University Report: Accounting for Leases and AASB (IFRS 16)

VerifiedAdded on 2022/09/15

|13

|3013

|17

Report

AI Summary

This report assesses the impact of the new lease standard AASB/IFRS 16 on reporting entities listed on the Australian stock exchange, specifically Harvey Norman Holdings and Myer Holdings Group, both from the retail sector. The analysis reveals significant changes in accounting processes due to the adoption of the standard. The report examines how the accounting treatment for leases has changed after the implementation of AASB 16, which replaced the previous standard AASB 117. The introduction of IFRS 16 has brought revolutionary changes in lease accounting, impacting entities across all industries, particularly the retail sector due to its considerable use of rented premises. The report details the impact on financial statements, including balance sheets and income statements, by recognizing assets as right-of-use and liabilities, affecting the balance sheet and operating costs. It also summarizes the lease values of the companies as stated in their financial reports and identifies the short and long-term impacts of the changes to lease reporting.

Running head: ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

Accounting for leases- The impact of AASB (IFRS 16)

Name of the Student

Name of the University

Author Note

Accounting for leases- The impact of AASB (IFRS 16)

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

Executive summary:

The report is prepared to assess the impact of the new lease standard AASB/IFRS 16 on the

reporting entities listed on the Australian stock exchange. For the assessment of the impact of

such standard, two entities from the retail sector have been chosen named Harvey Norman

Holdings and Myer Holdings Group. It is ascertained from the analysis of the facts about the

adoption of the standard that the reporting entities would be identifying significant changes in

their accounting process. Nonetheless, such standard intends to serve the users of the

financial statements by making the information transparent by the disclosure of the lease

contracts and those as operating lease on the balance sheet.

Executive summary:

The report is prepared to assess the impact of the new lease standard AASB/IFRS 16 on the

reporting entities listed on the Australian stock exchange. For the assessment of the impact of

such standard, two entities from the retail sector have been chosen named Harvey Norman

Holdings and Myer Holdings Group. It is ascertained from the analysis of the facts about the

adoption of the standard that the reporting entities would be identifying significant changes in

their accounting process. Nonetheless, such standard intends to serve the users of the

financial statements by making the information transparent by the disclosure of the lease

contracts and those as operating lease on the balance sheet.

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................3

Impact of the lease arrangements on the financial report by demonstrating financial and

operating lease:...........................................................................................................................3

Summarizing the lease values of company as stated in their financial reports:.........................4

Identifying the impact of the accounting rules for lease on two entities:..................................5

Determining the short term and long term impact of the changes to lease reporting:...............8

Conclusion:................................................................................................................................8

References list:.........................................................................................................................10

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................3

Impact of the lease arrangements on the financial report by demonstrating financial and

operating lease:...........................................................................................................................3

Summarizing the lease values of company as stated in their financial reports:.........................4

Identifying the impact of the accounting rules for lease on two entities:..................................5

Determining the short term and long term impact of the changes to lease reporting:...............8

Conclusion:................................................................................................................................8

References list:.........................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

Introduction:

The paper is developed to demonstrate an insight into lease accounting in relation to

two well-known retailers of Australia that is Myer Holdings Limited and Harvey Norman

Holdings limited. Major changes brought by the introduction of new lease standard has been

examined and how the accounting treatment for lease has changed after the implementation

of new lease standard AASB 16 is outlined in the report. It is believed that the former

accounting standard did not reflect the economic reality as many of the operating lease are

not recorded in the balance sheet. Due to this, off balance sheet liabilities considerably higher

than the liabilities reported on the balance sheet. Harvey Norman and Myer are Australian

based retailer with the former engaged in the retailing of bedding, furniture, electronic

products and latter operates the departmental stores. The existing accounting requirements

under the former lease standard that is AASB 117 has been replaced by the new lease

standard AASB 16 which is implemented and has been effective from July 1st, 2019 (Hladika

and Valenta 2018). These two entities under discussion have not adopted a single accounting

lease model that do not classify between the financial and operating lease.

