Accounting Fundamentals in Business Management - Desklib

VerifiedAdded on 2023/06/18

|12

|2312

|292

AI Summary

This report covers the accounting fundamentals present in business management. It includes financial statements, balance sheets, and ratio analysis. The report explains why financial statement balances are always equal and interprets the ratio analysis. The subject is Accounting Fundamentals and Business Management, and the course code and college/university are not mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................4

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................4

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

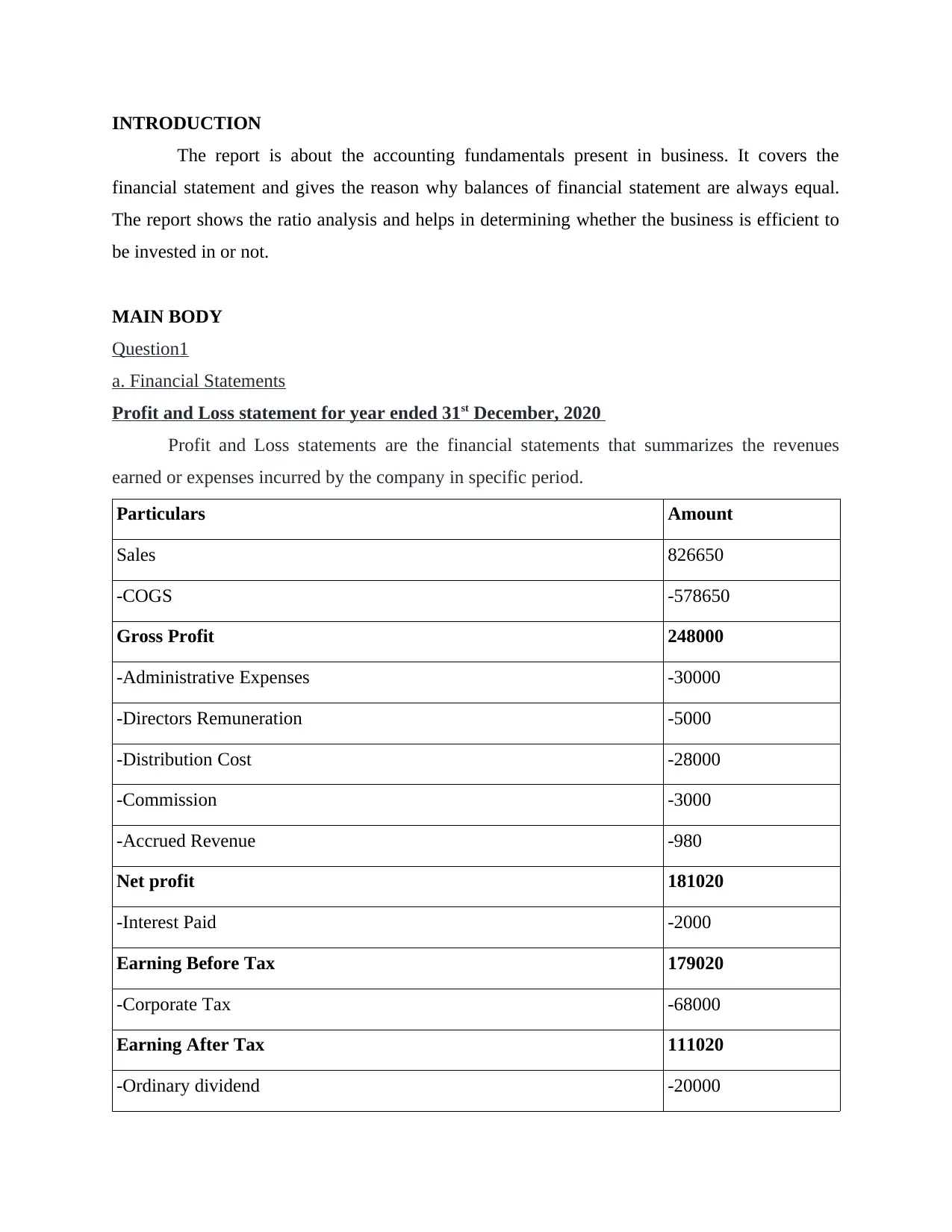

INTRODUCTION

The report is about the accounting fundamentals present in business. It covers the

financial statement and gives the reason why balances of financial statement are always equal.

The report shows the ratio analysis and helps in determining whether the business is efficient to

be invested in or not.

MAIN BODY

Question1

a. Financial Statements

Profit and Loss statement for year ended 31st December, 2020

Profit and Loss statements are the financial statements that summarizes the revenues

earned or expenses incurred by the company in specific period.

Particulars Amount

Sales 826650

-COGS -578650

Gross Profit 248000

-Administrative Expenses -30000

-Directors Remuneration -5000

-Distribution Cost -28000

-Commission -3000

-Accrued Revenue -980

Net profit 181020

-Interest Paid -2000

Earning Before Tax 179020

-Corporate Tax -68000

Earning After Tax 111020

-Ordinary dividend -20000

The report is about the accounting fundamentals present in business. It covers the

financial statement and gives the reason why balances of financial statement are always equal.

The report shows the ratio analysis and helps in determining whether the business is efficient to

be invested in or not.

MAIN BODY

Question1

a. Financial Statements

Profit and Loss statement for year ended 31st December, 2020

Profit and Loss statements are the financial statements that summarizes the revenues

earned or expenses incurred by the company in specific period.

