Contemporary Accounting and Management Accounting Issues: Agency Theory

VerifiedAdded on 2023/06/13

|13

|2480

|369

AI Summary

This research paper explores the role of agency theory and related factors in maintaining effective carbon disclosure in organizations. It discusses the significance of carbon emission disclosure for organizations in consideration to increasing financial performance through employing agency theory.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING ISSUES AND AGENCY THEORY

MGT723 Research Project

Semester 2 2017

Assessment Task 1: Research Proposal

Student Name: XXX

Your assigned research topic*: Contemporary Accounting and Management Accounting Issues:

Agency Theory

Draft Research Question: What is the role of agency theory and related factors in maintaining

effective carbon disclosure in organizations?

Title: XXX

Submission Date: XXX

MGT723 Research Project

Semester 2 2017

Assessment Task 1: Research Proposal

Student Name: XXX

Your assigned research topic*: Contemporary Accounting and Management Accounting Issues:

Agency Theory

Draft Research Question: What is the role of agency theory and related factors in maintaining

effective carbon disclosure in organizations?

Title: XXX

Submission Date: XXX

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ACCOUNTING ISSUES AND AGENCY THEORY

Table of Contents

Literature Review................................................................................................................2

Motivation........................................................................................................................2

Practical Motivation.....................................................................................................2

Theoretical Motivation................................................................................................2

Conflicting Previous Results.......................................................................................3

Agency Theory............................................................................................................4

Key Theoretical Constructs.........................................................................................4

Relationship between Slack and Information Asymmetry..........................................4

Conceptual Framework Model............................................................................................5

Hypothesis...........................................................................................................................6

Proxy Measures for Theoretical Constructs........................................................................7

Research Method.................................................................................................................8

Data Collection................................................................................................................8

Sampling and Size of Sample..........................................................................................8

Method of Data Analysis.................................................................................................8

References..........................................................................................................................10

Appendices........................................................................................................................11

Table of Contents

Literature Review................................................................................................................2

Motivation........................................................................................................................2

Practical Motivation.....................................................................................................2

Theoretical Motivation................................................................................................2

Conflicting Previous Results.......................................................................................3

Agency Theory............................................................................................................4

Key Theoretical Constructs.........................................................................................4

Relationship between Slack and Information Asymmetry..........................................4

Conceptual Framework Model............................................................................................5

Hypothesis...........................................................................................................................6

Proxy Measures for Theoretical Constructs........................................................................7

Research Method.................................................................................................................8

Data Collection................................................................................................................8

Sampling and Size of Sample..........................................................................................8

Method of Data Analysis.................................................................................................8

References..........................................................................................................................10

Appendices........................................................................................................................11

2ACCOUNTING ISSUES AND AGENCY THEORY

3ACCOUNTING ISSUES AND AGENCY THEORY

Literature Review

Motivation

Practical Motivation

Coad, Jack and Kholeif (2015) stated that the vital sources of carbon emission are there in

organizations and for this reason they might contribute in decreasing the emission level. With

emergence of Corporate Social Responsibility concept within nation’s regulatory framework, the

organizations are becoming aware. Moreover, they are also considering carbon emission

disclosure as this is related with the financial performance. Hoque (2018) indicated that the

major concern of the environment is increasing carbon emission level by organizations for the

reason that it greatly impacts global warning along with increasing harmful environmental

consequences. Carbon emissions also impacts business conducts like investment, competition

along with investor and stakeholder activities. This also greatly puts huge impact on the goods

and raw materials supply along with government co-operation risks and decreased share prices.

In contrast, Christensen, Nikolaev and Wittenberg‐Moerman (2016) revealed that there is

different connection between carbon emissions performance disclosure, financial performance

and company’s growth. Voluntary disclosure by organizations indicates their management

efficiency of emissions. This leads to development of shareholders interest in consideration to

business investment within the organization relied on its potential. For this reason, carbon

emission disclosure is a vital concern for all international organizations.