Discussion:

Impact of the lease arrangements on the financial report by demonstrating financial

and operating lease:

The assessment of the impact of the new lease standard IFRS 16 on the financial

statement of the companies is identified in this section. Introduction of IFRS 16 has brought a

revolutionary changes in the world of lease accounting as the entities across all the industries

would be impacted by it. With the continuous evolvement in the landscape of retail,

unexpected vacancies is being faced by the commercial establishment and malls in areas of

high traffic. The concept of recognizing the asset as right to use is introduced under the new

Introduction:

The paper is developed to demonstrate an insight into lease accounting in relation to

two well-known retailers of Australia that is Myer Holdings Limited and Harvey Norman

Holdings limited. Major changes brought by the introduction of new lease standard has been

examined and how the accounting treatment for lease has changed after the implementation

of new lease standard AASB 16 is outlined in the report. It is believed that the former

accounting standard did not reflect the economic reality as many of the operating lease are

not recorded in the balance sheet. Due to this, off balance sheet liabilities considerably higher

than the liabilities reported on the balance sheet. Harvey Norman and Myer are Australian

based retailer with the former engaged in the retailing of bedding, furniture, electronic

products and latter operates the departmental stores. The existing accounting requirements

under the former lease standard that is AASB 117 has been replaced by the new lease

standard AASB 16 which is implemented and has been effective from July 1st, 2019 (Hladika

and Valenta 2018). These two entities under discussion have not adopted a single accounting

lease model that do not classify between the financial and operating lease.

Discussion:

Impact of the lease arrangements on the financial report by demonstrating financial

and operating lease:

The assessment of the impact of the new lease standard IFRS 16 on the financial

statement of the companies is identified in this section. Introduction of IFRS 16 has brought a

revolutionary changes in the world of lease accounting as the entities across all the industries

would be impacted by it. With the continuous evolvement in the landscape of retail,

unexpected vacancies is being faced by the commercial establishment and malls in areas of

high traffic. The concept of recognizing the asset as right to use is introduced under the new

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

standard and this calls for the evaluation of the assets for impairment. New standard offers a

detail guidance for assessing the contract containing service or lease. IFRS 16 is likely to

impact the retail industry the most given the considerable use of rented premises for the

stores. Many of the leases of retail companies is classified as operating lease and no impact is

identified on the balance sheet under the previous lease standard. Such type of leases are in

the form of IT equipment, leases, premises that often has variable rentals due to contingent

rentals and adjustments (Aasb.gov.au 2020). With the split of the expense between operating

and finance cost, the new standard does not only impact the balance sheet but also the

operating cost.

The financial statements of the retailers would be significantly impacted by the

changes introduced by IFRS 16 because the retail business has largest volume of operating

leases. Profile of lease expenses is changed every year and the balance sheet recognizing

almost all the leases. It is important for the retailers to account for the new extensions and

agreements and consider the impact of existing long dates lease as the pre-existing leases

would be impacted by the new standard (Morales and Zamora 2018). Changes in accounting

of lease would impact the financial report because of changes in the income statement and

balance sheet. The balance sheet of the company recognizes all the leases as lease liability

and corresponding as the “right to use assets”. Recognition of lease expenses in the income

statement changes in terms of timing of recognition of cost in each lease year and

presentation of the statement (Giner and Pardo 2018).

Summarizing the lease values of company as stated in their financial reports:

Harvey Norman Holding limited is a retail icon and the company operates under the

three brand names Domayne, Harvey Norman and Joyce Mayne. The principal activities of

Harvey Norman Holdings involves franchise, retail, digital enterprise and property and offers

standard and this calls for the evaluation of the assets for impairment. New standard offers a

detail guidance for assessing the contract containing service or lease. IFRS 16 is likely to

impact the retail industry the most given the considerable use of rented premises for the

stores. Many of the leases of retail companies is classified as operating lease and no impact is

identified on the balance sheet under the previous lease standard. Such type of leases are in

the form of IT equipment, leases, premises that often has variable rentals due to contingent

rentals and adjustments (Aasb.gov.au 2020). With the split of the expense between operating

and finance cost, the new standard does not only impact the balance sheet but also the

operating cost.

The financial statements of the retailers would be significantly impacted by the

changes introduced by IFRS 16 because the retail business has largest volume of operating

leases. Profile of lease expenses is changed every year and the balance sheet recognizing

almost all the leases. It is important for the retailers to account for the new extensions and

agreements and consider the impact of existing long dates lease as the pre-existing leases

would be impacted by the new standard (Morales and Zamora 2018). Changes in accounting

of lease would impact the financial report because of changes in the income statement and

balance sheet. The balance sheet of the company recognizes all the leases as lease liability

and corresponding as the “right to use assets”. Recognition of lease expenses in the income

statement changes in terms of timing of recognition of cost in each lease year and

presentation of the statement (Giner and Pardo 2018).