Particulars Amount

Sales 826650

-COGS -578650

Gross Profit 248000

-Administrative Expenses -30000

-Directors Remuneration -5000

-Distribution Cost -28000

-Commission -3000

-Accrued Revenue -980

Net profit 181020

-Interest Paid -2000

Earning Before Tax 179020

-Corporate Tax -68000

Earning After Tax 111020

-Ordinary dividend -20000

-Preference dividend -30000

Retained Profits 61020

Retained Profits at 1st January 2020 132000

Retained Earnings 193020

Balance Sheet of Kedison PLC as on 31st December 2020

Balance sheet determines the assets and liabilities and shareholder fund availability in a

company at specific point,

Particulars Amount

Assets:

Fixed Asset:

Plant and Equipments 632730

Current Asset:

Debtors 170125

Inventories 330600

Cash & Bank 12900

-Commission (3000) 9900

Total Assets 1144335

Liabilities:

Equity and Liability:

Shares 610000

4% Debentures 100000

Retained Earnings 193020

Retained Profits 61020

Retained Profits at 1st January 2020 132000

Retained Earnings 193020

Balance Sheet of Kedison PLC as on 31st December 2020

Balance sheet determines the assets and liabilities and shareholder fund availability in a

company at specific point,

Particulars Amount

Assets:

Fixed Asset:

Plant and Equipments 632730

Current Asset:

Debtors 170125

Inventories 330600

Cash & Bank 12900

-Commission (3000) 9900

Total Assets 1144335

Liabilities:

Equity and Liability:

Shares 610000

4% Debentures 100000

Retained Earnings 193020

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

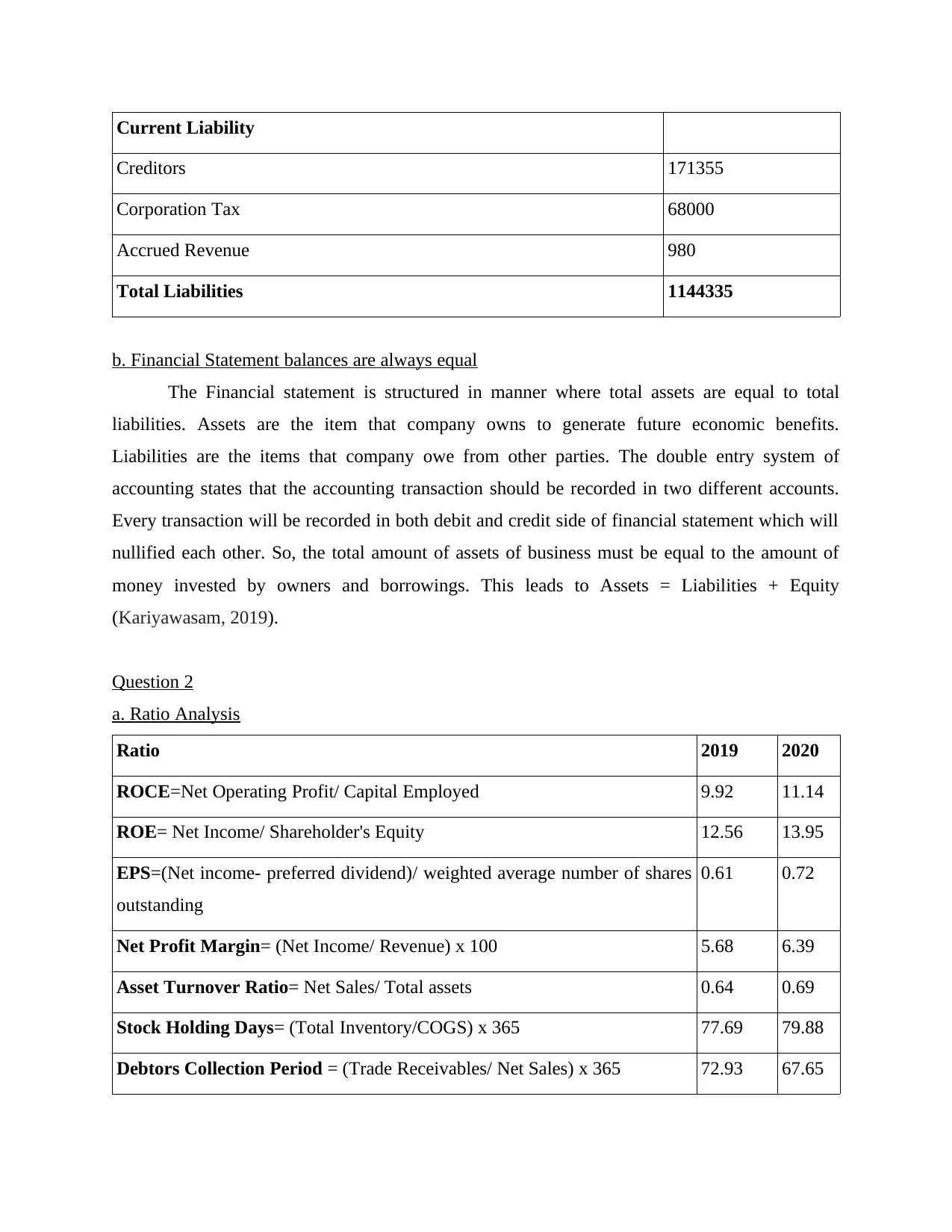

Current Liability

Creditors 171355

Corporation Tax 68000

Accrued Revenue 980

Total Liabilities 1144335

b. Financial Statement balances are always equal

The Financial statement is structured in manner where total assets are equal to total

liabilities. Assets are the item that company owns to generate future economic benefits.

Liabilities are the items that company owe from other parties. The double entry system of

accounting states that the accounting transaction should be recorded in two different accounts.

Every transaction will be recorded in both debit and credit side of financial statement which will

nullified each other. So, the total amount of assets of business must be equal to the amount of

money invested by owners and borrowings. This leads to Assets = Liabilities + Equity

(Kariyawasam, 2019).

Question 2

a. Ratio Analysis

Ratio 2019 2020

ROCE=Net Operating Profit/ Capital Employed 9.92 11.14

ROE= Net Income/ Shareholder's Equity 12.56 13.95

EPS=(Net income- preferred dividend)/ weighted average number of shares

outstanding

0.61 0.72

Net Profit Margin= (Net Income/ Revenue) x 100 5.68 6.39

Asset Turnover Ratio= Net Sales/ Total assets 0.64 0.69

Stock Holding Days= (Total Inventory/COGS) x 365 77.69 79.88

Debtors Collection Period = (Trade Receivables/ Net Sales) x 365 72.93 67.65

Creditors 171355

Corporation Tax 68000

Accrued Revenue 980

Total Liabilities 1144335

b. Financial Statement balances are always equal

The Financial statement is structured in manner where total assets are equal to total

liabilities. Assets are the item that company owns to generate future economic benefits.

