Ways to Increase Shareholder Value

VerifiedAdded on 2021/04/21

|7

|1853

|40

AI Summary

The assignment provides a detailed analysis of ways to increase shareholder value, including compliance with environmental sustainability policies, selecting right customers and suppliers, optimizing assets, and lowering cost of capital. It also highlights the importance of productivity and after-sales services in increasing revenue and gross profit. The document is based on various studies and research papers that emphasize the significance of stakeholder management theory and triple bottom line approach to business sustainability.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING IN ORGANIZATION AND SOCIETY

Accounting in Organization and Society

Name of the Student

Name of the University

Author’s Note

Accounting in Organization and Society

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ACCOUNTING IN ORGANIZATION AND SOCIETY

Table of Contents

Requirement 2..................................................................................................................................2

Requirement 3..................................................................................................................................3

Requirement 4..................................................................................................................................4

Requirement 5..................................................................................................................................5

References........................................................................................................................................6

Table of Contents

Requirement 2..................................................................................................................................2

Requirement 3..................................................................................................................................3

Requirement 4..................................................................................................................................4

Requirement 5..................................................................................................................................5

References........................................................................................................................................6

2ACCOUNTING IN ORGANIZATION AND SOCIETY

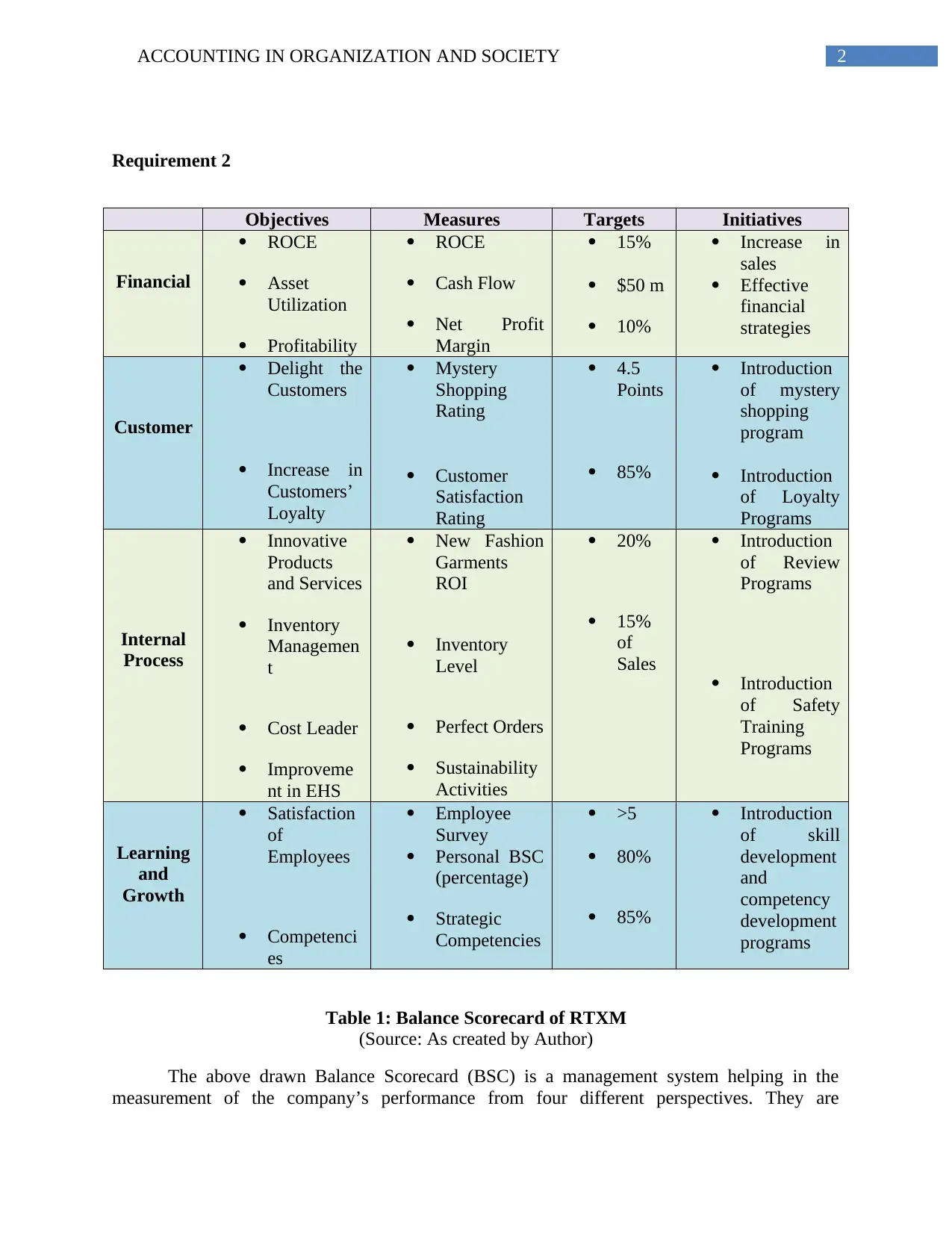

Requirement 2

Objectives Measures Targets Initiatives

Financial

ROCE

Asset

Utilization

Profitability

ROCE

Cash Flow

Net Profit

Margin

15%

$50 m

10%

Increase in

sales

Effective

financial

strategies

Customer

Delight the

Customers

Increase in

Customers’

Loyalty

Mystery

Shopping

Rating

Customer

Satisfaction

Rating

4.5

Points

85%

Introduction

of mystery

shopping

program

Introduction

of Loyalty

Programs

Internal

Process

Innovative

Products

and Services

Inventory

Managemen

t

Cost Leader

Improveme

nt in EHS

New Fashion

Garments

ROI

Inventory

Level

Perfect Orders

Sustainability

Activities

20%

15%

of

Sales

