Accounting for Management Decisions

VerifiedAdded on 2023/06/03

|10

|2481

|306

AI Summary

This text covers topics such as breakeven analysis, accounting rate of return, cash flow statements, and liquidity analysis. It provides explanations, calculations, and recommendations for each topic. The subject is Accounting for Management Decisions and the course code is not mentioned. The college/university is not mentioned either.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING FOR MANAGEMENT DECISIONS

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 1

(a) Let the breakeven agency monthly revenue be $ X

Monthly Variable Costs

Sales staff Commission = (55/100)*X = 0.55X

Supplies & Printing = (12/100)*X = 0.12X

Usage costs for phones & computers = (9/100)*X = 0.09X

Total variable costs = 0.55X + 0.12X + 0.09X = 0.76X

Monthly Fixed Costs

Office rent = $ 4,000

Electricity = $ 700

Multi-line telephone system = $ 600

Computer Cabling Connection = $400

Salary of office manager = $ 8,500

Office furniture depreciation = $ 500

Total fixed costs = 4000 + 700 + 600 + 400 + 8500 + 500 = $ 14,700

Break even Analysis

For break even, Revenue = Costs

Hence, X = 0.76X + 14700

Solving the above, we get X = $ 61,250

Thus, to break even the agency must generate monthly revenue of $ 61,250.

(b) Intended monthly net profit (Assumed before tax) = $ 15,000

Profit = Revenue – Total Costs

Let the requisite monthly revenue be $ Y

(a) Let the breakeven agency monthly revenue be $ X

Monthly Variable Costs

Sales staff Commission = (55/100)*X = 0.55X

Supplies & Printing = (12/100)*X = 0.12X

Usage costs for phones & computers = (9/100)*X = 0.09X

Total variable costs = 0.55X + 0.12X + 0.09X = 0.76X

Monthly Fixed Costs

Office rent = $ 4,000

Electricity = $ 700

Multi-line telephone system = $ 600

Computer Cabling Connection = $400

Salary of office manager = $ 8,500

Office furniture depreciation = $ 500

Total fixed costs = 4000 + 700 + 600 + 400 + 8500 + 500 = $ 14,700

Break even Analysis

For break even, Revenue = Costs

Hence, X = 0.76X + 14700

Solving the above, we get X = $ 61,250

Thus, to break even the agency must generate monthly revenue of $ 61,250.

(b) Intended monthly net profit (Assumed before tax) = $ 15,000

Profit = Revenue – Total Costs

Let the requisite monthly revenue be $ Y

15000 = Y- 0.76Y -14700

Solving the above, we get Y = $ 123,750

(c) Commission made by the real estate agent is 6% of the gross property sales

Hence, if the real estate agency has to earn $ 15,000 in pre-tax profits, then the property sales should

be such that the commission revenue generated must be $ 123,750.

Let the gross property sales be $ Z

Hence, (6/100)*Z = $ 123,750

Solving the above, Z = $2,062,500

(d) The CVP analysis is based on certain assumptions which are satisfied in the given case. One of the

key assumptions is that the sale price, variable cost per unit and fixed cost would remain constant.

Clearly, this is true for the given business where commission is a fixed percentage of the gross

property sale and all the variable costs are constant functions of the revenue of agency. Further, the

revenue and cost functions are linear as is apparent from the description. Also, there is no issue of any

dynamic product mix owing to which the contribution margin for the business can be assumed to

remain constant (Drury, 2016).

Question 2

(a) Accounting rate of return

The tax rate has been assumed as 30%

This method involves calculating the average profit for the investment.

Project A (Investment) = $ 250,000

Project A (Average annual profit) = [175000-(250000/5)]*0.7 = $ 87,500

Project A (Accounting rate of return) = (87500/250000) = 35%

Project B (Investment) = $ 1,000,000

Project B (Average annual profit) = [300000-(1000000/5)]*0.7 = $ 70,000

Solving the above, we get Y = $ 123,750

(c) Commission made by the real estate agent is 6% of the gross property sales

Hence, if the real estate agency has to earn $ 15,000 in pre-tax profits, then the property sales should

be such that the commission revenue generated must be $ 123,750.

Let the gross property sales be $ Z

Hence, (6/100)*Z = $ 123,750

Solving the above, Z = $2,062,500

(d) The CVP analysis is based on certain assumptions which are satisfied in the given case. One of the

key assumptions is that the sale price, variable cost per unit and fixed cost would remain constant.

