Impairment of Assets at Myer Holdings

VerifiedAdded on 2020/02/24

|7

|1642

|55

AI Summary

This assignment delves into the impairment of assets at Myer Holdings Ltd., focusing on their adherence to AASB 136 guidelines. It examines how the company determines recoverable amounts, conducts impairment tests, and handles potential reversals. The analysis highlights the flexibility afforded to management in carrying out these procedures while ensuring compliance with accounting standards.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING STANDARD AND REGULATION

Accounting standard and regulation

Name of the student

Name of the university

Author note

Accounting standard and regulation

Name of the student

Name of the university

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ACCOUNTING STANDARD AND REGULATION

Table of Contents

a. Evidence required for impairment testing of Myer’s asset..................................................3

b. Procedures required to be addressed for determination of impairment...............................4

C. Information required for determination of impairment.......................................................5

d. availability of flexibility from the management for determination of impairment...............6

Reference....................................................................................................................................7

Table of Contents

a. Evidence required for impairment testing of Myer’s asset..................................................3

b. Procedures required to be addressed for determination of impairment...............................4

C. Information required for determination of impairment.......................................................5

d. availability of flexibility from the management for determination of impairment...............6

Reference....................................................................................................................................7

2ACCOUNTING STANDARD AND REGULATION

AASB 136 and IAS 36 Impairment of assets assure that an organization’s asset is not

written in the financial statement at the value which is more than its recoverable amount. The

recoverable amount for the asset is higher among the value in use and the fair value less the

disposal cost. Only exception to this is some intangible assets and the goodwill. All the

organizations are required to conduct the test for impairment of its assets if there is any

indication that the asset will be impaired. Further, the test can be carried on for the cash

generating unit where the asset does not create any cash flow which is widely independent of

those of the other assets (Linnenluecke et al. 2015).

An organization shall assess at end of the each accounting period that whether any

indication exists there for the impairment of any asset and if any indication is there, then the

recoverable amount of the asset shall be measured. Various indications for impairment of

assets are as follows –

External sources –

Reduction in the market value of the asset

Negative changes with regard to markets, laws, technologies or economies

Increase in the interest rate of the market

Higher level of net asset of the company as compared to market capitalization

Internal sources –

Physical damage or obsolescence

The asset is held for disposal or it is idle or part of the asset is restructuring

Worse performance as compared to the expectation

a. Evidence required for impairment testing of Myer’s asset

Flow of the asset – it has been recognized from the given data flow of the company

that the flow for all the stores of the company is either stable or has increased and for

none of the asset any reduction trend is found for the past one year period. Therefore

no indication of impairment is there.

Asset base – from the asset base of the company is recognized that the asset base for

all the assets has not altered much and all the assets are maintaining more or less the

same percentage of contribution towards total assets for last few years. Therefore, no

indication of impairment is there (Malone, Tarca and Wee 2015).

AASB 136 and IAS 36 Impairment of assets assure that an organization’s asset is not

written in the financial statement at the value which is more than its recoverable amount. The

recoverable amount for the asset is higher among the value in use and the fair value less the

disposal cost. Only exception to this is some intangible assets and the goodwill. All the

organizations are required to conduct the test for impairment of its assets if there is any

indication that the asset will be impaired. Further, the test can be carried on for the cash

generating unit where the asset does not create any cash flow which is widely independent of

those of the other assets (Linnenluecke et al. 2015).

An organization shall assess at end of the each accounting period that whether any

indication exists there for the impairment of any asset and if any indication is there, then the

recoverable amount of the asset shall be measured. Various indications for impairment of

assets are as follows –

External sources –

Reduction in the market value of the asset

Negative changes with regard to markets, laws, technologies or economies

Increase in the interest rate of the market

Higher level of net asset of the company as compared to market capitalization

Internal sources –

Physical damage or obsolescence

The asset is held for disposal or it is idle or part of the asset is restructuring

Worse performance as compared to the expectation

a. Evidence required for impairment testing of Myer’s asset

Flow of the asset – it has been recognized from the given data flow of the company

that the flow for all the stores of the company is either stable or has increased and for

none of the asset any reduction trend is found for the past one year period. Therefore

no indication of impairment is there.

Asset base – from the asset base of the company is recognized that the asset base for

all the assets has not altered much and all the assets are maintaining more or less the

same percentage of contribution towards total assets for last few years. Therefore, no

indication of impairment is there (Malone, Tarca and Wee 2015).