Introduction

of Review

Programs

Introduction

of Safety

Training

Programs

Learning

and

Growth

Satisfaction

of

Employees

Competenci

es

Employee

Survey

Personal BSC

(percentage)

Strategic

Competencies

>5

80%

85%

Introduction

of skill

development

and

competency

development

programs

Table 1: Balance Scorecard of RTXM

(Source: As created by Author)

The above drawn Balance Scorecard (BSC) is a management system helping in the

measurement of the company’s performance from four different perspectives. They are

Requirement 2

Objectives Measures Targets Initiatives

Financial

ROCE

Asset

Utilization

Profitability

ROCE

Cash Flow

Net Profit

Margin

15%

$50 m

10%

Increase in

sales

Effective

financial

strategies

Customer

Delight the

Customers

Increase in

Customers’

Loyalty

Mystery

Shopping

Rating

Customer

Satisfaction

Rating

4.5

Points

85%

Introduction

of mystery

shopping

program

Introduction

of Loyalty

Programs

Internal

Process

Innovative

Products

and Services

Inventory

Managemen

t

Cost Leader

Improveme

nt in EHS

New Fashion

Garments

ROI

Inventory

Level

Perfect Orders

Sustainability

Activities

20%

15%

of

Sales

Introduction

of Review

Programs

Introduction

of Safety

Training

Programs

Learning

and

Growth

Satisfaction

of

Employees

Competenci

es

Employee

Survey

Personal BSC

(percentage)

Strategic

Competencies

>5

80%

85%

Introduction

of skill

development

and

competency

development

programs

Table 1: Balance Scorecard of RTXM

(Source: As created by Author)

The above drawn Balance Scorecard (BSC) is a management system helping in the

measurement of the company’s performance from four different perspectives. They are

3ACCOUNTING IN ORGANIZATION AND SOCIETY

Financial; Customer; Internal Process; and Learning and Growth. As per the above table, there

are certain objectives under each perspective along with the means to measure them. The

achievement of each objectives will be measured against the previously set targets so that the

performance gap can be analyzed. The BSC matrix also shows the required initiatives to be taken

for the achievement of these objectives (Bititci et al. 2012).

The four important metrics are mentioned below:

Return on Capital Employed (ROCE): ROCE is considered as an important metric as it is used

for measuring the profitability of the company after considering the factors of capital used for it.

Increase in Customers’ Loyalty: Increase in customers’ loyalty refers to the retention of

customers and for this reason, it is considered as a fundamental metric for the success of the

companies (Taylor and Baines 2012).

Innovative Products and Services: The introduction of innovative products and services is

considered as an important metric as it is highly necessary for increasing the revenue of the

companies.

Employee Satisfaction: Employees are considered as the greatest assets of the businesses as they

help in the achievement of the goals and objectives of the companies. For this reason, it is

considered as one of the major matrices for measuring the organizational success (Nørreklit et al.

2012).

