Accounting for Business: Sales, Ratios, and Cash Inflows

VerifiedAdded on 2023/06/17

|6

|792

|98

AI Summary

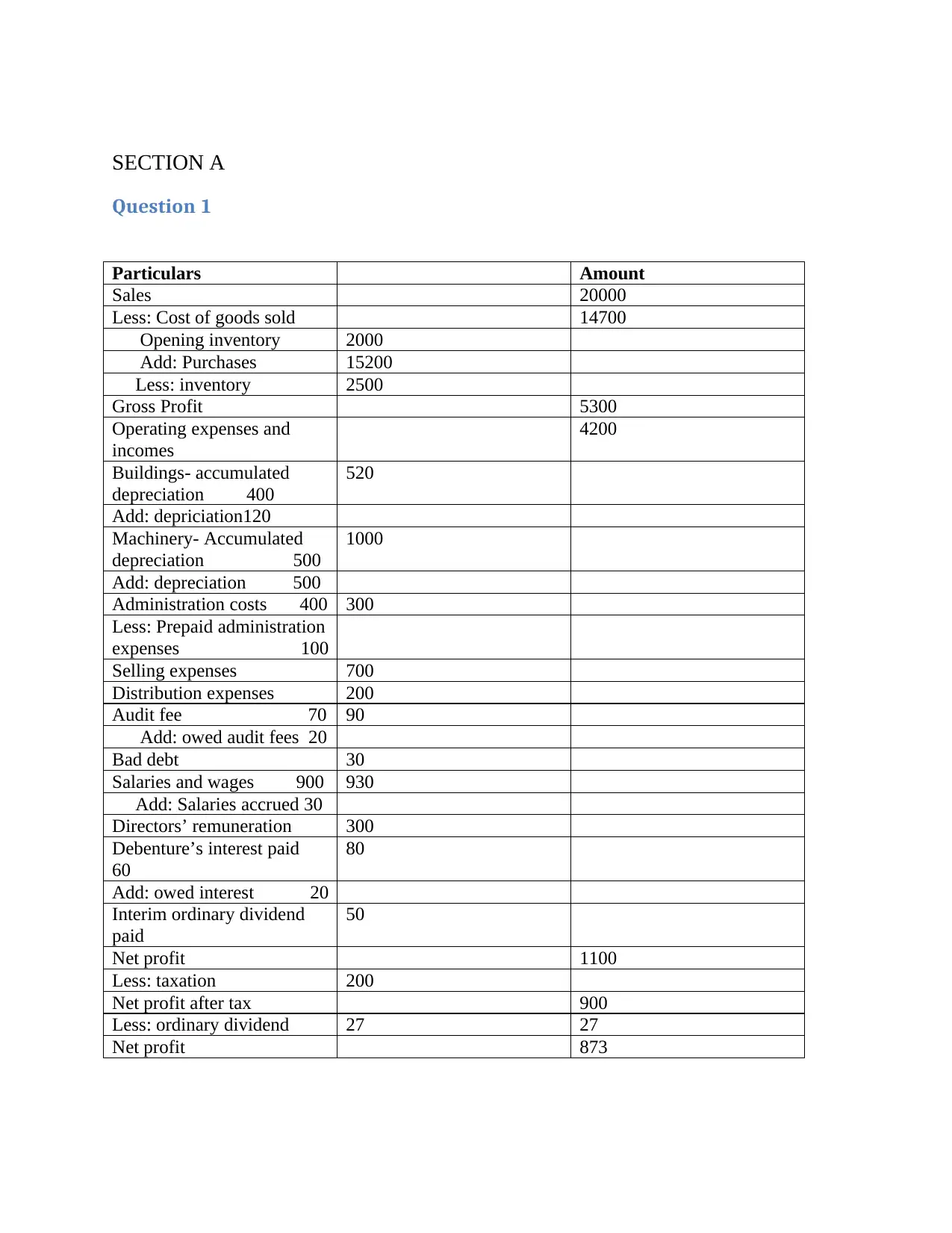

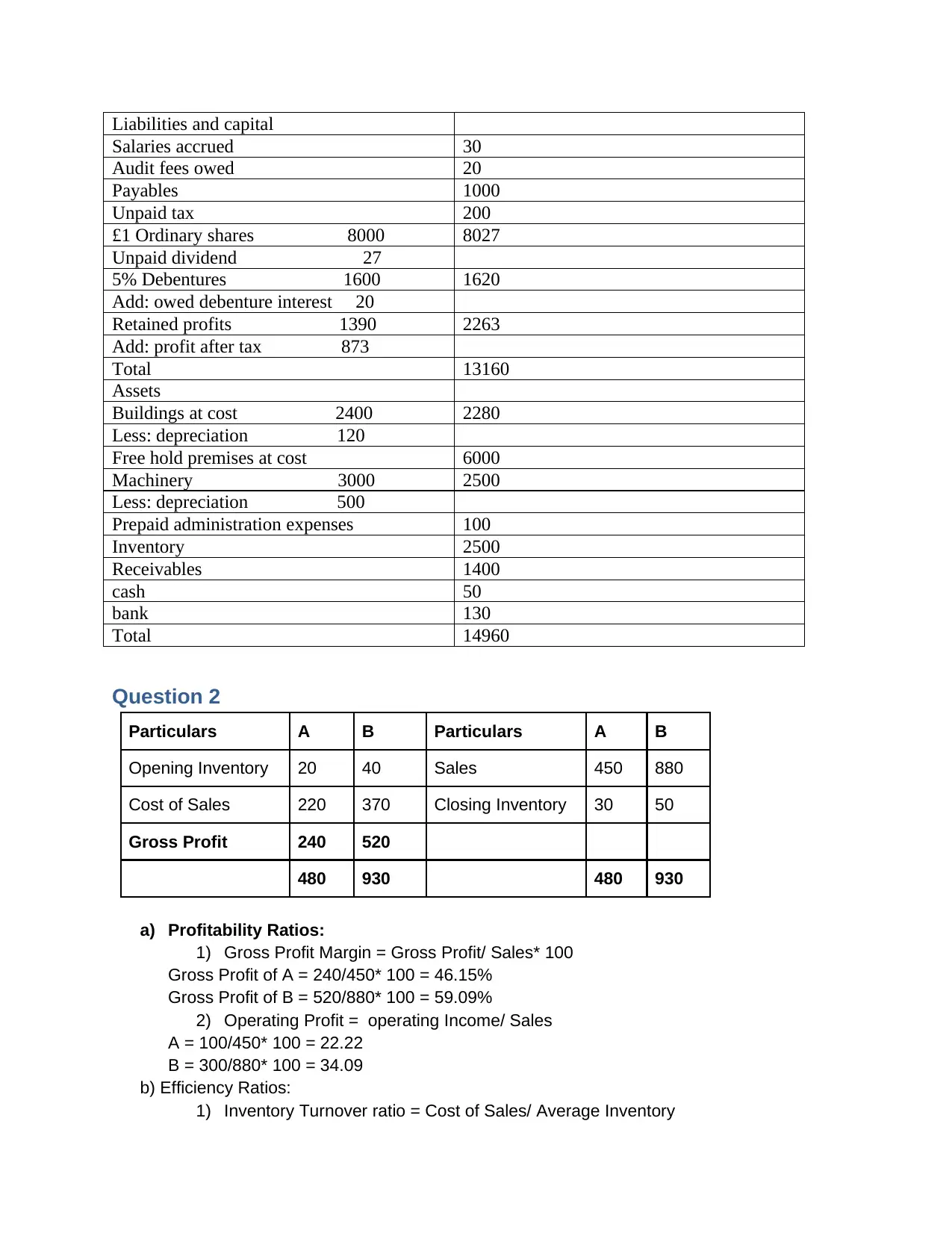

This content covers accounting for business with solved assignments, essays, and dissertations. It includes sales, cost of goods sold, gross profit, operating expenses, buildings, machinery, administration costs, selling expenses, audit fees, bad debt, salaries and wages, directors’ remuneration, debenture’s interest paid, interim ordinary dividend paid, liabilities and capital, and assets. It also covers profitability ratios, efficiency ratios, current ratio, acid test ratio, and financial viability. The output is in JSON format.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.