SCU - ACC00724 Accounting for Managers: Financial Performance

VerifiedAdded on 2023/06/08

|11

|1159

|68

Homework Assignment

AI Summary

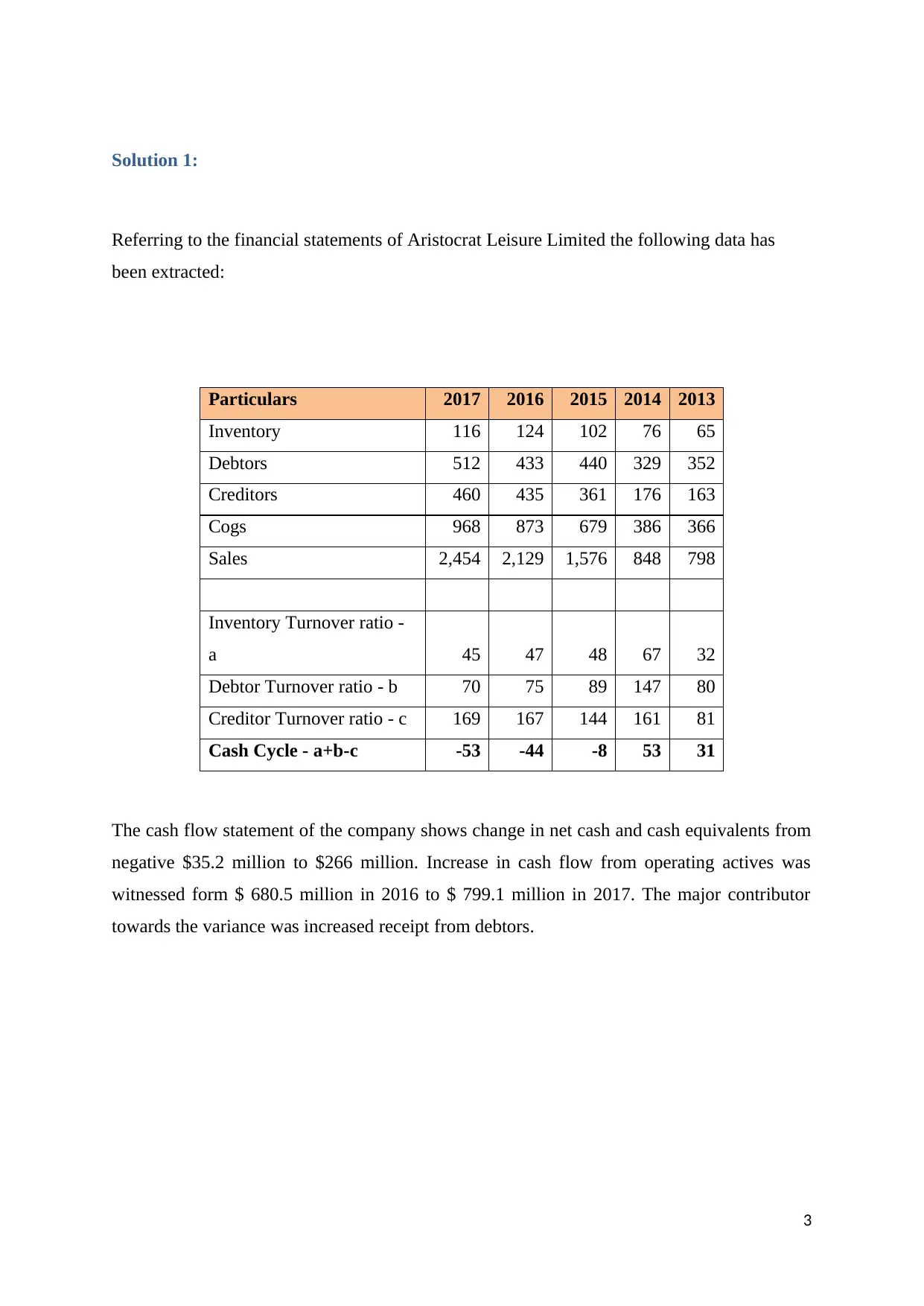

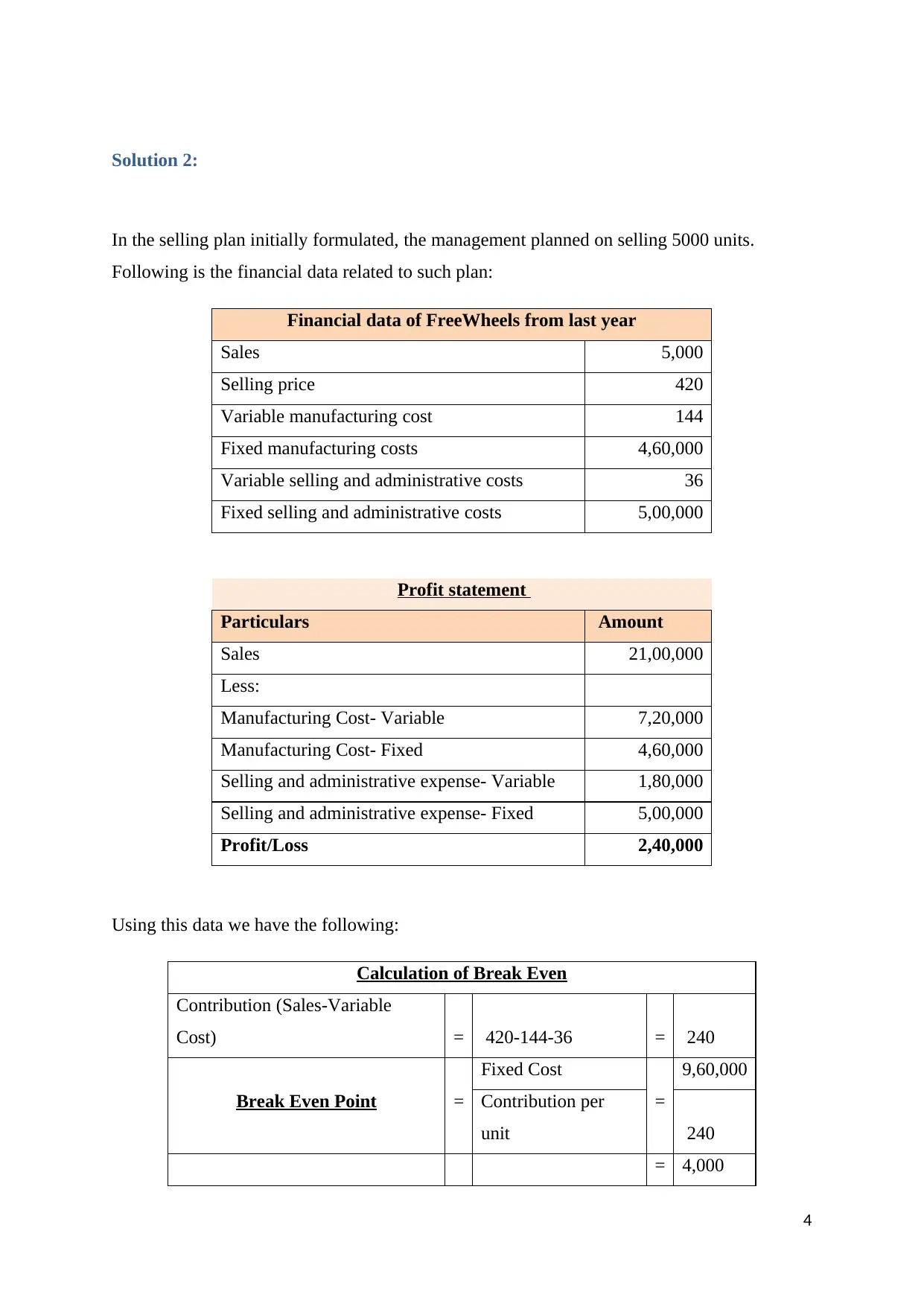

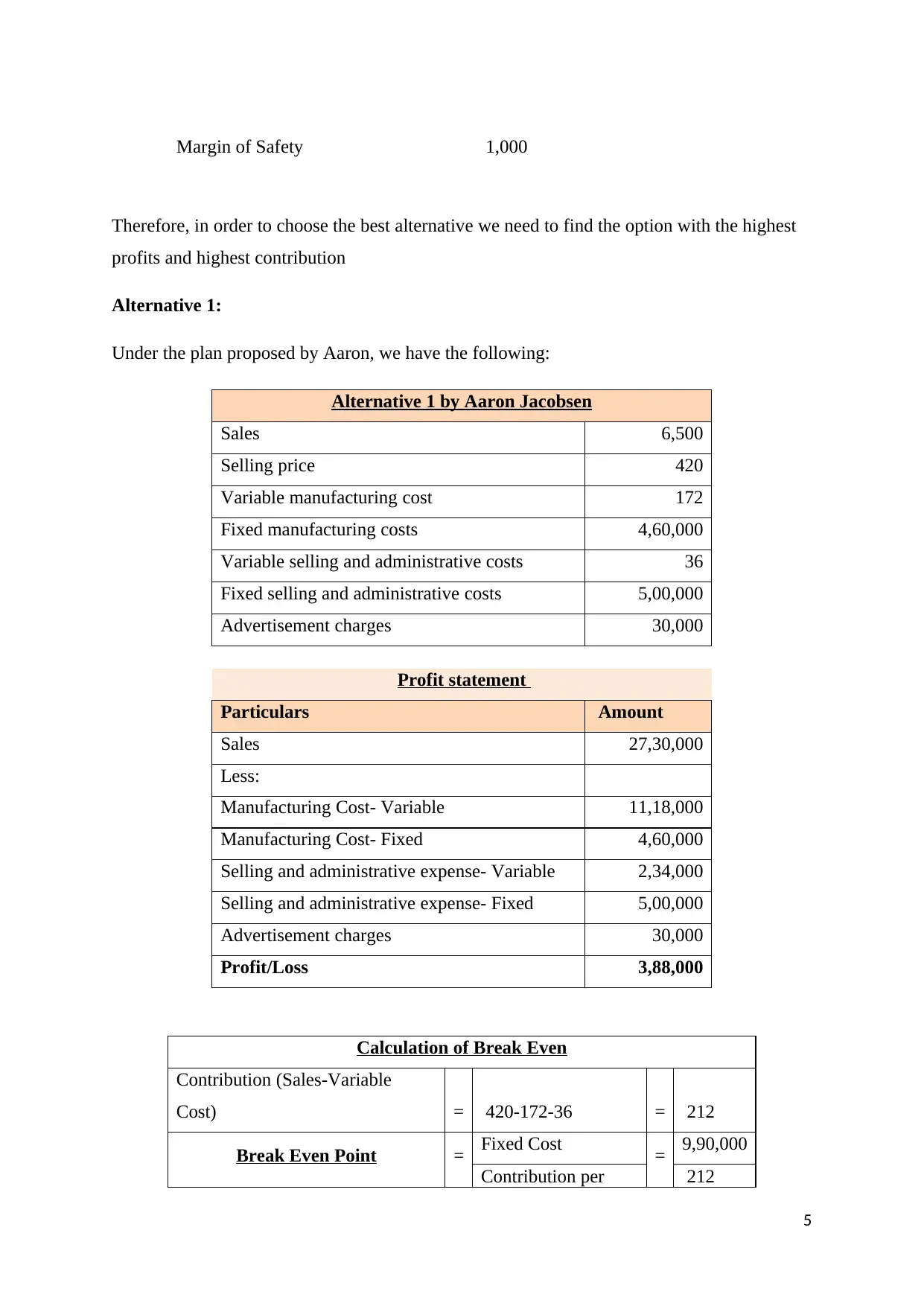

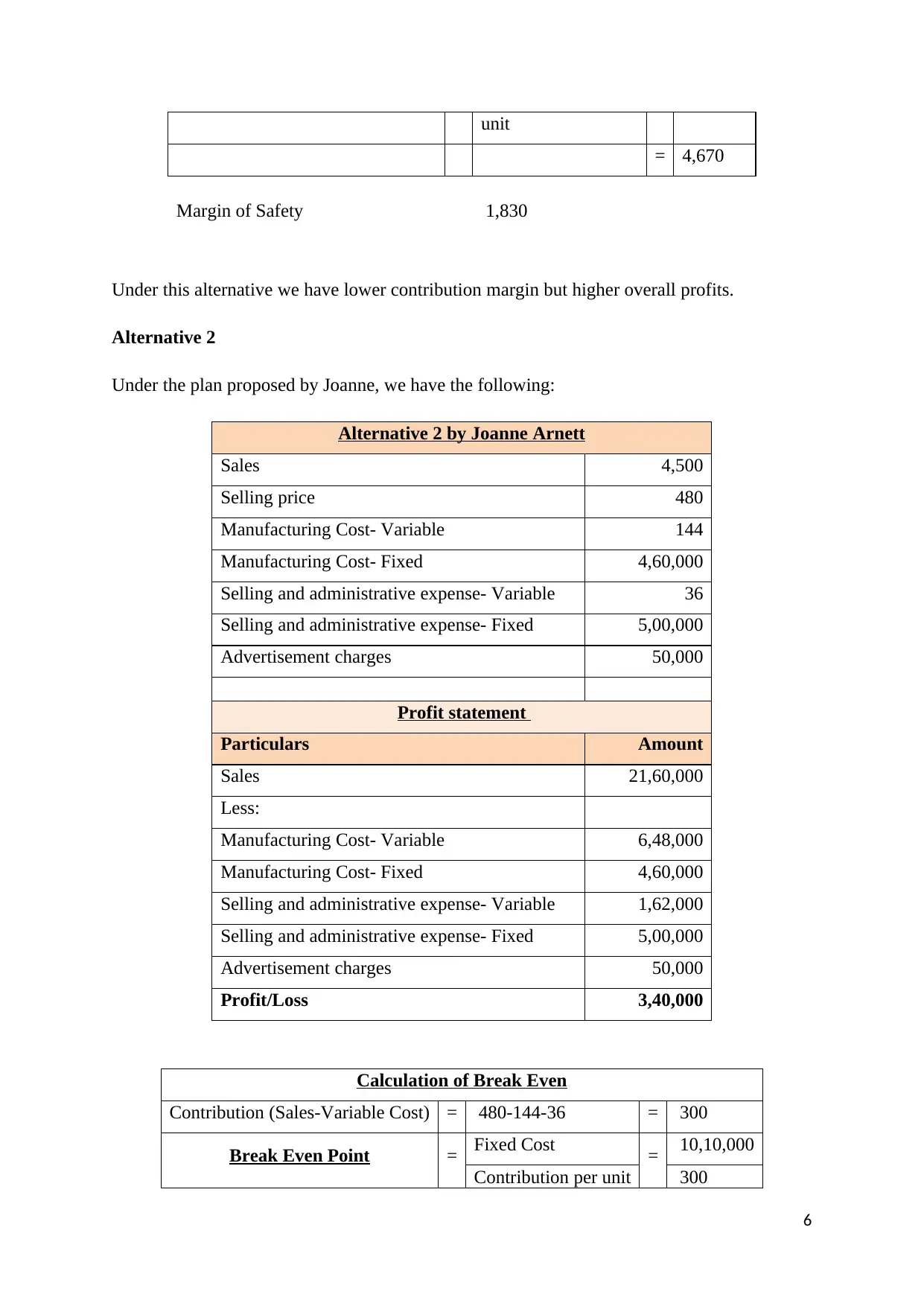