Clearly, this is true for the given business where commission is a fixed percentage of the gross

property sale and all the variable costs are constant functions of the revenue of agency. Further, the

revenue and cost functions are linear as is apparent from the description. Also, there is no issue of any

dynamic product mix owing to which the contribution margin for the business can be assumed to

remain constant (Drury, 2016).

Question 2

(a) Accounting rate of return

The tax rate has been assumed as 30%

This method involves calculating the average profit for the investment.

Project A (Investment) = $ 250,000

Project A (Average annual profit) = [175000-(250000/5)]*0.7 = $ 87,500

Project A (Accounting rate of return) = (87500/250000) = 35%

Project B (Investment) = $ 1,000,000

Project B (Average annual profit) = [300000-(1000000/5)]*0.7 = $ 70,000

Project B (Accounting rate of return) = (70,000/1000000) = 7%

Project C (Investment) = $ 500,000

Project C (Average annual profit) = [200000-(500000/5)]*0.7 = $ 70,000

Project C (Accounting rate of return) = (70000/500000) = 14%

Payback Period

Project A (Investment) = $ 250,000

Project A (Annual cash inflows) = 175000*0.7 + (250000/5)*0.3 = $137,500

Project A (Payback period) = 1+ (112500/137500) = 1.82 years

Project B (Investment) = $ 1,000,000

Project B (Annual cash inflows) = 300000*0.7 + (1000000/5)*0.3 = $270,000

Project B (Payback period) = 3+ (190000/270000) = 2.70 years

Project C (Investment) = $ 500,000

Project C (Annual cash inflows) = 200000*0.7 + (500000/5)*0.3 = $170,000

Project C (Payback period) = 2+ (160000/170000) = 2.94 years

Net Present Value

Project A (Investment) = $ 250,000

Project A (Annual cash inflows) = 175000*0.7 + (250000/5)*0.3 = $137,500

Project A (NPV) = -250000 + 137500 (0.877+ 0.769+ 0.675+ 0.592 +0.519) = $ 221,900

Project B (Investment) = $ 1,000,000

Project B (Annual cash inflows) = 300000*0.7 + (1000000/5)*0.3 = $270,000

Project B (NPV) = -1,000,000 + 270,000 (0.877+ 0.769+ 0.675+ 0.592 +0.519) = -$ 73,360

Project C (Investment) = $ 500,000

Project C (Investment) = $ 500,000

Project C (Average annual profit) = [200000-(500000/5)]*0.7 = $ 70,000

Project C (Accounting rate of return) = (70000/500000) = 14%

Payback Period

Project A (Investment) = $ 250,000

Project A (Annual cash inflows) = 175000*0.7 + (250000/5)*0.3 = $137,500

Project A (Payback period) = 1+ (112500/137500) = 1.82 years

Project B (Investment) = $ 1,000,000

Project B (Annual cash inflows) = 300000*0.7 + (1000000/5)*0.3 = $270,000

Project B (Payback period) = 3+ (190000/270000) = 2.70 years

Project C (Investment) = $ 500,000

Project C (Annual cash inflows) = 200000*0.7 + (500000/5)*0.3 = $170,000

Project C (Payback period) = 2+ (160000/170000) = 2.94 years

Net Present Value

Project A (Investment) = $ 250,000

Project A (Annual cash inflows) = 175000*0.7 + (250000/5)*0.3 = $137,500

Project A (NPV) = -250000 + 137500 (0.877+ 0.769+ 0.675+ 0.592 +0.519) = $ 221,900

Project B (Investment) = $ 1,000,000

Project B (Annual cash inflows) = 300000*0.7 + (1000000/5)*0.3 = $270,000

Project B (NPV) = -1,000,000 + 270,000 (0.877+ 0.769+ 0.675+ 0.592 +0.519) = -$ 73,360

Project C (Investment) = $ 500,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Project C (Annual cash inflows) = 200000*0.7 + (500000/5)*0.3 = $170,000

Project C (NPV) = -500000 + 170000 (0.877+ 0.769+ 0.675+ 0.592 +0.519) = $ 83,440

(b) The best investment would be project A since it has the highest ARR, lowest payback period and

highest positive NPV. The next in line would be project C which has a positive NPV. This ranking is

not supported by payback period and ARR since both those measures fail to take the time value of

money in consideration. Project B is not feasible and hence rejected owing to the NPV being negative

(Parrino and Kidwell, 2014).