3ACCOUNTING STANDARD AND REGULATION

Asset turnover – looking at the asset turnover ratio of the company, it is identified that

the asset turnover ratio of Myer Holdings Ltd for the last few years are moving around

1.41 to 1.76. Therefore, it can be said that no significant increase or decrease is found

with regard to the asset turnover ratio of the company. Therefore, this test also cannot

establish that there is any indication for impairment.

b. Procedures required to be addressed for determination of impairment

AASB 136 for Impairment of assets requires the organization to annually test the

assets for impairment and Myer holding Ltd follows this requirement. However, for testing

the assets for the purpose of impairment, recoverable amount is found out through usage of

value-in-use discounted cash flow model. This model utilises the cash flow forecasting on the

basis of the financial budget that is approved by the management and it covers the period of

five years. Further, the cash flow for the period of more than five years are extrapolated

through usage of the terminal growth rate. Key assumptions utilised for the mode are as

follows –

Rate of discount (pre-tax) at14.4%

Rate of terminal growth at 2.5%

Gross profit margin from operation at the rate of 39.5%

Thereafter the management determines the fact that whether level of the future cash

flows for the carrying value of the assets for the CGU of Myer further, during the period

under consideration, the review for the asset’s carrying value for each of the store of the

company is undertaken and identified whether indication of any impairment is exists. Where

there is any indication, the asset’s recoverable amount was measured through discounted cash

flow model. Major assumption for the model is consistent with the above mentioned

assumptions. However, no impairment indication is recognized at Myer stores for the year

ending 2016 of the company’s operation.

Asset turnover – looking at the asset turnover ratio of the company, it is identified that

the asset turnover ratio of Myer Holdings Ltd for the last few years are moving around

1.41 to 1.76. Therefore, it can be said that no significant increase or decrease is found

with regard to the asset turnover ratio of the company. Therefore, this test also cannot

establish that there is any indication for impairment.

b. Procedures required to be addressed for determination of impairment

AASB 136 for Impairment of assets requires the organization to annually test the

assets for impairment and Myer holding Ltd follows this requirement. However, for testing

the assets for the purpose of impairment, recoverable amount is found out through usage of

value-in-use discounted cash flow model. This model utilises the cash flow forecasting on the

basis of the financial budget that is approved by the management and it covers the period of

five years. Further, the cash flow for the period of more than five years are extrapolated

through usage of the terminal growth rate. Key assumptions utilised for the mode are as

follows –

Rate of discount (pre-tax) at14.4%

Rate of terminal growth at 2.5%

Gross profit margin from operation at the rate of 39.5%

Thereafter the management determines the fact that whether level of the future cash

flows for the carrying value of the assets for the CGU of Myer further, during the period

under consideration, the review for the asset’s carrying value for each of the store of the

company is undertaken and identified whether indication of any impairment is exists. Where

there is any indication, the asset’s recoverable amount was measured through discounted cash

flow model. Major assumption for the model is consistent with the above mentioned

assumptions. However, no impairment indication is recognized at Myer stores for the year

ending 2016 of the company’s operation.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ACCOUNTING STANDARD AND REGULATION