Liabilities are the items that company owe from other parties. The double entry system of

accounting states that the accounting transaction should be recorded in two different accounts.

Every transaction will be recorded in both debit and credit side of financial statement which will

nullified each other. So, the total amount of assets of business must be equal to the amount of

money invested by owners and borrowings. This leads to Assets = Liabilities + Equity

(Kariyawasam, 2019).

Question 2

a. Ratio Analysis

Ratio 2019 2020

ROCE=Net Operating Profit/ Capital Employed 9.92 11.14

ROE= Net Income/ Shareholder's Equity 12.56 13.95

EPS=(Net income- preferred dividend)/ weighted average number of shares

outstanding

0.61 0.72

Net Profit Margin= (Net Income/ Revenue) x 100 5.68 6.39

Asset Turnover Ratio= Net Sales/ Total assets 0.64 0.69

Stock Holding Days= (Total Inventory/COGS) x 365 77.69 79.88

Debtors Collection Period = (Trade Receivables/ Net Sales) x 365 72.93 67.65

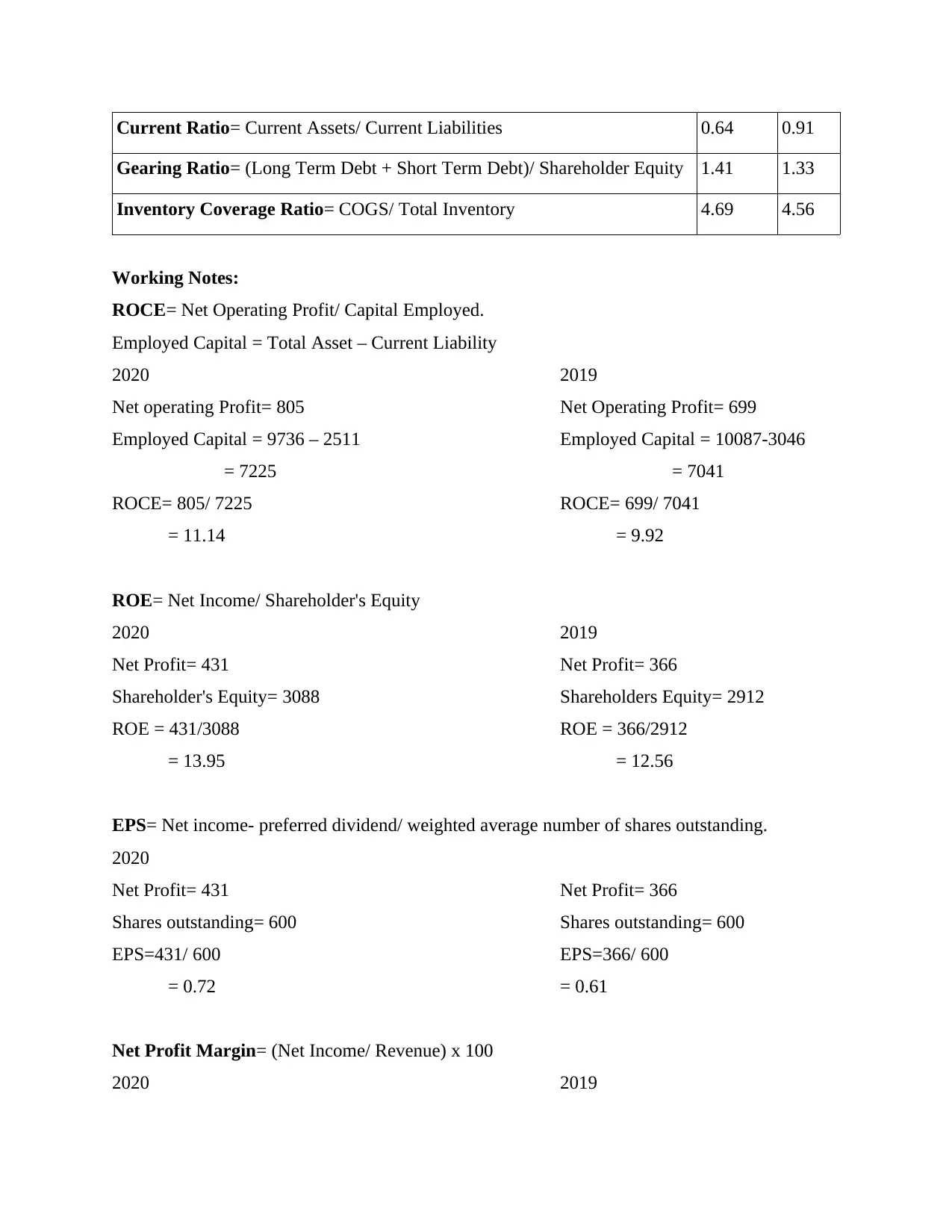

Current Ratio= Current Assets/ Current Liabilities 0.64 0.91

Gearing Ratio= (Long Term Debt + Short Term Debt)/ Shareholder Equity 1.41 1.33

Inventory Coverage Ratio= COGS/ Total Inventory 4.69 4.56

Working Notes:

ROCE= Net Operating Profit/ Capital Employed.

Employed Capital = Total Asset – Current Liability

2020 2019

Net operating Profit= 805 Net Operating Profit= 699

Employed Capital = 9736 – 2511 Employed Capital = 10087-3046

= 7225 = 7041

ROCE= 805/ 7225 ROCE= 699/ 7041

= 11.14 = 9.92

ROE= Net Income/ Shareholder's Equity

2020 2019

Net Profit= 431 Net Profit= 366

Shareholder's Equity= 3088 Shareholders Equity= 2912

ROE = 431/3088 ROE = 366/2912

= 13.95 = 12.56

EPS= Net income- preferred dividend/ weighted average number of shares outstanding.