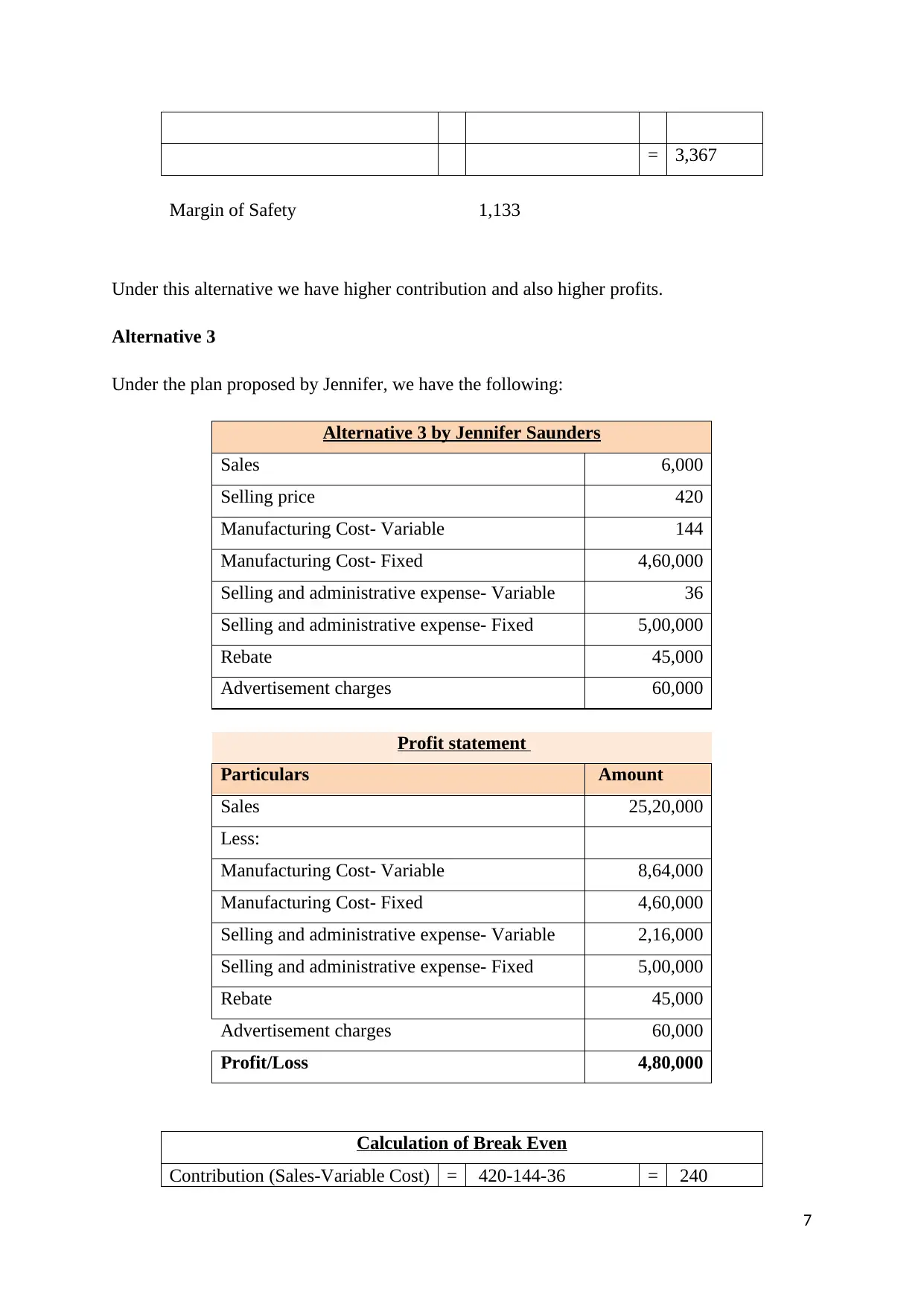

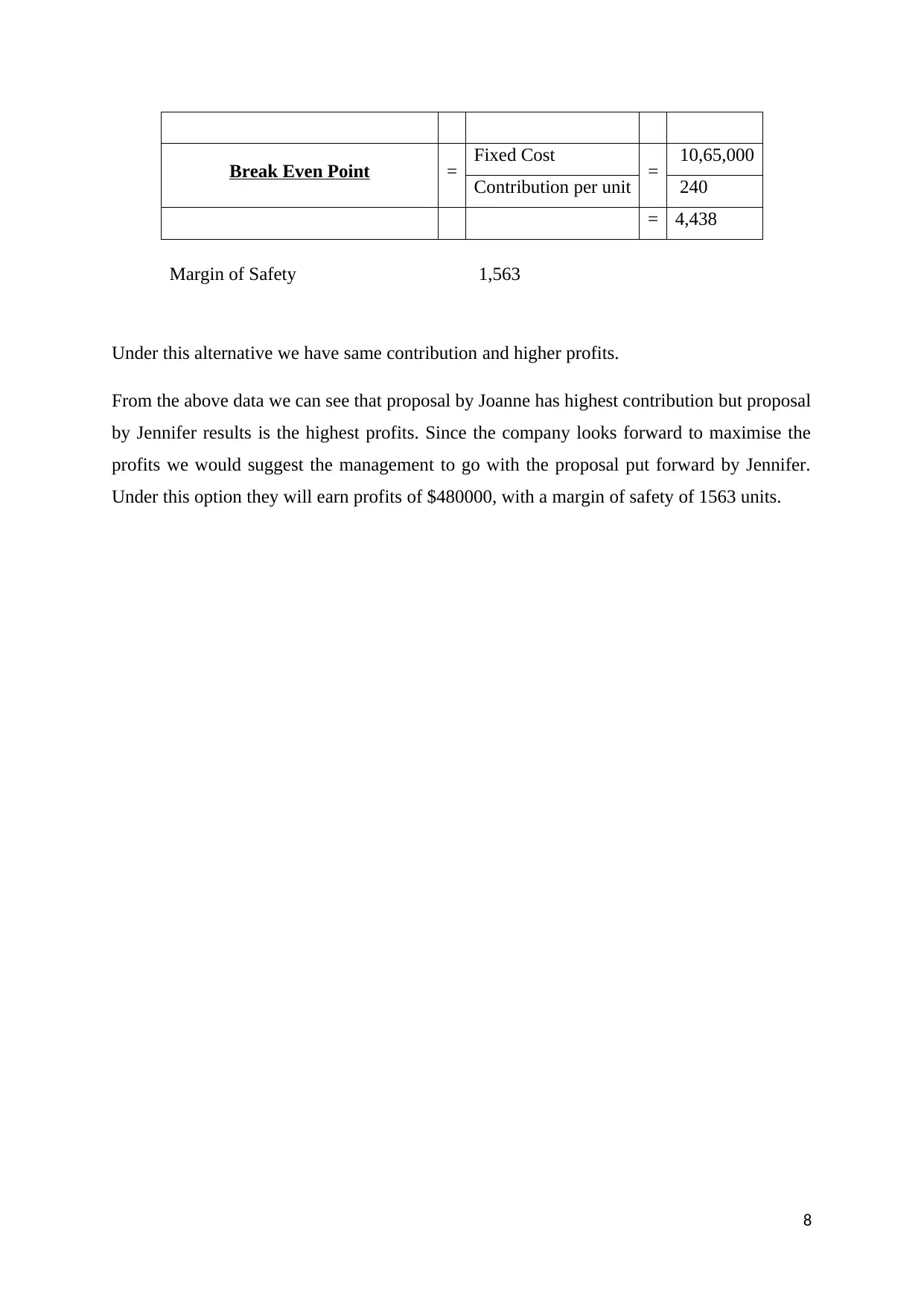

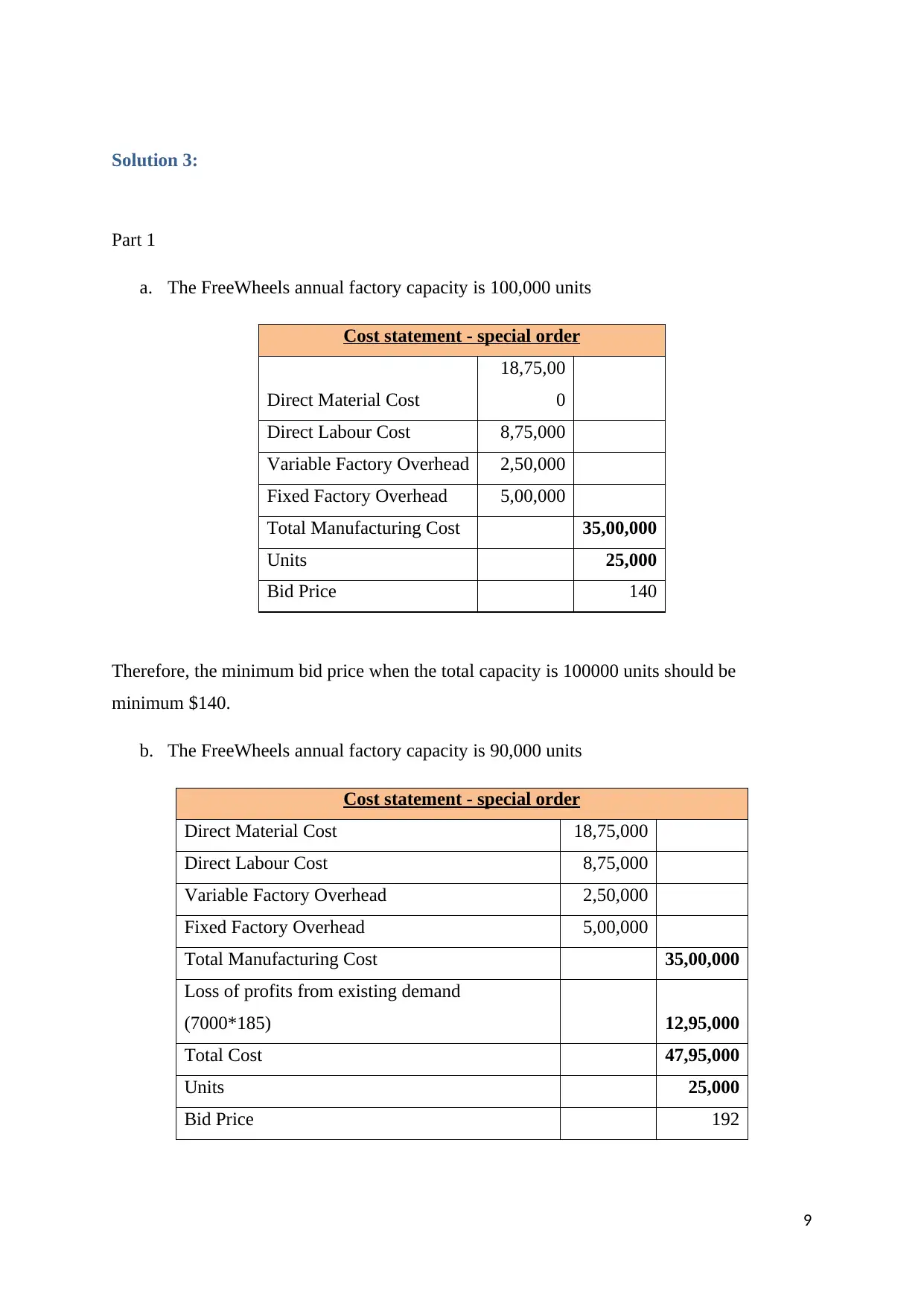

This assignment solution for ACC00724 Accounting for Managers includes a detailed financial analysis of Aristocrat Leisure Limited, focusing on key ratios such as debtor turnover, creditor turnover, and cash cycle. It also explores break-even analysis and profit maximization strategies for FreeWheels, evaluating different proposals to determine the most profitable option. Furthermore, the assignment addresses special order costing, calculating minimum bid prices based on varying production capacities and demand scenarios. The analysis incorporates variable and fixed costs to provide comprehensive recommendations for managerial decision-making.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.