be understood that the IRR has been able to answer the questions like what is rate of the

return which can be achieved, whereas NPV is able to consider answering the question whether

stream of cash flows is worth at a particular discount rate as per the recent value of the dollar6.

The appropriateness of the IRR is depicted to be only valid whether to accept a project or

a particular investment plan in which the IRR is greater in compare to the cost of capital.

5 Serfling, Matthew. "Firing costs and capital structure decisions." The Journal of Finance 71.5 (2016): 2239-2286.

6 Robb, Alicia M., and David T. Robinson. "The capital structure decisions of new firms." The Review of Financial

Studies 27.1 (2014): 153-179.

8ACCOUNTING & FINANCIAL MANAGEMENT

However, in case of any change in the rate of discount there several difficulties in making the

comparison. In case there are two or more mutually exclusive projects then the application of

IRR is not seen to be effective in nature. In addition to this, some of the various types of the

other consideration of NPV it needs to be seen that the discount rate for the NPV is depicted to

be remaining constant in nature. However, the calculation of the IRR is seen to be comprising of

the NOV to remain at zero and the total rate at which the conditions of the IRR is fulfilled7.

The various types of the other disadvantages of using IRR does not consider the primary

factors such as the project duration along with the future cost of the project. The IRR is seen to

compare the cash flow of the project and the existing cost and excluding factors8. The overall

disadvantage of the IRR may be summed up with economies of scale ignored, impractical

implicit assumption of reinvestment rate and dependency on the contingent projects. The pitfall

of the use of the IRR method is seen with ignoring the actual dollar benefits. The project value

ranking with IRR is considered with a very limited dollar benefit due to the fact of the increase in

the 50% increase in the value of IRR9.

The analysis of the implicit assumption of the reinvestment rate which is seen to be

depicted with the consideration of the various types of the low IRR. In such a state the receiving

the cash flows is seen to be rarely possible in nature. The finance managers are seen to come

across various situations in which the project evaluation creates a compulsion for investing in

other projects. For instance, investing in big projects needs to arrange for several activities and

7 Albul, Boris, Dwight M. Jaffee, and Alexei Tchistyi. "Contingent convertible bonds and capital structure

decisions." (2015).

8 Baker, Malcolm, and Jeffrey Wurgler. "Do strict capital requirements raise the cost of capital? Bank regulation,

capital structure, and the low-risk anomaly." American Economic Review 105.5 (2015): 315-20.

9 Faccio, Mara, and Jin Xu. "Taxes and capital structure." Journal of Financial and Quantitative Analysis 50.3

(2015): 277-300.

However, in case of any change in the rate of discount there several difficulties in making the

comparison. In case there are two or more mutually exclusive projects then the application of

IRR is not seen to be effective in nature. In addition to this, some of the various types of the

other consideration of NPV it needs to be seen that the discount rate for the NPV is depicted to

be remaining constant in nature. However, the calculation of the IRR is seen to be comprising of

the NOV to remain at zero and the total rate at which the conditions of the IRR is fulfilled7.

The various types of the other disadvantages of using IRR does not consider the primary

factors such as the project duration along with the future cost of the project. The IRR is seen to

compare the cash flow of the project and the existing cost and excluding factors8. The overall

disadvantage of the IRR may be summed up with economies of scale ignored, impractical

implicit assumption of reinvestment rate and dependency on the contingent projects. The pitfall

of the use of the IRR method is seen with ignoring the actual dollar benefits. The project value

ranking with IRR is considered with a very limited dollar benefit due to the fact of the increase in

the 50% increase in the value of IRR9.

The analysis of the implicit assumption of the reinvestment rate which is seen to be

depicted with the consideration of the various types of the low IRR. In such a state the receiving

the cash flows is seen to be rarely possible in nature. The finance managers are seen to come

across various situations in which the project evaluation creates a compulsion for investing in

other projects. For instance, investing in big projects needs to arrange for several activities and

7 Albul, Boris, Dwight M. Jaffee, and Alexei Tchistyi. "Contingent convertible bonds and capital structure

decisions." (2015).

8 Baker, Malcolm, and Jeffrey Wurgler. "Do strict capital requirements raise the cost of capital? Bank regulation,

capital structure, and the low-risk anomaly." American Economic Review 105.5 (2015): 315-20.

9 Faccio, Mara, and Jin Xu. "Taxes and capital structure." Journal of Financial and Quantitative Analysis 50.3

(2015): 277-300.