2020

Net Profit= 431 Net Profit= 366

Shares outstanding= 600 Shares outstanding= 600

EPS=431/ 600 EPS=366/ 600

= 0.72 = 0.61

Net Profit Margin= (Net Income/ Revenue) x 100

2020 2019

Gearing Ratio= (Long Term Debt + Short Term Debt)/ Shareholder Equity 1.41 1.33

Inventory Coverage Ratio= COGS/ Total Inventory 4.69 4.56

Working Notes:

ROCE= Net Operating Profit/ Capital Employed.

Employed Capital = Total Asset – Current Liability

2020 2019

Net operating Profit= 805 Net Operating Profit= 699

Employed Capital = 9736 – 2511 Employed Capital = 10087-3046

= 7225 = 7041

ROCE= 805/ 7225 ROCE= 699/ 7041

= 11.14 = 9.92

ROE= Net Income/ Shareholder's Equity

2020 2019

Net Profit= 431 Net Profit= 366

Shareholder's Equity= 3088 Shareholders Equity= 2912

ROE = 431/3088 ROE = 366/2912

= 13.95 = 12.56

EPS= Net income- preferred dividend/ weighted average number of shares outstanding.

2020

Net Profit= 431 Net Profit= 366

Shares outstanding= 600 Shares outstanding= 600

EPS=431/ 600 EPS=366/ 600

= 0.72 = 0.61

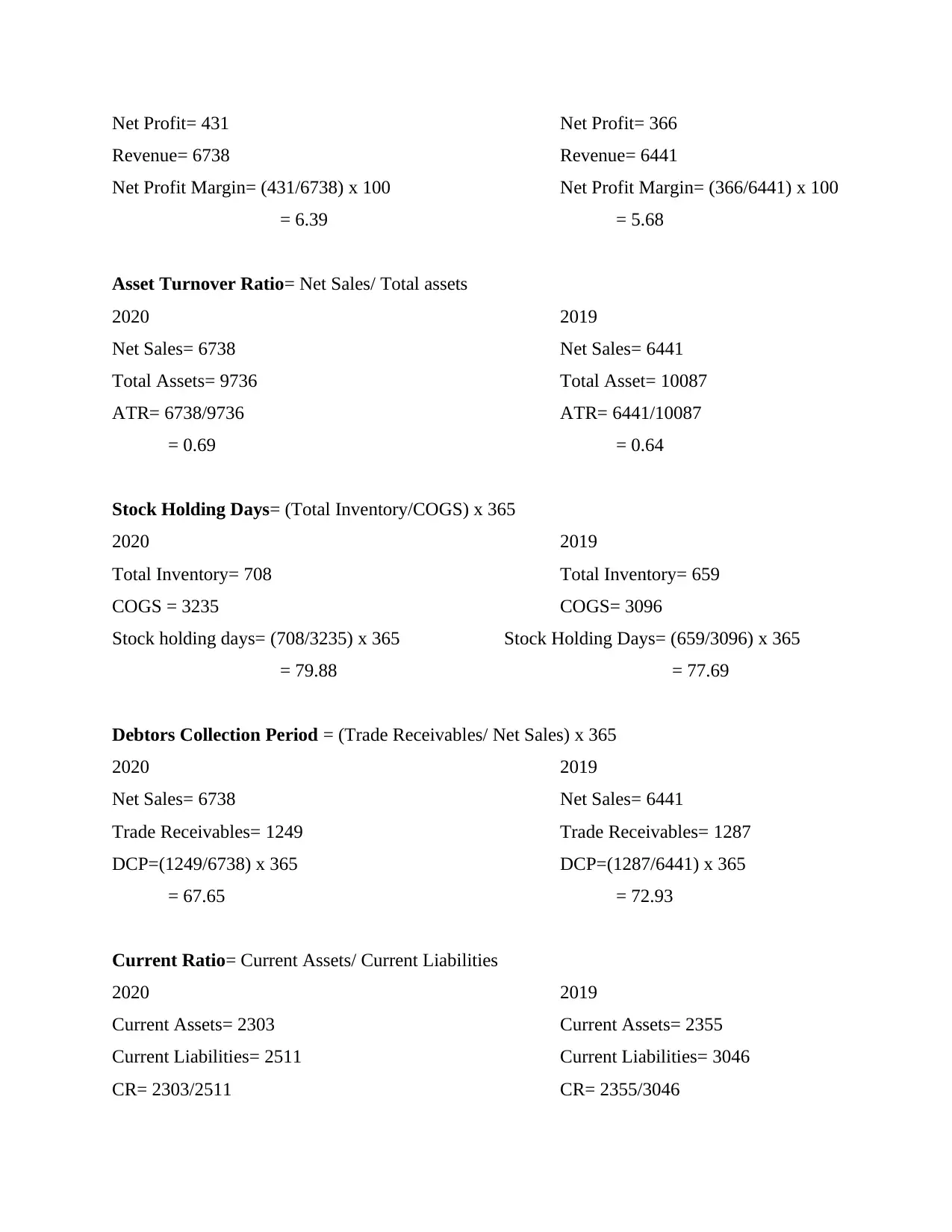

Net Profit Margin= (Net Income/ Revenue) x 100

2020 2019

Net Profit= 431 Net Profit= 366

Revenue= 6738 Revenue= 6441

Net Profit Margin= (431/6738) x 100 Net Profit Margin= (366/6441) x 100

= 6.39 = 5.68

Asset Turnover Ratio= Net Sales/ Total assets

2020 2019

Net Sales= 6738 Net Sales= 6441

Total Assets= 9736 Total Asset= 10087

ATR= 6738/9736 ATR= 6441/10087

= 0.69 = 0.64

Stock Holding Days= (Total Inventory/COGS) x 365

2020 2019

Total Inventory= 708 Total Inventory= 659

COGS = 3235 COGS= 3096

Stock holding days= (708/3235) x 365 Stock Holding Days= (659/3096) x 365

= 79.88 = 77.69

Debtors Collection Period = (Trade Receivables/ Net Sales) x 365

2020 2019

Net Sales= 6738 Net Sales= 6441

Trade Receivables= 1249 Trade Receivables= 1287

DCP=(1249/6738) x 365 DCP=(1287/6441) x 365

= 67.65 = 72.93

Current Ratio= Current Assets/ Current Liabilities

2020 2019

Current Assets= 2303 Current Assets= 2355

Current Liabilities= 2511 Current Liabilities= 3046