(c) Besides NPV also, there are several other alternative techniques of project analysis and capital

budgeting. The various advantages of NPV are indicated below (Arnold, 2015).

It considers the time value of money into cognizance which is essentially considering the fact

that money has opportunity cost. ARR, payback period fail to consider this.

NPV considers the cash flows of the project over the complete project life unlike payback

period which considers cash flows till the achieving of break even.

Also, NPV is very useful in reliable ranking of different projects.

The various shortcomings of NPV are listed below (Petty et. al., 2015).

NPV computation is quite sensitive to discount rate and hence it needs to be computed

accurately which is not easy.

Forecasting of the future cash flows especially over a longer period can be quite challenging

and often unreliable.

People lacking finance background find difficulty in interpreting this.

Question 3

(a) The requisite reasons are as indicated below (Bhimani et. al., 2017).

The cost of sales as reflected in the accrual income statement is only $ 850,000. In

comparison, the actual amount that has been given to suppliers during the year is 1,610,000

which is leading to operational cash flow being negative.

In the income statement, the sales are reported as $ 1,800,000 whereas the corresponding cash

receipts in cash flow statement are significantly lower at $ 1,330,000.

In the income statement, the other expenses are $ 22,000. In sharp contrast, the corresponding

payment to these other expenses during the year is $ 112,000 which is leading to cash flow

from operations being negative.

Project C (NPV) = -500000 + 170000 (0.877+ 0.769+ 0.675+ 0.592 +0.519) = $ 83,440

(b) The best investment would be project A since it has the highest ARR, lowest payback period and

highest positive NPV. The next in line would be project C which has a positive NPV. This ranking is

not supported by payback period and ARR since both those measures fail to take the time value of

money in consideration. Project B is not feasible and hence rejected owing to the NPV being negative

(Parrino and Kidwell, 2014).

(c) Besides NPV also, there are several other alternative techniques of project analysis and capital

budgeting. The various advantages of NPV are indicated below (Arnold, 2015).

It considers the time value of money into cognizance which is essentially considering the fact

that money has opportunity cost. ARR, payback period fail to consider this.

NPV considers the cash flows of the project over the complete project life unlike payback

period which considers cash flows till the achieving of break even.

Also, NPV is very useful in reliable ranking of different projects.

The various shortcomings of NPV are listed below (Petty et. al., 2015).

NPV computation is quite sensitive to discount rate and hence it needs to be computed

accurately which is not easy.

Forecasting of the future cash flows especially over a longer period can be quite challenging

and often unreliable.

People lacking finance background find difficulty in interpreting this.

Question 3

(a) The requisite reasons are as indicated below (Bhimani et. al., 2017).

The cost of sales as reflected in the accrual income statement is only $ 850,000. In

comparison, the actual amount that has been given to suppliers during the year is 1,610,000

which is leading to operational cash flow being negative.

In the income statement, the sales are reported as $ 1,800,000 whereas the corresponding cash

receipts in cash flow statement are significantly lower at $ 1,330,000.

In the income statement, the other expenses are $ 22,000. In sharp contrast, the corresponding

payment to these other expenses during the year is $ 112,000 which is leading to cash flow

from operations being negative.

(b) The performance is more accurately reflected by the income statement since it is based on accrual

basis. The accrual basis considers the revenue that is earned from the business operations and also

considers the various expenses incurred in this process. The actual cash flow may have a lag and the

same presents a distorted picture as the effect of transactions in multiple periods is captured in the

cash flow statement. Hence, accrual system based income statement is more representative of

financial performance (Heisinger, 2014).

(c) Balance sheet highlights the financial position of the company and provides information about the

asset and liabilities outstanding on a given date for the company. It provides information about capital

structure, liquidity and solvency. The income statement is reflective of the profitability of the

operations and hence indicates the profits generated by the company during the given year. The cash

flow statement is prepared on cash basis and highlights the transactions in cash that take place to

reflect the closing cash balance (Arnold, 2015).

Question 4

(a) Based on the given data, it is apparent that the accounts receivable days have surged during the

period at a rate which is significantly higher than the industry average. This indicates difficulty on the

company’s part in collection of receivables arising from credit based sales. The effect of this is

witnessed on the cash cycle which becomes longer and hence leads to working capital requirement

increase (Petty et. al., 2015).