Requirement 3

The costs and benefits are shows below:

Super Cheap

Benefits: The main benefit is that RTXM will get their required products in a large range from

Super Cheap for the purpose of their business expansion plan. Most importantly, this supplier is

offering these products to RTXM on a very low price than its competitors. Apart from this,

RTXM will be getting these products delivered in a short time. All these aspects will increase the

profitability of RTXM that is helpful for their business expansion (Kiron et al. 2013).

Cost: It needs to be mentioned that Super Cheap is not an environmentally sustainable company,

as they do not take any action against their anti-sustainable business activities. In addition, this

supplier is also involved in the issues like child labor, low wages, health and safety issues and

others. Thus, RTXM will lose their business goodwill by involving with this supplier (Fischer et

al. 2012).

Green Fashion

Benefits: Green Fashion is well known for their sustainability activities. As per their

sustainability agenda, this supplier extract resources on ethical basis and their product material is

kind to the environment. In addition, the company promote work-life balance of the employees

and provides inventive. By involving with this supplier, RTXM will get sustainable recognition

Financial; Customer; Internal Process; and Learning and Growth. As per the above table, there

are certain objectives under each perspective along with the means to measure them. The

achievement of each objectives will be measured against the previously set targets so that the

performance gap can be analyzed. The BSC matrix also shows the required initiatives to be taken

for the achievement of these objectives (Bititci et al. 2012).

The four important metrics are mentioned below:

Return on Capital Employed (ROCE): ROCE is considered as an important metric as it is used

for measuring the profitability of the company after considering the factors of capital used for it.

Increase in Customers’ Loyalty: Increase in customers’ loyalty refers to the retention of

customers and for this reason, it is considered as a fundamental metric for the success of the

companies (Taylor and Baines 2012).

Innovative Products and Services: The introduction of innovative products and services is

considered as an important metric as it is highly necessary for increasing the revenue of the

companies.

Employee Satisfaction: Employees are considered as the greatest assets of the businesses as they

help in the achievement of the goals and objectives of the companies. For this reason, it is

considered as one of the major matrices for measuring the organizational success (Nørreklit et al.

2012).

Requirement 3

The costs and benefits are shows below:

Super Cheap

Benefits: The main benefit is that RTXM will get their required products in a large range from

Super Cheap for the purpose of their business expansion plan. Most importantly, this supplier is

offering these products to RTXM on a very low price than its competitors. Apart from this,

RTXM will be getting these products delivered in a short time. All these aspects will increase the

profitability of RTXM that is helpful for their business expansion (Kiron et al. 2013).

Cost: It needs to be mentioned that Super Cheap is not an environmentally sustainable company,

as they do not take any action against their anti-sustainable business activities. In addition, this

supplier is also involved in the issues like child labor, low wages, health and safety issues and

others. Thus, RTXM will lose their business goodwill by involving with this supplier (Fischer et

al. 2012).

Green Fashion

Benefits: Green Fashion is well known for their sustainability activities. As per their

sustainability agenda, this supplier extract resources on ethical basis and their product material is

kind to the environment. In addition, the company promote work-life balance of the employees

and provides inventive. By involving with this supplier, RTXM will get sustainable recognition

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ACCOUNTING IN ORGANIZATION AND SOCIETY

among the customers that will increase the revenue and profitability of the company (Willard

2012).

Costs: By involving with Green Fashion, RTXM will not be able to get the required products in a

large variety of range for the purpose of their expansion. In addition, RTXM will have to pay

high price for the products from Green Fashion that can increase the overall cost of the company.

Apart from all these, RTXM will not get the delivery of their products from the supplies in quick

time. All these aspects can affect the profitability and expansion of the company.