CR= 2303/2511 CR= 2355/3046

Revenue= 6738 Revenue= 6441

Net Profit Margin= (431/6738) x 100 Net Profit Margin= (366/6441) x 100

= 6.39 = 5.68

Asset Turnover Ratio= Net Sales/ Total assets

2020 2019

Net Sales= 6738 Net Sales= 6441

Total Assets= 9736 Total Asset= 10087

ATR= 6738/9736 ATR= 6441/10087

= 0.69 = 0.64

Stock Holding Days= (Total Inventory/COGS) x 365

2020 2019

Total Inventory= 708 Total Inventory= 659

COGS = 3235 COGS= 3096

Stock holding days= (708/3235) x 365 Stock Holding Days= (659/3096) x 365

= 79.88 = 77.69

Debtors Collection Period = (Trade Receivables/ Net Sales) x 365

2020 2019

Net Sales= 6738 Net Sales= 6441

Trade Receivables= 1249 Trade Receivables= 1287

DCP=(1249/6738) x 365 DCP=(1287/6441) x 365

= 67.65 = 72.93

Current Ratio= Current Assets/ Current Liabilities

2020 2019

Current Assets= 2303 Current Assets= 2355

Current Liabilities= 2511 Current Liabilities= 3046

CR= 2303/2511 CR= 2355/3046

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

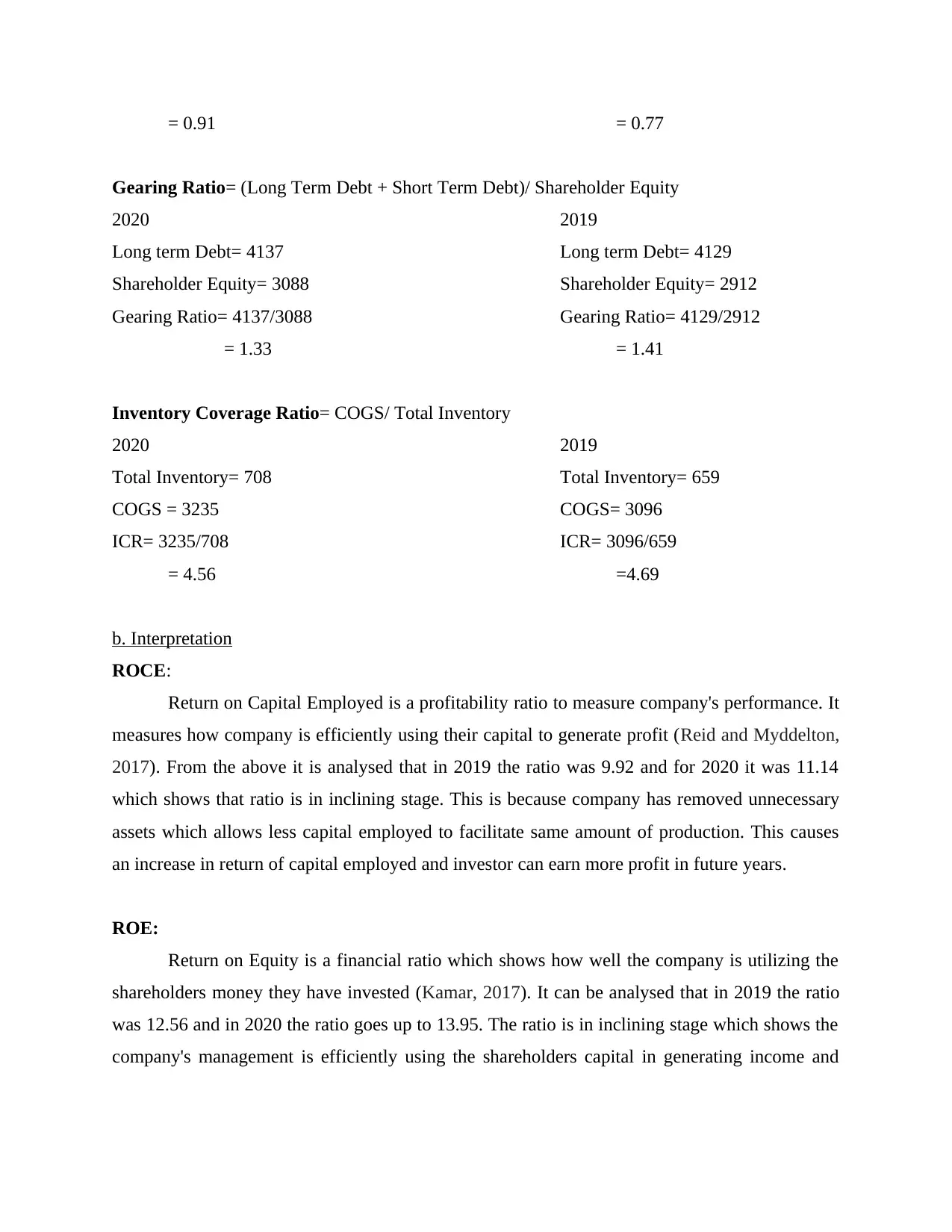

= 0.91 = 0.77

Gearing Ratio= (Long Term Debt + Short Term Debt)/ Shareholder Equity

2020 2019

Long term Debt= 4137 Long term Debt= 4129

Shareholder Equity= 3088 Shareholder Equity= 2912

Gearing Ratio= 4137/3088 Gearing Ratio= 4129/2912

= 1.33 = 1.41

Inventory Coverage Ratio= COGS/ Total Inventory

2020 2019

Total Inventory= 708 Total Inventory= 659

COGS = 3235 COGS= 3096

ICR= 3235/708 ICR= 3096/659

= 4.56 =4.69

b. Interpretation

ROCE:

Return on Capital Employed is a profitability ratio to measure company's performance. It

measures how company is efficiently using their capital to generate profit (Reid and Myddelton,

2017). From the above it is analysed that in 2019 the ratio was 9.92 and for 2020 it was 11.14

which shows that ratio is in inclining stage. This is because company has removed unnecessary

assets which allows less capital employed to facilitate same amount of production. This causes

an increase in return of capital employed and investor can earn more profit in future years.