Summarizing the lease values of company as stated in their financial reports:

Harvey Norman Holding limited is a retail icon and the company operates under the

three brand names Domayne, Harvey Norman and Joyce Mayne. The principal activities of

Harvey Norman Holdings involves franchise, retail, digital enterprise and property and offers

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

its customers with an unparalleled retail experience. The company owns and operated ninety

branded stores and boosting the position as global retailer. Diversity in offerings and great

strengths and effectively operating across array of products offerings makes it difficult for

other company to compete with Harvey Norman. The company being a lessee is required to

recognize the right of use asset representing the lease liability and right to use the underlying

assets. Harvey Norman has reported a total amount of operating lease liabilities of $ 693554

in year 2019 compared to $ 689219 in year 2018. Minimum lease receivable is recorded at $

306991 and $ 337341 in year 2019 and 2018 respectively. In addition to this, present value of

lease payment is 3564 and 4265 in year 2019 and 2018 (harveynormanholdings.com.au

2020).

Myer holdings is one of the largest departmental store group of Australia that

prioritizes customer in every decision making process. That is the decisions are taken by the

company in the best interest of the shareholders and customers. Offer of company’s

merchandise include the categories of product such as children wear, menswear, electrical

good, home ware and beauty. Majority of operations of Myer are in Australia and it

encompasses the departmental stores and the online business forming significant assets that

helps in delivering strong growth. Financial year 2019 has recorded a minimum lease

payment of $ 225965 compared to $ 229075 in year 2018. Total amount of rental expense

relating to operating lease is $ 228268 in year 2019 and $ 231787 in year 2018. In addition to

this, company also maintained a provision to support current and non-current onerous lease of

amount of $ 4806 and $ 3499 in year 2019. The commitment of organization in relation to

minimum lease payment for the operating lease is $ 2,427,902 and $ 2,537,556 for 2019 and

2018 for year 2019 and 2018 respectively (investor.myer.com.au 2020). The company has

recognized the right of use assets to account for the operating lease under the new accounting

standard for lease.

its customers with an unparalleled retail experience. The company owns and operated ninety

branded stores and boosting the position as global retailer. Diversity in offerings and great

strengths and effectively operating across array of products offerings makes it difficult for

other company to compete with Harvey Norman. The company being a lessee is required to

recognize the right of use asset representing the lease liability and right to use the underlying

assets. Harvey Norman has reported a total amount of operating lease liabilities of $ 693554

in year 2019 compared to $ 689219 in year 2018. Minimum lease receivable is recorded at $

306991 and $ 337341 in year 2019 and 2018 respectively. In addition to this, present value of

lease payment is 3564 and 4265 in year 2019 and 2018 (harveynormanholdings.com.au

2020).

Myer holdings is one of the largest departmental store group of Australia that

prioritizes customer in every decision making process. That is the decisions are taken by the

company in the best interest of the shareholders and customers. Offer of company’s

merchandise include the categories of product such as children wear, menswear, electrical

good, home ware and beauty. Majority of operations of Myer are in Australia and it

encompasses the departmental stores and the online business forming significant assets that

helps in delivering strong growth. Financial year 2019 has recorded a minimum lease

payment of $ 225965 compared to $ 229075 in year 2018. Total amount of rental expense

relating to operating lease is $ 228268 in year 2019 and $ 231787 in year 2018. In addition to

this, company also maintained a provision to support current and non-current onerous lease of

amount of $ 4806 and $ 3499 in year 2019. The commitment of organization in relation to

minimum lease payment for the operating lease is $ 2,427,902 and $ 2,537,556 for 2019 and

2018 for year 2019 and 2018 respectively (investor.myer.com.au 2020). The company has

recognized the right of use assets to account for the operating lease under the new accounting

standard for lease.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

Identifying the impact of the accounting rules for lease on two entities:

For the measurement and identification of lease arrangements, Harvey Norman has

adopted the new accounting standard AASB 16 with effect from 1st July, 2019. Under this

standard, the company has recognized all the lease assets and liabilities that has a term of 12

months and unless the value of assets is low. The right of use assets is also recognized by the

lessee under the new standard and representing the rights to be used as leased liability and

underlying assets long with the future lease payments present value. As permitted under the

new standard, an approach of modified retrospective is applied by the consolidated entity and

the cumulative impact of the application would result in identifying the adjustment to the

retained earnings opening balance at 1st July, 2019. Measurement of the right of use assets on

transition is done at the carrying value and at the same time incremental borrowing rate is

used to arrive at the discounted value of the assets. Under the lease, measurement of lease

liability is done at future payables net present value including the renewal period options.

Therefore, it is identified that the adoption of AASB 16 would result in recognizing the right

of assets use and meeting the investment property definition (Cpaaustralia.com.au 2020).

