Accounting 101: General Journal, Ledger, Trial Balance and Statements

VerifiedAdded on 2023/01/10

|11

|1273

|49

Homework Assignment

AI Summary

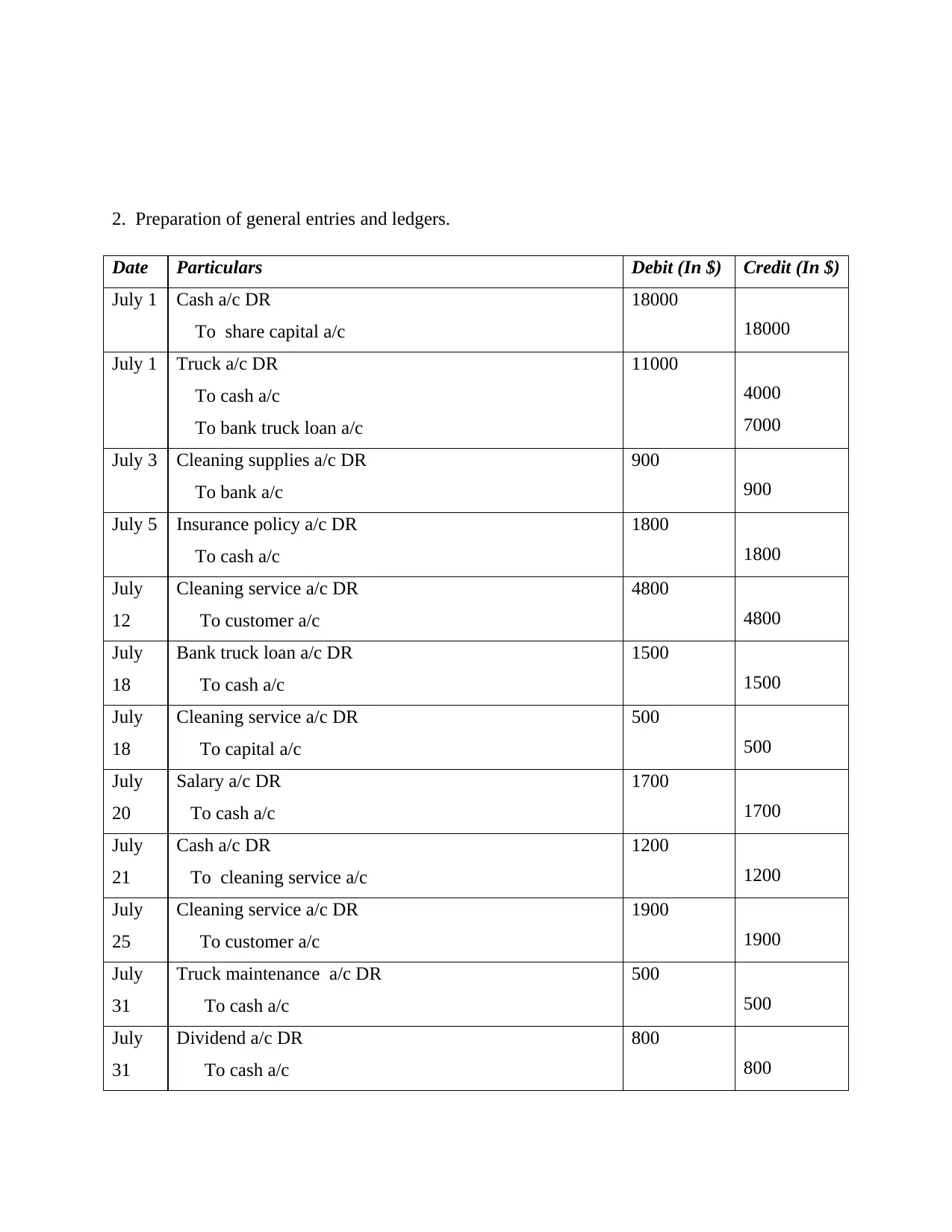

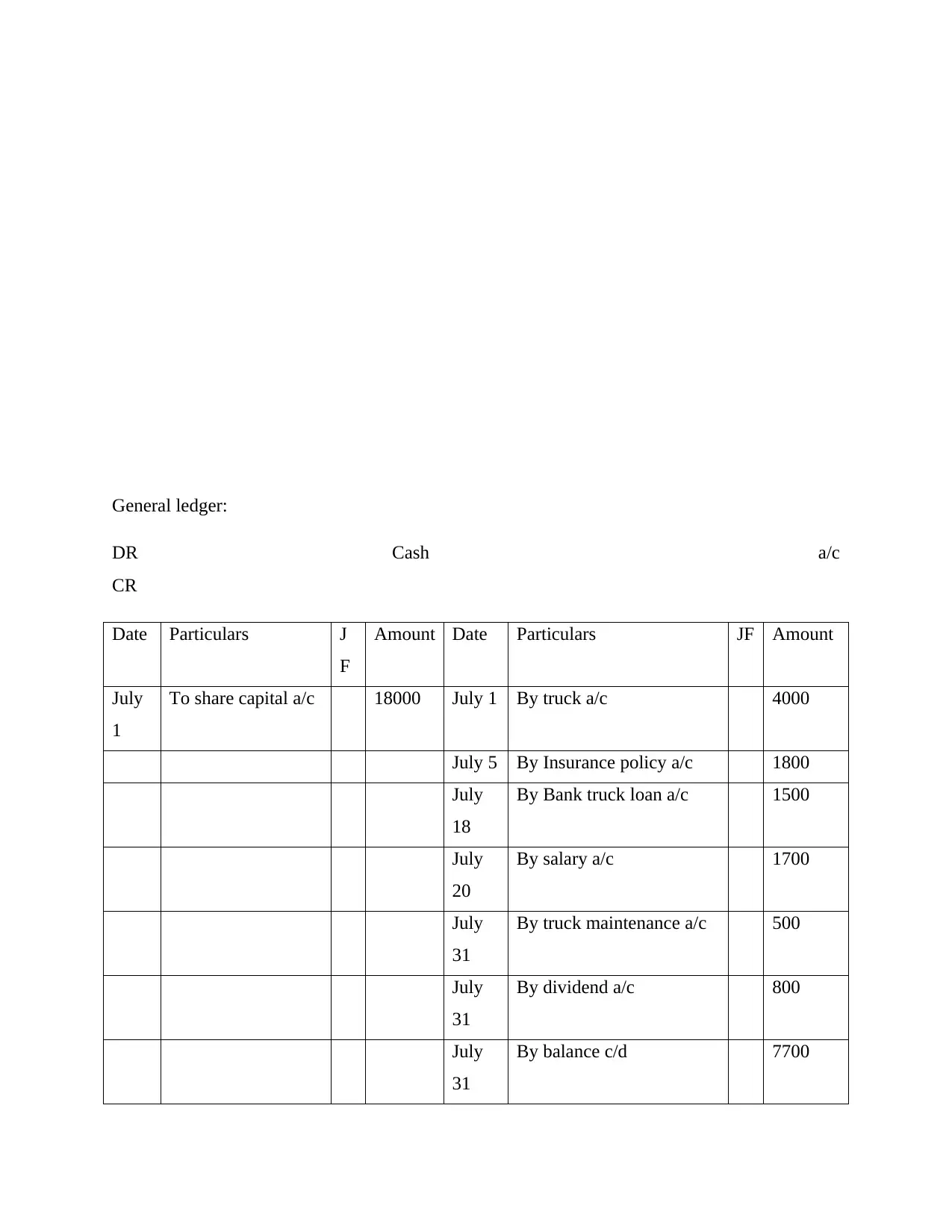