ROE:

Return on Equity is a financial ratio which shows how well the company is utilizing the

shareholders money they have invested (Kamar, 2017). It can be analysed that in 2019 the ratio

was 12.56 and in 2020 the ratio goes up to 13.95. The ratio is in inclining stage which shows the

company's management is efficiently using the shareholders capital in generating income and

Gearing Ratio= (Long Term Debt + Short Term Debt)/ Shareholder Equity

2020 2019

Long term Debt= 4137 Long term Debt= 4129

Shareholder Equity= 3088 Shareholder Equity= 2912

Gearing Ratio= 4137/3088 Gearing Ratio= 4129/2912

= 1.33 = 1.41

Inventory Coverage Ratio= COGS/ Total Inventory

2020 2019

Total Inventory= 708 Total Inventory= 659

COGS = 3235 COGS= 3096

ICR= 3235/708 ICR= 3096/659

= 4.56 =4.69

b. Interpretation

ROCE:

Return on Capital Employed is a profitability ratio to measure company's performance. It

measures how company is efficiently using their capital to generate profit (Reid and Myddelton,

2017). From the above it is analysed that in 2019 the ratio was 9.92 and for 2020 it was 11.14

which shows that ratio is in inclining stage. This is because company has removed unnecessary

assets which allows less capital employed to facilitate same amount of production. This causes

an increase in return of capital employed and investor can earn more profit in future years.

ROE:

Return on Equity is a financial ratio which shows how well the company is utilizing the

shareholders money they have invested (Kamar, 2017). It can be analysed that in 2019 the ratio

was 12.56 and in 2020 the ratio goes up to 13.95. The ratio is in inclining stage which shows the

company's management is efficiently using the shareholders capital in generating income and

growing of company. It also indicates the company is generating profit without any need of extra

capital.

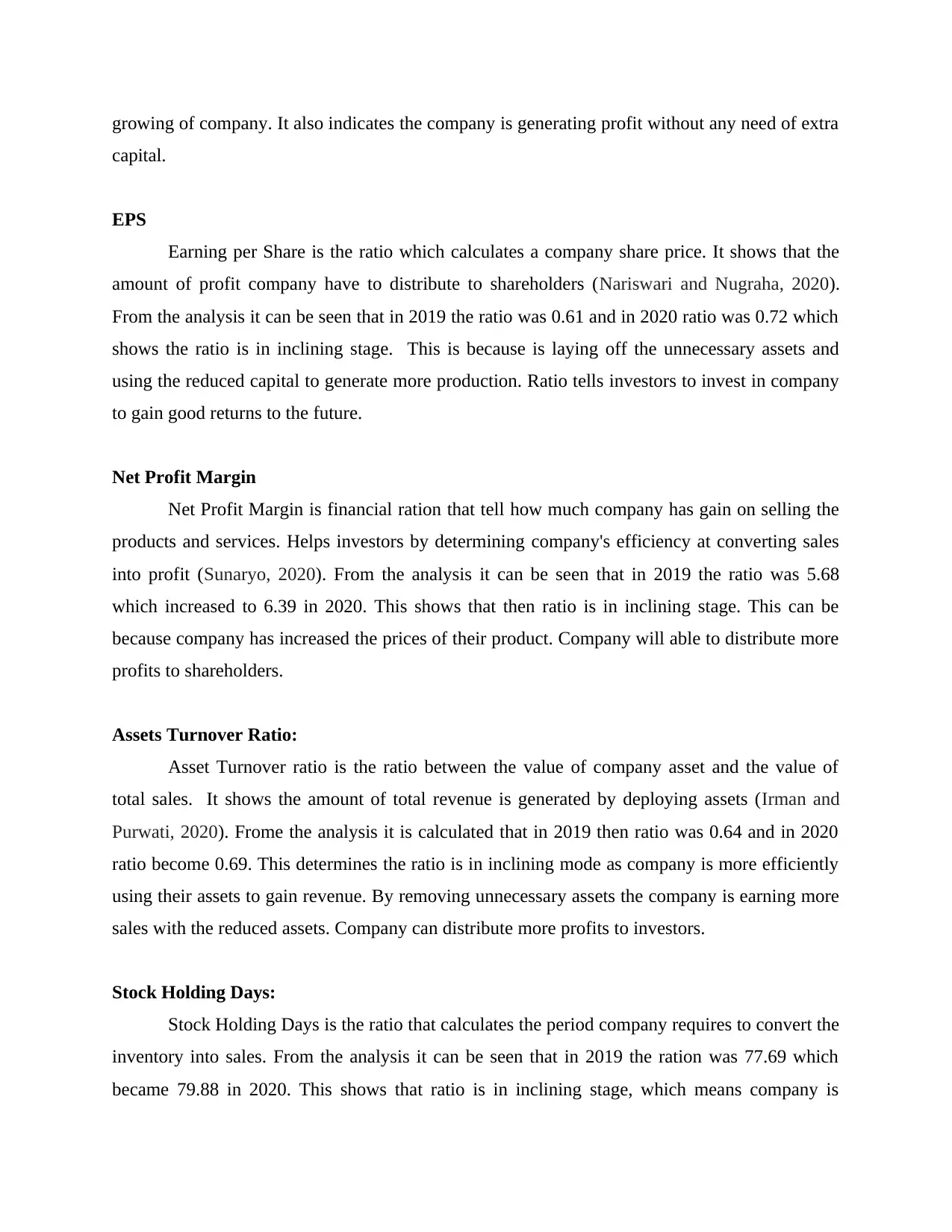

EPS

Earning per Share is the ratio which calculates a company share price. It shows that the

amount of profit company have to distribute to shareholders (Nariswari and Nugraha, 2020).