Theoretical Motivation

This research is intended to explain the significance of carbon emission disclosure for the

organizations in consideration to increasing financial performance through employing agency

Literature Review

Motivation

Practical Motivation

Coad, Jack and Kholeif (2015) stated that the vital sources of carbon emission are there in

organizations and for this reason they might contribute in decreasing the emission level. With

emergence of Corporate Social Responsibility concept within nation’s regulatory framework, the

organizations are becoming aware. Moreover, they are also considering carbon emission

disclosure as this is related with the financial performance. Hoque (2018) indicated that the

major concern of the environment is increasing carbon emission level by organizations for the

reason that it greatly impacts global warning along with increasing harmful environmental

consequences. Carbon emissions also impacts business conducts like investment, competition

along with investor and stakeholder activities. This also greatly puts huge impact on the goods

and raw materials supply along with government co-operation risks and decreased share prices.

In contrast, Christensen, Nikolaev and Wittenberg‐Moerman (2016) revealed that there is

different connection between carbon emissions performance disclosure, financial performance

and company’s growth. Voluntary disclosure by organizations indicates their management

efficiency of emissions. This leads to development of shareholders interest in consideration to

business investment within the organization relied on its potential. For this reason, carbon

emission disclosure is a vital concern for all international organizations.

Theoretical Motivation

This research is intended to explain the significance of carbon emission disclosure for the

organizations in consideration to increasing financial performance through employing agency

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ACCOUNTING ISSUES AND AGENCY THEORY

theory. Research carried out by Bosse and Phillips (2016) explained that the carbon emission

disclosure has great impact on financial performance of organizations. Organizations must focus

on decreasing the environmental concerns that can gradually offer economic advantages. For this

reason, they can voluntarily disclose that an organization cares for its environment and focus on

considering climate change due to operations of the organization. Nevo, Nevo and Pinsonneault

(2016) indicated that climate change is essential concern for the research. Carbon disclosure by

the organizations must be voluntary and accurate relied on real figures and facts that can

facilitate shareholders in determining real financial performance and value of the organization.

This also focuses on facilitating the organization in order to prove the environmental

effectiveness. For this research, it will be considered to realize the effect of carbon emission

disclosure on the organizations non-financial performance as well as financial performance.

Conflicting Previous Results

Ott, Schiemann and Günther (2017) gathered that this attracts shareholders for investing

within the company attaining financial benefits for the organization. Moreover, from

administrative viewpoint an organization might follow CSR policy for maintaining an effective

relationship within the legal and government bodies. This effective relationship also increases

reputation along with company’s goodwill. Bosse and Phillips (2016) added that on the other

hand there is a relationship between the suppliers and consumers. This is because they turn out to

be stronger as consumers all through the world are environment conscious and contribute to

efforts that focuses on environment protection.

theory. Research carried out by Bosse and Phillips (2016) explained that the carbon emission

disclosure has great impact on financial performance of organizations. Organizations must focus

on decreasing the environmental concerns that can gradually offer economic advantages. For this

reason, they can voluntarily disclose that an organization cares for its environment and focus on

considering climate change due to operations of the organization. Nevo, Nevo and Pinsonneault

(2016) indicated that climate change is essential concern for the research. Carbon disclosure by

the organizations must be voluntary and accurate relied on real figures and facts that can

facilitate shareholders in determining real financial performance and value of the organization.

This also focuses on facilitating the organization in order to prove the environmental

effectiveness. For this research, it will be considered to realize the effect of carbon emission

disclosure on the organizations non-financial performance as well as financial performance.

Conflicting Previous Results

Ott, Schiemann and Günther (2017) gathered that this attracts shareholders for investing

within the company attaining financial benefits for the organization. Moreover, from

administrative viewpoint an organization might follow CSR policy for maintaining an effective

relationship within the legal and government bodies. This effective relationship also increases

reputation along with company’s goodwill. Bosse and Phillips (2016) added that on the other

hand there is a relationship between the suppliers and consumers. This is because they turn out to

be stronger as consumers all through the world are environment conscious and contribute to

efforts that focuses on environment protection.

5ACCOUNTING ISSUES AND AGENCY THEORY

Agency Theory

Depoers, Jeanjean and Jérôme (2016) explained agency theory as prices that explain the

relationship between agents and principles in consideration to a particular problem. The major

reason of such issue and agents spreading the issue can be recognized using agency theory.