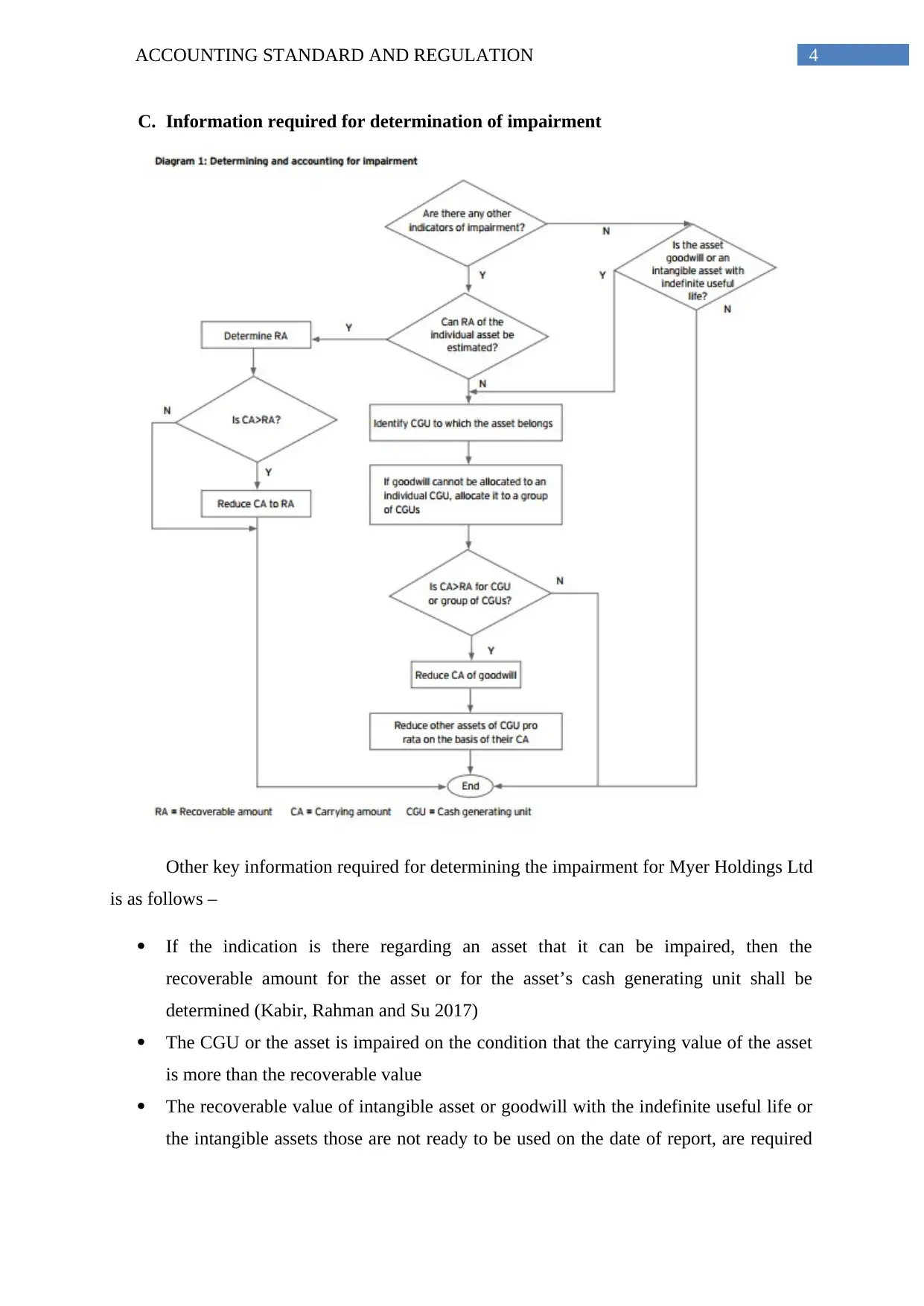

C. Information required for determination of impairment

Other key information required for determining the impairment for Myer Holdings Ltd

is as follows –

If the indication is there regarding an asset that it can be impaired, then the

recoverable amount for the asset or for the asset’s cash generating unit shall be

determined (Kabir, Rahman and Su 2017)

The CGU or the asset is impaired on the condition that the carrying value of the asset

is more than the recoverable value

The recoverable value of intangible asset or goodwill with the indefinite useful life or

the intangible assets those are not ready to be used on the date of report, are required

C. Information required for determination of impairment

Other key information required for determining the impairment for Myer Holdings Ltd

is as follows –

If the indication is there regarding an asset that it can be impaired, then the

recoverable amount for the asset or for the asset’s cash generating unit shall be

determined (Kabir, Rahman and Su 2017)

The CGU or the asset is impaired on the condition that the carrying value of the asset

is more than the recoverable value

The recoverable value of intangible asset or goodwill with the indefinite useful life or

the intangible assets those are not ready to be used on the date of report, are required

5ACCOUNTING STANDARD AND REGULATION

to be valued at least per year basis, irrespective of the fact that there exists any

indication of impairment or not.

For the purpose of measurement, the recoverable value is stated as higher among the

value in use and fair value less the selling cost (Bond, Govendir and Wells 2016)

The amount of loss from impairment is identified as expense under the profit and loss

account and is carried out at cost. Further, if the impacted asset is already a revalued

asset under the permission of IAS 16 PPE (IAS 16) and the intangible asset (IAS 38)

and impairment if any is 1st recorded against the revaluation recognized previously

recognized as gains and then as the comprehensive income to the other assets.

Wide disclosures are required for the rest of impairment and recognition of

impairment loss (Guthrie and Pang 2013)

Impairment loss that is recognized in the previous period for the goodwill or any asset

must be reversed if any alteration is there with regard to the estimates that were used

for determining the recoverable amount of the asset.

d. availability of flexibility from the management for determination of impairment

It is recognized that the management of Myer Holdings Ltd is quite flexible in

carrying out the tests for determining the impairment with regard to the asset. As per the

requirement of AASB 136, they assure to carry out the test for impairment at least one in each

year (Zhuang 2016). Further, the management determines various facts like determination of

the fact that whether level of the future cash flows for the carrying value of the assets for the

CGU of Myer. Moreover, the management carries out review for the asset’s carrying value for

each of the store of the company is undertaken and identified whether indication of any

impairment is exists. Where there is any indication, the asset’s recoverable amount was

measured through discounted cash flow model. Major assumption for the model is consistent

with the above mentioned assumptions (Bond, Govendir and Wells 2016). Further, the

management of the company determines the recoverable value of the cash generating unit on

the basis of VIU approach. Therefore, taking into consideration all these facts, it can be said

that the management of Myer Holdings Ltd take active part and comply with all the

requirements of AASB 136 for carrying out the procedures for impairment test and

determination of impairment.

to be valued at least per year basis, irrespective of the fact that there exists any

indication of impairment or not.