From the analysis it can be seen that in 2019 the ratio was 0.61 and in 2020 ratio was 0.72 which

shows the ratio is in inclining stage. This is because is laying off the unnecessary assets and

using the reduced capital to generate more production. Ratio tells investors to invest in company

to gain good returns to the future.

Net Profit Margin

Net Profit Margin is financial ration that tell how much company has gain on selling the

products and services. Helps investors by determining company's efficiency at converting sales

into profit (Sunaryo, 2020). From the analysis it can be seen that in 2019 the ratio was 5.68

which increased to 6.39 in 2020. This shows that then ratio is in inclining stage. This can be

because company has increased the prices of their product. Company will able to distribute more

profits to shareholders.

Assets Turnover Ratio:

Asset Turnover ratio is the ratio between the value of company asset and the value of

total sales. It shows the amount of total revenue is generated by deploying assets (Irman and

Purwati, 2020). Frome the analysis it is calculated that in 2019 then ratio was 0.64 and in 2020

ratio become 0.69. This determines the ratio is in inclining mode as company is more efficiently

using their assets to gain revenue. By removing unnecessary assets the company is earning more

sales with the reduced assets. Company can distribute more profits to investors.

Stock Holding Days:

Stock Holding Days is the ratio that calculates the period company requires to convert the

inventory into sales. From the analysis it can be seen that in 2019 the ration was 77.69 which

became 79.88 in 2020. This shows that ratio is in inclining stage, which means company is

capital.

EPS

Earning per Share is the ratio which calculates a company share price. It shows that the

amount of profit company have to distribute to shareholders (Nariswari and Nugraha, 2020).

From the analysis it can be seen that in 2019 the ratio was 0.61 and in 2020 ratio was 0.72 which

shows the ratio is in inclining stage. This is because is laying off the unnecessary assets and

using the reduced capital to generate more production. Ratio tells investors to invest in company

to gain good returns to the future.

Net Profit Margin

Net Profit Margin is financial ration that tell how much company has gain on selling the

products and services. Helps investors by determining company's efficiency at converting sales

into profit (Sunaryo, 2020). From the analysis it can be seen that in 2019 the ratio was 5.68

which increased to 6.39 in 2020. This shows that then ratio is in inclining stage. This can be

because company has increased the prices of their product. Company will able to distribute more

profits to shareholders.

Assets Turnover Ratio:

Asset Turnover ratio is the ratio between the value of company asset and the value of

total sales. It shows the amount of total revenue is generated by deploying assets (Irman and

Purwati, 2020). Frome the analysis it is calculated that in 2019 then ratio was 0.64 and in 2020

ratio become 0.69. This determines the ratio is in inclining mode as company is more efficiently

using their assets to gain revenue. By removing unnecessary assets the company is earning more

sales with the reduced assets. Company can distribute more profits to investors.

Stock Holding Days:

Stock Holding Days is the ratio that calculates the period company requires to convert the

inventory into sales. From the analysis it can be seen that in 2019 the ration was 77.69 which

became 79.88 in 2020. This shows that ratio is in inclining stage, which means company is

purchasing too many stuffs. Having too much idle inventory can eventually become obsolete

which will negatively impact cash flow.

Debtors Collection Period

Debtors Collection Period shows the number of days company takes to convert the debts

taken by customer into cash (Podile, Sivasree and Rani, 2020). From the analysis it can be seen

that in 2019 the ration was 72.93 which became 67.65 in 2020. This shows the ratio is in

declining stage which means the company efficiency of converting the debts into cash is rising.

This will result in more cash availability to do business operations and earn more profit.

Current Ratio:

The current ratio is financial ratio which determines company's efficiency to meet their

short term obligations (Rochim and Ghoniyah, 2017). The analysis shows that the ratio in 2019

was 0.64 which became 0.93 in 2020. This shows that the ratio is in inclining stage which is

because there have been delayed in payments by customers and company makes more purchase

of stocks, which results in increase of assets. Thais is a good thing for investor in knowing

company's efficiency to pay their debts.

Gearing Ratio

Gearing ratio are the financial ratio that gives the idea of company's existing equity to

pay of their debts (Wahyuni, Ayem and Suyanto, 2017). From the analysis it can be seen that the

ratio in 2019 was 1.41 which became 1.33 in 2020. This shows that the ratio is declining stage

company is having less debt as compared to equity. The company is selling of their stick easily

which increases the generation of cash to pay debts faster.

Inventory Coverage Ratio:

Inventory Turnover ratio is the efficiency ratio that is used to measurer how efficiently

company is managing its inventory (Amanda, 2019). From the above analysis it can be seen that

in 2019 the ratio was 4.69 which became 4.56 in 2020. This shows that the ratio is in inclining

stage which means that company's sales are increasing, which leads to more profit. This results

in more distribution of profits among investors.

which will negatively impact cash flow.

Debtors Collection Period

Debtors Collection Period shows the number of days company takes to convert the debts

taken by customer into cash (Podile, Sivasree and Rani, 2020). From the analysis it can be seen

that in 2019 the ration was 72.93 which became 67.65 in 2020. This shows the ratio is in

declining stage which means the company efficiency of converting the debts into cash is rising.

This will result in more cash availability to do business operations and earn more profit.

Current Ratio:

The current ratio is financial ratio which determines company's efficiency to meet their

short term obligations (Rochim and Ghoniyah, 2017). The analysis shows that the ratio in 2019

was 0.64 which became 0.93 in 2020. This shows that the ratio is in inclining stage which is

because there have been delayed in payments by customers and company makes more purchase

of stocks, which results in increase of assets. Thais is a good thing for investor in knowing

company's efficiency to pay their debts.

Gearing Ratio

Gearing ratio are the financial ratio that gives the idea of company's existing equity to

pay of their debts (Wahyuni, Ayem and Suyanto, 2017). From the analysis it can be seen that the

ratio in 2019 was 1.41 which became 1.33 in 2020. This shows that the ratio is declining stage

company is having less debt as compared to equity. The company is selling of their stick easily

which increases the generation of cash to pay debts faster.