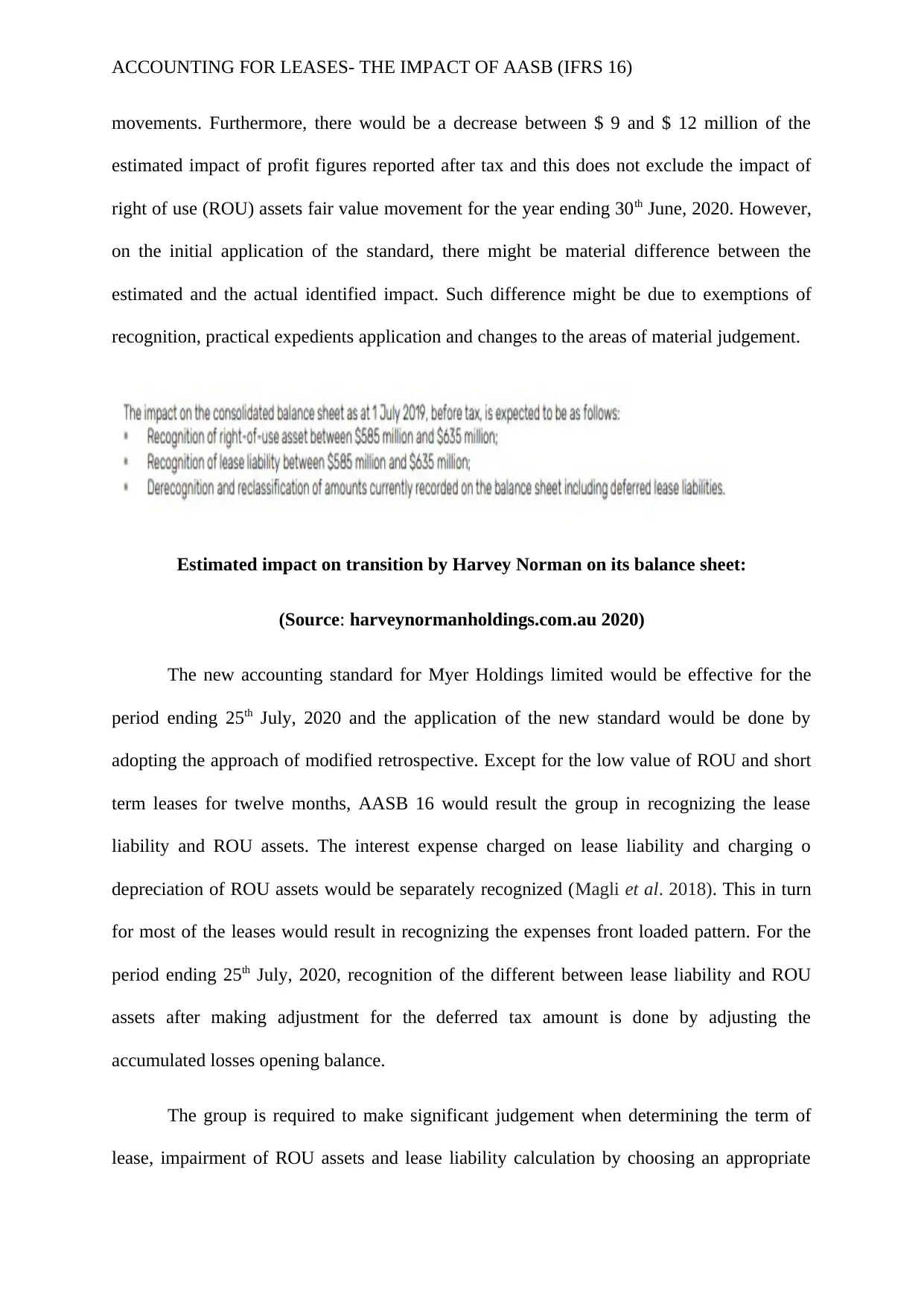

New standard is expected to impact the consolidated balance sheet by lease liability

recognition between $ 585 and $ 635 million and right of use assets recognition between $

585 and $ 635 million (harveynormanholdings.com.au 2020). In addition to this, the amount

currently recorded in the balance sheet and this include the deferred lease liabilities is

reclassified and derecognized.

The income statement of Harvey Norman would replace the lease expense by the

interest expense on lease liability, right of use assets and right of use assets fair value

Identifying the impact of the accounting rules for lease on two entities:

For the measurement and identification of lease arrangements, Harvey Norman has

adopted the new accounting standard AASB 16 with effect from 1st July, 2019. Under this

standard, the company has recognized all the lease assets and liabilities that has a term of 12

months and unless the value of assets is low. The right of use assets is also recognized by the

lessee under the new standard and representing the rights to be used as leased liability and

underlying assets long with the future lease payments present value. As permitted under the

new standard, an approach of modified retrospective is applied by the consolidated entity and

the cumulative impact of the application would result in identifying the adjustment to the

retained earnings opening balance at 1st July, 2019. Measurement of the right of use assets on

transition is done at the carrying value and at the same time incremental borrowing rate is

used to arrive at the discounted value of the assets. Under the lease, measurement of lease

liability is done at future payables net present value including the renewal period options.