Key Theoretical Constructs

Pepper and Gore (2015) stated that based on the agency theory, the expenses related with

environmental responsibilities increases the profit of the organization and for this reason,

environmental activity has negative impact on a company’s profitability. These researchers also

indicated that there exists a neural relationship between environmental ad company

performances. Moreover, they contend that a company’s ideal level of interest within social

environmental responsibility might be analyzed within an indistinguishable path through taking

into consideration supply and demand sides. Shogren et al. (2015) evidenced that they also

indicate that organizations that does not take part in environmental responsibility will offer these

products at cheaper rate. Moreover, the organizations that are involved in CSR might provide

higher prices for the products. It can also be stated that environmental and financial performance

has neutral relationship.

Relationship between Slack and Information Asymmetry

Shogren et al. (2015) explained through the use of agency theory that because of the

climate change effect on the economy there are several nations that are making attempts in

decreasing the emission disclosure and measurement. Such efforts are relied on realizing the

financial market factor pressure and slack for business carbon emission disclosure in several

sectors. This can facilitate the programs and incentives for encouraging meeting and

participation for national targets (Bosse and Phillips 2016).

Agency Theory

Depoers, Jeanjean and Jérôme (2016) explained agency theory as prices that explain the

relationship between agents and principles in consideration to a particular problem. The major

reason of such issue and agents spreading the issue can be recognized using agency theory.

Key Theoretical Constructs

Pepper and Gore (2015) stated that based on the agency theory, the expenses related with

environmental responsibilities increases the profit of the organization and for this reason,

environmental activity has negative impact on a company’s profitability. These researchers also

indicated that there exists a neural relationship between environmental ad company

performances. Moreover, they contend that a company’s ideal level of interest within social

environmental responsibility might be analyzed within an indistinguishable path through taking

into consideration supply and demand sides. Shogren et al. (2015) evidenced that they also

indicate that organizations that does not take part in environmental responsibility will offer these

products at cheaper rate. Moreover, the organizations that are involved in CSR might provide

higher prices for the products. It can also be stated that environmental and financial performance

has neutral relationship.

Relationship between Slack and Information Asymmetry

Shogren et al. (2015) explained through the use of agency theory that because of the

climate change effect on the economy there are several nations that are making attempts in

decreasing the emission disclosure and measurement. Such efforts are relied on realizing the

financial market factor pressure and slack for business carbon emission disclosure in several

sectors. This can facilitate the programs and incentives for encouraging meeting and

participation for national targets (Bosse and Phillips 2016).