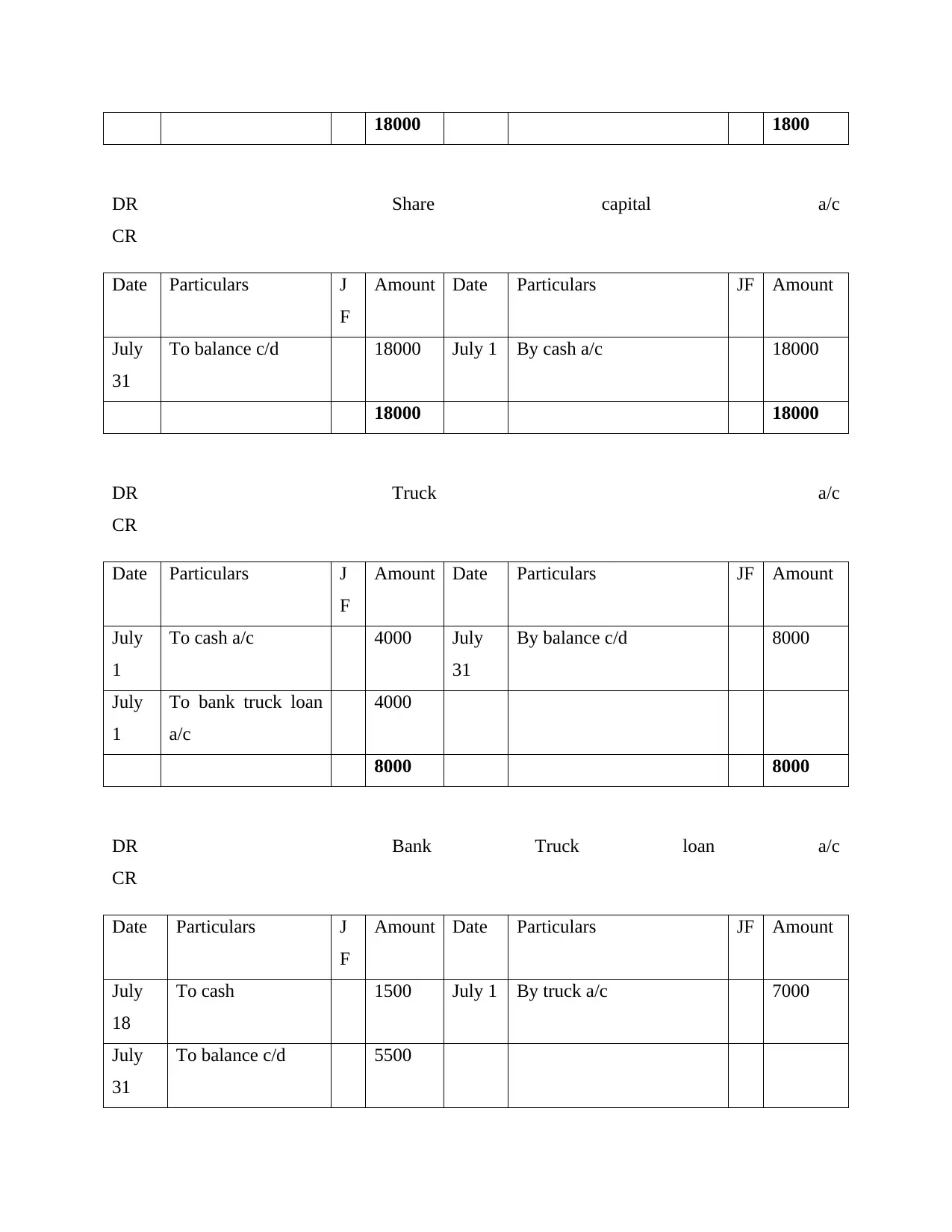

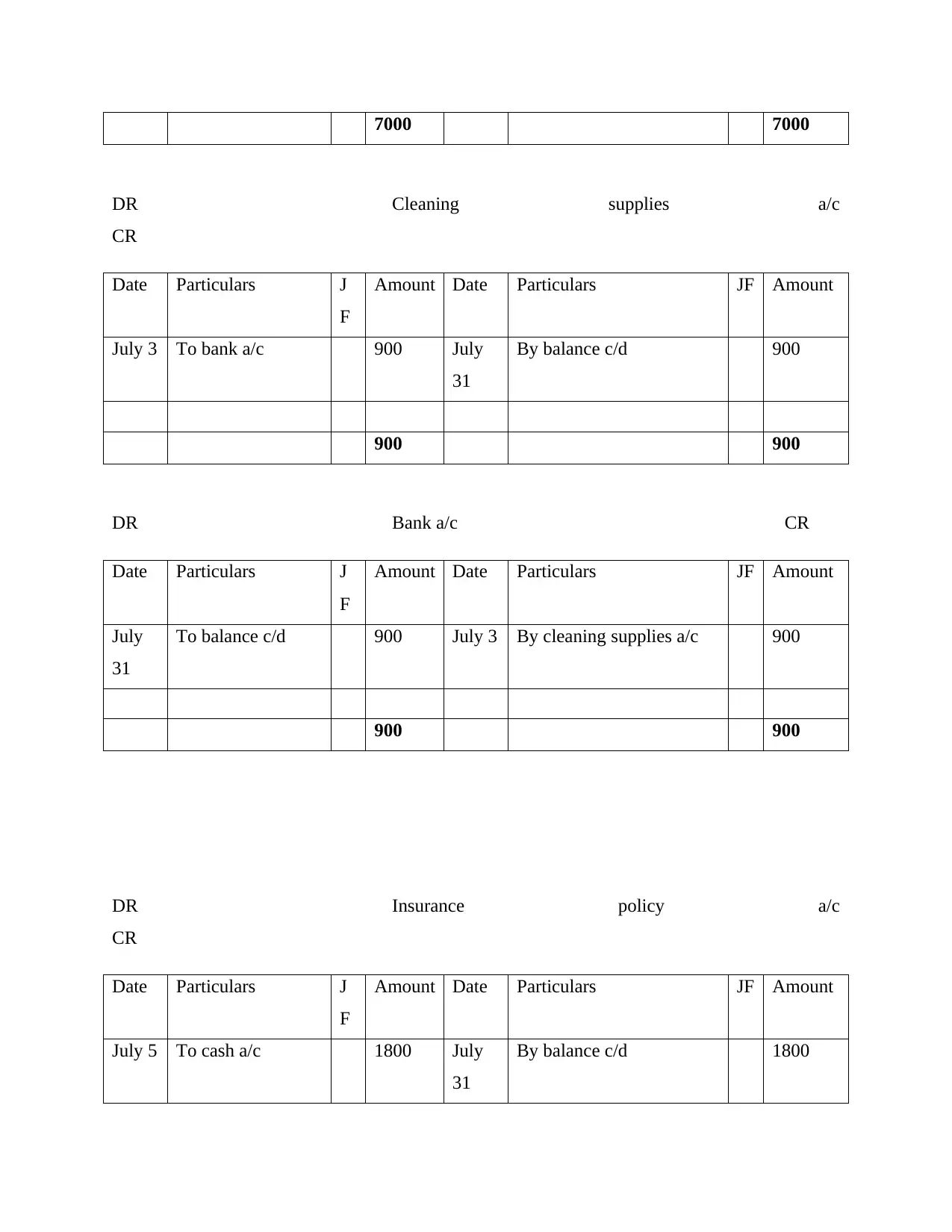

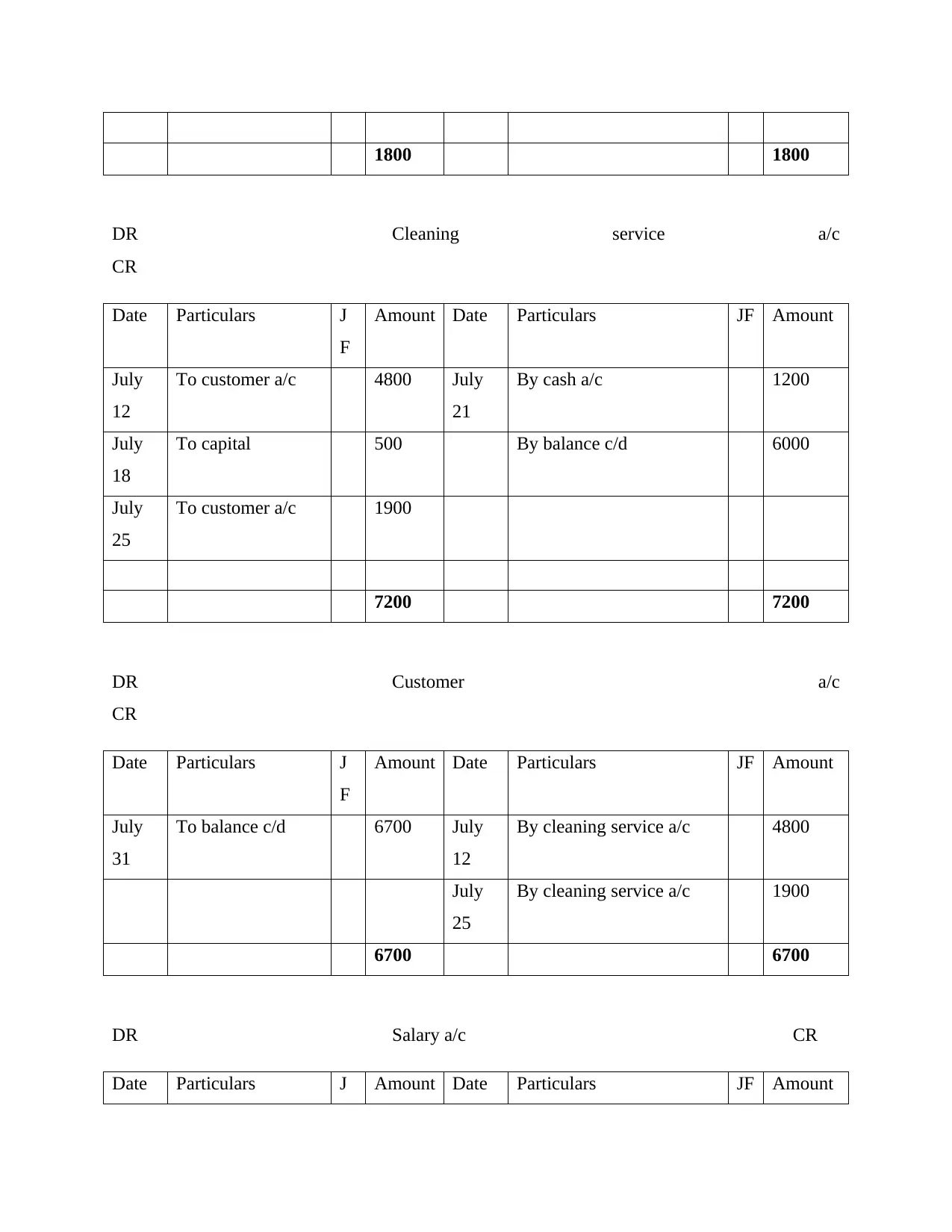

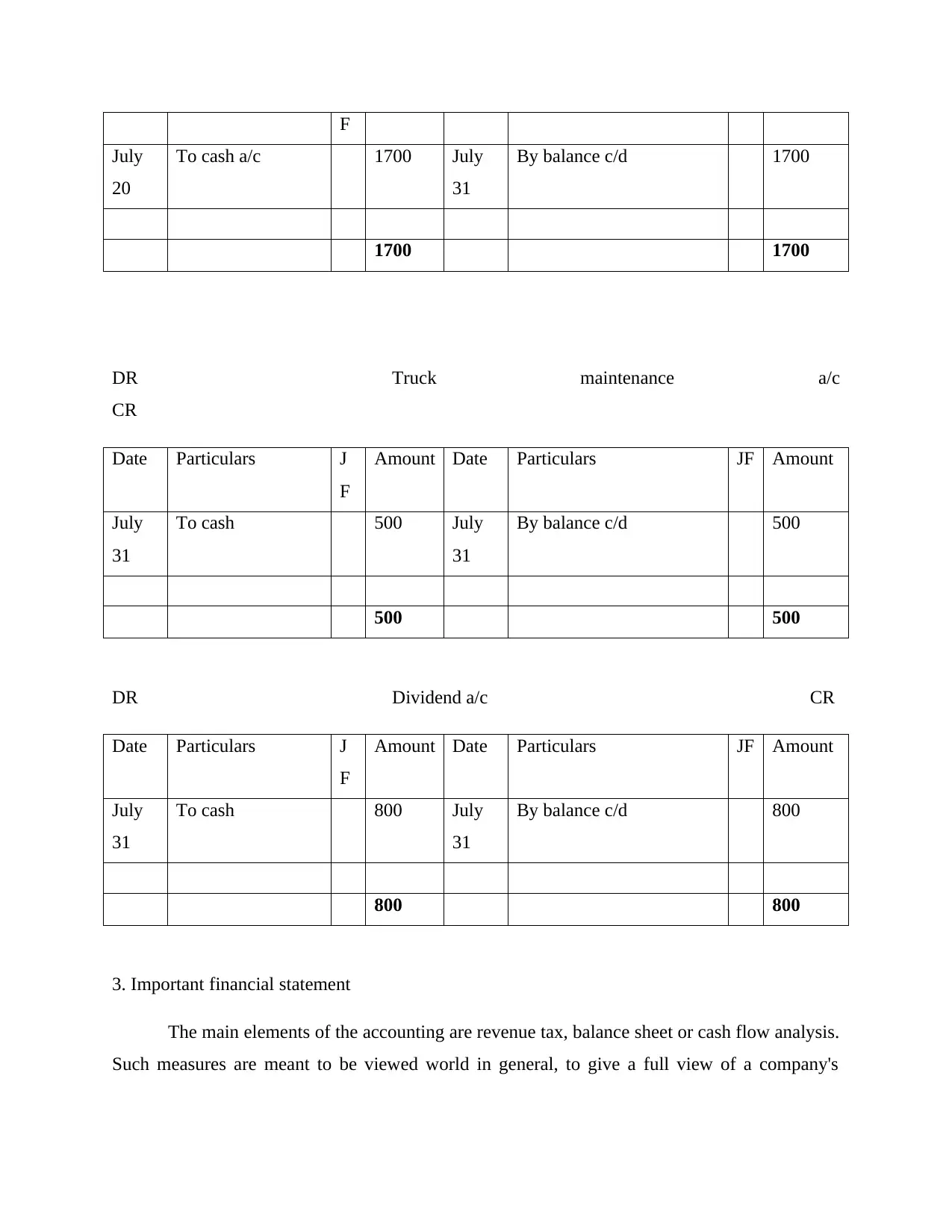

This assignment delves into the fundamental components of the accounting process, including the general journal, general ledger, trial balance, and financial statements. It describes the purpose of each, emphasizing their interconnectedness within the accounting cycle. The general journal serves as the initial record of transactions, detailing debits and credits. These entries are then posted to the general ledger, which organizes transactions by account. The trial balance ensures the equality of debits and credits, providing a summary of account balances. Finally, financial statements, such as the income statement and balance sheet, are prepared using the trial balance data to provide insights into a company's financial performance and position. The assignment also includes example journal entries and ledger accounts illustrating the practical application of these concepts, using the New Era Cleaning Service, Inc. scenario provided in the assignment brief.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.