9ACCOUNTING & FINANCIAL MANAGEMENT

these projects are dependent with the contingent projects which is to be considered by the

manager10.

10 Allen, Franklin, Elena Carletti, and Robert Marquez. "Deposits and bank capital structure." Journal of Financial

Economics118.3 (2015): 601-619.

these projects are dependent with the contingent projects which is to be considered by the

manager10.

10 Allen, Franklin, Elena Carletti, and Robert Marquez. "Deposits and bank capital structure." Journal of Financial

Economics118.3 (2015): 601-619.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ACCOUNTING & FINANCIAL MANAGEMENT

References

Albul, Boris, Dwight M. Jaffee, and Alexei Tchistyi. "Contingent convertible bonds and capital

structure decisions." (2015).

Allen, Franklin, Elena Carletti, and Robert Marquez. "Deposits and bank capital

structure." Journal of Financial Economics118.3 (2015): 601-619.

Baker, Malcolm, and Jeffrey Wurgler. "Do strict capital requirements raise the cost of capital?

Bank regulation, capital structure, and the low-risk anomaly." American Economic Review 105.5

(2015): 315-20.

DeAngelo, Harry, and René M. Stulz. "Liquid-claim production, risk management, and bank

capital structure: Why high leverage is optimal for banks." Journal of Financial Economics116.2

(2015): 219-236.

Faccio, Mara, and Jin Xu. "Taxes and capital structure." Journal of Financial and Quantitative

Analysis 50.3 (2015): 277-300.

Graham, John R., Mark T. Leary, and Michael R. Roberts. "A century of capital structure: The

leveraging of corporate America." Journal of Financial Economics 118.3 (2015): 658-683.

Robb, Alicia M., and David T. Robinson. "The capital structure decisions of new firms." The

Review of Financial Studies 27.1 (2014): 153-179.

Serfling, Matthew. "Firing costs and capital structure decisions." The Journal of Finance 71.5

(2016): 2239-2286.

References

Albul, Boris, Dwight M. Jaffee, and Alexei Tchistyi. "Contingent convertible bonds and capital

structure decisions." (2015).

Allen, Franklin, Elena Carletti, and Robert Marquez. "Deposits and bank capital

structure." Journal of Financial Economics118.3 (2015): 601-619.

Baker, Malcolm, and Jeffrey Wurgler. "Do strict capital requirements raise the cost of capital?

Bank regulation, capital structure, and the low-risk anomaly." American Economic Review 105.5

(2015): 315-20.

DeAngelo, Harry, and René M. Stulz. "Liquid-claim production, risk management, and bank

capital structure: Why high leverage is optimal for banks." Journal of Financial Economics116.2

(2015): 219-236.

Faccio, Mara, and Jin Xu. "Taxes and capital structure." Journal of Financial and Quantitative

Analysis 50.3 (2015): 277-300.

Graham, John R., Mark T. Leary, and Michael R. Roberts. "A century of capital structure: The

leveraging of corporate America." Journal of Financial Economics 118.3 (2015): 658-683.

Robb, Alicia M., and David T. Robinson. "The capital structure decisions of new firms." The

Review of Financial Studies 27.1 (2014): 153-179.

Serfling, Matthew. "Firing costs and capital structure decisions." The Journal of Finance 71.5

(2016): 2239-2286.

11ACCOUNTING & FINANCIAL MANAGEMENT

Ukhriyawati, Catur F., Tri Ratnawati, and Slamet Riyadi. "The Influence of Asset Structure,

Capital Structure, Risk Management and Good Corporate Governance on Financial Performance

and Value of The Firm through Earnings and Free Cash Flow As An Intervening Variable in

Banking Companies Listed in Indonesia Stock Exchange." International Journal of Business and

Management 12.8 (2017): 249.

Zeitun, Rami, and Gary Tian. "Capital structure and corporate performance: evidence from

Jordan." (2014).

Ukhriyawati, Catur F., Tri Ratnawati, and Slamet Riyadi. "The Influence of Asset Structure,

Capital Structure, Risk Management and Good Corporate Governance on Financial Performance

and Value of The Firm through Earnings and Free Cash Flow As An Intervening Variable in

Banking Companies Listed in Indonesia Stock Exchange." International Journal of Business and

Management 12.8 (2017): 249.

Zeitun, Rami, and Gary Tian. "Capital structure and corporate performance: evidence from

Jordan." (2014).

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.