6ACCOUNTING ISSUES AND AGENCY THEORY

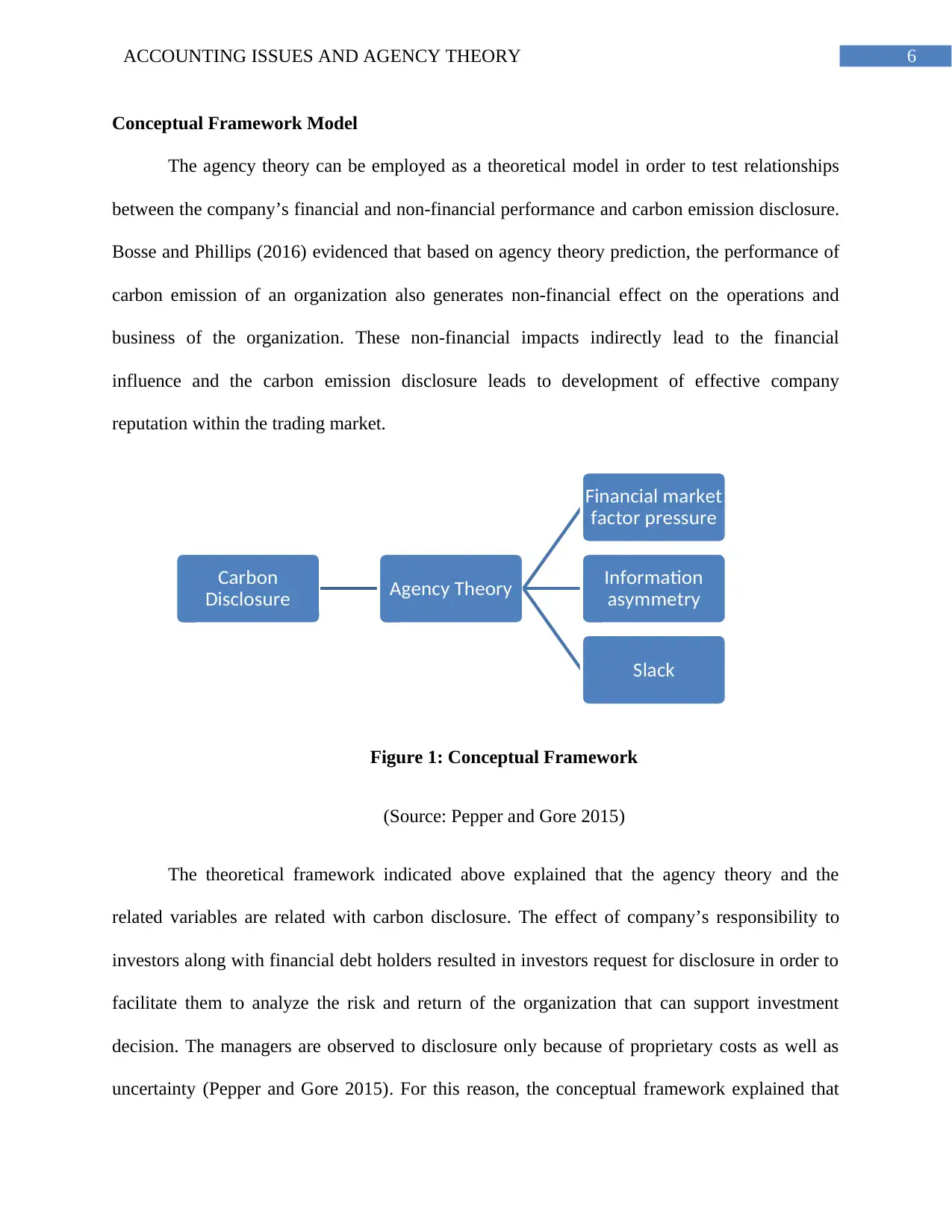

Conceptual Framework Model

The agency theory can be employed as a theoretical model in order to test relationships

between the company’s financial and non-financial performance and carbon emission disclosure.

Bosse and Phillips (2016) evidenced that based on agency theory prediction, the performance of

carbon emission of an organization also generates non-financial effect on the operations and

business of the organization. These non-financial impacts indirectly lead to the financial

influence and the carbon emission disclosure leads to development of effective company

reputation within the trading market.

Figure 1: Conceptual Framework

(Source: Pepper and Gore 2015)

The theoretical framework indicated above explained that the agency theory and the

related variables are related with carbon disclosure. The effect of company’s responsibility to

investors along with financial debt holders resulted in investors request for disclosure in order to

facilitate them to analyze the risk and return of the organization that can support investment

decision. The managers are observed to disclosure only because of proprietary costs as well as

uncertainty (Pepper and Gore 2015). For this reason, the conceptual framework explained that

Carbon

Disclosure Agency Theory

Financial market

factor pressure

Information

asymmetry

Slack

Conceptual Framework Model

The agency theory can be employed as a theoretical model in order to test relationships

between the company’s financial and non-financial performance and carbon emission disclosure.

Bosse and Phillips (2016) evidenced that based on agency theory prediction, the performance of

carbon emission of an organization also generates non-financial effect on the operations and

business of the organization. These non-financial impacts indirectly lead to the financial

influence and the carbon emission disclosure leads to development of effective company

reputation within the trading market.

Figure 1: Conceptual Framework

(Source: Pepper and Gore 2015)

The theoretical framework indicated above explained that the agency theory and the

related variables are related with carbon disclosure. The effect of company’s responsibility to

investors along with financial debt holders resulted in investors request for disclosure in order to

facilitate them to analyze the risk and return of the organization that can support investment

decision. The managers are observed to disclosure only because of proprietary costs as well as

uncertainty (Pepper and Gore 2015). For this reason, the conceptual framework explained that

Carbon

Disclosure Agency Theory

Financial market

factor pressure

Information

asymmetry

Slack

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING ISSUES AND AGENCY THEORY

failure of information disclosure might lead to information asymmetry between the investment

providers and management. This can facilitate in increasing organization’s investment expenses.