Inventory Coverage Ratio:

Inventory Turnover ratio is the efficiency ratio that is used to measurer how efficiently

company is managing its inventory (Amanda, 2019). From the above analysis it can be seen that

in 2019 the ratio was 4.69 which became 4.56 in 2020. This shows that the ratio is in inclining

stage which means that company's sales are increasing, which leads to more profit. This results

in more distribution of profits among investors.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONCLUSION

From the above report it is concluded that analysis of financial statement is very

important to determine the performance and position of the company. Likewise, from task 2 it is

also concluded that the all ratio are increasing. Hence, Chocco PLC performance is rising which

makes a good company for investors to invest in.

From the above report it is concluded that analysis of financial statement is very

important to determine the performance and position of the company. Likewise, from task 2 it is

also concluded that the all ratio are increasing. Hence, Chocco PLC performance is rising which

makes a good company for investors to invest in.

REFERENCES

Books and journals

Amanda, R.I., 2019. The Impact of Cash Turnover, Receivable Turnover, Inventory Turnover,

Current Ratio and Debt to Equity Ratio on Profitability. Journal of research in

management. 2(2).

Irman, M. and Purwati, A.A., 2020. Analysis On The Influence Of Current Ratio, Debt to Equity

Ratio and Total Asset Turnover Toward Return On Assets On The Otomotive and

Component Company That Has Been Registered In Indonesia Stock Exchange Within

2011-2017. International Journal of Economics Development Research (IJEDR). 1(1).

pp.36-44.

Kamar, K., 2017. Analysis of the effect of return on equity (ROE) and debt to equity ratio (DER)

on stock price on cement industry listed in Indonesia stock exchange (IDX) in the year

of 2011-2015. IOSR Journal of Business and Management. 19(05). pp.66-76.

Kariyawasam, H.N., 2019. Analysing the Impact of Financial Ratios on a Company’s Financial

Performance. International Journal of Management Excellence. 13(1). pp.1898-1903.

Nariswari, T.N. and Nugraha, N.M., 2020. Profit Growth: Impact of Net Profit Margin, Gross

Profit Margin and Total Assests Turnover. International Journal of Finance & Banking

Studies (2147-4486). 9(4). pp.87-96.

Podile, V., Sivasree, C.H.V. and Rani, K.S., 2020. Receivables Management in Micro and Small

Enterprises. Journal of Critical Reviews. 7(18). pp.722-726.

Reid, W. and Myddelton, D.R., 2017. Gearing. In The Meaning of Company Accounts. (pp. 164-

166). Routledge.

Rochim, R. and Ghoniyah, N., 2017. Analysis On The Effect of Current Ratio, Cashflow From

Operation to Debt, Firm Size and Return on Equity on Stock Return. International

Journal of Islamic Business Ethics. 2(3). pp.41-51.

Sunaryo, D., 2020. The Effect of Net Profit Margin, Return on Asset, Return on Equity on Share

Prices in The Southeast Asian Metal Industry. International Journal of Science,

Technology & Management. 1(3). pp.198-208.

Wahyuni, T., Ayem, S. and Suyanto, S., 2017. Pengaruh Quick Ratio, Debt To Equity Ratio,

Inventory Turnover Dan Net Profit Margin Terhadap Pertumbuhan Laba Pada

Perusahaan Manufaktur Yang Terdaftar Di Bursa Efek Indonesia Tahun 2011–

2015. Jurnal Akuntansi Dewantara. 1(2). pp.12-21.

1

Books and journals

Amanda, R.I., 2019. The Impact of Cash Turnover, Receivable Turnover, Inventory Turnover,

Current Ratio and Debt to Equity Ratio on Profitability. Journal of research in

management. 2(2).

Irman, M. and Purwati, A.A., 2020. Analysis On The Influence Of Current Ratio, Debt to Equity

Ratio and Total Asset Turnover Toward Return On Assets On The Otomotive and

Component Company That Has Been Registered In Indonesia Stock Exchange Within

2011-2017. International Journal of Economics Development Research (IJEDR). 1(1).

pp.36-44.

Kamar, K., 2017. Analysis of the effect of return on equity (ROE) and debt to equity ratio (DER)

on stock price on cement industry listed in Indonesia stock exchange (IDX) in the year

of 2011-2015. IOSR Journal of Business and Management. 19(05). pp.66-76.

Kariyawasam, H.N., 2019. Analysing the Impact of Financial Ratios on a Company’s Financial

Performance. International Journal of Management Excellence. 13(1). pp.1898-1903.

Nariswari, T.N. and Nugraha, N.M., 2020. Profit Growth: Impact of Net Profit Margin, Gross

Profit Margin and Total Assests Turnover. International Journal of Finance & Banking

Studies (2147-4486). 9(4). pp.87-96.

Podile, V., Sivasree, C.H.V. and Rani, K.S., 2020. Receivables Management in Micro and Small

Enterprises. Journal of Critical Reviews. 7(18). pp.722-726.

Reid, W. and Myddelton, D.R., 2017. Gearing. In The Meaning of Company Accounts. (pp. 164-

166). Routledge.

Rochim, R. and Ghoniyah, N., 2017. Analysis On The Effect of Current Ratio, Cashflow From

Operation to Debt, Firm Size and Return on Equity on Stock Return. International

Journal of Islamic Business Ethics. 2(3). pp.41-51.

Sunaryo, D., 2020. The Effect of Net Profit Margin, Return on Asset, Return on Equity on Share

Prices in The Southeast Asian Metal Industry. International Journal of Science,

Technology & Management. 1(3). pp.198-208.

Wahyuni, T., Ayem, S. and Suyanto, S., 2017. Pengaruh Quick Ratio, Debt To Equity Ratio,

Inventory Turnover Dan Net Profit Margin Terhadap Pertumbuhan Laba Pada

Perusahaan Manufaktur Yang Terdaftar Di Bursa Efek Indonesia Tahun 2011–

2015. Jurnal Akuntansi Dewantara. 1(2). pp.12-21.

1

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.