Therefore, it is identified that the adoption of AASB 16 would result in recognizing the right

of assets use and meeting the investment property definition (Cpaaustralia.com.au 2020).

New standard is expected to impact the consolidated balance sheet by lease liability

recognition between $ 585 and $ 635 million and right of use assets recognition between $

585 and $ 635 million (harveynormanholdings.com.au 2020). In addition to this, the amount

currently recorded in the balance sheet and this include the deferred lease liabilities is

reclassified and derecognized.

The income statement of Harvey Norman would replace the lease expense by the

interest expense on lease liability, right of use assets and right of use assets fair value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

movements. Furthermore, there would be a decrease between $ 9 and $ 12 million of the

estimated impact of profit figures reported after tax and this does not exclude the impact of

right of use (ROU) assets fair value movement for the year ending 30th June, 2020. However,

on the initial application of the standard, there might be material difference between the

estimated and the actual identified impact. Such difference might be due to exemptions of

recognition, practical expedients application and changes to the areas of material judgement.

Estimated impact on transition by Harvey Norman on its balance sheet:

(Source: harveynormanholdings.com.au 2020)

The new accounting standard for Myer Holdings limited would be effective for the

period ending 25th July, 2020 and the application of the new standard would be done by

adopting the approach of modified retrospective. Except for the low value of ROU and short

term leases for twelve months, AASB 16 would result the group in recognizing the lease

liability and ROU assets. The interest expense charged on lease liability and charging o

depreciation of ROU assets would be separately recognized (Magli et al. 2018). This in turn

for most of the leases would result in recognizing the expenses front loaded pattern. For the

period ending 25th July, 2020, recognition of the different between lease liability and ROU

assets after making adjustment for the deferred tax amount is done by adjusting the

accumulated losses opening balance.

The group is required to make significant judgement when determining the term of

lease, impairment of ROU assets and lease liability calculation by choosing an appropriate

movements. Furthermore, there would be a decrease between $ 9 and $ 12 million of the

estimated impact of profit figures reported after tax and this does not exclude the impact of

right of use (ROU) assets fair value movement for the year ending 30th June, 2020. However,

on the initial application of the standard, there might be material difference between the

estimated and the actual identified impact. Such difference might be due to exemptions of

recognition, practical expedients application and changes to the areas of material judgement.

Estimated impact on transition by Harvey Norman on its balance sheet:

(Source: harveynormanholdings.com.au 2020)

The new accounting standard for Myer Holdings limited would be effective for the

period ending 25th July, 2020 and the application of the new standard would be done by

adopting the approach of modified retrospective. Except for the low value of ROU and short

term leases for twelve months, AASB 16 would result the group in recognizing the lease

liability and ROU assets. The interest expense charged on lease liability and charging o

depreciation of ROU assets would be separately recognized (Magli et al. 2018). This in turn

for most of the leases would result in recognizing the expenses front loaded pattern. For the

period ending 25th July, 2020, recognition of the different between lease liability and ROU

assets after making adjustment for the deferred tax amount is done by adjusting the

accumulated losses opening balance.

The group is required to make significant judgement when determining the term of

lease, impairment of ROU assets and lease liability calculation by choosing an appropriate

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

rate of discount. For reporting and accounting under the new standard, group has established

control and procedures and has implemented a system of IT for reporting and collating lease

data along with applying the lease payment using appropriate rate of discount. Furthermore, it

is reported by the group that there would be significant impact on the cash flow classification

relating to lease contracts, on the income statement and liabilities and on the reported assets

value. Moreover, a number of key measures such as cash flow from operating and financing

activities and earnings before interest and tax along with the measures of alternative

performance by the group is impacted by the adoption of the standard (investor.myer.com.au

2020).