With regards to inventory days, the trend is similar to that which has been witnessed for the accounts

receivable days. Also, consideration needs to be given to the continuously rising closing inventory

balance which is indicative of the lack of demand for the products of the company which leads to

rising inventory and lower sales for the business (Parrino & Kidwell, 2014). The accounts payable

days for the company are on the rise which potentially can imply lowering cash cycle and limited

working capital requirements. But, in this case considering the rising accounts payable balance

coupled with the decreasing cash balance, it seems likely that the company is facing a severe cash

crunch and thereby delaying the payment to the suppliers (Damodaran, 2015).

On the basis of the above, it is apparent that the company currently is facing a short term liquidity

crunch which is negatively impacting the company’s operations and the severity of the issue can be

gauged from the fact that at FY2017 end, the cash balance for the company stood at $ 5,000 only

(Arnold, 2015).

(b) The various actions that need to be urgently taken by the company to improve the situation are

outlined as follows.

basis. The accrual basis considers the revenue that is earned from the business operations and also

considers the various expenses incurred in this process. The actual cash flow may have a lag and the

same presents a distorted picture as the effect of transactions in multiple periods is captured in the

cash flow statement. Hence, accrual system based income statement is more representative of

financial performance (Heisinger, 2014).

(c) Balance sheet highlights the financial position of the company and provides information about the

asset and liabilities outstanding on a given date for the company. It provides information about capital

structure, liquidity and solvency. The income statement is reflective of the profitability of the

operations and hence indicates the profits generated by the company during the given year. The cash

flow statement is prepared on cash basis and highlights the transactions in cash that take place to

reflect the closing cash balance (Arnold, 2015).

Question 4

(a) Based on the given data, it is apparent that the accounts receivable days have surged during the

period at a rate which is significantly higher than the industry average. This indicates difficulty on the

company’s part in collection of receivables arising from credit based sales. The effect of this is

witnessed on the cash cycle which becomes longer and hence leads to working capital requirement

increase (Petty et. al., 2015).

With regards to inventory days, the trend is similar to that which has been witnessed for the accounts

receivable days. Also, consideration needs to be given to the continuously rising closing inventory

balance which is indicative of the lack of demand for the products of the company which leads to

rising inventory and lower sales for the business (Parrino & Kidwell, 2014). The accounts payable

days for the company are on the rise which potentially can imply lowering cash cycle and limited

working capital requirements. But, in this case considering the rising accounts payable balance

coupled with the decreasing cash balance, it seems likely that the company is facing a severe cash

crunch and thereby delaying the payment to the suppliers (Damodaran, 2015).

On the basis of the above, it is apparent that the company currently is facing a short term liquidity

crunch which is negatively impacting the company’s operations and the severity of the issue can be

gauged from the fact that at FY2017 end, the cash balance for the company stood at $ 5,000 only

(Arnold, 2015).

(b) The various actions that need to be urgently taken by the company to improve the situation are

outlined as follows.

There is a need to bring down the accounts receivable days. This can be enabled by extending

attractive discounts to those customers who pay in cash instead of credit or make early

payment. The concern of this strategy is in the form of shrinking margins but it should prove

effective for resolving the liquidity crisis (Damodaran, 2015).

There is a need to reduce the inventory turnover days. The inventory is continuously piling

owing to the company’s inability to generate sales. Lucrative discounts should be given on the

inventory so that this could be converted into cash. The concern of this strategy is in the form

of shrinking margins but it should prove effective for resolving the liquidity crisis (Petty et.

al., 2015).

Even though accounts payables days have increased but this increase is not because of

favourable terms from suppliers but delay in payments. The company should make efforts to

provide payments to as many suppliers as possible so as not to default on any payment.

Further, for those suppliers for whom payment would be delayed, some financial incentive

should be provided (Parrino and Kidwell, 2014).