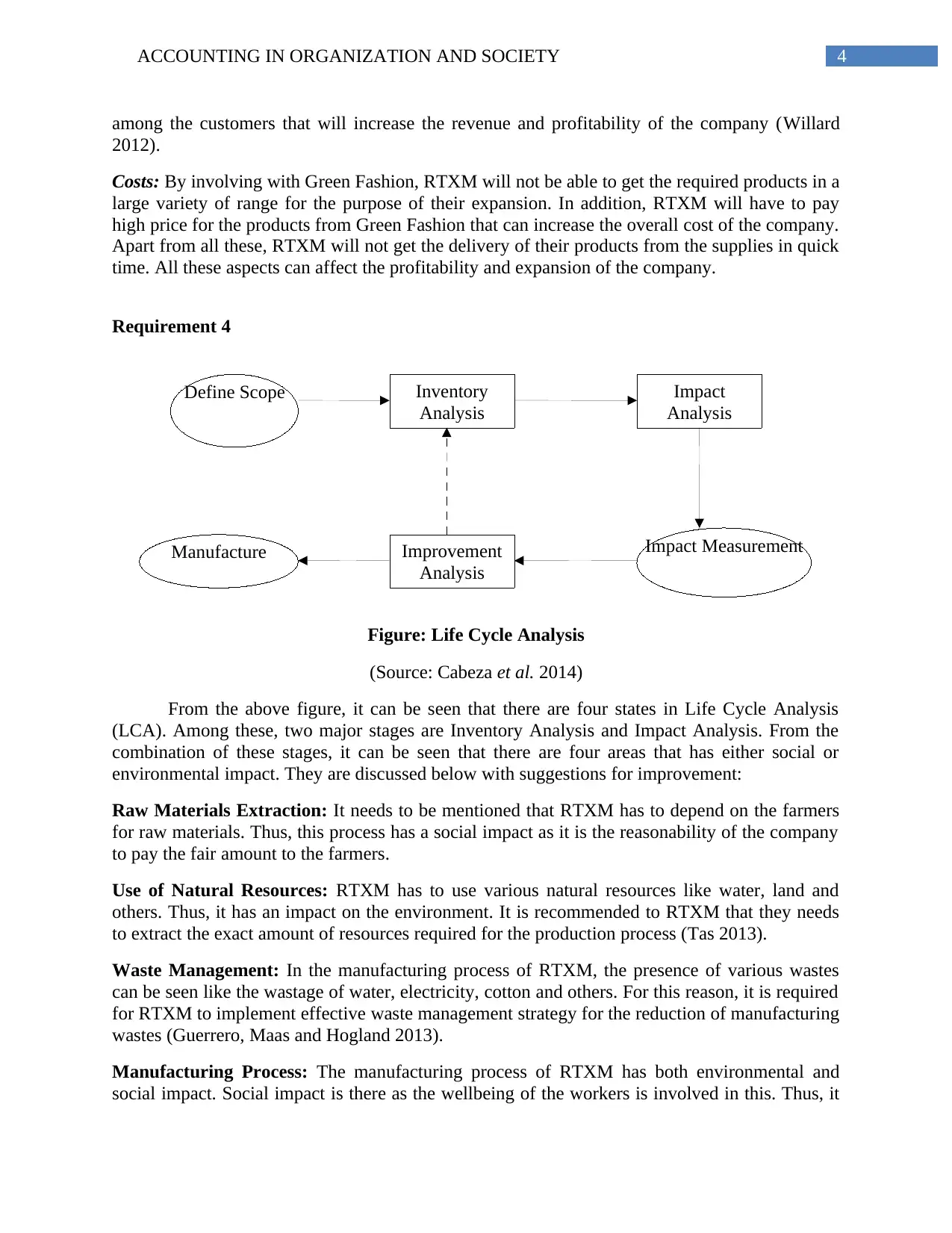

Requirement 4

Figure: Life Cycle Analysis

(Source: Cabeza et al. 2014)

From the above figure, it can be seen that there are four states in Life Cycle Analysis

(LCA). Among these, two major stages are Inventory Analysis and Impact Analysis. From the

combination of these stages, it can be seen that there are four areas that has either social or

environmental impact. They are discussed below with suggestions for improvement:

Raw Materials Extraction: It needs to be mentioned that RTXM has to depend on the farmers

for raw materials. Thus, this process has a social impact as it is the reasonability of the company

to pay the fair amount to the farmers.

Use of Natural Resources: RTXM has to use various natural resources like water, land and

others. Thus, it has an impact on the environment. It is recommended to RTXM that they needs

to extract the exact amount of resources required for the production process (Tas 2013).

Waste Management: In the manufacturing process of RTXM, the presence of various wastes

can be seen like the wastage of water, electricity, cotton and others. For this reason, it is required

for RTXM to implement effective waste management strategy for the reduction of manufacturing

wastes (Guerrero, Maas and Hogland 2013).

Manufacturing Process: The manufacturing process of RTXM has both environmental and

social impact. Social impact is there as the wellbeing of the workers is involved in this. Thus, it

Define Scope

Manufacture

Inventory

Analysis

Impact

Analysis

Improvement

Analysis

Impact Measurement

among the customers that will increase the revenue and profitability of the company (Willard

2012).