The conceptual framework explained through the use of agency theory that because of

the climate change effect on the economy there are several nations that are making attempts in

decreasing the emission disclosure and measurement. Such efforts are relied on realizing the

financial market factor pressure and slack for business carbon emission disclosure in several

sectors. This can facilitate the programs and incentives for encouraging meeting and

participation for national targets (Bosse and Phillips 2016). Financial market factors impact

company’s responsibility towards investors along with financial debt holders. This facilitated

them to ask for information for evaluating real value of the company and for enabling investment

judgment along with company ownership. This has a considerable association with the reports.

Hypothesis

The hypotheses that are to be tested through the research on contemporary and

management accounting issues in consideration to Agency theory is explained under:

H1: The carbon emissions disclosure by the organizations leads to opposite relationship

between the environmental responsibility and profitability effect on growth, sustainability

and profitability of an organization

H2: Target slack will be more in the initial year within which the targets are set

H3: Target slack will be more in the existence of performance-based incentives

Proxy Measures for Theoretical Constructs

Theoretical Proxy measure Dependent (DV), Source

failure of information disclosure might lead to information asymmetry between the investment

providers and management. This can facilitate in increasing organization’s investment expenses.

The conceptual framework explained through the use of agency theory that because of

the climate change effect on the economy there are several nations that are making attempts in

decreasing the emission disclosure and measurement. Such efforts are relied on realizing the

financial market factor pressure and slack for business carbon emission disclosure in several

sectors. This can facilitate the programs and incentives for encouraging meeting and

participation for national targets (Bosse and Phillips 2016). Financial market factors impact

company’s responsibility towards investors along with financial debt holders. This facilitated

them to ask for information for evaluating real value of the company and for enabling investment

judgment along with company ownership. This has a considerable association with the reports.

Hypothesis

The hypotheses that are to be tested through the research on contemporary and

management accounting issues in consideration to Agency theory is explained under:

H1: The carbon emissions disclosure by the organizations leads to opposite relationship

between the environmental responsibility and profitability effect on growth, sustainability

and profitability of an organization

H2: Target slack will be more in the initial year within which the targets are set

H3: Target slack will be more in the existence of performance-based incentives

Proxy Measures for Theoretical Constructs

Theoretical Proxy measure Dependent (DV), Source

8ACCOUNTING ISSUES AND AGENCY THEORY

Construct Independent (IV)

Target slack will

be greater in the

first year in which

targets are set

based on agency

theory

Increase in

remuneration

and being able to

attain the target

in case

unexpected

factors are

present.

Slack is deemed to

be the dependent

variable

The target that is explained in

CDP. Previous research

available in budgetary process

and incentives for managers.

Target slack will

be greater in the

presence of

performance

based incentives

based on agency

theory

Information

asymmetry is

observed to

decrease with

time. This is

measured as the

number of years

before the

company has

been setting

targets for

emission of

carbon.

Independent

variable is deemed

to be the

information

asymmetry

Data related with this variable

will be gathered through

evaluating the performance

based incentives of the

company that can increase the

pressure to generate target

slack.

Construct Independent (IV)

Target slack will

be greater in the

first year in which

targets are set

based on agency

theory

Increase in

remuneration

and being able to

attain the target

in case

unexpected

factors are

present.

Slack is deemed to

be the dependent

variable

The target that is explained in

CDP. Previous research

available in budgetary process

and incentives for managers.

Target slack will

be greater in the

presence of

performance

based incentives

based on agency

theory

Information

asymmetry is

observed to

decrease with

time. This is

measured as the

number of years

before the

company has

been setting

targets for

emission of

carbon.

Independent

variable is deemed

to be the

information

asymmetry

Data related with this variable

will be gathered through

evaluating the performance

based incentives of the

company that can increase the

pressure to generate target

slack.