Question 5(a)

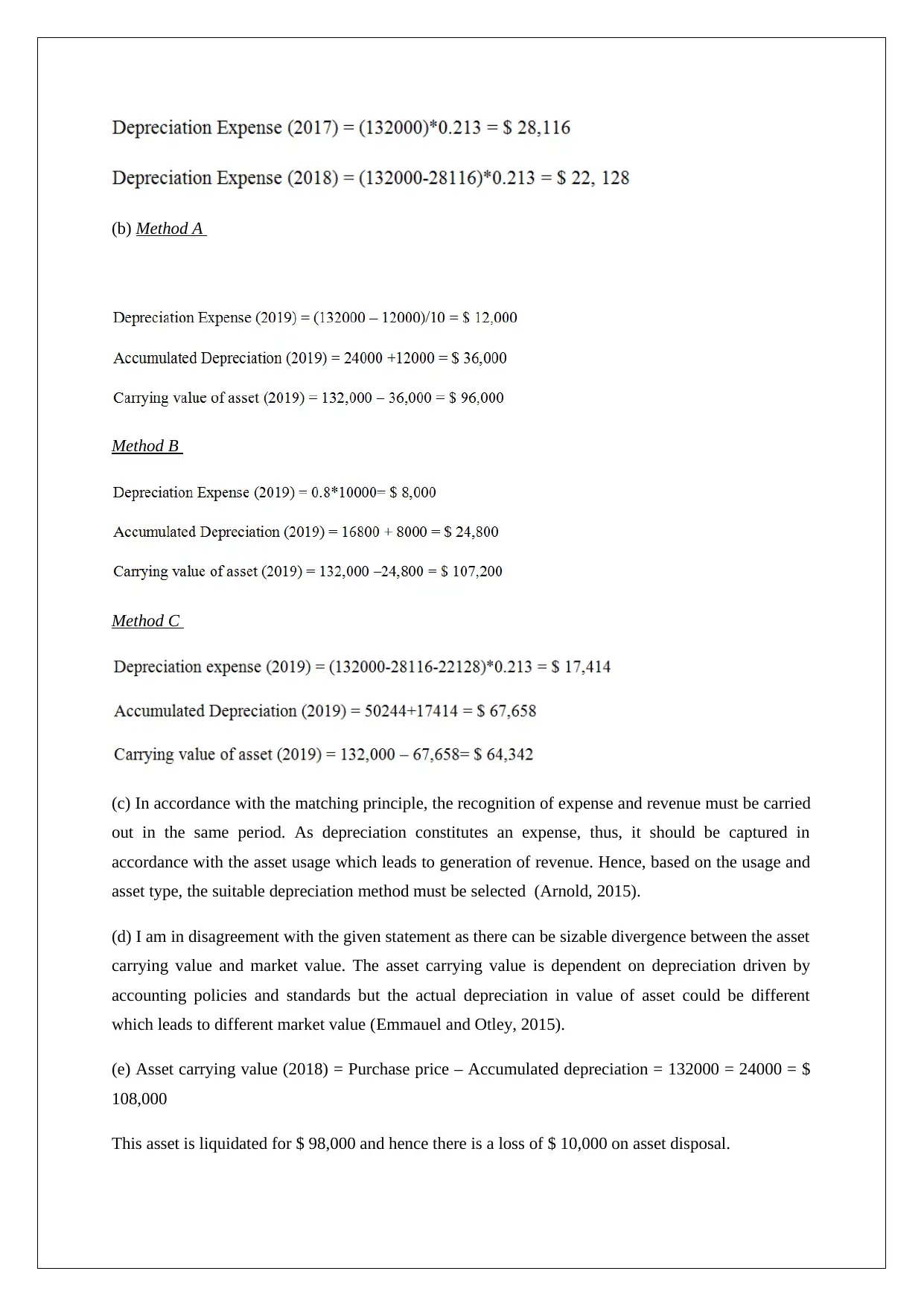

(a) Method A = Straight line depreciation

Reasoning: Depreciation remains same in 2017 and 2018

Method B = Units of production depreciation

Reasoning: Depreciation increases in 2018 and so does the production

Method C = Declining balance depreciation

Reasoning: 2017 has the higher depreciation while the depreciation expense for 2018 is lower

attractive discounts to those customers who pay in cash instead of credit or make early

payment. The concern of this strategy is in the form of shrinking margins but it should prove

effective for resolving the liquidity crisis (Damodaran, 2015).

There is a need to reduce the inventory turnover days. The inventory is continuously piling

owing to the company’s inability to generate sales. Lucrative discounts should be given on the

inventory so that this could be converted into cash. The concern of this strategy is in the form

of shrinking margins but it should prove effective for resolving the liquidity crisis (Petty et.

al., 2015).