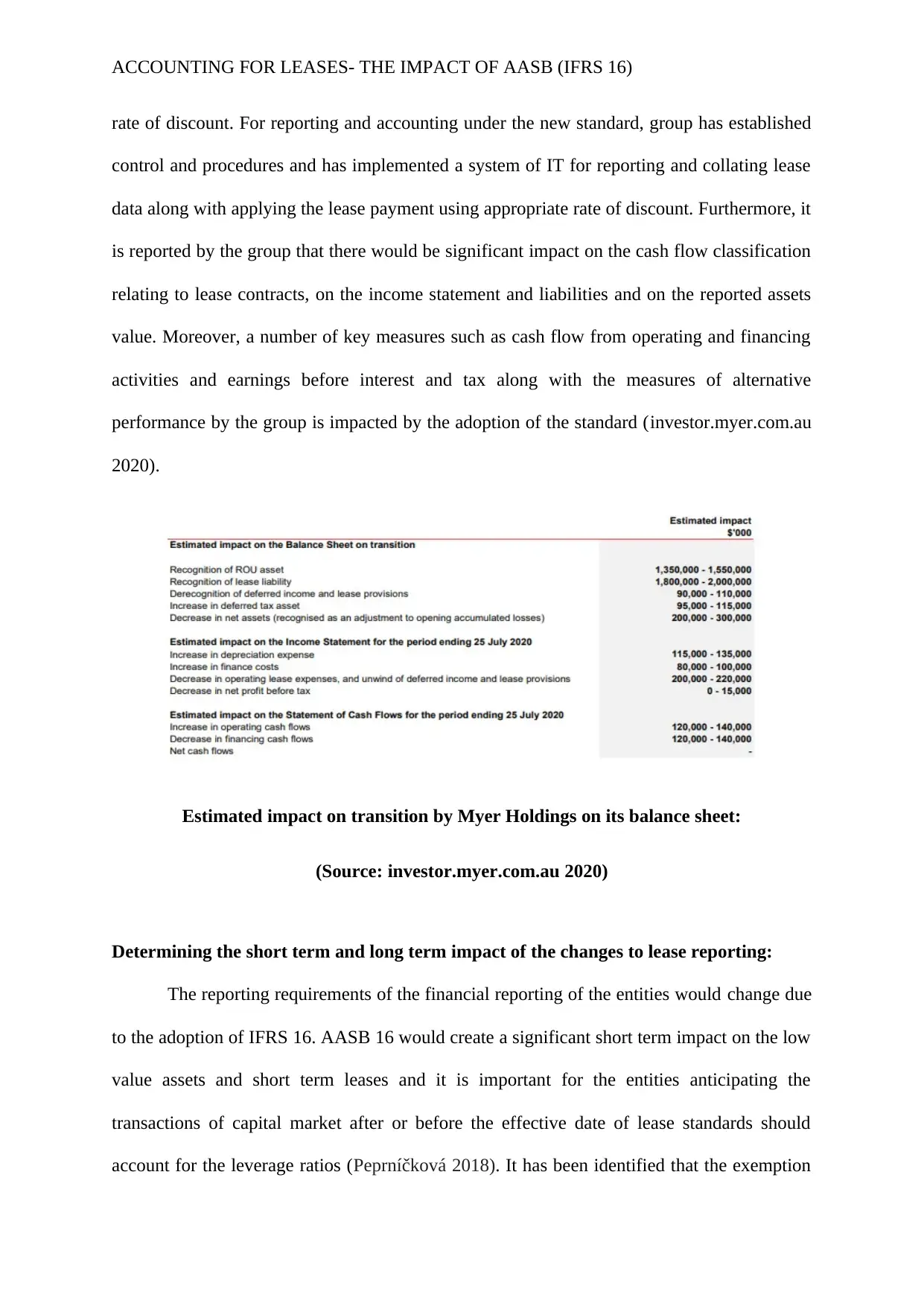

Estimated impact on transition by Myer Holdings on its balance sheet:

(Source: investor.myer.com.au 2020)

Determining the short term and long term impact of the changes to lease reporting:

The reporting requirements of the financial reporting of the entities would change due

to the adoption of IFRS 16. AASB 16 would create a significant short term impact on the low

value assets and short term leases and it is important for the entities anticipating the

transactions of capital market after or before the effective date of lease standards should

account for the leverage ratios (Peprníčková 2018). It has been identified that the exemption

rate of discount. For reporting and accounting under the new standard, group has established

control and procedures and has implemented a system of IT for reporting and collating lease

data along with applying the lease payment using appropriate rate of discount. Furthermore, it

is reported by the group that there would be significant impact on the cash flow classification

relating to lease contracts, on the income statement and liabilities and on the reported assets

value. Moreover, a number of key measures such as cash flow from operating and financing

activities and earnings before interest and tax along with the measures of alternative

performance by the group is impacted by the adoption of the standard (investor.myer.com.au

2020).