For the purpose of measurement, the recoverable value is stated as higher among the

value in use and fair value less the selling cost (Bond, Govendir and Wells 2016)

The amount of loss from impairment is identified as expense under the profit and loss

account and is carried out at cost. Further, if the impacted asset is already a revalued

asset under the permission of IAS 16 PPE (IAS 16) and the intangible asset (IAS 38)

and impairment if any is 1st recorded against the revaluation recognized previously

recognized as gains and then as the comprehensive income to the other assets.

Wide disclosures are required for the rest of impairment and recognition of

impairment loss (Guthrie and Pang 2013)

Impairment loss that is recognized in the previous period for the goodwill or any asset

must be reversed if any alteration is there with regard to the estimates that were used

for determining the recoverable amount of the asset.

d. availability of flexibility from the management for determination of impairment

It is recognized that the management of Myer Holdings Ltd is quite flexible in

carrying out the tests for determining the impairment with regard to the asset. As per the

requirement of AASB 136, they assure to carry out the test for impairment at least one in each

year (Zhuang 2016). Further, the management determines various facts like determination of

the fact that whether level of the future cash flows for the carrying value of the assets for the

CGU of Myer. Moreover, the management carries out review for the asset’s carrying value for

each of the store of the company is undertaken and identified whether indication of any

impairment is exists. Where there is any indication, the asset’s recoverable amount was

measured through discounted cash flow model. Major assumption for the model is consistent

with the above mentioned assumptions (Bond, Govendir and Wells 2016). Further, the

management of the company determines the recoverable value of the cash generating unit on

the basis of VIU approach. Therefore, taking into consideration all these facts, it can be said

that the management of Myer Holdings Ltd take active part and comply with all the

requirements of AASB 136 for carrying out the procedures for impairment test and

determination of impairment.

6ACCOUNTING STANDARD AND REGULATION

Reference

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136. Accounting & Finance, 56(1), pp.259-

288.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairment decisions by

Australian firms and whether this was impacted by AASB 136.

Guthrie, J. and Pang, T.T., 2013. Disclosure of Goodwill Impairment under AASB 136 from

2005–2010. Australian Accounting Review, 23(3), pp.216-231.

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308.

Kabir, H., Rahman, A.R. and Su, L., 2017. The Association between Goodwill Impairment

Loss and Goodwill Impairment Test-Related Disclosures in Australia.

Linnenluecke, M.K., Birt, J., Lyon, J. and Sidhu, B.K., 2015. Planetary boundaries:

implications for asset impairment. Accounting & Finance, 55(4), pp.911-929.

Malone, L., Tarca, A. and Wee, M., 2015. Non-GAAP earnings disclosures and

IFRS. Accounting and Finance.

Zhuang, Z., 2016. Discussion of ‘An evaluation of asset impairments by Australian firms and

whether they were impacted by AASB 136’. Accounting & Finance, 56(1), pp.289-294.

Reference

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136. Accounting & Finance, 56(1), pp.259-

288.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairment decisions by

Australian firms and whether this was impacted by AASB 136.

Guthrie, J. and Pang, T.T., 2013. Disclosure of Goodwill Impairment under AASB 136 from

2005–2010. Australian Accounting Review, 23(3), pp.216-231.

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308.

Kabir, H., Rahman, A.R. and Su, L., 2017. The Association between Goodwill Impairment

Loss and Goodwill Impairment Test-Related Disclosures in Australia.

Linnenluecke, M.K., Birt, J., Lyon, J. and Sidhu, B.K., 2015. Planetary boundaries:

implications for asset impairment. Accounting & Finance, 55(4), pp.911-929.

Malone, L., Tarca, A. and Wee, M., 2015. Non-GAAP earnings disclosures and

IFRS. Accounting and Finance.

Zhuang, Z., 2016. Discussion of ‘An evaluation of asset impairments by Australian firms and

whether they were impacted by AASB 136’. Accounting & Finance, 56(1), pp.289-294.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.