Even though accounts payables days have increased but this increase is not because of

favourable terms from suppliers but delay in payments. The company should make efforts to

provide payments to as many suppliers as possible so as not to default on any payment.

Further, for those suppliers for whom payment would be delayed, some financial incentive

should be provided (Parrino and Kidwell, 2014).

Question 5(a)

(a) Method A = Straight line depreciation

Reasoning: Depreciation remains same in 2017 and 2018

Method B = Units of production depreciation

Reasoning: Depreciation increases in 2018 and so does the production

Method C = Declining balance depreciation

Reasoning: 2017 has the higher depreciation while the depreciation expense for 2018 is lower

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b) Method A

Method B

Method C

(c) In accordance with the matching principle, the recognition of expense and revenue must be carried

out in the same period. As depreciation constitutes an expense, thus, it should be captured in

accordance with the asset usage which leads to generation of revenue. Hence, based on the usage and

asset type, the suitable depreciation method must be selected (Arnold, 2015).

(d) I am in disagreement with the given statement as there can be sizable divergence between the asset

carrying value and market value. The asset carrying value is dependent on depreciation driven by

accounting policies and standards but the actual depreciation in value of asset could be different

which leads to different market value (Emmauel and Otley, 2015).

(e) Asset carrying value (2018) = Purchase price – Accumulated depreciation = 132000 = 24000 = $

108,000

This asset is liquidated for $ 98,000 and hence there is a loss of $ 10,000 on asset disposal.

Method B

Method C

(c) In accordance with the matching principle, the recognition of expense and revenue must be carried

out in the same period. As depreciation constitutes an expense, thus, it should be captured in

accordance with the asset usage which leads to generation of revenue. Hence, based on the usage and

asset type, the suitable depreciation method must be selected (Arnold, 2015).

(d) I am in disagreement with the given statement as there can be sizable divergence between the asset

carrying value and market value. The asset carrying value is dependent on depreciation driven by

accounting policies and standards but the actual depreciation in value of asset could be different

which leads to different market value (Emmauel and Otley, 2015).

(e) Asset carrying value (2018) = Purchase price – Accumulated depreciation = 132000 = 24000 = $

108,000

This asset is liquidated for $ 98,000 and hence there is a loss of $ 10,000 on asset disposal.

Asset change = Increase in cash (98,000) = Decrease in non-current assets (108,000) = -$ 10,000

The liabilities would not change. Further, the loss on the sale would be reflected in the equity which

would be decreased by $ 10,000 and hence lead to the accounting equation balancing.

References

The liabilities would not change. Further, the loss on the sale would be reflected in the equity which

would be decreased by $ 10,000 and hence lead to the accounting equation balancing.

References

Arnold, G. (2015) Corporate Financial Management. 3rd ed. Sydney: Financial Times Management.

Bhimani, A., Horngren, C.T., Datar, S.M. and Foster, G. (2017), Management and Cost Accounting

4th ed. Harlow: Prentice Hall/Financial Times

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York: Wiley, John

& Sons.

Drury, C. (2016) Cost and Management Accounting: An Introduction. 6th ed. New York: Cengage

Learning

Emmauel, R.C. and Otley, T.D. (2015) Accounting for Management Control. 8th ed. London: Cengage

Learning.

Heisinger, K.(2014) Essentials of Managerial Accounting 4th ed. London: Cengage Learning.

Parrino, R. & Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London: Wiley

Publications

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., & Nguyen, H. (2015).

Financial Management, Principles and Applications, 6th ed.. NSW: Pearson Education, French Forest

Australia

Bhimani, A., Horngren, C.T., Datar, S.M. and Foster, G. (2017), Management and Cost Accounting

4th ed. Harlow: Prentice Hall/Financial Times

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York: Wiley, John

& Sons.

Drury, C. (2016) Cost and Management Accounting: An Introduction. 6th ed. New York: Cengage

Learning

Emmauel, R.C. and Otley, T.D. (2015) Accounting for Management Control. 8th ed. London: Cengage

Learning.

Heisinger, K.(2014) Essentials of Managerial Accounting 4th ed. London: Cengage Learning.

Parrino, R. & Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London: Wiley

Publications

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., & Nguyen, H. (2015).

Financial Management, Principles and Applications, 6th ed.. NSW: Pearson Education, French Forest

Australia

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.