Estimated impact on transition by Myer Holdings on its balance sheet:

(Source: investor.myer.com.au 2020)

Determining the short term and long term impact of the changes to lease reporting:

The reporting requirements of the financial reporting of the entities would change due

to the adoption of IFRS 16. AASB 16 would create a significant short term impact on the low

value assets and short term leases and it is important for the entities anticipating the

transactions of capital market after or before the effective date of lease standards should

account for the leverage ratios (Peprníčková 2018). It has been identified that the exemption

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

from the short term lease and low value assets would benefit most of the entities. There

would not be any negative impact on the free cash flow as charging deprecation because it

represents a non-cash item. Short term impacts can be assessed from the valuation of leased

liabilities and assets and bringing in shift in the values recorded in the balance sheet and

income statement of the company. On other hand, long term impact of the new standard

would be identified in terms of significant changes in the financial metrics such as return on

invested capital gearing ratio. There will be an increase in the net debt with the equity value

remaining same and thereby increasing the enterprise value of the companies. The long term

impact would be identified in the valuation of discounted cash flow as it would be more

sensitive to errors, complex and presumably would result in changing the equity valuation

(Colares et al. 2018).

Conclusion:

The paper discussing the impact of accounting standard on two reporting entities of

Australia identifies that the adoption of IFRS/AASB 16 would considerably impacts the

accounting treatment relating to lease and would witness several changes to the accounts on

transition. The adoption of single lease accounting model would eliminate the distinction

between operating and financial lease and make all the leases accountable and more

transparent to the users of the financial statements of the entity. The flaws of the off balance

sheet liabilities is technically addressed under the new standard and it would contribute in

enhancing the transparency by disclosing the actual amount of the lease liabilities which was

earlier reported as operating lease in the off balance sheet and allocation of capital would

improve. However, impact can also be identified on the financial metrics of the entities

accordingly.

from the short term lease and low value assets would benefit most of the entities. There

would not be any negative impact on the free cash flow as charging deprecation because it

represents a non-cash item. Short term impacts can be assessed from the valuation of leased

liabilities and assets and bringing in shift in the values recorded in the balance sheet and

income statement of the company. On other hand, long term impact of the new standard

would be identified in terms of significant changes in the financial metrics such as return on

invested capital gearing ratio. There will be an increase in the net debt with the equity value

remaining same and thereby increasing the enterprise value of the companies. The long term

impact would be identified in the valuation of discounted cash flow as it would be more

sensitive to errors, complex and presumably would result in changing the equity valuation

(Colares et al. 2018).

Conclusion:

The paper discussing the impact of accounting standard on two reporting entities of

Australia identifies that the adoption of IFRS/AASB 16 would considerably impacts the

accounting treatment relating to lease and would witness several changes to the accounts on

transition. The adoption of single lease accounting model would eliminate the distinction

between operating and financial lease and make all the leases accountable and more

transparent to the users of the financial statements of the entity. The flaws of the off balance

sheet liabilities is technically addressed under the new standard and it would contribute in

enhancing the transparency by disclosing the actual amount of the lease liabilities which was

earlier reported as operating lease in the off balance sheet and allocation of capital would

improve. However, impact can also be identified on the financial metrics of the entities

accordingly.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

References list:

Aasb.gov.au., 2020. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 7 Apr.

2020].

Colares, A.C.V., Gomes, A.P.M., de Lima Bueno, L.C. and Pinheiro, L.E.T., 2018.

EFFECTS OF THE ADOPTION OF IFRS 16 IN THE PERFORMANCE INDICATORS OF

RENTAL ENTITIES. Revista De Gestao, Financas E Contabilidade, 8(2), pp.46-66.

Cpaaustralia.com.au., 2020. [online] Available at:

https://www.cpaaustralia.com.au/-/media/corporate/allfiles/document/professional-

resources/reporting/implementing-aasb-16-leases-report.pdf?

la=en&rev=5472e7493bb442958583f9d17a81bfe9 [Accessed 7 Apr. 2020].

Giner, B. and Pardo, F., 2018. The Value Relevance of Operating Lease Liabilities:

Economic Effects of IFRS 16. Australian Accounting Review, 28(4), pp.496-511.

Harvey Norman Holdings., 2020. Reports & Announcements — Harvey Norman Holdings.

[online] Available at: http://www.harveynormanholdings.com.au/reports-announcements-1

[Accessed 7 Apr. 2020].

References list:

Aasb.gov.au., 2020. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 7 Apr.

2020].

Colares, A.C.V., Gomes, A.P.M., de Lima Bueno, L.C. and Pinheiro, L.E.T., 2018.

EFFECTS OF THE ADOPTION OF IFRS 16 IN THE PERFORMANCE INDICATORS OF

RENTAL ENTITIES. Revista De Gestao, Financas E Contabilidade, 8(2), pp.46-66.