9ACCOUNTING ISSUES AND AGENCY THEORY

Research Method

Data Collection

The research on the agency theory and carbon disclosure will consider employing

primary as well as secondary data that can facilitate in attaining desired research outcomes.

Gathered quantitative data signifies the information section which can be evaluated for collecting

data in alignment with the research results. Collection of the secondary data for investigating

“Contemporary Accounting and Management Accounting Issues: Agency Theory” will be

collecting data from authenticate government websites and journals (Taylor, Bogdan and

DeVault 2015). Primary data might be collected from employing the technique of questionnaire

survey. This is the reason for which suitable survey respondents has been chosen to participate

within the process of survey and for obtaining reliable research results on agency theory practice

along with carbon disclosure theory.

Sampling and Size of Sample

Non-probability sampling method will be used in this research. This sampling is based on

the subjective judgment of researcher in opposition to the random selection (Silverman 2016). In

order to attain results from the research, 5 managers of the companies operating in Australia will

be selected for taking part in the survey process. The gathered responses will be evaluated for

attaining views on agency theory and its relevance on addressing carbon disclosure issues.

Method of Data Analysis

In order to attain relevant research results certain statistical methods will be employed

such as MS Excel and graphical representation of data. This can facilitate in evaluating the

opinions of the survey participants and can properly plan, design and represent collected data.

Research Method

Data Collection

The research on the agency theory and carbon disclosure will consider employing

primary as well as secondary data that can facilitate in attaining desired research outcomes.

Gathered quantitative data signifies the information section which can be evaluated for collecting

data in alignment with the research results. Collection of the secondary data for investigating

“Contemporary Accounting and Management Accounting Issues: Agency Theory” will be

collecting data from authenticate government websites and journals (Taylor, Bogdan and

DeVault 2015). Primary data might be collected from employing the technique of questionnaire

survey. This is the reason for which suitable survey respondents has been chosen to participate

within the process of survey and for obtaining reliable research results on agency theory practice

along with carbon disclosure theory.

Sampling and Size of Sample

Non-probability sampling method will be used in this research. This sampling is based on

the subjective judgment of researcher in opposition to the random selection (Silverman 2016). In

order to attain results from the research, 5 managers of the companies operating in Australia will

be selected for taking part in the survey process. The gathered responses will be evaluated for

attaining views on agency theory and its relevance on addressing carbon disclosure issues.

Method of Data Analysis

In order to attain relevant research results certain statistical methods will be employed

such as MS Excel and graphical representation of data. This can facilitate in evaluating the

opinions of the survey participants and can properly plan, design and represent collected data.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ACCOUNTING ISSUES AND AGENCY THEORY

Moreover, quantitative data will be represented through tables and graphs that can ensure the

clarity and authenticity of collected data (Flick 2015). Pearson correlation test will be carried out

that will ensure the reliability and validity of data. In order to test the relationship between the

dependent and independent variables, correlation and regression analysis will be carried out in

this research.

Moreover, quantitative data will be represented through tables and graphs that can ensure the

clarity and authenticity of collected data (Flick 2015). Pearson correlation test will be carried out

that will ensure the reliability and validity of data. In order to test the relationship between the

dependent and independent variables, correlation and regression analysis will be carried out in

this research.

11ACCOUNTING ISSUES AND AGENCY THEORY

References

Bosse, D.A. and Phillips, R.A., 2016. Agency theory and bounded self-interest. Academy of

Management Review, 41(2), pp.276-297.

Christensen, H.B., Nikolaev, V.V. and WITTENBERG‐MOERMAN, R.E.G.I.N.A., 2016.

Accounting information in financial contracting: The incomplete contract theory

perspective. Journal of accounting research, 54(2), pp.397-435.

Coad, A., Jack, L. and Kholeif, A.O.R., 2015. Structuration theory: reflections on its further

potential for management accounting research. Qualitative Research in Accounting &

Management, 12(2), pp.153-171.

Depoers, F., Jeanjean, T. and Jérôme, T., 2016. Voluntary disclosure of greenhouse gas

emissions: Contrasting the carbon disclosure project and corporate reports. Journal of Business

Ethics, 134(3), pp.445-461.