Costs: By involving with Green Fashion, RTXM will not be able to get the required products in a

large variety of range for the purpose of their expansion. In addition, RTXM will have to pay

high price for the products from Green Fashion that can increase the overall cost of the company.

Apart from all these, RTXM will not get the delivery of their products from the supplies in quick

time. All these aspects can affect the profitability and expansion of the company.

Requirement 4

Figure: Life Cycle Analysis

(Source: Cabeza et al. 2014)

From the above figure, it can be seen that there are four states in Life Cycle Analysis

(LCA). Among these, two major stages are Inventory Analysis and Impact Analysis. From the

combination of these stages, it can be seen that there are four areas that has either social or

environmental impact. They are discussed below with suggestions for improvement:

Raw Materials Extraction: It needs to be mentioned that RTXM has to depend on the farmers

for raw materials. Thus, this process has a social impact as it is the reasonability of the company

to pay the fair amount to the farmers.

Use of Natural Resources: RTXM has to use various natural resources like water, land and

others. Thus, it has an impact on the environment. It is recommended to RTXM that they needs

to extract the exact amount of resources required for the production process (Tas 2013).

Waste Management: In the manufacturing process of RTXM, the presence of various wastes

can be seen like the wastage of water, electricity, cotton and others. For this reason, it is required

for RTXM to implement effective waste management strategy for the reduction of manufacturing

wastes (Guerrero, Maas and Hogland 2013).

Manufacturing Process: The manufacturing process of RTXM has both environmental and

social impact. Social impact is there as the wellbeing of the workers is involved in this. Thus, it

Define Scope

Manufacture

Inventory

Analysis

Impact

Analysis

Improvement

Analysis

Impact Measurement

5ACCOUNTING IN ORGANIZATION AND SOCIETY

is recommended to RTXM that the company needs to make timely and fair payment to their

workers. In addition, RTXM is also required to develop effective environmentally sustainable

strategies after taking into consideration the negative effects of their manufacturing process on

the environment.

Requirement 5

It needs to be mentioned that the business organizations or industries use specific

techniques to increase the value of shares in long-term by considering the major stakeholders.

For this reason, the garment industry of Singapore is selected to know the ways to increase the

value of the shareholders. They are discussed below:

One major way to increase the value of the shareholders is to comply with the policies

and regulations of environmental sustainability. In the recent years, environmental

sustainability has attracted the attention of the customers. Thus, it can be done to

increase the value of the shareholders (Verbeke and Tung 2013).

The company can also increase the value of the shareholders by increasing the revenue

of the company by the selection of right types of customers. At the same time, the

company needs to offer the customers different attractive products with better after

sales services (Stout 2012).

The increase of the value of the shareholders also depends on the increase in gross

profit with the selection of right suppliers and to maintain a good relationship with

them.

The company can also increase the value of the shareholders by increasing the return on

operating cost investments with the selection of right employees as it will help in the

increase of productivity of the company (Armour and Gordon 2014).

Another major ways to increase the value of the shareholders is to lower the cost of

capital of the companies with the optimization of assets.

is recommended to RTXM that the company needs to make timely and fair payment to their

workers. In addition, RTXM is also required to develop effective environmentally sustainable

strategies after taking into consideration the negative effects of their manufacturing process on

the environment.

Requirement 5

It needs to be mentioned that the business organizations or industries use specific

techniques to increase the value of shares in long-term by considering the major stakeholders.

For this reason, the garment industry of Singapore is selected to know the ways to increase the

value of the shareholders. They are discussed below:

One major way to increase the value of the shareholders is to comply with the policies

and regulations of environmental sustainability. In the recent years, environmental

sustainability has attracted the attention of the customers. Thus, it can be done to

increase the value of the shareholders (Verbeke and Tung 2013).

The company can also increase the value of the shareholders by increasing the revenue

of the company by the selection of right types of customers. At the same time, the

company needs to offer the customers different attractive products with better after

sales services (Stout 2012).

The increase of the value of the shareholders also depends on the increase in gross

profit with the selection of right suppliers and to maintain a good relationship with

them.

The company can also increase the value of the shareholders by increasing the return on

operating cost investments with the selection of right employees as it will help in the

increase of productivity of the company (Armour and Gordon 2014).

Another major ways to increase the value of the shareholders is to lower the cost of

capital of the companies with the optimization of assets.

