ACC539 - Analyzing Internal Controls: Chipps Limited Expenditure

VerifiedAdded on 2023/03/23

|10

|1597

|22

Report

AI Summary

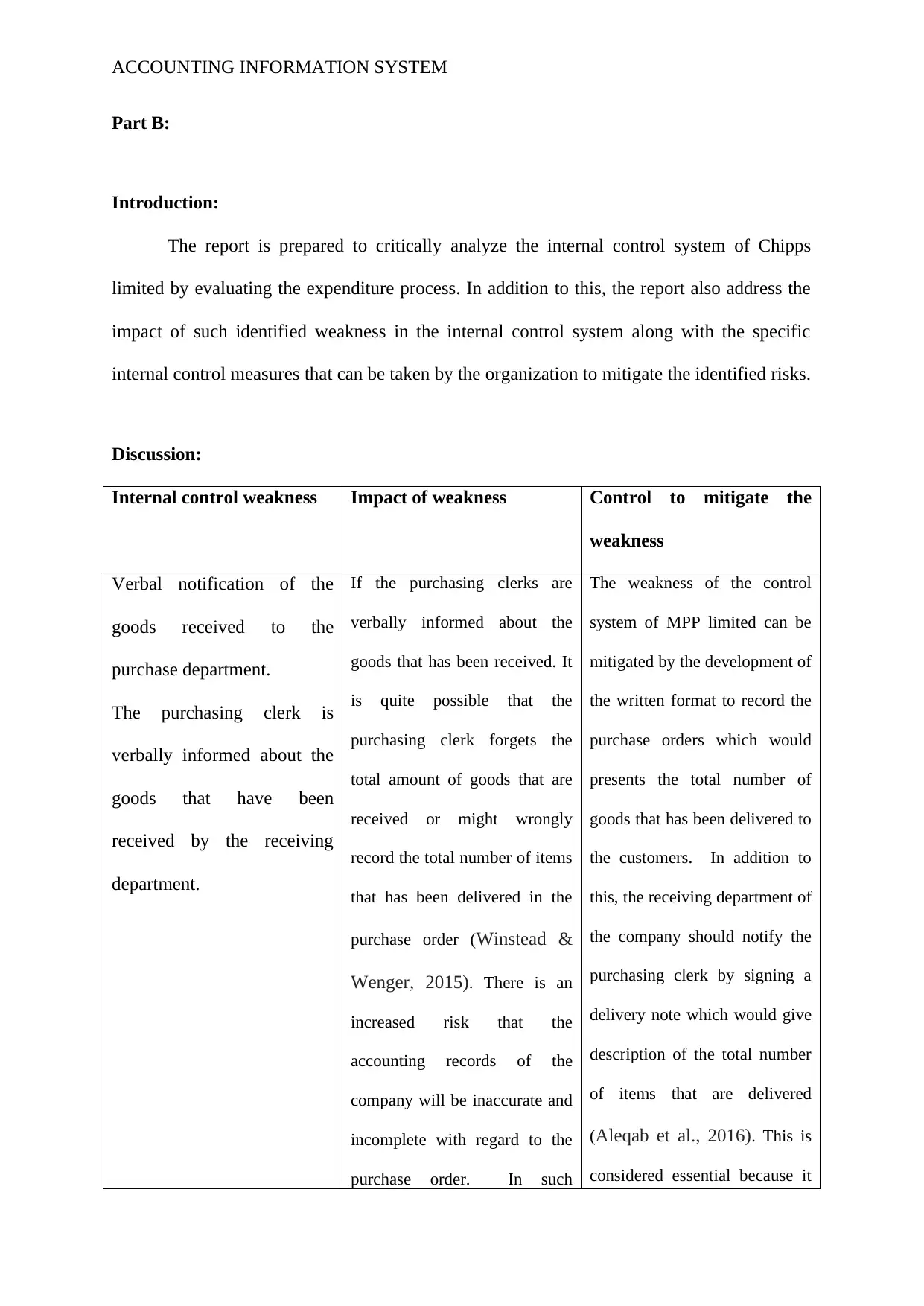

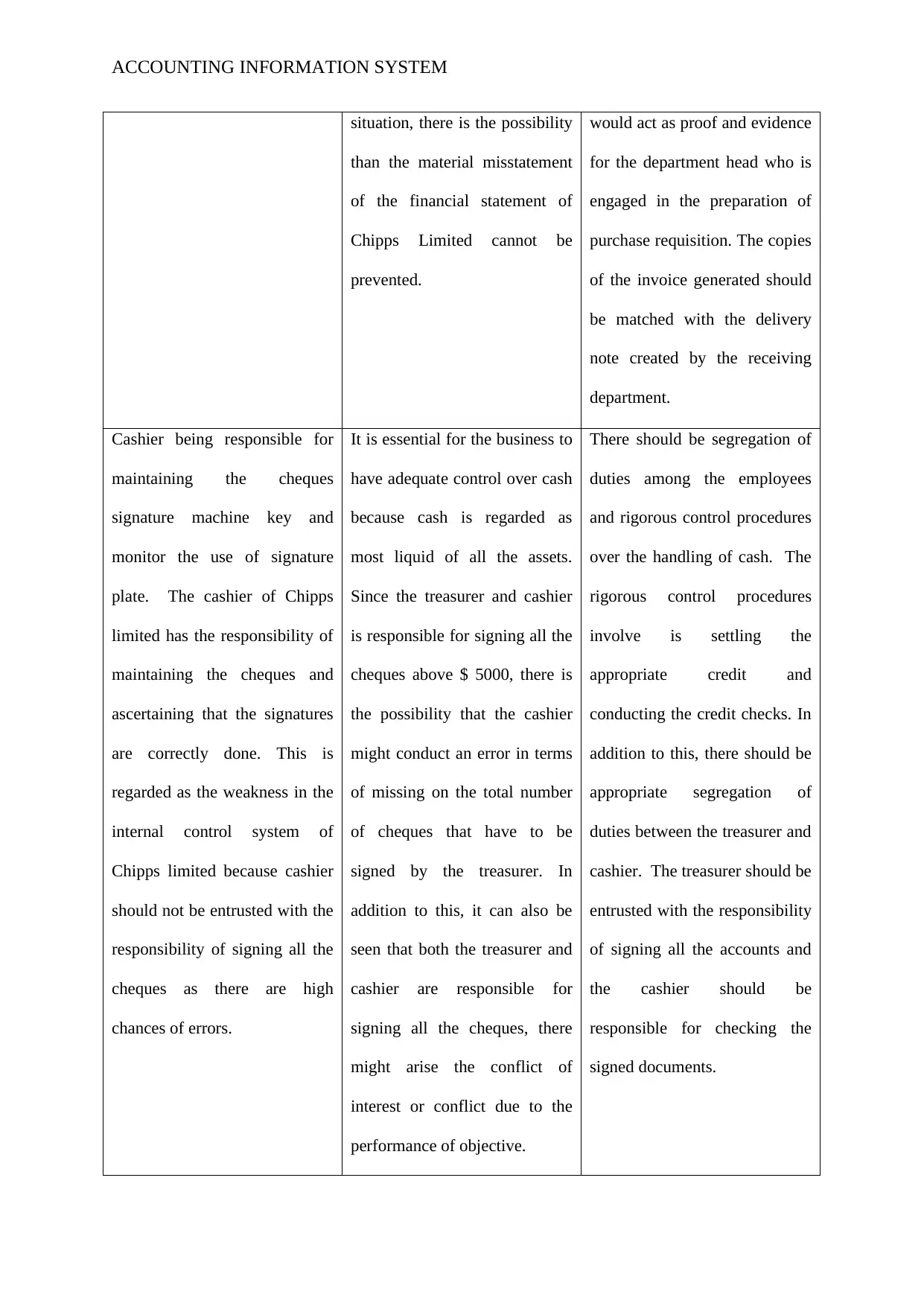

This report provides a critical analysis of the internal control system at Chipps Limited, focusing on the expenditure cycle. It identifies weaknesses in areas such as verbal notification of goods received, cashier responsibilities, numerous purchasing clerks, and inadequate reviewing of open purchase orders. The report discusses the impact of these weaknesses, including the potential for material misstatements in financial statements and increased risks of errors and fraud. To mitigate these risks, the report suggests implementing specific internal control measures, such as developing written purchase order records, segregating duties, reducing the number of purchasing clerks, promoting coordination between staff, and regularly reviewing open purchase order transactions. The analysis concludes that addressing these weaknesses through effective internal control systems and appropriate strategies is essential for maintaining the integrity of Chipps Limited's financial reporting.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.