Flick, U., 2015. Introducing research methodology: A beginner's guide to doing a research

project. Sage.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Nevo, S., Nevo, D. and Pinsonneault, A., 2016. A Temporally Situated Self-Agency Theory of

Information Technology Reinvention. Mis Quarterly, 40(1), pp.157-186.

Ott, C., Schiemann, F. and Günther, T., 2017. Disentangling the determinants of the response

and the publication decisions: The case of the Carbon Disclosure Project. Journal of Accounting

and Public Policy, 36(1), pp.14-33.

References

Bosse, D.A. and Phillips, R.A., 2016. Agency theory and bounded self-interest. Academy of

Management Review, 41(2), pp.276-297.

Christensen, H.B., Nikolaev, V.V. and WITTENBERG‐MOERMAN, R.E.G.I.N.A., 2016.

Accounting information in financial contracting: The incomplete contract theory

perspective. Journal of accounting research, 54(2), pp.397-435.

Coad, A., Jack, L. and Kholeif, A.O.R., 2015. Structuration theory: reflections on its further

potential for management accounting research. Qualitative Research in Accounting &

Management, 12(2), pp.153-171.

Depoers, F., Jeanjean, T. and Jérôme, T., 2016. Voluntary disclosure of greenhouse gas

emissions: Contrasting the carbon disclosure project and corporate reports. Journal of Business

Ethics, 134(3), pp.445-461.

Flick, U., 2015. Introducing research methodology: A beginner's guide to doing a research

project. Sage.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Nevo, S., Nevo, D. and Pinsonneault, A., 2016. A Temporally Situated Self-Agency Theory of

Information Technology Reinvention. Mis Quarterly, 40(1), pp.157-186.

Ott, C., Schiemann, F. and Günther, T., 2017. Disentangling the determinants of the response

and the publication decisions: The case of the Carbon Disclosure Project. Journal of Accounting

and Public Policy, 36(1), pp.14-33.

12ACCOUNTING ISSUES AND AGENCY THEORY

Pepper, A. and Gore, J., 2015. Behavioral agency theory: New foundations for theorizing about

executive compensation. Journal of management, 41(4), pp.1045-1068.

Shogren, K.A., Wehmeyer, M.L., Palmer, S.B., Forber-Pratt, A.J., Little, T.J. and Lopez, S.,

2015. Causal agency theory: Reconceptualizing a functional model of self-

determination. Education and Training in Autism and Developmental Disabilities, pp.251-263.

Silverman, D. ed., 2016. Qualitative research. Sage.

Taylor, S.J., Bogdan, R. and DeVault, M., 2015. Introduction to qualitative research methods: A

guidebook and resource. John Wiley & Sons.

Appendices

Questionnaire for Managers

1. To which stakeholders does the company report CSR information o carbon emissions?

2. Does the company raise awareness within the organization regarding carbon emissions

issue?

3. Please share the ways in which the company has an environmental sustainability

responsible employee?

4. How can you say that the management person is responsible for corporate disclosure

compliance?

5. What are the formal environmental policies and continuous improvement policies

followed by the company?

Pepper, A. and Gore, J., 2015. Behavioral agency theory: New foundations for theorizing about

executive compensation. Journal of management, 41(4), pp.1045-1068.

Shogren, K.A., Wehmeyer, M.L., Palmer, S.B., Forber-Pratt, A.J., Little, T.J. and Lopez, S.,

2015. Causal agency theory: Reconceptualizing a functional model of self-

determination. Education and Training in Autism and Developmental Disabilities, pp.251-263.

Silverman, D. ed., 2016. Qualitative research. Sage.

Taylor, S.J., Bogdan, R. and DeVault, M., 2015. Introduction to qualitative research methods: A

guidebook and resource. John Wiley & Sons.

Appendices

Questionnaire for Managers

1. To which stakeholders does the company report CSR information o carbon emissions?

2. Does the company raise awareness within the organization regarding carbon emissions

issue?

3. Please share the ways in which the company has an environmental sustainability

responsible employee?

4. How can you say that the management person is responsible for corporate disclosure

compliance?

5. What are the formal environmental policies and continuous improvement policies

followed by the company?

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.