Cpaaustralia.com.au., 2020. [online] Available at:

https://www.cpaaustralia.com.au/-/media/corporate/allfiles/document/professional-

resources/reporting/implementing-aasb-16-leases-report.pdf?

la=en&rev=5472e7493bb442958583f9d17a81bfe9 [Accessed 7 Apr. 2020].

Giner, B. and Pardo, F., 2018. The Value Relevance of Operating Lease Liabilities:

Economic Effects of IFRS 16. Australian Accounting Review, 28(4), pp.496-511.

Harvey Norman Holdings., 2020. Reports & Announcements — Harvey Norman Holdings.

[online] Available at: http://www.harveynormanholdings.com.au/reports-announcements-1

[Accessed 7 Apr. 2020].

ACCOUNTING FOR LEASES- THE IMPACT OF AASB (IFRS 16)

Hladika, M. and Valenta, I., 2018. Analysis of the effects of applying the new IFRS 16

Leases on the financial statements. Economic and Social Development: Book of Proceedings,

pp.255-263.

Investor.myer.com.au., 2020. Myer Investor and Media Centre. [online] Available at:

http://investor.myer.com.au/Investor-Centre/ [Accessed 7 Apr. 2020].

Magli, F., Nobolo, A. and Ogliari, M., 2018. The Effects on Financial Leverage and

Performance: The IFRS 16. International Business Research, 11(8), pp.76-89.

Morales Díaz, J. and Zamora Ramírez, C., 2018. IFRS 16 (leases) implementation: Impact of

entities’ decisions on financial statements. Aestimatio: The IEB International Journal of

Finance, 17, 60-97.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. The impact of IFRS 16 on key financial

ratios: a new methodological approach. Accounting in Europe, 15(1), pp.105-133.

Patricia Stebbens, M., 2020. AASB 16 Check: Impact on small proprietary companies.

[online] KPMG. Available at: https://home.kpmg/au/en/home/insights/2019/02/aasb-16-

check-small-proprietary-companies.html [Accessed 7 Apr. 2020].

Peprníčková, M., 2018. What Are the Origins of New Leasing Conceptual Models and How

These Models Are Coming True in IFRS 16?. In The Impact of Globalization on

International Finance and Accounting (pp. 291-299). Springer, Cham.

Pwc.com.au., 2020. [online] Available at:

https://www.pwc.com.au/assurance/ifrs/assets/new-leasing-standard-and-retailers.pdf

[Accessed 7 Apr. 2020].

Pwc.in., 2020. [online] Available at: https://www.pwc.in/assets/pdfs/services/accounting-

advisory/a-study-on-the-impact-of-lease-capitalisation.pdf [Accessed 7 Apr. 2020].

Hladika, M. and Valenta, I., 2018. Analysis of the effects of applying the new IFRS 16

Leases on the financial statements. Economic and Social Development: Book of Proceedings,

pp.255-263.

Investor.myer.com.au., 2020. Myer Investor and Media Centre. [online] Available at:

http://investor.myer.com.au/Investor-Centre/ [Accessed 7 Apr. 2020].

Magli, F., Nobolo, A. and Ogliari, M., 2018. The Effects on Financial Leverage and

Performance: The IFRS 16. International Business Research, 11(8), pp.76-89.

Morales Díaz, J. and Zamora Ramírez, C., 2018. IFRS 16 (leases) implementation: Impact of

entities’ decisions on financial statements. Aestimatio: The IEB International Journal of

Finance, 17, 60-97.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. The impact of IFRS 16 on key financial

ratios: a new methodological approach. Accounting in Europe, 15(1), pp.105-133.

Patricia Stebbens, M., 2020. AASB 16 Check: Impact on small proprietary companies.

[online] KPMG. Available at: https://home.kpmg/au/en/home/insights/2019/02/aasb-16-

check-small-proprietary-companies.html [Accessed 7 Apr. 2020].

Peprníčková, M., 2018. What Are the Origins of New Leasing Conceptual Models and How

These Models Are Coming True in IFRS 16?. In The Impact of Globalization on

International Finance and Accounting (pp. 291-299). Springer, Cham.

Pwc.com.au., 2020. [online] Available at:

https://www.pwc.com.au/assurance/ifrs/assets/new-leasing-standard-and-retailers.pdf

[Accessed 7 Apr. 2020].

Pwc.in., 2020. [online] Available at: https://www.pwc.in/assets/pdfs/services/accounting-

advisory/a-study-on-the-impact-of-lease-capitalisation.pdf [Accessed 7 Apr. 2020].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.