6ACCOUNTING IN ORGANIZATION AND SOCIETY

References

Armour, J. and Gordon, J.N., 2014. Systemic harms and shareholder value. Journal of Legal

Analysis, 6(1), pp.35-85.

Bititci, U., Garengo, P., Dörfler, V. and Nudurupati, S., 2012. Performance measurement:

challenges for tomorrow. International journal of management reviews, 14(3), pp.305-327.

Cabeza, L.F., Rincón, L., Vilariño, V., Pérez, G. and Castell, A., 2014. Life cycle assessment

(LCA) and life cycle energy analysis (LCEA) of buildings and the building sector: A

review. Renewable and sustainable energy reviews, 29, pp.394-416.

Fischer, J., Dyball, R., Fazey, I., Gross, C., Dovers, S., Ehrlich, P.R., Brulle, R.J., Christensen, C.

and Borden, R.J., 2012. Human behavior and sustainability. Frontiers in Ecology and the

Environment, 10(3), pp.153-160.

Guerrero, L.A., Maas, G. and Hogland, W., 2013. Solid waste management challenges for cities

in developing countries. Waste management, 33(1), pp.220-232.

Kiron, D., Kruschwitz, N., Reeves, M. and Goh, E., 2013. The benefits of sustainability-driven

innovation. MIT Sloan Management Review, 54(2), p.69.

Nørreklit, H., Nørreklit, L., Mitchell, F. and Bjørnenak, T., 2012. The rise of the balanced

scorecard! Relevance regained?. Journal of Accounting & Organizational Change, 8(4), pp.490-

510.

Stout, L.A., 2012. The shareholder value myth: How putting shareholders first harms investors,

corporations, and the public. Berrett-Koehler Publishers.

Tas, E., 2013. Integrated water resources management. Aerul si Apa. Componente ale Mediului,

p.217.

Taylor, J. and Baines, C., 2012. Performance management in UK universities: implementing the

Balanced Scorecard. Journal of Higher Education Policy and Management, 34(2), pp.111-124.

Verbeke, A. and Tung, V., 2013. The future of stakeholder management theory: A temporal

perspective. Journal of Business Ethics, 112(3), pp.529-543.

Willard, B., 2012. The new sustainability advantage: seven business case benefits of a triple

bottom line. New Society Publishers.

References

Armour, J. and Gordon, J.N., 2014. Systemic harms and shareholder value. Journal of Legal

Analysis, 6(1), pp.35-85.

Bititci, U., Garengo, P., Dörfler, V. and Nudurupati, S., 2012. Performance measurement:

challenges for tomorrow. International journal of management reviews, 14(3), pp.305-327.

Cabeza, L.F., Rincón, L., Vilariño, V., Pérez, G. and Castell, A., 2014. Life cycle assessment

(LCA) and life cycle energy analysis (LCEA) of buildings and the building sector: A

review. Renewable and sustainable energy reviews, 29, pp.394-416.

Fischer, J., Dyball, R., Fazey, I., Gross, C., Dovers, S., Ehrlich, P.R., Brulle, R.J., Christensen, C.

and Borden, R.J., 2012. Human behavior and sustainability. Frontiers in Ecology and the

Environment, 10(3), pp.153-160.

Guerrero, L.A., Maas, G. and Hogland, W., 2013. Solid waste management challenges for cities

in developing countries. Waste management, 33(1), pp.220-232.

Kiron, D., Kruschwitz, N., Reeves, M. and Goh, E., 2013. The benefits of sustainability-driven

innovation. MIT Sloan Management Review, 54(2), p.69.

Nørreklit, H., Nørreklit, L., Mitchell, F. and Bjørnenak, T., 2012. The rise of the balanced

scorecard! Relevance regained?. Journal of Accounting & Organizational Change, 8(4), pp.490-

510.

Stout, L.A., 2012. The shareholder value myth: How putting shareholders first harms investors,

corporations, and the public. Berrett-Koehler Publishers.

Tas, E., 2013. Integrated water resources management. Aerul si Apa. Componente ale Mediului,

p.217.

Taylor, J. and Baines, C., 2012. Performance management in UK universities: implementing the

Balanced Scorecard. Journal of Higher Education Policy and Management, 34(2), pp.111-124.

Verbeke, A. and Tung, V., 2013. The future of stakeholder management theory: A temporal

perspective. Journal of Business Ethics, 112(3), pp.529-543.

Willard, B., 2012. The new sustainability advantage: seven business case benefits of a triple

bottom line. New Society Publishers.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.